I just wrote in the Sunday Times about the political and economic case for a land value tax. I think the principled argument for LVT is compelling, and our (likely) next Prime Minister has supported it for many years.1, calling it “aspirational socialism”; a 2022 LBC interview described LVT as “a very productive form of taxation” that could discourage land hoarding; and at his 22 May 2026 Makerfield launch he said he had “long been persuaded of the argument for a Land Value Tax”, while describing council tax as “highly regressive” and its 1991 valuations as “not justifiable”. But Burnham has also supported Fairer Share‘s tax on the whole value of property, which is not LVT. There’s a good CIOT article on Andy Burnham’s tax positions.[/mfn] The challenge is the detail – and wrapped up in that is who wins and who loses. So this article is not about the case for land value tax. It’s about the detail: how a land value tax would work in practice, and what the key design questions and challenges are. It’s based on a simplified model of how a land value tax could apply to English residential property. The model helps answer the first question most people have: who will pay? More importantly, the model prompts a series of questions around the problems and limitations of a land value tax, and the potential compromises with reality that have to be made.

The principled case for LVT is easy. The practical case for LVT seems equally straightforward if we look at the headline result that (on our model) at least 63% of people will benefit in immediate cash terms2, and easier still if you consider the long run benefits for everybody. But, once we get beyond that headline figure, the implementation is difficult, and the politics is really difficult. This article is intended to help frame both.3

At this point, I do not have answers, but I have a better idea of what the questions are. It’s normally said the big problem with land value tax is valuation. That’s certainly a very serious challenge, but to my mind bigger problems are (1) very substantial tax increases for some people, particularly in London, and (2) capitalisation: the prospect of a sudden shock that, overnight, greatly reduces property prices in some parts of the country (think: Kensington) and greatly increases them in others (think: Blackpool). Neither is desirable. The most plausible solution is to phase in the tax over a long period. That may not be enough – and land value tax proponents may have to accept complexity and deviation from the beautiful purity of the LVT concept.

This report starts with the model – which you can see here. Below this is a full discussion of how to use the model, what it means, and — most importantly — its limitations. You may find it helpful to open the model in a separate tab by clicking here, so you can view model and discussion at the same time.

We are not the first to publish a sophisticated online model of land value tax. PolicyEngine has produced a much better model than ours for examining the distributional consequences across households: it is a proper microsimulation model, using household survey data to show effects by income, family type and poverty status. Anyone principally interested in who gains and loses across the income distribution should start there. Progress and Property, meanwhile, has produced a much more spatially detailed valuation tool, using property boundaries and local data to estimate land values at something approaching individual-property level. Its underlying methodology and code do not appear to be published, however, so unlike our model (or PolicyEngine’s) its results cannot presently be reproduced or independently tested.

Our model was built to answer a different set of questions: what happens if residential council tax and stamp duty are replaced by LVT; how the results vary geographically; and what difference is made by progressive rates, regionalisation, transitional relief, deferral and phase-in. As far as we are aware, this is the first public model to combine those features. It is therefore not the best available model for every purpose, but it is (I think) the first that does the particular job we wanted done.

The way the model works, what it tells us, and wider questions about a land value tax are discussed in detail below. You can click these buttons to jump to each section.

Why a land value tax?

A very short version of my Sunday Times piece would go: the UK’s three existing property taxes: stamp duty land tax, council tax, and business rates4 are broken, unfair and anti-growth. They are also huge – and result in the UK having the largest property tax (as a portion of GDP) of any OECD country:

Stamp duty is particularly bad: it reduces household mobility, results in inefficient use of land, and plausibly holds back economic growth.5 A land value tax would be more equitable and efficient. And taxing land is better for growth than taxing any other income or asset because normally when you tax something, you get less of it, but when you tax land, you do not. In fact, you incentivise more efficient use of the land.6

Whatever your view of tax and the size of the State, land value tax makes sense. If you believe in a smaller State, then you should want income and corporation tax cut and land taxes to go up. If you believe in a larger State, you should want more tax raised from land. Either way, taxing land is pro-growth.7 The burden should fall primarily on landlords not tenants. How many other ideas are backed by the Institute of Economic Affairs, the Adam Smith Institute, the Institute for Fiscal Studies, the New Economics Foundation, the Resolution Foundation, the Centre for Economic Policy Research, and the chief economics correspondent at the FT?8

Our LVT model

This is a simple model with many limitations, and I talk about them below. It’s useful for seeing the rough overall impact of a land value tax – who gains, who loses, by roughly how much, and how design decisions change these results. It is not, by any means, a robust model of how a land value tax would actually work, and none of the individual figures should be treated as precise. I support a land value tax that covers residential and commercial property, but to keep this project manageable, the model and this article only discuss residential property.

You should start by launching the model (clicking that and the other links below open a new tab with a saved view illustrating the point). This shows that a pure land value tax can replace residential stamp duty land tax and council tax if we set it at a rate of 1.28%.

You can then see:

- Biggest winners: deprived North East and coastal towns – Hartlepool, Blackpool, Middlesbrough – where households would pay around £1,600 a year less

- Biggest losers: prime London and the commuter belt. £550,000 buys you a one-bedroom flat in Kensington & Chelsea. Our model shows that flat pays about £4,000 more in LVT than it paid in council tax; Hammersmith and Camden about £3,000 more. Important to repeat that this is an impressionistic model, and the direction will be correct, but the precise figures will not be.

- The starkest case: in the cheapest parts of Blackpool the land is worth almost nothing once you subtract rebuilding costs – so those homes, which today pay some of the highest council tax in England, would pay next to nothing.

- The other end: Westminster’s council tax take of roughly £180m would become a land value tax bill of about £1.5bn.

- The high end: Properties worth hundreds of millions of pounds will, fairly obviously, end up with millions of pounds of annual land value tax.9

Although when looking at the high figures for expensive property, bear in mind that stamp duty is disappearing. So for a new buyer, this is a much more attractive deal than for an established homeowner.10

Adding different thresholds doesn’t raise much more money

Any vaguely left-wing politician is going to be tempted to do better than revenue neutrality. They may want to use land value tax to raise additional funding. The obvious way to do that is to create a higher rate for higher value properties.

Let’s say, for example, we take a similar approach to the current mansion tax and impose a higher rate on land worth £2m+. Say a 2% rate.

You can dial that into the model by pressing the “Add a higher band” button. And the surprising result is that this raises less than a billion pounds. For the same reason, a land value tax that only applies to high-value properties is not really worth doing.11

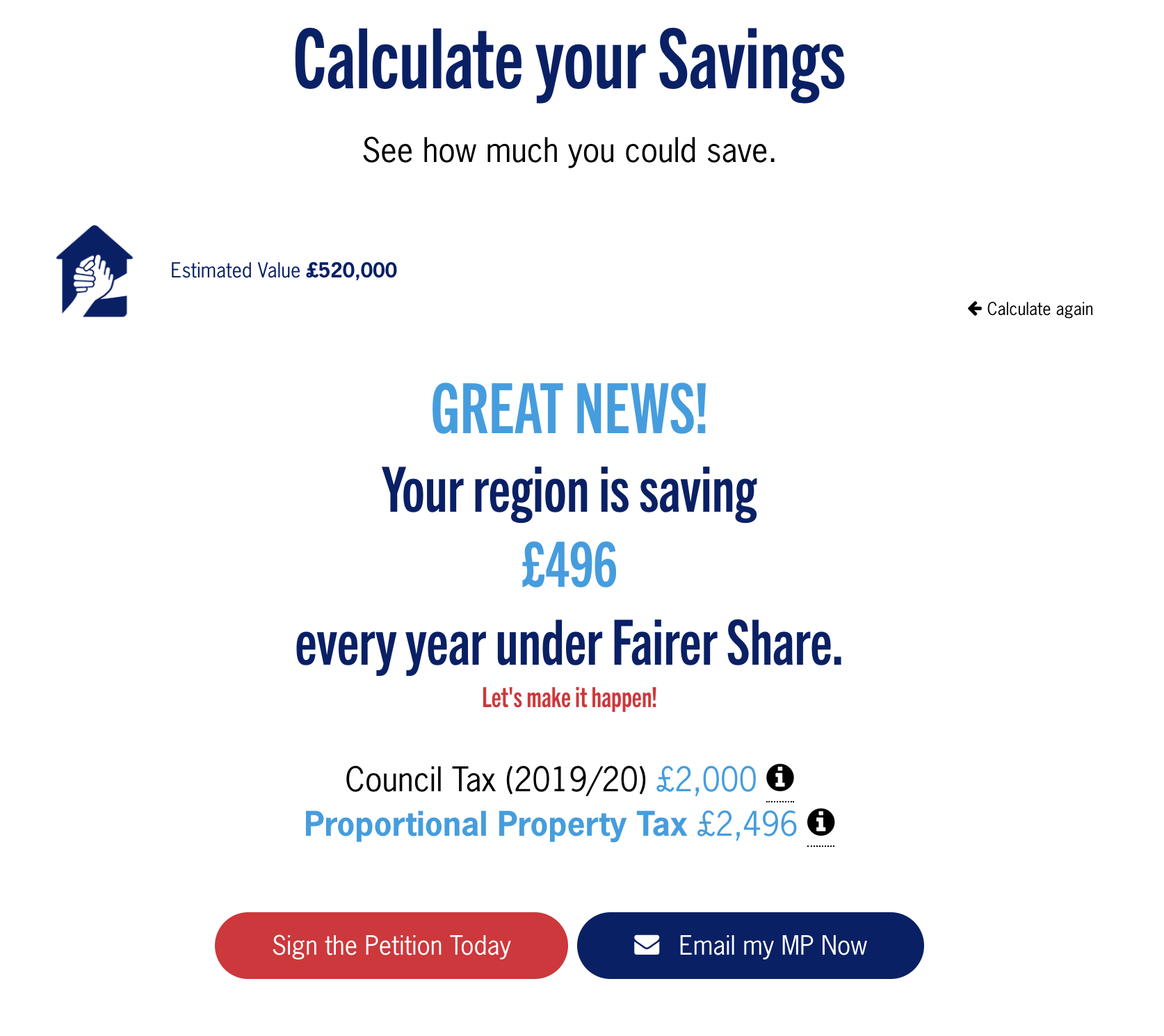

The transition is unfair

Anyone buying an average £520,000 property in Islington would no longer suffer £16,000 stamp duty.12 But council tax of £2,000 would be replaced by LVT of £5,000. That’s a big increase. And it’s one thing if you’re about to buy that house – the disappearance of stamp duty may be some consolation, even (for some people) a good deal. It’s something else if you bought the house a week before land value taxes were announced.

People would be furious, and I think they would be right. It would be a desperately unfair result.13

Even if you don’t agree, you should be worried about something else. There would be years between an announcement of LVT and implementation. If there aren’t transitional rules, then few people would buy property and pay stamp duty, knowing that they’ll have to essentially pay again when land value tax comes in.

So realistically, I think you have to credit recently paid stamp duty against people’s increased bills (i.e. new land value tax minus old council tax).14

There are many ways this could be done. Perhaps the simplest approach is something like: full credit for stamp duty paid in the previous tax year, 90% credit for stamp duty paid the year before that, and so on.15 That credit is then used to reduce each year’s land value tax (the excess over old council tax), until it is used up.16

That’s the “Transitional rule” checkbox in the model. It simulates the kind of credit rule I described in the previous paragraph. I think it’s something you have to do – but there’s a catch. It creates a significant reduction in revenue in the first year – about £5bn at the rates shown. You will see the text below the checkboxes now says that, to remain revenue neutral, the rate has to go up to 1.41%. If you click the “use it” button then that rate will be applied.17

The regional redistribution is just too high

Now imagine that £520,000 Islington property was purchased by a couple of teachers who have been saving for ten years, and put everything they have into the purchase.18 They face £5,600 of LVT per year19 – £3,600 more than their Band D old council tax bill. It will be a significant sum to them – about 4% of their annual post-tax income.

There will be lots of people in this position: people owning valuable land, particularly in London, who will struggle to afford the land value tax. That feels a fairer result if it’s households who bought when property was much less valuable and have benefited from significant appreciation, but it feels much less just where people recently bought at great personal cost. We have no way to distinguish between these two cases in the application of the tax. So our Islington teachers are being punished for buying at the wrong time.

Now imagine an equally experienced couple of teachers in Blackpool. They would earn about £45,000 each. For £200,000 they could buy a four-bedroom semi-detached house of about 1,500 square feet, with front and rear gardens, a garage and off-street parking. Their home would be more than twice the size of the Islington flat, but would cost less than half as much. And their £2,100 council tax would be replaced by LVT of only £459.

This feels unfair. The stratospheric valuations of London property have caused many problems, and in my view it’s right that there is a correction. But not this much. Many otherwise-sympathetic people hesitate when they see results like this. And indeed there’s evidence that the greatest problems with horizontal equity for land value taxes can be on the lowest-value homes.

The answer is to forget the idea of a pure land value tax applying across the country and make it, to at least some degree, regional. If you take the slider at the top of the model and drag it from the left all the way to the right, then the land value tax becomes entirely regional. The LVT rate varies in each region so each region collects an amount equal to the total council tax and stamp duty previously collected from that region (although if you are using transitional rules then there are short term differences). Any redistribution in London (for example) is therefore solely between different properties in London. Our Islington teachers see an increase of £1,000 rather than £3,600. They are the main winners.

The regional table shows what this does to different rates. If we make the slider “all regional” then the rate becomes 3.4% in the North East, but 0.82% rate in London. That means a regional LVT greatly increases land value tax for wealthy areas within poorer regions. There are about 1,000 houses in Trafford in the top council tax band, worth an average of £2.5m. Under a national LVT they pay an average of £33,000. Under a regional LVT, £49,000 – higher than Kensington. Even an average Band C house in Trafford now pays about £2,300 more LVT than council tax. Things are even worse in Newcastle-upon-Tyne, because its land valuations are so much higher than the surrounding areas. An average Band C property pays £2,700 more than it did under council tax; the 120 Band H properties pay an average of £84,509. 3.4% is just not a sustainable rate for a land value tax.

(I should repeat the caveat that this is an impressionistic model, and the direction will be correct, but the precise figures will not be.)

If you drag the slider to, say, the 50% mark, you can try to get a result somewhat balanced between the extremes, but you’re choosing between bad options.

One could try to avoid these problems by applying rates on a local authority basis. But there is never a free lunch. There will always be winners (with the degree of winning limited because LVT does not go below zero) and losers (with little limit on the degree to which they lose). If the intention is to stop very large increases (in all but the highest-end properties), then some other, more ad hoc solution is required. We make no attempt to model that.

Regional rates also – necessarily – mean there’s no equal national treatment: two identical land values can face different bills because of a boundary, and local rate-setting can create tax competition (which some will regard as advantageous and some as problematic).

The choice between national and regional rates is fundamentally a political one, but my takeaway from this is that a pure land value tax that replaces council tax and stamp duty is not viable without measures to soften the blow on people who’d experience very large increases. More on that later.

The impact on asset-rich, cash-poor

The classic problem case for the land value tax is an elderly person living in a large house without much income. They have no prospect of affording the land value tax.

A purist LVT response is to say that is an intended outcome.20 The point of the land value tax is for land to be used as efficiently as possible, and someone without income occupying a large house is not an efficient use. There are also ways that someone asset-rich, cash-poor can generate cash from their asset, whether it is by taking in a lodger or by borrowing under a reverse mortgage or similar arrangement.

The delightful old lady rattling around in a huge house is the most often cited example, but in reality it’s not a terribly common one.21 These aren’t reasons for ignoring liquidity issues. They’re good news, because they mean liquidity is an easier problem to solve.

Our model’s (optional) solution is a deferral, where a taxpayer can opt for LVT to “roll up” each year, with a modest interest rate, until they sell the property or die. Similar schemes abroad have had a surprisingly low take-up.22

The model does this if you check the “Deferral option” box. It assumes 10% of the eligible excess charge is deferred (a conservatively high figure given the overseas experience).

Deferral reduces first-year cash receipts by about £2bn. If we adjust the rate to reflect both deferral and transitional relief, then that increases the revenue-neutral rate to 1.46%.

(An important point. Some people have proposed deferral of land value tax completely. Our model takes the approach that, since you can’t defer council tax today, you should only be able to defer the excess of land value tax over the old council tax amount. That makes deferral very significantly less expensive.)

Some people face a very large charge

It shouldn’t be a surprise that very expensive properties have a very large land value tax charge. That is, in the end, the point.

The model shows top Band H properties in Kensington carrying an average LVT charge of about £53,000 a year (once more: this is an approximation).

This is likely to create concern that people will leave the UK. But a land value tax is the tax that worries least about such concerns, because land cannot emigrate. If a Kensington owner moves abroad, the house – and its land value tax – stays exactly where it is, paid either by them as a non-resident or by whoever buys it. Unlike income tax, a tax on profits, or a wealth tax on movable assets, the base cannot follow the taxpayer across a border. To repeat myself, it’s the one asset that we can tax more but not get less of.23

This is all made easier if the tax phases in – over ten years with 10% more of council tax and stamp duty abolished every year and 10% more of LVT applying. The “ten-year phase-in” switch in the model shows you the effect of that – every bill just moves a little bit towards the full LVT result (be that a cut or an increase).

The effect is somewhat soothing. Our Islington teachers, staring down a £3,600 increase on day one of a big-bang reform, now face £360. Kensington’s eye-watering five-figure rises become merely four-figure ones. Blackpool still benefits, but only a little. Everything moves in the same direction as before, and towards the same destination, but more slowly.

Farmers

Farmland creates a particular design problem. Many farmers report a return of around 1% of the value of their farmland.24 This surprises many people – and many economists. The reason seems to be that valuation is driven by uses other than farming: development “hope” value, lifestyle and amenity demand, capital-gains rollover relief, and agricultural and business property relief. A small probability of planning permission can rationally add substantial value because the potential uplift is so large. There also seems to be an extent to which farmers’ behaviour is not rational in narrow economic terms (and farmers I speak to readily admit this). A rational economic actor inheriting a £5 million farm would sell it, invest the proceeds in index funds, and never work again. Farmers inheriting land rarely do this.

The same mismatch between farmers’ income and the market value of their property contributed to the inheritance-tax controversy we previously discussed.

There are two possible policy responses.

The fundamentalist LVT response is that an owner unable to earn enough to cover the tax should sell, lease, intensify or change use. That need not mean the end of the farm – another operator might use it more productively – but it could mean the end of small farms.

There are obvious objections to that. Perhaps the result is following not from real economics but from a series of distortions in the market? And perhaps we want to maintain small farms for community, environmental and food security reasons, even if the farms are not economically efficient?

I take the second view, although I live in a rural area and I may not be objective. But on that basis, I would create a significant reduction in land value tax for actively farmed farmland.25

This is fundamentally an easier point to resolve than the application of inheritance tax to farmland. Agricultural relief for inheritance tax has always been a fantastic avoidance opportunity, because someone with assets subject to inheritance tax, who wants to avoid IHT, can exchange them for agricultural land which is exempt or partly exempt. Someone with land subject to land value tax who wants to avoid LVT can exchange them for assets other than land. There is no incentive to buy agricultural land to avoid land value tax.26

None of this is terribly relevant to our model because our model only covers residential property – but farmhouses would in many cases need to be covered by any farmland LVT relief or exemption.

What if we just replace stamp duty?

All the very big LVT figures in some of the examples above are a consequence of replacing council tax and stamp duty. There are many properties, particularly in the north of England, whose council tax is dramatically reduced by its replacement with land value tax. That then piles up as land value tax on London properties.

This creates obvious political challenges. So an equally obvious solution is to drop the idea of replacing council tax and only replace stamp duty. Then you only have to raise £11.5bn rather than £57bn, and things then become much easier.

Our model lets you do this with the big switch at the top. And suddenly, our teachers in Islington with their £520,000 house pay only £1,500 LVT each year, not the £3,600 increase they saw under “full-fat” LVT. And their neighbour in a £3.4m home would only pay £12,800 each year, instead of £48,000. The lowest council tax band properties in Blackpool pay nothing.

In many ways, this is an attractive approach – even if one buys the argument for a full land value tax, this could be a transitional step.27 But (as always) there are catches.

An administrative catch: the valuation work required for an £11.5bn LVT is exactly the same as for the full-fat £57bn LVT.28

And a political catch. Around 63% of people benefit in immediate cash terms under a full-fat LVT with transition and deferral. Their council tax disappears, and their LVT bill is less than council tax. Nobody receives this benefit from an LVT that only replaces stamp duty. Their annual bills can only go up. They may not mind if they are planning to move soon because they benefit from the abolition of stamp duty. They may be forgiving if they moved recently because they’ll benefit from transitional relief (at least for a while). But everyone else – people neither recently moved nor planning to move – loses from a stamp duty-replacing LVT. For all the economic advantages that I and many others would say replacing stamp duty has, in cash terms this proposal offers them nothing29 except a new annual bill – about £400 on average.

So I’m afraid a mere stamp duty replacement does not look very viable. It looks even less viable once we start thinking about administration costs…

The cost of running LVT

Having spoken to a variety of people with experience of HMRC and other government projects, we think the figure would be somewhere between £300m and £1bn each year. That’s the steady-state figure – the upfront cost would be larger. These figures should be seen in the context of existing council tax collection costs of £300m (incurred by local authorities) and an overall HMRC budget (not including council tax) of about £4.5 billion. So £1bn is very large indeed.

These figures are not very scientific, and the following paragraphs will try to justify them.

Our starting point should be that the current £300m cost of collecting council tax tells us little about the cost of collecting land value tax because, whilst council tax is much simpler than land value tax, it is administered individually by local authorities, and so there is a significant amount of inefficiency.

The new High Value Council Tax Surcharge (“mansion tax”) is a better point of comparison, because it requires a reasonably large number of new valuations to be conducted, albeit in bands and not with precision. It’s been reporting this is requiring the recruitment of 300 new valuation officers. 300 officers at an average gross employment cost of £70,000 comes to about £21m, which we should roughly double to allow for IT systems and associated costs. That covers the valuation of roughly 165,000 homes worth more than £2m. If we naively gross this up to England’s 26 million dwellings we get £6bn.

This figure must be nonsense, for two reasons:

- Ordinary homes are far cheaper to value than mansions. The mansion tax is expensive per property precisely because each £2m-plus home is unique, high-value, and valued individually against a bright-line threshold – which invites clustering, disputes and appeals over whether a house is worth £1.98m or £2.05m. The LVT would apply automated valuation models (see further on this below), which are an order of magnitude cheaper, and people would only have an incentive to dispute valuations if they were very significantly wrong.

- Land valuation is cheaper than property valuation. As we discuss in the valuation section below, property valuation is dependent upon the unique characteristics of particular properties. Land valuation is not.

- Economies of scale. The systems, data and methodology are largely fixed costs; spread across 26 million properties rather than 165,000, the cost per property falls sharply.

- Although… as a banded tax, one would think valuation for the mansion tax is a more straightforward task than valuation for a tax which applies on a percentage basis.

A useful sanity check is the HMRC Valuation Office (formerly the Valuation Office Agency, and created to administer Lloyd George’s original LVT attempt). In 2023-24 the VOA cost around £180m to run. Whilst it provides ad hoc valuation advice to the public sector, its main role is maintaining the council tax and business rates lists. The scope is therefore very similar to any new LVT valuation office, but the work required is significantly smaller given that neither council tax nor business rates require annual valuations. So some small multiplier of that £180m feels like the right figure.

Faced with these datapoints, the experienced HMRC and civil service personnel we spoke to essentially shrugged and estimated numbers in the range of £300m to £1bn.

If a full-fat £57bn LVT (replacing stamp duty and council tax) costs £1bn to collect, then that is a somewhat high collection cost – about four times the HMRC average. But £500m to collect an £11.5bn stamp duty-replacement LVT is another matter.

Our model, of course, ignores all administrative costs, for both HMRC and taxpayers.

Capitalisation – the known unknown

A classic blunder is to calculate the revenue from a tax by multiplying the tax base by the rate. That is a “static” estimate which ignores the consequences of the tax and the way people respond to it. There are approximately ten million men with beards in the UK. If the Government introduces a £10,000 tax on beards, it will not raise £100bn.30 For most other taxes, there is a more subtle taxpayer response than shaving, but the point remains: you cannot estimate tax revenue with a static analysis.

Our LVT model estimates LVT revenue with a static analysis. This is for two reasons: a dynamic analysis is too difficult, and a dynamic analysis changes many things, but (for reasons I will discuss) in practice ends up having only a limited net effect on tax revenue.

The reason this matters is that a credible, permanent land value tax would change property prices – in some places sharply. Not uniformly, and not always in the direction most people assume. Some homes would fall in value; others would rise. And that would change the rate, the revenue, the measured land share and the distribution. We know there would almost certainly be an effect. But for the reasons I’ll discuss below, the scale of the effect is unclear.

This effect is called “capitalisation”. To explain it, we should start by asking an easier and apparently unrelated question: how much would you pay to buy the right to receive £128,000 each year, forever?

We first need to determine your “discount rate” – how much happier you are to receive money today than money next year. Say it’s 3% – that means that you’d pay £97 today for £100 in a year’s time. You should then be willing to pay £4.3m – because if you put £4.3m in a bank account yielding 3%, you’d receive £128,000 each year.31

Now imagine an empty plot of land worth £10m (before anyone expects LVT to be introduced). The Government initially wants to raise the equivalent of 1.28% of that value: £128,000 a year. At a 3% discount rate, a permanent annual liability of £128,000 has a present value of £4.27m. The land would therefore fall in value to about £5.73m – a fall of 42.7%32. The Government still wants its £128,000, so it would have to charge 2.23% of the new, lower land value. That is the stable point: 2.23% of £5.73m is £128,000.

Do that across all of English residential property – on a 1.28% rate,33 and on the assumption that land is 55% of housing value – and a 42.7% fall in land value looks like an average fall in total residential property values of about 23.5%.34 That is the mathematical result of introducing a land value tax. It is also wrong – or rather, it is the answer to the wrong question.

The mistake is to look at land value tax in isolation. Every home in England already pays council tax, and everyone who buys one already pays stamp duty – and today’s prices already reflect both.35 A full-fat land value tax does not add a tax; it abolishes council tax and stamp duty and puts LVT in their place. So what gets capitalised into the price is not the whole land value tax, but the change in the annual bill: the new LVT minus the council tax it replaces.

That’s why, “overall”, there is probably little effect. Because the reform is revenue-neutral, the total land value tax (£56.7bn) is, by construction, exactly equal to the council tax and stamp duty it replaces. Across England, we are simply swapping one stream of payments for another of exactly the same size. The average home’s annual bill is unchanged, so there is little to capitalise, and no reason for prices to fall significantly. The frightening 23.5% is mostly an artefact of forgetting the two taxes we are abolishing.36

But, beneath the surface of overall flatness, plenty is going on. Employment can be flat even while millions of people lose jobs and millions of others find them. If everyone is an economics professor, then everyone gets a change in home value equal to the change in their annual bill divided by the discount rate. The model already shows you the change in the annual council tax bill. It’s the number used to colour the map. So everywhere you see coloured red, replacing council tax with LVT drives price falls, and everywhere coloured blue sees price increases. That is, however, only part of the picture because it doesn’t take stamp duty into account – the abolition of stamp duty should increase prices, with a bigger effect on high-value properties with huge stamp duty charges. But a perpetual annual charge is a far bigger thing, economically and in psychological terms, than a one-off saving on some future sale, so the very top still faces a net fall – just a smaller one than the coloured map implies.37

Our model generally ignores capitalisation, but displays a crude capitalisation estimate if you hover over the results table for a local authority or region. You’ll see an estimate for the one-off change in that home’s value – the change in the annual bill divided by 3%, taking account of the saved stamp duty. A few examples:

- Most of the country barely moves. Hover over a typical home in an ordinary area – say Leeds – and the estimate is within a whisker of zero: a Band D home is about −1%, the average home about +7%. The new land tax is close in size to the council tax and stamp duty it replaces, so for the typical household there’s not much going on. In practice, these kinds of changes would likely be invisible.

- At the top the effects are significant. The average home in Kensington & Chelsea faces about £15,750 a year more, which capitalises to roughly £525,000 off its value at 3%. Abolishing stamp duty softens the blow – a £100,000 saving on a sale – but a perpetual annual charge dwarfs a one-off saving, so the estimate tooltip still lands at about a 27% fall in property prices. The effect is exacerbated by the fact that, in prime London, land is a much higher proportion of the property price.

- Our Islington teachers sit in between. Their £520,000 flat would pay about £3,000 a year more – and, after taking into account the stamp duty saving, it’s a fall in value of 17%. Quite possibly negative equity, if the teachers bought a week before the announcement.

- Massive increases in value in some areas. In Blackpool or Hartlepool, where council tax is high and the land is worth almost nothing, the annual savings are large, and the tooltip estimate shows gains in value of 40 to 70%.

So capitalisation under a full-fat LVT is not a national crash. It’s an average nothing, disguising a large, concentrated fall at the top – prime London and the commuter belt – mirrored by a large, concentrated rise across much of the North and the coastal towns.

The losses in prime London and the South East could mean negative equity, real losses for lenders, and stress right up to insolvency for ongoing and planned construction, development and infrastructure. The obvious upside is that it improves affordability in these areas, but, even for those of us who believe current house prices are too high, and that this is a serious problem, the answer is not a sudden dramatic drop in house prices.

There is also an equity problem which bothers me. Capitalisation behaves a lot like a one-off levy on the land wealth of whoever owns at announcement. Someone who acquired land immediately before an LVT announcement may lose the full capitalisation amount. Someone who acquired land afterwards can lose little or nothing (because they pay the LVT in the future, but saved because it was “capitalised” into a lower purchase price). That’s a very random and unfair one-off wealth tax – I sometimes call it the “hot potato” problem, but people look at me strangely.

And of course we see the opposite effect in e.g. Blackpool. A long-term rise in Blackpool property prices may well be a good thing, but a sudden one-off rise is a different matter. It’s the opposite of the hot potato problem – call it the “pass the parcel” problem. Whoever owns property in Blackpool at the point a land value tax is announced suddenly receives an arbitrary windfall. The speed means it doesn’t result in a big win for Blackpool, but a big win for the lucky people holding the property when the music stops. Landlords gain; renters do not. Affordability for new buyers gets worse. Wealth inequality between Blackpool and Kensington improves, but wealth inequality within Blackpool gets worse.

These are not obviously great results.

How big any of these effects are depends heavily on the discount rate, which I just blithely assumed at 3%, without doing any thinking. That figure is on the low side, which is a good choice if we are trying to stress test scenarios. At a 6% discount rate every figure above roughly halves.

It also depends on how realistic it is to say that market value follows a mathematical formula. Even on its own terms, that formula assumes a constant rent, a fully credible and permanent tax, no credit constraints, no supply response and full information – all of which push the real effect down, not up. So the 27% collapse in Kensington example is highly theoretical and, even taken at face value, close to the top of the range.

At this point, I’d usually turn to the literature. But, less than helpfully, estimates in that literature range from no capitalisation to more than full capitalisation.38

Some people say phasing is the answer. I am not sure it is a complete one, but it clearly helps. In theory, a fully credible phase-in should be priced into land immediately (with a discount), even if it took twenty years for the LVT to fully apply. But in practice nothing is fully credible, and people are bad at incorporating long term effects into their planning. So it would be most surprising if twenty years of uncertainty produced an instant, complete repricing. More realistically, phasing gives households and markets time to adjust, and it is precisely the concentrated high-value falls – the dangerous part – that a long transition can spread out most effectively. That is what happened in the Australian Capital Territory, which in 2012 began a 20-year switch from stamp duty towards annual land taxation. There was no market crash – and the land value tax isn’t even visible if you eyeball the data.39 And whilst a large crash in land values could be a disaster, a gentle decline is – in my view – no bad thing at all.

So where does capitalisation leave us? It is, again, regional redistribution – sharp, concentrated falls in high-value areas, offset by rises in cheaper ones. My tentative conclusion is that this makes a full-fat land value tax a genuinely high-risk endeavour – and manageable only if the transition is slow, credible and deliberately gentle, and if the real-world discount rate is kinder than the naive arithmetic.

We’d minimise these effects if land value tax only replaced stamp duty but, as we have seen, that leaves too many people simply worse off, with (from their point of view) no upside.

Valuation: the known challenge

How do we value land?

The whole difficulty of a land value tax is separating the value of the land from the building on it. That’s relatively easy in rural areas where bare plots frequently change hands – you just look at the market price (although the question of how LVT applies to agricultural land is difficult – see above). New development on formerly empty land gives you an ideal data point because you see the purchase price of the empty land and the subsequent price of the developed housing. But in built-up areas, this approach runs into the immediate problem that sales of bare plots are unusual. You can’t rely on direct market evidence of market value and have to construct a synthetic market value. And those built-up areas are exactly the areas where most land value tax will be collected from. Think central London.

There are basically three workarounds: abstraction (the residual method we use – property value minus depreciated rebuild cost); allocation (assume land is a typical percentage of value for the area); or hedonic40 / contribution-value regression (statistically estimate the marginal value of land attributes from a large body of sales).41

In the modern world, all these methods can be combined using public and government data to model location value. However, proponents of land value tax have to acknowledge that there is no magic bullet; there is a solid literature on theoretical approaches, but the history of actual implementation is discouraging.4243

The Welsh research

There is more analysis on valuation methodologies today than at any point in the past, thanks to the Welsh Government. In March 2026 the Welsh Government published parallel studies by the Valuation Office Agency, universities and commercial teams using hedonic regression, machine learning, formulaic, conventional and entirely new and experimental approaches. All the work used desktop data rather than visiting sites.

The many different approaches broadly agreed about where Welsh land values are high or low; and machine learning predicted whole-property prices better than simpler models.

But absolute land-value levels differed, and differed enough that no land/building decomposition could be uniquely validated. None of the tested methods was accurate enough to be deployed in a live land value tax.

So, whilst this was a hugely valuable exercise which anyone interested in LVT would do well to read, it did not result in placing an implementation-ready solution onto our shelf. The key documents are footnoted here.44

The wider LVT literature

One of the most consistent elements in the LVT literature is the inconsistency of different approaches to valuation. When the Lincoln Institute compared land-value estimates across three US jurisdictions, the methods disagreed markedly – differences45 of about 23% (contribution value), 32% (abstraction) and 44% (allocation), all above the professional standards for the taxes in question. Those were differences between the three jurisdictions, not error against a true market price: urban vacant sales were too sparse to supply any. So we can’t know if any of the jurisdictions were in fact correct. In theory, there would be data from the twenty-nine US states that require land and improvements to be recorded separately, but ordinary property-tax liability does not depend on that split, so neither taxpayers nor tax authorities have any motivation to perfect or test the figures.

Land is valued at scale elsewhere despite the difficulty: Estonia values land from databases and New South Wales values about 2.7 million parcels annually, using a component and benchmark system. Taiwan operates both an annual land value tax and a land value increment tax. Denmark is a cautionary example. It introduced a land tax in the 1920s, at almost exactly the moment Britain gave up on one. Danish valuations were suspended in 2013, after the national audit office found three-quarters of house valuations bore no relation to market prices. So they decided to replace the old valuation system with an automated computer model. Nine years after the scheduled completion date, the rollout remains incomplete – it’s regarded in Denmark as a major IT scandal. Denmark’s response to all this has been to apply their land tax on a value that’s discounted by 20% from their modelled valuation.

Lloyd George tried to implement land value tax from 1909-1914, but failed for a variety of complex and disputed reasons – the tax was eventually repealed in 1920.46 Samuel Watling has used that history to argue that a pure tax on the unimproved value of land “has never been successfully implemented anywhere”. Watling adds that Australia and New Zealand later wound their land taxes back, that Denmark’s land tax raises under 2% of revenue, and that Taiwan exempts owner-occupied housing and agriculture. Pure land taxation, he says, has never really worked. It’s a powerful and well-argued paper and substantially correct. One criticism can be that the taxes he critiques were not true land value taxes, but this type of reasoning is never very convincing.

Lloyd George’s failure has prevented any attempt to return to land value taxation in the UK, aside from an experiment in Whitstable in the 1960s and 1970s.

So it is impossible to deny that land value tax has historically floundered in valuation difficulties. Any UK implementation has to seriously consider all of the history, messy as it is47

I tend to think the correct answer to the fairly dismal history of LVTs is in part technological and in part pragmatic. The technological part is that modern valuation methods and modern technology mean that some of the historic failures are not relevant – although it is obviously imperative that no land value tax is allowed to commence until valuations have been validated (one can imagine some kind of oversight body created to perform such a function).48 The pragmatic part is that some degree of error is inevitable in all valuation systems. Even our existing taxes suffer from it – council tax bands are an exercise in time travel to 1991. Stamp duty is almost always overpaid to some degree because most people don’t separate “fittings” such as curtains from the price paid.49 These are relatively small errors, but any property tax based on a percentage of property value will have much larger ones – and there is reason to believe that errors in land value tax valuation create no more distortion than errors in an ordinary property tax.50. Accuracy is less important than consistency, fairness and perceived fairness.

The alternative – the PPT

Fairer Share’s Proportional Property Tax (PPT) is a serious alternative and would be a significant improvement on council tax and stamp duty. It is not, however, a land value tax. It is, as its name implies, a simple percentage tax on property (buildings and land).

I have a strong preference for land value tax, because taxing the whole property also taxes extensions, rebuilding and renovation: improve the home and the tax base rises. So the PPT creates an incentive to not improve property. Or the flip side: it doesn’t create an incentive to improve property. We can put a number on this effect: a 0.48% annual tax is equivalent to imposing an approximately 16% up-front tax on the value created by home improvements.51

That might be a price worth paying if a PPT eliminated the valuation difficulty – and that’s basically the claim being made:

“Valuing land separately from the property is far more complex, requiring subjective estimates of “bare land” values that are harder to administer, update, and defend. By contrast, whole property values are well understood, widely available, and already used in the market, making them a more robust tax base.”

It’s true that property is frequently valued, but most property is not valued every year or, indeed, very often at all. About 42% of housing hasn’t sold since 1995, and there is no data available on the price it fetched. Looking at the market price achieved for a house is highly reliable when the sale was last week. It is less reliable when the sale was last year (what if the property was completely refurbished?), and of doubtful relevance when the sale was 20 years ago. Some suggest this can be resolved by cross-checking on an automated basis with the Land Registry, local authority planning permissions, and satellite imagery. That is not a viable approach. None of this tells you anything about construction technique, condition, fittings and refurbishment, or indeed the standard of any work that was undertaken. You can’t see a kitchen from a satellite, and a £300,000 kitchen and a £2,000 kitchen may appear identical on a planning application. The variation in construction cost between different projects of identical size can be extreme.

Property valuation has to be done by reference to the actual features of the inside and outside of the property in question: floor area, extension, age, condition, fittings and refurbishment. Land value is driven more by plot, permitted use, location and surrounding amenities, which can be determined on an automated basis from public and private data sources.

This is why council tax and the recently introduced “mansion tax” apply to valuation bands, not precise valuations. It means valuation disputes occur only at the boundaries, and so greatly reduces the need to look at people’s kitchens.

All of which creates a paradox. Land valuation is rarely undertaken in practice, but in principle land across England can be valued from the desktop. Property valuation is commonplace in practice, but cannot accurately be undertaken from the desktop.

My view is that, counterintuitively, land value tax is therefore very possibly easier to apply across England than a proportional property tax. Easier but not easy – for the reasons discussed above.

I should, though, be fair to the other side of the argument. A whole-property valuation has one advantage a land valuation can never match: you can check it against something real – what the house next door actually sold for. A land valuation has no such anchor. As the Welsh research showed, there is simply no market in urban land against which to test the land/building split, so that split is, in the end, unverifiable. So while I think land is, on balance, the easier of the two to value across England, it is a genuinely close-run thing – and anyone who weighs verifiability most heavily should reasonably land the other way.

The details of the Fairer Share proposal:

- an annual charge of 0.48% of the current market value of the whole property for an owner-occupied home: so £960 on £200,000.

- Then 0.96% for second homes, empty homes and overseas-owned homes (I don’t think these are good features because of the definitional complexity, potential for unfairness, and the sheer randomness of taxing one person with two £200k houses more than another person with one £400k house).

- It would replace council tax, residential stamp duty and the “bedroom tax” and is calibrated to raise the same revenue, not extra revenue.

- Fairer Share says roughly 75-77% of households would pay less. Its parliamentary evidence gives an indicative 0.32% national / 0.16% local split, combining redistribution with a locally retained element.

- The transitional rules are that, for an existing owner the annual increase, not the total bill, would be capped at £1,200. I feel they have not properly thought through the implications of this in terms of deterring future sales and/or falls in value. The capitalisation effects will be as difficult as those discussed above.

- The reform would be phased in over three years.

- An owner unable to pay could defer payment until affordable or until sale; and the cap disappears when the home is sold, so the purchaser pays the full 0.48%.

- See Fairer Share’s 2020 Treasury Committee evidence and the later FAQ for details.

- See also the PPT overview, manifestos and technical reports, and IPPR’s analysis of the national design and London impact.

Fairer Share published figures on the impact of their proposal. The methodology is described at a high level here, but the most important element – how they value individual properties – is not fully explained and not reproducible, and Fairer Share don’t publish the underlying detail or code. We hope they consider doing so, as enabling researchers and the public to model changes in tax design is incredibly useful. The constituency and local-authority modelling published on their website appears to rely on a simplified area-based approach rather than individual property valuations. The individual-property-estimator appears to be broken.

{kind=link}

Incidence, planning and local government

This report was intended to look at modelling an LVT, and the policy choices and difficulties that can be illustrated by the modelling. There are other important issues and challenges of an LVT which a model does not help us with at all. So this report doesn’t cover those issues – but I will mention them in passing.

Economic incidence

Who pays a tax? The obvious answer is: the person responsible for paying tax. This is the “legal incidence”. When I buy a bar of chocolate, the person legally paying the VAT is the shop. If Labour increase corporation tax, it’s the company paying the tax.

But who is actually paying the economic cost of the tax?

I think everyone knows that if VAT went up, it would be the customers who economically pay the additional tax in the form of an increased price. If corporation tax goes up, then the company is not economically getting anything because the company is a mere legal fiction. The real cost of an increase in corporation tax is borne by some mixture of shareholders, employees, customers, suppliers (it is highly contested, and muddled by people striving to reach the conclusion that suits their political agenda).

What about land value tax?

Legally it’s paid by the landowner. That means the owners of freeholds and long leaseholds (e.g. most London flats). It’s never paid by tenants under assured periodic tenancies as a legal matter.

But can the landlord then pass it on to tenants, either directly (via some kind of indemnity) or indirectly (through rises in rent)?

The orthodox economic answer is that the landlord cannot do this, and a tax on land falls primarily on the landowner. Rents are determined by what tenants are willing to pay and the supply of competing homes, not by the landlord’s costs. Instead, the future tax liability is capitalised into a lower value for the land. The owner when the tax is introduced bears the loss; a later purchaser buys more cheaply, in return for accepting the annual tax. A counter-intuitive but inevitable consequence of capitalisation is that landlords carry the can.52 It is not, however, certain that this would be the result – and for this reason, it’s sometimes suggested, even by the IMF, that landlords should be explicitly prohibited from passing on LVT costs to tenants (I’m unclear how effective such a rule would be in practice).

This creates a limitation in our model. It compares the LVT attached to a home with the council tax attached to that home, as though the two taxes were always paid by the same person. For an owner-occupier, they are. For a rented home, the tenant loses their council tax bill and the landlord acquires the LVT bill. The long-run economic benefit or cost may still fall mainly on the owner, but the immediate cash flows are different. So when we describe “winners”, the precise claim is that a home carries a lower modelled liability — not necessarily that its current occupier personally receives the whole saving.

In other words, if we imagine a property where land value tax is exactly equal to council tax, in the short term land value tax is a big gain for tenants and a big loss for landlords. In the long term, as prices adjust, the position of a tenant and landlord of such a property should be flat.

Planning and “highest and best use”

The claim that LVT encourages land to be used efficiently depends on how the land is valued. There are three broad possibilities: its existing use, its currently permitted use, or its “highest and best use” — broadly, the most valuable development that could realistically obtain planning permission.

Existing-use value is the easiest to apply, but reduces the incentive that is the cornerstone of the economic case for land value tax. A criminally under-developed site continues to be taxed as an under-developed site. Land value tax becomes just another tax, rather than a way of reforming the use of land.

Highest-and-best-use valuation creates an economically useful pressure to develop or sell, but requires the valuer to predict what the planning system would permit. Every little cottage, boutique shop and piece of farmland in the country would require a psychic valuation officer to determine if planning consent could be obtained for some maximalist development project. That seems unworkable.

“Currently permitted use” seems more sensible – in other words, it’s not what you’re doing with land today, it’s what you could do given the limits of planning law. There’s an advance on this in Hughes, Sayce, Shepherd and Wyatt’s report for the Scottish Land Commission, which suggests “most profitable permissible development” as a possible definition. In other words, you look solely at the current planning position, but think about what you can do within that.

As with everything land value tax related, things get more difficult at the edges. Planning permission doesn’t require you to undertake work. It just enables it. Permission lapses after three years, but if you’ve started development, the permission remains live forever. So it’s common for people to apply for planning permission for something very ambitious (say, numerous buildings on a site), but actually only build one. Anyone owning or buying a property like this could be surprised by a much higher LVT bill than they expected. And going forward, people would apply for paying permission on a more modest basis to avoid an escalating LVT charge. Some people might go further and deliberately make applications that reduce the value of their land.

There’s then the evil version of that. Under current law, anyone can apply for planning permission for any site. I could right now apply for permission to convert the BBC’s headquarters into flats. I suspect the BBC would object, but if that permission was granted the land value tax liability of the BBC would soar. Tricks like this could be a licence for mischief-makers and aggressive developers.Perhaps Planning Law would need to change to restrict the people entitled to apply?

Local government finance

Our model treats English council tax as if it were one national pot of money. It isn’t. Council tax is set and collected locally, and sits inside the spectacularly complicated system by which local government is financed.

This operates by a formula. In simplified terms, central government estimates each council’s relative need for services, adjusts for differences in the cost of providing them, and then takes account of the resources the council could raise locally from council tax. Grants and retained business rates are adjusted so that councils with high needs and weak tax bases receive more support.53

Some people wail and gnash their teeth at land value tax and say that it would be quite wrong to break the local nature of council tax (and its predecessors). But council tax is only as local as the formula permits it to be. Land value tax merely requires a new formula; if it was desired to leave local authorities in the same position as they are today, then the formula could achieve that. No doubt this would be very complicated, but it is not a point of principle.

Conclusion

So where does all this leave us? I remain a supporter of a land value tax. The principled case is overwhelming, and the practical prize is real and large: abolishing stamp duty, the worst tax we have, and replacing the wheezing 1991 relic that is council tax with something far more equitable.

But our model – with all its limitations – has made me much more cautious about how we get there. A land value tax done carelessly would inflict real individual hardship – on the Islington teachers, on the asset-rich and cash-poor – and risk serious market disruption through capitalisation. Avoiding that is not optional, and it is not easy. It probably requires most of the tools in this article at once: transitional relief for people who have recently paid stamp duty, deferral for those who genuinely cannot pay, and – above all – a long and credible phase-in that lets prices and people adjust gently rather than overnight.

The price of doing it safely is patience. Each of those softeners pushes the full benefit years, even decades, into the future – which is frustrating for those of us who find the argument compelling today. But a reform this big, reaching into the home that is most people’s largest asset, has to be done slowly or not at all. And the prize – a country that no longer taxes people for the crime of moving house, and no longer asks a modest home in Blackpool to pay more than a mansion in Westminster – is worth waiting for.

Caveats and limitations

This is an impressionistic model. More than “just a bit of fun”, but certainly not a robust valuation exercise. It is built to show the rough scale of a land value tax and, above all, its geography – who wins and who loses, and roughly by how much. The direction of travel should be correct, but individual figures are no more than illustrative.

This is a quick summary of the main limitations of our approach, but it’s not a complete one. See more in the methodology below:

- An entirely static model. There is no attempt to model any response in prices, construction, tenure, moving, borrowing, avoidance, evasion, collection or planning to the tax. Capitalisation, particularly for the LVT that replaces council tax and stamp duty, could change both the statutory rate required and the measured distribution. All of these factors would require careful consideration.

- Land value per home, not per acre. We take a crude but, we think, defensible approach to estimate the value of the land sitting beneath each dwelling. It’s all set out in the methodology below, but our figures can look badly wrong if set against the wrong benchmark. Land in central London is worth vastly more per acre than land in the suburbs – yet a central London flat sits on a tiny sliver of it, while a suburban house sits on a much larger plot. Measured per home, those two effects largely cancel, so our modelled land values per home vary far less between areas than land values per acre. Someone comparing our per-home land figures against a per-acre land-value map could therefore mistakenly conclude that we are wildly wrong – potentially by an order of magnitude.

- Administrative costs for taxpayers and HMRC are not included in our model. We suggest above this could be of the order of £500m for HMRC; taxpayer costs might be similar. Not very significant for a complete land value tax, but of outsized significance for a land value tax that only replaces stamp duty.

- Residential only. Commercial, industrial, agricultural and undeveloped land are absent. The model therefore tests replacement of English residential council tax and residential SDLT only; it does not model replacing business rates or non-residential SDLT. Generally speaking, the argument for a commercial land value tax is stronger and easier than for a residential land value tax because businesses are already taxed on the basis of property value (albeit in a very inefficient way).

- The land/building split cannot be verified. Urban vacant sales are unusual, so the overall level rests on assumed rebuild costs and a 55% land-share calibration. These are assumptions.

- No adjustment for council tax support schemes. There is no national scheme for relief from council tax for people on low incomes or otherwise in need of support, but individual local authorities are required to provide support schemes. None of this is modelled by our model, and so council tax will in some cases be overstated.

- No adjustment for social housing. About 16% of dwellings are social housing. Our model makes no attempt to separate social housing from privately owned housing. There are, however, two key differences. First, whilst a design and political question, it seems most unlikely that net land value tax would be collected from social housing, because it would be government taxing government (or government taxing housing associations, which is technically possible but surely politically unpalatable). So real LVT would exempt social housing; our model does not, and so overcounts land value tax revenue. This will probably not be a large error because social housing is usually relatively low value. But fundamentally, we cannot determine the degree of overcount for social housing; it follows that we cannot determine how much the rate would have to rise to keep revenues neutral. If we were modelling non-residential land, then we would have the significant challenge of excluding government-owned land, however that is something the current residential-only model does not need to do.

- Homes outside the retained sample. About 42% of housing hasn’t sold since 1995 and isn’t in the price paid database. Others will have been excluded by property type or removed as anomalous. The value and type distribution of these missing properties is inferred from sales. We expect, although this is intuition rather than data, that this results in an undercount of land value tax because some very high-value estates never change hands (for example, because they are held by a long-established trust) or held by a company and sales are effected by selling the company. But there will also be cases of, e.g., abandoned properties that haven’t changed hands for generations but are worthless.

- Aggregated, not individual. Figures are built up to local-authority-by-band cells, not valuations of individual homes. Within any cell the model is just an approximation.

- Synthetic council-tax bands. Price Paid Data does not supply the council tax band, so 2026-ranked sales are cut to reproduce 2025 band counts. Relative values absolutely will have changed since the statutory 1991 valuation date.

- Rough inputs. We approximate floor areas using typical national values by property type, and approximate building costs using broad regional factors.

- No household characteristics. The model has no income, age, tenure, mortgage, benefit, disability, occupancy or ownership-portfolio data. Its “winners” are representative valuation points, not identified families, and it cannot measure distribution by income or wealth.

- First-year position only. Transition and deferral are aggregate first-year cash calculations. Historical SDLT and take-up are simplified. We don’t consider what happens in subsequent years. Almost inevitably, revenue will rise, and policymakers would have to choose between keeping neutrality and reducing the rate, or keeping the rate and raising revenue. It seems to me imperative that this choice is made up front and locked into the way the land value tax works (and my strong preference is neutrality).

- No exemptions or special rates. I suspect there has never been a tax without exemptions or special rates. However, this model assumes land value tax is such a tax. That is clearly incorrect, given that I think it is almost inevitable there would be an exemption or special rate for farmland, and some residential property is realistically part of farmland. So this will lead to a slight over-count in revenue.

- Highly approximate valuations. Everything relies upon interpolating and extrapolating property values from Land Registry data, and then applying a simplified abstraction method to estimate the value of land. This is a highly approximate process. More about that in the methodology section below.

- Displayed bands ignore council tax complexities. The global council tax revenue calculation takes into account the level of single person discounts and other exemptions. It doesn’t take into account council tax reduction/support schemes. The displayed figures for individual bands in a Local Authority take no account of any discounts or exemptions and are therefore showing the basic council tax result (not a model limitation, but a design choice taken to avoid too much visual complexity).

- We ignore that LVT would be tax-deductible for landlords. Albert Salter spotted this in the comments, and he’s right: we’d missed it. Council tax is paid by the tenant, who gets no deduction for it. Land value tax would be paid by the landlord – and an annual tax on a let property is an ordinary expense of a property business, so it comes off their rental profits.54 HMRC therefore collects less income tax and corporation tax, and our revenue figure is too high. An extremely approximate estimate based on housing data suggests the hole is around £2.54n.55 We can cross-check this from rents and reach about the same figure.56 Either way that’s about 4% of the £56.7bn we’re trying to raise, which would push the revenue-neutral rate from about 1.28% to about 1.34%. This is a serious amount of money, but haven’t rebuilt the model for it for several reasons: (a) the £2.4bn figure is highly approximate, even by the standards of this model, (b) it’s also about a fifth of the ~20% valuation error we’ve already said we expect, and (c) it changes none of our conclusions.57

- No economic modelling at all. The whole point of the reform is that land value tax has pro-growth effects, in terms of replacing existing anti-growth taxes and creating positive incentives for economic growth. We make no attempt to model any of this (it’s not our expertise).

To give an idea of what all this means in practice, our mansion tax estimate undervalued property overall by about 20% compared to the much-more-sophisticated OBR figures. There are many more uncertainties in our land value tax calculation than in our mansion tax calculation; whether, overall, this results in an under-valuation or an over-valuation is hard to say. It would be realistic to expect an error in a similar ballpark.

Methodology

The model uses public data to estimate a current value for millions of individual homes, splits each into land and building value, and then aggregates everything to the level of a local authority and a council-tax band. The model was designed and tested by humans. The code for the model and the UI was written with the help of AI (Claude Code), and AI/Claude was used to ensure that the methodology described below is an accurate description of the model. All the code is available on our GitHub.

The data

- HM Land Registry Price Paid Data – qualifying residential transactions lodged for registration since 1995; it is not a complete record of every change of ownership.

- ONS National Statistics Postcode Lookup (May 2026) – maps each postcode to its 2025 local authority and region.

- UK House Price Index (to April 2026) – used to uprate old sale prices to current values.

- VOA Council Tax stock of properties (2025) – the official count of dwellings in each council-tax band in each billing authority.

- MHCLG Council Tax levels (2025-26) – the area-average Band D charge for each billing authority.

- ONS Local Authority District boundaries (May 2025) – for the map.

Estimating each home’s current value

We start from 30,706,118 price-paid records whose property type is detached, semi-detached, terraced or flat; Land Registry’s “other” category is excluded. We identify a home by normalised postcode, primary address number/name and secondary address (for example, the flat number), then keep its most recent recorded sale. That produces 16,070,913 apparent unique homes, of which 15,259,039 match to an English local authority. This address key can occasionally merge or split properties incorrectly. Each retained price is uprated to 1 April 2026 with the all-property House Price Index for its local authority, falling back to its region and then England where an index is unavailable. This assumes the particular home moved with the area-wide index between its sale and April 2026; it cannot observe extensions, deterioration or renovations after sale.

Some records are not reliable estimates of a whole home’s open-market value – for example shared-ownership fractions, connected transfers and nominal consideration. Left in, these cluster in the cheapest modelled band and can dominate it where band A contains few homes. We therefore drop an uprated value if it is below the higher of £30,000 and 30% of its local authority median – about 1.8% of records. This is a crude attempt to exclude anomalies.

Screening out anomalous sale prices

A small number of HM Land Registry records do not describe one home changing hands at one market price. Instead they show a whole block of flats, a portfolio of properties, or a mixed commercial-and-residential building, which is all sold at once, and is then registered with a single price across all the titles. This can result in anomalously large prices – for example, if a street of modest houses are all sold together for £5 million, then sometimes each property will have £5m separately on its Land Registry entry. Or a £1m residential property sold with a £539 million commercial property can both have £540m on their entries.

This happened in the first version of the model with one cell in Waltham Forest recorded as a £540m “terraced house”.58

Removing these records is harder than it looks, because a high price is not the same as a wrong price. Genuine homes in prime central London change hands for £50m and more.

We therefore judge each sale against its own like-for-like local market. A sale is set aside only if its value exceeds a set multiple of the median value for the same property type in the same local authority, with the benchmark widening to the region where a local sample is too small to be reliable. The multiple is loosest for detached houses, which can genuinely stand far above their local median, and tightest for flats, where a price many times the local norm almost always means a whole block booked as one unit.

We use these multiples:

- Detached – 25x the local like-for-like median

- Semi-detached – 18x

- Terraced – 15x

- Flat – 12x

This screening process removes about 1,300 of roughly 15 million sales. It leaves national picture essentially unchanged, but avoids anomalous local results.

Splitting land from buildings: the abstraction method

For this model, land value is the estimated whole-property value minus an assumed rebuilding cost. We assign every detached home 147m², semi-detached home 96m², terrace 82m² and flat 57m²; multiply by type-specific base costs of £2,100, £1,950, £1,900 and £2,400 per m² respectively; apply a regional factor from 0.92 in the North East to 1.15 in London; and finally apply one national calibration factor (0.70550 in the current data). The model has no actual floor area, building age, condition, depreciation, construction quality, plot size, planning status or individual rebuild cost. A newly built mansion and a dilapidated detached house in the same region receive the same assumed building cost if their Land Registry type is the same. This is why it must not be used to value an individual home.59

We then force everything to fit so we end up with the correct national totals. First, all property estimates are multiplied by 0.77885 so the grossed-up English housing stock is about £8 trillion. That target is an approximate England share of Savills’ £9.18tn UK estimate. Second, the rebuilding-cost calibration is chosen so land equals 55% of value in the retained sold-home sample; after grossing up, the model contains £4.433 trillion of land, 55.4% of £8 trillion of housing. There is no single external series that validates any of this, and it should all be regarded as unverified but convenient (and, we think, reasonable) assumptions.60 Where assumed rebuilding cost exceeds estimated property value, land is floored at zero rather than allowed to become negative. About 13% of the retained sold-home sample is at that floor.61

From homes to council-tax bands

The Price Paid Data does not identify a home’s council-tax band. We therefore rank the retained sold homes within each local authority by estimated 2026 value and cut that ranking at the shares needed to reproduce the authority’s official VOA band counts. This is all a heuristic – the model does not know the actual band of any sale, and band boundaries based on 1991 relative values will not always match a ranking by 2026 value. The model is designed to reproduce the official 25,755,290 dwellings and the A-to-H counts in each authority.

Gross council tax is the authority’s area-average Band D figure multiplied by the statutory ratios, from six-ninths for A to eighteen-ninths for H. For national and regional revenue only, we multiply gross liability by 0.83 to produce £45.217bn. That factor is calibrated to approximate aggregate receipts after discounts, exemptions, council-tax reduction and non-collection; it is not calculated household by household. We add an external £11.5bn estimate for annual English residential SDLT, producing a £56.717bn baseline. This is what’s targeted when the model is trying to be “revenue-neutral”.

Aggregation and coverage

Everything is aggregated to 296 local authorities × eight bands, with empty combinations omitted. Each cell keeps ten representative points: the mean land value in each equal-count tenth of the retained sold-home sample. Their unweighted mean equals the cell sample mean, so a flat rate reconciles to the displayed totals; a progressive schedule remains an approximation because every tenth is represented by one mean. The roughly 15.0m retained sales-derived homes are then reweighted to 25.8m official dwellings. This assumes unsold homes in each authority and synthetic band have the same type and value distribution as sold homes there – an untested and potentially important selection assumption.

The tax you design, and the “revenue-neutral” rate

The land value tax is applied to each representative land value using the schedule a user sets: a flat rate or marginal bands. Tax is calculated at all ten points and averaged, which is more accurate for a progressive schedule than taxing the single cell mean, but remains an approximation of the unknown within-cell distribution.

The “roughly revenue-neutral” flat rate is solved by bisection so first-year net LVT equals the model’s £56.717bn council-tax-plus-SDLT baseline. None of this takes any account of capitalisation, or any behavioural effects. It is an entirely static model. This is an important limitation, but for the reasons discussed above, we think it is significantly less important than for most tax modelling.

Transitional stamp-duty relief

The optional transitional rule creates a notional credit for recent purchasers: 100% for the most recent cohorts, then ten percentage points less for each earlier year, reaching zero after ten years. Credit shelters only LVT above the gross council-tax bill, never the council-tax-equivalent amount. The calculation is aggregated. For each authority × band × purchase-year cell, the model stores the buyer count and total notional SDLT, computes the average credit and compares it with the cell’s average excess LVT.

Historical SDLT is approximated by applying the standard rates in force from April 2025 to the modelled latest nominal purchase price. The model does not reconstruct the rates and thresholds on the purchase date, first-time buyer relief, the higher rates for additional dwellings or non-residents, linked transactions, lease rent, reliefs or refunds (that was somewhat lazy – or, to be more generous, we were trying to avoid spiralling complexity – but differences over this period are small, particularly in the high value properties where the effects are largest). Only first-year cash cost is modelled; later use and expiry of the credit pot are not. Accordingly, the 1.41% “neutral” rate is the rate that funds this modelled first-year relief while raising the baseline in that year. It isn’t the permanent rate a real multi-year transition would require.

The deferral option