Updated: raising corporation tax to 25% will take the effective rate to the highest it’s ever been in the UK, and one the highest in the developed world. That’s bad – but the alternatives are worse.

The Johnson government increased corporation tax from 19% to 25% from April 2023. The mini-Budget reversed this. Then Jeremy Hunt’s Autumn Statement reversed the reversal, taking the rate back to 25% from April. Not a hugely stable environment for business. But how should we assess the merits of the increase to 25%? Should we reverse the reversal of the reversal?

The standard argument for the increase goes something like this:

“We’ve been cutting corporate tax for 25 years, it’s gone too far, and it’s time to go back to 25%. After all, the rate was 33% in the 80s, and is now 19%, so 25% is still a pretty good deal.”

That argument is usually accompanied by this chart, showing the headline rate falling dramatically:

This is rather less persuasive if we look at the corporate tax actually paid – here’s an overlay showing UK corporation tax receipts (in red) as a % of GDP:

The rate fell. The revenues bounced around with the business cycle, but fundamentally didn’t change much, if at all.

Could it just be that corporate profits rose, so the declining rate multiplied by increased profits kept revenues broadly constant? We can test that by dividing corporation tax revenues by the corporate “gross operating surplus” in the national accounts, which gives us a reasonable proxy for the overall effective tax rate.1 Again we see that the plummeting headline rate does not lead to much, or perhaps any, reduction in the actual effective rate (particularly bearing in mind that the 2020 figures are depressed by Covid).2:

How can the tax take remain the same when the rate has fallen so dramatically? Because of a series of technical changes that meant that, at each stage when the rate went down, the tax base (the definition of “profits” to which the rate applies) expanded. Tax = rate x base. So, through accident or brilliant HM Treasury design, nothing much changed.3

The rate increase to 25% is, by contrast, accompanied by nothing that reduces the tax base. It will therefore simply represent a 1/3 increase in the amount of tax companies pay, making our chart look like this:4

And UK corporate tax will, as a % of GDP, become one of the highest in the developed world – of large economies, only Japan and Canada’s would be higher:5

So I am convinced that raising corporate tax is a bad idea. The problem, however, is that the 25% increase was “banked” in government accounts, and the cancellation of the increase in the mini-Budget was unfunded. The £16bn+ it costs would therefore have been distributed opaquely throughout society through inflation and/or higher interest rates. I don’t regard that as good tax policy.

Alternatively one could keep the rate at 19% by cutting spending, or raising taxes elsewhere – that would certainly be a rational position to take (whether you agree with it or not), but it’s an argument that I don’t hear anyone making.

And, finally, you could argue that increasing the rate to 25% will actually bring in no more revenue, because profits will drop – in other words, the 25% is past the “revenue maximising point”. The problem with this is that there’s no evidence for it in the response to previous rate reductions.

So taking the rate to 25% feels like the least bad of several bad ideas. I therefore unenthusiastically support it.

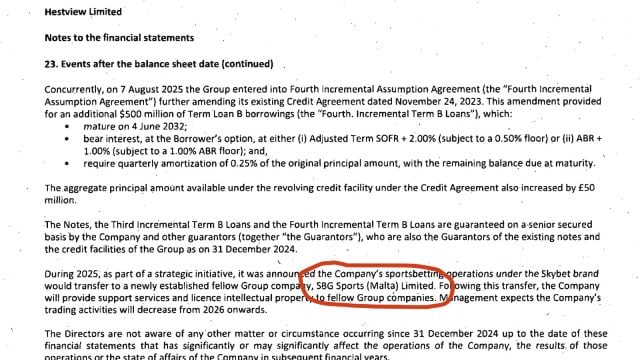

Betting on tax avoidance – is Sky Bet avoiding £55m tax per year?

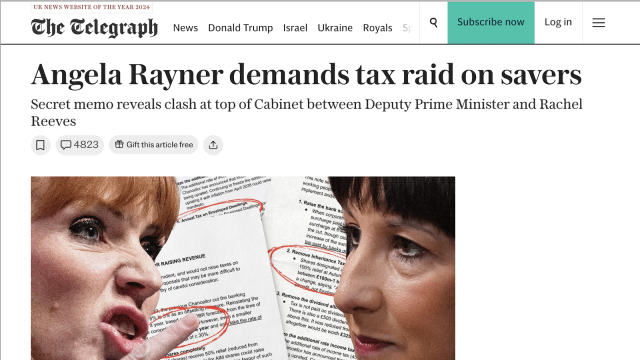

The Angela Rayner tax proposals – how much sense do they make?

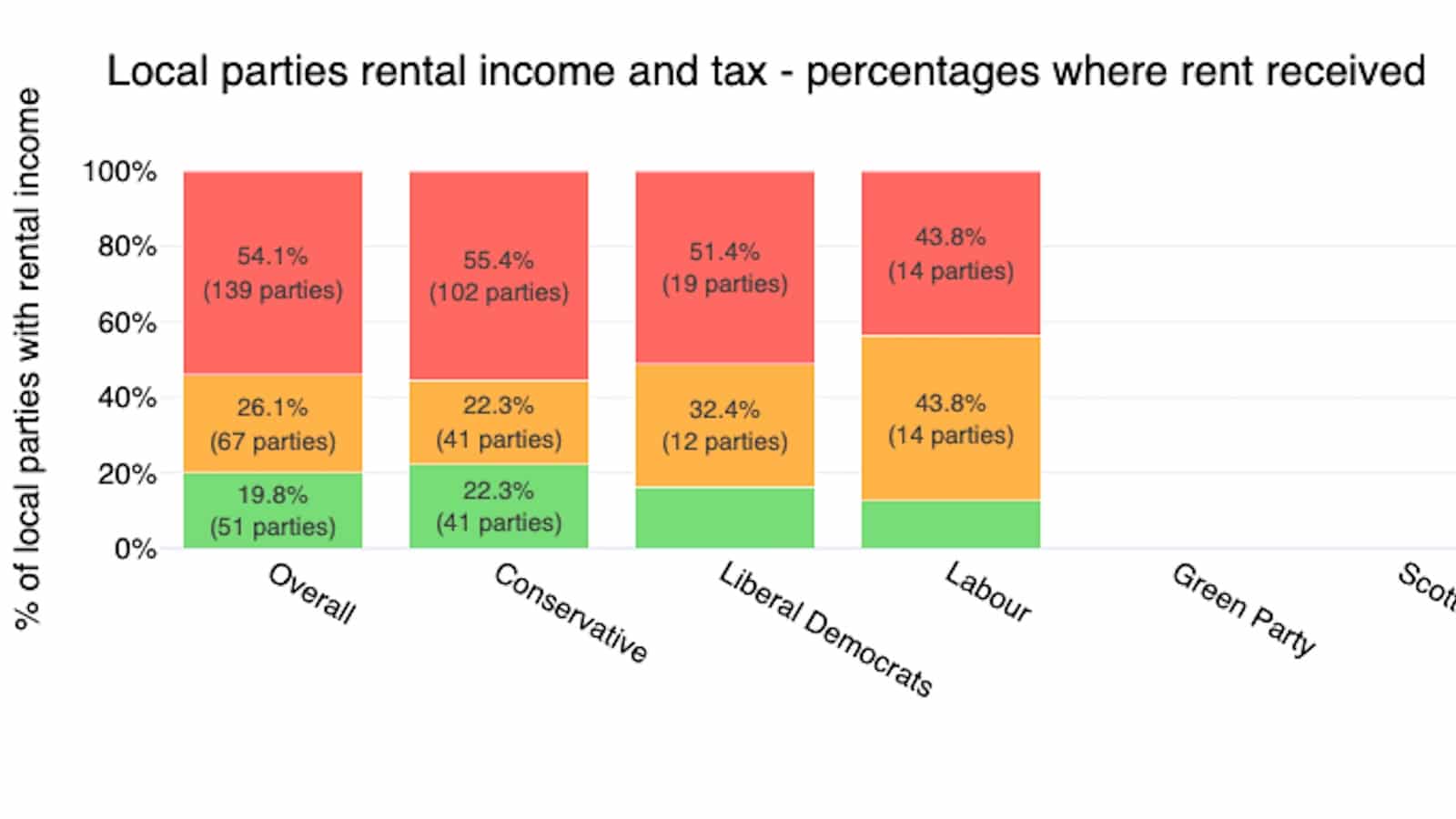

Political parties failing to pay tax on rent – including rent funded by MPs’ expenses

The tax longlist – 35 ways Rachel Reeves could raise £22bn

How to reform corporation tax

The reality of tax complexity, and how to fix it

Footnotes

Two big caveats: (1) GOS is not the same as accounting profit, and in particular excludes depreciation (so the chart understates ETR), (2) the tax stats are for cash collected by HMRC in a tax year, which used to lag profits by around a year, and now mainly doesn’t – neither factor should affect the overall trend, but both will create/mask considerable noise. With some work they could be corrected, and I’d love it if someone did that. ↩︎

I’ve added a trendline which shows a slight increase over time, but I’d be hesitant to draw too many conclusions given the large fluctuations across the business cycle ↩︎

Another factor is that a wave of incorporation by small businesses has artificially inflated corporation tax revenues, but at the cost of (greater) reductions in income tax. This effect, however, is too small to impact the trends visible in the charts above – it’s about £1bn. ↩︎

It would have gone higher than this, because this chart doesn’t include the effect of the bank surcharge, which at 8% would have meant banks would have been be paying 33% on their profits. However, controversially but sensibly, the increase to 25% was accompanied by a reduction in the surcharge to 3% ↩︎

And Canada, like Australia, is driven by the high tax revenues from mining/oil/gas ↩︎

Leave a Reply