The Labour Party has published its manifesto. Labour claims to raise £7.35bn from additional tax – but almost three-quarters of that is from increased tax compliance rather than actual new taxes. The most obvious criticism is a lack of ambition, and lack of any proposals to reform the most serious problems with our tax system.

We set out the issues in more detail below.

The overall tax effect of the manifesto

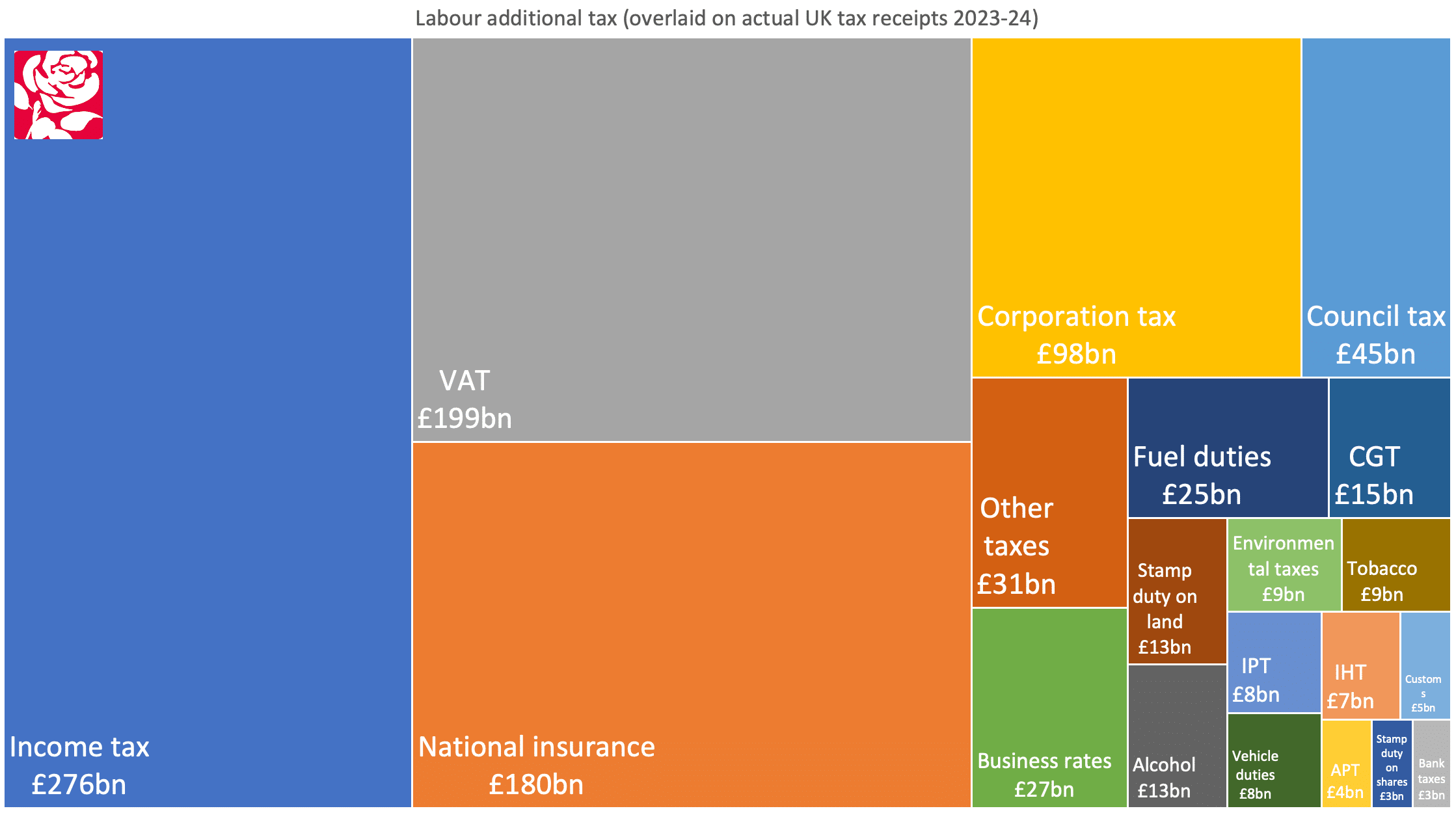

We have previously said that the tax increases that Labour and the Conservatives were arguing about were so small as to be irrelevant. That is very much true for the Labour manifesto. The total new tax they’ve identified, most of which isn’t an actual tax increase, vanishes into insignificance compared with the almost trillion pounds collected by HMRC each year.

This chart superimposes the size of Labour’s proposed new tax revenues over all the figures for UK tax receipts in 2023/24 (and, for ease, it’s in the top left, but none of the proposed Labour tax increases come from income tax):

The Labour manifesto says this.

“The Conservatives have raised the tax burden to a 70-year high. We will ensure taxes on working people are kept as low as possible. Labour will not increase taxes on working people, which is why we will not increase National Insurance, the basic, higher, or additional rates of Income Tax, or VAT”

We are concerned about politicians boxing themselves into an impossible corner with this kind of promise. These three taxes make up more than two-thirds of all UK tax receipts; once you’ve promised not to increase them, what do you do if you find you need to fund additional expenditure?

- Break your promise and increase tax anyway, saying circumstances have changed. This has historically not gone well for politicians.

- Scrabble around making lots of increases to minor taxes to make up the sums you need. But that will also often come at a political cost: most of these taxes either directly hit households (e.g. council tax or stamp duty) or will be passed onto them (e.g. alcohol duties; insurance premium tax; fuel duties). There are a few others, but they don’t add up to much.

- Create entirely new taxes that aim to raise large amounts of money without hitting typical households. This, however, is hard. The wealth tax proposed by the Wealth Tax Commission might fit the bill; but nobody, anywhere in the world, has ever implemented such a tax1, and its actual consequences are unclear. The recent Spanish wealth tax, targeted at the very wealthy, raised only €632m in 2023. Perhaps for this reason, Labour appear to have ruled out a wealth tax altogether.

- Do nothing, freeze tax thresholds and allowances, and let income growth/inflation push people into higher tax brackets – “fiscal drag”. It’s taxation by stealth, and it can raise very large sums – the current Government’s freeze of the personal allowance and higher rate threshold is forecast to raise £34bn of tax in 2028/29.2

We expect the answer in practice (whoever wins the election) will be the tried-and-tested last one. That is an unfortunate, but a consequence of having expediently ruled out the better, and more honest, options.

No tax reform. No pro-growth tax policies.

From a tax policy perspective, the most important thing about this manifesto is what’s not in it – tax reform. We made the same criticism of the Conservative Party manifesto, so if you’ve read that, you can skip right past this.

There are serious problems with many of the UK’s most important taxes:

- VAT is inefficient; the VAT threshold is too high, and that stops small businesses from growing. The exemptions and zero rates are too broad, causing uncertainty for business and disproportionately benefiting the wealthy⚠️. The flat rate scheme is being widely abused by criminals.

- Corporation tax has become impossibly complicated. The move to “full expensing” was incomplete. The constant changes to the rate (three in one year) make it difficult to plan. The OECD global minimum tax means that the largest companies now have to undertake two completely different corporate tax calculations.

- Income tax has been damaged by a series of gimmicks, bodges and compromises employed to avoid increasing the rate. There’s an “accidental” top marginal rate of 62% (if we include national insurance) for people earning between £100k and £125k (and, if they’re a graduate, 9% more than that). Someone with three children under 18 faces a top marginal rate of 57%. Anyone claiming free childcare and earning £100k potentially faces a marginal rate of over one million percent.

- Employer national insurance creates a massive difference between the cost of employing someone and the cost of engaging an independent contractor. This means that the thin – and ultimately notional – line between employment and self-employment becomes hugely important. Complex rules are created to guard the line. HMRC’s efforts to police it waste their time and that of taxpayers. And there remains plenty of avoidance and evasion.

- Stamp duty land tax reduces labour mobility, results in inefficient use of land, and plausibly holds back economic growth.

- Council tax is hilariously broken, based on 1991 valuations, and with bands which mean that the Buckingham Palace residence pays less council tax than a semi in Blackpool.

- Inheritance tax is deservedly unpopular. The rate is too high. The burden falls on the upper middle class. The very wealthy easily escape it.

- Bank taxation is unnecessarily complex, with an entire tax that has no reason to exist, and could easily be shifted to another, better, tax.

- Capital gains tax has a rate that’s so low it invites avoidance from people shifting income into capital.

- Our environmental taxes are a muddled mess. There’s an economic consensus across the political spectrum in favour of a carbon tax. This is hard to do unilaterally, but the UK could play an important role advocating for a carbon tax in current OECD discussions.

- There is now a widespread view, amongst individual taxpayers, business3 and the tax profession, that HMRC is seriously under-resourced.4 That is highly inconvenient for taxpayers (and sometimes much more serious than that). But it also means that some tax is not being paid: taxpayers are making mistakes, and HMRC is not helping them.

We believe a pro-growth agenda has to include tax reform. It’s therefore a shame that there is little discussion of any of these issues in the Labour Party manifesto (or indeed any of the others).

The only items in the Labour manifesto which might qualify as tax reform are a commitment to slow down the rate of constant change in business taxation. That’s welcome – but it barely scratches the surface of what’s needed.

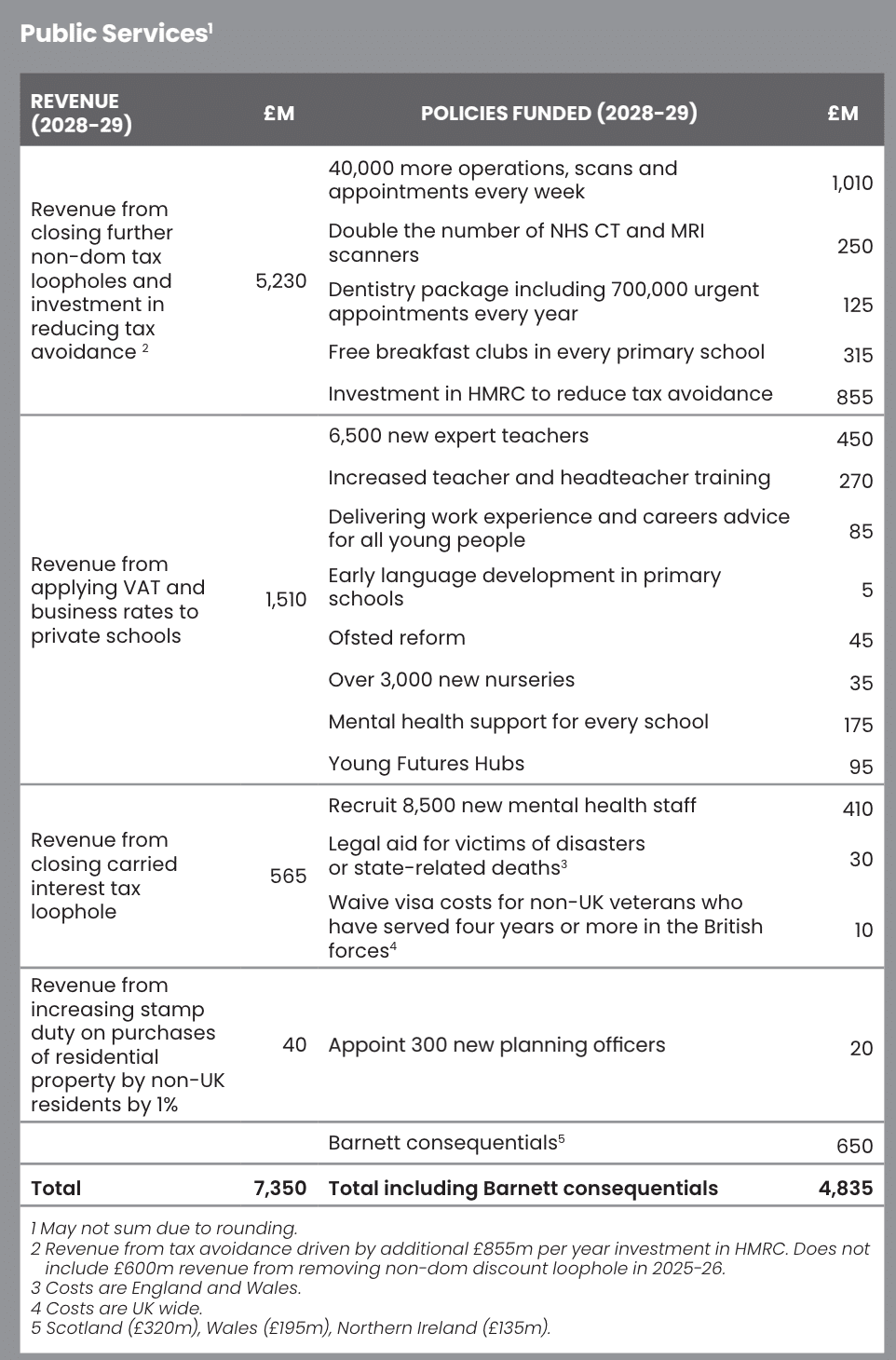

Costings

Labour publishes these costings. The white space on the left side of the page makes clear how little Labour are planning to do to the tax system:

and:

Tackle avoidance and evasion – £5bn

“We will modernise HMRC and change the law to tackle tax avoidance. We will increase registration and reporting requirements, strengthen HMRC’s powers, invest in new technology and build capacity within HMRC. This, combined with a renewed focus on tax avoidance by large businesses and the wealthy, will begin to close the tax gap and ensure everyone pays their fair share.“

An important point of detail: it’s unlikely to be possible to raise £5bn by clamping down on tax avoidance, because HMRC figures identify only £1bn of tax avoidance:

The focus on tax avoidance by “large businesses and the wealthy” may play well with focus groups, but doesn’t reflect the reality of where the “tax gap” actually is:

To be fair, Labour have published a fairly detailed plan which justifies the £5bn figure, and it covers compliance and evasion as well as tax avoidance. It’s unfortunate that the manifesto mis-states what they actually say they’ll do.

The other parties are also promising to raise large sums from increased tax compliance:

The Conservatives included a plan to “clamp down on tax avoidance and evasion” as part of their National Service press release. The document doesn’t appear to be publicly available; we published it here.

The origin of the £6bn figure common to Labour and the Conservatives appears to be the head of the National Audit Office, who said earlier this year that £6bn could be raised by cracking down on avoidance and evasion. But he didn’t say how, or how much it would cost.

The Lib Dems just present the £7.2bn figure as 2028/29 funding in their manifesto costings document. They don’t give figures for earlier years. There is no published plan.

In our view, targeted and carefully managed investment in HMRC compliance, customer service, investigation and enforcement functions could raise significant sums. We wrote about this in detail here. We are a little sceptical about whether Labour’s £5bn figure is realistic – naturally that scepticism applies to the other parties too (and more so, given their larger numbers).

Business taxation

The manifesto says:

“The business tax regime matters for investors. It is not just the rates of tax that matter, but also certainty. Under the Conservatives there has been constant chopping and changing – corporation tax has changed 26 times – and multiple fiscal events have made drastic changes often at little notice. Labour will stop the chaos, and turn the page with a strategic approach that gives certainty and allows long-term planning. We are committed to one major fiscal event a year, giving families and businesses due warning of tax and spending policies. We will publish a roadmap for business taxation for the next parliament which will allow businesses to plan investments with confidence.”

We expect business will welcome a slow-down in tax policy. We would, however, suggest that Labour go further: publish the roadmap with the first Budget and commit to make no changes to business taxation, other than simplification and targeted anti-avoidance measures.

“Labour will cap corporation tax at the current level of 25 per cent, the lowest in the G7, for the entire parliament, and we will act if tax changes in other countries pose a risk to UK competitiveness.”

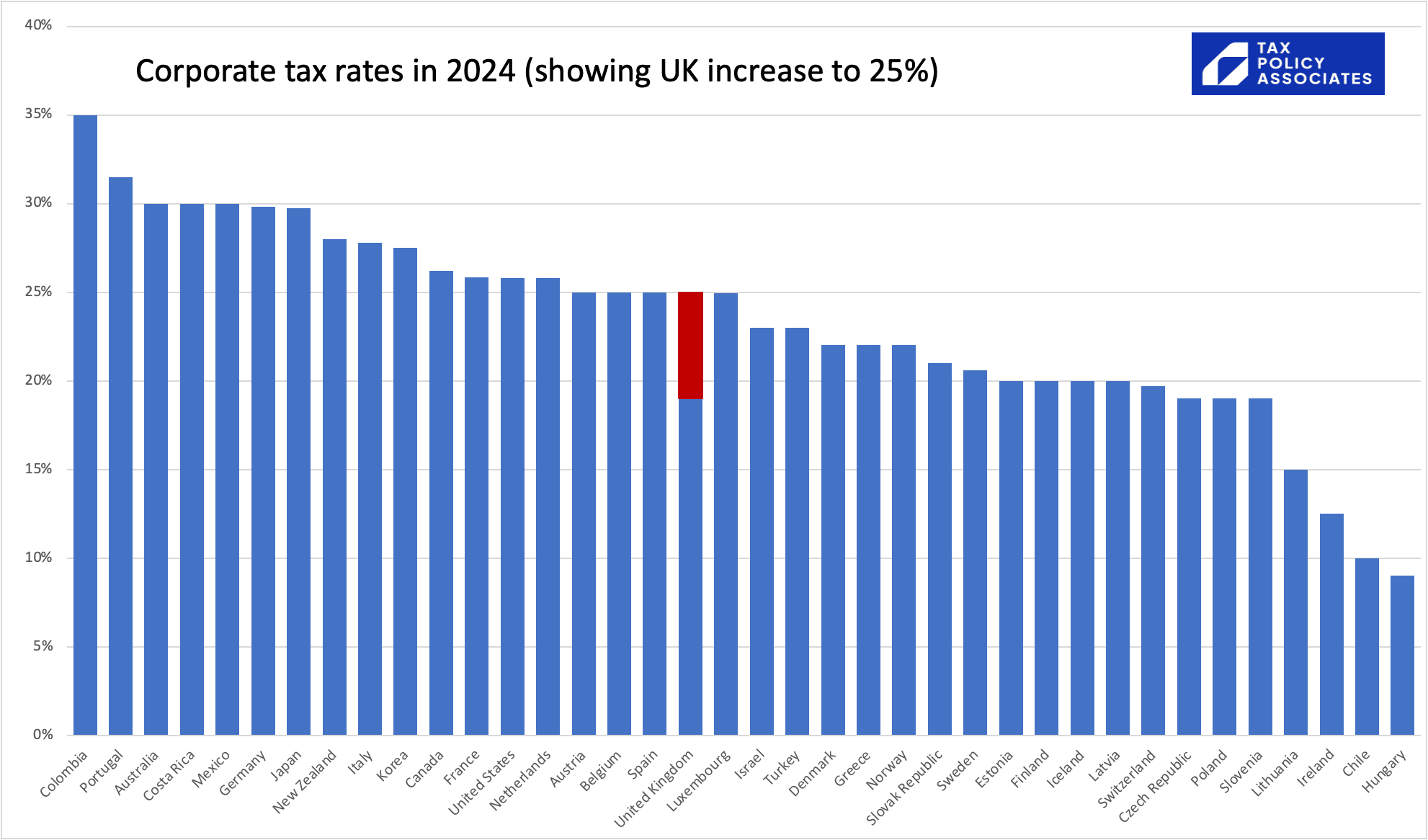

It is correct that the 25% UK corporation tax rate is the lowest in the G7; it is, however, fairly average by international standards:

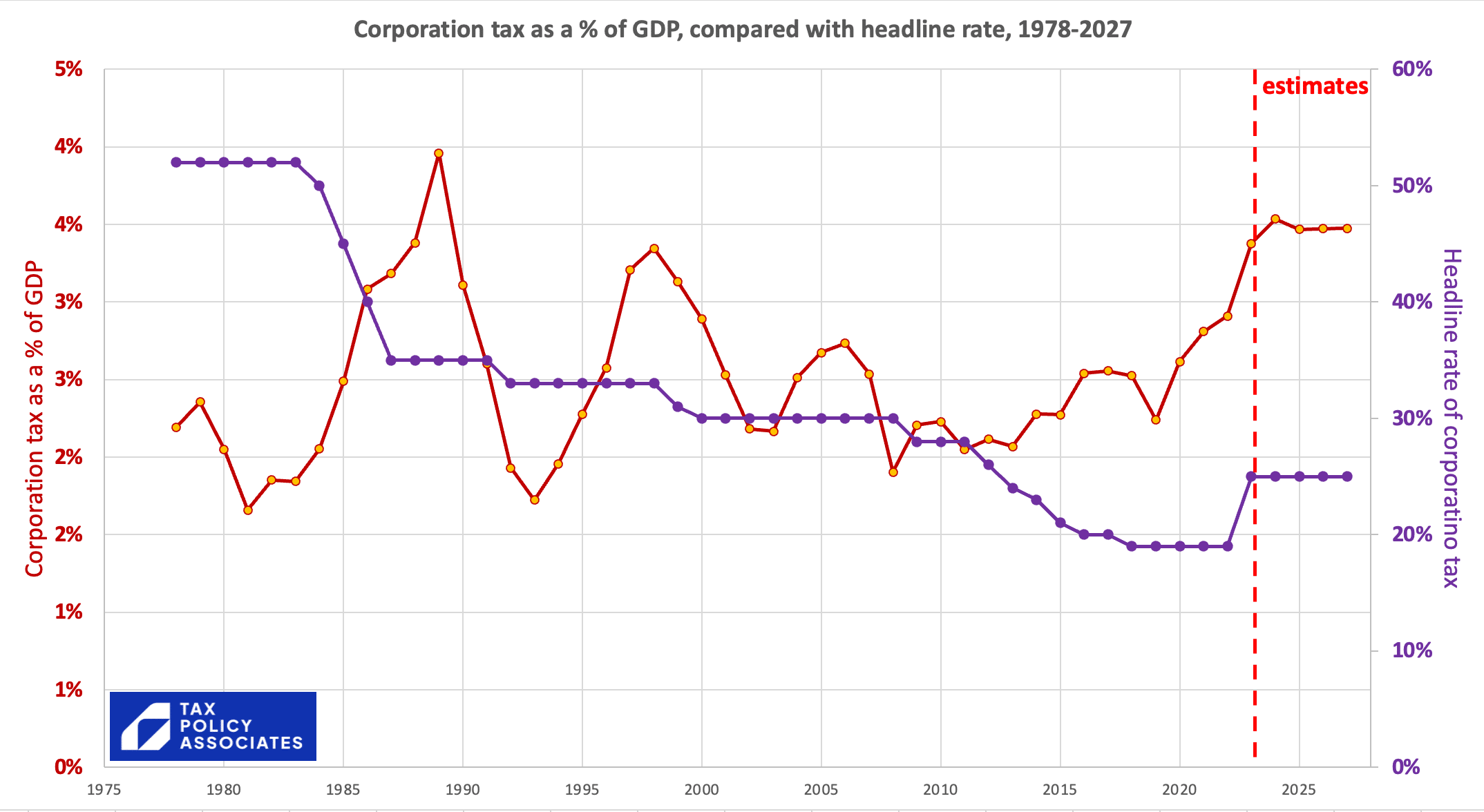

There has also been a significant widening of the UK tax base over the last 30 years, and so UK corporation tax collects significantly more now (as a % of GDP) than it did in the 1970s when the rate was 52%:

The effect of increasing the UK rate to from 19% to 25% in 2023/34, at a point when the base had become historically wide, was therefore to significantly increase the overall tax on companies. In our view this was likely the correct decision given economic circumstances, but we would be cautious about raising the rate further. We therefore believe Labour’s approach is sensible. Indeed it appears that no party is currently proposing to increase the rate.

“We will retain a permanent full expensing system for capital investment and the annual investment allowance for small business. And we will give firms greater clarity on what qualifies for allowances to improve business investment decisions.“

“Full expensing” was introduced by the Conservative Government in the 2023 Spring Budget. It gives a business up-front tax relief for all the cost of an investment rather than, as was historically the case, requiring the cost to be written-off for tax purposes over many years. That historic treatment created an unfortunate bias in the tax system against long-term investment, which is the opposite of what a sensible tax system should do. Full expensing was therefore a good pro-growth tax reform.

The move towards full expensing followed a long campaign from the Adam Smith Institute and others. It’s a good policy, which should boost growth, and will cost less than first thought.

Full expensing was unusual in that its effectiveness under a Conservative Government was highly dependent on the attitude of the Opposition: businesses would only take long-term business decisions on the basis of full expensing if they thought the rules would be there in the long-term. So Labour’s embrace of full expensing last year was important.

However this is an area where Labour could consider going further. Something like a third of investments do not benefit from full expensing. That means the policy is less effective in supporting growth than it could be. It also creates uncertainty for businesses on where precisely the line should be drawn. The best way to increase clarity would be to dramatically extend full expensing to all investment; that would realistically have to form part of a major reform of the corporation tax base, including a curtailing of interest relief for debt financing. Such a move would face considerable technical and political challenges; but it is something we would hope a new Government would seriously consider.

Ending the use of offshore trusts by non-doms – £0

“Labour will address unfairness in the tax system. We will abolish non-dom status once and for all, replacing it with a modern scheme for people genuinely in the country for a short period. We will end the use of offshore trusts to avoid inheritance tax so that everyone who makes their home here in the UK pays their taxes here.“

For hundreds of years, people living in the UK but born elsewhere5 have been “non-doms”, taxed on their UK income but only taxed on foreign income if they bring it into the UK. An even more important benefit: non-doms weren’t subject to UK inheritance tax on their non-UK property. This regime encouraged wealthy people to come to, and stay in, the UK – but has been perceived by many as unfair.

The Conservative Party announced the end of the non-dom regime in the Spring Budget, along lines very similar to what we had proposed the previous month. They intend to replace the non-dom rules with a four year exemption on income/gains, and likely a ten year exemption from inheritance tax. But they proposed to permit existing non-doms to use trusts to escape inheritance tax forever.

We believe this was a pragmatic compromise, aimed at preventing an exodus of the most wealthy non-doms. Many very wealthy people would not regard paying UK income tax and capital gains tax on their worldwide assets as a disaster. In some cases (e.g. Americans) the tax result is not so very different from their home tax result. For others, there is more tax but the difference is not hugely material. However UK inheritance tax, at 40%, has one of the highest rates in the world. Emotionally (rightly or wrongly) many non-doms regard it as an anathema, and would leave the UK rather than subject their estates to it if they die.

There are really three questions here:

- Is it simply wrong in principle for some people to be able to live most of their life in the UK, but (because of where they were born) for their estates to be mostly outside inheritance tax? Regardless of the cost/benefit?

- Is it perfectly fine in principle for the UK to have a special inheritance tax rate for non-doms, regardless of the cost/benefit?

- Or is this a question where we should reach our view based upon pragmatism – whether scrapping the favoured inheritance tax treatment results in more tax being paid, or less tax being paid?

Most politicians move immediately to the third position. The problem with that, however, is that it’s very hard to say what the effect would be of removing non-dom inheritance tax trust privileges. There have been no such changes before that we can measure.6

Labour have previously suggested a £600m benefit from ending the trust “loophole”; however it’s interesting that this figure is now relegated to a footnote, and not included in Labour’s costings calculation:

No reason is given for this, but we would speculate that it reflects a recognition of the unpredictable effect of this policy.

Ultimately this is a matter of political choices and priorities, rather than assessing evidence, because we do not believe there is adequate evidence (and it’s not clear to us, even in principle, how evidence could be found).

One important step that could be taken to reduce a non-dom exodus – and because it makes sense in its own right – would be to reform inheritance tax. Close down loopholes, expand the base, and reduce the rate to something more in line with other countries.

Business rates

The manifesto says:

“The current business rates system disincentivises investment, creates uncertainty and places an undue burden on our high streets. In England, Labour will replace the business rates system, so we can raise the same revenue but in a fairer way. This new system will level the playing field between the high street and online giants, better incentivise investment, tackle empty properties and support entrepreneurship.“

This characterisation of business rates is common; it is therefore unfortunate that it is incorrect. It is well established that, whilst business tenants pay business rates, the person who actually pays economically is the landlord (in the jargon, the “incidence” of the tax is on the landlord).

It is unclear how Labour will achieve the stated objectives. A tax on land cannot easily (or perhaps at all) distinguish between different types of user of the land. Landlords should already pay business rates on empty properties (and some tricks some were using to avoid that were recently kiboshed).

We would suggest the answer lies in something more radical: scrapping business rates and the two other unpopular and failed taxes on land: stamp duty and council tax. Replace them instead with a land value tax. That would be a major pro-growth tax reform which would have support from economists and think tanks across the political spectrum. Would Labour have the courage for such a step?

Carried interest – £600m

“Private equity is the only industry where performance-related pay is treated as capital gains. Labour will close this loophole.“

A banker pays tax on their bonus at a marginal rate of 47%; but that comes out of a bonus pot that was all subject to 13.8% employer national insurance. That’s a total tax of about 54%. By contrast, when private equity executives receive a share of the returns of their fund – called “carried interest” – it is taxed as a capital gain, at 28%. That treatment wasn’t enacted by Parliament – it results from a spectacularly successful lobbying effort in 1987.

Our view is that this treatment is both inequitable and wrong in law. We welcome Labour ending it.

The question is how much that will raise. Private equity executives made gains on carried interest of £3.4bn in 2020/21, which if taxed as income would have potentially meant another £600m of tax.7. The gains in 2021/22 were much higher – about £5bn, which if taxed as income would potentially yield almost £1bn.

And there is significant additional carried interest earned by private equity executives who are non-doms, which isn’t even included in these figures – and those tend to be the most senior executives, who earn the largest amounts. Our discussions with private equity industry figures suggest that carried interest reforms plus the non-dom reforms could potentially yield up to £2bn.

The important word in the previous paragraphs is “potentially”. There is no doubt that many private equity executives, particularly non-doms, would leave the UK rather than pay tax at 47%. Other countries in Europe and around the world would have more favourable regimes, and private equity executives are highly mobile, with many having only temporary ties to the UK.

One answer would be for Labour to increase the rate of tax, but not equalise it. That, however, seems ruled out by the manifesto wording.

It therefore seems likely that a significant number of private equity executives would respond to the additional tax by leaving the UK. Were this to happen, the economic effect of is debatable – it would not (or at least, not necessarily) reduce private equity investment into the UK, but change the location that investment is made from. There would be wider effects, e.g. on service industries and asset prices, which deserve consideration but are beyond our expertise.

There are, therefore, a great deal of uncertainties, but Labour’s £600m figure seems to us to be reasonably prudent given that it is so much lower than the potential static yield.

We would make two suggestions for Labour’s reform, which would create useful pro-growth incentives for the private equity industry:

- Labour’s reform should be targeted at the controversial “buyout funds“, not venture capital or infrastructure investment funds.

- Labour’s reform should only apply to traditional carried interest – where either the executives put in no money, or money is “round-tripped” and not actually at risk. It shouldn’t apply where private equity executives make a genuine investment into their funds. So if a private equity executive genuinely puts £1m into their fund, risks losing it, but the fund succeeds, then there remains a good argument that their return should be taxed as capital.

We would add as an aside that there is speculation that Labour are secretly considering equalising the rate of capital gains tax and income tax. If Labour were going to equalise the rates, they would not need to change the tax treatment of carried interest.

Windfall tax – £1.2bn

“To support investment in this plan, Labour will close the loopholes in the windfall tax on oil and gas companies. Companies have benefitted from enormous profits not because of their ingenuity or investment, but because of an energy shock which raised prices for British families. Labour will therefore extend the sunset clause in the Energy Profits Levy until the end of the next parliament. We will also increase the rate of the levy by three percentage points, as well as removing the unjustifiably generous investment allowances.“

We have written previously about the flaws in the Government’s windfall tax (which we don’t view as a windfall tax at all; just another profits tax). We suggested £5bn could be raised; Labour’s £1.2bn looks modest.

Stamp duty – £40m

“Labour will support local authorities by funding additional planning officers, through increasing the rate of the stamp duty surcharge paid by non-UK residents“

Non-residents buying UK property have to pay a surcharge of an additional 2% stamp duty land tax. Labour are proposing a 1% increase, and say that will raise £40m in 2028/29. The charge was brought in during 2021 having been proposed by Theresa May’s government – it was probably prohibited by EU law prior to Brexit.

HMRC publishes a document showing estimates of the impact of various tax changes – they show this change as raising £40m in 2026/27. If HMRC are correct, Labour’s figure will therefore be a slight under-estimate.

We expect this is only partially about revenue-raising, and partially about (very) slightly weighting the housing system in favour of UK residents.

We should reiterate that we regard stamp duty land tax as a bad tax that should be abolished. However the non-resident charge is not its worst feature: it is somewhat complex, but reasonably well designed and doesn’t cause too many difficulties in practice.

Private schools – £1.5bn

“Labour will end the VAT exemption and business rates relief for private schools to invest in our state schools.“

This is another proposal where many politicians say their position is based on a pragmatic assessment of whether it will gain or lose revenue, but in reality they are (on both sides) arguing from an ideological position. That is inevitable in any political system, and we make no criticism of it, – but we will ignore that political debate and focus on the numbers.

The easy question is: if Labour ends the private VAT exemption then by how much will private school fees rise? The answer is “a bit less than 15%”, because the net cost of VAT for most private schools will be around 15%, and some will be able to take cost-saving measures to absorb part of that 15% net cost. But evidence suggests that, as with most VAT changes on single products/services, most of the net 15% cost will be passed onto parents.

The hard question that follows is: how many parents will therefore take their children out of private school? And what effect will that have on the net tax revenue yield, given that the State sector will have to educate those children?

This is ultimately a question of education policy and economics; areas where we do not have expertise. We have, however, noted that some of the high estimates reported in the press have no good statistical basis.

We wrote about the difficulties of coming up with an estimate here. The only serious attempt to come up with an estimate is this from the IFS.8 The analysis is, as the authors note, subject to numerous uncertainties, but it takes a rigorous approach.

We therefore expect that the correct answer as to the net tax impact of the change will be in the region of the Institute for Fiscal Studies’ estimate of £1.3–£1.5 billion per year. Labour’s figure is at the top end of this.

Disclosure: Our founder, Dan Neidle, is a member of the Labour Party, and sits on its most senior disciplinary body. His tax policy analysis is widely regarded as non-partisan, and he was highly critical of Labour Party tax proposals in the 2017 and 2019 elections.

Footnotes

I don’t regard the various wartime and post-war emergency taxes as a useful precedent, economically or politically ↩︎

See page 68 of the Office for Budget Responsibility’s March 2024 economic and fiscal outlook. ↩︎

See page 31 of the CBI report ↩︎

It’s not merely that HMRC funding has failed to keep pace with inflation; its most experienced personnel have been moved onto other projects, particularly Brexit and the pandemic. See paragraph 1.8 onwards in this National Audit Office report. This was probably sensible, but is having long term consequences. ↩︎

A considerable simplification – in reality the domicile concept is much more complex ↩︎

The impressive research from Arun Advani and Andy Summers on the effect of the 2017 non-dom reforms shows what happened to “ordinary” non-doms who lost that status – very few of them left. However the 2017 reforms permitted the very wealthy to use trusts to escape essentially all the effects of the reforms. Hence we cannot use evidence from 2017 to predict how the very wealthy will behave today if the benefits of trusts are removed. ↩︎

i.e. £3.4bn x (47% – 28%). ↩︎

There’s also a report from the Adam Smith Institute. It contains some valid criticisms of the IFS approach, but in our view is then fatally undermined by using figures with no statistical validity. ↩︎

A tax reform agenda for tomorrow’s Chancellor

Our take on the Reform UK manifesto

Our take on the Green Party manifesto

Our take on the Conservative manifesto

Our take on the Lib Dem manifesto

Leave a Reply