The UK has 90 taxes.1 This chart shows them all, and this article explains why we have so many.

Update 29 May 2026: the Exchequer Secretary to the Treasury responded to this article by pointing out that the Government had just abolished bingo duty, folded diverted profits tax into corporation tax, and ended the pseudo-tax shadow ACT.

The chart is interactive: click on a segment or category to drill down. The control underneath switches between pounds, % of GDP and % of all tax take.

Data is for 2024/25, and the full methodology is below.

It’s immediately clear how dependent we are on taxes on employment.2 The UK is pretty typical here – all OECD countries have a similar dependence on taxes on employment (excepting very small and/or oil/gas rich countries).

Those taxes, together with VAT and corporation tax make up about 3/4 of all tax revenue – which is why Labour’s decision to rule out increasing any of those taxes was so unfortunate, given they clearly intended to put up tax.

Note that there are only 81 taxes visible on the chart3; the other nine can’t be seen, because they don’t currently yield any revenue.4

The obvious question is: why do we need so many taxes?

Part of the answer is sensible. Different taxes do different jobs. We tax income, consumption, business profits, property, capital gains and environmental harms because we want to tax these different things differently. Some taxes are deliberately behavioural: we tax tobacco, alcohol, gambling, landfill and carbon emissions not just to raise revenue, but because we would like less smoking, drinking, gambling, dumping and emitting.

But that only explains some of the chart. The rest is politics. Governments create small targeted taxes because they sound painless: a levy on banks, a surcharge on banks, a duty on shares, another duty on shares, a levy on this sector, a charge on that activity. Each one had a speech and a press release. None had a repeal date.

So the UK tax system is not really a designed object. It is a very long-running game of Jenga, where each generation of politician carefully adds new taxes and new tweaks to the top of the pile, and rarely does anyone dare to touch the horrors lurking lower down.

Perhaps the oddest of the UK’s many tax oddities is bearer instrument duty (BID). It’s a tax on instruments that don’t exist any more, never applies in practice, and raises no revenue. It looked like BID was finally going to get the axe last year – but still it survives. If they can’t abolish this sorry historical relic, then there’s little prospect of any serious reform.

Nigel Lawson used to pride himself on abolishing one tax every year. Rachel Reeves would shock everyone if she did the same – but it probably wouldn’t cost one penny of tax revenue.

Methodology

The starting point for the chart is the Office for Budget Responsibility’s March 2026 forecast for 2024-25 “National Accounts taxes”: £1,013.286bn, or 34.536% of GDP. Our chart treats the £58.870bn of VAT refunds as reducing VAT, rather than (as the OBR National Accounts do) having a higher amount of VAT and then a deduction. So our total is £954.416bn compared to the National Accounts’ £1,013.286bn.

The GDP denominator is OBR nominal GDP for 2024-25: £2,934.021bn.

We use 2024-25 because it is the latest complete OBR outturn year with a full all-tax taxonomy. There are newer monthly figures from ONS and HMRC, but they are either provisional, cash-basis, or less convenient for a complete map of the tax system.

The underlying numbers are official, but there is no single official “right” way to group taxes. So the classification is ours, constructed to be helpful, and group taxes by the thing being taxed: employment, asset income, consumption, business profits, property, wealth, environmental externalities, and so on.

Income tax on dividends and savings interest is taken from HMRC’s Table 2.6 Income Tax liabilities by income source, scaled to the OBR income-tax total used in the chart. Income tax on rents is estimated from HMRC’s Table 3.7 property-income distribution by total-income band, applying broad 2024-25 non-savings income tax rates.

Some lines are awkward in a sunburst chart. Negative receipts, such as petroleum revenue tax repayments and some income-tax repayment lines, are netted into their parent totals rather than displayed as positive slices.

A few tax-like receipts, such as the TV licence fee, some regulatory levies, and visa charges are included because the OBR includes them in National Accounts taxes (they are “unrequited“). There are some surprising entries in that category – ATOL (the £2.50 compulsory, per-passenger fee paid by travel operators for flight-inclusive package holidays) was reclassified as a tax by the ONS in April 2012. Others (like passport fees) are not included because the OBR does not consider them taxes (they are “requited”). On the other hand, the ONS thinks that National Insurance is requited and therefore not a tax; we think that is unrealistic, given the extremely tenuous relationship between national insurance contributions and benefits. So we classify all National Insurance as tax.

Sources were:

- OBR Economic and fiscal outlook, March 2026: main control total, detailed tax taxonomy and GDP denominator.

- OBR Devolved tax and spending forecast, March 2026: devolved property, landfill and aggregates taxes.

- HMRC Income Tax liabilities statistics, tax years 2021-22 to 2024-25: dividend and savings income tax liabilities.

- HMRC Personal incomes: Table 3.7: property, interest, dividend and other income distribution used to estimate income tax on rents.

- ONS Public sector current receipts, Appendix D: latest official public-sector current receipts cross-check.

- HMRC tax receipts and National Insurance contributions for the UK: detailed HMRC-administered tax receipts cross-check.

The code that generated the chart is available on our GitHub, together with the underlying data.

Thanks to B for help with the data. Chart created using Apache ECharts, by the Apache Software Foundation and contributors (Apache-2.0).

Photo “Jenga work” by santibon, CC BY-NC-ND 2.0, modified by Tax Policy Associates.

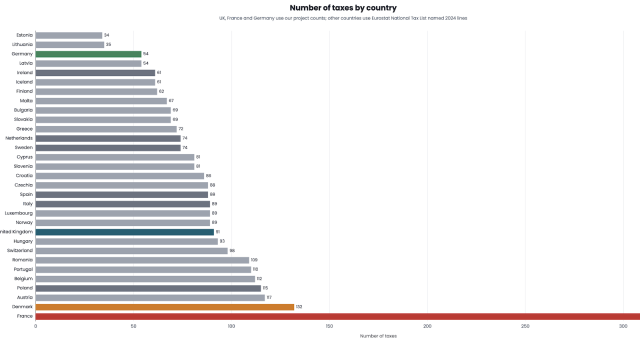

The UK has 90 different taxes. France has 348. Germany has 60. Why?

Why does Britain have more taxes than at any time since 1834?

What would a land value tax actually do?

What if Andy Burnham lowered the mansion tax threshold to £1.5m?

Has Britain run out of “other people” to tax?

Tax will go up but public services will get worse. This is why.

Footnotes

The first version of this article said 85. We apologise for the error. ↩︎

i.e. income tax, National Insurance contributions and the apprenticeship levy. Employer NICs and the apprenticeship levy belong in this category because they are, economically, a tax on employment income. ↩︎

We split income tax into its constituent elements – work, dividends, rent, investments, but count it as one tax in this total number. ↩︎

There are two oddities: bearer instrument duty (a very old tax, these days probably never applied in practice) and the Public Interest Business Protection Tax (essentially a regulatory fix, intended to dissuade energy companies from stripping assets out of failing suppliers). Then some taxes which are too new to yield revenue in 2024/25: CBAM, Vaping products duty, Extended producer responsibility fees, Building Safety Levy, Scottish aggregates tax, the International student levy, and multinational top-up tax. ↩︎

Leave a Reply