Reform UK has published its manifesto. They plan personal tax cuts which they say will cost £70bn; however our analysis shows that they’ve miscalculated, and the actual cost will be at least £88bn.

Reform UK says it will fund these tax costs with £70bn of savings and additional revenue, but it provides few details. Their proposal to change Bank of England reserve rules is over-stated by at least £15bn, and the cost would likely fall on businesses and consumers, not banks.

These two factors mean that Reform UK’s plans have a total unfunded cost of at least £33bn – about twice the unfunded cost of Liz Truss’ ill-fated 2022 “mini-Budget“.1

We hope other estimates become available soon, but for the moment this is the only currently available estimate of the impact of Reform UK’s proposals. We asked Reform UK for the calculations they had used; they did not respond.

We have published our methodology in full, together with the supporting spreadsheet and modelling. We welcome suggestions and corrections.

Our analysis is for tax year 2025/26 only; the cost will be higher towards the end of the Parliament. And, as the Institute for Fiscal Studies points out, the long-run annual cost will be higher still.

The overall tax effect of the manifesto

We have previously said that the tax increases that Labour and the Conservatives were arguing about were so small as to be irrelevant.

Reform UK, on the other hand, are proposing £70bn of personal tax cuts:

And £18bn of business tax cuts:

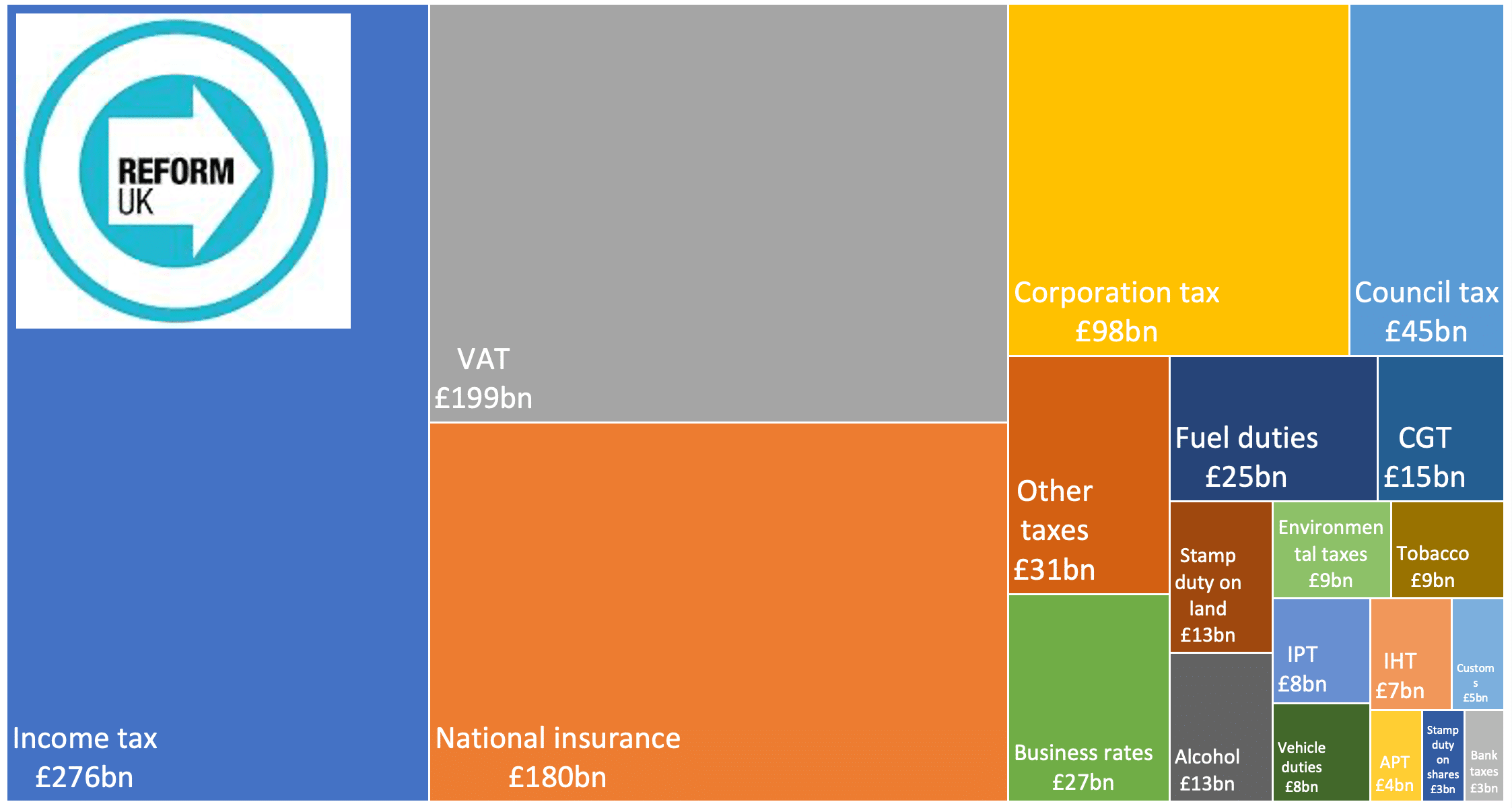

This chart superimposes the size of Reform’s tax cuts over all the figures for UK tax receipts in 2023/24 (and, for ease, it’s in the top left, but not all the cuts are to income tax):

Costing the tax cuts

Reform UK don’t break down their estimates between their various tax cuts, and provide no explanation for how they arrived at their figures. All they present is the £70bn and £18bn totals:

Reform UK’s lack of detail is very disappointing given the ambition and magnitude of their tax costs.

Our analysis is that the £70bn figure for personal tax cuts is a significant under-counting of the actual cost, even when we make very generous assumptions as to the cost of each measure.2 Our breakdown looks like this:

We were not able to properly assess the £18bn figure for business tax cuts, because it lacks sufficient detail. In particular, we do not know what is meant by “abolish IR35”. However we believe that the minimum cost is very close to Reform UK’s actual estimated cost. The actual cost could be many £bn higher, depending upon what precisely Reform UK’s proposals actually are:

If Reform UK are serious about entirely abolishing IR35, and not just changing the enforcement rules, then the cost would be very much higher than this.

We set out below the methodology we used in arriving at these figures.

Methodology – income tax cuts

Increase income tax personal allowance to £20k and increase higher rate from £50k to £70k

Increasing the personal allowance is very expensive, because it benefits everyone earning above £12,5703 – that’s 70% of all taxpayers. Increasing the higher rate affects everyone earning over £50k – which will be about 21% of all taxpayers in 2025/26.

The easiest way to assess many proposed changes in tax rules is to use the “direct effects of illustrative tax changes bulletin” provided by HMRC – sometimes called the “ready-reckoner”.

Using the figures in the ready-reckoner suggests that increasing the personal allowance by 10% costs £10.6bn for 2025-26, and increasing the starting point of the higher rate by 10% costs £5.4bn. On its face, that means the overall cost of the Reform UK proposals would be £82bn.4

However the ready-reckoner was prepared to illustrate the effect of small changes. It is not intended or designed to be used to model the kinds of large changes Reform UK are proposing.

Reform UK’s proposal can be modelled statically as follows:

- Take HMRC’s income percentiles for 2020/21

- Update the income in each percentile by an inflator so that the percentage paying higher rate tax accords with the percentage for 2025/26 set out in table 3.4 of the OBR’s latest economic and fiscal outlook.

- For each percentile:

- Calculate the tax due under current rules, and subtract the tax due under the Reform UK proposals. This gives the revenue cost of Reform UK’s income tax proposals for one taxpayer in this percentile.

- Multiply that by the total number of income tax payers (also from table 3.4) and divide by 100 – this gives the total revenue cost for all taxpayers in this percentile.

- Repeat for all percentiles and add together: this gives the total revenue cost of the Reform UK income tax proposals.

The result of this is an estimated revenue cost of £70bn.

This is a simple static calculation. In reality, declared taxable income increases when tax rates reduce; in part this is people paying tax that was previously avoided or evaded. In part this is people rationally deciding to take on more work when tax rates drop. Any realistic estimate of the impact of tax changes, particularly large ones, should take account of these “dynamic” effects.

We can express these effects quantitatively as the “elasticity of taxable income” or ETI – the amount that declared income will change when the rate of tax changes.5 However estimating the ETI is very difficult, and there has always been a wide variation in results. We see larger elasticities for large tax changes, and larger elasticities for higher earners⚠️. Research suggests that for moderate earners in the UK (i.e. not the very wealthy), the figure is likely between 0.10 and 0.30. There is an excellent summary of the state of the research in this Scottish Fiscal Commission paper, table 4.2, page 17, and a clear explanation of how ETIs work on page 16 (although they refer to ETIs as TIEs).

We included dynamic effects into the methodology above, using what we think is a reasonable “best case” scenario for Reform UK by taking the rather high ETIs used by the Scottish Fiscal Commission (see page 20 of the paper). We say this is a “best case” because Scottish ETIs are higher than rest-of-UK ETIs for the obvious reason that it’s relatively easy for many Scottish taxpayers to escape Scottish tax by moving over the border to England. However, as we will explain below, the exact ETI chosen does not materially impact the analysis.

The methodology for each income percentile is then as follows:

- calculate the tax position of a taxpayer in that percentile under current rules, and their marginal rate

- calculate the tax position of the taxpayer under Reform UK’s proposals

- increase their pre-tax income by (% increase in marginal rate) x ETI for that level of income

- calculate final tax position in light of increased taxable income

On this basis, the estimated revenue cost is £68bn, only slightly less than the static costs.

One might wonder why dynamic effects are so limited. The reason is that ETI operates at the marginal rate, and the Reform UK proposal doesn’t do much to marginal rates:

- Moving the higher rate threshold to £70k reduces the marginal rate for taxpayers earning between £50k and £70k, because they are now paying the 22% basic rate (plus NI) or their income instead of 42% higher rate (plus NI). In our model, for example a taxpayer on £60k increases their declared taxable income by about £2k, meaning they pay around £500 more tax.

- A taxpayer earning more than £70k pays £4k less tax (i.e. because they now have £20k of income taxed at 22% not 42%) but this is a windfall that doesn’t change their marginal rate. Tax elasticity theory says they therefore have no additional incentive to earn.

- Moving the personal allowance to £20k has a big benefit for people on incomes just below that – someone on £19k sees their marginal rate fall from 28% to 19%. But on such low incomes the magnitude of incentive effects are limited.

- And taxpayers earning more than £20k receive a £1,634 tax cut (because they now have £7.5k taxed at 0% rather than 22%) but again it’s a windfall that doesn’t change their marginal rate. Increasing the personal allowance is very expensive.

So the final result is not very sensitive to the ETIs used – if we (unrealistically) double the ETIs, only £2bn of additional tax is collected. Dynamic effects are much greater if you cut rates rather than increase thresholds. For example, and purely for illustrative purposes, our model suggests that if took the very dramatic step of replacing all of income tax with a flat tax of 17% it would cost £84bn on a static basis, but £12bn of dynamic effects mean the end cost would be about the same as Reform UK’s (£72bn). That is, however, on the basis of the unrealistically high ETIs we are using to be generous to Reform UK’s proposal, and a very simplified model – that would almost certainly not be the result in reality. However it does illustrate that tax cuts should be designed to cut marginal rates – this makes them more affordable, which is another way of saying that they are then more effective at driving growth.

These are, therefore, badly designed tax cuts, that don’t provide much “bang for the buck” and are unlikely to drive growth.

All these calculations were performed using an adaption of the well-tested code used to create our marginal tax rate chart. We have made the new code available on our GitHub here.6

This is a simple model with important limitations. In particular:

- It assumes everybody is only receiving employment income (and not self-employment income, rent, dividends etc). That means the model cannot be used for e.g. changes in the level of national insurance or tax on passive income. However, Reform UK’s proposal affects all types of income without regard to the source, and therefore this limitation doesn’t impact our analysis.

- It doesn’t properly model the income of the top 1%, because it analyses it as if all the top 1% earned the base pre-tax income for that percentile of £216k. In fact the income of the top 1% is much higher than this – there are 28,000 people with income over £1 million, collectively paying £28.3 billion in income tax – that’s more tax than the 18 million taxpayers earning less than £20k. This means the model will dramatically undercount the cost and ETI effects of tax changes that impact the marginal rates of people earning more than £216k. However, Reform UK’s proposal does not affect the marginal rates of anyone earning more than £70k, and therefore this limitation doesn’t impact our analysis.

- When people’s after-tax income increases, they are likely to spend more, especially those on lower incomes. This increased spending often results in higher VAT revenue and stimulates economic activity, creating positive ripple effects throughout the economy. Conversely, reduced government expenditure resulting from a tax cut can decrease the income of others in the economy, leading to negative ripple effects.7A full analysis would require detailed econometric modelling, but the economists we spoke to were reasonably confident there would be an overall negative effect given that most of the benefit of Reform UK’s tax cuts goes to higher-income individuals, who have a lower propensity to spend.

Methodology – other personal tax cuts

All the calculations supporting the figures below are set out in the spreadsheet available on our GitHub.

Scrap VAT on energy bills

There is a figure for this in HMRC’s document setting out the cost of different reliefs – the current rate of 5% is estimated to represent a revenue cost of £8bn compared to if it was at the standard rate of 20%. Hence the cost of scrapping the 5% rate will be approximately £3bn.8

Lower fuel duty by 20p per litre

The ready-reckoner suggests a cost of £9bn for reducing fuel duty by 20p. We understand that this figure includes dynamic effects (i.e. people using more fuel when duty falls).

We can sense-check this result by adjusting the current £25bn fuel duty yield to reflect a 20p cut. That results in a figure of £10bn – this will be a slight over-estimate given that the HMRC data includes non-domestic fuel duty (e.g. aviation fuel).

We can sense-check again using RAC figures for the volume of petrol and diesel sold in the UK. That gives a figure of £12bn – but it will include agricultural petrol and diesel, which is not taxed.

We will therefore use the £9bn figure.

These calculations are shown in the spreadsheet available on our GitHub here.

Stamp duty

The current rates are 0% for up to £250k, 5% to £925k, 10% to £1.5m and 12% thereafter.

Reform want to cut this to 0% up to £750k, 2% up to £1.5m and 4% thereafter.

We can calculate this with the HMRC ready-reckoner.9 The total comes to £3bn.

The calculations are again shown in the spreadsheet available on our GitHub.

It’s important to note that this change would likely result in increased property prices – buyers would probably not end up better off. This therefore ends up as an expensive house price subsidy. We explain why here.

Inheritance tax – increase nil rate band from £325k to £2m

This is again too big an increase for the HMRC “ready-reckoner” to be useful.10

We can better estimate the result from the raw data on IHT returns, calculating the revenue reduction at each level of estate value. This comes to £5bn. Dynamic effects are obviously limited.11

Methodology – business tax cuts

All the calculations supporting the figures below are set out in the spreadsheet available on our GitHub.

Reduction in corporation tax from 25% to 20%

The “ready-reckoner” suggests a figure of £18.5bn, but that should be viewed with caution given the magnitude of the change.

The 2022 Autumn Statement reversed the tax cut from the controversial Spring Statement, and put the rate back from 19% to 25%. The stated revenue from this was £17bn for 2025/26. It follows that we can prudently estimate the cost of a cut from 25% to 20% as £14.2bn. We would suggest that is the appropriate figure to use.

Lift minimum profit threshold to £100k

We do not understand this proposal.

Currently the rate for companies with profit of less than £50k is 19%; the rate for companies with a profit of more than £250k is 25%. Between these £50k and £250k the rate smoothly increases.

But Reform UK are proposing cutting the rate to 20%. What is the point of a special small company rate of 19%? The small company rules are highly complex and create an administration headache for taxpayers and HMRC. That is perhaps justified where the tax rate saving is 6% – it cannot be sensible where the tax rate saving is 1%.

We calculate the cost of the tax cut, and therefore the total benefit to small business, as a very small £100m.

Lift VAT threshold to from £90k to £120k

In our view this would be a serious mistake which would cause many growing small companies to constrain their growth to £120,000. We already see this effect at the £85,000 level of the current VAT threshold, where there is a “bulge” in the statistics of companies holding back their growth. That effect would be more serious (and more deleterious to economic growth) at a higher turnover level. Our analysis of the current situation is here.

We can estimate this in two ways.

First, we can look at the £185m cost of increasing the threshold from £85k to £90k in the most recent budget, and simply multiply that by five. That results in a figure of £1.1bn.

Alternatively, we can look at the £2.3bn of total VAT (see table T5b) paid by companies with a turnover of between £85k and £150k, and pro-rate that linearly to reflect a £120k threshold, resulting in a figure of £1.2bn.

We will use the £1.1bn figure.

Abolish IR35

We do not know what this means.

“IR35” is name usually given to the rules introduced in 2000 to stop people who are realistically employed from instead being engaged as contractors, via a personal service company (PSCs). PSCs were widely used in cases where someone (particularly IT consultants working for large businesses) was working as part of a team for a long period of time, and being treated in almost every respect as an employee.

If Reform UK were really going to abolish these rules then we would see a return to the very large-scale levels of avoidance seen in the 1990s – except it would now be worse given that corporation tax has fallen, and income tax has risen, making PSCs more attractive and the losses from avoidance therefore greater. We are not at this point able to estimate the cost in lost tax, but it would be very high indeed, plausibly £10bn or more.

There have been more recent changes to IR35. Some larger employers failed to apply the rules correctly, relying on the fact that the risk of this was on the contractor or their PSC, not the employer. So in 2017, rules were introduced putting liability on public sector employers ; the stated revenue from this measure was around £150m/year. In 2021, this was extended to the private sector; the stated revenue from this for 2025/26 was about £1.7bn/year.12 It is important to stress that the 2017 and 2021 changes do not alter the technical application of IR35 at all; all they do is change the person who is liable to the employing business, and therefore effectively force businesses to take the rules more seriously.

It may be that Reform UK are only proposing to abolish the 2017 and 2021 reforms – in that case the cost would be around £1.8bn. This would in our view be unwise, because it rewards businesses that ignore the law.

Assessing the revenue-raising

Reform UK say:

And they put figures on these proposals here:

These are massive numbers – about 5% of GDP in total. No details are provided; it is also unclear how “first 100 day tax cuts” can be funded from savings that would take time to implement. The 5% figure ignores the fact that some areas (e.g. the NHS) are said to be protected from cuts. And the long-term impact of significantly reducing immigration surely deserves more analysis than one number in a table.

We, however, will focus on the “stop bank interest” figure of £35bn figure, which arises from (broadly speaking) ending the practice of the Bank of England paying interest on the reserves placed with it by UK banks.

This is a proposal that’s been made by others, including Chris Giles (the economic commentator) and the Left-wing New Economics Foundation. However Reform UK’s figure is much higher than anyone else’s, and we doubt it is correct:

- The fundamental business of banks is charging customers an interest rate that reflects their own average/marginal cost of funding (plus a margin). If their costs increase, the interest rate increases. So, for example, there is good evidence⚠️ that the cost of a levy on banks isn’t actually borne by banks, but by their mortgage customers in the form of higher rates. We expect the same would be true here – ultimately it would be consumers and (non-bank) businesses paying the most of that £35bn cost, in higher borrowing rates or lower savings rates.

- That is all the more so given that we estimate that total UK profits of the bank sector are around £30bn.13.

- If interest rates fall, the figure will fall from £35bn. This is not a sustainable way of funding a long term tax cut.

- Experts in monetary policy think £35bn is much too big a figure. The New Economics Foundation suggested a realistic figure was £19bn. The Institute for Fiscal Studies thinks slightly less. Chris Giles has said around £5bn to £10bn is a realistic figure.14.

- And economics and financial markets expert Toby Nangle thinks there would be much wider economic implications to Reform UK’s approach. In macroeconomic terms, the proposal amounts to “helicopter money“. More seriously, the Bank of England would risk losing monetary control. Toby thinks these risks would be minimal if the Bank of England slowly ramped up the proportion of reserves on which it didn’t pay interest (to say the kind of £5-10bn figure Chris Giles suggests).

- Reform UK don’t appear to have considered any of these issues at all; the Toby Nangle article gives the impression that Reform UK were hearing them for the first time.

Reform UK’s revenue projections therefore appear to be over-stated by at least £15bn and possibly as much as £30bn, the actual revenues would likely come at the expense of households and businesses, not banks and their shareholders, and there are complex macroeconomic consequences which Reform UK appears to not have considered.

Thanks to O, R and K for their work on the calculations and modelling.

Disclosure: Our founder, Dan Neidle, is a member of the Labour Party, and sits on its most senior disciplinary body. His tax advice has always been regarded as non-partisan, and he was highly critical of Labour Party tax proposals in the 2017 and 2019 elections.

Footnotes

The cost of the mini-Budget was projected by the Truss government to be £19bn in 2022/23, rising to £45bn by 2026/27, and others thought the true figures would be higher ↩︎

Note that these figures don’t include Reform UK’s proposal to exempt all NHS medical staff from basic rate income tax for three years – this seems to be included in the £17bn “NHS pledge” rather than on the tax side. No breakdown of the £17bn is provided, but we can estimate the cost from the 627,000 FTE medically-qualified NHS staff and the average NHS FTE pay of £38,000. After Reform UK’s £20k personal allowance, that’s a basic rate tax saving of £3,600 each, so about £2.3bn altogether. Thanks to James Goffin for asking about this. ↩︎

Until the point at the personal allowance gets phased out; £125k at the moment. ↩︎

With Reform’s 60% increase in the personal allowance costing £60bn and the 40% increase in the higher rate costing £22bn ↩︎

Or, more precisely, the rate of retaining after-tax income changes) ↩︎

UK_tax_change_calculator.py is the script, using the same UK_marginal_tax_datasets.json as the marginal tax rate calculator, with a new dataset added into that json for the Reform UK proposal ↩︎

One might expect these two effects to cancel out, but that is not necessarily the case. It largely depends on who receives the benefit of the tax cuts and who faces lower income from reduced government expenditure. Tax cuts for lower-income individuals typically have a higher multiplier effect compared to cuts for higher-income individuals who might save more – people on lower income spend more – they have a higher “propensity to spend“. Government spending can also have a higher multiplier effect, depending on the nature of the spending, the economy’s capacity at the time, and wider macroeconomic conditions – in some circumstances government spending can “crowd out” private spending. The OBR has published an excellent summary of how they model multiplier effects. ↩︎

Many thanks to Paul in the comments for pointing out an error in the initial version of this report. Our apologies. ↩︎

Reform UK’s bands are different from the current stamp duty bands; we adjusted for that with a simple pro rata calculation. ↩︎

It provides an estimate of £90m for increasing the nil rate band by £5,000. A linear application of that to Reform UK’s increase results in reduced revenues of £30bn, which is obviously nonsensical. ↩︎

But not zero – there is evidence that the timing of reported deaths is affected by inheritance tax rates. ↩︎

The figure comes as a result of the Truss/Kwarteng abolition of this rule in the 2021 “mini-Budget” and its subsequent reinstatement. There is an extended analysis for this here. ↩︎

See the second tab of our spreadsheet, available on our GitHub. Note that this is lower than the figure for the total profits of the UK banks, because much of this profit is generated overseas. Our figure is, however, too high, because it will include foreign banks with UK operations; but only UK banks place reserves with the Bank of England. ↩︎

That is derived from the “non-remunerated” tier and so is a sustainable figure, not affected by changes in rates ↩︎

Ten better tax cuts than Reform’s £14bn overtime gimmick

The £34bn cost of Reform UK’s “Britannia card” proposal

A tax reform agenda for tomorrow’s Chancellor

Our take on the Labour manifesto

Our take on the Green Party manifesto

Leave a Reply