Robert Venables KC has a reputation for providing tax avoidance scheme promoters with convenient opinions that their schemes work. The courts usually disagree. But on one occasion he went further – in 2018 he promoted a loan charge avoidance scheme where his client was a company called “Citadel Limited”1. The scheme was promoted to desperate and vulnerable taxpayers by an adviser who later disappeared with his clients’ money. And what Venables didn’t add: he controlled Citadel.

We’ve previously reported on the “loan schemes” sold to taxpayers in the 2010s. The schemes replaced normal taxable income with “loans” from offshore trusts, supposedly avoiding all tax on wage income. The Government eventually killed these schemes with the “loan charge” – a harsh one-off tax on the value of all these outstanding loans.

The loan charge was announced in 2016 and would apply on 5 April 2019, in many cases creating six figure tax bills. So, by 2018, those affected were desperate to find a solution.

For some avoidance scheme promoters, this created an irresistible opportunity to sell schemes to make the loan charge disappear. None of these schemes had any prospect of working. In February 2017 and August 2017, HMRC had published “Spotlights” making clear their position that the only way to avoid the loan charge was to (genuinely) repay the loan. But that didn’t stop the promoters.

We’ve previously written about the loan charge avoidance scheme promoted by Douglas Barrowman’s company, Vanquish. Many others were playing the same game.

One was Robert Venables KC.2

The fraudster

Venables’ scheme was promoted via an individual called Phil Manley.

Manley had previously worked for HMRC in a largely administrative role, which he exaggerated, claiming to have technical expertise and inside knowledge of the loan charge. Manley claimed to have been the “tech lead responsible for finding the way to defeat” avoidance schemes (a role which doesn’t exist).

Manley used the Loan Charge Action Group⚠️ to boost his profile and gain clients. 3 Manley told clients he could save them from the loan charge, so they could ignore the upcoming 30 September 2020 HMRC settlement deadline. Just before that deadline, Manley abandoned his clients and fled the UK, leaving his clients in a very difficult position. Many have told me he took their money.4

It appears from this and other reports that Venables was working with Manley. Venables neither confirms nor denies this (see below). We believe Venables should have been suspicious that Manley was exaggerating his experience and expertise; other tax experts and laypeople drew unfavourable conclusions at the time from Manley’s behaviour and communications.

The scheme

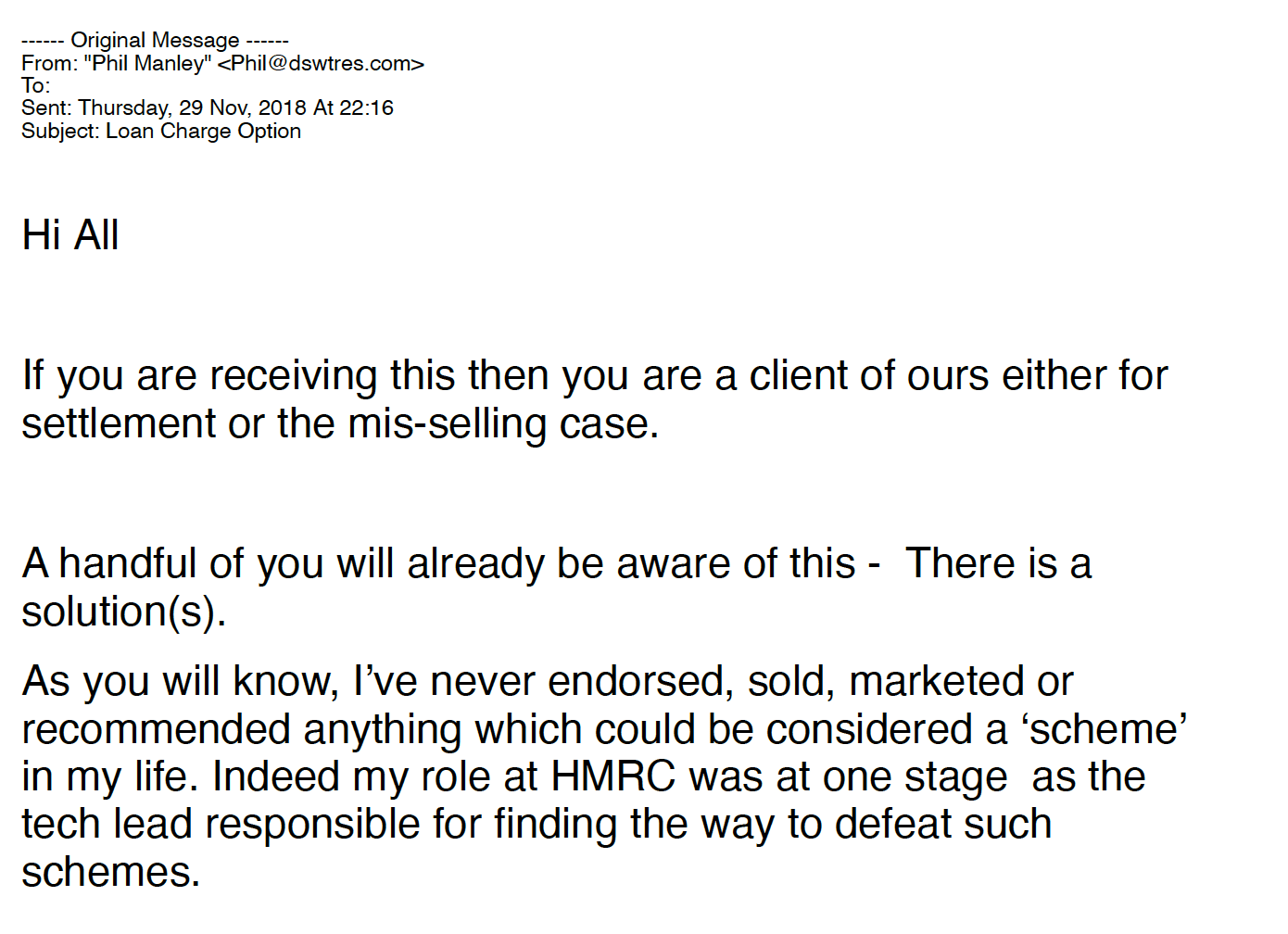

Six months before the report in The Times, Manley had sent this email to his clients: 5

Manley was, in fact, absolutely endorsing a tax avoidance scheme. Or, rather, two schemes – one for people who were employees, another for the self-employed:

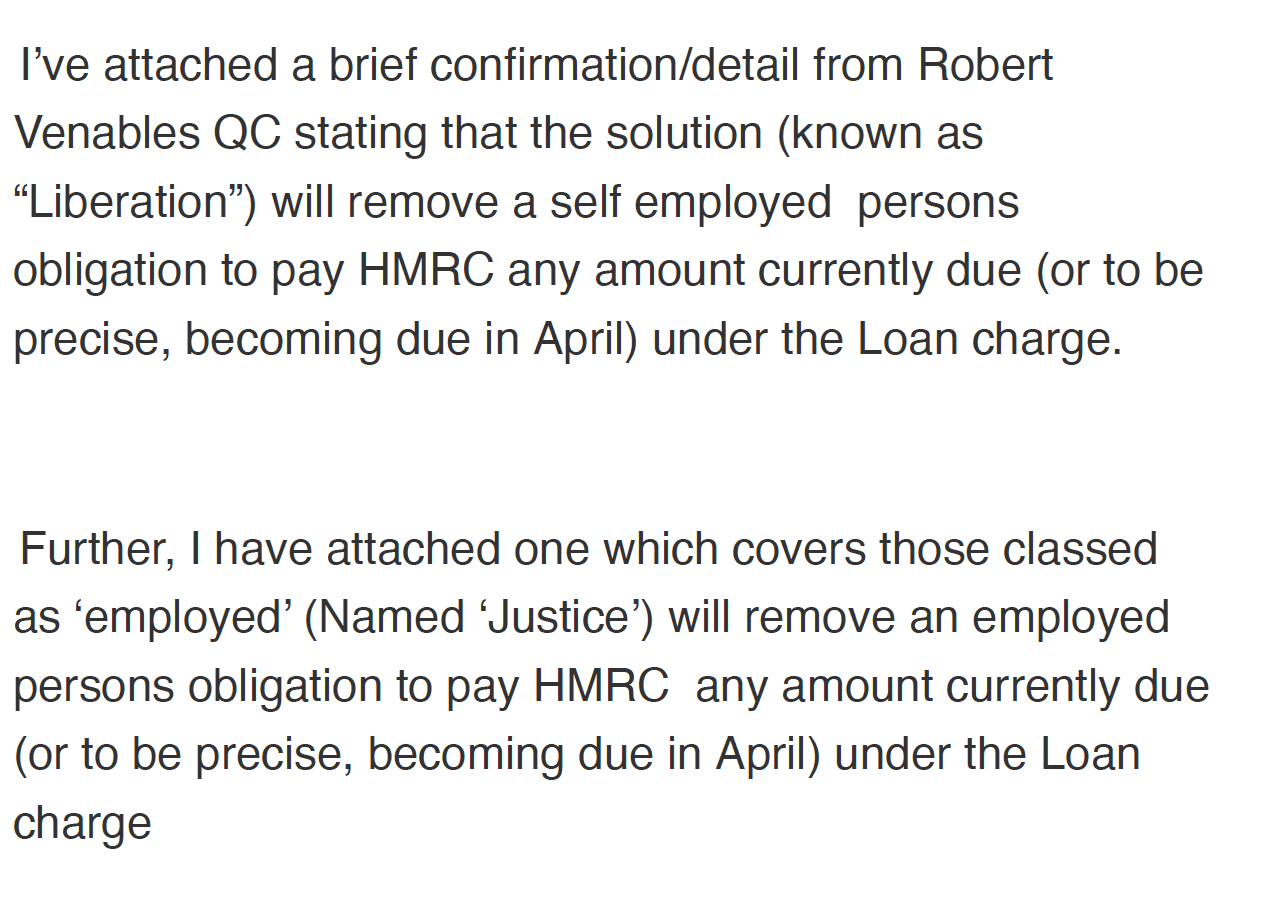

We’ve uploaded a copy of the “Justice” (employed) document here, and the “Liberation” (self-employed) document here.

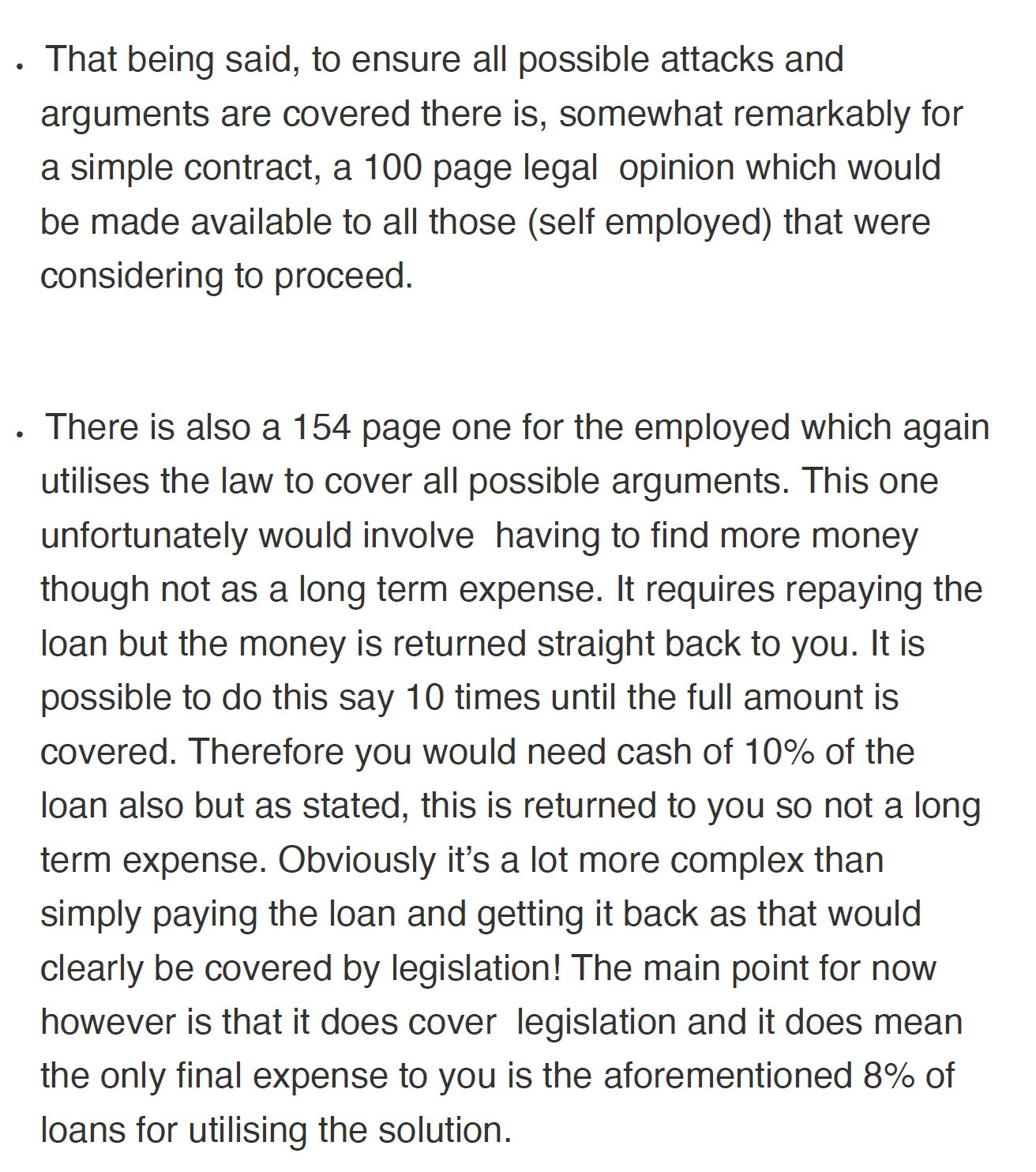

The email and the specification documents don’t set out the details of the scheme, but the concept was clear: pay 8% of the outstanding loans, and your loans – and the loan charge – would disappear:

And there’s then a clear sign in Manley’s email that this is very dangerous territory:

In the commercial world one sometimes sees lengthy tax opinions running to dozens of pages. These are for the largest and most complex transactions involving sophisticated multinational companies. Even so, a hundred page tax opinion would be highly unusual (none of our team can recall seeing one).

It is in our view extremely unwise for a normal individual to enter into an arrangement where the analysis is so complex that a 100+ page opinion is required.

The conflict of interest

The “Justice” and “Liberation” specification documents are peculiar.

This isn’t a case where a taxpayer client was approaching Venables with a structure, and asking Venables to independently advise on it. Venables (perhaps via Manley) was promoting a structure to taxpayers – vulnerable individuals who were desperate to escape the loan charge.

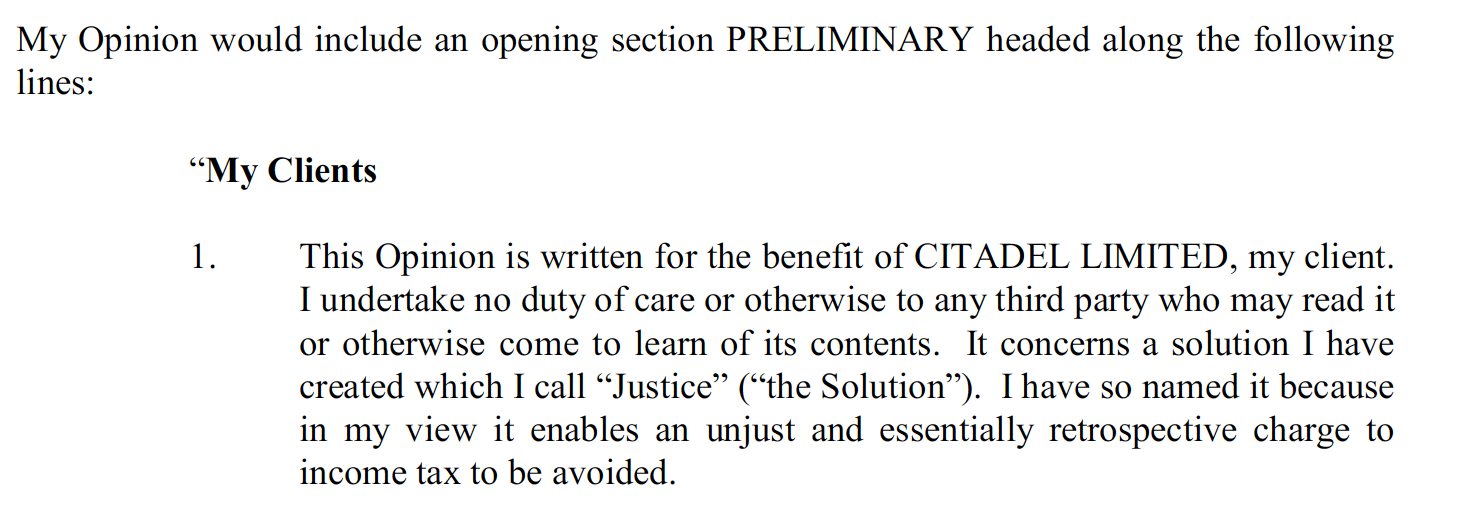

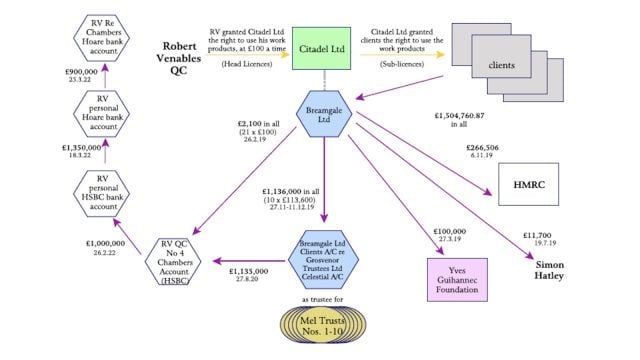

But those taxpayers weren’t Venables’ client. His client was “Citadel Limited”:

Citadel Limited is a UK company (with nothing to do with the well-known fund manager of similar name).

Who controlled Citadel Limited?

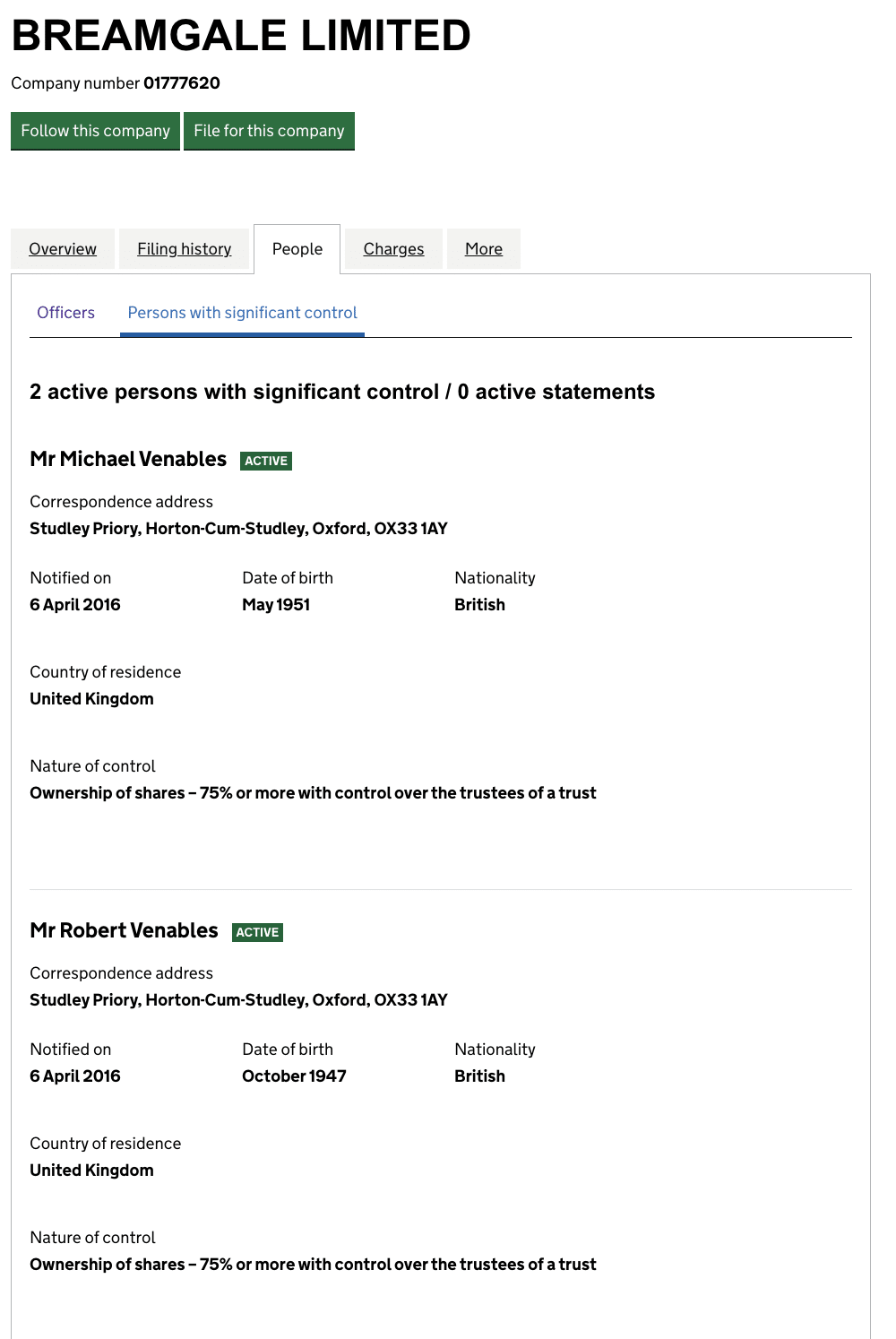

Robert Venables and Michael Venables, plus a company called Breamgale Limited:

Michael Venables is Robert Venables’ brother6 – he runs a specialist tax publishing company⚠️.

Who controlled Breamgale Limited? Again, Michael and Robert Venables:

Nowhere in the “specification” documents promoting the scheme does Venables disclose his interest in Citadel.

So it appears that Venables was selling an opinion to taxpayers, knowing they wouldn’t be able to rely on it, and without disclosing that he was closely connected to his actual client (to whom the taxpayers would be paying a fee).

We don’t know how many schemes were sold by Venables/Citadel, but Citadel’s accounts for the year to 31 March 2019 show £1.5m of profit.

The prospects of success

The consensus amongst tax professionals has always been that attempts to avoid the loan charge are doomed7.

So, whilst we don’t know the details of how Venables’ 2018 scheme was structured, we can be reasonably confident that it had no realistic prospect of success:8

HMRC “Spotlights” of February 2017 and August 2017 made clear that HMRC would challenge loan charge avoidance schemes. There were at least five ways HMRC could do this:.

- The loan charge applied to all loans outstanding on 5 April 2019. There were specific provisions in the loan charge legislation to prevent a loan being somehow eliminated without the loan being actually repaid in cash.

- These provisions were backed-up by a a targeted anti-avoidance rule (“TAAR”) that countered schemes that artificially “repaid” loans.

- Any attempt to release or write-off a loan would also potentially face a separate tax charge under the normal disguised remuneration rules (and perhaps under the normal rules for beneficial loans and general earnings charge as well).

- Since at least the early 2000s, the courts have lost patience with tax avoidance schemes; we believe there is only one, the SHIPS case, where the taxpayer has prevailed.

- After SHIPS, Parliament enacted a General Anti-Abuse Rule (GAAR) to counter schemes that no reasonable person could regard as a reasonable course of action. In our view it’s clear that entering into an artificial arrangement to defeat the loan charge (an anti-avoidance rule) was not a reasonable course of action, regardless of the detail of how the scheme works.

None of this requires the benefit of hindsight – the fact that loan charge avoidance schemes were doomed was obvious to professionals at the time Venables promoted his scheme in 2018.

Six years further on, as far as we are aware, every single loan charge avoidance scheme has either been abandoned or is the subject of an ongoing HMRC enquiry. Some of those promoting the schemes have been arrested for tax fraud – HMRC has said it is investigating 200 people for criminal offences relating to loan charge avoidance.

The Justice and Liberation schemes should have been disclosed under DOTAS, given that they were being mass-marketed and clearly had a main benefit of obtaining a tax advantage. We rather expect that they were not.

The problem with the Tax Bar

In 2014, Jolyon Maugham (not then a KC) wrote an article about the “Boys Who Won’t Say No” – the handful of tax KCs who had a reputation for issuing opinions that avoidance schemes would work.

Those opinions were vital for the promoters selling the scheme, as they could reassure clients that they had a KC opinion. However in practice these schemes were doomed, and had no real prospect of success – the clients would almost certainly lose their money. But the KCs knew that the clients couldn’t sue them, because the KC’s client was the promoter, who did just fine out of the scheme. And only the client can sue.

Ten years later, nothing has changed. Some tax KCs (it must be stressed, a small minority) still write highly dubious opinions for scheme promoters, knowing that the actual scheme users will have no recourse when (inevitably) the scheme fails.

The Justice and Liberation schemes appear to be an unusual and even worse case. Venables wasn’t just an adviser acting on someone else’s scheme – he was closely involved in the creation of the scheme and had an undisclosed interest in it. He surely knew that the scheme would be promoted to unrepresented and vulnerable individuals.

We don’t believe a solicitor would be permitted by the SRA to act in this way. The question is whether the Bar Standards Board will act.

A failure of regulation

The Bar remains the last outpost of cowboy tax advisers.

CIOT/ATT-qualified tax advisers and solicitors are required to adhere to the the “Professional Conduct in Relation to Taxation” (PCRT) guidelines.

The PCRT includes this key paragraph:

This is an important consumer protection for clients – any structure that sets out to achieve results contrary to the clear intention of Parliament will, given the modern caselaw, almost inevitably fail.

However, barristers are not required to follow the PCRT.9 They remain free to promote highly artificial and contrived schemes with no realistic prospect of success, secure in the knowledge that in practice they face no adverse consequences when the scheme fails.

There is a live Government consultation on regulating the tax profession and “improving standards”. The proposals will have no effect on the Bar, as it is already regulated.

Given the significance of KC opinions for tax avoidance schemes, this looks like a major omission. We will be writing shortly on our wider concerns with the consultation. In our view they will fail to curtail modern forms of tax avoidance, whilst imposing an unnecessary regulatory burden on people who have no involvement in tax avoidance.

Venables’ response

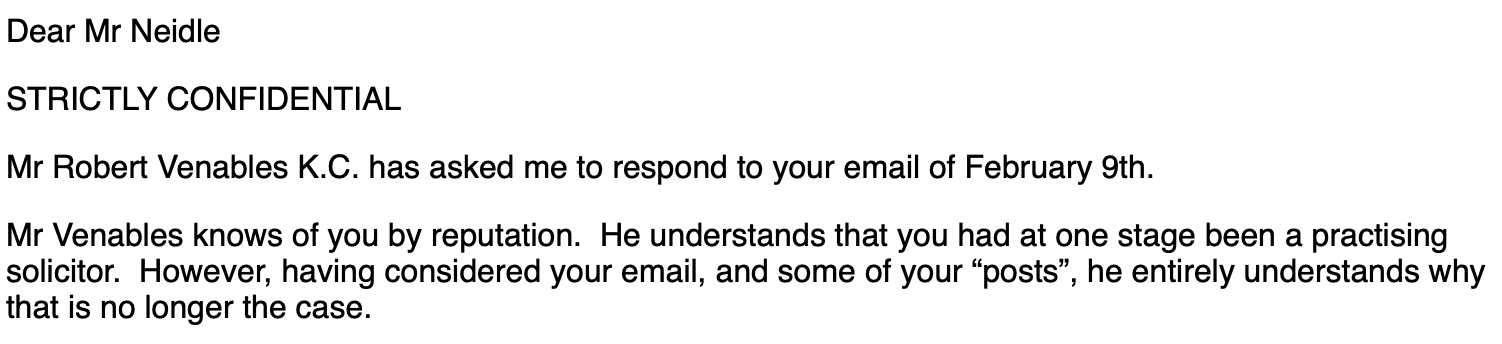

We wrote to Robert Venables KC asking for comment.

Venables’ response started with a rather childish insult…

… and then provided a series of highly specific statements which neither confirmed nor denied the points we had put to him:

Denial of promoting the scheme with Phil Manley

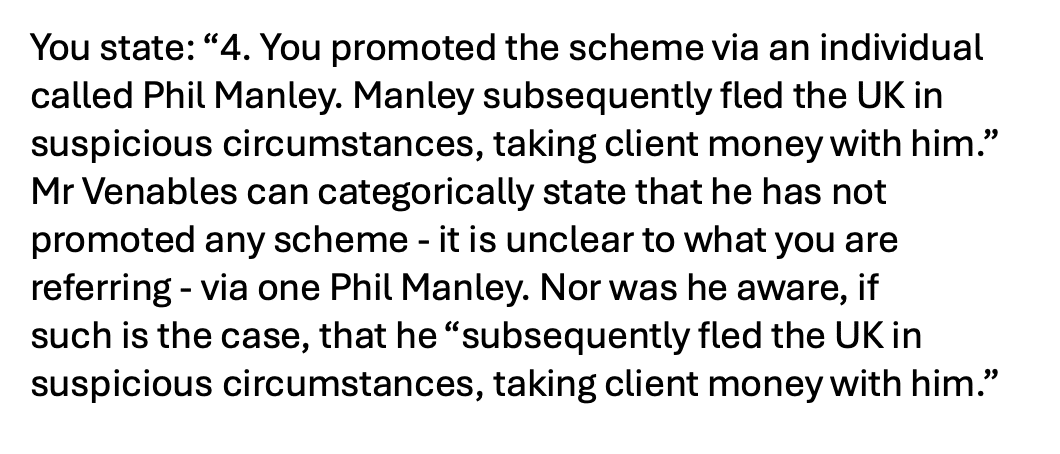

Venables categorically denied that he promoted the scheme:

It is, however, not obvious how this is consistent with the “specification” documents, which appear to be aimed at promoting the scheme to individual taxpayers. It is possible that Venables is using a particular meaning of “promoting”.

We asked Venables specifically if he caused the specification documents to be circulated to taxpayers; he declined to comment.

In his answer above, Venables seems to be trying to distance himself from Manley. We note the reports from 2019 that Manley and Venables were involved in a scheme to avoid the loan charge called “Insella” (confirmed by our discussions with contractors and by contemporaneous forum posts). It is surprising that Venables was unaware of these reports, and that someone following the loan charge as closely as Venables was unaware of the controversy around Mr Manley.

We gave Venables the opportunity to specifically confirm or deny that he worked with Manley, and that he caused the Justice and Liberation specifications to be circulated to taxpayers via Manley. Venables declined to comment.

Denial of ownership of Citadel

We asked Venables about the details of his scheme saying that – as Citadel was his company – usual considerations of client confidentiality shouldn’t prevent him responding.

Venables’ response was to distance himself from Citadel:

The implication is that Breamgale is a trustee for some unknown third party, who holds the beneficial interest in the Citadel shares. That is consistent with Breamgale’s PSC disclosure. But it doesn’t explain why Venables has been listed, at all times, as a PSC of Citadel Limited, and that unknown third party has not been.

We asked Venables to explain this; he declined to comment.

However, in our view whether or not Venables holds a beneficial interest in Citadel is not the key question. Even on Venables’ account, he still controls the company (unless his Companies House filings were incorrect). And that was not disclosed to the taxpayers receiving the scheme proposal.

Denial of a duty to disclose

Mr Venables doesn’t think there’s anything improper about marketing a scheme to unrepresented individual taxpayers without disclosing his links to Citadel:

And:

This is a very narrow view of a barrister’s duties, which go beyond the narrow duty to the barrister’s own client. In our view, the BSB’s requirements of honesty, integrity and independence preclude a barrister from promoting a tax scheme to unrepresented individuals without disclosing that he personally, or persons related to him, will benefit from the fees that they pay.

Claim of confidentiality

Venables’ email to us was headed “strictly confidential”. We asked what the basis was for claiming confidentiality, and received this response:

That is not how the law of confidence works.

We are publishing the correspondence in full here.

Many thanks to M, J and C for technical remuneration tax input, and to B for advice on barristers’ professional standards. Thanks to Simon Lock for the genealogical research, and thanks to all the contractors who provided us with background on Messrs. Venables and Manley.

Footnotes

Unrelated to the well-known Citadel, the fund manager. ↩︎

Venables’ reputation as a provider of avoidance opinions is hard to prove from publicly available sources, as the opinions he issues are rarely public. One exception is the Hyrax case – see in particular paragraph 80 of the judgment. Venables provided an opinion the structure wasn’t disclosable to HMRC under the DOTAS rules. The tribunal had no difficulty coming to the opposite conclusion. ↩︎

After Manley’s activities were reported in The Times in April and then June 2019, Ed Davey wrote on behalf of the All-Party Parliamentary Loan Charge Group⚠️ saying Manley “hadn’t promoted tax avoidance schemes” and never had a formal role with the APPG or the Loan Charge Action Group. Manley clearly had promoted tax avoidance schemes. He may never have had a formal role, but Manley accompanied Davey on meetings with HMRC, and worked with the LCAG on their input to the Independent Loan Charge Review. Both bodies were at best naive in giving prominence to someone who was fairly clearly not an expert in the matters he purported to advise on. It’s hard to understand why Davey then defended Manley. ↩︎

The only explanation provided by Manley was that HMRC had “thrown [him] under the bus”. It is unclear what was meant. Some of Manley’s former clients believe he was delusional enough to think he could persuade HMRC/HMT to drop the loan charge, and he fled upon realising that this would not happen. Others believe he was a fraudster from the start; that seems plausible to us, given the gulf between Manley’s claims and his actual expertise. ↩︎

It is possible that the schemes discussed in this report were in fact “Insella”, or changed into “Insella”. It is also possible they were different schemes. How many schemes Venables and Manley promoted is an interesting question, but only of limited relevance to the matters discussed in this report. ↩︎

We weren’t sure about this when we first published this report, but are now reasonably confident they are brothers thanks to birth registration index data. Michael and Robert share a place of birth and mother’s maiden name, and the father owned a company now owned by Robert and Michael Venables. Many thanks to Simon Lock for the research on this. ↩︎

See for example Pett on Disguised Remuneration at 15.6 ↩︎

Just as if someone claimed to have a scheme which eliminated an employee’s tax on £100k of PAYE income then we would be reasonably confident that the scheme would fail, without knowing the details of the scheme. ↩︎

Unless they are also CIOT or ATT regulated, which most are not. ↩︎

Robert Venables, senior tax KC, is being prosecuted by HMRC for tax evasion

The Venables prosecution

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Tax barristers and fraud: how the Bar responded to our allegations

Leave a Reply