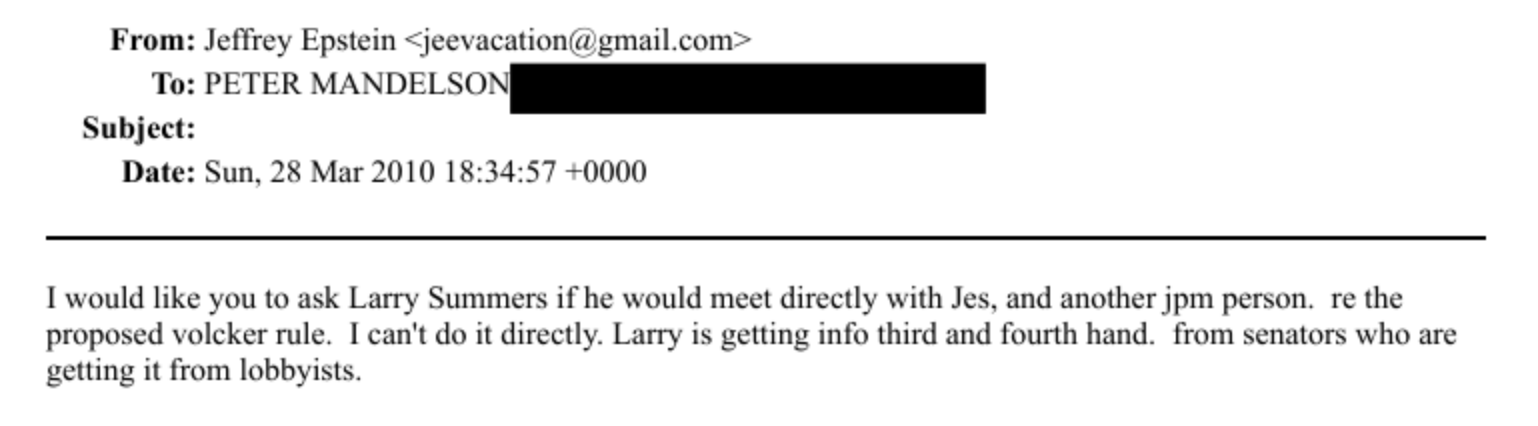

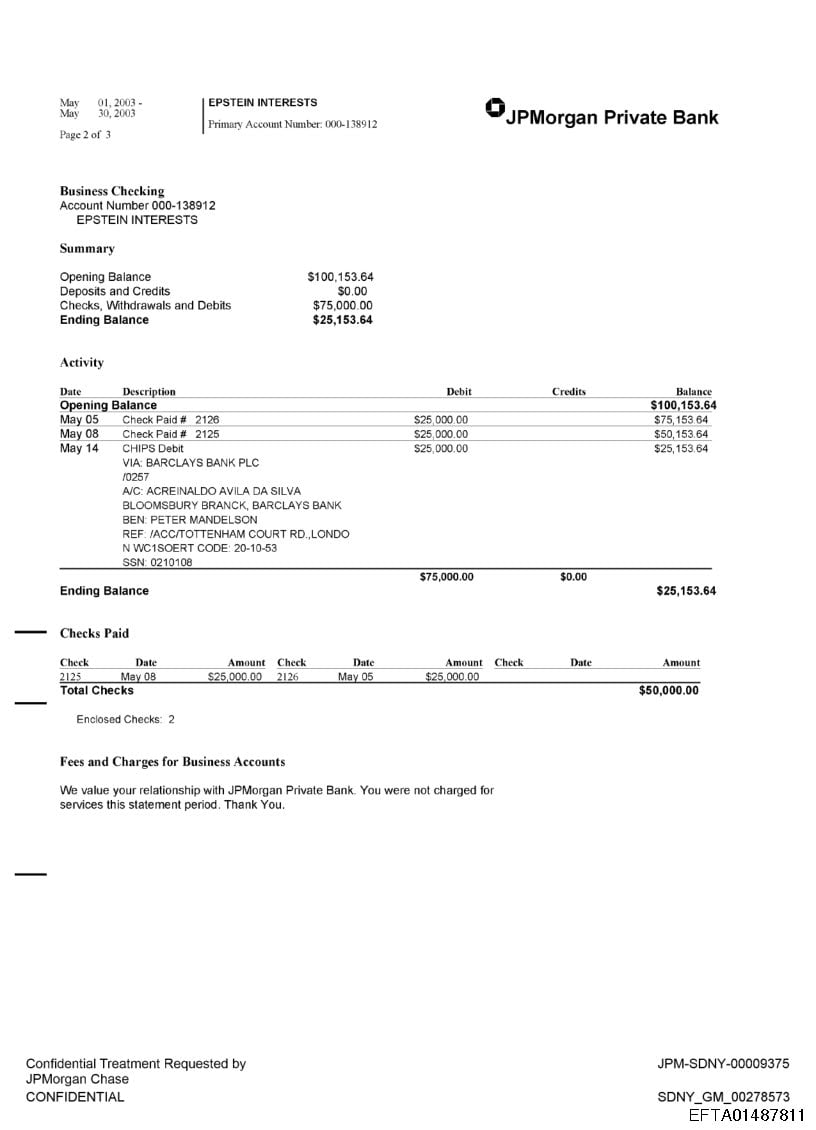

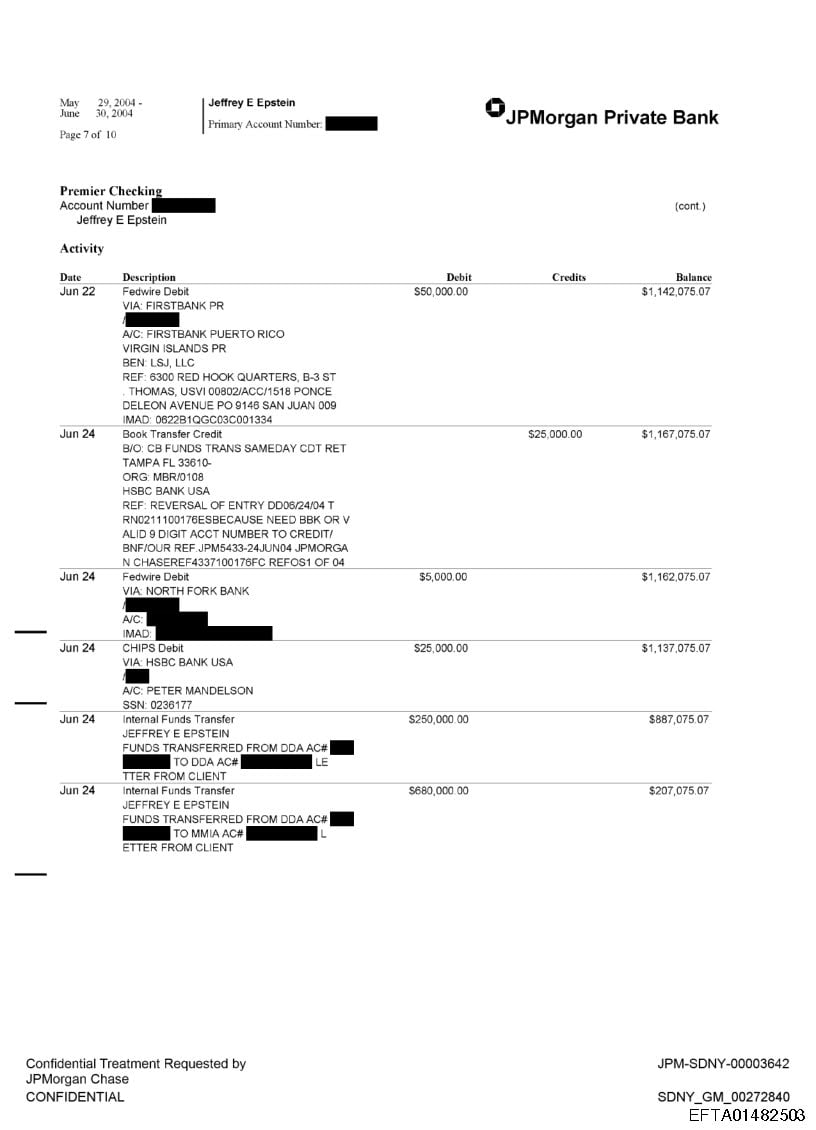

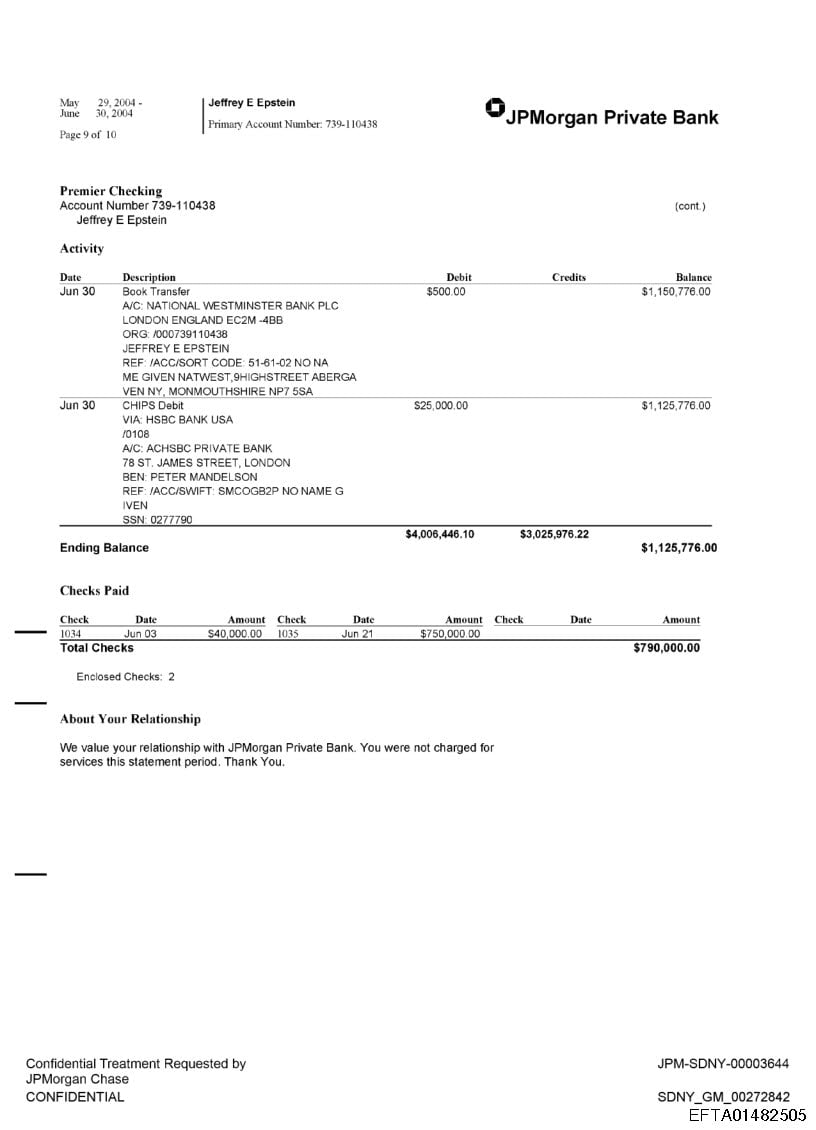

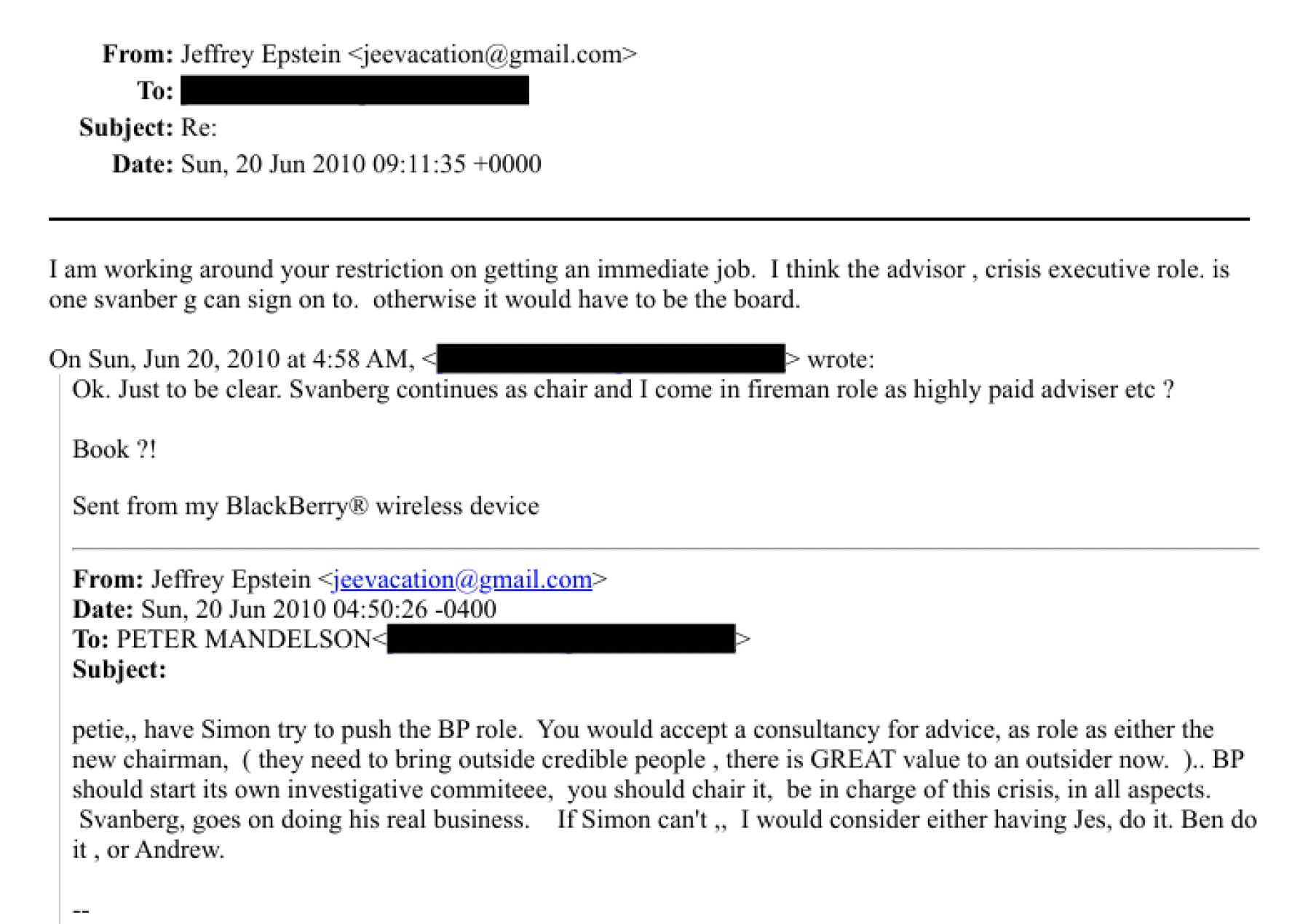

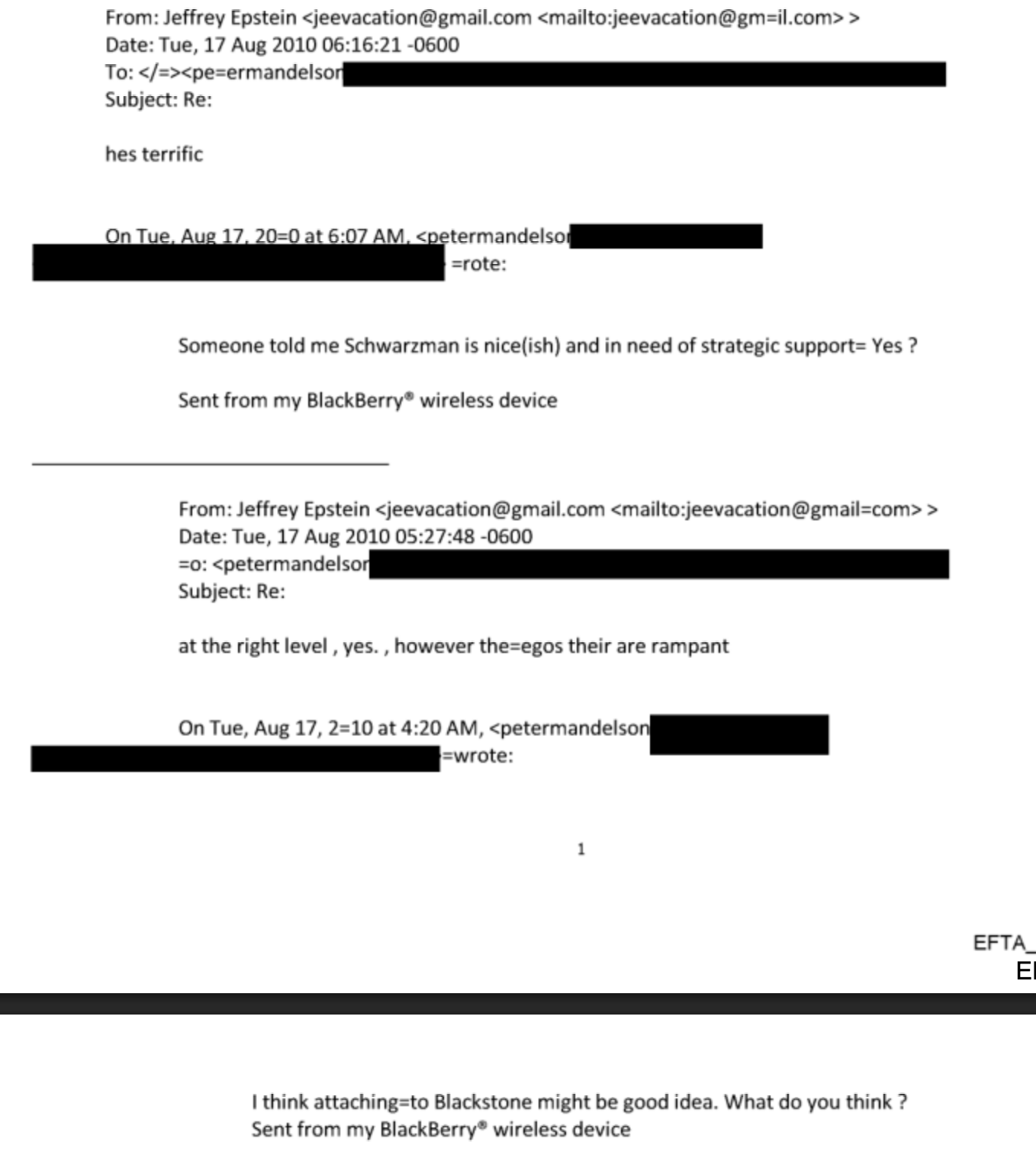

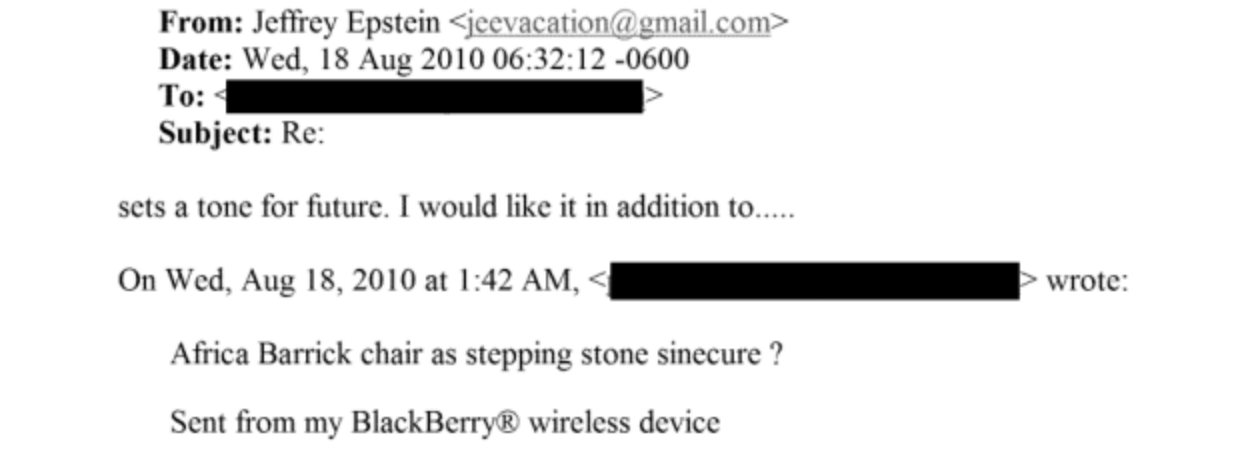

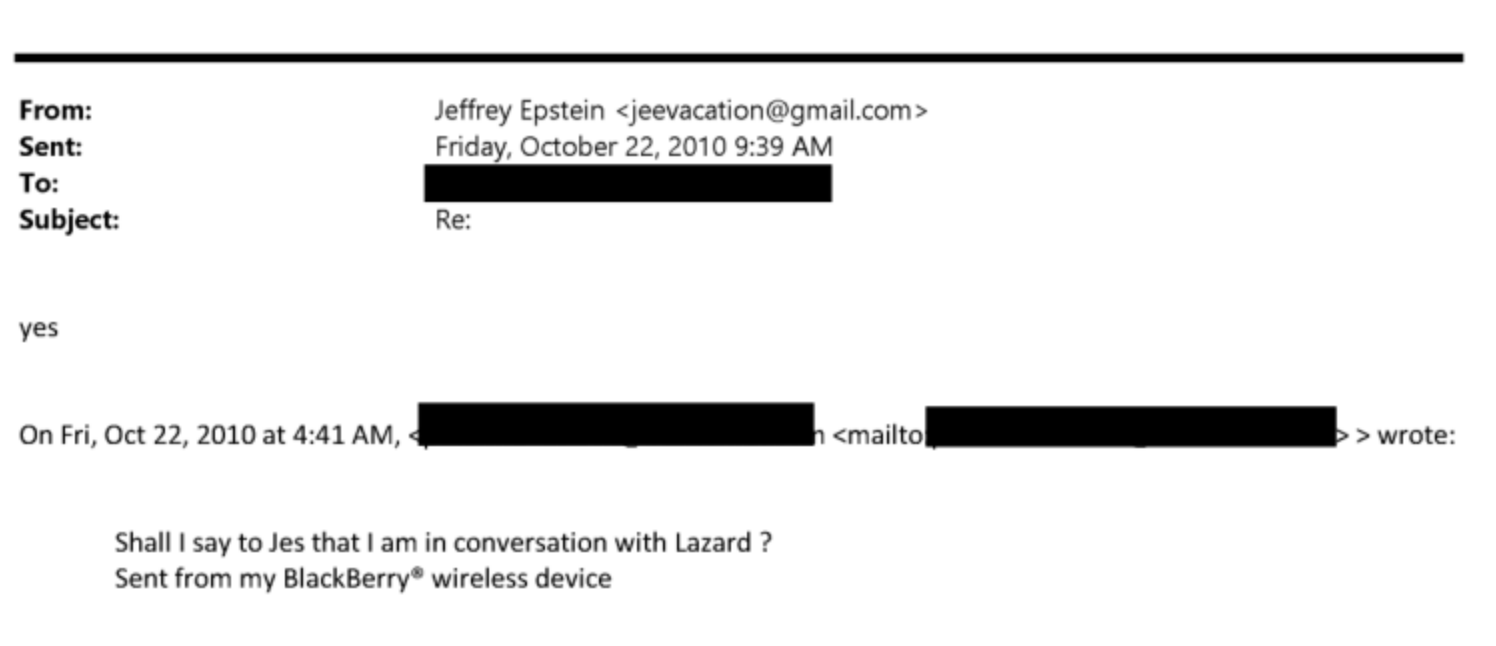

At 2.30pm today, the Government published a series of documents relating to the appointment of Peter Mandelson as His Majesty’s Ambassador to Washington.

This is in the form of three PDF files, each with multiple messages, and about 1,500 pages in total. It’s not very easy to navigate through – we’ve created a simple search tool.

The tool breaks those large PDFs into individual message records where possible. Users can search the text, filter by sender, subject and date, and open both the extracted text and the relevant PDF page extract for each result.

Full details are below – here is the tool:

This was done very quickly with automated tools and should be seen as an aid to research, not an official republication or authoritative database. The source material is complex. Many documents are email chains, forwarded messages, scanned pages, redactions, WhatsApp transcripts or OCR text. That creates lots of limiations:

Some messages are easy to identify; others are ambiguous.

Some message boundaries may be imperfect.

Some sender, recipient, subject or date fields may be wrong or incomplete.

Some PDF page extracts may include more than the relevant message, or occasionally miss part of it.

OCR errors in the original text may affect search results.

Redactions in the Government publication remain redacted here.

The original PDFs should always be treated as the authoritative source. The extracted text and metadata are provided to make the documents easier to search and navigate.

The documents are Crown copyright and were published under the Open Government Licence.

The code we used to index the files and create the web app is available on our GitHub.

Iain Clifford Stamp told his followers the IRS owed them millions. Not because they had paid US tax, or because they had US investments. But because they had once signed mortgages, loans and credit-card agreements here in the UK.

Stamp says his organisation filed claims for 3,000 people, worth $600 million. The IRS froze the money. Stamp now says that was our fault — and says he will sue us for $120 million.

Stamp is a British fugitive, currently in Northern Cyprus, sentenced to 12 months’ imprisonment for contempt of court after refusing to comply with FCA proceedings.

He previously ran Matrix Freedom, a mortgage-elimination scheme which failed catastrophically at the High Court. The scheme was described as showing “every appearance of deceit, of abuse and contempt of court”, and left hundreds of Stamp’s “clients” thousands of pounds out of pocket and often in default on their mortgages.

The latest scheme has created thousands more victims, who’ve paid large fees to Stamp, in return for becoming unwitting participants in a US tax fraud.

The claims of free millions

The man in this video claims that everybody – in the UK and across the world – is owed huge tax refunds from the United States tax authority, the Internal Revenue Service (IRS):

“Did you know that you are actually owed back taxes on every mortgage, every loan, and every credit card you’ve ever had, going back to the age of 18?

Think about that for a second. I’m 56 years old. That means I’m owed back taxes going back 38 years. The longer you’ve had those loans, credit cards, and mortgages, the more tax you’re owed. So imagine getting all of that back in one lump sum. How life-changing would that be?

Before you assume this sounds too good to be true or some kind of loophole, it’s not. This is lawful. This is legal. All the elites and wealthy people of the world know exactly how to do this. I guarantee they’re doing it every single year.”

The man is part of a sovereign citizen1 movement led by a man called Iain Clifford Stamp, currently living in Northern Cyprus as a fugitive following a UK conviction for contempt of court.2

Stamp charges his followers thousands of pounds in “donations” to make these claims, and says the average is between two and three million dollars3, and over your lifetime you could claim $100m:

Well, my final thoughts are based on those that are already doing this, about the average is around somewhere between two and three million dollars is what you can recoup of taxes.

…

So if you’re if you’ve got another 20, 30 years on the monopoly board, then or maybe 40 years, 50 years, however many years you’ve got to play the play the game out and multiply that two to three million by how many years left?

…

It could be for a lot of people, it could be over $100 million that we’re talking about.

Stamp says his “Republic of Old Souls” organisation made claims in 2025 totalling $600m:

“Well, in 2025, we had IRS confirmed wages and tax transfers in excess of $600 million, and those recoupments4 were due to be funded to our membership between September of 2025 and now.”

And here’s Stamp’s explanation for why it works:

“You see, the birth certificate construct, an artificial player piece acting as a banker under the Bills of Exchange Act 1882 has made a deposit of energy.

The signature is the conduit of the energy transfer from the living man or woman through the birth certificate construct, a banker that is making a deposit, issuing a security promise to pay in the future that has no entitlement, no lawful standing to recoup that signature energy back to the birth certificate construct.

So if you’re going to recoup abandoned signature credit energy, which is taxes, you have to put a new piece on the monopoly board that is clean, that can operate as a nominee, as it says in the IRS Publication 1212. And if that entity, which is an artificial entity as a grantor trust, files a 1099-OID, it is making a claim that the signature, the creator of the signature, the living man-woman is the true beneficiary of the taxes that are being paid, at the moment, to the United States Treasury. On their ledgers, they are keeping those taxes.”

Stripped of the pseudo-legal language, Stamp’s claim is this: when you sign a loan agreement, a secret tax asset is created; that asset can be claimed from the IRS through a grantor trust using Form 1099-OID. Every part of that is false.

Form 1099-OID is not a magic refund form. It reports a specific kind of interest-like income on real debt instruments. 5 It does not turn a mortgage signature, credit-card agreement or birth certificate into a US tax refund. There is no such thing as “signature credit energy” or a “birth certificate construct”. A loan is money that you owe, not an asset. 6

We think most people would realise that these claims are nonsensical. The IRS does not hand out vast tax refunds to British citizens because they once signed a mortgage, loan agreement or credit-card application.

Some people, however, fall for this. Sometimes because they’ve fallen down a “rabbit hole” of internet conspiracy theories, and become unable to tell fact from fiction. Often because they are desperate; often in debt, and willing to believe anyone who offers a way out; sometimes because they are very vulnerable and with a history of mental illness. We’ve spoken to nine people who’ve seen family members fall under Stamp’s spell. There’s a common pattern: thousands, sometimes tens of thousands, of pounds paid in “donations”; debts mounting; relationships strained or broken; and the victim becoming more committed to the scheme, despite the promised riches never arriving.7

The reality – it’s just tax fraud

The scam Stamp is selling is well known. It exploits a vulnerability in the way the IRS processes a particular US tax form, the “1099-OID”. If you complete a form apparently showing that you suffered US tax, then the IRS will sometimes mail you out a cheque, even if in fact you never paid any US tax at all.8

A real 1099-OID refund scenario looks like this:

Diagram connections

Diagram connections

From Company issues $10,000 bond to investor for $9,500 cash to A year later, company redeems bond, paying investor $10,000 (Label: None)

From A year later, company redeems bond, paying investor $10,000 to Company withholds $150 tax from this (i.e. 30% of the $500 OID) and pays to IRS (Label: None)

From Company withholds $150 tax from this (i.e. 30% of the $500 OID) and pays to IRS to Company gives investor 1099-OID showing $500 OID and $150 withheld (Label: None)

From Company gives investor 1099-OID showing $500 OID and $150 withheld to Investor files tax return with 1099-OID and claims credit/refund of the $150 (Label: None)

What Stamp is doing is this:

Diagram connections

Diagram connections

From UK resident borrows $10,000 to Stamp fabricates 1099-OID for resident's trust showing $10,000 of OID and $10,000 of tax withheld. No tax was actually withheld (Label: None)

From Stamp fabricates 1099-OID for resident's trust showing $10,000 of OID and $10,000 of tax withheld. No tax was actually withheld to Stamp files tax forms showing the trust had $10,000 of income and overpaid tax (Label: None)

From Stamp files tax forms showing the trust had $10,000 of income and overpaid tax to IRS 'refunds' the $10,000 to the trust (Label: None)

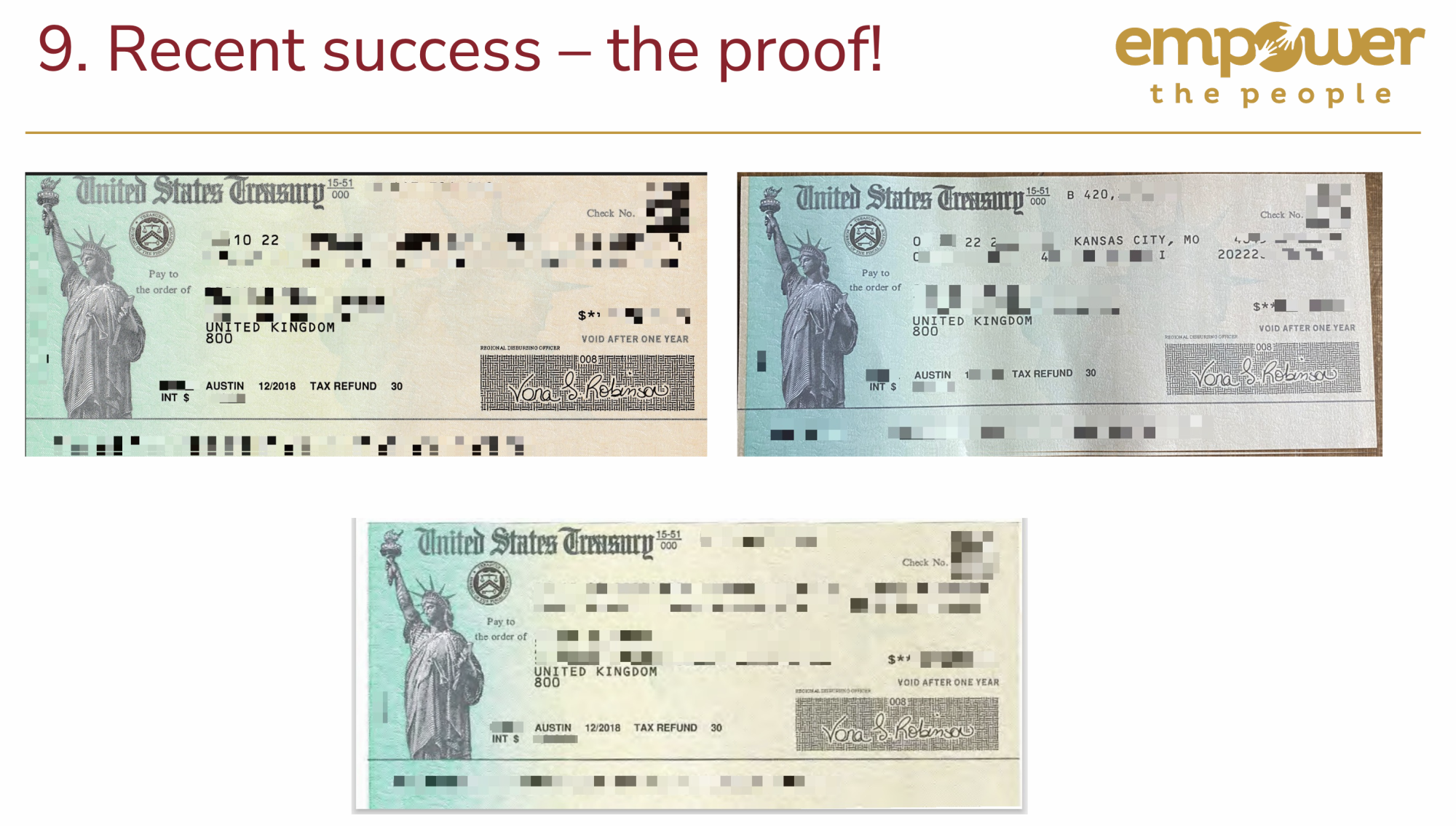

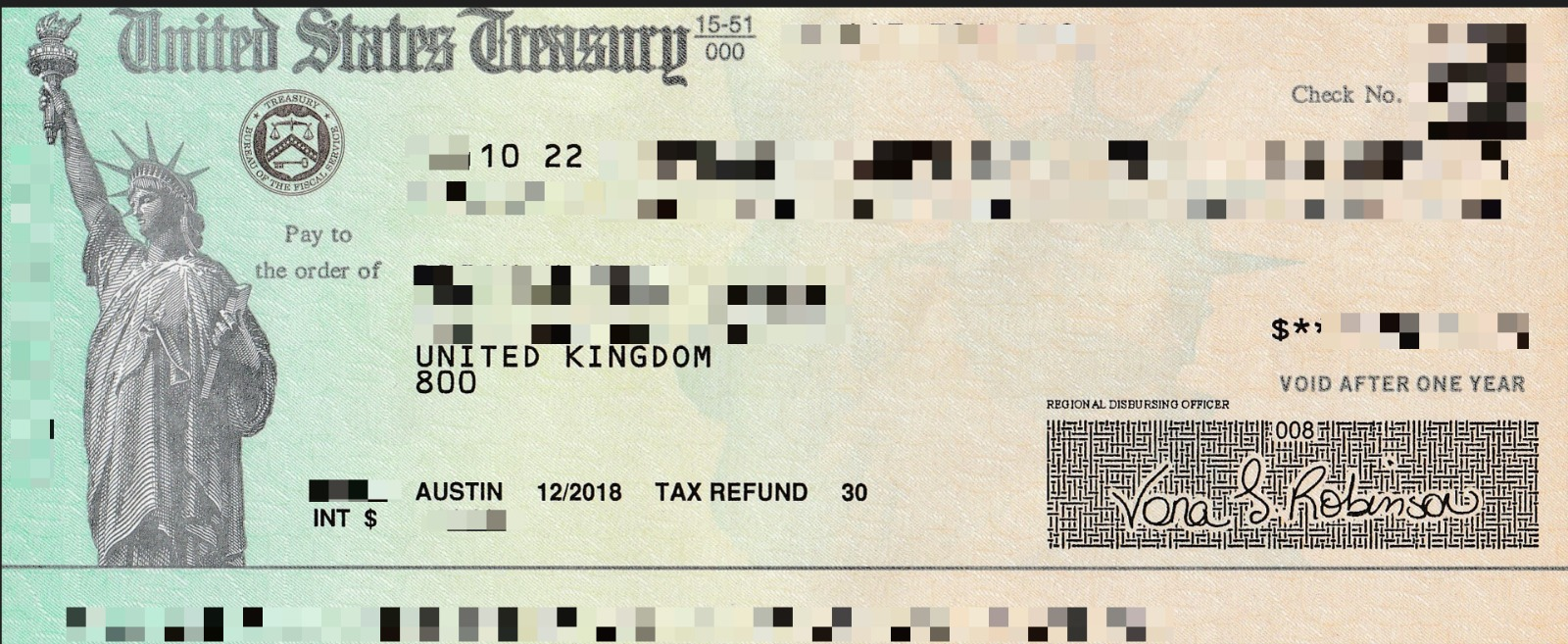

This will sometimes appear to work – the IRS may actually send you a cheque. The one shown here is probably genuine:

But there is an obvious problem: if you complete a form saying that you suffered US tax when you didn’t, then you’ve committed fraud.9

It’s a fraud the IRS are very aware of. They publish an annual “dirty dozen” list of tax scams, and the 2009 list explicitly called out a 1099-OID fraud that perfectly describes the Stamp scheme:

These schemes are so persistent that the IRS continues to issue warnings about them, most recently including them in its 2026 list. And the US authorities do more than issue warnings; they aggressively prosecute 1099-OID promoters. In May 2024, a promoter was sentenced to five years in jail for running a scheme remarkably similar to Stamp’s:

There have been dozens of prosecutions over the years.10 While most of the frauds prosecuted to date involved US citizens, international borders do not offer immunity. The IRS has successfully extradited 1099-OID fraudsters from Trinidad and Tobago and from Canada to face trial:

If you’ve read our report on Simon Goldberg’s group “Empower the People”, Stamp’s scheme will look familiar. But where Empower the People processed perhaps 80 claims and attempted to defraud the IRS of around $1 million, Stamp claims to have filed returns for 3,000 trusts, claiming $600 million.

(As an aside, Stamp and Goldberg despise each other. Both have published extensive materials and videos accusing the other of fraud. Of course both are right.)

Stamp appears to believe he is different from Goldberg and all the other cases because he’s added a trust, and invented a vocabulary of “signature credit”, “98-series” trusts and an “810 Algorithm”. He has not. If you file, or cause to be filed, a Form 1099-OID claiming fictitious withholding on a fictitious debt instrument, the form is false. And that’s what’s happening here: there is no withholding and no debt instrument – that makes it fraud. Attempts by defendants in tax prosecutions to run these kinds of sovereign citizen arguments have consistently failed.11

We gave Stamp the opportunity to respond. He initially responded through “Ecclesia Law” – a Wyoming LLC that says it is a “a USA law firm operating exclusively under Attorney-in-Fact mandates”12 – sending us numerous nonsensical, repetitive and AI generated13 documents, of which this is typical.14

Did Stamp really submit $600m of fraudulent claims?

It would be easy to dismiss this all as a fantasy. $600m is a huge number, and one of the largest 1099-OID frauds ever.15

We had a long email exchange with Stamp in which he was adamant that he really did make $600m of claims. In the course of that correspondence, Stamp sent us what appears to be a genuine IRS wage and income transcript for the “Iain Clifford OID Trust”, used to make a $4.477m refund claim:

If, as it appears, the document is genuine, then this is remarkable piece of self incrimination – Stamp has sent us evidence that he committed US tax fraud – and at over $4m it would be one of the largest individual 1099-OID frauds ever. It is – obviously – not evidence that the IRS approved anything: IRS wage and income transcripts show data reported to the IRS on information returns; they do not, and cannot, show the IRS approved the report.16 So we can probably take Stamp at his word that he really did submit three 1099-OID records for Stamp’s trust, claiming about $4.477m of federal tax withholding. That claim is fraudulent on its face. Form 1099-OID is for original issue discount on real debt instruments; the IRS says the description box should identify the instrument by its “CUSIP” identification number.17 Stamp’s transcript instead says “ITEM DESCRIPTION: N/A”.18 The IRS has repeatedly warned that 1099-OID schemes are used to make false withholding claims and seek refunds based on fictitious “Treasury” or debt-discharge theories.19

Stamp claims to have established 3,000 “grantor trusts”, all making similar claims, with the total amounting to over $600m.

Is that true? Are there really 3,000 grantor trusts, with average claims of around $200,000 each? We have no evidence, and Stamp repeatedly refused to provide it. However, Stamp’s communications with his members/clients is consistent with there being thousands of participants. More specifically, recent litigation in New York between Stamp and a former associate provides some support that the 3,000 grantor trusts exist, and identify that an individual called William R Kimball made the claims for the trusts. We discuss the litigation further below.

“In 2025, we had IRS confirmed wages and tax transfers in excess of $600 million. And those recoupments were due to be funded to our membership between September of 2025 and now.

And of course, none of them were funded because some of the saboteurs, in fact, all of the saboteurs within our organization were reading Dan Neidle’s blogs. Dan Neidle was calling me a fraudster. Dan Neidle saying that the recruitment program, the Clifford Protocol doesn’t work.

All of those things contributed and tortiously interfered with the contracts that our membership had with the US trustees. Or as you know, the US trustees sent in fraud identity reports to the IRS and canceled all of the recoupments.”

Stamp makes a slightly contradictory claim in his New York lawsuit (more below), where he says his former associate Amy Jo Sanger “filed fabricated identity theft reports”:

Ms. Sanger maliciously filed fabricated identity theft reports to the IRS. These false reports directly undermined 3,000 legitimate grantor trusts that William Kimball had lawfully filed tax returns on. These 3,000 trusts belong to the customers of PT ICS Remedy Consulting (Indonesia), which serves as my administrative and tax filing firm.

It must also be possible that there never were $600m of claims, or they were immediately rejected, and blaming us or Ms Sanger is more convenient for Stamp than admitting the truth.

The New York lawsuit – and what it reveals about Stamp’s operation

A live lawsuit in New York shows us where the money went, who was filing the tax returns, and how Stamp was operating after leaving the UK.

On the surface, it is a narrow fight about a precious-metals account. GoldSilver LLC, a precious metals investment company, says it is holding about $883,00020 of gold, silver and cash in an account for something called the MTRXF Ministry Trust, and it asked the Southern District of New York to decide who is entitled to control it.21 This is an “interpleader” – someone essentially asking the court to adjudicate a dispute, rather than Goldsilver LLC take the decision itself, and risk being sued.

The account was opened in April 2025 in the name of “MTRXF Ministry Trust”, by a Colorado woman called Amy Jo Sanger (who said she was the settlor and trustee).2223

Stamp’s name is not on the trust documentation at all. He has not filed a conventional motion or witness statement with the court, but instead filed a document he describes alternately as a “statement of facts” and a “memorandum of law”. His case appears to be that Sanger was his bookkeeper who stole money from PT ICS Remedy Consulting, an Indonesian company controlled by Stamp, and placed it in MTRXF, her own trust. Stamp says that Sanger was trustee of another trust, the “OSN LLC trust” which had Stamp as settlor and Sanger as trustee.24

Stamp’s evidence for this consists of an “expert report” from an uncredited firm he runs25, and a witness statement from a US individual called William R Kimball who is authorised to make IRS electronic filings26 and appears to be the person making Stamp’s 3000 fraudulent refund claims. The “expert report” and “witness statement” just make a series of allegations without any stated basis, and are unlikely to be taken very seriously by the court.27

Kimball’s witness statement says his firm, William Kimball LLC, provides professional tax administration and filing services. We can find no evidence that Kimball actually carries on such a business. We are reasonably confident (from the identity documentation provided to the court) that this is the same William Kimball who ran a small biotech company.28 We don’t know why someone with a legitimate business would be involved with Stamp – we wrote to several email addresses that we verified were used by Kimball, but received no response.

So all of this tells us several things.

Stamp is now operating through an Indonesian company, PT ICS Remedy Consulting which he controls and capitalised with $2.3m.29

We now know who made the 3,000 claims – on Stamp’s account, it was William Kimball. If that’s true, he has exposed himself to criminal sanctions and, unlike Stamp, he’s living in the US.

Stamp’s “OSN LLC” trust document says all fees, donations, success fees and other income from MATRIXFREEDOM and I AM FREE, plus bank balances, intellectual property, code, platform design, and member and affiliate contact details, are trust property. The beneficiary is Iain Clifford. Until 2023, Clifford/Stamp was living in the UK – there must be a question whether he properly declared his income to HMRC.

One possible explanation is money laundering. Stamp appears to have made large amounts of money from Matrix Freedom and related ventures. The New York proceedings show money moving through an Indonesian company, a US citizen, a disputed trust and a US precious-metals account. We cannot know the full explanation, but this is exactly the kind of pattern that should attract scrutiny from banks, regulators and prosecutors.

Stamp’s response – a $120m lawsuit

Stamp has a very personal interest in the $600m of 1099 OID refund claims. He charges his members/clients “donations” – typically hundreds or thousands of pounds. But the real money would come if the claims were successful, as Stamp would have claimed a 20% “tithe” from any refunds actually received. In theory, a total of $120m.

When Stamp’s scheme collapsed (for whatever reason) his response was to blame our founder, Dan Neidle, and to threaten to sue him for $120m in Wyoming:30

The email says it’s a “Final Ultimatum” demanding removal of all Tax Policy Associates’ articles about Matrix Freedom within three days, after which Stamp would “transfer” his libel claims to “Ecclesia Law, – a trading name of MLITR Research LLC” which would then “prosecute” Dan in Wyoming.

By March 2026, Stamp changed his mind and was threatening to sue in Texas:

Stamp is a former financial services professional with a background of business failure and losing investors’ money in dubiouscircumstances. At some point after losing his regulatory authorisation, he started selling, and perhaps believing, “sovereign citizen” conspiracy theories.31 Stamp then founded an organisation called “Matrix Freedom”, selling pseudo-legal “remedies” to (very often) desperate and vulnerable people. These included a “mortgage elimination” scheme which charged clients £3,000 for template documents that (Stamp claimed) would make their mortgage disappear. Over 200 people brought claims in the High Court using these documents. Every single one was struck out, with the court saying:

” It is to all intents and purposes a ‘get-rich-quick’ scheme. Only it is nothing of the sort because the arguments that it relies upon, and which have clearly been made available to people to widely adopt, are so misconceived as to be fundamentally wrong. This deceit is all the uglier because the material that forms the building blocks of the claims (and the large group of claims) is a nonsensical and harmful mix of legal words, terms, maxims, extracts and statutes which are designed to look and sound good, at least to some. But they stand only as an approximation of a claim in law, a parody of the real thing.

…

The totality of claims that are the subject of this judgment have not revealed the full extent of the source, and nature, of encouragement and co-ordination that lies behind them but there is every appearance of deceit, of abuse and contempt of court, and it is a matter of time before a full picture of these comes to light.”

OpenDemocracy published an article on Stamp; Stamp responded by suing for libel. The claim was struck out because (amongst other failings), the pleadings were “so unreasonably vague and incoherent so as to be abusive”, and contained “the very same reliance on incoherent legal propositions that were the subject of serious and unequivocal criticism” in the mortgage case.

Stamp made a series of other claims, including against HMRC, which were dismissed as “wholly without merit”. All of this resulted in the High Court making a “general civil restraint” order against Stamp, which requires him to obtain the consent of the court before filing a lawsuit. Mr Justice Cotter said Stamp’s claims relied upon “misconceived and/or incoherent and inherently inconsistent arguments based on false propositions which have been invented to circumvent the current law”:

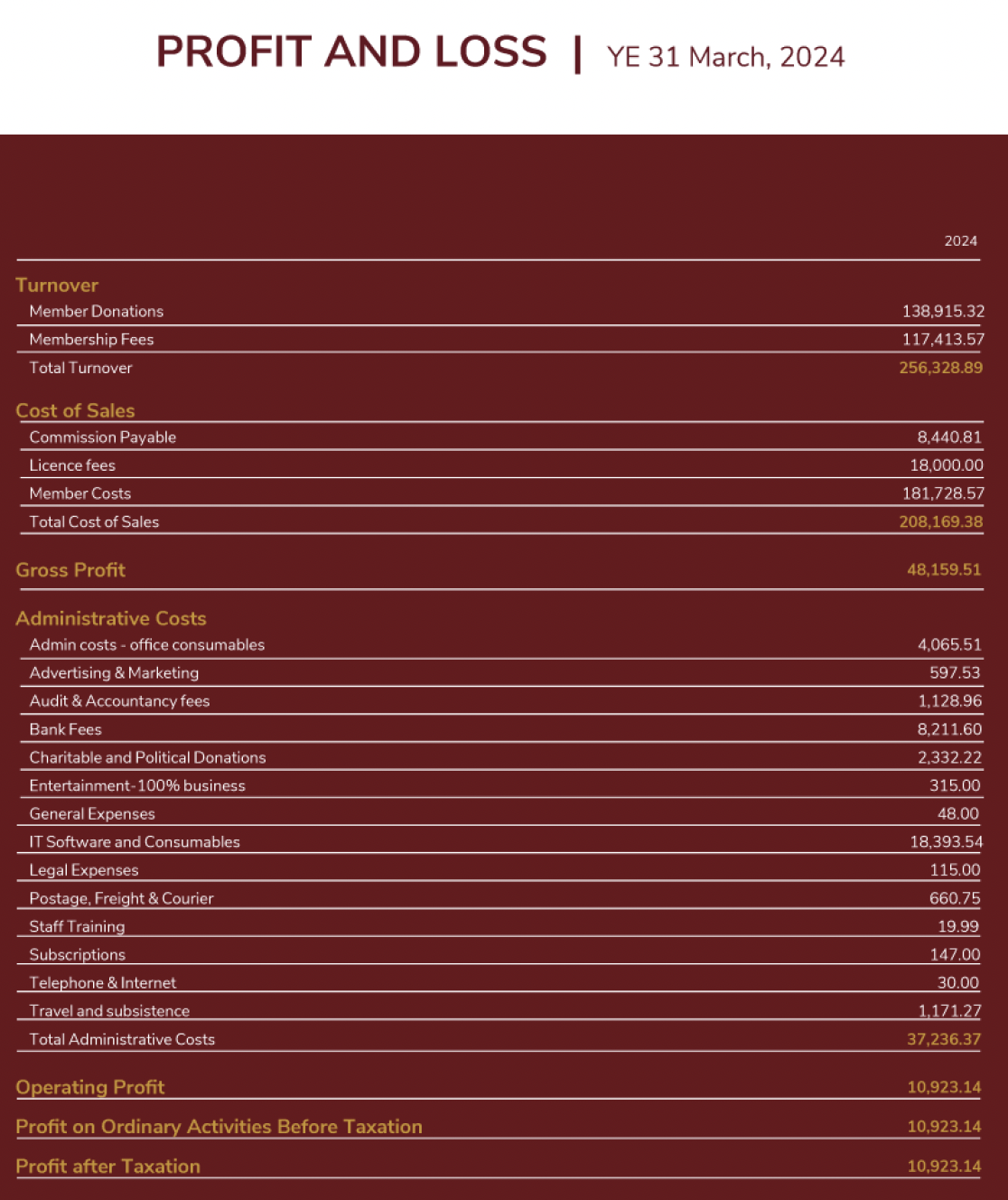

None of these failures stopped Stamp making very large amounts of money from selling his “get rich quick” schemes. In a leaked management meeting, Stamp’s team revealed that in its best month in 2022, Matrix Freedom made £500,000 from its clients. The organisation is now significantly larger, with many millions of profit made (and there’s more about this in the New York proceedings, see below).

As these schemes involve attempting to deal in mortgages and consumer loans, they require authorisation from the Financial Conduct Authority which, unsurprisingly, Stamp does not have. By 2023, the FCA had obtained an all-assets restraint order against Stamp. He was arrested and interviewed at his home in Swanmore, Hampshire. He then fled the country – first to Bali, then to Northern Cyprus.

Stamp was required by a court order to disclose all his assets. He served a witness statement saying he had “no assets, bank accounts, shareholdings, directorships or investments.” This was a lie. The court found that he had at least six undisclosed bank accounts, a BullionVault precious metals account and crypto accounts, with which he spent over $24,000 on luxury goods (Cartier, Chanel, Dior, Balenciaga) and over $60,000 on travel and hotels. He was also an undisclosed director of ten companies.32

The court found Stamp in contempt on all nine counts and sentenced him to 12 months’ imprisonment. He filed documents that were “nonsensical and difficult to understand” and “gibberish”, and didn’t show up for either hearing. His “attorney-in-fact”33, David Ayerst, did turn up and was physically removed from the courtroom when he refused to leave.

Stamp says he has appealed to the Court of Appeal, but the documents we’ve seen suggest it’s unclear if he made a valid appeal application and, if he did, it is unlikely an appeal would be granted.

Stamp has a 12-month prison sentence waiting for him in England. He has an FCA criminal investigation hanging over him. His assets are frozen (in theory). And yet he continues to run the operation, now rebranded as “The Republic of Old Souls” — filing tax returns from Indonesia, threatening journalists from Wyoming, and posting videos explaining why it’s everyone else’s fault. He changed his name to “Iain Clifford” in August 2024 by deed poll34; we will continue to refer to him as “Stamp” for consistency.

What happens now?

The reality for Stamp’s followers is that the promised millions are not coming.

Many will have paid thousands of pounds in “donations”. Some may have built their finances, relationships and hopes around the belief that the IRS owed them life-changing sums. But there is no secret tax asset. There is no “signature credit energy”. There is no lawful route by which a British borrower can claim a US tax refund because they once signed a mortgage, loan or credit-card agreement.

On Stamp’s own account, his organisation created 3,000 trusts and caused $600m of fraudulent refund claims to be filed with the IRS. He has publicly explained the scheme. He has identified the supposed legal basis. He has blamed us and others for the IRS freezing the money. And he has sent us what appears to be an IRS transcript showing a $4.477m fraudulent withholding claim for his own trust. It is very strange that someone would incriminate themselves so thoroughly, but that is what Stamp has done. Northern Cyprus may not be as safe as Stamp imagines – it has recently shown a willingness to deport foreign fugitives.

If William Kimball really made false US tax filings for 3,000 trusts, then his position is also extremely serious.

The position of Stamp’s clients is different. In principle, a person who knowingly submits a false tax claim can commit a criminal offence. But many of Stamp’s followers appear to be victims themselves: people persuaded by pseudo-legal nonsense, conspiracy theories and promises of impossible wealth. Some may have had little idea what was being filed in their name or in the name of a trust created for them. In theory they should take independent legal advice if any IRS forms were filed using their details, and do so with particular urgency if any refund money is actually received. We fear that few if any will have either the willingness or the resources to do that.

The tragedy is that the people least able to afford the consequences of Stamp’s actions are likely to suffer most. Stamp can reinvent himself, change his name, move jurisdiction, create new entities, and publish new videos blaming saboteurs. His followers are left with the losses, the broken promises, and the legal consequences of false documents filed in their names.

All this could have been prevented if action had been taken against Stamp before he fled the UK. Not mere sanctions for regulatory breaches (effective as the FCA appears to have been), but arrest and prosecution for defrauding his mortgage “clients”. The failure to stop him then led to the much larger fraud now, and the much greater number of victims.

The promised millions were never real. The fraud, the victims and the consequences are.

Many thanks to K for extensive research, and to K, P and C for their US tax expertise.

Footnotes

The conspiracy theory that individuals have access to a secret “government account” originated in far-Right anti-government movements in the United States in the early 1980s. By the late 1980s, Roger Elvick developed the idea further, claiming that these supposed accounts could be accessed by filing fraudulent tax forms with the IRS see analysis. Elvick obtained payments from the US Treasury using these methods before being convicted of fraud and imprisoned for much of the 1990s. Elvick’s scheme involved submitting false IRS Forms 1099-OID to fabricate withholding credits, triggering refunds. Courts consistently treated these filings as fraudulent, and similar schemes continue to be prosecuted.

Elvick was also associated with extremist groups, includingreportedly participating in networks linked to Aryan Nations and other white supremacist groups, which were influential in developing pseudo-legal theories about government “strawman” accounts. From the 2000s onwards, variants of his theory spread more widely online, becoming embedded in what courts and researchers now describe as the “sovereign citizen” movement. ↩︎

Stamp claims the conviction is a “jurisdictional nullity”. The points he raises are, at most, allegations of procedural or evidential error. In English law, a decision is a nullity only where the court lacked jurisdiction or there was a fundamental defect going to its authority (for example, no valid service and no submission to the court’s jurisdiction). Stamp’s complaints, even if well-founded, would render the decision at most voidable on appeal; they do not make it a nullity. In the event, his arguments are untenable; Stamp plainly had notice of the proceedings (both in law and in fact), any issue as to the prosecutor’s internal authority does not affect the court’s jurisdiction, and Stamp failed to pursue either point at the hearing (indeed he failed to attend the hearing). It’s also unclear whether Stamp actually brought an appeal within the applicable time limit. We’d therefore be surprised if he’s granted permission to appeal. ↩︎

At this point Stamp can’t keep his story straight. If he’s made $600m of claims for 3,000 people then the average is $200,000, not $2-3m. We are very doubtful any of his followers have recouped anything like $2m, not least because Stamp would be proudly displaying large cheques as evidence. ↩︎

Stamp may use the word “recoupment” because a Google search for “1099-OID refund” makes very clear the scheme is fraudulent. ↩︎

Nothing Stamp says has any connection with the actual content of IRS Publication 1212. Publication 1212 is a guide to original issue discount – broadly, interest-like income on debt instruments issued at a discount – and to the reporting obligations of brokers, middlemen and holders of such instruments. Its references to “nominees” are mundane: a broker or middleman may hold an actual OID debt instrument for the true owner, and may therefore have to issue information returns. That does not create OID where none exists, and it does not turn a mortgage, credit-card application, birth certificate or signature into a tax-refund-generating security. Stamp takes ordinary words from Publication 1212 – “nominee”, “OID”, “beneficiary”, “1099-OID” – and attaches them to an entirely imaginary theory. Nothing in Publication 1212 or US tax law supports that theory. ↩︎

Modern commercial banks do create new money when they make a loan. They do this by recording a loan asset (you owe them £X) and creating a matching deposit liability (your account now has £X). This is standard double-entry bookkeeping. However whilst the deposit belongs to you (you can spend it), the asset belongs to the bank (your obligation to repay). ↩︎

There’s a well-documented phenomenon of members of cult-like groups rationalising the group’s failures, and becoming more committed to the cult. When Prophecy Fails is the classic text. ↩︎

Why does anyone get a cheque when, in principle, the IRS should be able to see that they never received the withholding tax? There are additional warning signs the IRS should register – the withholding tax is in most reported fraud cases equal to the “discount” – that should ring alarm bells given the actual withholding tax rate is 30%, not 100%. And a further bell should ring because, when the issuer of a debt security gives a 1099-OID to an investor, they file an identical copy to the IRS – a modern tax system really should only issue refunds once withholding tax payments and 1099-OID forms have been received, and basic initial checks have been satisfied. But the IRS is famously reliant on paper forms, and in practice the timing of returns and refunds mean that the IRS often pays out refunds before it has reconciled refund claims with the filings it has received. The reconciliation also seems imperfect, probably because of the very large volumes and antiquated systems – so many 1099-OID frauds continue for a while before being discovered, and in the meantime it’s common for at least some cheques to be issued. Mistaking this for IRS approval is a serious mistake. ↩︎

The applicable US criminal provisions include 18 U.S.C. § 1343 (wire fraud), if customers were solicited online or false filings were transmitted through interstate or foreign wires; 26 U.S.C. § 7207 (fraudulent returns, statements or other documents), for delivering Forms 1099-OID or related documents known to be false as to material matters; 18 U.S.C. § 371 (conspiracy to defraud the United States), if Stamp, PT ICS Remedy Consulting and an ERO agreed to obstruct or impair IRS functions by filing false returns; 26 U.S.C. § 7206(1) and (2) (fraud and false statements), for making, subscribing, aiding, assisting, procuring, counselling or advising tax documents false as to material matters; and potentially 18 U.S.C. § 1956 / 18 U.S.C. § 1957 (money laundering / monetary transactions in criminally derived property), if proceeds of the fraud were routed through PT ICS Remedy Consulting in Indonesia and into US accounts or bullion accounts. ↩︎

The leading Supreme Court authority is Cheek v United States, 498 U.S. 192 (1991). Cheek pre-dates the modern sovereign citizen movements, but the arguments run by Cheek look very familiar. The case supplies the governing rule for criminal tax cases: the government must prove “wilfulness”: the voluntary, intentional violation of a known legal duty. A genuine good-faith misunderstanding of what the Internal Revenue Code requires may negate wilfulness, even if the misunderstanding is objectively unreasonable. But a belief that the tax laws are invalid, unconstitutional, or do not bind the defendant is different, particularly when the defendant is fully aware of previous prosecutions and IRS statements. The courts characterise this as a rejection of the law, not a misunderstanding of the law, and it provides no defence – and Federal appellate courts have repeatedly applied this principle to sovereign-citizen and tax-protester arguments. In United States v Sloan, the Seventh Circuit rejected the claim that the defendant was a “freeborn, natural individual” and state citizen outside federal tax jurisdiction. In United States v Ward, the Eleventh Circuit rejected arguments that the United States’ taxing jurisdiction was limited to federal enclaves and that the defendant was not an “individual” within the Code. And in United States v Gerads, the Eighth Circuit sanctioned litigants who claimed to be “Free Citizens of the Republic of Minnesota” and not subject to federal taxation – their arguments were “utterly without merit”. So a defendant may, in principle, rely on a genuine misunderstanding of a complex tax obligation. But pseudo-legal theories that the taxpayer is sovereign, outside federal jurisdiction, not a “person” or “individual”, or immune from tax law are routinely treated as frivolous, not as a defence. ↩︎

“Attorney in fact” is a US term for someone acting under a power of attorney. Claims that an “attorney-in-fact” can act as a courtroom representative are a standard sovereign-citizen trope, and have been rejected by US courtsfordecades. We have reported Ecclesia Law to the Wyoming State Bar. ↩︎

The documents have numerous signs of AI-generation – for example overuse of em dashes, heavy/unnecessary use of tables, broken footnotes, and fluent but empty and sterile prose. In one case, Stamp sent us an email in which he forgot to delete “Gemini says” at the start (it’s visible in the plain text/source but not the html). ↩︎

The document is based on the standard sovereign citizen claim that there is a distinction between someone’s physical body (“the living man”) and a “corporate debtor legal fiction” created by their birth certificate. As the High Court recently noted, there’s no record of any court, anywhere in the world, accepting these kinds of arguments. It makes a series of”pseudo legal” arguments, which look like law to some laypeople, but have no legal meaning whatsoever. Neither this nor any other document refers to actual US tax law; when we challenged Stamp for the legal basis for the claims he made. For completeness, we have set out his claims and the actual position here:

Under the Bills of Exchange Act 1882, a signed mortgage loan is a negotiable instrument. The Bills of Exchange Act is a UK Act of Parliament. It is irrelevant to the US tax code, and Stamp surely knows this. The US Treasury said: “The theory behind their use is bogus and incomprehensible”. For completeness, a standard “mortgage loan” is not a bill of exchange under the Act because it is a two-party loan/security agreement, not an order addressed by one person to another requiring payment. It is also not normally a “promissory note” because it is a wider contractual arrangement, not an unconditional negotiable promise to pay a sum certain; the amount ultimately payable is also rarely a fixed “sum certain”.

26 U.S.C. §6049(d)(4) and Treas. Reg. §1.6049-4(b)(3), support a “nominee reporting mandate”. These are realcitations, but nothing in these provisions authorises a borrower/beneficiary/trust to prepare and file its own 1099-OID.

A trust can file its own “corrective 1099-OID”.26 U.S.C. § 6049(a) requires information returns from the person who pays interest, or a nominee receiving interest on behalf of the true owner. It does not let the recipient invent a Form 1099-OID. IRS Publication 1212 says the issuer or broker provides Form 1099-OID, and nominee reporting applies where someone receives a Form 1099-OID for amounts belonging to another actual owner: IRS Publication 1212.

OID arises from signing a loan.26 U.S.C. § 1273(a) defines original issue discount as the excess of a debt instrument’s stated redemption price at maturity over its issue price. It has no relevance to a borrower signing a mortgage.

The issue price is zero because credit is created “ex nihilo”. § 1273(b) determines issue price by reference to what investors paid for the instrument, its stated principal amount, or other statutory pricing rules. It is not zero because a borrower signed a document.

Banks remit Form 945 taxes on “signature OID”. Form 945 is for non-payroll withholding, including backup withholding on reportable interest and dividends. It is not a secret pool of tax generated by loan signatures.

The “810 Algorithm” clears refunds. IRS materials use Transaction Code 810 as a refund-freeze code. The Internal Revenue Manual says a freeze is set by posting TC 810: IRM 21.5.6, Freeze Codes. Stamp’s own account that the claims were hit by TC-810 freezes is therefore consistent with IRS fraud controls, not IRS approval. Stamp’s refund claims are fraudulent whether or not they are immediately blocked by the IRS, and whether or not he correctly understands the algorithm the IRS uses when determining which claims to block.

Publication 1212 permits “nominee correction”. Publication 1212 is about genuine OID instruments. Nominee reporting applies where a nominee actually receives a Form 1099-OID for amounts belonging to someone else. The result (very broadly) is that the nominee issues another 1099-OID to the beneficiary; the amount of OID does not change. This does not allow a trust to create a new Form 1099-OID from an ordinary loan, PAYE deduction, utility bill or service contract.

A “98-series EIN” gives special Holder in Due Course status. EIN prefixes are administrative. They do not grant commercial-law rights, tax-credit status or standing to reclaim bank withholding.

HJR-192 is the legal foundation. HJR-192 was a 1933 gold-clause measure about payment obligations in lawful money. It has no connection to OID, Form 1099-OID, IRS withholding, refund credits or grantor trusts. ↩︎

The Brekke fraud was for $763m and, like this one, mostly involved non-US citizens. $13m was actually received by the Brekke participants. The Poynter fraud was for $100m; $3m was paid out. The Jenkins fraud was for $562.4m; it’s unclear how much was paid out. According to the IRS, all the various schemes have together claimed $3.3 trillion in fraudulent refunds. ↩︎

IRS, Topic no. 159: a wage and income transcript “shows the data reported to us on information returns such as Forms W-2, Form 1099 series, Form 1098 series, and Form 5498 series”. ↩︎

IRS, Instructions for Forms 1099-INT and 1099-OID, Box 7: “Enter the CUSIP number, if any. If there is no CUSIP number, enter the abbreviation for the stock exchange, the abbreviation for the issuer used by the stock exchange, the coupon rate, and the year of maturity… If the issuer of the obligation is other than the payer, show the name of the issuer.” See also IRS Publication 1212, explaining that OID reporting concerns debt instruments and that a nominee who receives a Form 1099-OID for amounts belonging to another person files a nominee Form 1099-OID for the actual owner, not for invented “signature credit”. The statutory framework is 26 U.S.C. §1272 (current inclusion of OID by the holder), §1273 (OID is the excess of stated redemption price at maturity over issue price), and §6049 (returns regarding payments of interest, including nominee reporting). ↩︎

We asked Stamp about this in correspondence. He said the IRS “810 Algorithm does not rely on text-based item descriptions” but instead “cross-references the Payer EIN and the specific CUSIP number against the Payer’s Form 945 tax module”. This is gobbledegook. Stamp’s reference to the “810 Algorithm” is to the IRS’s procedure for putting a fraud hold on refund claims. Stamp confuses this with substantive law – he believes (or pretends to believe) that if you successfully fool the IRS’s fraud detection processes, and the IRS don’t put a hold on your refund claims, then your refund claim is lawful. ↩︎

IRS, The Truth About Frivolous Tax Arguments: in OID schemes, filers falsely list large OID income and corresponding withholding, often using debt such as credit card debts and mortgages; Form 1099-OID “is in no way a financial instrument” and is not a method of payment or Treasury redemption. IRS processing guidance also treats suspicious 1099-OID withholding claims as potential fraud: see IRM 3.11.6 on “outlandish and/or unsubstantiated credits” often involving Forms 1099-OID, and IRM 3.12.8, which says to flag Form 1099-OID submissions for fraud where federal tax withheld exceeds income or the submission appears fraudulent. ↩︎

The numbers shift a little across the filings: $700,000 in the February letter and Ecclesia Law “expert” report, approximately $900,000 in the later statement of facts and March letters. The 6 February letter refers to “approximately USD $700,000” of Indonesian company funds; the 11 February statement of facts refers to “approximately $900,000”; the 3 March and 27 March letters refer to approximately $900,000 frozen by GoldSilver. See Clifford amended supplemental letter, 6 February 2026, p.1; Clifford statement of facts, pp.1 and 3; Clifford letter, 3 March 2026, p.1; and Clifford status report, filed 7 April 2026, pp.1-2. ↩︎

GoldSilver’s interpleader complaint says the account held “27 100-ounce silver bars, 269 ten-ounce silver bars, seven ten-ounce gold bars, 68 one-ounce gold bars, and $5,437.47 in cash”, and that the approximate value of the assets was $883,613.38. It says GoldSilver has “competing claims” from Sanger and Clifford as to their roles in the trust and authority over the account. See GoldSilver interpleader complaint, 21 October 2025, pp.1-5. GoldSilver says the online application was apparently filled out by Sanger. GoldSilver says: “The Account was funded on or about June 25, 2025 through a transfer deposit from another account held at GoldSilver in the name of ICS Remedy Consulting. GoldSilver understands that Sanger controls the ICS Remedy Consulting account.” See GoldSilver interpleader complaint, p.3. ↩︎

We spoke to an experienced Colorado trust attorney who thought the MTRXF trust document would likely have no legal effect, and that the trust assets would be regarded as owned by Sanger.The trust document has numerous strange features – to name just three: it doesn’t name beneficiaries (they are in secret “Trust Minutes”), it claims to be created by the “Common Law Right of Contract” (trusts in Colorado are governed by the Colorado Uniform Trust Code and the law of equity); the trust claims to have “absolute sovereign immunity from all outside interference” and says “No court’s authority is recognized to intercede”. ↩︎

Sanger says Stamp later gave GoldSilver a different document, dated 17 February 2025, which concerned an “OSN CORPORATION Trust”. She says that was a different trust, not the document she used to open the GoldSilver account, and not something that amended or replaced the MTRXF paperwork. See Sanger declaration, pp.1-2. ↩︎

Our view is that this “trust” would not be not recognised under English law and probably creates some kind of agency relationship under which Sanger acts for Stamp. The document fails the English law requirement that a trust must be certain. There is uncertainty as to who is the trustee – the document says the trustee is “Amy Sanger the shareholder and director of OSN LLC (the “Trustee”)”. There is uncertainty as to whether a trust relationship is actually intended – the trust is said to be irrevocable (clause 12). but it also says the settlor can collapse the trust at any time (clause 10) and the settlor can direct the trustee and appoint a replacement trustee. There is also uncertainty of subject matter: the trust is stated to be over future acquired property (generally not possible). English law does not recognise revocable trusts. Colorado law does, but we understand from Colorado counsel that Colorado would not recognise this trust given the lack of certainty. The document says “this Trust is established under Common Law” which is a non-sequitur – trusts are a creation of equity, not common law. ↩︎

“Ecclesia Law” which “functions as the Attorney-in-Fact division of MLITR Research LLC, a Wyoming-registered company”. Stamp says he writes the LLC’s materials, and it seems reasonable to assume it is controlled by him. The report consists of conclusions and allegations against Sanger but does not explain the basis of the conclusions and reasons for the allegations. ↩︎

The “expert report” provides no reasoning or methodology. The “witness statement” contains no first hand account of events, and contains conclusory statements such as that Sanger is a “a very dishonest person”, and statements outside Kimball’s knowledge, such as the nature of Ms Sanger’s role. Kimball claims to have filed a IRS Form 3949-A against Sanger – the form is used to report breaches of tax law. Stamp characterises this as the IRS formally accepting Kimball’s “repudiation” and Sanger becoming subject to an active federal criminal investigation. There is no evidence of that at all. The form itself is just an IRS information referral form, and its own instructions say Form 3949-A is not the right form for identity theft or unauthorised preparer filing. ↩︎

We say “ran” because, whilst the website lists Lee Thibodeau as the co-founder, but he died last year. ↩︎

The Indonesian registry categorises the company’s business activity under KBLI Code 70209: “Other Management Consulting Activities”. The description for this code covers generic business advice, human resources, and management information. It is a broad, catch-all classification commonly used by foreign entities that do not want to trigger regulatory scrutiny in Indonesia. The company’s profile says it changed its name to ICS Remedy Consulting in on 11 February 2026, and that was approved/recorded by the Indonesian authorities on 5 March 2026. The timing is odd given that Stamp made a filing in the New York litigation on 11 February 2026 referring to “my Indonesian entity, PT ICS Remedy Consulting”. ↩︎

Since late 2024, Stamp has conducted a sustained campaign of pseudo-legal threats against Tax Policy Associates and its founder. In November 2024 he sent Dan Neidle the first of three sovereign-citizen “estoppel notices,” before issuing a fake “Lien Judgment” from his own invented court claiming Dan owed him money. ↩︎

Like most sovereign citizens, he denies he is a sovereign citizen, but the language he uses, and the arguments he employ, makes clear that he realistically is. ↩︎

As noted above in the context of Ecclesia Law, “Attorney in fact” is a US term for someone acting under a power of attorney, which sovereign citizens frequently claim permits someone who is not a qualified lawyer to represent a third party. US courts have consistently rejected that proposition. The position in England and Wales is the same: rights of audience are reserved to authorised persons, and a power of attorney does not create an exception (which is why Ayerst was not permitted to represent Stamp). ↩︎

It’s unenrolled, the wording is eccentric, and it gave a correspondence address rather than an actual address. It’s unclear why he changed his name; our suspicion is it was an attempt to escape or defeat the FCA proceedings. ↩︎

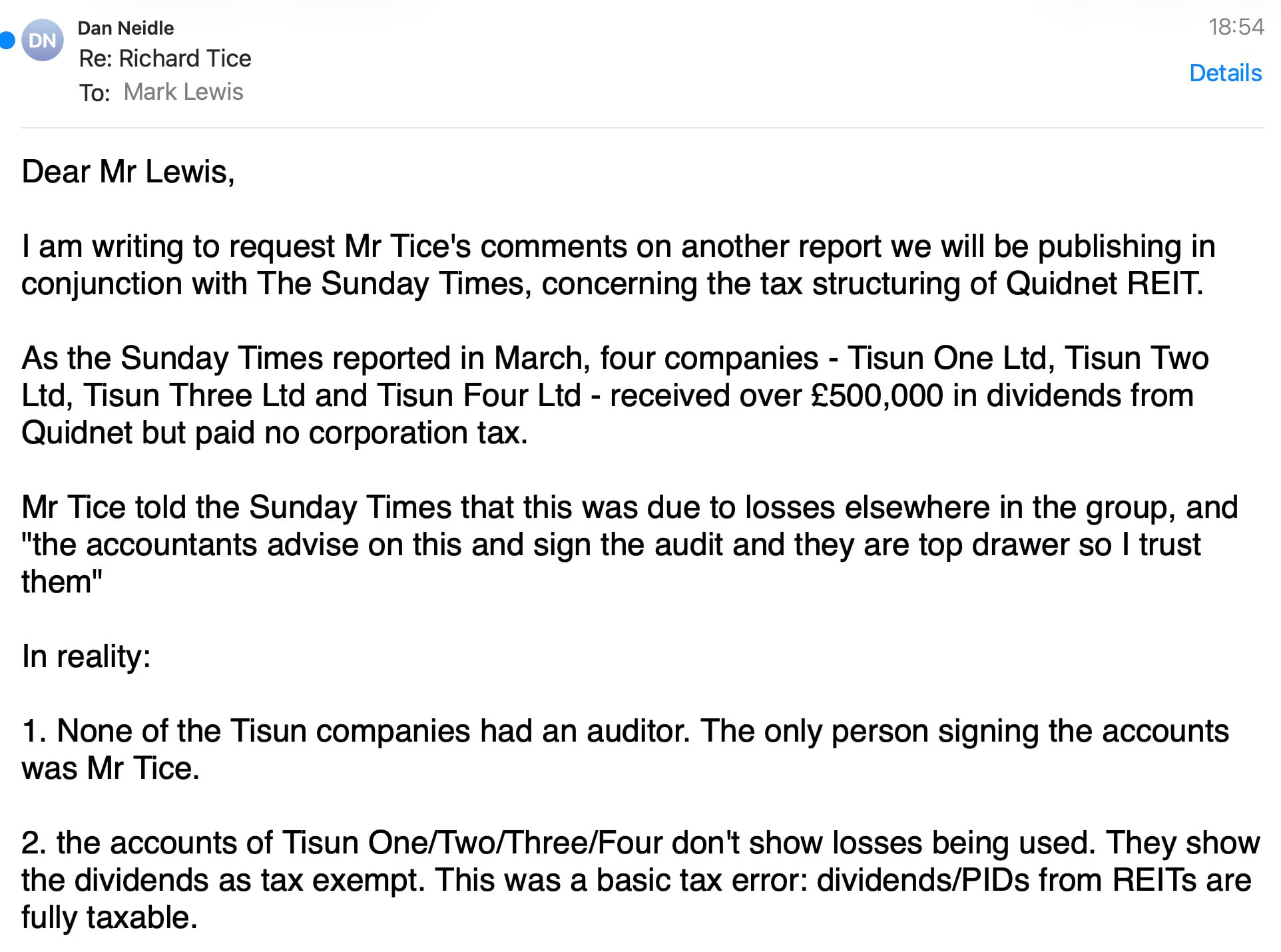

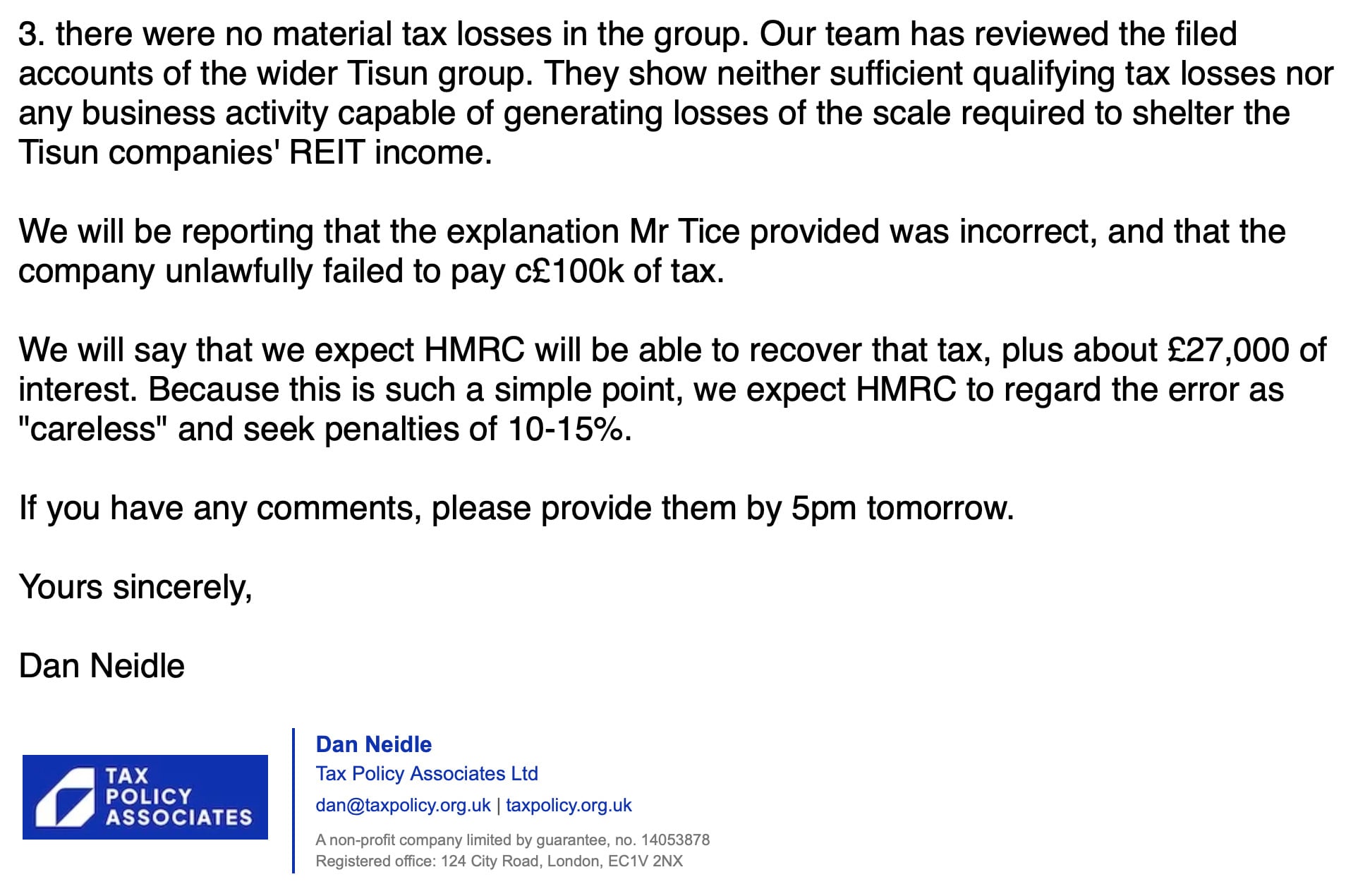

Richard Tice, the deputy leader of Reform UK, used his Quidnet property company’s REIT status to save tax. That meant Quidnet itself paid no corporation tax on its property business – but the quid pro quo was that its corporate shareholders had to pay tax on the dividends they received. They did not. Instead, Mr Tice signed accounts wrongly claiming that the dividends – £514,000 in total – were tax exempt. The result: they failed to pay £98,000 of corporation tax.

This is a different issue from our previous report, which found that Quidnet REIT failed to withhold about £120,000 of tax on distributions to Mr Tice and his offshore trust. But it arises from the same underlying mistake: claiming the tax benefits of a REIT but ignoring the tax liabilities.

Diagram connections

Diagram connections

From Quidnet REIT to Tice companies (Label: £514k dividend)

From Quidnet REIT to Tice companies (Label: £514k dividend)

Key points:

Quidnet REIT paid about £514,000 of property income distributions to four companies: Tisun One, Tisun Two, Tisun Three and Tisun Four.

Quidnet REIT paid no corporation tax on this income, because it was a REIT. The four Tisun companies were supposed to pay tax instead — but they didn’t.

The payments were wrongly treated in the accounts as tax-exempt ordinary dividends. In fact they were taxable REIT property income distributions.

The result was about £98,000 of unpaid corporation tax.

Mr Tice has previously said the lack of tax was due to losses elsewhere in the group. The accounts contradict that, and our analysis finds there were insufficient losses in the group to eliminate the tax.

HMRC should be able to assess the tax, plus roughly £27,000 of interest and penalties likely in the region of 10–15%.

These are basic errors. That raises a further question: what else went wrong? In particular, did Mr Tice’s offshore trust also fail to pay tax on the distributions it received from the REIT?

Mr Tice did not respond to requests for comment from us or The Sunday Times.

Technical terms in this article

Real Estate Investment Trust (REIT)

A UK company that elects into a special tax regime for property investment. Broadly, the REIT does not pay corporation tax on its qualifying property rental business; the tax point is shifted to investors.

A distribution paid by a REIT out of its property rental business profits or gains. Unlike an ordinary dividend, a PID is generally taxable in the hands of the investor.

Tax deducted by the payer before money is paid out. In the REIT context, PIDs are generally paid under deduction of income tax at the basic rate unless an exception applies.

A normal company dividend. For most UK corporate recipients, ordinary dividends are generally exempt from corporation tax. That is different from a REIT PID.

The main UK tax on company profits. In this article, the key point is that UK companies receiving REIT PIDs are generally taxed on them as property business income.

A UK tax relief allowing certain losses of one company to be surrendered to another company in the same 75% group. It is often used to offset one company’s profits with another’s losses.

Where companies are only in the same group for part of an accounting period, group relief is limited to the period of common ownership. The relevant shared period is called the overlapping period.

A note in a company’s accounts showing how you get from the accounting profit to the tax charge. It can reveal whether a company says tax was reduced by dividends, losses, group relief or something else.

A digital filing format for accounts and tax documents. It looks like an ordinary document on screen, but has machine-readable tags embedded in it so software and regulators can identify what each figure means.

From 10 September 2018 to 9 August 2021, Quidnet was a REIT: a form of tax-exempt investment fund that invests in real estate. The consequence is that the company becomes exempt from corporation tax on its property rental business, but its investors are (broadly speaking) taxed as if they held the real estate directly.1

Quidnet REIT direct shareholders as at 1 July 2021

From Richard Tice (direct) to Quidnet REIT (Label: 13.00%)

From RJS Tice Family Settlement to Quidnet REIT (Label: 16.88%)

From RJS Tice Family SIPP to Quidnet REIT (Label: 34.98%)

From Tisun One to Quidnet REIT (Label: 7.80%)

From Tisun Two to Quidnet REIT (Label: 7.78%)

From Tisun Three to Quidnet REIT (Label: 7.78%)

From Tisun Four to Quidnet REIT (Label: 3.38%)

From Huntress (CI) Nominees to Quidnet REIT (Label: 4.42%)

From NJG Tribe SIPP to Quidnet REIT (Label: 2.99%)

From Employees to Quidnet REIT (Label: 0.98%)

Quidnet REIT correctly paid no tax on its property income. But that shifted the burden elsewhere.

It had to withhold tax on dividends it paid out of that income to Richard Tice and his offshore trust – “property income distributions”. As we’ve previously reported, it didn’t do that. Quidnet mistakenly treated the dividends as ordinary dividends and failed to withhold about £120,000.

This report is about another, potentially more serious, error. Quidnet’s UK corporate shareholders had to pay tax on their dividends. They did not – they treated them as tax-exempt.2

There were four corporate shareholders:3 Tisun One Ltd, Tisun Two Ltd, Tisun Three Ltd and Tisun Four Ltd. The sole director of all four companies was Richard Tice.

Quidnet REIT made about £514,000 of payments to the four Tisun companies.4 None of them ever paid tax.

The consequences are straightforward: HMRC can recover the tax, with interest and penalties. We return to this below.

Richard Tice’s original explanation

The Sunday Times asked Mr Tice why none of the four Tisun companies ever paid any corporation tax. Mr Tice told The Sunday Times that this was because of “wider losses suffered by the group”:

These statements were incorrect:

The accounts do not show losses being used.

There were in fact no tax losses in the group.

The front page of the accounts shows that the Tisun companies had no auditor – the only person who signed the accounts was Mr Tice:

The accounts don’t show loss utilisation

What the Tisun companies’ accounts actually show is an incorrect claim for a dividend exemption.

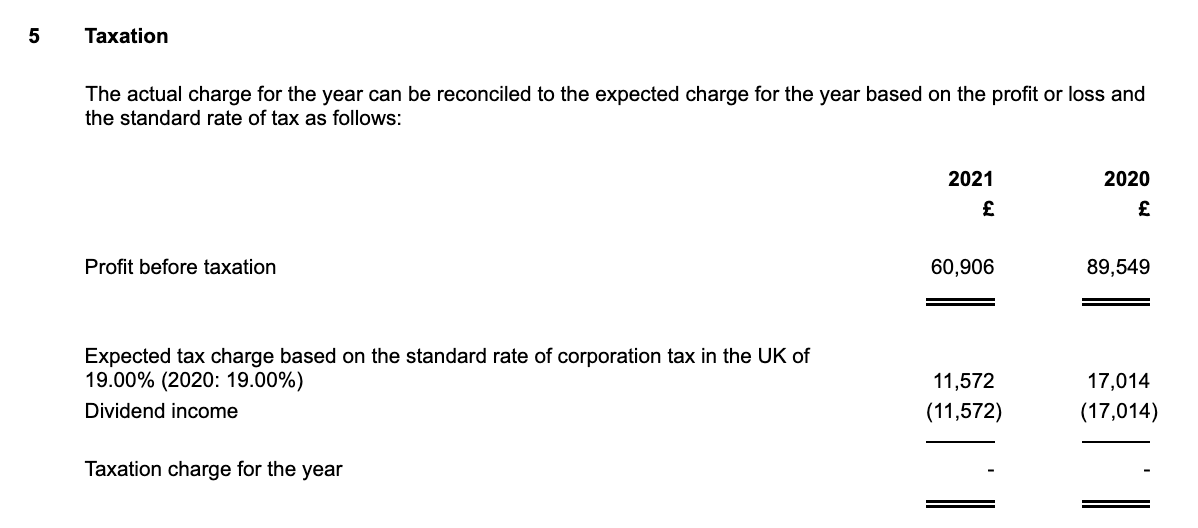

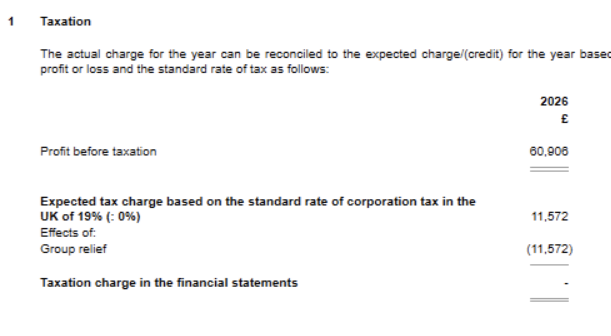

Here’s Tisun Three Limited’s tax reconciliation from its 2021 accounts (the tax reconciliation shows how you get from the profit in the accounts to the tax charge).

In this period, Tisun Three received £60,906 of property income distributions from the REIT. The accounts show the expected tax charge of £11,572 if you just apply the corporation tax rate of 19% to the £60,906 of income.

The tax reconciliation then explains why this tax doesn’t in fact arise. It shows the £11,572 of tax cancelled-out by a £11,572 negative entry labelled “dividend income”. The meaning is clear: the accounts are saying this was a dividend, and companies are normally exempt from corporation tax on dividends.

The problem is that this wasn’t a normal dividend at all. It was a “property income distribution” from a REIT – the REIT had been exempt on that profit, but corporate shareholders were not exempt. Tisun Three Ltd made the same mistake as Quidnet REIT did – it treated the payments from Quidnet as normal dividends, not as property income distributions.

The company therefore unlawfully failed to pay tax.

The result was that Tisun Three failed to pay tax on £60,906 of income in 2021, meaning lost corporation tax of £11,572 (at the 19% rate at the time).

This is repeated across almost all the Tisun companies accounts for all relevant years.5 You can download all the relevant accounts here.

The total untaxed income was £513,901, and therefore the lost tax was £97,641.6 Our methodology for this calculation is set out in full below.

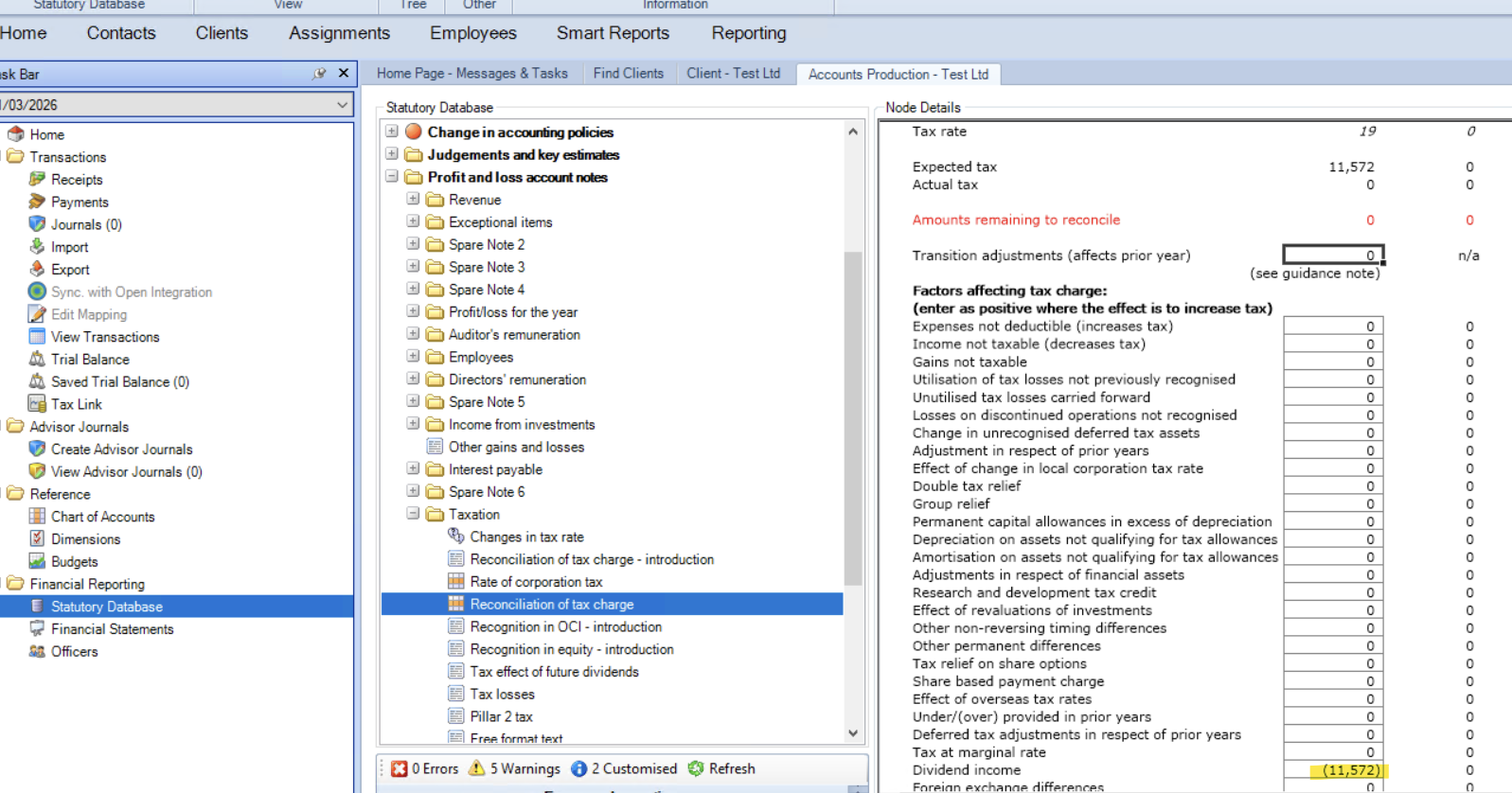

We should, however, consider the possibility that someone was being sloppy and typed “dividend income” when they really meant “dividend income is sheltered by losses”. If all we had was the printed accounts then we couldn’t exclude that possibility. We can, however, go beyond the printed accounts and read the underlying iXBRL code7 that Tisun Three Ltd’s accounting software uploaded to Companies House. The code for this line is:

This shows that the “(11,572)” figure in the tax reconciliation, negating the tax, was given the tag “TaxIncreaseDecreaseFromEffectDividendsFromCompanies”. This is a specific tag for the dividend exemption.8

If the company really had sheltered its income with losses, we would expect to see a group relief or loss-related reconciliation item (such as “TaxIncreaseDecreaseArisingFromGroupReliefTaxReconciliation”), not a dividends-from-companies item.

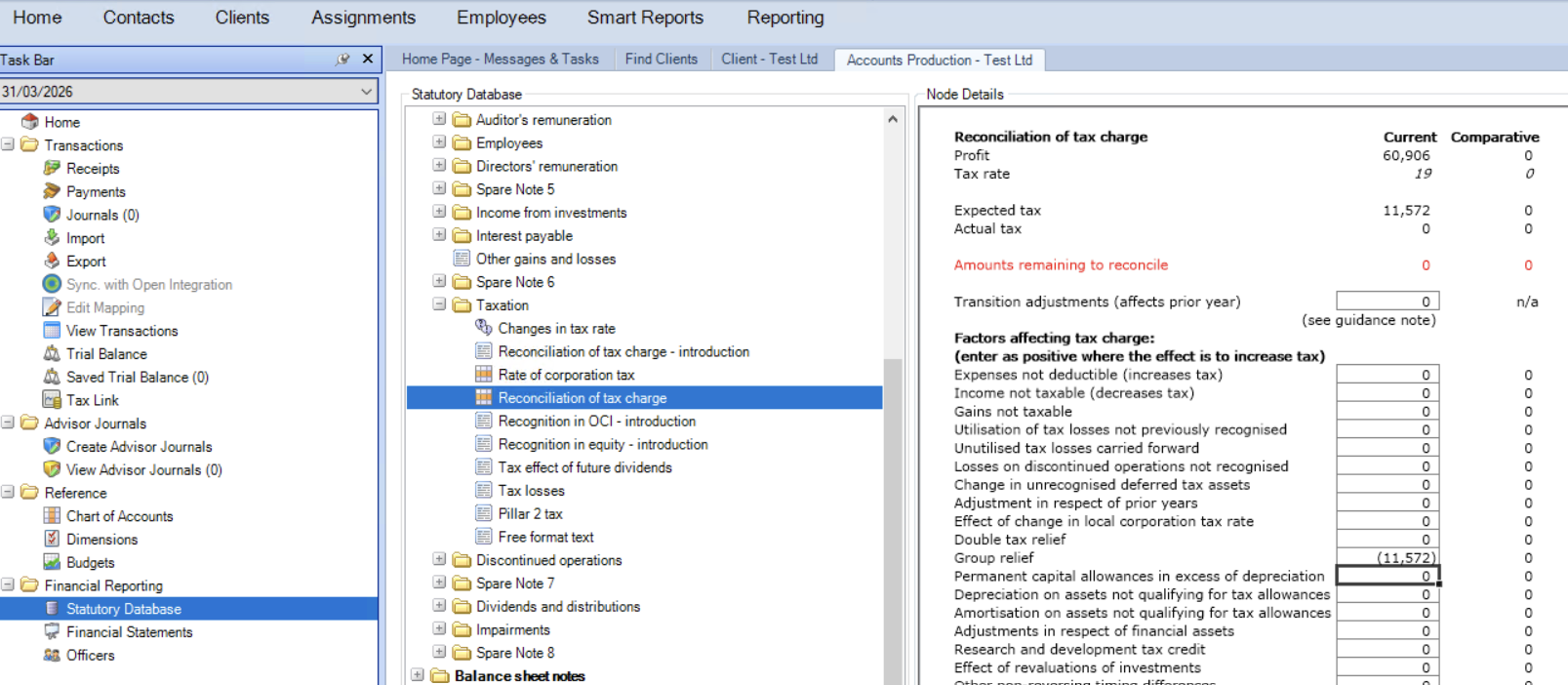

The iXBRL code also shows the accounts were submitted using CCH Accounts Production software. Here’s a screenshot showing what the accountant would have seen when entering the figures into that software, and what they would have entered to get the result that we see:

And here’s what they would have entered if they were actually claiming group relief:

The iXBRL code tells us that the tax reconciliation wasn’t merely poorly or sloppily worded – the accountant submitting the return actively selected the dividend exemption – when the dividend exemption could not in fact apply.

Is it theoretically possible tax losses were used?

It is possible in principle that Mr Tice was correct that group relief was claimed, and the accounts are simply wrong. For example, an accountant simply absent-mindedly used the dividend exemption box, when actually the Tisun companies were utilising losses from elsewhere in the group. The tax accountants we spoke to thought this would be unlikely. This is not a “fat finger” error, because it was repeated for three different companies across three years: 2020, 2021 and 2022.

There is, however, a more fundamental problem: our team undertook detailed due diligence of the wider group (including a review of 38 companies’ filings and 260 sets of accounts), and we found no material losses that could have been used to shelter the Tisun companies’ profits. That’s because, in short, the parent of the Tisun companies didn’t have assets or liabilities that could generate a material tax loss, and the way the group was structured means that losses of companies in the wider group were unavailable. Full details of this analysis are set out below.

So we believe we can exclude the possibility that the reason the Tisun companies paid no tax was the availability of losses elsewhere in the group.

Could the accounts just be wrong and tax really was paid?

We can exclude this for two reasons.

First, all four Tisun companies received dividends from Quidnet and then passed them straight up10 to their parent, Tisun Investments, without retaining anything to pay tax. The Tisun companies show no sign of any borrowing to fund any tax liabilities, and no creditor liability reflecting an upcoming tax bill. Their accounts show that each company’s sole asset was its investment in Quidnet REIT shares (funded by an inter-company loan).

Second, when the Sunday Times first asked Mr Tice about the lack of tax in the Tisun companies, he agreed they paid no tax, but said that was because of group relief.

The consequences

This is not tax avoidance. There was no loophole or grey area here. The rules on REIT property income distributions are clear: they are taxable in the hands of UK corporate recipients. This is understood by all advisers and (in our experience) most businesspeople owning and operating REITs.

Nor is this tax evasion – a criminal offence requiring dishonesty and intent. There is no evidence of either here.

The Tisun companies just paid the wrong amount of corporation tax. The practical consequence is that HMRC is likely to seek to recover that tax.

In most cases, HMRC would do this by issuing a “discovery assessment” — reopening a closed tax year where it discovers that tax has been underpaid. This is routine where an error only becomes apparent after the original return was filed.

Where a company has failed to take reasonable care — what the law calls a “careless” error — HMRC has six years from the end of the relevant accounting period to assess the additional tax. All of the periods in question here appear to fall comfortably within that window.11 We expect HMRC’s starting position would be that a failure to tax property income distributions is careless, and it is not obvious what explanation the company could provide that would overcome that.

In addition to the tax itself, penalties are likely. For careless inaccuracies, the statutory penalty range is up to 30% of the tax due. In practice, where the taxpayer cooperates and the error is disclosed, penalties are often lower — commonly around 10–15%.

Interest would also be payable on the late-paid tax: HMRC charges interest automatically on underpaid liabilities, calculated from the original due date, and in this case it would come to about £27,000 – the calculation is below.

There is then a wider question. If Quidnet failed to withhold tax because it didn’t understand the nature of REIT distributions, and the Tisun companies failed to pay tax on those distributions for the same reason… what other errors were made? In particular, did Mr Tice’s offshore trust pay any tax at all on its distributions? It certainly should have done – but the errors we have found make us wonder if in fact it did.

Richard Tice’s response

The Sunday Times wrote to Mr Tice on Thursday. We wrote on Friday:

We didn’t receive a response; neither did The Sunday Times.

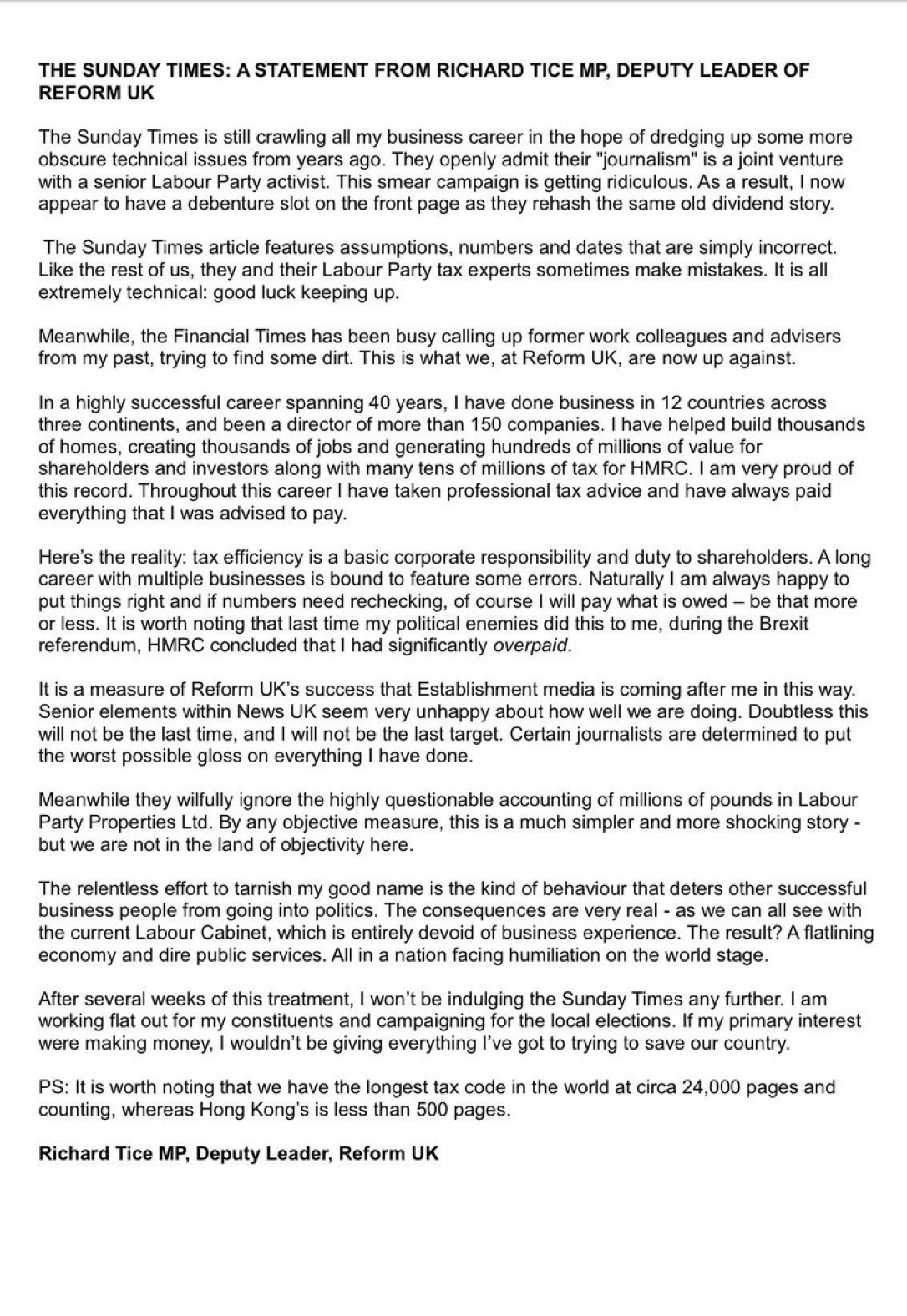

Shortly after publication of this report, Mr Tice published a statement. It does not deny any element of our reporting:

Methodology – determining the taxable profit

We calculate the £513,901 figure by:

identifying the REIT distributions (PIDs) declared by Quidnet

matching them to Tisun shareholdings

reconciling against the filed accounts

The first step was to reconcile the dividend income shown in the Tisun accounts against the dividends we know Quidnet REIT declared, and the shareholdings recorded in Companies House filings.

Quidnet’s own accounts explicitly disclose the PID per share for each financial year. The table below sets out, for each year, the total PID per share, the individual dividends that make it up, and the treatment we have adopted:

Financial year

Total PID per share

Individual dividends making up the total

Notes / treatment

FY2019

12.75p

12.75p FY2019 final dividend, paid March 2020.

100% PID.

FY2020

10.43p (weighted annual average)

5.00p H1 interim (paid September 2020 as scrip) + 6.00p FY2020 final (paid April 2021).

100% PID. The 10.43p figure ≈ total FY2020 dividends (£682,432) ÷ year-end shares (6,542,911). The 2020 dividends were paid as scrip — shares in Quidnet rather than cash — but the corporation tax treatment of scrip dividends for a REIT is the same as for a normal company, i.e. identical to cash dividends.

FY2021

6.99p (of which 5.50p H1 interim + 1.49p “REIT-period” slice of the final)

5.50p H1 interim (paid August 2021); 5.30p FY2021 final declared 10 May 2022 for the period 1 July – 31 December 2021.

Quidnet ceased to be a REIT on 9 August 2021. The full 5.50p H1 interim was declared while Quidnet was still a REIT and so we treat it as 100% PID. Of the 5.30p final, only 1.49p qualifies as PID (covering the pre-9 August 2021 part of the post-H1 period); the remaining 3.81p is a post-REIT ordinary dividend and is not PID.

FY2022 onwards

0.00p

—

No PIDs after the REIT period ended.

We can cross-check these figures against the Tisun accounts. For Tisun One, the FY2019 final (£63,028) plus the H1 2020 interim (£26,665) totals £89,693 — the accounts show £89,680 (a trivial difference from scrip share rounding). This gives us high confidence that the PID calculations are correct.

There are, however, three anomalies that affect all the other accounts:

Anomaly 1: the dividends that didn’t exist

As we have reported, in 2020, all of the REIT distributions were paid in shares, not cash. According to Quidnet’s Companies House filings, those shares remained owned by the four Tisun companies. Yet the four sets of accounts show dividends being paid up to their parent company, Tisun Investments. There was no cash to fund those dividends, and no capital raising or increase in creditors to fund a cash dividend.

We don’t think this can be correct, but it’s not clear what happened. However, this does not change our calculations – the tax position is unaffected by whether the four Tisun companies in fact retained the shares or paid them as a dividend to Tisun Investments.

Anomaly 2: the FY2021 ~3.5% shortfall in Tisun One, Two and Three

For the year ended 31 December 2021, each of Tisun One, Two and Three booked dividend income of roughly £2,300 less than the per-dividend, per-share calculation implies. The shortfall is consistent in size (about 3.5%) and consistent in direction (accounts are lower than the calculated figure) across all three companies.

The per-dividend calculation for 2021 is simply the FY2020 final dividend (6.00p PID) plus the H1 2021 interim dividend (5.50p PID), each multiplied by the relevant Tisun shareholding at the record date:

Company

Quidnet shares

FY2020 final 6.00p × shares

H1 2021 interim 5.50p × shares

Calculated 2021 total

Per filed accounts

Shortfall (£)

Shortfall (%)

Tisun One

550,494

£33,030

£30,277

£63,307

£61,029

£2,278

3.6%

Tisun Two

549,383

£32,963

£30,216

£63,179

£60,906

£2,273

3.6%

Tisun Three

549,383

£32,963

£30,216

£63,179

£60,906

£2,273

3.6%

Total

£98,956

£90,709

£189,665

£182,841

£6,824

3.6%

The shareholdings are taken from the Quidnet confirmation statements on file at Companies House. The PID rates are the figures Quidnet discloses in its own 2020 and 2021 accounts: a 10.43p annual PID for FY2020 (broadly equal to the 5p H1 interim plus the 6p FY2020 final — we have treated it as 6p for the final on the basis of the stated per-dividend rates) and a 5.5p interim for H1 2021.

We cannot explain the ~3.6% shortfall. It is consistent in percentage terms across three separately-filed sets of accounts in one year; it could be some kind of intentional methodology but it seems more likely to be a calculation error.

In any event, for the purposes of the corporation tax calculation we will use the amounts Quidnet actually paid, per Quidnet’s audited accounts and the confirmation-statement shareholdings.

The effect is to increase our calculation of the Tisun companies’ taxable PID income by about £6,800 in aggregate, or about £1,300 of corporation tax at 19%.

Anomaly 3: Tisun Four’s dividend that didn’t exist

Tisun Four was incorporated on 11 September 2020 and subscribed for 238,233 Quidnet shares on 21 September 2020. Both dates are after the record date for Quidnet’s H1 2020 interim dividend, so ordinarily Tisun Four should not have received any part of the H1 2020 dividend, only the FY 2020 final dividend (paid in 2021) and then the H1 2021 interim dividend (paid later in 2021).

Tisun Four’s accounts for its first period (11 September 2020 to 31 December 2021) record total dividend income of £37,951. The comparative column in its 2022 accounts splits that 2021 income between a “Final paid” figure of £24,848 for 2020 and an “Interim paid” figure for 2021 of £13,103.

We can reconcile the “interim 2021” figure exactly:

Line in Tisun Four accounts

Amount Booked in Tisun Four’s accounts

Reconciles to line in Quidnet’s accounts

Calculation based on Quidnet accounts and Tisun Four’s holding

Match?

Interim 2021 paid

£13,103

H1 2021 interim @ 5.50p

5.50p × 238,233 = £13,103

Exact

However we cannot reconcile the £24,848 “final 2020” figure against Tisun Four’s actual legal entitlement to dividends in 2020:

Line in Tisun Four accounts

Amount Booked in Tisun Four’s accounts

Reconciles to line in Quidnet’s accounts

Calculation based on Quidnet accounts and Tisun Four’s holding

Match?

Final paid — the 6.00p paid when Tisun Four was shareholder

£24,848

FY2020 final @ 6.00p

6.00p × 238,233 = £14,294

Does not match booked figure

The £24,848 only reconciles against all Quidnet REIT’s 2020 dividends – which is wrong, because Tisun Four shouldn’t have been entitled to the 2020 interim dividend, as it wasn’t a shareholder on the record date.

Line in Tisun Four accounts

Amount Booked in Tisun Four’s accounts

Reconciles to line in Quidnet’s accounts

Calculation based on Quidnet accounts and Tisun Four’s holding

Match?

Final paid (2021 comparative) — as booked

£24,848

Full FY2020 annual PID @ 10.43p

10.43p × 238,233 = £24,848

Exact

This cannot be correct, not least because Quidnet’s 2020 accounts (the statement of changes in equity in particular) only reconciles if the 2020 interim dividend was not paid to Tisun Four.

We will again resolve this by following the Quidnet audited accounts, not the Tisun Four accounts. That has the effect of reducing Tisun Four’s taxable PID income by £10,554, i.e. reducing the tax underpayment by £2,005.

Net effect on the corporation tax calculation

Anomalies 2 and 3 pull in opposite directions but the headline number is unchanged:

Adjustment

PID income

CT at 19%

Tisun One/Two/Three FY2021 shortfall (added back to match Quidnet-paid PID)

+£6,824

+£1,297

Tisun Four H1 2020 excess (removed to match Quidnet)

(£10,554)

(£2,005)

Total adjustment vs. booked accounts

(£3,730)

(£708)

The full reconciliation

Adjusting for the anomalies, and using the Quidnet audited accounts PID rates and the known shareholdings at each dividend record date, we can calculate the PIDs received by each Tisun company:

Dividend

Tisun One

Tisun Two

Tisun Three

Tisun Four

Total

FY2019 final (12.75p PID)

£63,028

£62,900

£62,900

£188,828

H1 2020 interim (5.00p PID)

£26,665

£26,611

£26,611

£79,887

FY2020 final (6.00p PID)

£33,030

£32,963

£32,963

£14,294

£113,250

H1 2021 interim (5.50p PID)

£30,277

£30,216

£30,216

£13,103

£103,812

FY2021 final (1.49p PID)

£8,202

£8,186

£8,186

£3,550

£28,124

Total PIDs

£161,202

£160,876

£160,876

£30,947

£513,901

The FY2019 final and (subject to anomaly 3) the H1 2020 interim dividends pre-date Tisun Four’s existence – it was incorporated in September 2020. The later dividends were received by all four companies.

This produces total taxable income of £513,901. The corporation tax rate at the time was 19%, and so the unpaid tax was £97,641.

Methodology – group relief

The Tisun group from 20 November 2020

At the time of the later REIT payments, the Tisun companies were in a small group. This diagram shows the group, and the other Quidnet REIT shareholders:

Tisun / Quidnet group structure as at 1 July 2021

From Richard Tice to Tisun Holdco (Label: 77.1%)

From Richard Tice to Tisun Holdco (Label: 22.9%)

From Tisun Holdco to Tisun Investments (Label: 100%)

From Tisun Investments to Tisun One (Label: 100%)

From Tisun Investments to Tisun Two (Label: 100%)

From Tisun Investments to Tisun Three (Label: 100%)

From Tisun Investments to Tisun Four (Label: 100%)

From Richard Tice (direct) to Quidnet REIT (Label: 13.00%)

From RJS Tice Family Settlement to Quidnet REIT (Label: 16.88%)

From RJS Tice Family SIPP to Quidnet REIT (Label: 34.98%)

From Tisun One to Quidnet REIT (Label: 7.80%)

From Tisun Two to Quidnet REIT (Label: 7.78%)

From Tisun Three to Quidnet REIT (Label: 7.78%)

From Tisun Four to Quidnet REIT (Label: 3.38%)

From Huntress (CI) Nominees to Quidnet REIT (Label: 4.42%)

From NJG Tribe SIPP to Quidnet REIT (Label: 2.99%)

From Employees to Quidnet REIT (Label: 0.98%)

A company in a group can use “group relief” to utilise another group member’s tax trading losses, property business losses, and losses on certain financial and other types of assets, but not losses on capital assets.

There are, furthermore, stringent conditions for companies to be in a group relief group. There has to be a 75% common corporate shareholding (i.e. not via an individual owner). So the only possible companies that could have generated losses for the four Tisun companies are those in this diagram, and not other companies held separately by Mr Tice.12

Tisun Holdco never had any material assets or liabilities other than its shareholding in Tisun Investments.13 That leaves Tisun Investments Ltd as the only entity that could in principle have had losses that the four Tisun companies could have used. Tisun Investments’ accounts for 202014, 2021 and 2022, show that it did have sizeable accounting losses every year. However the nature of its assets and liabilities mean that we expect almost none of these losses would be recognised for tax purposes.

Tisun Investments Ltd’s assets were:

Two flats in Kent, combined into a single dwelling, in a building where all the other flats are now owned by the Tice family. The value of the dwelling was around £600,000 and at the time in question it was unmortgaged.15 So, whether used by the family or rented out, the property is unlikely to have generated material tax losses, and certainly not the ~£170k/year needed to shelter the Tisun profits.16

A motor vehicle on hire purchase – likely a personal car. The cost of this may be partially allowable for tax purposes, but the amounts are not material (probably £5-15k each year of capital allowances and running costs).

Unlisted investment assets, never more than £120,000. We don’t have any information about what the investments are, but the limited value means that they won’t have justified material management expenses, and any loss on disposal would be a capital loss (which can’t be used to shelter trading profits or property income).

Shareholdings in its subsidiaries – Tisun One, Two, Three and Four, and JMT Holdco. Management expenses incurred wholly and exclusively for the purposes of managing these assets would be tax deductible; but given the passive nature of the companies, it’s difficult to see how that could generate material deductible costs.

Loans to its subsidiaries (Tisun One, Two, Three and Four), and its parent, (Tisun Holdco).17 Loans to connected parties generally generate no deductible debits for the lender (even if impaired or written off). The Tisun subsidiaries’ accounts suggest no interest is charged but, even if it was, the tax deductions for the payer would be matched by taxable income in Tisun Investments. These loans are therefore not a plausible source of net deductible tax losses.

Loans to related parties, with a balance fluctuating between £0.8m and £1.1m. These include loans to Richard Tice personally, to Reform UK, and to other connected parties. The loans are all either interest-free or non-commercial. Non-commercial loans don’t generate deductible losses for the lender, and (again) neither do loans to connected parties.

Its liabilities were:

270,000 preference shares at 7% – treated as debt for accounting purposes but not for tax purposes, so no tax deduction available.

£1,679,712 owed to JMT Corporation, an associated company that’s not part of the group relief group. The loan is interest-free18, so doesn’t generate any losses for Tisun Investments.

Loans from related parties – again, these appear to be non-commercial funding arrangements. Any associated costs would be unlikely to be deductible, and there is no evidence of significant interest expense in the accounts.

We therefore conclude that Tisun Investments Ltd did not generate material losses that could be used to shelter profits elsewhere in the group. It looks like the company’s accountants agreed, as there’s no sign of a deferred tax asset, or any mention of losses or group relief.

It follows that the accounting did not merely misstate a group relief claim as a dividend exemption. There was no group relief in 2021 and 2022.

The Tisun group in 2020

Until 20 November 2020, Tisun Investments and its subsidiaries were part of a much larger group, headed by Sunley Family Holding Ltd.1920

Sunley / Tisun group structure as at 19 November 2020

From Sunley Family Holding to Sunley Family Limited (Label: None)

From Sunley Family Holding to Tisun Investments (Label: None)

From Sunley Family Holding to JMT Corporation (Label: None)