It is a national scandal that teachers, doctors and others earning fairly ordinary salaries can face marginal tax rates of more than 60%, and sometimes approaching 80%. It’s inequitable and holds back growth. Rachel Reeves should commit to ending these anomalies.

This Government was elected on a platform of kickstarting economic growth. It has a large majority, and four or five years until the next election. It’s a rare chance for real pro-growth tax reform. That’s all the more necessary if we are going to see tax rises.

We’ll be presenting a series of tax reform proposals over the coming weeks. This is the fifth – you can see the complete set here.

Marginal rates

The “marginal rate” is the percentage of tax you’ll pay on your next £1 of income. It therefore affects your incentive to earn that £1.1

If you doubt that, imagine that you pay tax at 20% on your £30k income, but the next £1 you earn will be taxed at a marginal rate of 100%. Would you work extra hours for zero after-tax pay? I think most people would not. The overall tax you pay would only be a bit over 20%, but your decision to work more hours is affected by your after-tax pay for those hours.

That seems a silly example (although we can find worse ones in our own tax system – see below). But a marginal rate below 100% will also change your incentives.

Perhaps you are only just managing to afford childcare, and every hour you earn increases your childcare costs? A marginal rate of 70% might mean your take-home pay is less than that childcare cost.

Or it may just be that you value your own time so that, if your take-home pay from working additional hours drops below a certain point, it’s not worth it to you.

Marginal rates – a normal example

In the current, 2024/25 tax year, combined income tax and national insurance rates for an employee look like this:2

- No tax on incomes below the £12,570 personal allowance.

- £12,570 to £50,270 – a combined income tax and employee national insurance rate of 28%

- £50,271 to £125,140 – a combined rate of 42%3

- Above £125,140 – a combined rate of 47%.

It’s important to realise that the different tax brackets only apply to income in that bracket. If you earn £50,271 you’re in the higher tax bracket, but you only pay 42% tax on £1. You still pay 28% tax on everything you earned before above the personal allowance. This is unfortunately not very well understood.

Imagine Bob is an employee earning £12,569. None of his income is taxed. Bob has the opportunity4 to earn an additional £1,000, putting him in the 28% tax bracket.5

There are three ways we could describe Bob’s position after earning that £1,000.

- The applicable headline rate. Bob is a basic rate 28% taxpayer.

- The overall effective tax rate. This is the total tax paid divided by Bob’s income. Total tax paid = £1,000 x 28% = £280. Income = £13,570. So effective tax rate is 280/13570 = about 2%.

- The marginal rate – the percentage tax you’re paying on that new £1,000. This is 280/1000 = 28%.

Each of these has their uses.

The first figure is simple.

The second is useful for assessing how much tax Bob pays overall. If a political party proposed a sweeping set of tax reforms, Bob would be very interested in the impact on his effective rate.

But the third – the marginal rate – is important, because it affects Bob’s incentive to earn the additional pound. Right now it’s the same as the headline rate – but that’s not always the case…

Marginal rates – the problem

Jane is earning £60k and claiming child benefit for three children. That’s worth £3,094.

She’s now in the 42% tax band.6 Jane still pays basic rate tax for her income between £12,570 and £50,270, but now pays 42% tax for everything over that. So her total tax bill is (50270 – 12570) * 28% + (60000-50270) * 42% = £14,643 and Jane takes home £45,357.

Jane is thinking of working a few more hours to earn another £1,000. She’s in the higher tax band – so in a sane world she’d expect another £420 of tax, and a marginal rate of 42%.

But that is not the result. Once Jane’s income hits £60,200, the “High Income Child Benefit Charge” (introduced by George Osborne) starts to apply to claw back her child benefit – 1% for every £200 of earnings.

So that £1,000 of additional earnings costs Jane HICBC of £154.70, on top of the £420 of “normal” tax. A total of £565.

So how do we describe Jane’s position after earning that £1,000?

- The applicable headline rate. Jane is a higher rate 42% taxpayer.

- The overall effective tax rate – the total tax paid divided by Jane’s income. That’s 15207/61000 = about 25%.

- The marginal rate – the tax Jane is paying on that new £1,000. This is 56.5% – and we will have the same result for all incomes between £60k and £80k. 7

As I mentioned at the start, there can be practical reasons for people to turn down work if the marginal tax rate gets too high – but there are also psychological factors. For many people, 50% feels like a high rate.

Charting the effect

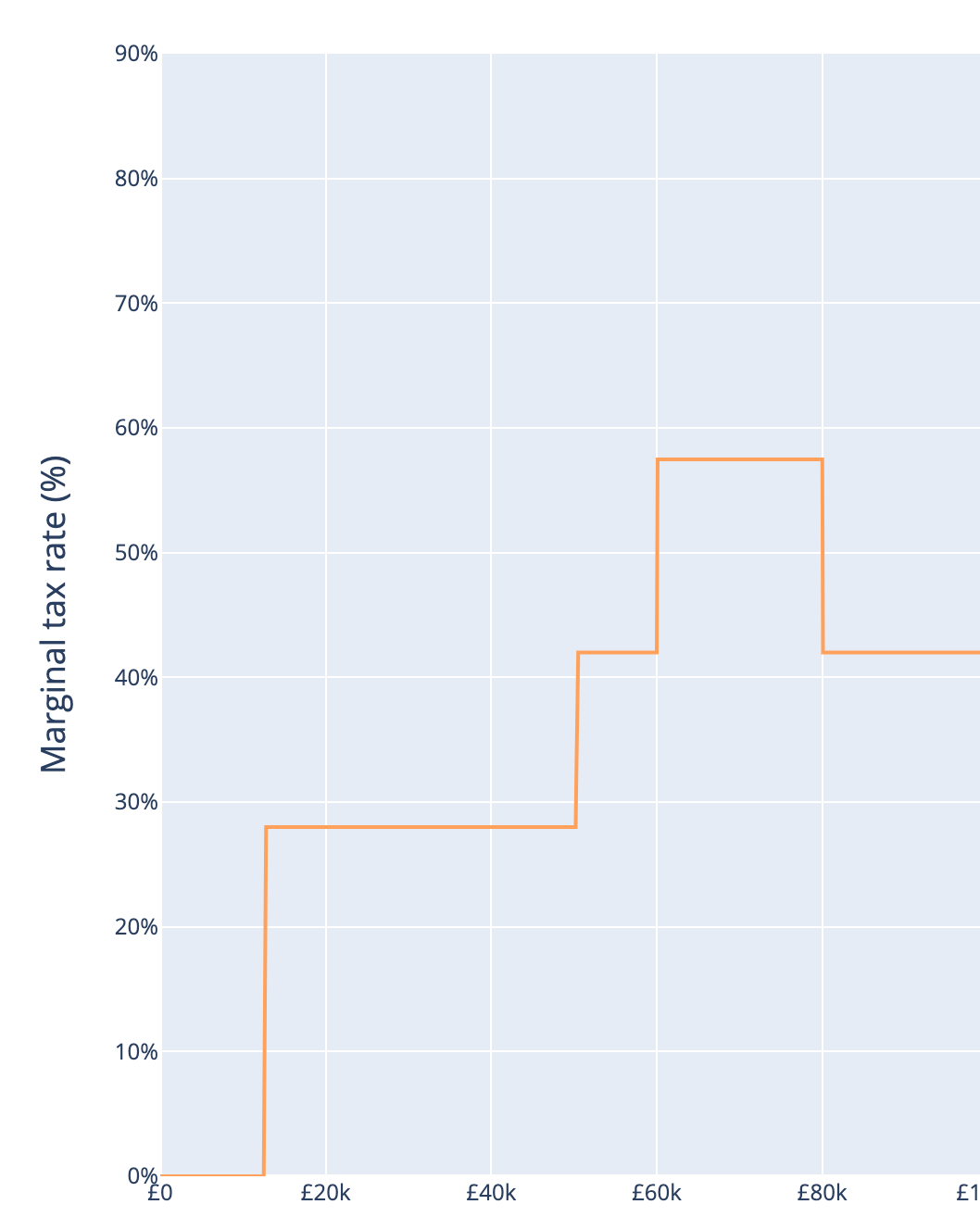

We can chart Jane’s marginal rate for each pound of income she could earn. Incomes along the bottom, marginal rate along the top:

You can see the HICBC as the “tower” between £60k and £80k, which should be a smooth 42% plateau. Instead it hits 57%. (I’m hiding what happens after £100k)

The HICBC is a gimmick which enabled George Osborne to somewhat-surreptitiously raise tax on people on high incomes without raising the tax rate itself.

It’s a really bad policy:

- It means that Jane pays a higher marginal rate rate than someone earning £90k, or indeed £900k. Where’s the logic in that?

- The way in which HICBC works creates a nasty trap for the unwary, with thousands of people accidentally incurring HMRC penalties.

The politics are nice and intuitive – surely it’s not right for people on high incomes to receive child benefit? But the reality is that this logic inexorably leads to a high marginal rate, and a cumbersome and sometimes unjust collection mechanism.

Can it get worse?

Very much worse.

George Osborne’s HICBC was copying a trick invented by Gordon Brown to clawback the personal allowance for people earning £100k.

Again, the politics are nice, but the consequences are a mess.

If Jane starts earning between £100k and £125k then she faces a marginal tax rate of 62%. It then drops to 47% from £125k. Her marginal rate chart looks like this:

Needless to say, 62% is a very high rate.

The graduate tax

And if Jane has a student loan, that will add on 9% to the marginal rate, meaning that her marginal rate chart now looks like this:

The student loan system behaves like a crude graduate tax so that, between £100k and £125k, Jane’s marginal rate reaches 71%.

The anomalous marginal rates

Student loan repayments, personal allowance tapering and child benefit clawback all result in high marginal rates. But the rates are at least within “normal” bounds – they don’t exceed 100%.

There are points at which the marginal rate sails way over 100%, meaning that you are actually worse off after a pay rise. This occurs when tax benefits/allowances have a “cliff edge” after which they disappear completely:

- The £1,000 personal savings allowance drops to £500 once you hit the higher rate band, and to zero once you hit the additional rate band.8

- The marriage allowance lets a non-working spouse transfer £1,260 of their unused personal allowance to their partner, if they’re earning less than the £50,270 higher rate threshold. So it’s worth £252 – and it disappears once the higher rate band is hit.

These are irrational rules, but the tax at stake is small, and so the high marginal rate is limited to a small range of incomes. The significance is limited.

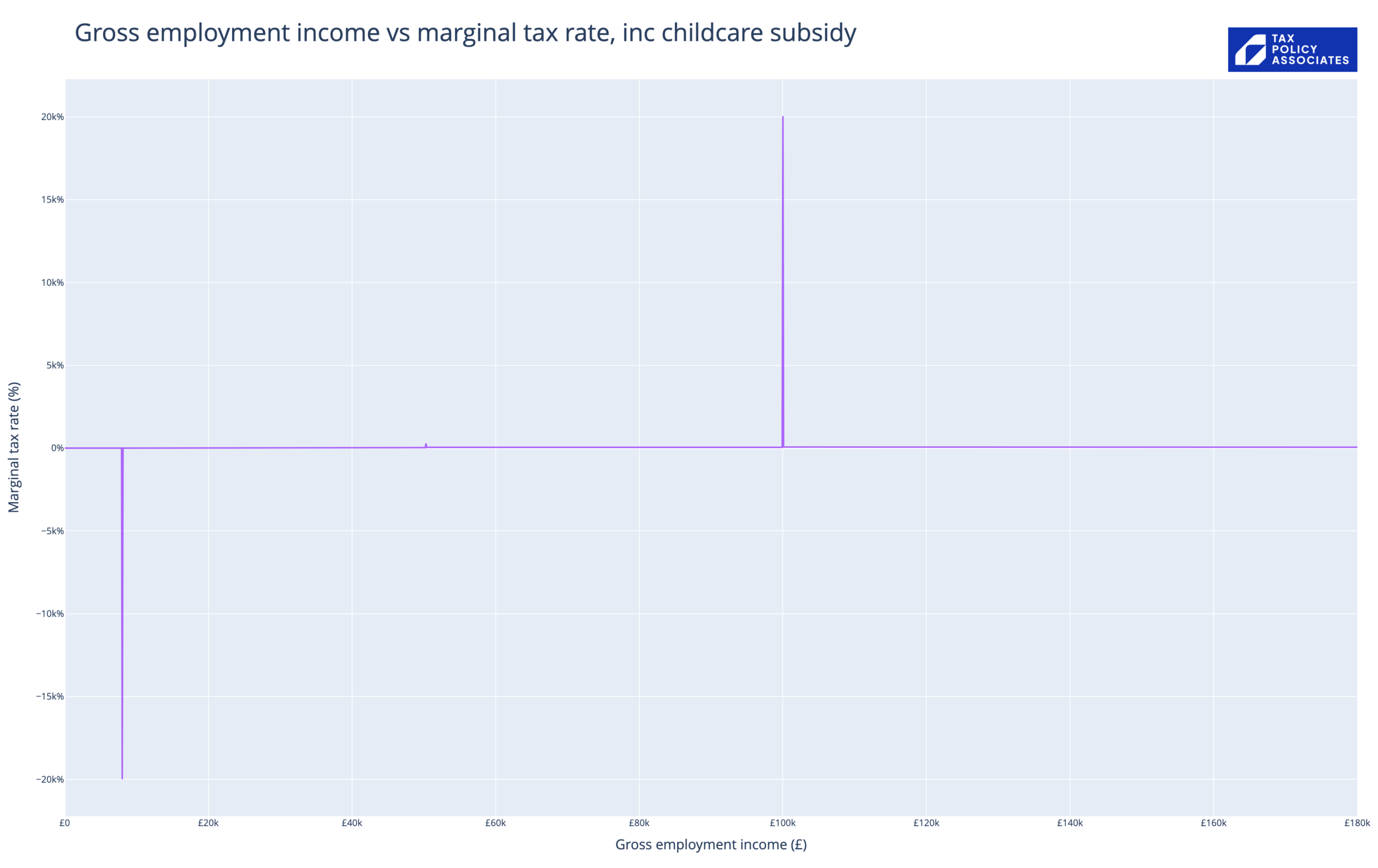

A much more significant cliff-edge effect results from the childcare schemes created by the previous Government. These provide generous subsidies that are removed suddenly when your wage hits £100,000. That creates a marginal rate that is truly anomalous – so high it is hard to calculate.

The childcare support scheme for parents with children under 3 could be worth £10,000 per child for parents living in London. And it vanishes once one parent’s earnings hit £100k. Here’s what that does to the marginal tax rate:9

The 20,000% spike at £100,000 is absolutely not a joke – someone earning £99,999.99 with two children under three in London will lose an immediate £20k if they earn a penny more.10 And the negative spike at £8,668 is because it’s at that point you qualify for the scheme – you have a huge negative marginal tax rate (which has the potential to create obvious distortions of its own).

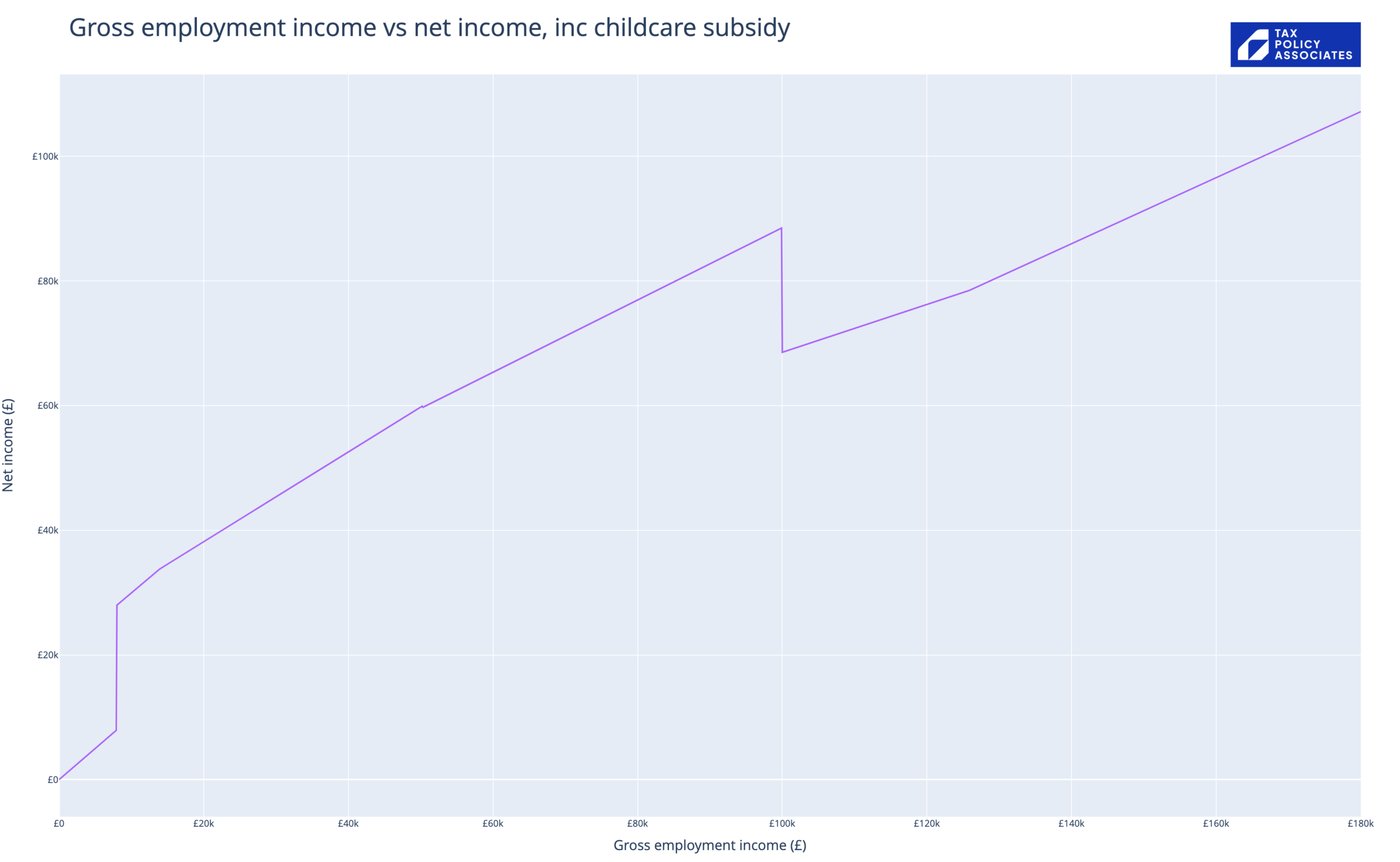

The practical effect is clearer if we plot gross vs net income:

After-tax income drops calamitously at £100k, and doesn’t recover to where it was until the gross salary hits £145k.

This is ignoring the pre-existing tax-free childcare scheme, which also vanishes at £100k. The amounts are less (usually under c£7k/child) so the curve would look less dramatic. However, as the scheme applies to children under 11, taxpayers feel these effects for many more years.

Marginal rates for high earners

If Jane started earning beyond £145k, all of these problems go away, and she has a nice straightforward marginal rate of 47% forever.11

What kind of tax system creates complexities and high marginal rates for people earning £60-125k, and simplicity and lower marginal rates for people earning more than £125k?

The complete picture

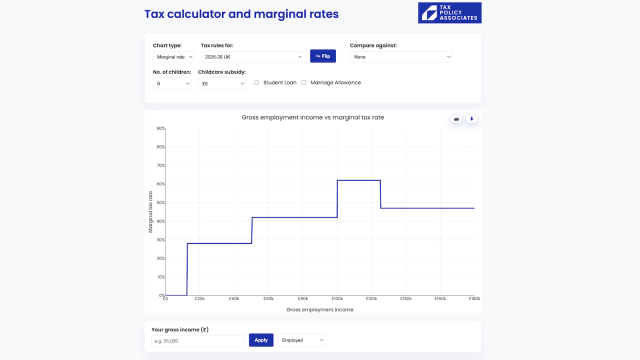

Here’s an interactive chart showing all the UK and Scottish marginal rates. You can click on the legend at the bottom to see the effect of child benefit clawback and student loans. Or you can view in fullscreen here.12

You’ll see that if you are a recent graduate living in Scotland with three children under 18, between £100k and £125k you face a marginal rate of 78.5%.13

The chart doesn’t include marriage allowance, childcare subsidies and the other extremely anomalous marginal rates, as the rates are so high that they make the chart unreadable.

The effect

We’ve received many reports saying that high marginal rates affecting senior doctors/consultants are an important factor in the NHS’s current staffing problems – exacerbated by the fact that the starting salary for a full time consultant is just under £100,000.

But it’s important not to just focus on the impact on jobs that we might think are of particular societal importance.

It’s also problematic if an accountant, estate agent or telephone sanitiser turns away work because of high marginal rates – it represents lost economic growth and lost tax revenue.14 It also makes people miserable.

Sometimes people take the work, but use salary sacrifice or additional pension contributions so their taxable income doesn’t hit the threshold. But that doesn’t work for everyone; sometimes they’ve hit the pensions allowance; sometimes it doesn’t always make sense to work harder now, for money that they can’t touch for years.

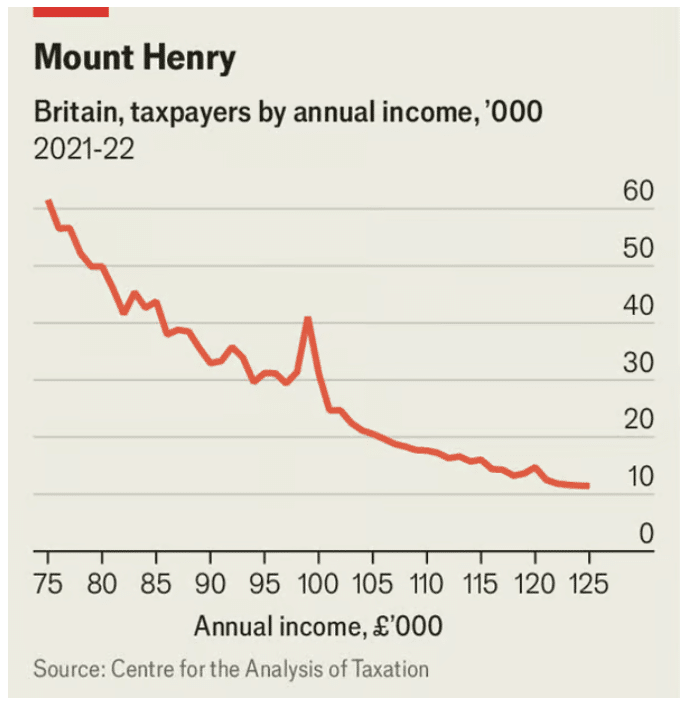

We can see the effect in this chart from the Economist, based on data from the Centre for the Analysis of Taxation:

That cliff at the £100k point is people holding back their earnings so they don’t hit the £100k marginal rates. That represents a loss of working hours to the public and private sectors and a macroeconomic impact on the UK as a whole. Quite how large an impact is an interesting question, which I hope someone looks at.

What’s the solution?

These problems are getting worse over time, as fiscal drag takes more and more people into the thresholds that trigger these high marginal rates.

When Gordon Brown introduced the personal allowance taper in 2009, only 2% of taxpayers earned £100,000; by 2025/26 over 5% of taxpayers will. When George Osborne introduced child benefit clawback a year later, only 8% if taxpayers earned £50,000; by 2025/26 over 20% of taxpayers will (which is likely what motivated Jeremy Hunt to increase the threshold to £60,000).15

This creates a double problem. First, the economic distortions created by the high marginal rates start to impact into mainstream occupations (doctors, teachers). Second, the revenues raised by the marginal rates are now so great that they become hard to repeal.

Ending the high marginal rates in one Budget is, therefore, not realistic – particularly in the current fiscal environment. The cost of making child benefit, the personal allowance, and childcare subsidies universal, would be expensive (somewhere between £5-10bn, depending on your assumptions). The obvious way of funding this – increasing income tax on high earners, appears to have been ruled out.

We would suggest four modest steps:

- An acknowledgment that the top marginal rates are damagingly high, and that the Government will take steps to reduce them when economic circumstances permit.

- Some immediate easing of the worst effects, at minimal cost to the Exchequer, for example by smoothing out the personal allowance taper over a longer stretch of income, therefore reducing the top marginal rate.

- A commitment to uprate the thresholds for the HICBC, personal allowance clawback and childcare subsidy in line with earnings growth.

- A commitment that no steps will be taken to make the high marginal rates worse, or create new ones.

- A new rule that Budgets will be accompanied by an OBS scoring of the highest income tax marginal rates before and after the budget.

There’s a coherent political case for people on high incomes paying higher tax (whether we agree with it or not). There is no coherent case for people earning £60k, or £100k, to pay a higher marginal rate than someone earning £1m. It’s inequitable and economically damaging. Ms Reeves should call time on high marginal rates.

Graphic by DALL-E 3⚠️: “A businesswoman climbing a set of stairs labeled with different tax percentages, with the middle step showing 100% and the others smaller %s, representing the different marginal tax rates. Widescreen. Cinematic.”

Footnotes

Everything interesting happens at the margin. For more on why that is, and some international context, there’s a fascinating paper by the Tax Foundation here. ↩︎

Ignoring Scotland for the moment; we’ll get to the Scottish rates later. ↩︎

That’s the headline rate – the actual rate is different… for which see further below. ↩︎

Perhaps he is self-employed and chooses which clients/work he takes on. Perhaps he is employed, and can choose how much overtime to work, or whether to accept a promotion. Perhaps he is going back to work after time spent looking after young children. Many people have the ability to work additional hours if they wish. ↩︎

Strictly that doesn’t exist – you’re paying basic rate tax plus Class 1 employee national insurance contributions. But realistically this amounts to 28% tax. I’m going to count income tax and national insurance as if they’re one tax throughout this article. ↩︎

Strictly that doesn’t exist – she’s paying 40% higher rate tax plus 2% Class 1 employee national insurance contributions. Realistically this is 42% tax. ↩︎

Note that the marginal rate will vary depending on how we calculate it, and the size of the “perturbation” we calculate the marginal rate over. Most textbooks define the marginal rate as the % tax on the next pound/dollar of income. Say that we looked at the tax Jane paid on £60,199 of income – that would be £14,726. A £1 pay rise takes her to £60,200, and tips her into the HICBC – she now pays £0.42 more higher rate tax, plus an additional HICBC charge of 1% of your child benefit – £30.94 (assuming you have three kids). So the marginal rate is 100 * (£31.63/£1) = 3,163%. This is not very meaningful, as nobody’s incentives are going to be affected by the consequence of a £1 pay rise. It also creates the silly result that the marginal rate on her next £1 pay rise will be 42%, because the HICBC won’t increase until she gets to £60,400. So it’s better to use a more realistic figure like £1,000. The practical consequence is that the 56.5% figure isn’t *the* correct answer, but it’s a sensible and useful one, and it’s important to check that weird marginal rates aren’t just an artifact of the chosen perturbation. Our charting code uses a £100 perturbation for convenience, but then “smooths” the HICBC formula so the marginal rate doesn’t leap up and down. ↩︎

The £5,000 starting rate for savings tapers out, but slowly, and so it just somewhat increases the marginal rate – it’s also less relevant for most people. ↩︎

The chart is for a single earner, but if they have a partner, the partner would also need to be earning at least £8,668 (the national minimum wage for 16 hours a week) ↩︎

The 20,000% figure is a consequence of the code that produces the chart incrementing the gross salary by £100 in each step. It would be a mere 2,000% if we used the same £1,000 perturbation as above. Two million percent if we used the conventional £1 perturbation. Or two hundred million percent if we looked at the one penny increase. ↩︎

Ignoring pensions, which create a marginal rate problem all of their own… ↩︎

Note that the gap between the Scottish and UK marginal rates is much higher than the gap between statutory rates. The HICBC and personal allowance tapers have a bigger effect on higher rates, and so magnify the difference. ↩︎

Particularly when the economy is running at very little spare capacity; it would be different if there was high unemployment/plenty of spare capacity, because the work that was turned away would (at least in theory, in the long term) be undertaken by others ↩︎

Data from the HMRC percentile stats, uprated for post-2022 inflation. ↩︎

The Scottish Budget – four thoughts on a tiny tax cut

The Budget 2025 tax calculator

How to stop IHT avoidance but protect farmers

The Budget – a missed opportunity

How to reform HMRC penalties for people on low incomes

Leave a Reply