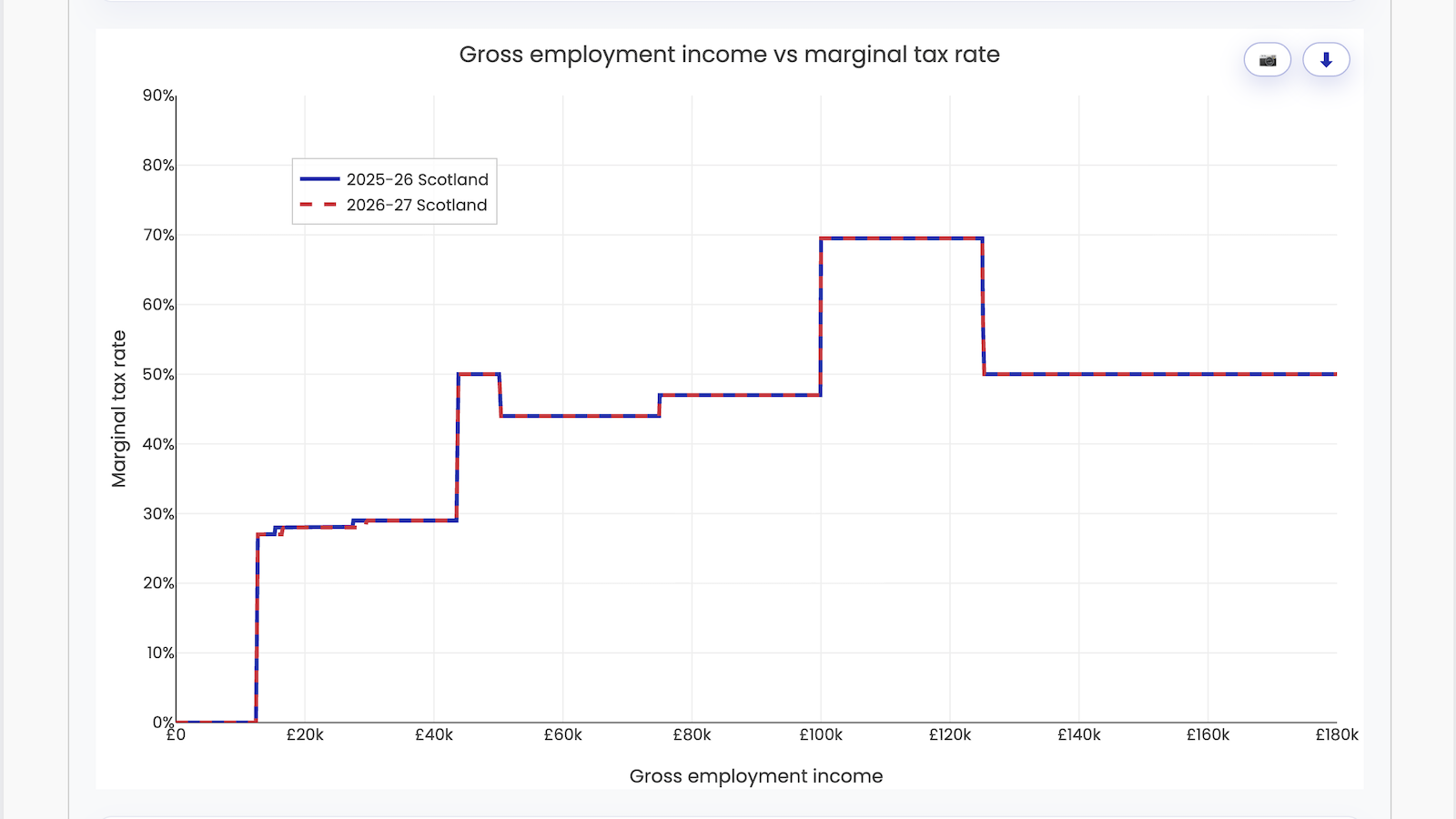

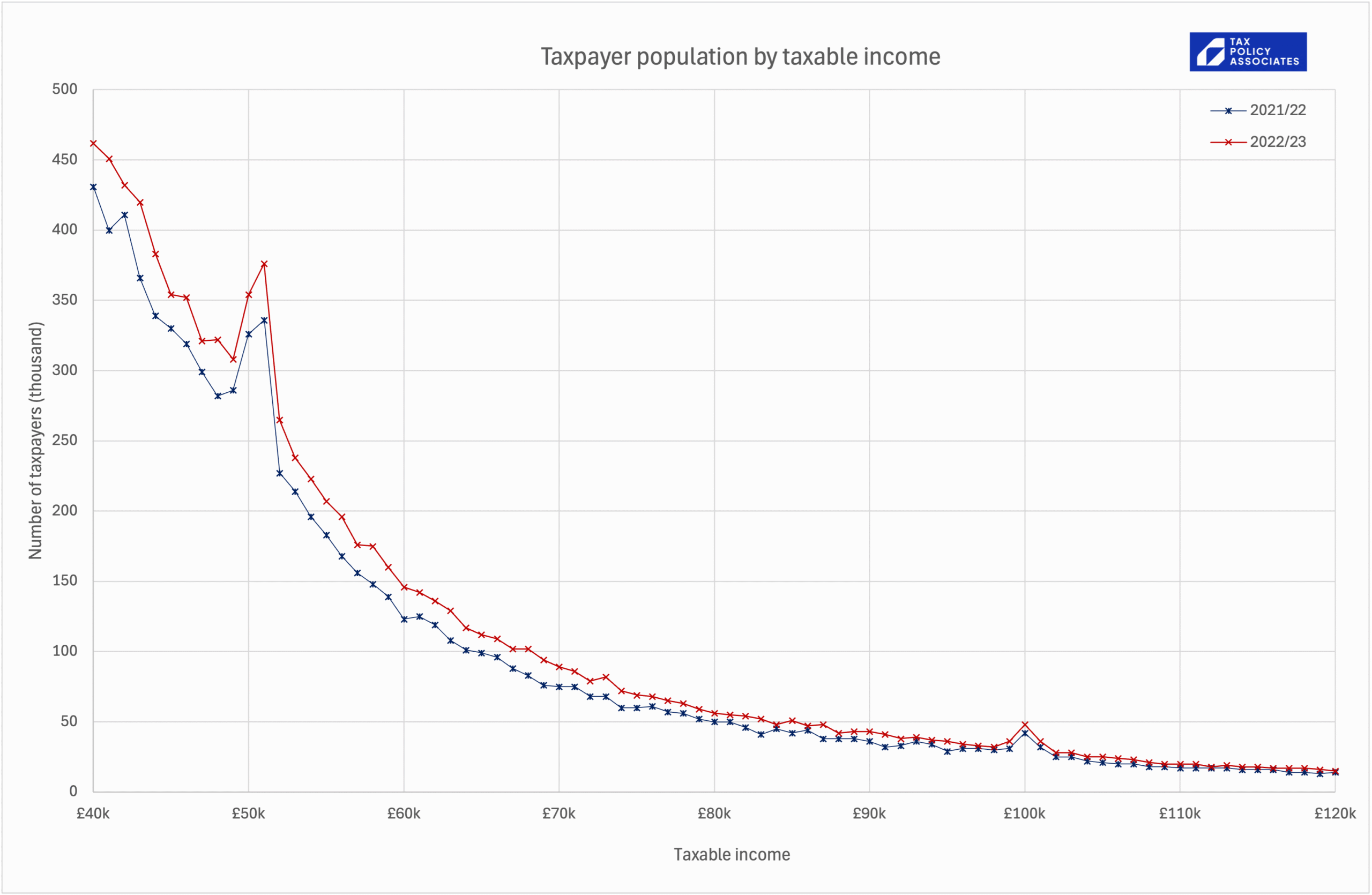

This interactive chart lets you see the current rUK and Scottish marginal tax rates for 2023/24 and 2024/25, with/without child benefit and student loans. You can turn on/off different years and options by clicking on the legend below the chart. Some of these charts won’t work well on mobile; you can see static versions here.

This interactive chart plots the same data, but gross income vs net income:

Finally, this chart again plots gross vs net income, but adds in the effect of the marriage allowance and a £20k childcare subsidy:

Income tax/NI as for tax year 2023/24 and 2024/25 in the UK and Scotland (but applying the September 2023 national insurance change as if it applied for the whole of 23/24)

One earner in a household, who is over 21 and not an apprentice, not a veteran, and under the state pension age

Ignores benefits aside from child benefit (although benefits are notorious for creating very high marginal rates – not, however, an area where I and our team have expertise). Child benefit assumes three children (you can freely change that in the code).

Doesn’t include tapering of pensions annual allowance (starting at £240k)

Do please send us any corrections, additions or comments.

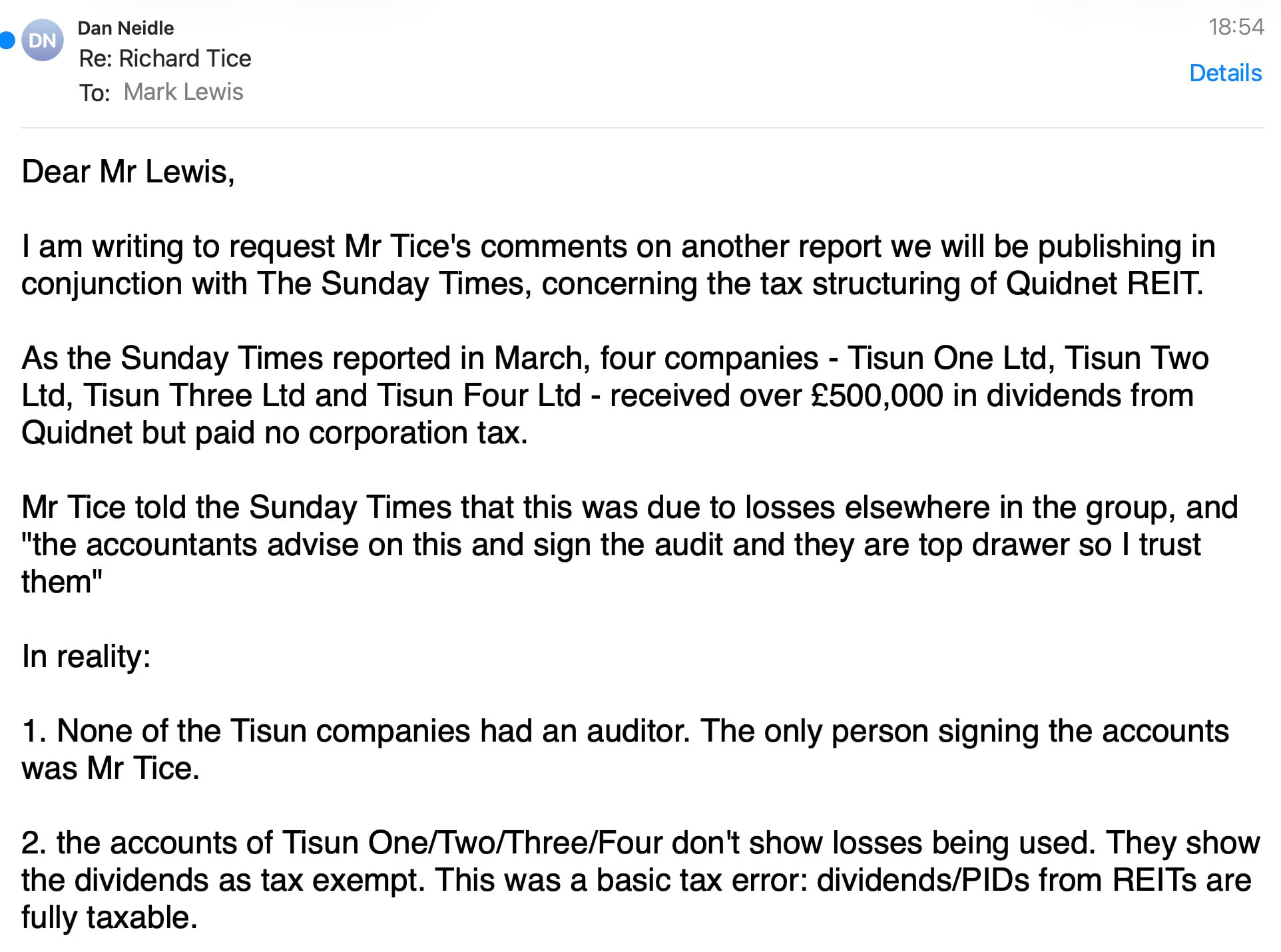

Richard Tice, the deputy leader of Reform UK, used his Quidnet property company’s REIT status to save tax. That meant Quidnet itself paid no corporation tax on its property business – but the quid pro quo was that its corporate shareholders had to pay tax on the dividends they received. They did not. Instead, Mr Tice signed accounts wrongly claiming that the dividends – £514,000 in total – were tax exempt. The result: they failed to pay £98,000 of corporation tax.

This is a different issue from our previous report, which found that Quidnet REIT failed to withhold about £120,000 of tax on distributions to Mr Tice and his offshore trust. But it arises from the same underlying mistake: claiming the tax benefits of a REIT but ignoring the tax liabilities.

Diagram connections

Diagram connections

From Quidnet REIT to Tice companies (Label: £514k dividend)

From Quidnet REIT to Tice companies (Label: £514k dividend)

Key points:

Quidnet REIT paid about £514,000 of property income distributions to four companies: Tisun One, Tisun Two, Tisun Three and Tisun Four.

Quidnet REIT paid no corporation tax on this income, because it was a REIT. The four Tisun companies were supposed to pay tax instead — but they didn’t.

The payments were wrongly treated in the accounts as tax-exempt ordinary dividends. In fact they were taxable REIT property income distributions.

The result was about £98,000 of unpaid corporation tax.

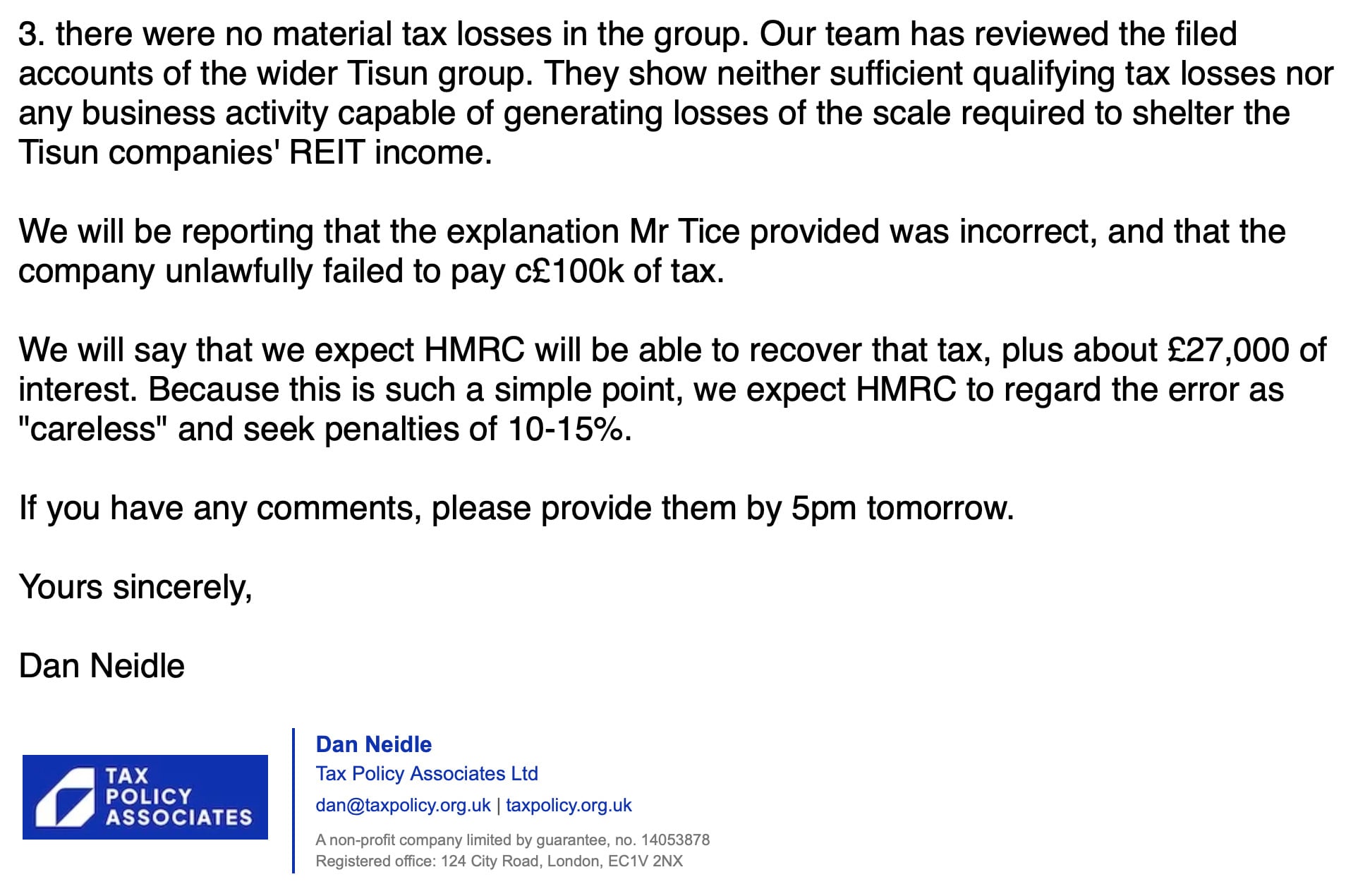

Mr Tice has previously said the lack of tax was due to losses elsewhere in the group. The accounts contradict that, and our analysis finds there were insufficient losses in the group to eliminate the tax.

HMRC should be able to assess the tax, plus roughly £27,000 of interest and penalties likely in the region of 10–15%.

These are basic errors. That raises a further question: what else went wrong? In particular, did Mr Tice’s offshore trust also fail to pay tax on the distributions it received from the REIT?

Mr Tice did not respond to requests for comment from us or The Sunday Times.

Technical terms in this article

Real Estate Investment Trust (REIT)

A UK company that elects into a special tax regime for property investment. Broadly, the REIT does not pay corporation tax on its qualifying property rental business; the tax point is shifted to investors.

A distribution paid by a REIT out of its property rental business profits or gains. Unlike an ordinary dividend, a PID is generally taxable in the hands of the investor.

Tax deducted by the payer before money is paid out. In the REIT context, PIDs are generally paid under deduction of income tax at the basic rate unless an exception applies.

A normal company dividend. For most UK corporate recipients, ordinary dividends are generally exempt from corporation tax. That is different from a REIT PID.

The main UK tax on company profits. In this article, the key point is that UK companies receiving REIT PIDs are generally taxed on them as property business income.

A UK tax relief allowing certain losses of one company to be surrendered to another company in the same 75% group. It is often used to offset one company’s profits with another’s losses.

Where companies are only in the same group for part of an accounting period, group relief is limited to the period of common ownership. The relevant shared period is called the overlapping period.

A note in a company’s accounts showing how you get from the accounting profit to the tax charge. It can reveal whether a company says tax was reduced by dividends, losses, group relief or something else.

A digital filing format for accounts and tax documents. It looks like an ordinary document on screen, but has machine-readable tags embedded in it so software and regulators can identify what each figure means.

From 10 September 2018 to 9 August 2021, Quidnet was a REIT: a form of tax-exempt investment fund that invests in real estate. The consequence is that the company becomes exempt from corporation tax on its property rental business, but its investors are (broadly speaking) taxed as if they held the real estate directly.1

Quidnet REIT direct shareholders as at 1 July 2021

From Richard Tice (direct) to Quidnet REIT (Label: 13.00%)

From RJS Tice Family Settlement to Quidnet REIT (Label: 16.88%)

From RJS Tice Family SIPP to Quidnet REIT (Label: 34.98%)

From Tisun One to Quidnet REIT (Label: 7.80%)

From Tisun Two to Quidnet REIT (Label: 7.78%)

From Tisun Three to Quidnet REIT (Label: 7.78%)

From Tisun Four to Quidnet REIT (Label: 3.38%)

From Huntress (CI) Nominees to Quidnet REIT (Label: 4.42%)

From NJG Tribe SIPP to Quidnet REIT (Label: 2.99%)

From Employees to Quidnet REIT (Label: 0.98%)

Quidnet REIT correctly paid no tax on its property income. But that shifted the burden elsewhere.

It had to withhold tax on dividends it paid out of that income to Richard Tice and his offshore trust – “property income distributions”. As we’ve previously reported, it didn’t do that. Quidnet mistakenly treated the dividends as ordinary dividends and failed to withhold about £120,000.

This report is about another, potentially more serious, error. Quidnet’s UK corporate shareholders had to pay tax on their dividends. They did not – they treated them as tax-exempt.2

There were four corporate shareholders:3 Tisun One Ltd, Tisun Two Ltd, Tisun Three Ltd and Tisun Four Ltd. The sole director of all four companies was Richard Tice.

Quidnet REIT made about £514,000 of payments to the four Tisun companies.4 None of them ever paid tax.

The consequences are straightforward: HMRC can recover the tax, with interest and penalties. We return to this below.

Richard Tice’s original explanation

The Sunday Times asked Mr Tice why none of the four Tisun companies ever paid any corporation tax. Mr Tice told The Sunday Times that this was because of “wider losses suffered by the group”:

These statements were incorrect:

The accounts do not show losses being used.

There were in fact no tax losses in the group.

The front page of the accounts shows that the Tisun companies had no auditor – the only person who signed the accounts was Mr Tice:

The accounts don’t show loss utilisation

What the Tisun companies’ accounts actually show is an incorrect claim for a dividend exemption.

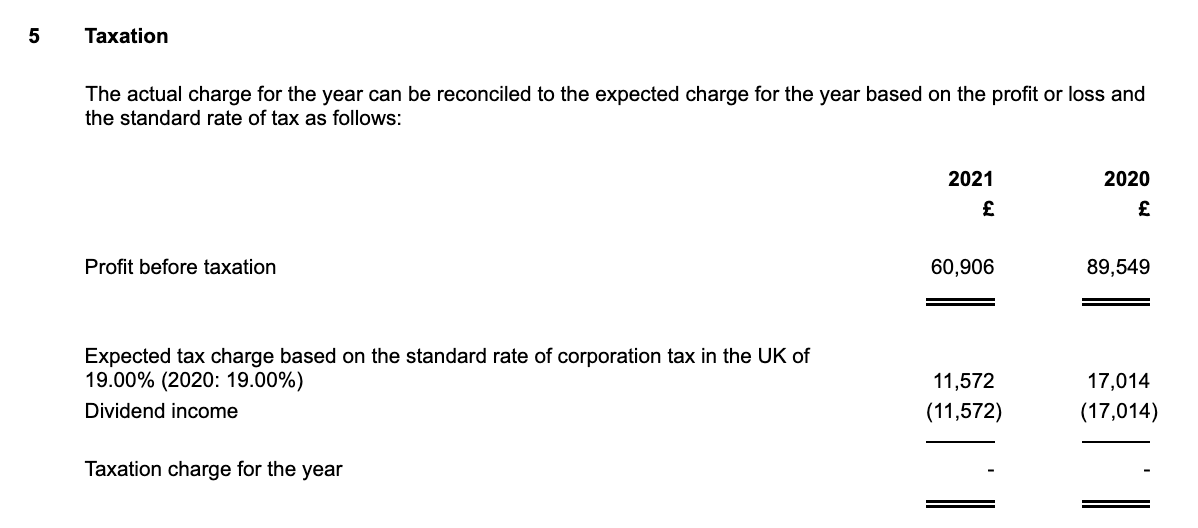

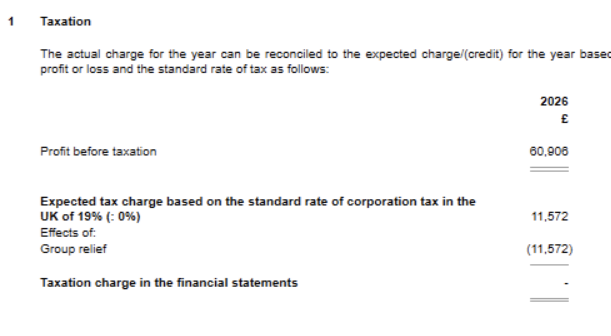

Here’s Tisun Three Limited’s tax reconciliation from its 2021 accounts (the tax reconciliation shows how you get from the profit in the accounts to the tax charge).

In this period, Tisun Three received £60,906 of property income distributions from the REIT. The accounts show the expected tax charge of £11,572 if you just apply the corporation tax rate of 19% to the £60,906 of income.

The tax reconciliation then explains why this tax doesn’t in fact arise. It shows the £11,572 of tax cancelled-out by a £11,572 negative entry labelled “dividend income”. The meaning is clear: the accounts are saying this was a dividend, and companies are normally exempt from corporation tax on dividends.

The problem is that this wasn’t a normal dividend at all. It was a “property income distribution” from a REIT – the REIT had been exempt on that profit, but corporate shareholders were not exempt. Tisun Three Ltd made the same mistake as Quidnet REIT did – it treated the payments from Quidnet as normal dividends, not as property income distributions.

The company therefore unlawfully failed to pay tax.

The result was that Tisun Three failed to pay tax on £60,906 of income in 2021, meaning lost corporation tax of £11,572 (at the 19% rate at the time).

This is repeated across almost all the Tisun companies accounts for all relevant years.5 You can download all the relevant accounts here.

The total untaxed income was £513,901, and therefore the lost tax was £97,641.6 Our methodology for this calculation is set out in full below.

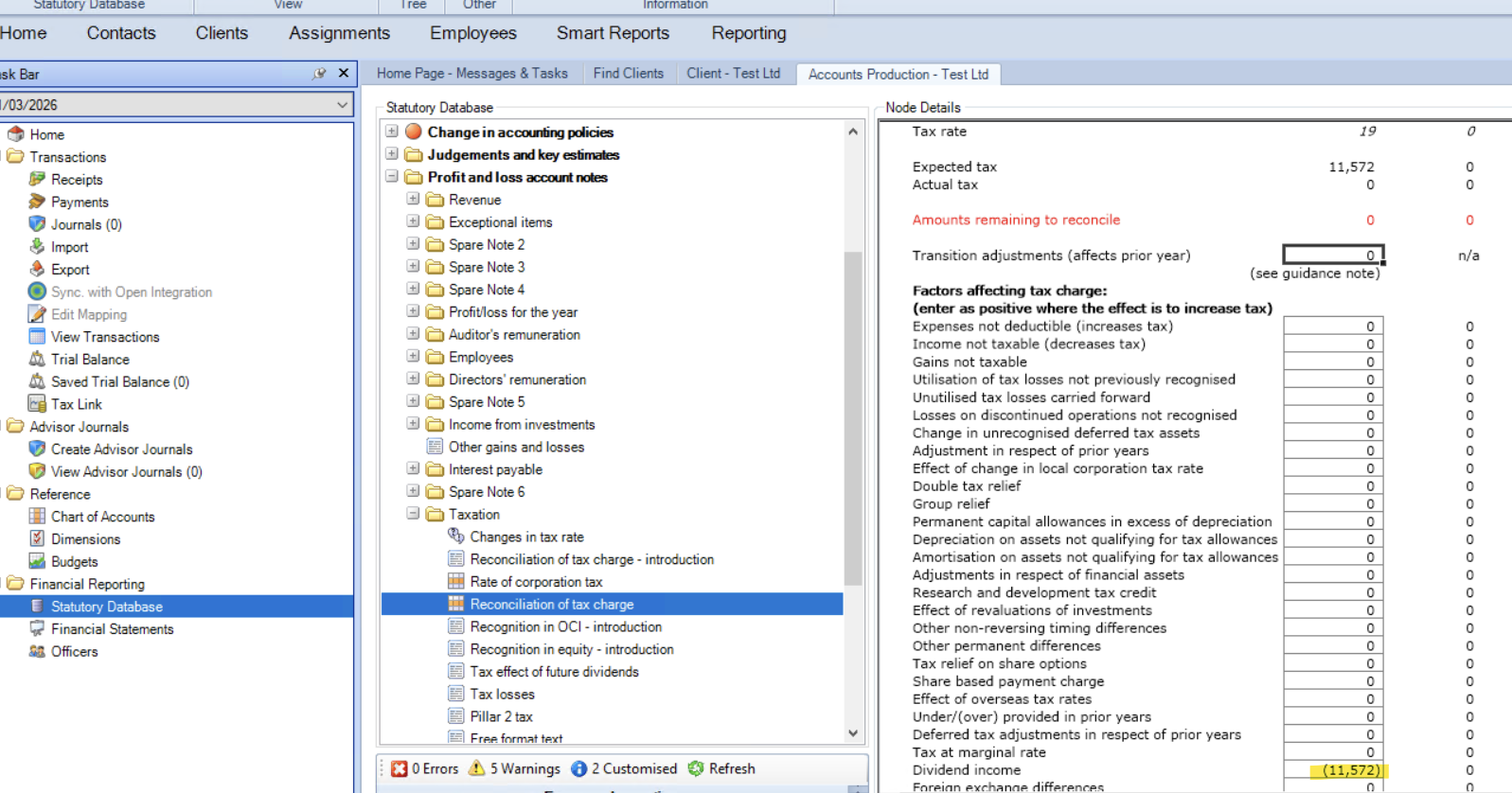

We should, however, consider the possibility that someone was being sloppy and typed “dividend income” when they really meant “dividend income is sheltered by losses”. If all we had was the printed accounts then we couldn’t exclude that possibility. We can, however, go beyond the printed accounts and read the underlying iXBRL code7 that Tisun Three Ltd’s accounting software uploaded to Companies House. The code for this line is:

This shows that the “(11,572)” figure in the tax reconciliation, negating the tax, was given the tag “TaxIncreaseDecreaseFromEffectDividendsFromCompanies”. This is a specific tag for the dividend exemption.8

If the company really had sheltered its income with losses, we would expect to see a group relief or loss-related reconciliation item (such as “TaxIncreaseDecreaseArisingFromGroupReliefTaxReconciliation”), not a dividends-from-companies item.

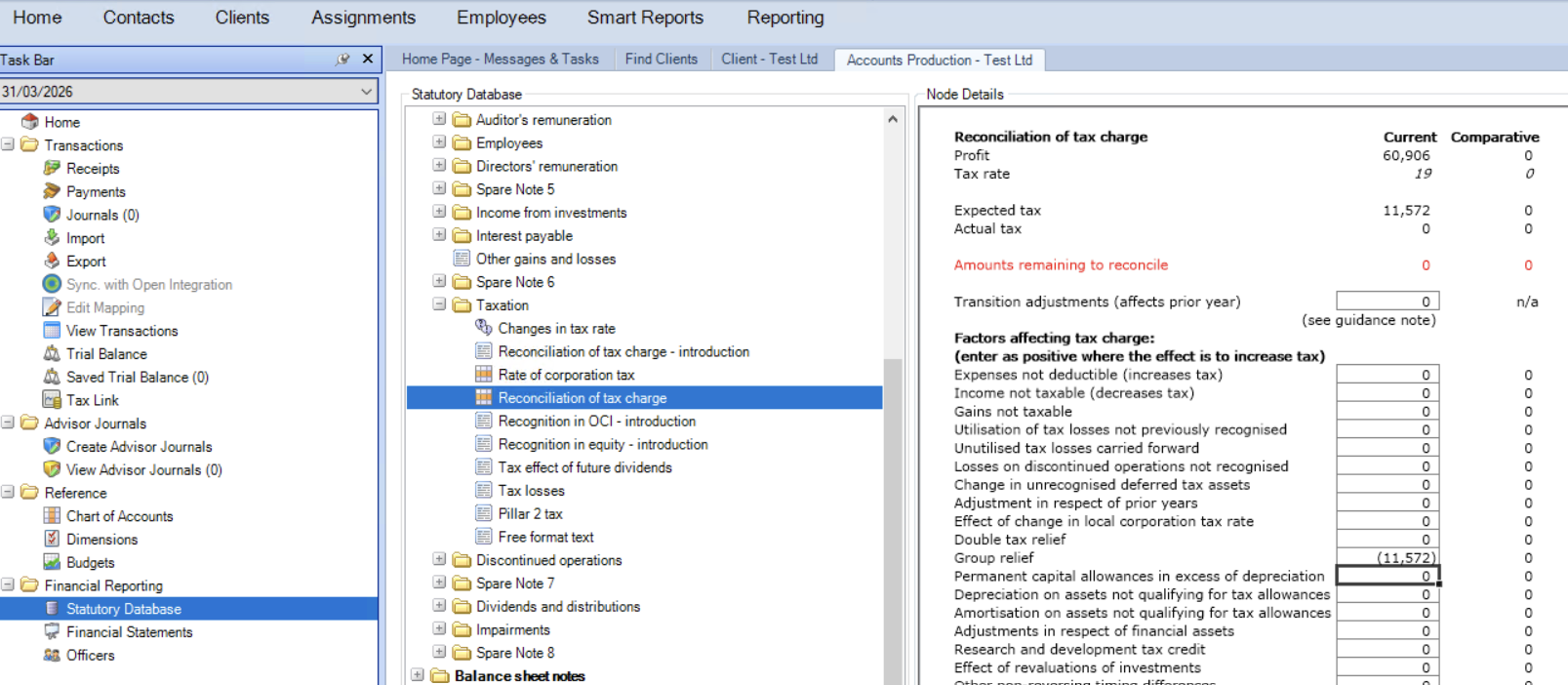

The iXBRL code also shows the accounts were submitted using CCH Accounts Production software. Here’s a screenshot showing what the accountant would have seen when entering the figures into that software, and what they would have entered to get the result that we see:

And here’s what they would have entered if they were actually claiming group relief:

The iXBRL code tells us that the tax reconciliation wasn’t merely poorly or sloppily worded – the accountant submitting the return actively selected the dividend exemption – when the dividend exemption could not in fact apply.

Is it theoretically possible tax losses were used?

It is possible in principle that Mr Tice was correct that group relief was claimed, and the accounts are simply wrong. For example, an accountant simply absent-mindedly used the dividend exemption box, when actually the Tisun companies were utilising losses from elsewhere in the group. The tax accountants we spoke to thought this would be unlikely. This is not a “fat finger” error, because it was repeated for three different companies across three years: 2020, 2021 and 2022.

There is, however, a more fundamental problem: our team undertook detailed due diligence of the wider group (including a review of 38 companies’ filings and 260 sets of accounts), and we found no material losses that could have been used to shelter the Tisun companies’ profits. That’s because, in short, the parent of the Tisun companies didn’t have assets or liabilities that could generate a material tax loss, and the way the group was structured means that losses of companies in the wider group were unavailable. Full details of this analysis are set out below.

So we believe we can exclude the possibility that the reason the Tisun companies paid no tax was the availability of losses elsewhere in the group.

Could the accounts just be wrong and tax really was paid?

We can exclude this for two reasons.

First, all four Tisun companies received dividends from Quidnet and then passed them straight up10 to their parent, Tisun Investments, without retaining anything to pay tax. The Tisun companies show no sign of any borrowing to fund any tax liabilities, and no creditor liability reflecting an upcoming tax bill. Their accounts show that each company’s sole asset was its investment in Quidnet REIT shares (funded by an inter-company loan).

Second, when the Sunday Times first asked Mr Tice about the lack of tax in the Tisun companies, he agreed they paid no tax, but said that was because of group relief.

The consequences

This is not tax avoidance. There was no loophole or grey area here. The rules on REIT property income distributions are clear: they are taxable in the hands of UK corporate recipients. This is understood by all advisers and (in our experience) most businesspeople owning and operating REITs.

Nor is this tax evasion – a criminal offence requiring dishonesty and intent. There is no evidence of either here.

The Tisun companies just paid the wrong amount of corporation tax. The practical consequence is that HMRC is likely to seek to recover that tax.

In most cases, HMRC would do this by issuing a “discovery assessment” — reopening a closed tax year where it discovers that tax has been underpaid. This is routine where an error only becomes apparent after the original return was filed.

Where a company has failed to take reasonable care — what the law calls a “careless” error — HMRC has six years from the end of the relevant accounting period to assess the additional tax. All of the periods in question here appear to fall comfortably within that window.11 We expect HMRC’s starting position would be that a failure to tax property income distributions is careless, and it is not obvious what explanation the company could provide that would overcome that.

In addition to the tax itself, penalties are likely. For careless inaccuracies, the statutory penalty range is up to 30% of the tax due. In practice, where the taxpayer cooperates and the error is disclosed, penalties are often lower — commonly around 10–15%.

Interest would also be payable on the late-paid tax: HMRC charges interest automatically on underpaid liabilities, calculated from the original due date, and in this case it would come to about £27,000 – the calculation is below.

There is then a wider question. If Quidnet failed to withhold tax because it didn’t understand the nature of REIT distributions, and the Tisun companies failed to pay tax on those distributions for the same reason… what other errors were made? In particular, did Mr Tice’s offshore trust pay any tax at all on its distributions? It certainly should have done – but the errors we have found make us wonder if in fact it did.

Richard Tice’s response

The Sunday Times wrote to Mr Tice on Thursday. We wrote on Friday:

We didn’t receive a response; neither did The Sunday Times.

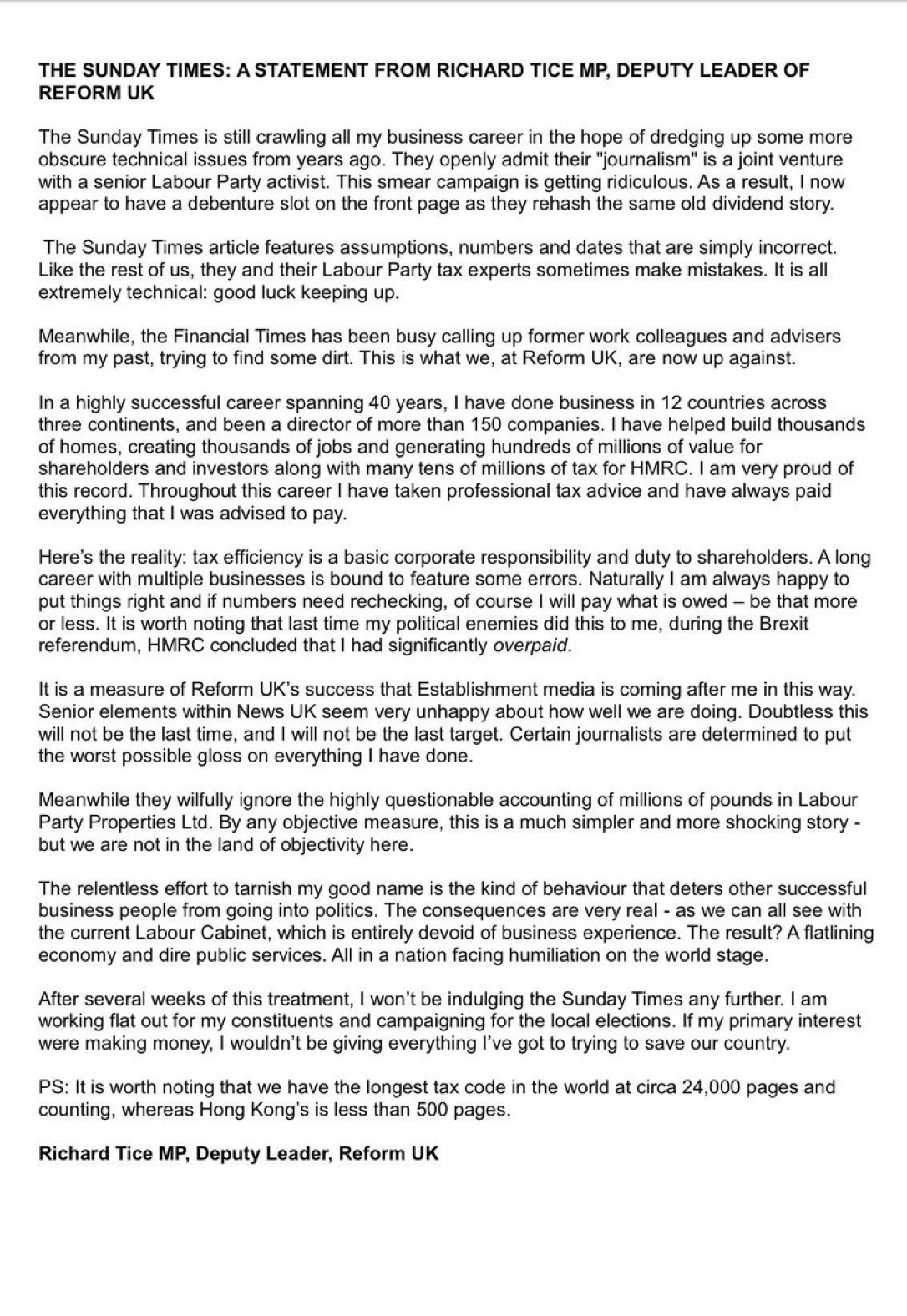

Shortly after publication of this report, Mr Tice published a statement. It does not deny any element of our reporting:

Methodology – determining the taxable profit

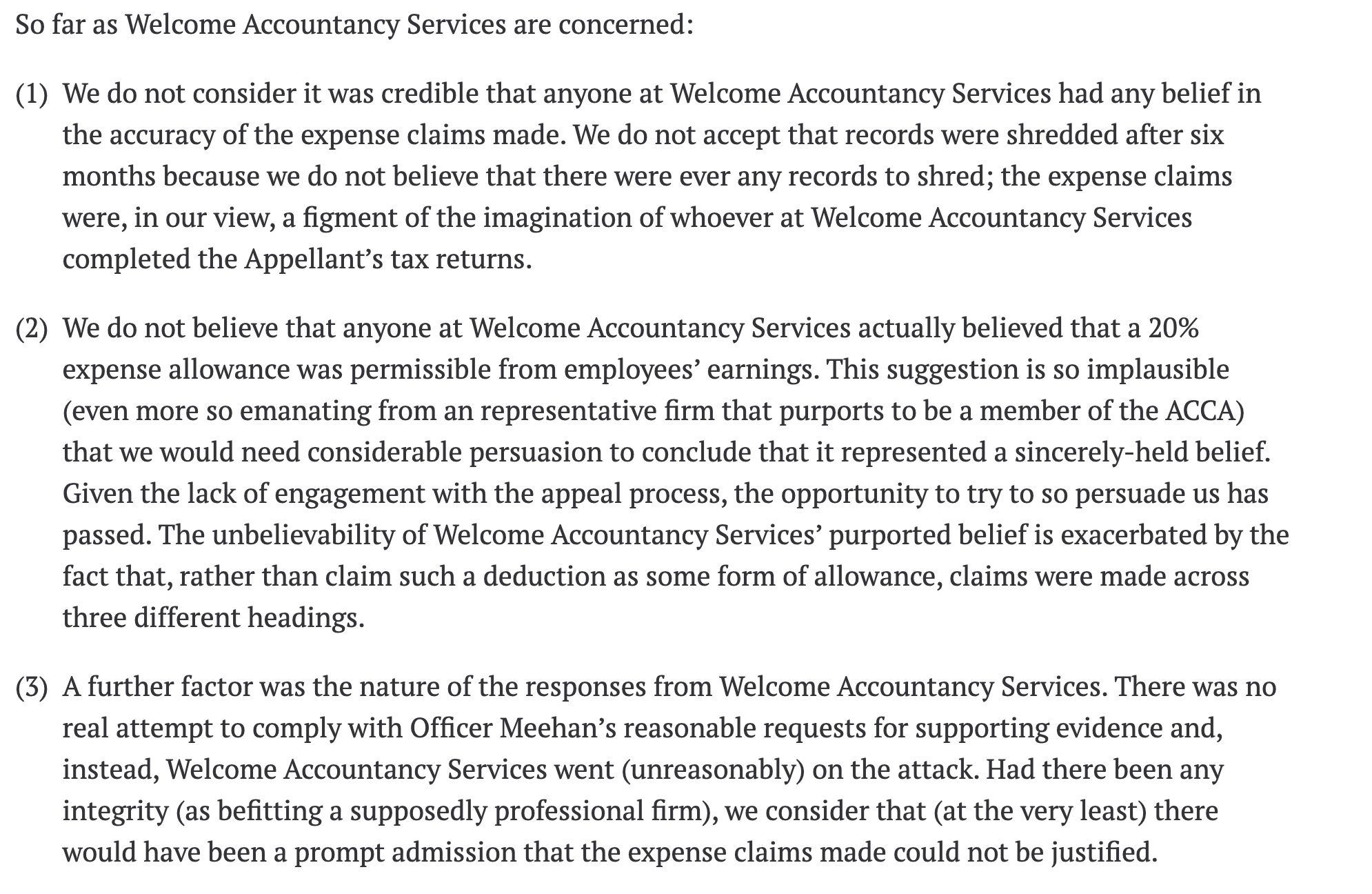

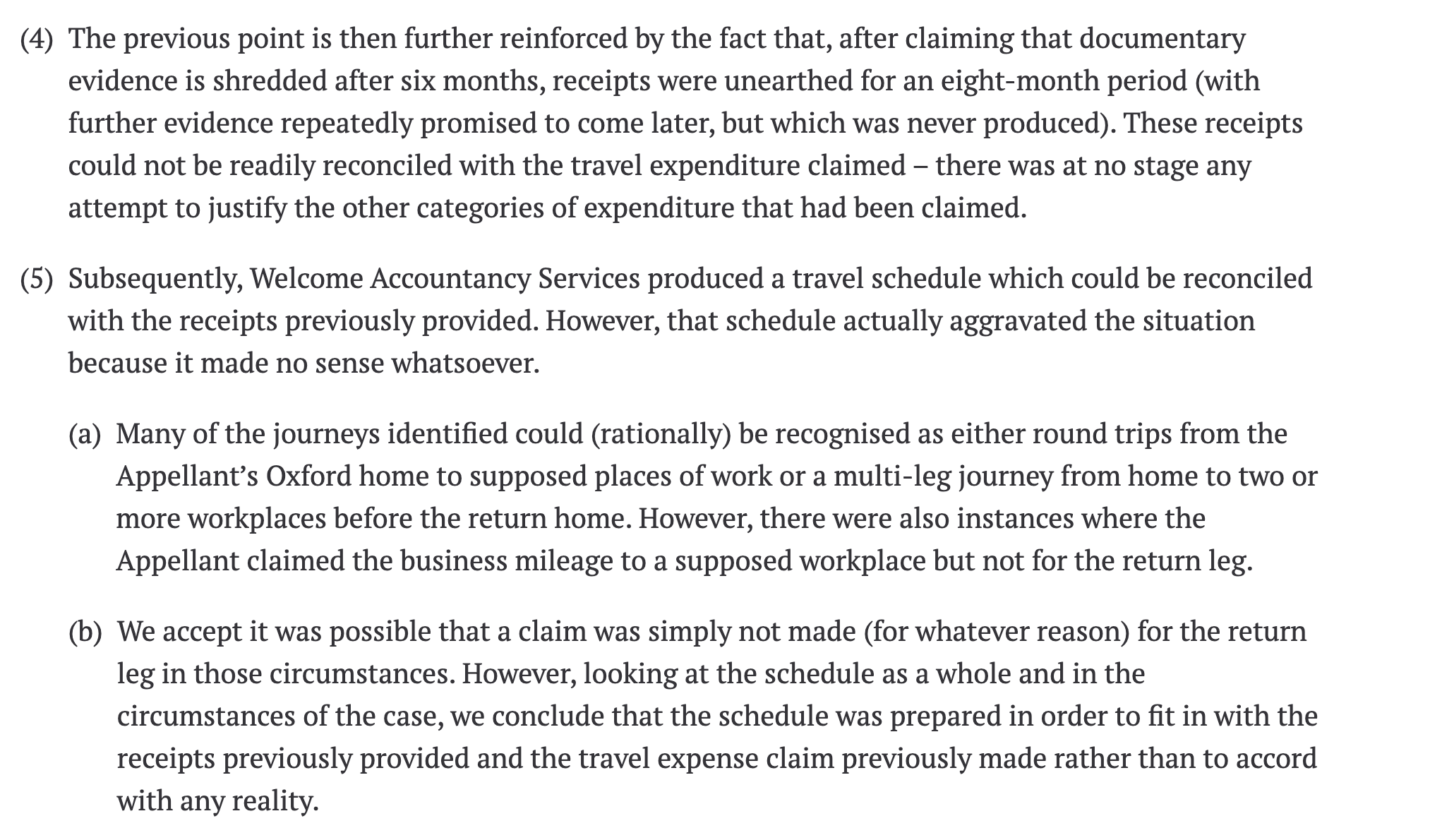

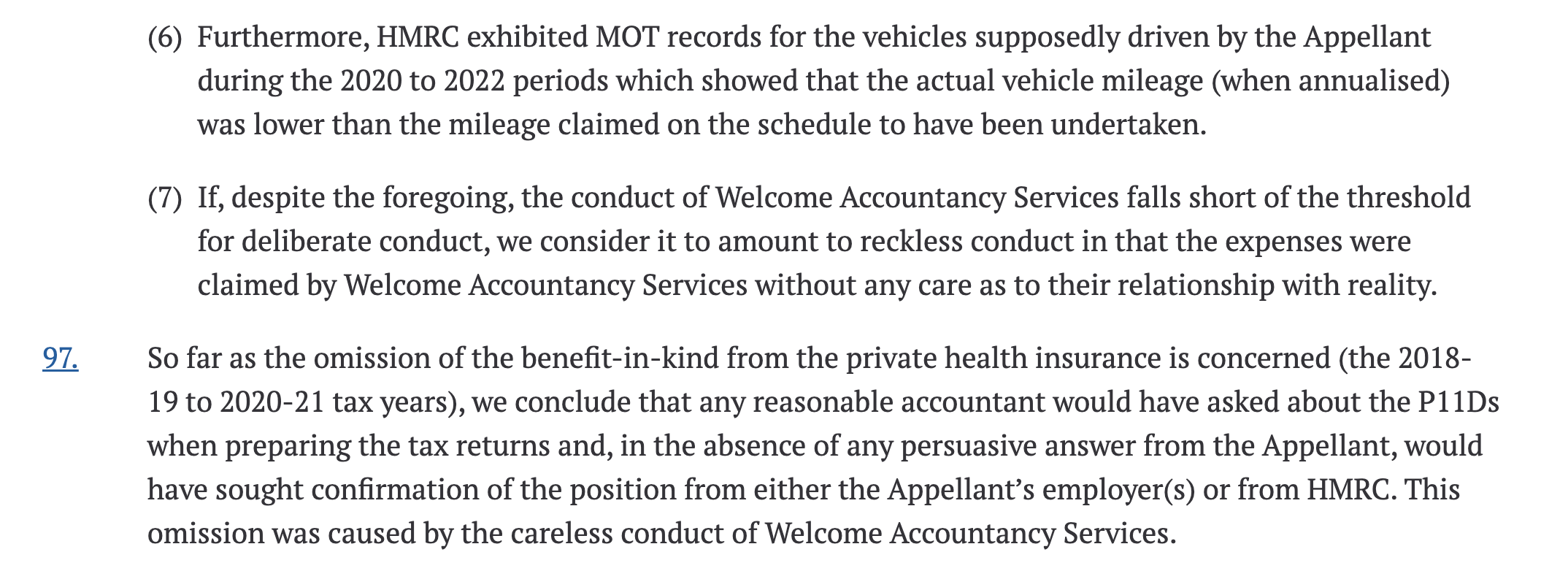

We calculate the £513,901 figure by:

identifying the REIT distributions (PIDs) declared by Quidnet

matching them to Tisun shareholdings

reconciling against the filed accounts

The first step was to reconcile the dividend income shown in the Tisun accounts against the dividends we know Quidnet REIT declared, and the shareholdings recorded in Companies House filings.

Quidnet’s own accounts explicitly disclose the PID per share for each financial year. The table below sets out, for each year, the total PID per share, the individual dividends that make it up, and the treatment we have adopted:

Financial year

Total PID per share

Individual dividends making up the total

Notes / treatment

FY2019

12.75p

12.75p FY2019 final dividend, paid March 2020.

100% PID.

FY2020

10.43p (weighted annual average)

5.00p H1 interim (paid September 2020 as scrip) + 6.00p FY2020 final (paid April 2021).

100% PID. The 10.43p figure ≈ total FY2020 dividends (£682,432) ÷ year-end shares (6,542,911). The 2020 dividends were paid as scrip — shares in Quidnet rather than cash — but the corporation tax treatment of scrip dividends for a REIT is the same as for a normal company, i.e. identical to cash dividends.

FY2021

6.99p (of which 5.50p H1 interim + 1.49p “REIT-period” slice of the final)

5.50p H1 interim (paid August 2021); 5.30p FY2021 final declared 10 May 2022 for the period 1 July – 31 December 2021.

Quidnet ceased to be a REIT on 9 August 2021. The full 5.50p H1 interim was declared while Quidnet was still a REIT and so we treat it as 100% PID. Of the 5.30p final, only 1.49p qualifies as PID (covering the pre-9 August 2021 part of the post-H1 period); the remaining 3.81p is a post-REIT ordinary dividend and is not PID.

FY2022 onwards

0.00p

—

No PIDs after the REIT period ended.

We can cross-check these figures against the Tisun accounts. For Tisun One, the FY2019 final (£63,028) plus the H1 2020 interim (£26,665) totals £89,693 — the accounts show £89,680 (a trivial difference from scrip share rounding). This gives us high confidence that the PID calculations are correct.

There are, however, three anomalies that affect all the other accounts:

Anomaly 1: the dividends that didn’t exist

As we have reported, in 2020, all of the REIT distributions were paid in shares, not cash. According to Quidnet’s Companies House filings, those shares remained owned by the four Tisun companies. Yet the four sets of accounts show dividends being paid up to their parent company, Tisun Investments. There was no cash to fund those dividends, and no capital raising or increase in creditors to fund a cash dividend.

We don’t think this can be correct, but it’s not clear what happened. However, this does not change our calculations – the tax position is unaffected by whether the four Tisun companies in fact retained the shares or paid them as a dividend to Tisun Investments.

Anomaly 2: the FY2021 ~3.5% shortfall in Tisun One, Two and Three

For the year ended 31 December 2021, each of Tisun One, Two and Three booked dividend income of roughly £2,300 less than the per-dividend, per-share calculation implies. The shortfall is consistent in size (about 3.5%) and consistent in direction (accounts are lower than the calculated figure) across all three companies.

The per-dividend calculation for 2021 is simply the FY2020 final dividend (6.00p PID) plus the H1 2021 interim dividend (5.50p PID), each multiplied by the relevant Tisun shareholding at the record date:

Company

Quidnet shares

FY2020 final 6.00p × shares

H1 2021 interim 5.50p × shares

Calculated 2021 total

Per filed accounts

Shortfall (£)

Shortfall (%)

Tisun One

550,494

£33,030

£30,277

£63,307

£61,029

£2,278

3.6%

Tisun Two

549,383

£32,963

£30,216

£63,179

£60,906

£2,273

3.6%

Tisun Three

549,383

£32,963

£30,216

£63,179

£60,906

£2,273

3.6%

Total

£98,956

£90,709

£189,665

£182,841

£6,824

3.6%

The shareholdings are taken from the Quidnet confirmation statements on file at Companies House. The PID rates are the figures Quidnet discloses in its own 2020 and 2021 accounts: a 10.43p annual PID for FY2020 (broadly equal to the 5p H1 interim plus the 6p FY2020 final — we have treated it as 6p for the final on the basis of the stated per-dividend rates) and a 5.5p interim for H1 2021.

We cannot explain the ~3.6% shortfall. It is consistent in percentage terms across three separately-filed sets of accounts in one year; it could be some kind of intentional methodology but it seems more likely to be a calculation error.

In any event, for the purposes of the corporation tax calculation we will use the amounts Quidnet actually paid, per Quidnet’s audited accounts and the confirmation-statement shareholdings.

The effect is to increase our calculation of the Tisun companies’ taxable PID income by about £6,800 in aggregate, or about £1,300 of corporation tax at 19%.

Anomaly 3: Tisun Four’s dividend that didn’t exist

Tisun Four was incorporated on 11 September 2020 and subscribed for 238,233 Quidnet shares on 21 September 2020. Both dates are after the record date for Quidnet’s H1 2020 interim dividend, so ordinarily Tisun Four should not have received any part of the H1 2020 dividend, only the FY 2020 final dividend (paid in 2021) and then the H1 2021 interim dividend (paid later in 2021).

Tisun Four’s accounts for its first period (11 September 2020 to 31 December 2021) record total dividend income of £37,951. The comparative column in its 2022 accounts splits that 2021 income between a “Final paid” figure of £24,848 for 2020 and an “Interim paid” figure for 2021 of £13,103.

We can reconcile the “interim 2021” figure exactly:

Line in Tisun Four accounts

Amount Booked in Tisun Four’s accounts

Reconciles to line in Quidnet’s accounts

Calculation based on Quidnet accounts and Tisun Four’s holding

Match?

Interim 2021 paid

£13,103

H1 2021 interim @ 5.50p

5.50p × 238,233 = £13,103

Exact

However we cannot reconcile the £24,848 “final 2020” figure against Tisun Four’s actual legal entitlement to dividends in 2020:

Line in Tisun Four accounts

Amount Booked in Tisun Four’s accounts

Reconciles to line in Quidnet’s accounts

Calculation based on Quidnet accounts and Tisun Four’s holding

Match?

Final paid — the 6.00p paid when Tisun Four was shareholder

£24,848

FY2020 final @ 6.00p

6.00p × 238,233 = £14,294

Does not match booked figure

The £24,848 only reconciles against all Quidnet REIT’s 2020 dividends – which is wrong, because Tisun Four shouldn’t have been entitled to the 2020 interim dividend, as it wasn’t a shareholder on the record date.

Line in Tisun Four accounts

Amount Booked in Tisun Four’s accounts

Reconciles to line in Quidnet’s accounts

Calculation based on Quidnet accounts and Tisun Four’s holding

Match?

Final paid (2021 comparative) — as booked

£24,848

Full FY2020 annual PID @ 10.43p

10.43p × 238,233 = £24,848

Exact

This cannot be correct, not least because Quidnet’s 2020 accounts (the statement of changes in equity in particular) only reconciles if the 2020 interim dividend was not paid to Tisun Four.

We will again resolve this by following the Quidnet audited accounts, not the Tisun Four accounts. That has the effect of reducing Tisun Four’s taxable PID income by £10,554, i.e. reducing the tax underpayment by £2,005.

Net effect on the corporation tax calculation

Anomalies 2 and 3 pull in opposite directions but the headline number is unchanged:

Adjustment

PID income

CT at 19%

Tisun One/Two/Three FY2021 shortfall (added back to match Quidnet-paid PID)

+£6,824

+£1,297

Tisun Four H1 2020 excess (removed to match Quidnet)

(£10,554)

(£2,005)

Total adjustment vs. booked accounts

(£3,730)

(£708)

The full reconciliation

Adjusting for the anomalies, and using the Quidnet audited accounts PID rates and the known shareholdings at each dividend record date, we can calculate the PIDs received by each Tisun company:

Dividend

Tisun One

Tisun Two

Tisun Three

Tisun Four

Total

FY2019 final (12.75p PID)

£63,028

£62,900

£62,900

£188,828

H1 2020 interim (5.00p PID)

£26,665

£26,611

£26,611

£79,887

FY2020 final (6.00p PID)

£33,030

£32,963

£32,963

£14,294

£113,250

H1 2021 interim (5.50p PID)

£30,277

£30,216

£30,216

£13,103

£103,812

FY2021 final (1.49p PID)

£8,202

£8,186

£8,186

£3,550

£28,124

Total PIDs

£161,202

£160,876

£160,876

£30,947

£513,901

The FY2019 final and (subject to anomaly 3) the H1 2020 interim dividends pre-date Tisun Four’s existence – it was incorporated in September 2020. The later dividends were received by all four companies.

This produces total taxable income of £513,901. The corporation tax rate at the time was 19%, and so the unpaid tax was £97,641.

Methodology – group relief

The Tisun group from 20 November 2020

At the time of the later REIT payments, the Tisun companies were in a small group. This diagram shows the group, and the other Quidnet REIT shareholders:

Tisun / Quidnet group structure as at 1 July 2021

From Richard Tice to Tisun Holdco (Label: 77.1%)

From Richard Tice to Tisun Holdco (Label: 22.9%)

From Tisun Holdco to Tisun Investments (Label: 100%)

From Tisun Investments to Tisun One (Label: 100%)

From Tisun Investments to Tisun Two (Label: 100%)

From Tisun Investments to Tisun Three (Label: 100%)

From Tisun Investments to Tisun Four (Label: 100%)

From Richard Tice (direct) to Quidnet REIT (Label: 13.00%)

From RJS Tice Family Settlement to Quidnet REIT (Label: 16.88%)

From RJS Tice Family SIPP to Quidnet REIT (Label: 34.98%)

From Tisun One to Quidnet REIT (Label: 7.80%)

From Tisun Two to Quidnet REIT (Label: 7.78%)

From Tisun Three to Quidnet REIT (Label: 7.78%)

From Tisun Four to Quidnet REIT (Label: 3.38%)

From Huntress (CI) Nominees to Quidnet REIT (Label: 4.42%)

From NJG Tribe SIPP to Quidnet REIT (Label: 2.99%)

From Employees to Quidnet REIT (Label: 0.98%)

A company in a group can use “group relief” to utilise another group member’s tax trading losses, property business losses, and losses on certain financial and other types of assets, but not losses on capital assets.

There are, furthermore, stringent conditions for companies to be in a group relief group. There has to be a 75% common corporate shareholding (i.e. not via an individual owner). So the only possible companies that could have generated losses for the four Tisun companies are those in this diagram, and not other companies held separately by Mr Tice.12

Tisun Holdco never had any material assets or liabilities other than its shareholding in Tisun Investments.13 That leaves Tisun Investments Ltd as the only entity that could in principle have had losses that the four Tisun companies could have used. Tisun Investments’ accounts for 202014, 2021 and 2022, show that it did have sizeable accounting losses every year. However the nature of its assets and liabilities mean that we expect almost none of these losses would be recognised for tax purposes.

Tisun Investments Ltd’s assets were:

Two flats in Kent, combined into a single dwelling, in a building where all the other flats are now owned by the Tice family. The value of the dwelling was around £600,000 and at the time in question it was unmortgaged.15 So, whether used by the family or rented out, the property is unlikely to have generated material tax losses, and certainly not the ~£170k/year needed to shelter the Tisun profits.16

A motor vehicle on hire purchase – likely a personal car. The cost of this may be partially allowable for tax purposes, but the amounts are not material (probably £5-15k each year of capital allowances and running costs).

Unlisted investment assets, never more than £120,000. We don’t have any information about what the investments are, but the limited value means that they won’t have justified material management expenses, and any loss on disposal would be a capital loss (which can’t be used to shelter trading profits or property income).

Shareholdings in its subsidiaries – Tisun One, Two, Three and Four, and JMT Holdco. Management expenses incurred wholly and exclusively for the purposes of managing these assets would be tax deductible; but given the passive nature of the companies, it’s difficult to see how that could generate material deductible costs.

Loans to its subsidiaries (Tisun One, Two, Three and Four), and its parent, (Tisun Holdco).17 Loans to connected parties generally generate no deductible debits for the lender (even if impaired or written off). The Tisun subsidiaries’ accounts suggest no interest is charged but, even if it was, the tax deductions for the payer would be matched by taxable income in Tisun Investments. These loans are therefore not a plausible source of net deductible tax losses.

Loans to related parties, with a balance fluctuating between £0.8m and £1.1m. These include loans to Richard Tice personally, to Reform UK, and to other connected parties. The loans are all either interest-free or non-commercial. Non-commercial loans don’t generate deductible losses for the lender, and (again) neither do loans to connected parties.

Its liabilities were:

270,000 preference shares at 7% – treated as debt for accounting purposes but not for tax purposes, so no tax deduction available.

£1,679,712 owed to JMT Corporation, an associated company that’s not part of the group relief group. The loan is interest-free18, so doesn’t generate any losses for Tisun Investments.

Loans from related parties – again, these appear to be non-commercial funding arrangements. Any associated costs would be unlikely to be deductible, and there is no evidence of significant interest expense in the accounts.

We therefore conclude that Tisun Investments Ltd did not generate material losses that could be used to shelter profits elsewhere in the group. It looks like the company’s accountants agreed, as there’s no sign of a deferred tax asset, or any mention of losses or group relief.

It follows that the accounting did not merely misstate a group relief claim as a dividend exemption. There was no group relief in 2021 and 2022.

The Tisun group in 2020

Until 20 November 2020, Tisun Investments and its subsidiaries were part of a much larger group, headed by Sunley Family Holding Ltd.1920

Sunley / Tisun group structure as at 19 November 2020

From Sunley Family Holding to Sunley Family Limited (Label: None)

From Sunley Family Holding to Tisun Investments (Label: None)

From Sunley Family Holding to JMT Corporation (Label: None)

From Sunley Family Holding to West Eleven Investments (Label: None)

From Sunley Family Holding to William Tice Family (Label: None)

From Sunley Family Limited to Sunley Holdings (Label: None)

From Sunley Holdings to Sunley Estates (Label: None)

From Sunley Holdings to Executive Centre Brighton (Label: None)

From Sunley Holdings to Environ (Kent) (Label: None)

From Sunley Holdings to Bach Homes (Sunley) (Label: None)

From Sunley Holdings to GMH (2004) (Label: None)

From Sunley Holdings to SP (2004) (Label: None)

From Sunley Holdings to Sunley FPR (Label: None)

From Sunley Holdings to Fairfax Shelfco 321 (Label: None)

From Sunley Family Limited to Prospero 2006 (Label: None)

From Sunley Family Limited to Sunley Investments (Label: None)

From Tisun Investments to Tisun One (Label: None)

From Tisun Investments to Tisun Two (Label: None)

From Tisun Investments to Tisun Three (Label: None)

From Tisun Investments to Tisun Four (Label: None)

In the interests of clarity, the diagram omits the REIT and its other shareholders. It also omits a large number of inactive and/or dormant companies21, and entities (LLPs, settlements) which are not companies and so not relevant for group relief purposes.

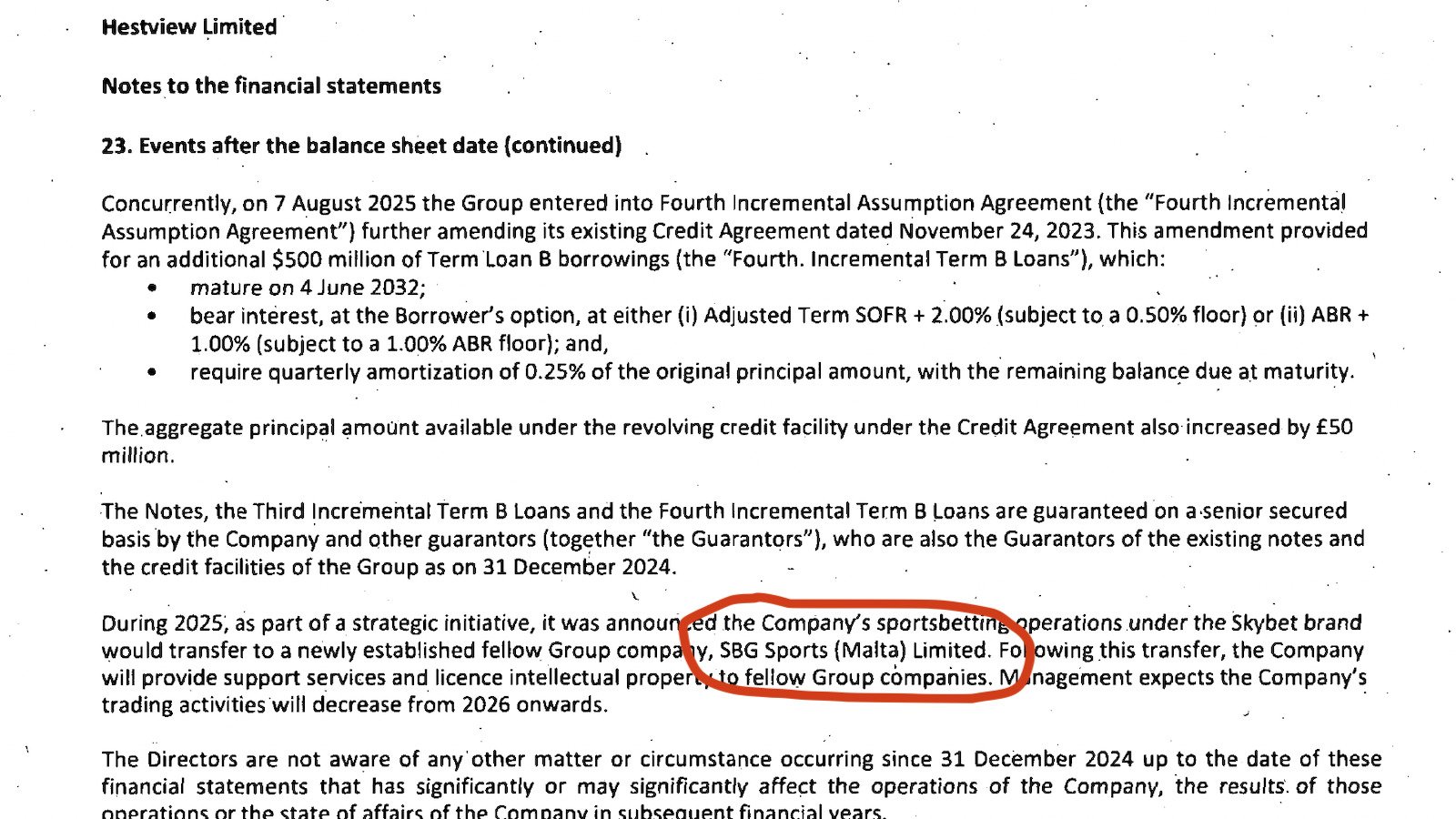

During this period, Tisun Investments’ assets and liabilities were, so far as material, as set out above regarding the post-2020 period – so it had no losses to surrender to the Tisun companies. However the Sunley group had companies with much a wider and more extensive degree of activity than Tisun Investments, and some of the Sunley companies could have had large losses – potentially hundreds of thousands of pounds.22232425 So, at first sight, this could be an answer to how the Tisun companies’ 2020 profits were eliminated.

There is, however, a technical barrier that means in fact no losses the Sunley group could be used by the Tisun companies. Sunley Family Ltd had a “tracking share”26 structure. The economic rights to Tisun Investments Limited were not held by the wider Sunley group but were reserved to holders of Sunley Family Ltd’s “B ordinary shares”.27 Those B shares were held by Richard Tice – partly for himself, and partly as trustee for his Tice children. This “broke” the tax group – if the economic interest in a company is held by a third party then it’s no longer a member of its parent company’s tax group:

The group relief legislation is in Part 5 CTA 2010. The basic rule is that two companies are in the same group if one is a 75% subsidiary of the other, or both are 75% subsidiaries of a third company.

There are a further series of complex tests which mean that if the economic rights of the subsidiary are in fact with a third party, the subsidiary is not in its parent’s tax group. The statutory gateway for this is section 151 CTA 2010.28

HMRC explain the policy rationale in CTM81005. The rules are designed to stop group relief where the apparent parent is not the true economic parent – otherwise it would be easy for economically unrelated companies to use each other’s losses. 29

It follows that Tisun Investments was not part of the Sunley group for tax purposes.30

The Sunley losses are therefore irrelevant – however large they were, they couldn’t have been used by the Tisun companies. The only potential source of losses for the four Tisun companies was Tisun Investments and, for the reasons set out above, it had no material tax losses.

Earlier periods

Tisun One, Two and Three were incorporated on 6 July 2018, and Tisun Four was incorporated on 11 September 2020. But Tisun Investments Ltd was not a newly-created shell when the Quidnet REIT structure was put in place: it had existed since 2006 and, as its filed accounts show, had a mixture of investment, property, loan and short-lived work-in-progress activity over the years.

However, any tax losses from these earlier activities could not have sheltered the £514,000 of Quidnet REIT property income distributions received by the Tisun companies. Until 1 April 2017, carried-forward losses in one company could never be surrendered as group relief to shelter the profits of another company at all – they stayed locked in the company that made them. From 1 April 2017, the new Part 5A CTA 2010 regime allows carried-forward losses to be surrendered as group relief, but only if they arose on or after 1 April 2017 and only where the surrendering and claimant companies were members of the same group when the loss arose.31 Pre-2017 Tisun Investments losses are therefore locked inside Tisun Investments.

For completeness, we reviewed every filed set of Tisun Investments accounts from 2007 to 2024.32 The picture is of an investment/holding company with some short-lived property and work-in-progress activity, paying tax in several years and with no material carried-forward losses.

Methodology – interest calculation

We calculated late-payment interest using HMRC’s published late-payment rates, applying simple daily interest to the corporation tax outstanding in each period. The first period starts on 1 October 2021, the first deadline for paying the tax. The amount outstanding then increases when later corporation tax liabilities fall due:

Period

HMRC rate

Amount owed

Interest

1 Oct 2021 to 7 Jan 2022

2.60%

£51,055.85

£356.41

7 Jan 2022 to 21 Feb 2022

2.75%

£51,055.85

£173.10

21 Feb 2022 to 5 Apr 2022

3.00%

£51,055.85

£180.44

5 Apr 2022 to 24 May 2022

3.25%

£51,055.85

£222.76

24 May 2022 to 11 Jun 2022

3.50%

£51,055.85

£88.12

11 Jun 2022 to 5 Jul 2022

3.50%

£56,261.28

£129.48

5 Jul 2022 to 23 Aug 2022

3.75%

£56,261.28

£283.23

23 Aug 2022 to 1 Oct 2022

4.25%

£56,261.28

£255.49

1 Oct 2022 to 11 Oct 2022

4.25%

£92,297.63

£107.47

11 Oct 2022 to 22 Nov 2022

4.75%

£92,297.63

£504.48

22 Nov 2022 to 6 Jan 2023

5.50%

£92,297.63

£625.85

6 Jan 2023 to 21 Feb 2023

6.00%

£92,297.63

£697.92

21 Feb 2023 to 13 Apr 2023

6.50%

£92,297.63

£838.26

13 Apr 2023 to 31 May 2023

6.75%

£92,297.63

£819.30

31 May 2023 to 11 Jul 2023

7.00%

£92,297.63

£725.74

11 Jul 2023 to 22 Aug 2023

7.50%

£92,297.63

£796.54

22 Aug 2023 to 1 Oct 2023

7.75%

£92,297.63

£783.90

1 Oct 2023 to 20 Aug 2024

7.75%

£97,641.19

£6,717.18

20 Aug 2024 to 26 Nov 2024

7.50%

£97,641.19

£1,966.20

26 Nov 2024 to 25 Feb 2025

7.25%

£97,641.19

£1,764.90

25 Feb 2025 to 6 Apr 2025

7.00%

£97,641.19

£749.03

6 Apr 2025 to 28 May 2025

8.50%

£97,641.19

£1,182.39

28 May 2025 to 27 Aug 2025

8.25%

£97,641.19

£2,008.33

27 Aug 2025 to 9 Jan 2026

8.00%

£97,641.19

£2,889.11

9 Jan 2026 to 15 Apr 2026

7.75%

£97,641.19

£1,990.28

£26,855.91

The calculation runs to 15 April 2026 and assumes no tax was paid before then.

This issue was identified by one of our contributors, D. We developed this report in conjunction with Gabriel Pogrund of the Sunday Times, who discovered the initial tax issues with the Quidnet structure.

The REIT and accounting analysis for this and our original report was mostly from K, M1, and P1, with additional insights from D, R, P2 and M2. Thanks to J, B and M3 for practical advice on, and demonstrations of, the CCH accounting software used by the Tisun companies.

And finally thanks to all the volunteers who worked on the group relief due diligence, reviewing filings for 38 companies and 260 sets of company accounts.

The logic is that funds don’t pay tax; their investors do – we see this across almost all forms of investment fund, although it’s achieved in a variety of different ways. ↩︎

When a UK company receives a normal dividend from another company, it doesn’t pay tax – there’s a corporation tax exemption for dividends. The reason is that the subsidiary would have paid tax on its profits, so it makes no sense to tax them again. However property income distributions from REITs are different. A REIT does not pay tax on its property income. So it stands to reason that a UK company receiving a property income distribution pays corporation tax on it – and that is indeed the result. ↩︎

Why have so many companies? At the time, the REIT rules penalised a REIT if any single corporate shareholder held 10% or more. By splitting a single ~27% holding across four companies, each holding under 10%, it was straightforward to avoid the prohibition. The 10% rule was regarded as rather pointless by both taxpayers and HMRC and changes in 2023 mean it now rarely applies. All of which means that we would regard the splitting of the ownership (of itself) as tax planning, not tax avoidance; we don’t believe HMRC would have any realistic prospect of challenging it. ↩︎

Because they were UK companies, there was no requirement for Quidnet REIT to withhold tax. ↩︎

We see the same exact approach in the Tisun One, Tisun Two and Tisun Three accounts from 2020 to 2022, and the Tisun Four accounts for 2022. Tisun Four has no tax reconciliation for 2020 and 2021 but its accounts for these two years are otherwise consistent with the other ten accounts. In 2022, the companies did receive some ordinary dividends which really were exempt, but also property income distributions which were not. Our reconciliation distinguishes the two cases. ↩︎

These figures fully take into account that some dividends were ordinary dividends which absolutely were exempt. ↩︎

When a UK company files accounts electronically, it often does not send Companies House a simple PDF. Instead, it sends an iXBRL file: a document that looks like ordinary accounts on screen, but with machine-readable tags embedded behind the text and numbers. The tags were standardised by the Financial Reporting Council – you can see and search them all here. ↩︎

Also note that the £60,906 income in the tax reconciliation statement is given the tag “DividendIncome”; not technically correct. ↩︎

The screenshots are from the current version of CCH Accounts Production; we understand from the accountants we spoke to that the screens were the same in 2020, 2021 and 2022. ↩︎

Subject to an oddity about scrip dividends, discussed further below. ↩︎

i.e. because the earliest accounting period ended 31 December 2020, meaning HMRC has until 31 December 2026. ↩︎

A significant entity – JMT Corporation Ltd – is excluded from the diagram and analysis below because, whilst it is held by Tisun Investments, it isn’t part of a 75% group with the Tisun companies and so can’t surrender losses to them. JMT Corporation was Richard Tice’s late mother’s former investment company. JMT Holdco was incorporated in March 2020, held by Richard Tice directly – it then acquired JMT Corporation. At some point between March and December 2021, Tice sold 55.4% of the shares in JMT Holdco to Tisun Investments; Tisun Investments therefore treats it as a subsidiary for accounting purposes (but it’s not part of a group relief group). By 2024, JMT Corporation’s sole material asset was a £1.66m intercompany loan to Tisun Investments. ↩︎

It was incorporated on 17 March 2020. From 2020 to 2023 it appears to have been a very thin holding company: its only visible asset was its 100% shareholding in Tisun Investments Limited, carried at £32,418, and its only visible liabilities were short-term group creditors and, in 2020-2021, accruals/deferred income. The filed accounts do not include a profit and loss account. From the balance sheet/reserve movements only, the apparent results are: 2020 loss £925; 2021 nil movement; 2022 positive movement/profit £925; 2023 nil movement. ↩︎

Note the 2020 accounts were massively restated the following year; the 2020 accounts themselves show a large profit. ↩︎

In late 2022, a further part of one of the flats was acquired, worth £126,000, and a £491,000 mortgage with Weatherbys was taken out over all three titles the following year 2023. ↩︎

The building is on a private estate. We have full details of the dwelling, have reviewed planning consents, and believe we have identified how the dwelling is used; we are, however, not publishing further details given the possible privacy implications for the Tice family. ↩︎

The identity of the borrowers is not explicitly disclosed but the £2,064,976 “owed by group undertakings” in Tisun Investments’ 2024 accounts exactly reconciles to the balances shown in the latest accounts of the four Tisun subsidiaries and Tisun Holdco. Tisun One shows £559,961 owed to group undertakings, Tisun Two £558,960, Tisun Three £558,960, Tisun Four £369,500 and Tisun Holdco £17,595, giving £2,064,976 in total. ↩︎

We know JMT Corporation was the lender because JMT Corporation’s 2022 accounts show a matching amount “owed by group undertakings”. We know it’s interest-free because we can use JMT Corporation’s balance sheet to reverse-engineer its profit and loss account. The accounts show the company’s total assets decreasing by £31,261 as it liquidated its entire £488,192 investment portfolio, drew down its cash and other debtors, and used these funds to increase the pre-existing loan to Tisun Investments. Concurrently, total liabilities decreased by £17,229 as the company paid down historical short-term creditors and deferred tax provisions. Offsetting the £31,261 drop in assets against the £17,229 reduction in liabilities results in a net asset decrease of £14,032, which matches the company’s reported loss for the year. We see the same in other years. We conclude that there cannot have been any interest received on the loan to Tisun Investments. ↩︎

Until October 2020, Tisun Investments sat “lower” in the group, under Sunley Family Limited group. In October 2020 it moved under Sunley Family Holding Ltd, and on 20 November 2020 it moved out to Tisun Holdco. We discuss the consequence of that below. We show the October to November 2020 picture for clarity. ↩︎

In particular, Sunley Estates Limited was a substantial property company. Its 2020 accounts show investment property of £2.1m, group debtors of £12.2m, group creditors of £1.5m and net assets of £13.6m. Its profit and loss account grew from £8,862,526 in 2019 to £9,426,401 in 2020, telling us that the company’s total profits were £563,875 that year (the accounts disclose no dividends). However we need to reverse out two elements that are disregarded for tax purposes: a £1,171,448 positive revaluation of property assets, and a “deferred tax” provision of £222,575. That tells us the company may actually have made a loss of about £385,000. That is absolutely not a robust number – it’s possible that some or even all of this loss would disappear if we actually knew the underlying revenue and expense items. The loss would also be smaller or disappear if dividends were paid. Subsequent accounts (and the lack of any obvious utilisation against later profits here or elsewhere) suggest to us this may not actually have been a tax loss. Nevertheless, we conservatively assume that the tax loss we’ve inferred was real. ↩︎

West Eleven Investments looks much larger at first sight. Its net assets fell from £1,497,834 to £1,151,898, and its profit and loss reserve moved from a £2,176 deficit to a £348,112 deficit. That is a raw reserve fall of about £346,000. But the notes show a £399,546 tangible-asset revaluation loss and a £35,653 investment revaluation gain. Reverse those revaluations and the large apparent loss disappears entirely — the adjusted position is a small profit, not a loss. But, again, it doesn’t matter how many losses were generated – the overlapping period rules still apply. ↩︎

William Tice Family may have generated some small losses. Its net assets increased from £1,936,930 to £1,967,402, and its profit and loss reserve increased from £724,348 to £754,820. It therefore did not show an accounting loss overall. The accounts include a £69,540 investment revaluation gain and deferred tax increased from £94,389 to £121,235; stripping those out suggests, at most, a small underlying loss of about £12,000. ↩︎

On the (rare) occasions when these companies submitted full accounts, there was evidence of group relief. Sunley Holdings Limited’s accounts for 2017 and for 2019 show group relief surrendered and received. JMT Corporation Limited’s 2011 accounts show losses surrendered. However neither company filed full accounts in 2020 and so this doesn’t help us determine if losses were surrendered in 2020. ↩︎

This is sometimes done where for e.g. historic/tax/contractual reasons shares have to stay owned by one person/company, but it’s been agreed that actually all the benefit should go to someone else. In other words, it’s a way of executing a demerger without all the consequences of an actual demerger. ↩︎

The B shares were created on 13 October 2006, reclassifying 12,512 ordinary shares held by Richard Tice as B ordinary shares tracking all economic rights in Tisun Investments (defined to be “B Company Limited”). A 2010 resolution re-designated 3,713 D ordinary shares as B ordinary shares, ranking pari passu with the existing B ordinary shares. The structure was restated in new articles adopted in December 2014. Those articles again defined “B Company Limited” as Tisun Investments Ltd and preserved the same tracking rights over distributions and assets from that company. By the 2020 confirmation statement there were 16,225 B ordinary shares. The structure was then unwound in October 2020. A 16 October 2020 share-exchange resolution put Sunley Family Holding Limited above Sunley Family Limited. A 19 October 2020 dividend-in-specie resolution then declared a dividend on the B ordinary shares, satisfied by transferring the entire issued share capital of Tisun Investments Ltd. The result was that Tisun Investments was now in both the legal and the economic ownership of Mr Tice. ↩︎

HMRC’s CTM81121 example illustrates the same point: ordinary share capital can give the appearance of a group, but if the profit rights show someone else is the true economic parent, the group-relief relationship fails. ↩︎

A point of detail: on 19 October 2020, Sunley Family Limited transferred the issued share capital of Tisun Investments to Sunley Family Holding Limited by dividend in specie; the B shares remained so Tisun Investments did not join Sunley Family Holding Ltd’s tax group. Then on 20 November 2020, Tisun Investments was acquired by Tisun Holdco. ↩︎

A separate anti-avoidance rule in CTA 2010 Part 14, Chapters 2C and 2D (ss.676CB, 676CE and 676CH) also blocks pre-entry carried-forward losses from being surrendered as group relief for five years after an accounting period in which there is a change of ownership of the surrendering company. ↩︎

The deputy leader of Reform UK, Richard Tice, owns a property company – Quidnet REIT Limited. From 2020 to 2022 it paid around £600,000 of dividends to Mr Tice and his offshore trust. Quidnet was required by law to withhold approximately £120,000 of tax from those dividends and pay it to HMRC. But we believe it’s clear from the company’s accounts and public filings that Quidnet did not pay this tax.

Mr Tice has refused to answer the question directly, instead saying that he paid income tax on the dividends. That’s not an answer: the company was legally required to pay tax; the law doesn’t permit REITs to opt to defer their tax obligations.

The issue was first identified by Gabriel Pogrund of The Sunday Times – his report is here. Since the paper went to press we have conducted further analysis of the two last dividends, and so the figures in this report are higher than those reported in The Sunday Times.

Quidnet REIT

Quidnet REIT Limited is a property company controlled by Richard Tice, the deputy leader of Reform UK.

From 10 September 2018 to 9 August 2021, Quidnet was a REIT: an investment fund that invests in real estate. A company wishing to become a REIT has to apply to HMRC; the consequence is that the company then becomes exempt from corporation tax on its property rental business, but its investors are (broadly speaking) taxed as if they held the real estate directly. The logic is that a REIT is an investment fund, and the usual principle is that funds don’t pay tax; their investors do.

However, Mr Tice’s REIT was unusual: throughout its life, it was almost entirely owned by him and entities connected to him.

REITs are usually required to be widely held by different investors – they’re supposed to be genuine investment funds, not tax planning vehicles. The rules provide for a three year grace period in which REITs can become compliant but, as The Sunday Timespreviously reported, Quidnet REIT Ltd never attracted more than a small number of outside investors. Quidnet therefore ceased to be a REIT on 9 August 2021.

It’s unclear if real efforts were made to find outside investors – if they were not then we would regard this as aggressive tax avoidance which probably does not work technically.1 However this article is not about tax avoidance. It’s about what appears to be a simple failure by Richard Tice’s company to pay the tax that was due.

The tax Quidnet failed to pay

As a UK REIT, Quidnet was required to distribute at least 90% of its tax-exempt property rental profits to shareholders as “Property Income Distributions” (PIDs). This is essentially the quid pro quo for the REIT tax exemption – you have to pay profits to your shareholders, and the expectation is that (unless they’re exempt) they’ll be taxed on those profits.

But HMRC isn’t content to just wait for the shareholders to pay tax. That could be over a year from the date the profits were made. There’s also a risk that the investors would simply fail to pay tax on the dividends they receive. So, just as an employer is required to withhold PAYE tax when paying wages to its employees, a REIT is required to withhold basic rate income tax (20%) from its dividends, and pay it to HMRC. Dividends paid to UK pension funds (such as SIPPs) and UK companies are exempt from this withholding requirement. The Assura plc REIT has published a helpful summary of the rules.

Quidnet paid around £600,000 in REIT dividends, or PID components of dividends,2 to Mr Tice and his offshore trust3 – the RJS Tice Family Settlement.

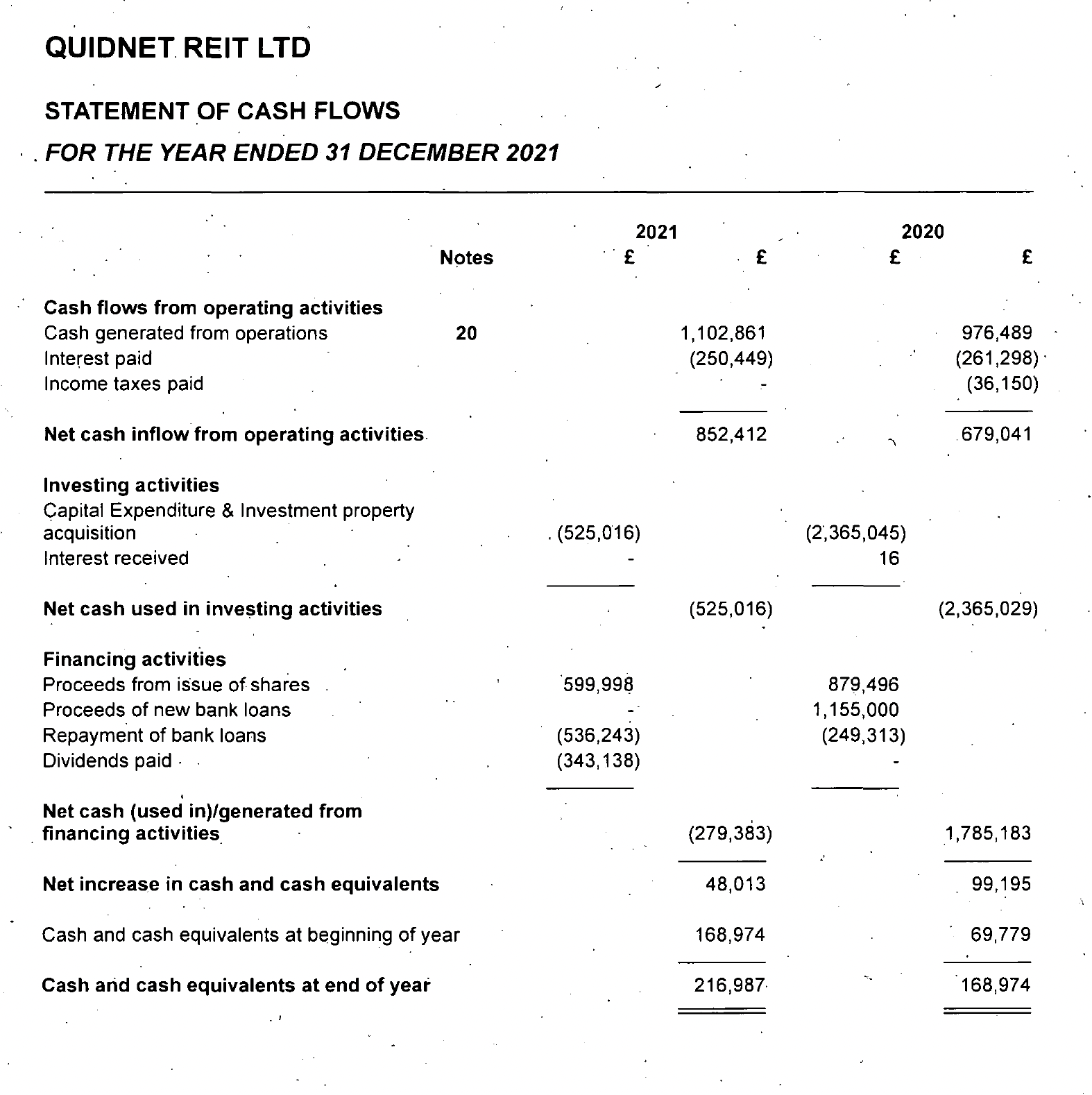

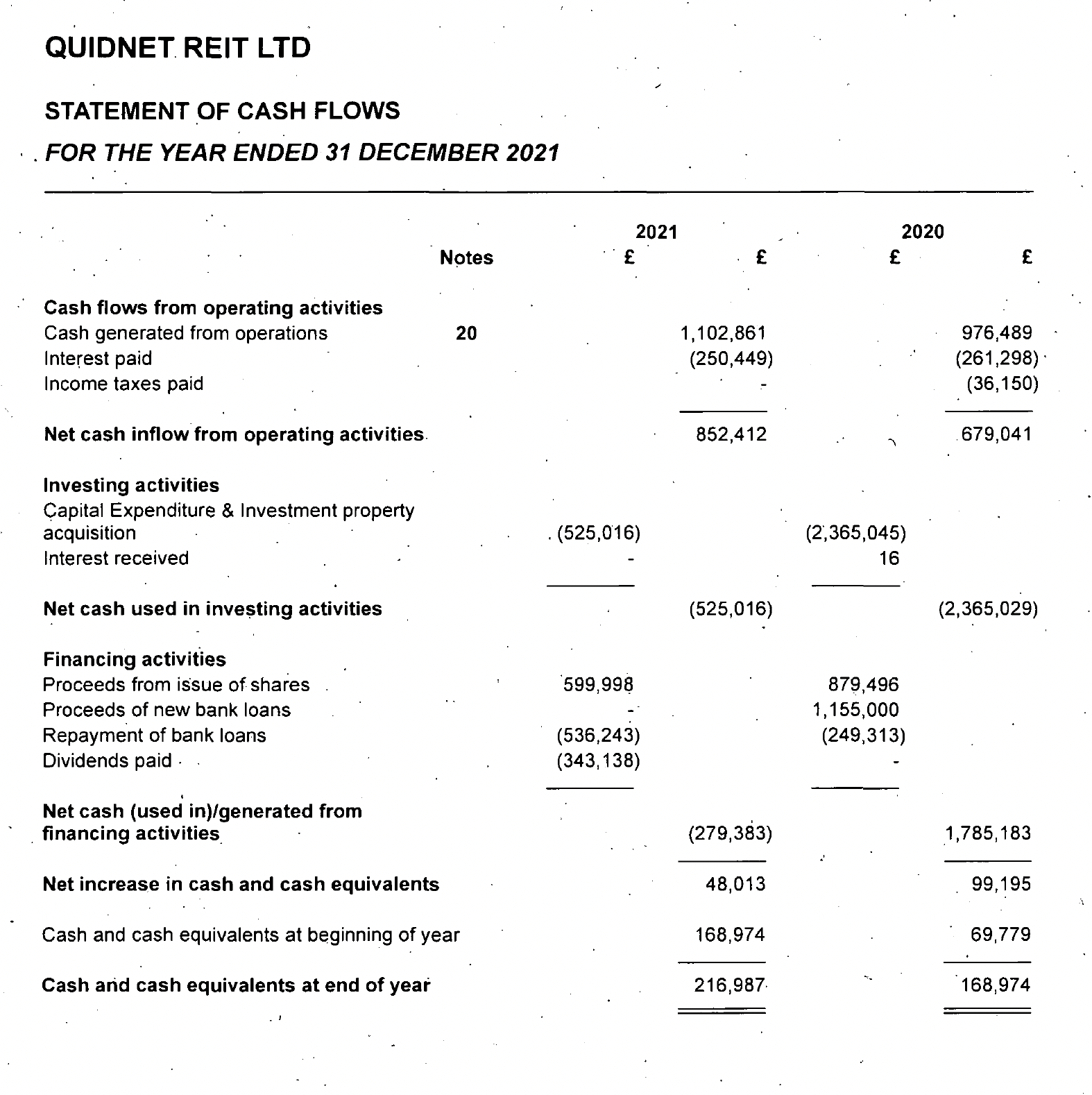

Quidnet should have withheld around £120,000 of income tax from these dividends, and paid it to HMRC. There is, however, no sign of this in the company’s cash flow statement – the tax should have been there (either under tax or dividends), and it isn’t:4

The “methodology” section below goes through a detailed analysis of how, independently from the accounting treatment, we can be confident that the company failed to withhold around £120,000 of tax.

The obligation for a REIT to withhold tax is well understood and (absent very unusual circumstances) we expect HMRC would say that the failure to withhold tax was careless. On that basis, HMRC would have six years to make an assessment and collect the tax5 plus interest and penalties.6

Richard Tice’s response

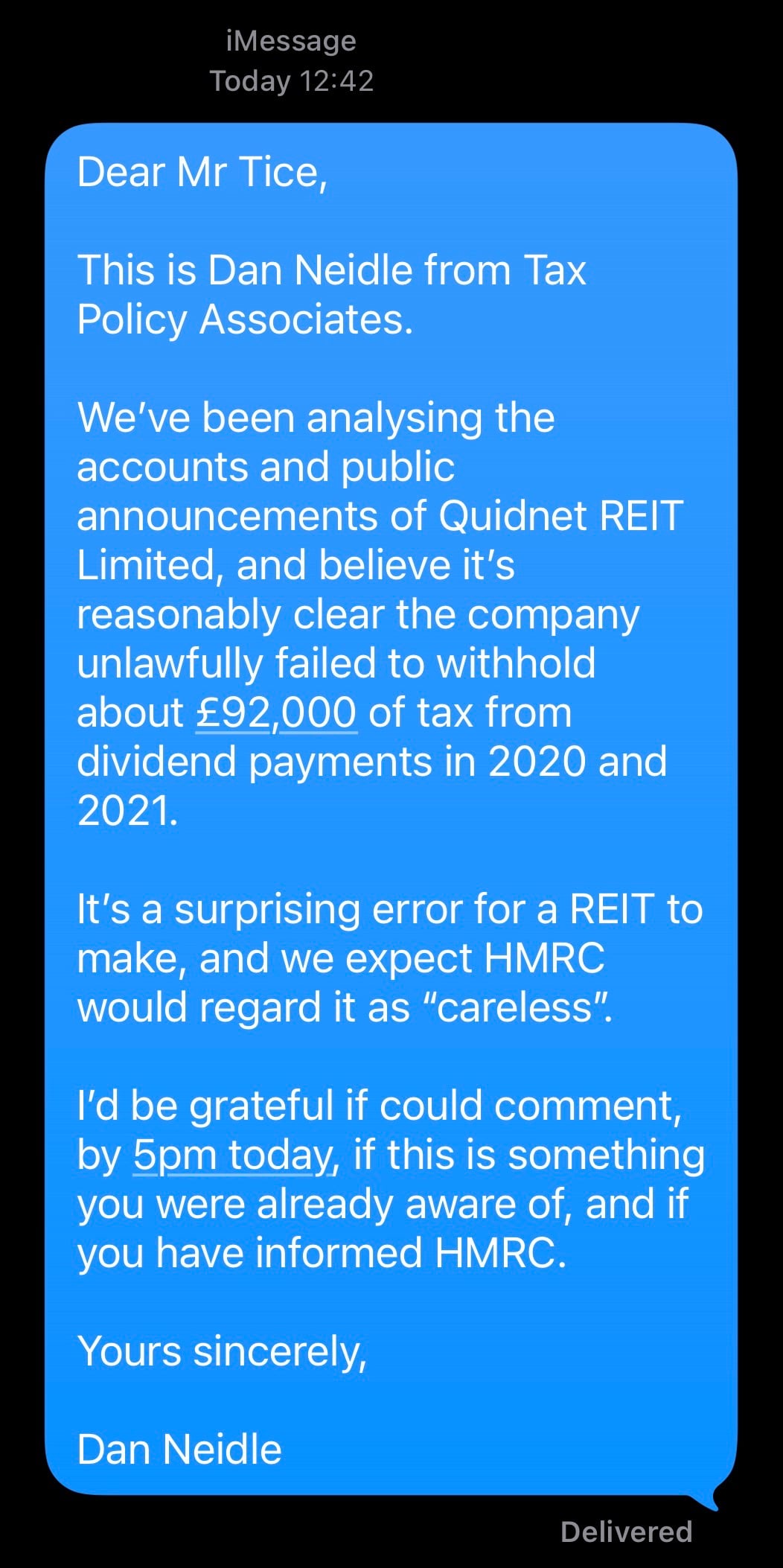

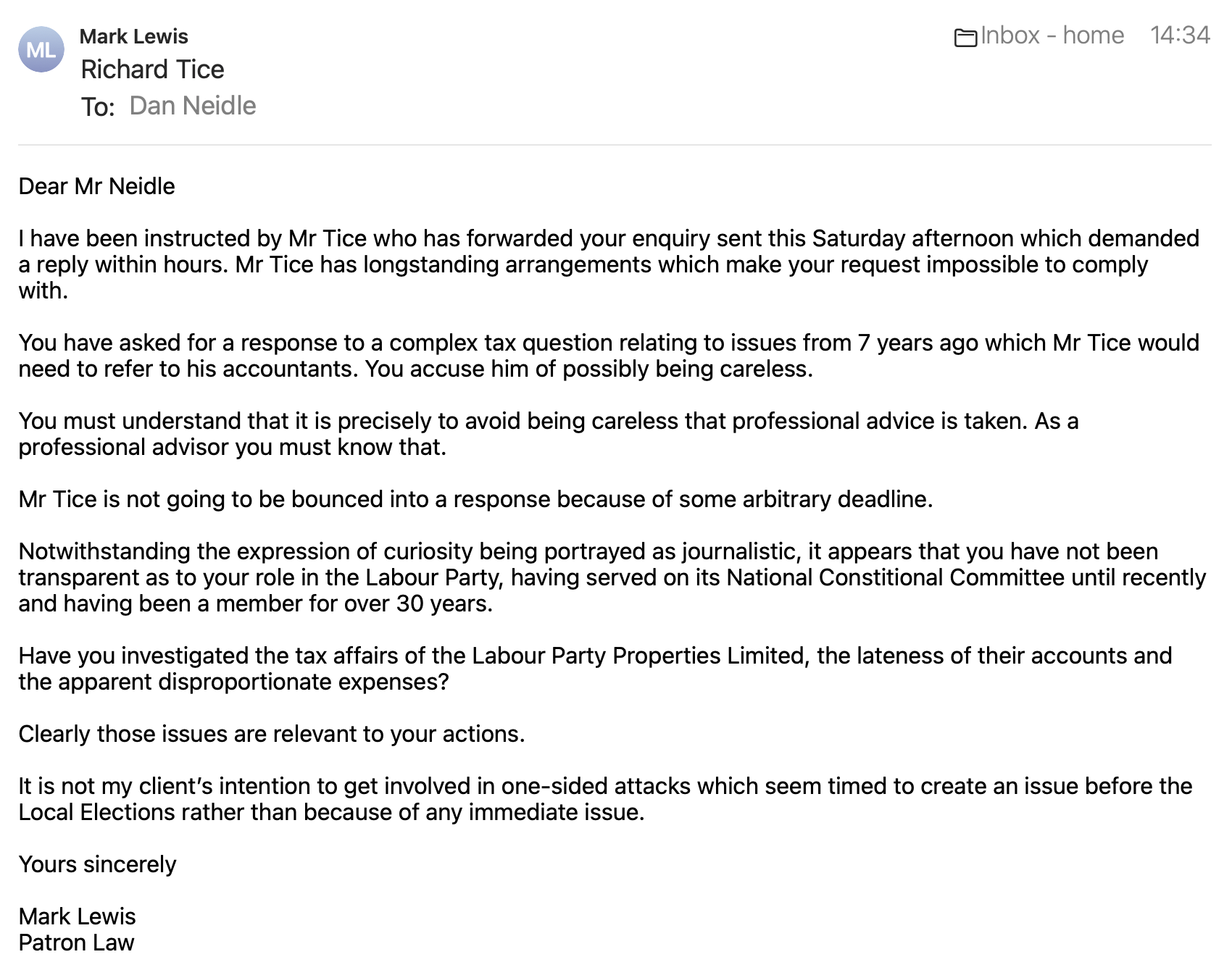

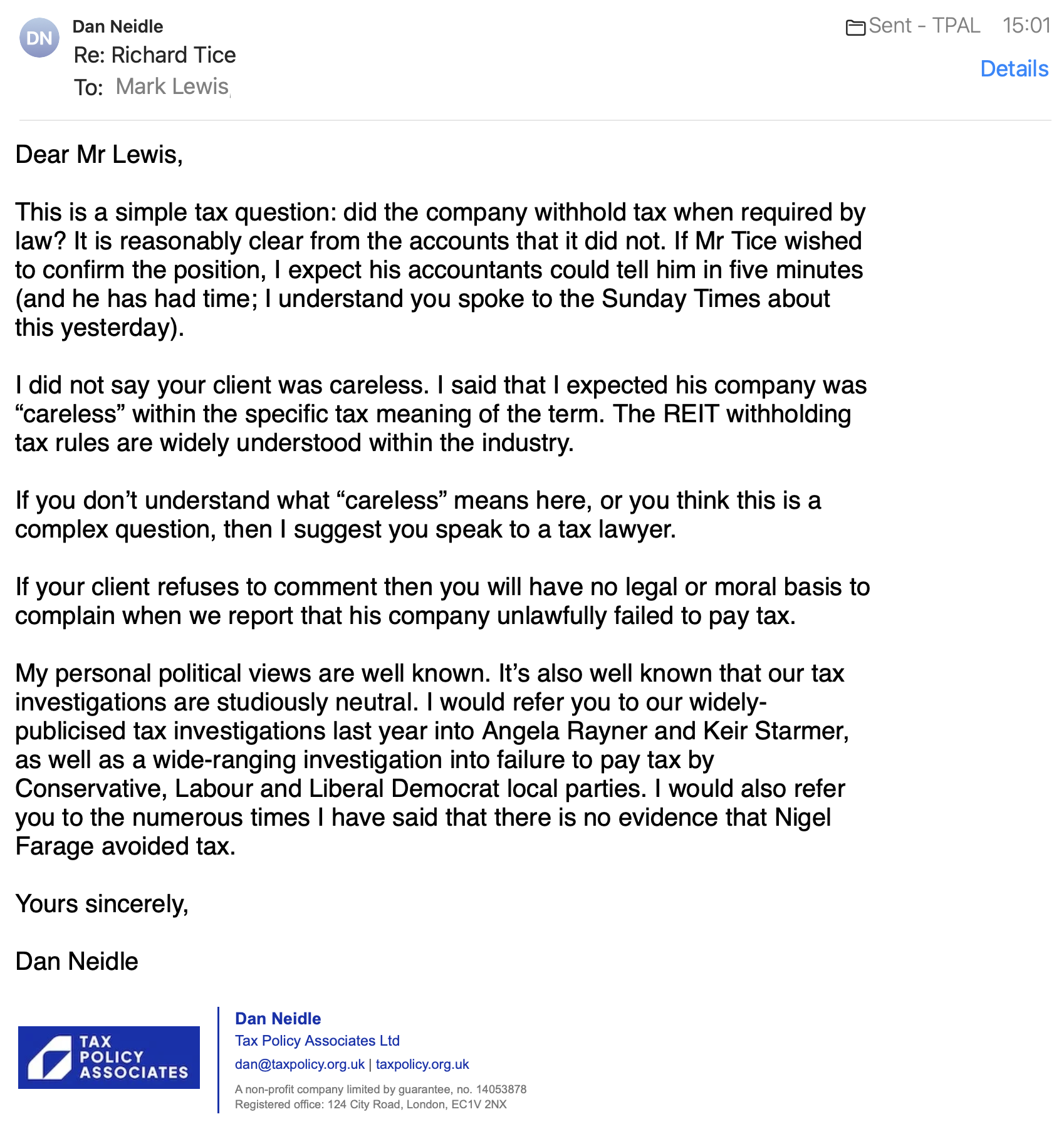

We wrote to Mr Tice seeking comment for this story. We received a response which failed to engage with the substance of the matter. Here’s our initial request, the response from Mr Tice’s lawyer, and our reply.

Tice, the Boston & Skegness MP, implied the failure amounted to a “technicality” and appeared to suggest it did not matter as he ultimately paid income tax on the dividends he received. He said: “I have paid all tax at the highest rate on all dividends received. HMRC has been paid in full.”

And then, shortly after we published this report, on X:

Mr Tice’s certainty that the correct overall amount of tax was paid is inconsistent with his solicitor’s complaint that Mr Tice hasn’t had time to refer the point to his accountants. And Mr Tice also doesn’t mention the Jersey trust – it’s unclear if the trust paid UK tax at all.

But the more important point is that, regardless of what tax was paid by Mr Tice and his trust, REITs and their investors have no choice how and when tax is paid. The law requires that a REIT withhold tax from its dividends immediately. It would be much more convenient for its shareholders if they could skip the withholding and wait to pay all the tax until they file their own tax return, up to 21 months later. The law, however, does not permit this. The law is also straightforward and, in our experience, well understood in the REIT industry.

It’s important to add that this was not tax evasion – a criminal offence – because there’s no reason to believe Quidnet’s directors or employees acted dishonestly – in our view that would be far-fetched. It was also not tax avoidance – an attempt to exploit a loophole. It was much more simple than that: Quidnet mistakenly failed to pay the tax required by law, and is now required to pay it.

Methodology

Many of the dividends in question were either paid by issuing new shares, or satisfied by issuing new shares. New shares are tracked in company records, and this gives us a second independent confirmation that there was a failure to withhold tax as required by law (in addition to the cashflow statement in the accounts).

The shareholdings

At the start of the period in question (July 2019), Quidnet had seven shareholders. Dividends paid to UK companies and pension funds are exempt from REIT withholding, leaving two shareholders subject to withholding tax on Quidnet’s dividends:

Richard Tice personally — 824,100 shares (15.36% of the total)

His Jersey trust — 1,033,598 shares (19.26% of the total)

Together they held 34.62% of the company’s 5,366,193 ordinary shares.7

The dividends

There were three types of dividends paid by Quidnet, and the 20% withholding tax rule applies to them all in a slightly different way:

Simple cash dividends Tax is simply deducted at 20%. So, for example, if a dividend of £100 is declared to an individual REIT shareholder, then £20 should be withheld by the REIT and remitted to HMRC, and £80 paid to the shareholder:

Diagram connections

Diagram connections

From REIT declares £100 cash dividend to HMRC (Label: £20 tax withheld)

From REIT declares £100 cash dividend to Investor (Label: £80 dividend)

Scrip dividends Instead of paying a dividend in cash, a company can pay a “scrip” dividend by issuing new shares to the shareholders.

A scrip dividend is subject to withholding in the same way as a cash dividend. So, for example, if a dividend of £100 is declared to an individual shareholder, and satisfied by issuing 100 shares worth £1 each, then the REIT should withhold 20 shares, issue 80 shares to the shareholder and pay £20 to HMRC.9

Diagram connections

Diagram connections

From REIT pays scrip dividend of 100 £1 shares to HMRC (Label: £20 tax withheld)

From REIT pays scrip dividend of 100 £1 shares to Investor (Label: 80 £1 shares issued)

For an example of how this is usually done in practice, see the bottom of page 3 of this document from LondonMetric Property Plc, and the worked example on the following page.

Dividend reinvestment plan

A company can declare a normal cash dividend but then satisfy it by issuing shares to investors, sometimes at the investors’ option (in which case it is often called a “dividend reinvestment plan” or DRIP). The end result looks the same as a scrip dividend, but legally it’s just a cash dividend followed by a share subscription. So, for example:

Diagram connections

Diagram connections

From REIT declares £100 cash dividend to HMRC (Label: £20 tax withheld)

From REIT declares £100 cash dividend to Investor (Label: Investor opts to receive 80 £1 shares instead of cash)

There’s an example here of how this is usually done – “the net dividend after tax is effectively reinvested by acquiring additional shares in the Company” (our emphasis).

The following paragraphs look in detail at the dividends paid out of REIT profits, and therefore subject to the withholding rules.

Dividend 1: FY2019 final (March 2020)

On 16 March 2020, the board declared a dividend of £684,055 for the year ended 31 December 2019. On the same day, it resolved to issue 423,040 new shares at £1.617 per share.10

The value of the shares issued — 423,040 × £1.617 = £684,055.68 – matches the gross dividend.11 This wasn’t a scrip dividend, but a cash dividend – satisfied in shares, with zero cash paid out.

If Quidnet had properly withheld 20% tax, it should have issued approximately 29,300 fewer shares and remitted around £47,364 to HMRC.12 Instead, shares were issued for the full gross value of the dividend – that provides independent confirmation (in addition to the accounts) that there was a failure to pay the correct tax.13

We can conclude that no tax was withheld from the £237,000 of dividends paid to Mr Tice and his trust, and £47,400 of tax was underpaid.

Dividend 2: H1 2020 interim (September 2020)

On 25 August 2020, Quidnet declared an interim dividend of 5p per ordinary share, to be paid on 21 September 2020 “by issuing shares at the new NAV per share of 155.1 pence”.

The announcement stated that “Shareholders are to receive 1 share for every 31.02 ordinary shares held”. A TISE announcement on 18 September 2020 confirmed that 186,627 shares settled the scrip dividend.14

This was a true scrip dividend. The conversion ratio is uniform for all shareholders — every holder gets 1 new share per 31.02 held, regardless of their tax status. If 20% had been withheld from non-exempt shareholders, the effective dividend would be 4p (not 5p) per share, and at an NAV of 155.1p this gives a ratio of 4/155.1 = one share for every 38.78 shares held.

Richard Tice received 28,661 shares worth about £44k. The trust received 35,947 shares worth about £56k. Both should have been subject to 20% withholding tax, but there’s no sign of that in the figures.15

We conclude that no tax was withheld from the c£100,000 of scrip dividends paid to Mr Tice and his trust, and around £20,000 of tax was underpaid.

Dividend 3: FY2020 final (April 2021)

On 17 March 2021, Quidnet declared a final dividend of 6p per ordinary share for the year ended 31 December 2020, with shareholders having the option16 to apply the dividend to subscribe for ordinary shares.

A small amount of this dividend was an ordinary dividend, not a property income distribution.17

By cross-referencing the share register18, we can determine that Richard Tice personally took this dividend in cash, receiving £55,000 cash, and the trust took the dividend in shares, receiving 40,145 shares worth £64,000.1920

Once again, the full gross dividend was distributed with no apparent deduction for withholding tax.21 The trust received about £64,000 in shares, of which approximately £62,500 was a PID from which £12,500 should have been withheld. Mr Tice received about £55,000 in cash, of which approximately £50,000 was a PID from which £10,000 should have been withheld. And again, there’s no sign of any tax being withheld in the company’s cash flow statement for 2021.

We conclude that no tax was withheld from the c£112,000 of PIDs paid to Mr Tice and his trust, and so about £22,500 of tax was underpaid.

Dividend 4: H1 FY 2021 (August 2021)

On 17 August 2021, Quidnet announced its interim results for the six months to 30 June 2021, and declared a further cash dividend of 5.5p per share, payable on 23 August 2021. Quidnet ceased to be a REIT on 9 August 2021. However this dividend was paid out of profits made when Quidnet was a REIT, and so we expect was fully subject to the REIT withholding tax rules.

To satisfy some of this dividend, filings show the company issued 132,212 new shares in late August at the newly reported net asset value of £1.613 per share.

Because we have the exact share counts from the July 2021 confirmation statement, we can calculate precisely what was owed and how it was paid. The trust held 1,191,173 shares, entitling it to a gross dividend of £65,515 (1,191,173 × 5.5p). If we divide the trust’s £65,515 gross dividend by the £1.613 share price, it equates to an allocation of 40,611 shares. Confirmation statements show the trust’s shareholding increasing by precisely that amount.22 This confirms the trust elected to take its entire 5.5p dividend as scrip, and that the shares were issued for the full gross amount, with no shares withheld for tax.

At that time, Richard Tice held 917,728 shares, entitling him to a gross dividend of £50,475 (917,728 × 5.5p). His shareholding remained unchanged after this; confirming he took his £50,475 dividend entirely in cash. Just as with the previous dividends, there is no evidence the company operated the required 20% tax deduction on this cash payment.

We conclude that no tax was withheld from the c£116,000 of dividends paid to Mr Tice and his trust, and so about £23,000 of tax was underpaid.

Dividend 5: FY 2021 final (10 May 2022)

On 10 May 2022, Quidnet announced a final cash dividend of 5.3p per ordinary share. This covered the period from 1 July 2021 to 31 December 2021. Quidnet was only a REIT for a small amount of that time. In principle the rules require withholding to be applied to such amount of that dividend as attributable to profits made during the REIT period. The accounts disclose total Property Income Distributions of 6.99p per share for FY2021; if the H1 2021 interim dividend was entirely a PID, that implies a PID element of 1.49p per share for this final dividend.23

On that basis, we estimate that the REIT rules applied to approximately £14,00024 of dividends paid to Mr Tice (received in cash) and £18,00025 of dividends paid to the trust. That’s a total of £32,000 – but there’s no sign of any income tax deducted in the accounts.26 It follows that £6,400 was underpaid.

Total tax at stake

Looking at the overall position:

Dividend Period

Type

PID paid to Tice and Trust

Unpaid income tax

FY2019 Final

Cash (Settled in Shares)

£236,810

£47,362

H1 2020 Interim

Scrip

£100,207

£20,041

FY2020 Final

Cash / Scrip Mix

£112,334

£22,467

H1 FY2021

Cash / Scrip Mix

£115,990

£23,198

FY2021 Final

Cash (accounts-based PID estimate)

£32,028

£6,406

TOTAL

£597,369

£119,474

The company’s accounts disclose Property Income Distributions of 12.75p per share for FY2019, 10.43p for FY2020, 6.99p for FY2021, and 0.00p for FY2022. Reconciling those figures to the dividend announcements produces the estimate above.

HMRC would be able to collect the £119,474 by a simple assessment. Whilst ordinarily a taxpayer receives a credit for tax that was withheld, Mr Tice is now out of time to claim an overpayment for 2019 to 2021. In a sense this is unfair – tax will have been paid twice. But Mr Tice established a structure in careful adherence to the letter of the rules in order to obtain a tax benefit. When you do this, HMRC tends to be unsympathetic to complaints of double taxation, and the courts have historicallyagreed. The courts have also held that HMRC has no discretionary authority to extend the overpayment correction period.

Disclosure

Dan Neidle, the founder of Tax Policy Associates, is a member of the Labour Party. Tax Policy Associates has no political affiliation. Our previous reports suggesting politicians failed to pay the tax due investigated Angela Rayner, Keir Starmer, Ian Lavery and Nadhim Zahawi.

Many thanks to Gabriel Pogrund of the Sunday Times, who discovered this story, and to K and M for the REIT and accounting analysis that underpins this report. Thanks to P for a forensic accounting redo/confirmation of the original figures (which moved them by a few hundred pounds).

Either because of the specific anti-avoidance rule in the REIT legislation or because of the general anti-abuse rule (GAAR). This announcement suggests that there may have been an attempt to technically meet the requirements, notwithstanding that the shareholders were all connected to Mr Tice, rather than an actual attempt to find genuine outside investors ↩︎

The accounts show that almost all the profits were property rental profits – see the “expected tax charge” line in the tax reconciliation. The accounts also explicitly disclose property income distributions of 12.75p per share for FY2019, 10.43p for FY2020, 6.99p for FY2021, and 0.00p for FY2022, as well as some much smaller ordinary dividends. After we published the first version of this report, we fully reconciled our conclusions with the declared PIDs; that has very slightly changed the numbers (a few hundred pounds). ↩︎

The cash flow statement does show £36,150 of “Income taxes paid” but that’s too small to be the tax that should have been withheld; we expect it was another item (the most common cause of REITs having a tax liability is failure to distribute 90% of their property rental profits, but there are several other ways tax can arise). Withholding tax could also be included in the “dividends paid” line, but the figures here are the same as the cash dividends (and so zero in 2020); there is no sign here either of any tax. ↩︎

If that results in double taxation, then it is possible (but far from certain) that HMRC would in practice not collect the tax (as that would result in economic double taxation); we expect that HMRC would still apply penalties. ↩︎

The original version of this report said that the usual penalties regime applied, meaning probably 15%. However that is likely incorrect; there is no specific tax-geared or daily penalty that applies to a failure to withhold tax. The position is probably that if Quidnet filed an incorrect CT61 then penalties are limited to £300 per return, or £3,000 per return if it was careless. So plausibly £15,000 overall. If, on the other hand, Quidnet did not file CT61s at all then the penalty is probably limited to £300 per return, so £1,500 overall. Daily penalties only start to run after notification from HMRC. This is a curious result and at some point it would make sense to bring withholding tax penalties in line with the usual penalty rules. ↩︎

The remaining shareholders were RJS Tice Family SIPP (36.04%), and NJG Tribe SIPP (1.75%) and three UK companies: Tisun One Ltd (9.21%), Tisun Two Ltd (9.19%), Tisun Three Ltd (9.19%). Another company, Tisun Four Ltd, was incorporated on 11 September 2020 and subscribed for 238,233 Quidnet ordinary shares on 21 September 2020, giving it about 3.38% of Quidnet by the July 2021 confirmation statement. ↩︎

The shareholder then gets a credit for the tax withheld, so overall the right amount of tax is paid, and the withholding tax is really just an advance payment. ↩︎

The authority for this is s973(3A) ITA 2007, which applies the usual rule that the cash value of a scrip dividend is treated as its “amount” for tax purposes. So when we apply the withholding rules, instead of withholding some shares and giving them to HMRC, the requirement is to hold a cash amount. That is by contradistinction with the “funding bond” rules, which (in a different context to a REIT) can require securities to be withheld and handed over to HMRC. ↩︎

These and other corporate announcements can be found on the Channel Islands stock exchange (The International Stock Exchange) website. ↩︎

If 20% had been withheld from the non-exempt shareholders (Tice 15.36% + trust 19.26% = 34.62% of the total), only ~393,700 shares should have been issued instead of 423,040. The difference of ~29,300 shares at £1.617 = ~£47,400. ↩︎

We can go further by reconciling share figures from the confirmation statements filed with Companies House, i.e. starting with share ownership figures in the July 2019 confirmation statement and adding in the shares that would have been received if tax had not been withheld; that equals the holdings we see in later confirmation statements. This confirms that Mr Tice and the trust received the gross number of shares – more on that below in the footnote to the second dividend. ↩︎

A further 567,051 shares were issued as new equity to fund a property acquisition. ↩︎

Perhaps the announcement was just sloppily worded and in fact tax was withheld and Mr Tice and the trust received 80% of the stated numbers? We can eliminate that possibility by looking at the change in Mr Tice’s shareholding from the July 2019 confirmation (when he held 824,100 shares) to the July 2021 confirmation (when he held 917,728 shares). That’s a difference of 93,628: exactly equal to the 64,967 shares he received for dividend 1 plus the 28,661 shares he received for dividend 2. So it’s clear that the shares were issued without any withholding. ↩︎

The announcement says that the option to subscribe was offered to shareholders who were directors or employees of the company; we believe this was loose wording and that Mr Tice’s trust also had this opportunity. Our reconciliation of share subscriptions shows that the trust did in fact subscribe for the shares. ↩︎

The accounts disclose FY2020 Property Income Distributions of 10.43p per share. Since the H1 2020 interim was 5p (entirely a PID), the PID element of this 6p final dividend was 5.43p, with the remaining 0.57p being an ordinary (non-PID) dividend not subject to withholding. We picked this up when, after publication, we reconciled our conclusions with the PID figures in the accounts. That results in slightly lower tax on this dividend, but slightly higher tax on the last dividend, with overall a change of just a few hundred pounds. ↩︎

Because his July 2021 shareholding of 917,728 is exactly explained by his original 824,100 shares plus the two 2020 pro-rata scrip allotments (64,967 + 28,661 = 917,728). He therefore received no new shares from this dividend. ↩︎

The RJS Tice Family Settlement’s holding increased by approximately 40,145 shares between the end of the H1 2020 interim dividend and the July 2021 confirmation statement — precisely matching scrip at the £1.602 issue price; i.e. no shares/tax were withheld. ↩︎

There is a small amount “missing” here. The trust had compounded its holdings to roughly 1,151,028 shares by this point, so a 6p per share dividend means it was actually entitled to a gross dividend of around £69,060. This implies the trust either took the remaining ~£4,760 in cash or there is a source of error we are missing. That’s not clear – so we will conservatively assume there was no cash dividend. ↩︎

The scrip shares (140,304 × £1.602 = £224,767) plus the cash (£168,246) total £393,013 — almost the same as the gross dividend of 6p × 6,542,911 shares = £392,575. ↩︎

It looks like Quidnet failed to file correct confirmation statements for 2022 and 2023, as they show no changes in shareholdings, but the July 2024 confirmation statement shows the trust holding 1,231,784 shares – i.e. a difference of 40,611 shares. ↩︎

We initially estimated it with a simple day-count; but we’ve now reconciled all the dividend numbers in the accounts and can be confident of the correct, higher, figure. ↩︎

Mr Tice’s holdings at this point were 917,728 shares. So 917,728 x 1.49p = £13,674. ↩︎

The trust’s holding at this point was 1,231,784 shares. So 1,231,784 x 1.49p = £18,354. ↩︎

The cashflow statement on page 14 of the 2022 accounts shows £69,095 of tax paid in 2022. That is almost exactly the same as the £69,098 of corporation tax shown on page 19. We conclude that no tax was deducted from dividends in 2022. ↩︎

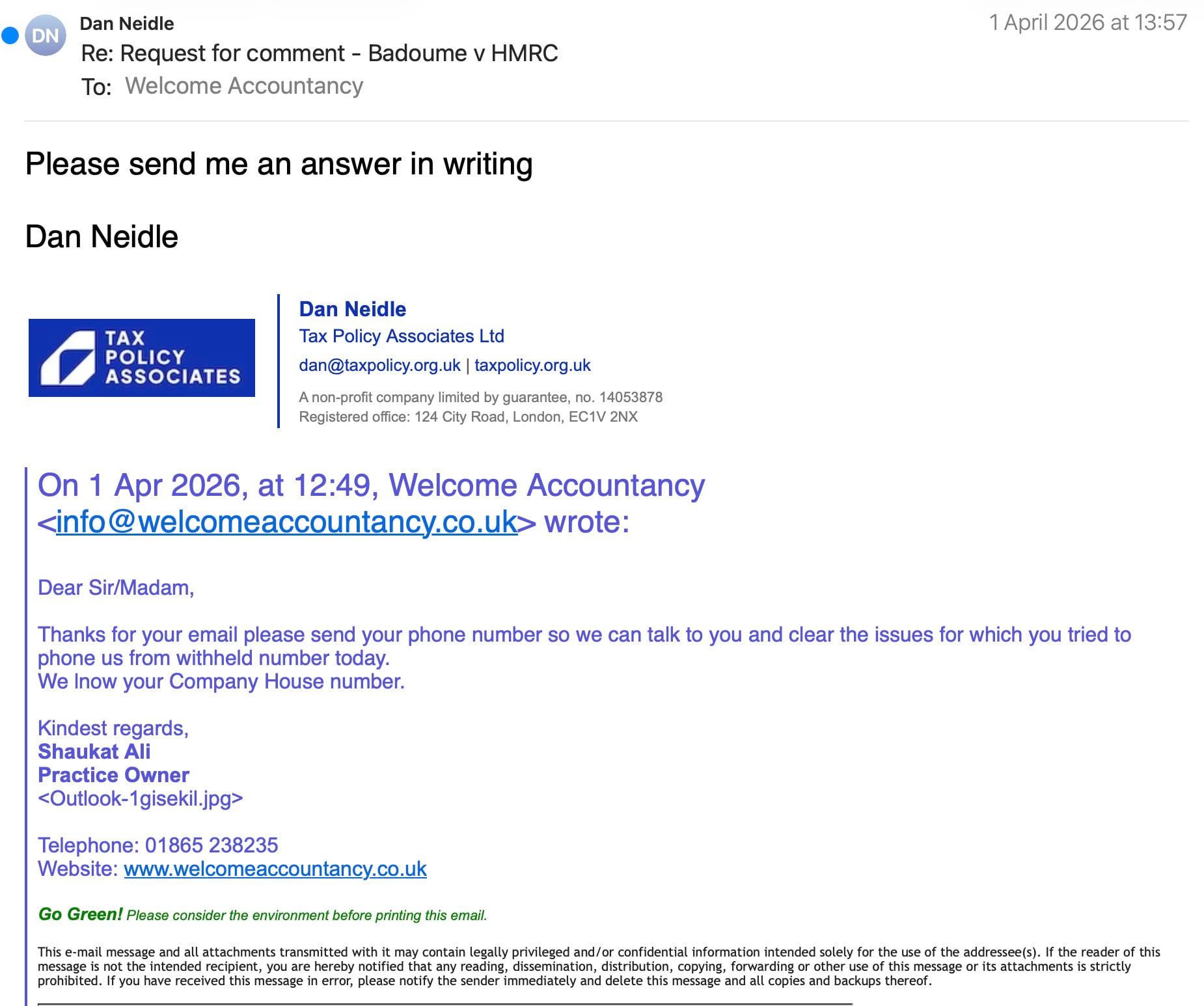

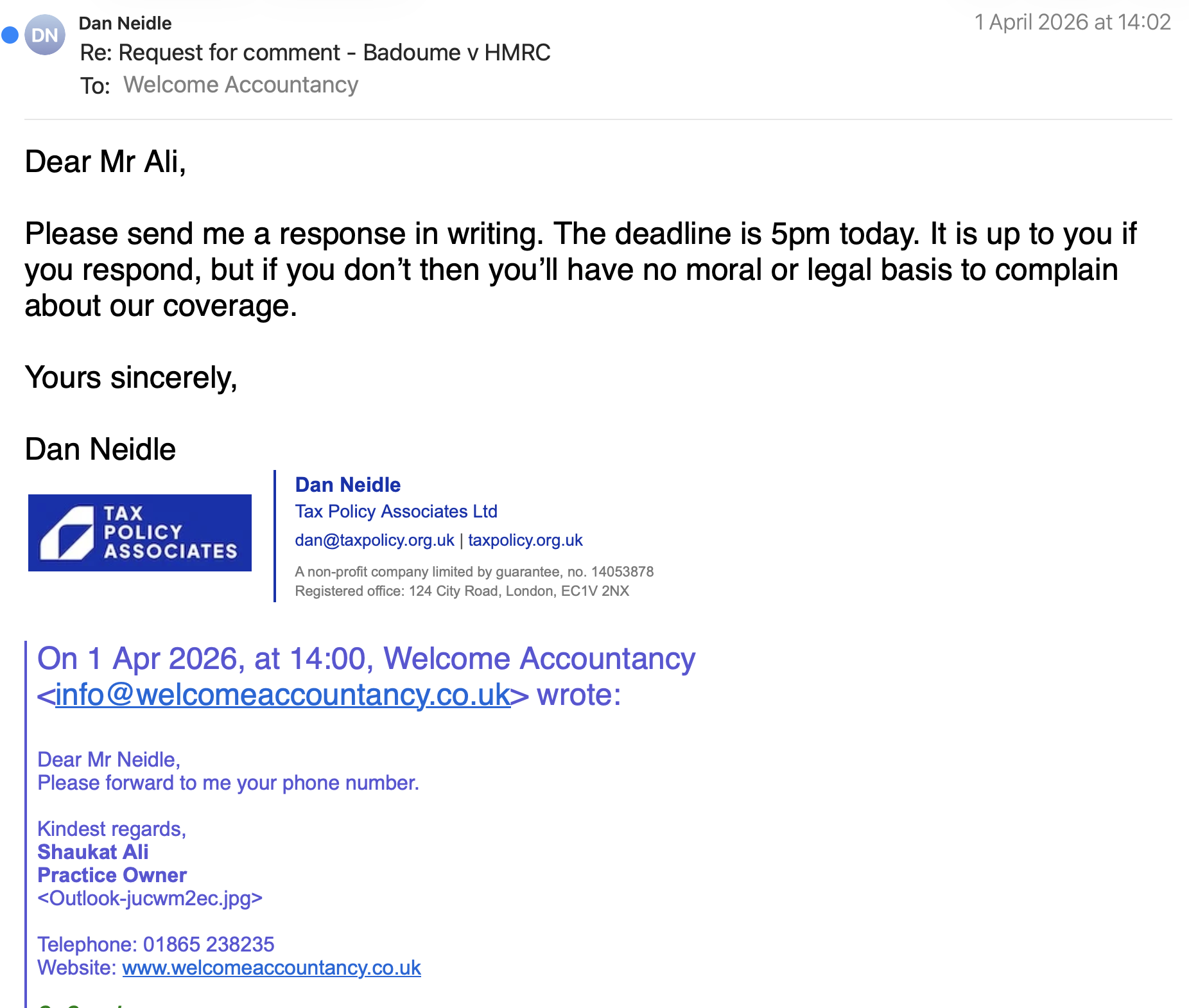

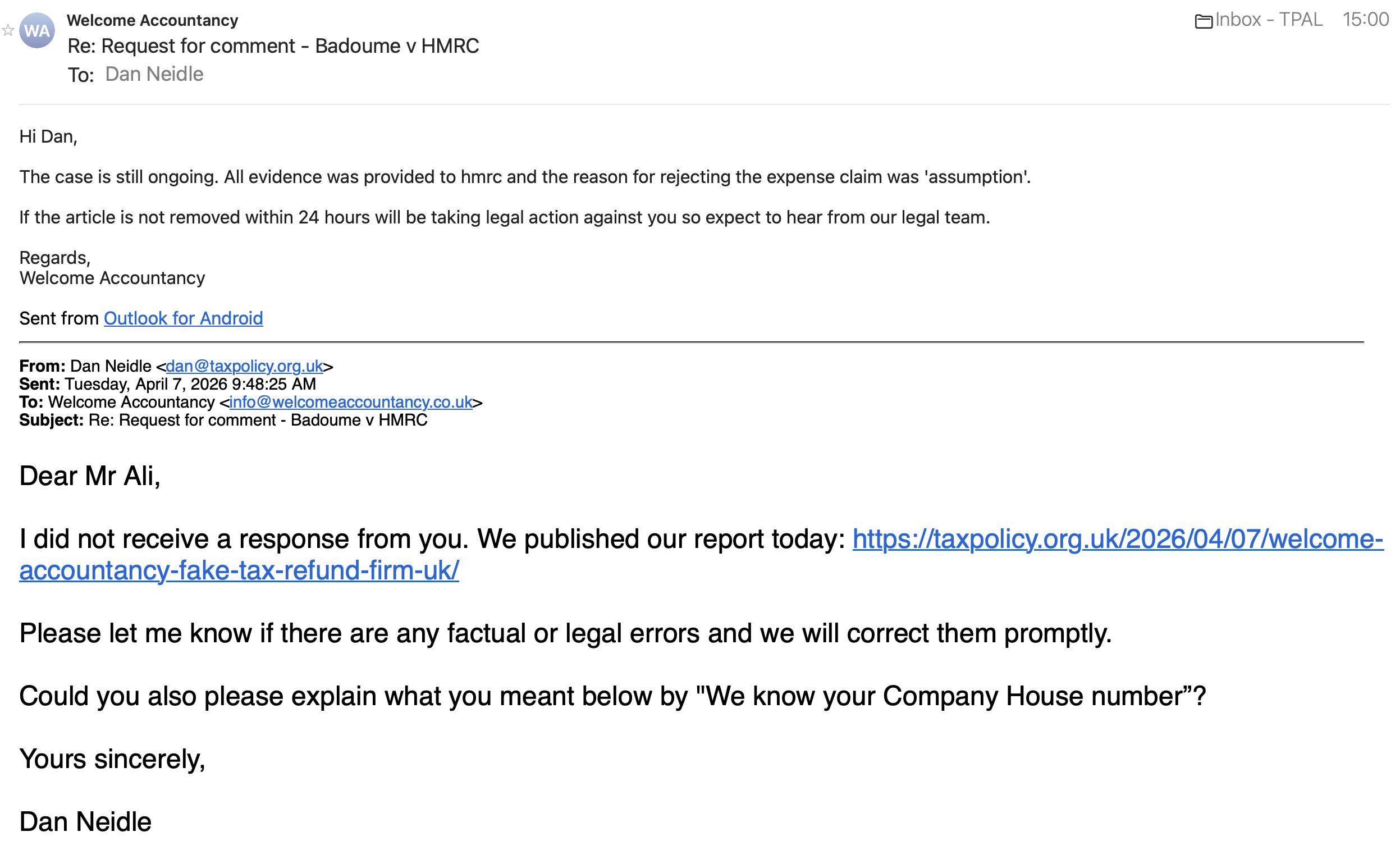

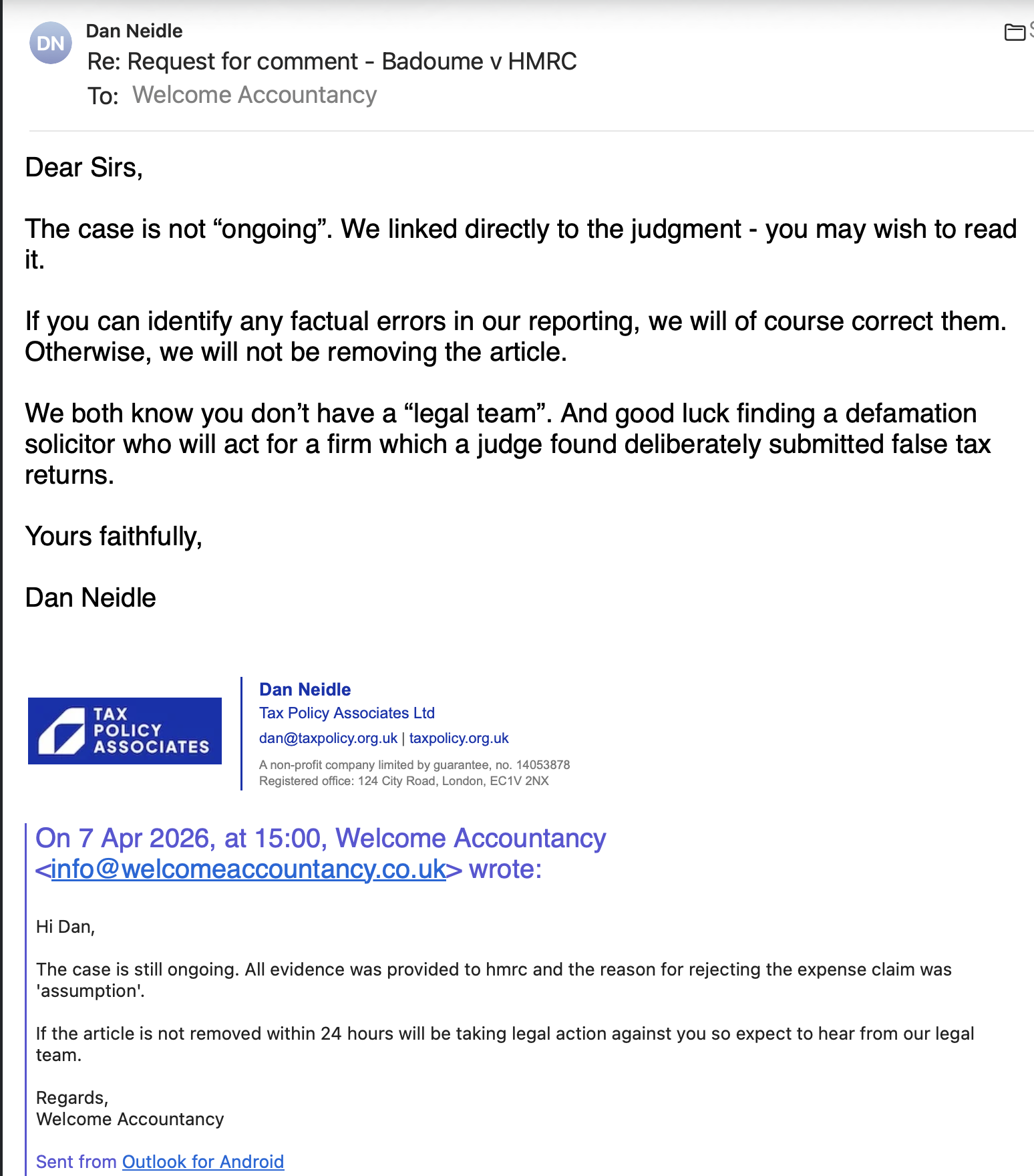

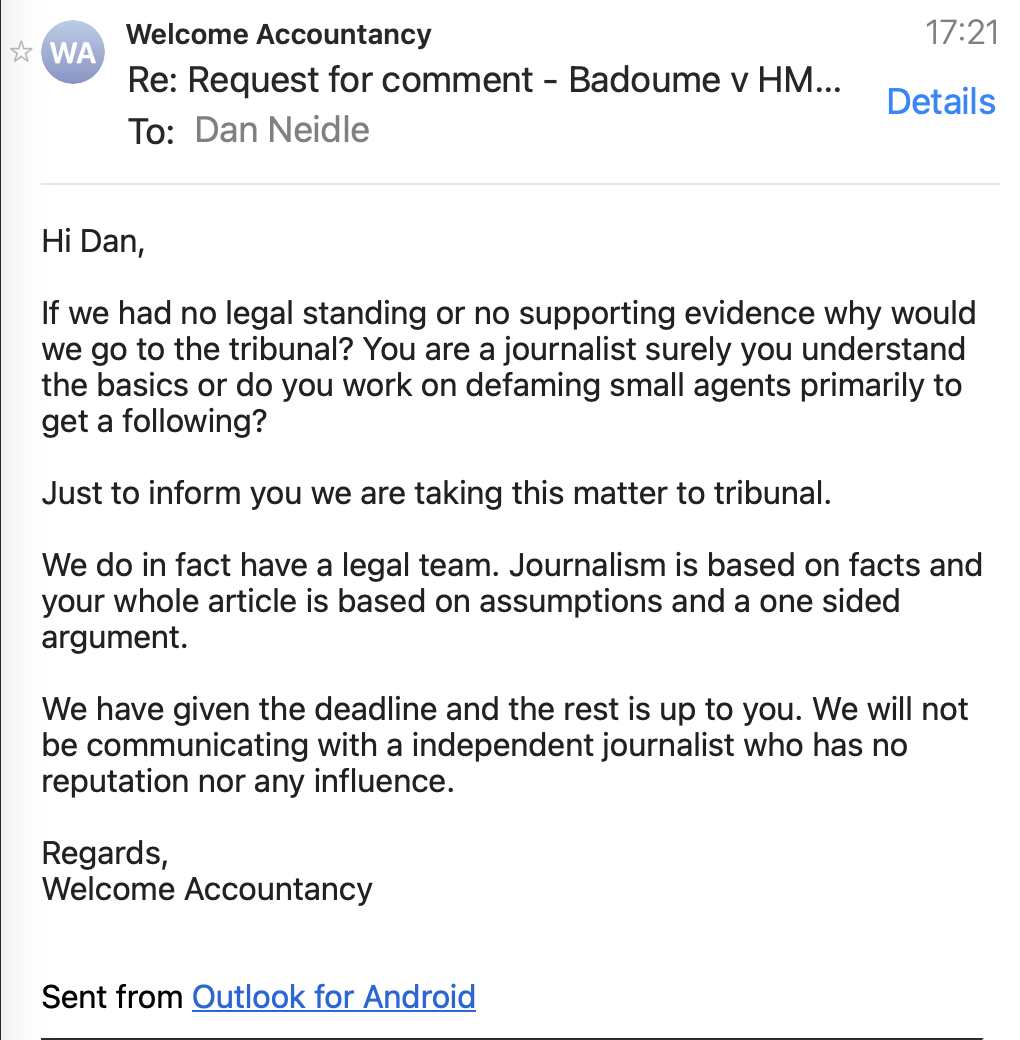

Updated 3.45pm on 7 April 2026 with Welcome Accountancy’s legal threat.

The internet is full of peoplepromising effortless tax refunds. For many, the business model is simple: invent expenses, file claims at volume, and take a cut. These “refund factories” exploit HMRC’s “process now, check later” systems, operating largely out of sight – but at a scale that may represent a material slice of the UK’s £47bn tax gap.

It is rare to see exactly how these schemes operate. Usually they remain hidden from view until a tax tribunal decision exposes what was done and how the claims were fabricated.

Until recently, the most notorious example was Apostle Accounting Ltd, the failed firm run by high-profile adviser Zoe Goodchild. A Tribunal last year found that Apostle had deliberately submitted a false tax return – and that Goodchild had reported her client to the police when he complained. This was no isolated incident – it’s been reported that Apostle made more than 800 false returns, shielded by vexatious criminal complaints.1

A reported case2 last week reveals another firm submitting fake tax refund claims – Oxford-based Welcome Accountancy.3

The current regulatory framework is visibly failing to stop firms like Welcome and Apostle. While new rules coming into force this year are intended to curb the abuse, there is a real risk they will miss the mark – imposing administrative burdens on normal advisers, while the fraudsters simply find a new workaround. We believe a better answer is aggressive enforcement, and the use of the criminal law. Bad actors will only stop when the personal risks outweigh the rewards.

The false claim

Yasir Badoume was an employee, paying tax on his employment income under PAYE. Employees can only claim a tax deduction for expenses in very limited cases. That, however, didn’t stop Welcome Accountancy Services.

In January 2020, Mr Badoume authorised Welcome Accountancy Services to act as his agent. Welcome then submitted tax returns for six tax years, claiming tax refunds for employment expenses. The refund claims were very large – in 2021-22 they claimed expenses of over £21,000 against income of £88,247, for supposed travel expenses, professional fees, other expenses and capital allowances.

This was implausible on its face. Employees don’t claim capital allowances.4

It was, however, initially successful: the returns generated tax repayments, made to Welcome Accountancy Services. We don’t know what proportion, if any, were paid to the actual taxpayer, Mr Badoume.5

This is often the problem with tax refunds – HMRC often grants the refunds automatically (sometimes instantly) and only checks them later. That is convenient for normal taxpayers making a genuine correction and refund claim; but it opens the door to bad actors.

In this case, HMRC opened an enquiry within the statutory deadline (a year from submission of the return) and assessed additional tax. Welcome Accountancy appealed, with the matter reaching a Tribunal last month.

More than negligence or incompetence

It is not a criminal offence to make a mistake preparing a tax return, even if the adviser is negligent or incompetent. This case, however, appeared rather more than a mistake.

When HMRC opened an enquiry into Mr Badoume’s tax return, they received this explanation from Mr Omar Ali, a partner at Welcome:

“By UK tax laws 20 percent of expenses6 paid by taxpayer are allowed to be claimed but if and where expenses are excessive, please amend the figures.”

As the Tribunal said, this is an “utterly false premise”. Indeed the Tribunal thought the suggestion was “so implausible” – particularly coming from a firm describing itself as certified chartered accountants – that it did not believe anyone at Welcome genuinely thought it was permissible.7

The Tribunal also noted the invitation to HMRC to “amend the figures” if they seemed excessive. As the Tribunal observed, “To a reasonable reader, this suggests that the representative himself had little confidence in the accuracy of the figures previously provided”.8