The Green Party has published its manifesto⚠️. The Green Party propose raising taxes by £115bn in 2026/27 and £172bn in 2029/30 – about 4.5% of GDP. There is very little detail presented and the proposals are impossible to assess in any depth. It’s a huge missed opportunity to advocate for radical tax proposals, and move them into the mainstream.

We set out the issues in more detail below.

Lack of detail

The Green Party manifesto has a very radical approach to tax, raising a large amount of money from complex new taxes. However this is covered in two brief pages, which present no detail and no figures.

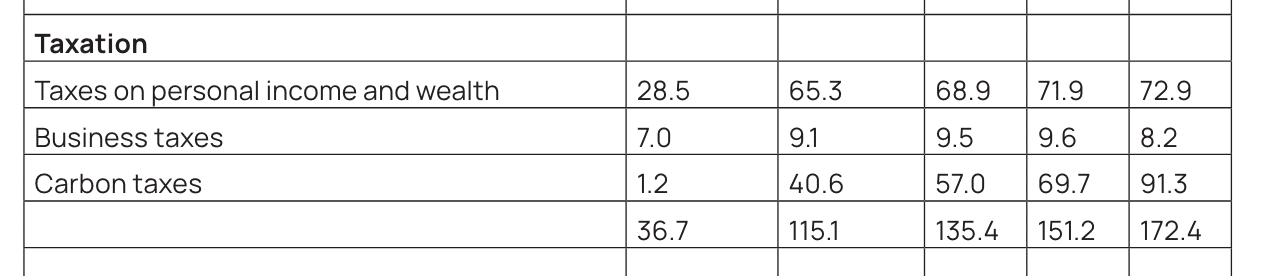

A statistical appendix then provides figures for the overall effect:

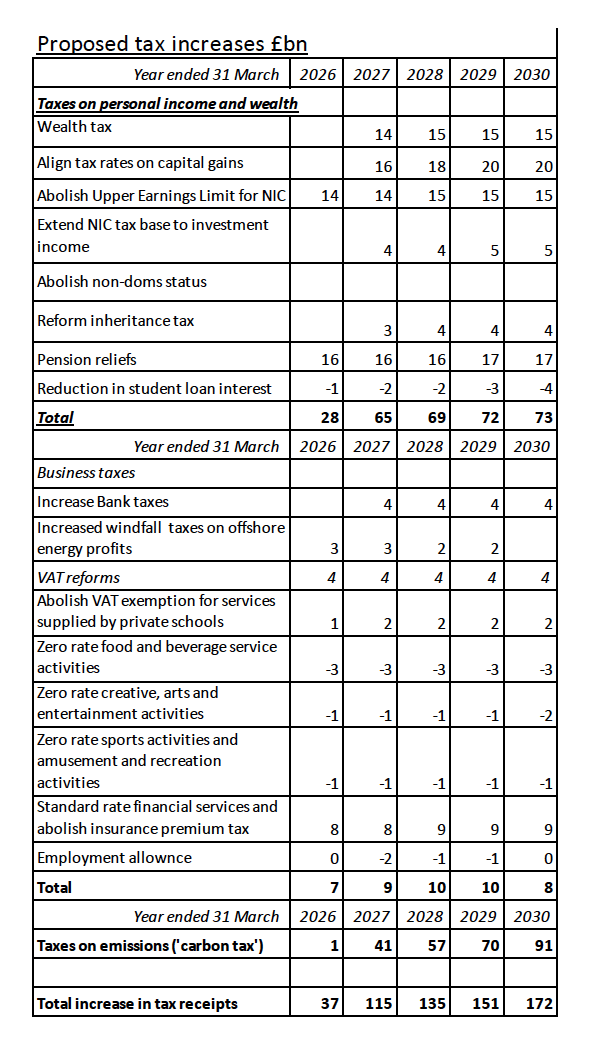

I asked the Green Party press office, and they kindly sent me this breakdown between the various proposals:

This is very unsatisfactory. It’s impossible to assess tax proposals, particularly radical ones, if they are not explained. Otherwise we are being asked to take these numbers on trust.

Tackle avoidance and evasion

The manifesto says:

We will clamp down on tax dodging. When companies and individuals fail to pay their fair share, it deprives our vital public services of much needed investment.

Greens support small businesses that are currently paying taxes for the services they use, and will take steps to tackle the global corporations that are not. It will be a priority to strengthen global tax agreements to stop corporate tax avoidance and evasion, and to ensure a level playing field between UK and transnational businesses. We will also ensure that HMRC has the resources it needs to reduce the gap between taxes due and taxes paid.

This is all very vague. The Labour and Conservative parties have set out plans to raise £5-6bn of additional annual tax from “tackling tax avoidance and evasion”. The Lib Dems don’t have a published plan, but think they can raise £7bn. The Greens just have these two paragraphs.

Wealth tax

The manifesto says:

“Elected Greens will push for a wealth tax. This will tax the wealth of individual taxpayers with assets above £10 million at 1% and assets above £1bn at 2% annually. Only a very small minority of people would be subject to the wealth tax, while the overwhelming majority would benefit. “

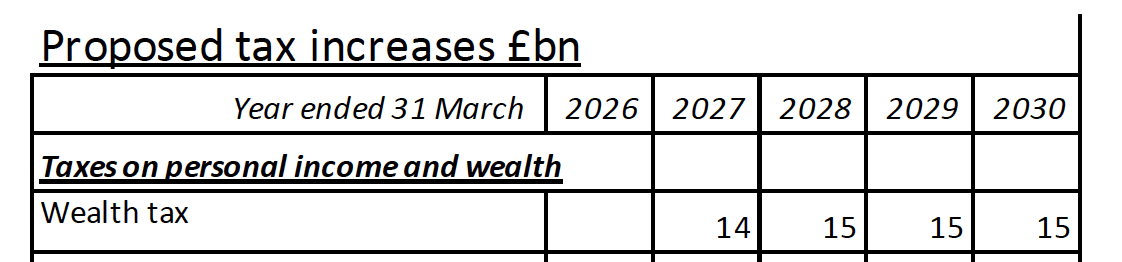

The Green Party plans to raise a very large amount from this:

There has never been a tax like this anywhere in the world, raising so much money from such a small number of people. The Green Party provide no calculations, no references, and no explanations of how this tax would work.

The closest tax is the Spanish “solidarity tax on large fortunes“, which applies at 1.7% for wealth of €3m, 2.1% for wealth of €5.4m, and 3.5% for wealth of €10.7m. The rates are therefore not dissimilar to the proposed Green tax, but it raised €632m in 2023. UK GDP is about twice Spanish GDP, but it’s not at all obvious from this why the Greens think they can raise £14bn.

Possibly the tax would be designed differently from the Spanish tax? But given we have no information at all on its design, it’s impossible to say.1

The Greens might well respond that the UK has many more internationally mobile billionaires living here than Spain does. That is certainly true – but their mobility means they are difficult to tax. One look at the Sunday Times Rich List shows that most of the billionaires associated with the UK have relatively limited ties here.

The Wealth Tax Commission produced a magisterial report on wealth taxes in 2020. It recommended against an annual wealth tax because of implementation and administration difficulties, and the likelihood of avoidance. It instead suggested a one-off retrospective wealth tax – the retrospection would mean it was impossible to avoid. We have doubts about the political economy of such a retrospective tax, but technically we agree that (if it could be implemented) it would be effective.

Inheritance tax

The manifesto says:

“We would reform inheritance tax, ensuring that intergenerational transfers of wealth are taxed more fairly”

That is the only mention of “inheritance tax” in any of the Green Party materials. We do not know what reforms are proposed.

Despite the absence of any proposals, the Green Party expects to book £4bn of new revenue from inheritance tax in 2026/27:

That’s a significant amount from a tax that currently raises £7bn.

Carbon tax

A carbon tax is a tax that places a price on carbon dioxide emissions, either in-country or imported. So the tax incentivises businesses to cut emissions. It’s a conceptually brilliant design which we support.

However, the Green manifesto has almost no detail:

“Elected Greens will propose levying a carbon tax at an initial rate of £120 per tonne, rising to a maximum of £500 per tonne of carbon emitted within ten years. This is deliberately designed to make it cheaper for the emitter to take steps to reduce emissions rather than pay the tax. We estimate we will be raising up to an additional £80bn by the end of the parliament, then falling back after that as carbon emissions reduce across the economy.”

We asked the Green Party for more information and they kindly sent us a short explanatory document. The document provides calculations but little in the way of technical detail on how the tax should work. It’s an extremely brief treatment of a complex tax, particularly when it’s set to raise such a huge sum (4% of GDP).

However those details they do provide suggest that the Greens are proposing a very unusual, and perhaps unique, carbon tax.

A simple carbon tax is on either the carbon emitted by UK production or the carbon emitted by UK consumption.

These days it’s more typical to talk about a “border adjusted” carbon tax. This means that we would tax domestic production and imports, but not exports. This has several advantages:

- It works extremely nicely as an international system, if others then adopt the same tax. No credit system or complexity is required – each country just taxes the products entering (or produced and consumed in) its own borders.

- And that’s the point: what the UK does with carbon taxes is irrelevant in global terms – the UK is responsible for 1% of global emissions. A more important aim is for the UK can help spearhead a global move to a carbon tax (e.g. as part of current OECD/Inclusive Forum discussions).

- More practically: if we tax exports then UK cars sold to the US (for example) are subject to a UK carbon tax, but Chinese cars sold to the US would not be subject to a carbon tax anywhere in the world. UK industry becomes globally uncompetitive. That’s obviously bad for the UK; but it doesn’t help global carbon emissions, because demand for cars would shift from the UK to China – “emissions leakage”. There would be no carbon reduction. It’s pointless.

The Green proposal is unusual, because it’s not border adjusted, and it applies to UK production, imports and exports. That does not seem very coherent or workable.

Carbon tax proposals usually phase in the tax gradually, rather than risk creating an economic shock. However the Green Party carbon tax starts at a high rate of £120 per tonne – much higher than the EU carbon price (which has never gone over €105 per tonne). It then increases to £265 per tonne by 2030. The document explains this:

“We apply a rising tax rate based on HMG carbon values (central estimate). These are the estimated prices at which iit is cheape [sic] for the emitter to reduce its emissions than pay the tax.”

That’s not how a carbon tax usually works. The idea is to price it at the “social cost of carbon emissions”. It’s unclear why the Greens are taking a different approach.

The regressivity problem

An obvious problem with the carbon tax is that it is regressive. Costs resulting from the carbon tax will (inevitably) increase prices, not just of fuel but of all products. That will disproportionately impact the poor, and people on middle incomes will also lose out.

For this reason, carbon tax proposals are usually accompanied by proposals to redistribute a significant proportion of the tax revenues to households in the form of tax rebates and/or benefits. Some have suggested simply distributing carbon tax refunds across the population. Others suggest more targeted subsidies.

The Green Party’s carbon tax paper says: “We would provide funding for poorer households to convert to lower carbon alternatives” but provides no details, and no such funding is evident in their figures. In any case, “funding for poorer households” would be insufficient to undo the regressive effects of the carbon tax.

The sad truth may be that the Greens wish to use carbon tax revenues for general spending, and this has eclipsed the more appropriate use of the revenues for redistribution.

Incompatibility with their other proposals

The rest of the Green manifesto speaks as if there is no carbon tax. It talks about an extended windfall tax on oil/gas production, and a new tax on frequent air passengers. The carbon tax document itself says “Carbon tax on aviation could include extensions to the existing Air Passenger Duty or a Frequent Flyer Levy.”2

All this should be irrelevant if a carbon tax is introduced.

National insurance increase

“Elected Greens will also call for the reform of tax rates on investment income, by aligning them with the tax and NIC rates on employment income

We would remove the Upper Earnings Limit that restricts the amount of National Insurance paid by high earners. Tax rates should not fall as income increases. “

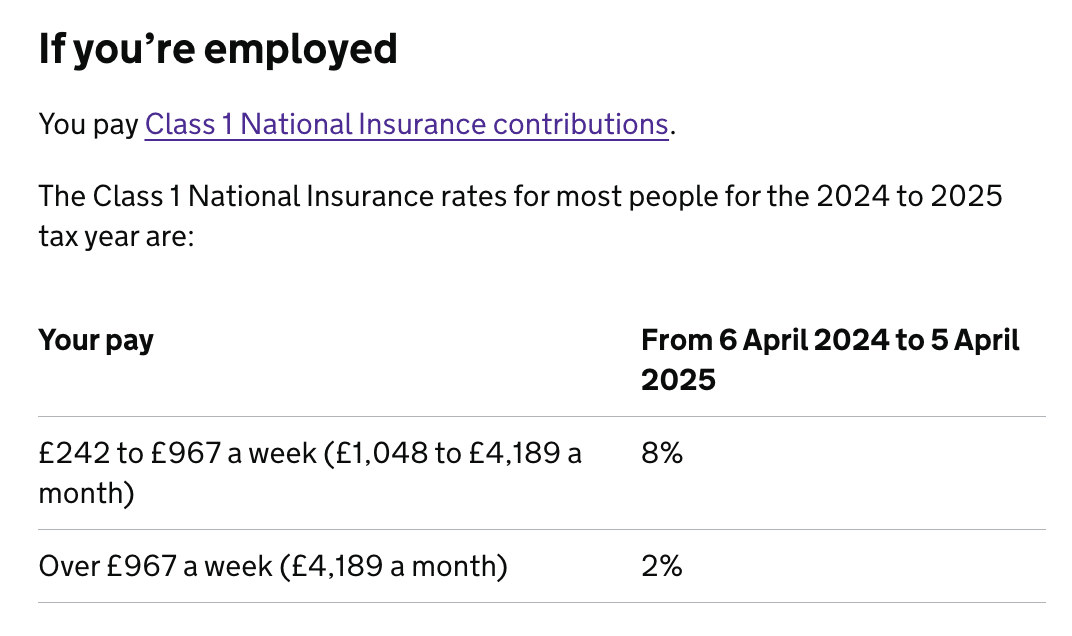

What does “removing the cap on national insurance” mean?

Here are the current Class 1 rates:3

£967 is the “upper earnings limit”. There used to be no national insurance past that point; it’s now 2%. “Uncapping” means removing the limit so that the 8% rate continues to apply past £967 a week.4

We should, however, discard the pretence there’s something special about national insurance. It’s just income tax by another name, with an antiquated weekly calculation, a complicated history and a funny national accounting treatment. A realistic approach looks at the overall combined rate of income tax and national insurance.

In the current, 2024/25 tax year, this looks like this for an employee:5

- No tax on incomes below the £12,570 personal allowance.

- £12,570 to £50,270 – a combined income tax and employee national insurance rate of 28%

- £50,271 to £125,140 – a combined rate of 42%

- Above £125,140 – a combined rate of 47%.

The Greens are therefore proposing that the third of these should rise to 48%, and the fourth to 53%.

However things aren’t that simple. The personal allowance starts to be withdrawn (“tapered”) when your income hits £100,000, and is gone by £125,140. This means that the marginal rate in the £100,000 to £125,140 range is much higher than the headline rate.

This chart shows the effect, as things stand today (blue) and under the Green proposal yellow):

There’s an interactive version of the chart here that lets you select different scenarios and touch/mouse over the chart to get exact figures.

This is not the only factor that means the actual marginal rate is higher than the headline rate. There are a series of poorly thought-through tricks and gimmicks that have this effect, most significantly child benefit withdrawal and student loan repayments.

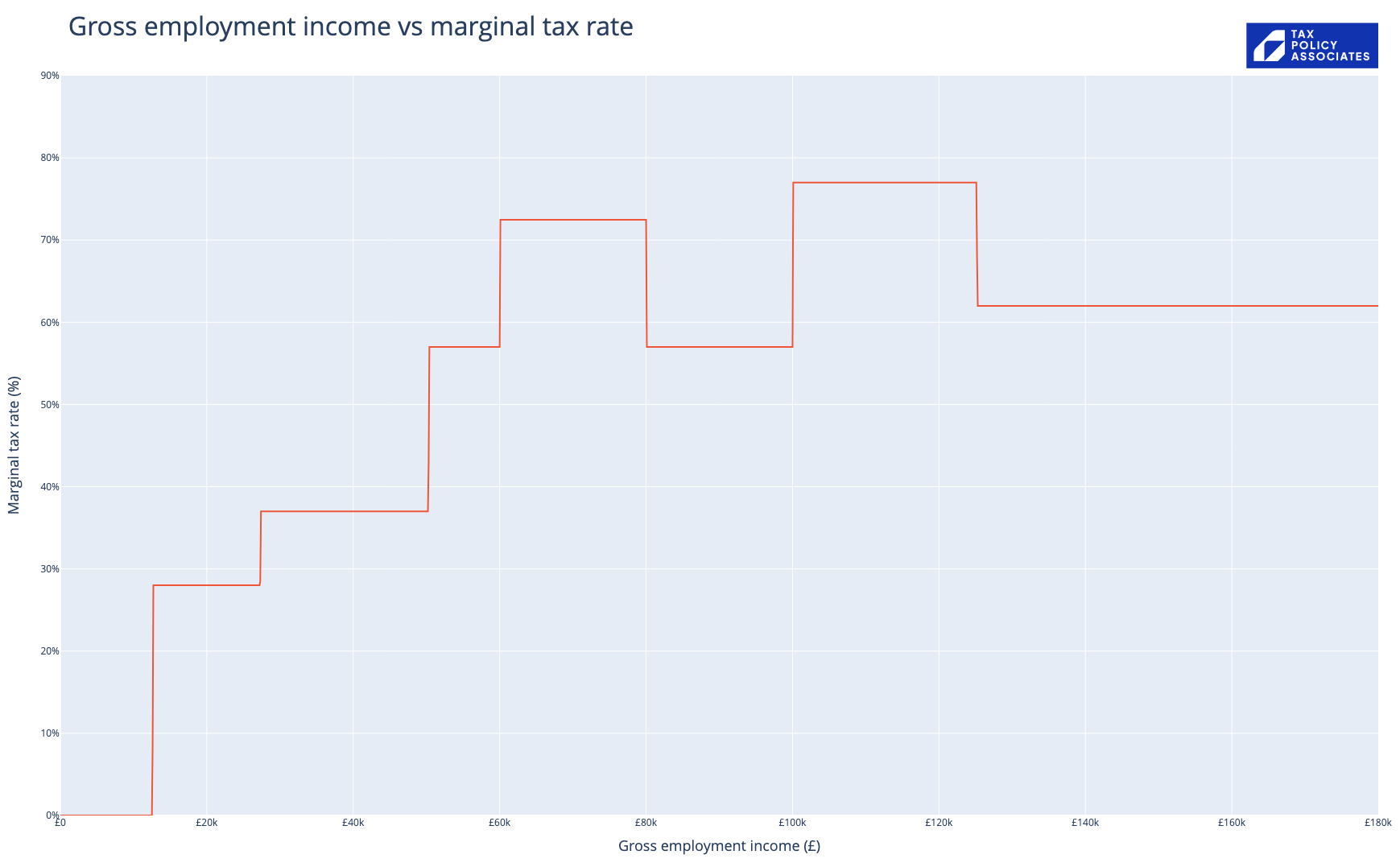

Here’s the marginal rates under the Green proposal for a graduate with three kids under 18:

So a graduate6 earning £60,000 with three kids pays a 72% marginal rate, and everyone earning £100k-£125k pays a 77% marginal rate. I don’t think this would be sensible or sustainable. There are many people (think: hospital consultants) who would prefer to reduce their hours than earn just 23p in the pound.

Uncapping national insurance was a perfectly rational policy in the 90s, but it’s not viable today unless the various tricks and gimmicks in the system are fixed or removed.

Who would pay this?

The Green proposal will affect quite a lot of people.

£50,270 is not that far above the average London salary. And, by 2027/28, one in five taxpayers, and one in four teachers will be affected; I expect a majority of households will have someone who earns that figure at some point in their life. To say this is a tax on the “richest” is not particularly accurate.

Pension tax relief limit

The manifesto says:

We would equate the rate of pension tax relief with the basic rate of income tax to help fund the social care that will allow elderly and disabled people on low incomes to live in dignity.

This is, on the face of it, a sensible way to raise money from the upper middle class without too many distortive effects. It doesn’t affect the very wealthy because they’re past the pension cap.

The Green Party’s annual revenue figures from this are:

No justification for these figures is provided, but they are likely in the right ballpark.

This will affect everyone earning £50k who makes a pension contribution. Many people would respond by stop making pension contributions – that will have obvious wider effects. There are also potential administrative complications.

VAT on financial services

“We would also propose a range of changes to VAT, reducing it on hard-pressed areas such as hospitality and the arts and increasing it on financial services and private education. “

Some financial services are currently either exempt from VAT or outside VAT altogether. These include lending, operating accounts, and most transactions in shares and securities. This means that banks don’t apply VAT to interest or fees on these services; it also means banks can’t recover their input VAT.

In principle it would be much preferable to end the financial services exemption. However there are significant technical difficulties in doing so; identifying the outputs and inputs is not straightforward (the issues are nicely set out in this paper⚠️, which also proposes a solution). There is also the significant practical problem that many customers of banks, such as household borrowers under mortgages, would not be able to recover any VAT they were charged – the likely impact of applying VAT to financial services would be to increase household mortgage bills.

There have been numerous EU discussions about ending the financial services exemption, but all have failed. The most recent one was abandoned because it was thought too politically difficult to increase prices for consumers during the “cost of living crisis”. We recently spoke to a leading VAT academic who advocates for ending all VAT exemptions; but even she balked at the financial services exemption – “just too difficult”.

Even if a solution was found, it would be preferable for the UK to proceed in lockstep with the EU; having two different VAT systems for financial services would complicate cross-border business and create the potential for avoidance and evasion.

All of which is to say that, if the Greens really plan to end the financial services VAT exemption, they need to do better than three words, and be a little more hesitant than assuming they can start booking £8bn of new revenue from April 2025.

Capital gains tax

“Elected Greens will push too for the reform [of] Capital Gains Tax (CGT) by aligning the rates paid by taxpayers on income and taxable gains. This would affect less than 2% of all income-tax payers.”

The Lib Dems think they can raise £5bn from aligning rates.7 The Greens show £16bn to £20bn:

£16bn in 2026/2027 is a very large number compared to the actual CGT receipts in 2023/24 of £15bn.

The problem with capital gains tax is that people can control when they pay it. If you say you’re going to increase the rate, they’ll sell early and take advantage of the current rate. And, if the above is to be believed, the Greens are planning to give people a year before they raise the rate (which is very strange).

We expect it’s for these reasons that HMRC data shows a projected loss in capital gains tax revenues of about £3bn if rates are equalised. We talk more about this in our analysis of the Lib Dem CGT proposal.

But the £16bn figure has to be regarded as very wrong.

Bank tax

The manifesto says:

“We would introduce a windfall tax on banks when excessive profits are being made.

This seems to leave open whether and how the Greens are proposing taxing the banks, but they nevertheless book £4bn a year of projected revenue from 2027:

Property tax

We at Tax Policy Associates are strong supporters of land value taxation, something the Green Party has historically supported.

So it’s very disappointing that the Green Party says this is a “long-term policy aim” and is just proposing modest tweaks to council tax and business rates:

“Our long-term policy aim is a Land Value Tax so that those with the most valuable and largest land holdings would contribute the most. In the next parliament, elected Greens will take steps towards this by pushing for:

• Re-evaluation of Council Tax bands to reflect big changes in value since 1990s.

• Removal of business rate relief on Enterprise Zones, Freeports, petrol stations and most empty properties.

• A survey of all landholdings to pave the way for fair taxation of land.”

There is no further detail on this, and no figures presented for the consequences.

Disclosure: Our founder, Dan Neidle, is a member of the Labour Party, and sits on its most senior disciplinary body. His tax policy analysis is widely regarded as non-partisan, and he was highly critical of Labour Party tax proposals in the 2017 and 2019 elections.

Footnotes

We understand that the Green Party wealth tax may be modelled on proposals from the University of Greenwich which suggest a wealth tax could raise as much as £130bn. We regard such figures as pure fantasy. ↩︎

The manifesto itself suggests that the carbon tax replaces fuel duty, which would result in a fuel duty cut – however it seems from the carbon tax document the fuel duty would be maintained until it was eclipsed by the rising carbon tax. ↩︎

The self-employed pay slightly less ↩︎

Uncapping the upper earnings limit was a key element of Labour’s “shadow budget” for the 1992 general election. The “shadow budget” in general, and this proposal in particular, are often blamed⚠️ for Labour’s loss, although whether that is correct is contested⚠️. ↩︎

Ignoring Scotland for the moment, and also ignoring weird marginal rate effects ↩︎

Reports on the Green Party manifesto sometimes say the Greens will cancel student debt,and this has been a Green Party policy in the past. But the actual manifesto for 2024 just has this as a “long term plan” (see page 30), with no figure for this included in their costings. ↩︎

Albeit after providing some new reliefs – there are no details. ↩︎

The Green Party – very shy about a big tax increase

A tax reform agenda for tomorrow’s Chancellor

Our take on the Reform UK manifesto

Our take on the Labour manifesto

Leave a Reply