The Conservative manifesto is here, and an accompanying costings document is here. It proposes £6bn of tax cuts in 2024/25, rising to £17bn in 2029/30. The tax cut figures appear realistic; the question is whether they are affordable. But the bigger question is why the manifesto is almost completely silent on tax reform, when so much of the UK tax system is badly broken.

And the manifesto itself falls into a tax trap our broken tax system creates. A proposed change to child benefit tax accidentally creates a new marginal rate of 70% for a parent earning £120k who has three children under 18.

If the governing party can’t spot these kinds of problems, what chance for the rest of us?

We set out the issues in more detail below.

No tax reform. No pro-growth tax policies.

From a tax policy perspective, the most important thing about this manifesto is what’s not in it – tax reform. We make the same criticism of the other parties’ manifestos.

There are serious problems with many of the UK’s most important taxes:

- VAT is inefficient; the VAT threshold is too high, and that stops small businesses from growing. The exemptions and zero rates are too broad, causing uncertainty for business and disproportionately benefiting the wealthy⚠️. The flat rate scheme is being widely abused by criminals.

- Corporation tax has become impossibly complicated. The move to “full expensing” was incomplete. The constant changes to the rate (three in one year) make it difficult to plan. The OECD global minimum tax means that the largest companies now have to undertake two completely different corporate tax calculations.

- Income tax has been damaged by a series of gimmicks, bodges and compromises employed to avoid increasing the rate. There’s an “accidental” top marginal rate of 62% (if we include national insurance) for people earning between £100k and £125k (and, if they’re a graduate, 9% more than that). Someone with three children under 18 faces a top marginal rate of 57%. Anyone claiming free childcare and earning £100k potentially faces a marginal rate of over one million percent.

- Employer national insurance creates a massive difference between the cost of employing someone and the cost of engaging an independent contractor. This means that the thin – and ultimately notional – line between employment and self-employment becomes hugely important. Complex rules are created to guard the line. HMRC’s efforts to police it waste their time and that of taxpayers. And there remains plenty of avoidance and evasion.

- Stamp duty land tax reduces labour mobility, results in inefficient use of land, and plausibly holds back economic growth.

- Council tax is hilariously broken, based on 1991 valuations, and with bands which mean that the Buckingham Palace residence pays less council tax than a semi in Blackpool.

- Inheritance tax is deservedly unpopular. The rate is too high. The burden falls on the upper middle class. The very wealthy easily escape it.

- Bank taxation is unnecessarily complex, with an entire tax that has no reason to exist, and could easily be shifted to another, better, tax.

- Capital gains tax has a rate that’s so low it invites avoidance from people shifting income into capital.

- Our environmental taxes are a muddled mess. There’s an economic consensus across the political spectrum in favour of a carbon tax. This is hard to do unilaterally, but the UK could play an important role advocating for a carbon tax in current OECD discussions.

- There is now a widespread view, amongst individual taxpayers, business1 and the tax profession, that HMRC is seriously under-resourced.2 That is highly inconvenient for taxpayers (and sometimes much more serious than that). But it also means that some tax is not being paid: taxpayers are making mistakes, and HMRC is not helping them.

We believe a pro-growth agenda has to include tax reform. It’s therefore a shame that there is little discussion of any of these issues in the Conservative Party manifesto (and we fear we won’t see it in the Labour manifesto either).

The only items in the Conservative Party manifesto which might qualify as tax reform are the income tax child benefit marginal rate change, and stamp duty – but in both cases their proposed solutions cause other problems. More on that below.

That leaves us with a few Conservative tax cut pledges that are of limited relevance.

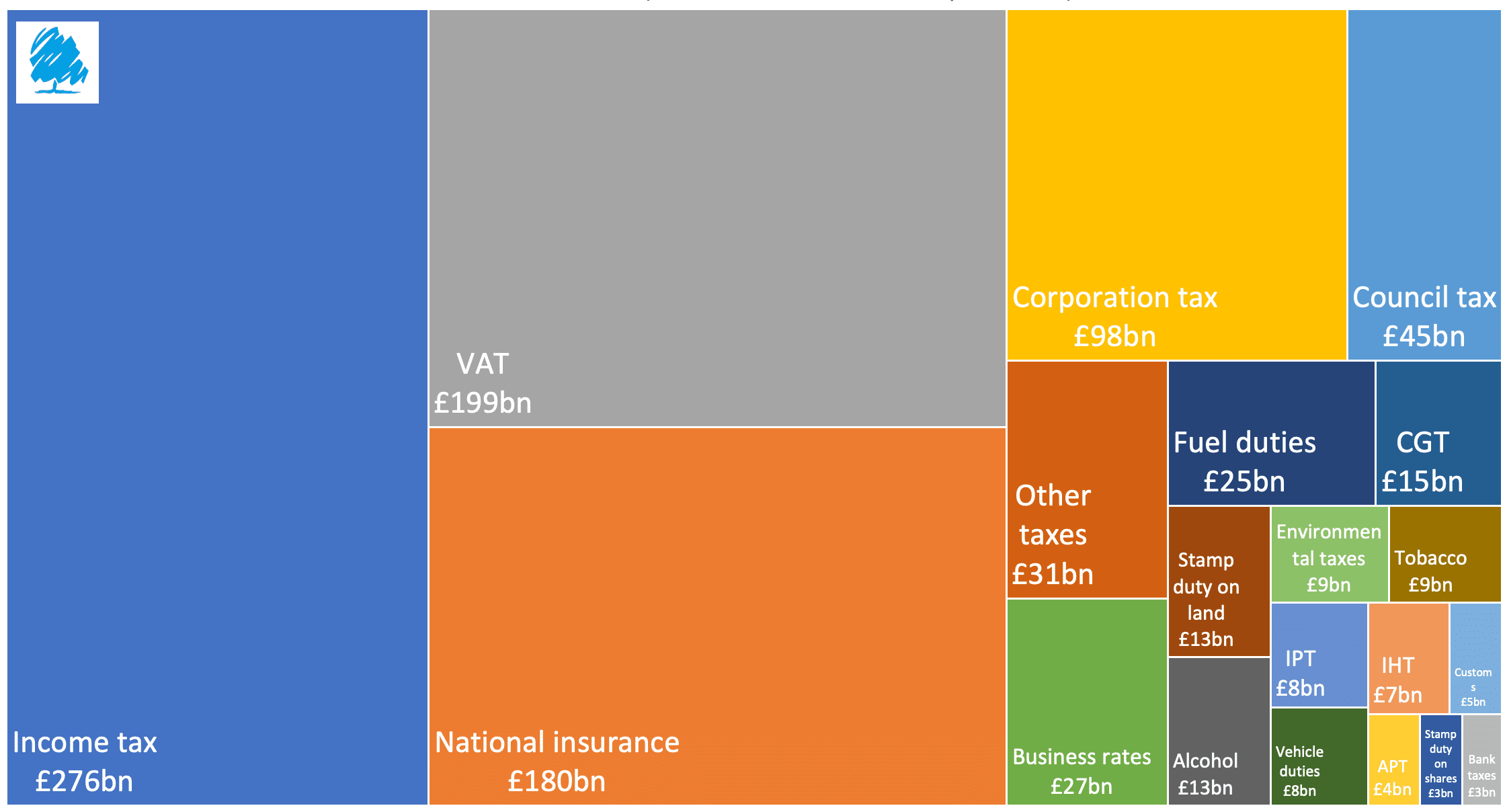

To provide some context, this chart shows current tax receipts for 2023/24. We’ve overlaid a Conservative Party logo equal to the size of the Conservatives’ proposed tax cuts for 2024/25 (for ease of reference, the logo is in the top left of the chart, but the cuts are not to income tax).

Cuts to national insurance – £5bn cost in 2025/26, rising to £13bn by 2029/30

The manifesto says the Conservatives plan to:

“Cut tax for workers by taking another 2p off employee National Insurance so that we will have halved it from 12% at the beginning of this year to 6% by April 2027, a total tax cut of £1,350 for the average

worker on £35,000 – and the next step in our longterm ambition to end the double tax on work when financial conditions allow.

Cut taxes to support the self-employed by abolishing the main rate of self-employed National Insurance entirely by the end of the Parliament.”

We believe the figures presented for the cost of these tax cuts are realistic.

If you are going to cut tax on income, then national insurance is a better tax to cut than income tax (because it’s only paid on working income, not investment income). Some have suggested the rich will benefit more from the cut – that misunderstands the nature of national insurance. Cutting the main rate of national insurance means it’s only income between £12,570 and £50,000 that benefits. So someone earning £1m benefits the same as someone earning £50,000.

The key questions are around whether this is realistically funded. In part that is by closing the tax gap, for which more below. In part it is by cutting welfare expenditure, where we have no expertise, but we note that the Institute for Fiscal Studies is sceptical.

Tackle avoidance and evasion – £6bn planned to be raised

Partly to fund those tax cuts, the manifesto says:

“It is vital we make sure people and companies are paying the tax they owe. That’s why, since 2010, Conservative Governments have introduced over 200 measures to tackle tax non-compliance. In total across all the fiscal events we have delivered since 2010, the OBR 16 has scored these measures as raising £95 billion across the forecasts it has produced – £6.7 billion for each year. Building on that, we will raise at least a further £6 billion a year from tackling tax avoidance and evasion by the end of the Parliament.”

The three main parties have provided three very different sets of claims for how much revenue they could raise in each year of the next Parliament:

Both Labour and the Conservatives cite the head of the National Audit Office, who said earlier this year that £6bn could be raised by cracking down on avoidance and evasion. But he didn’t say how, or how much it would cost.

The Labour Party plan is in their “Plan to Close the Tax Gap” document. The Conservatives’ included a plan as part of their National Service press release. This doesn’t appear to be publicly available; we’re publishing it here. The Conservative figures weren’t in that press release, but are in their manifesto costings document. The Lib Dems haven’t published any kind of plan.

Both Labour and the Conservatives cite figures for historic ninefold returns from compliance expenditure. In an email to us, the Lib Dems cited figures from nine to eighteen times. However, all these figures are derived from historic targeted compliance measures which were relatively small. We are a little sceptical that they can be extrapolated to very significant billion pound measures, as is now proposed.

Comparing the Labour and Conservative plans: the Conservatives’ in large part reflects current Government initiatives (unsurprisingly). Labour’s plans are more detailed (as you’d expect, from an opposition with something to prove).

We believe the Labour and Conservative figures are ambitious but may be achievable. We do not believe the Lib Dem figures are achievable in the early years, and the suggestion the £7.2bn figure is year-on-year may be a mistake.

“Triple Lock Plus” for pensioners – £800m in 2025/26, rising to £2.4bn by 2029/30

The manifesto says the Conservatives plan to:

“Cut tax for pensioners with the new Triple Lock Plus, guaranteeing that both the State Pension and the tax free allowance for pensioners always rise with the highest of inflation, earnings or 2.5% – so the new State Pension doesn’t get dragged into income tax.”

This means pensioners will receive a higher tax-free personal allowance than others. That used to be the case, but was phased out from April 2013. So this change is something of a reversal of policy.

The general personal allowance is being frozen, which in real terms means it’s being reduced – a tax rise. So what’s really happening here is that pensioners are being exempted from this tax rise. It’s hard to see how that’s justified, given that pensioners’ incomes are on average higher than those of working age (and their poverty rate is lower).

Abolish stamp duty for first time buyers. £320m cost in 2025/26 rising to £590m in 2029/30

The manifesto says:

“We will ensure the majority of first-time buyers pay no Stamp Duty at all, lowering the upfront costs of buying a first home. We will make permanent the increase to the threshold at which first-time buyers pay Stamp Duty to £425,000 from £300,000, which we introduced in 2022.”

Abolishing stamp duty is easy. The question is whether it makes any actual difference to first time buyers – and the evidence is that it does not.

Research has shown that stamp duty holidays⚠️ and reductions just increase house prices. An HMRC working paper found that the 2011 stamp duty relief for first time buyers had no measurable effect on the numbers of first time buyers. We expect the same result here.

Stamp duty is a terrible tax, and we should abolish it. But abolition needs to be carefully planned in conjunction with other tax reform – otherwise prices will rise, buyers won’t benefit, and the whole exercise just becomes a handout to existing property-owners.

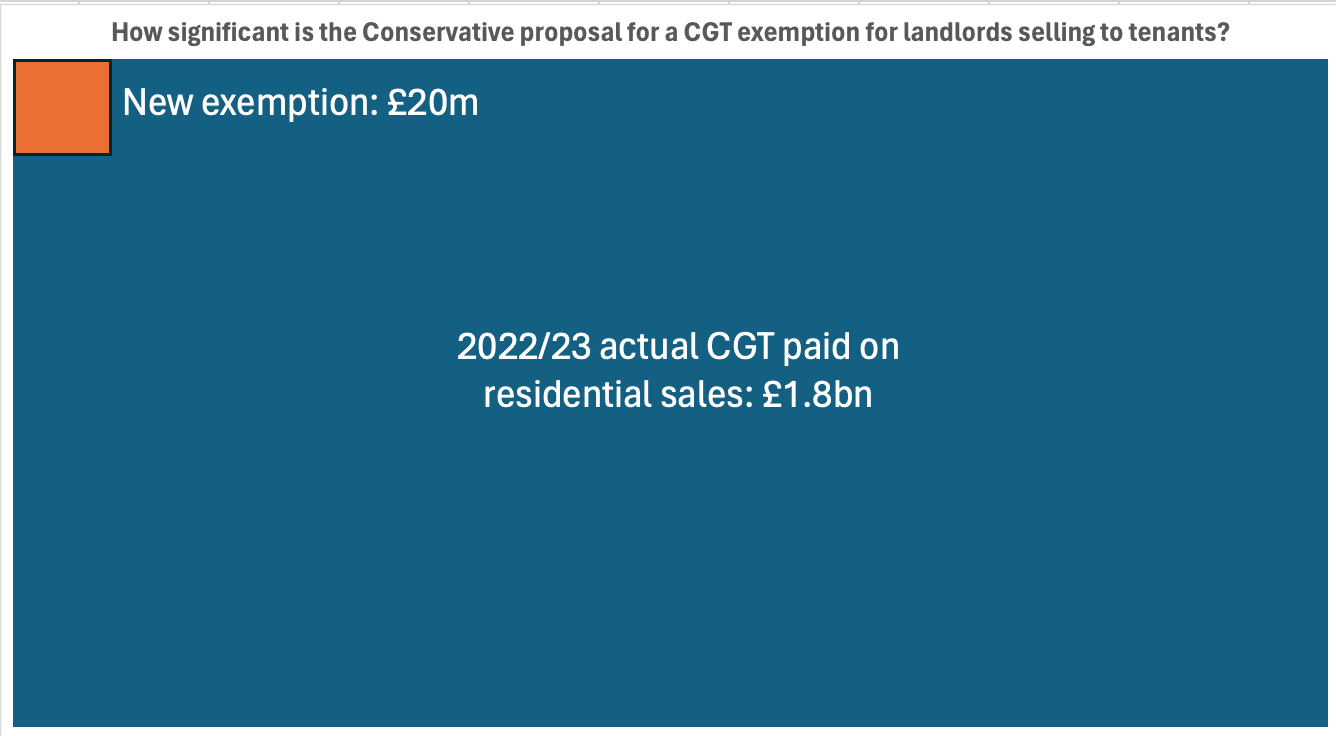

New landlord CGT exemption – £20m cost for two years

The manifesto says:

“To further support homeowners, we will introduce a two-year temporary Capital Gains Tax relief for landlords who sell to their existing tenants.”

This sounded significant until we looked at the costings – the cost this measure is put at just £20m. That means it is almost irrelevant in the context of total CGT on residential property sales:

There is also a serious problem with the proposal. This would be amazingly valuable to some people – there are individual landlords who potentially would have tens of millions of pounds of gains. There is much recent history of incompetent or unscrupulous tax advisers selling avoidance schemes to landlords – we would be confident that schemes would be marketed abusing this relief. It wouldn’t take much for the cost of that abuse to greatly exceed the £20m intended cost.

This comes back to a point we’ve often made: tax reliefs are inherently dangerous: policing the margins of reliefs is difficult, and people will inevitably try to abuse them. It’s much better to have a wide base (i.e. few reliefs) and a lower base.

In our view this is a gimmick which will benefit very few people and could badly backfire.

Child benefit reforms clawback – £954m cost in 2026/27 rising to £1.3bn in 2029/30

“End the unfairness in Child Benefit by moving to a household system, so families don’t start losing Child Benefit until their combined income reaches £120,000 – saving the average family which benefits £1,500.”

This is another cure to a problem created by a previous Conservative Government.

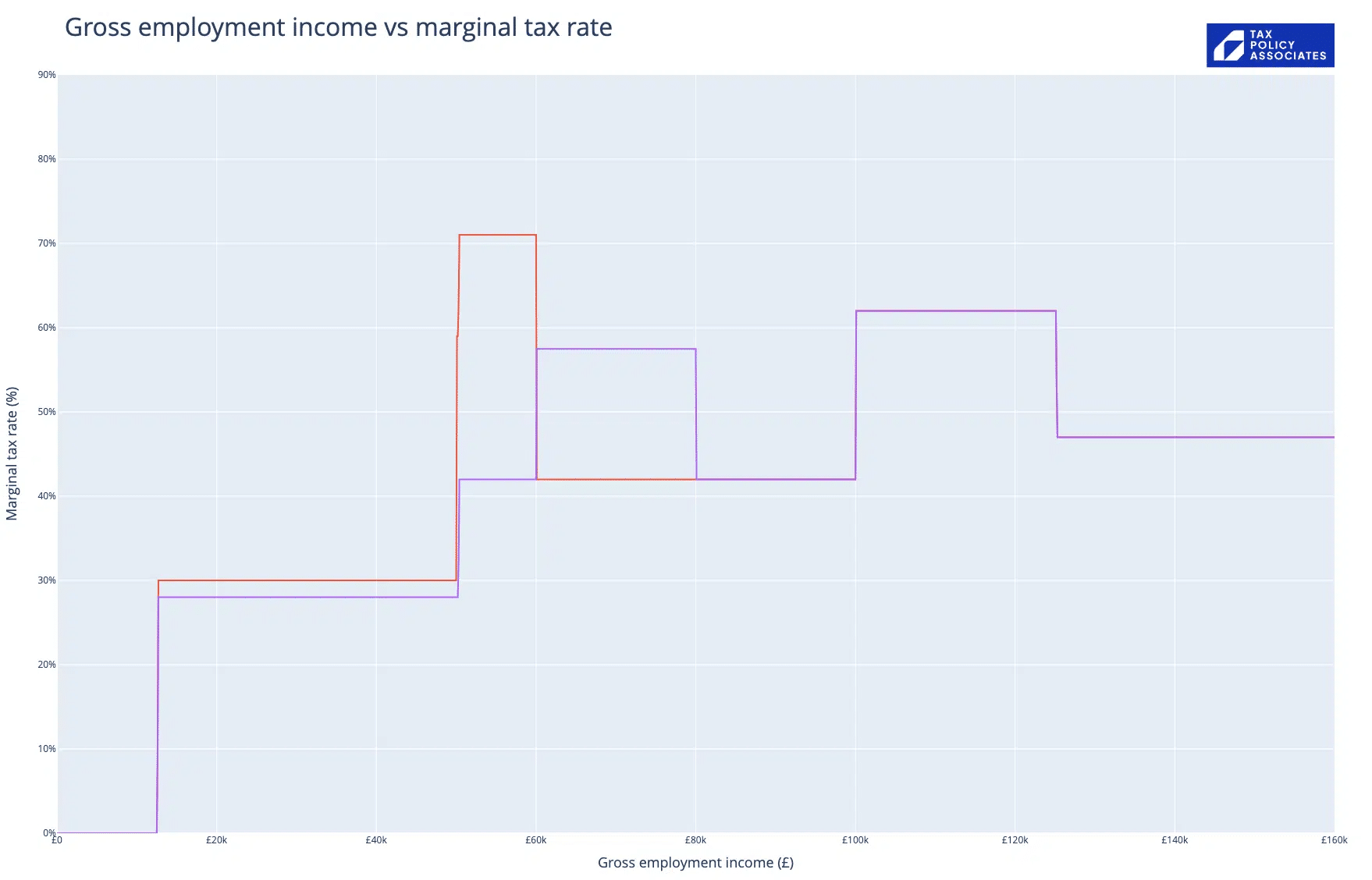

One of the worst of the gimmicks in the tax system is the “high income child benefit charge” (HICBC), which claws back child benefit once your income hits a certain threshold. Until the 2024 Budget, the HICBC meant that a family with three children where the highest earner was on £50k faced a marginal rate of tax of 68%.

The HICBC was, therefore, a problem (with other serious practical issues too, which we discuss here). So Jeremy Hunt deserves credit for making it significantly less awful in this year’s Budget. He moved the HICBC phasing so instead of applying on incomes from £50k to £60k, it applies from 6 April 2024 to incomes from £60k to 80k. That reduced the marginal rates for a graduate with three children under 18 to from 71% to 57%:

(Red is before the Budget; purple is after.)

There’s a more readable interactive version here, that lets you play with and compare all the rates discussed in this article – you can click on the legend to select different scenarios, finger/mouse over to see exact figures, and zoom in/out of details of the chart. The code that creates the marginal rate charts is available on our github.

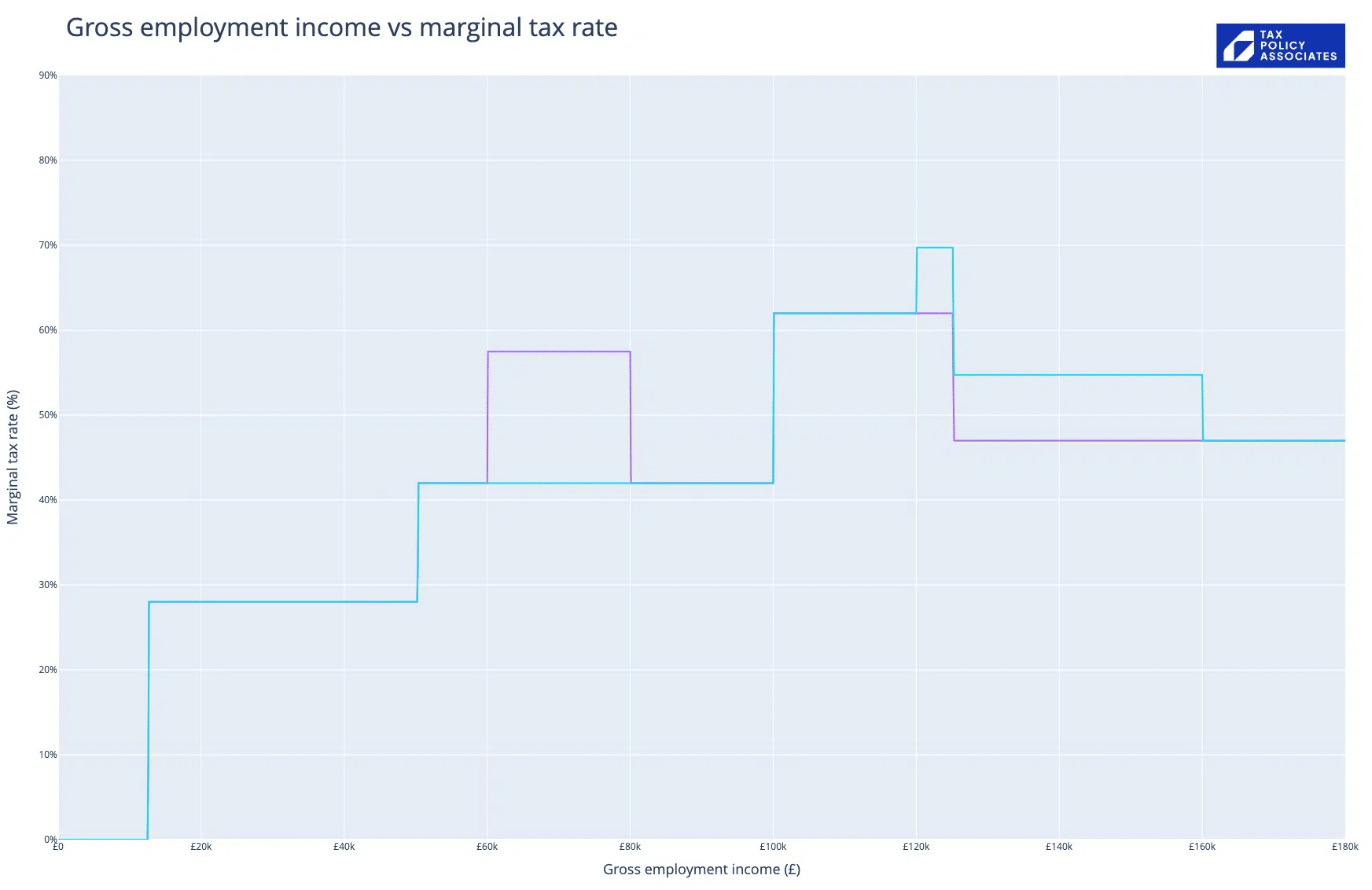

The Conservative manifesto now proposes to move the threshold from £60k to £120k.

That’s good news for people earning £60k – their marginal rate drops right back down to 42%.

However, this creates a new and very high marginal rate of 70% for parents with three children under 18 earning between £120k and £125k:

(Purple is after the Budget; blue is today’s announcement)

Why? Because the personal allowance clawback already creates a 62% marginal tax rate for everyone earning between £100k and £125k. And the Tories are moving the child benefit clawback so it partially overlaps with the personal allowance clawback.

The 70% rate is bad but temporary. The more serious effect is that, once earnings get past the £125k point, there’s a 55% marginal tax rate all the way up to £160k (after that, the marginal rate reverts to the standard 47%). Of course these rates will be less for people with less than three children under 18, and higher for people with more.

This feels like a serious mistake. The Conservatives should have had the courage of their convictions, and ended the HICBC altogether.

Moving to a household basis

The manifesto also adopts current Government policy of changing the HICBC so, instead of applying by reference to the highest earner in the household, it applies to the overall household income.

The difficulty is that the tax system doesn’t track household income. Married couples used to be taxed on their joint income – that was scrapped⚠️ following a decades-long feminist campaign for independent taxation. There’s an almost unanimous view amongst tax policy wonks that this change will be technically complex, and in some cases cause hardship.

It’s correct that applying HICBC to the highest earner is often unfair – a couple each earning £49k aren’t caught by the HICBC, but a couple where only one is working, earning £60k, are caught. But any change needs to fully think through the new unfairnesses that it will create. It’s not clear that has been done.

Thanks to P and L for their work on this article.

Disclosure: Our founder, Dan Neidle, is a member of the Labour Party, and sits on its most senior disciplinary body. His tax policy analysis is widely regarded as non-partisan, and he was highly critical of Labour Party tax proposals in the 2017 and 2019 elections.

Footnotes

See page 31 of the CBI report ↩︎

It’s not merely that HMRC funding has failed to keep pace with inflation; its most experienced personnel have been moved onto other projects, particularly Brexit and the pandemic. See paragraph 1.8 onwards in this National Audit Office report. This was probably sensible, but is having long term consequences. ↩︎

A tax reform agenda for tomorrow’s Chancellor

Our take on the Reform UK manifesto

Our take on the Labour manifesto

Our take on the Green Party manifesto

Our take on the Lib Dem manifesto

Leave a Reply