The November 2025 Budget introduced a “mansion tax” – formally, the “high value council tax surcharge” – an annual charge on homes worth £2m or more. The Mail on Sunday has reported that Andy Burnham may lower the threshold to £1.5m. We’ve looked at what that might mean: who would pay, where the properties are, and how much it could raise.

Our estimate: a £1.5m threshold would tax around 150,000 additional homes, almost doubling the number of properties in scope. But simply adding a lower band would not raise a great deal of extra money. To get close to doubling the yield, the tax would have to become more aggressive, with £1.5m homes paying the current lowest charge of £2,500, and the charges for the existing £2m-plus bands all being pushed upwards.

On that basis, the net revenue could rise to about £800m a year – so Mr Burnham may regard this option as tempting. There is, however, a serious downside: tax systems need stability. Expanding a tax before it’s even been introduced is, in our view, the opposite of stability.

The impact of a £1.5m threshold

When the high value council tax surcharge (HVCTS) was first announced, we mapped the impact using historic Land Registry data. We’ve now re-run the model at a £1.5m threshold, reflecting the April 2026 valuation date the tax will use.1

Dropping the threshold to £1.5m nearly doubles the number of properties caught, from around 127,000 to around 243,000.2 If those new properties are charged a lower amount than the current lowest band (£2,500/year) then the net revenue is modest, once you take into account the additional cost of valuing all those additional homes. So it’s more plausible that £1.5m properties would be charged £2,500/year, with the £2m and upper band charges all increased. That could almost double the net revenue, to approaching £800m – and we assume this is how any extension of the mansion tax would work. More on these calculations below.

It’s important to add that this is all speculation. We don’t know if Andy Burnham is really planning a change of this kind; but it’s useful to look at what the impact would be.

And none of this relates to Scotland, Wales and Northern Ireland. Land taxation is devolved, and so the HVCTS applies only to England – this article considers only the English position. Scotland is consulting on introducing new £1m+ council tax bands.

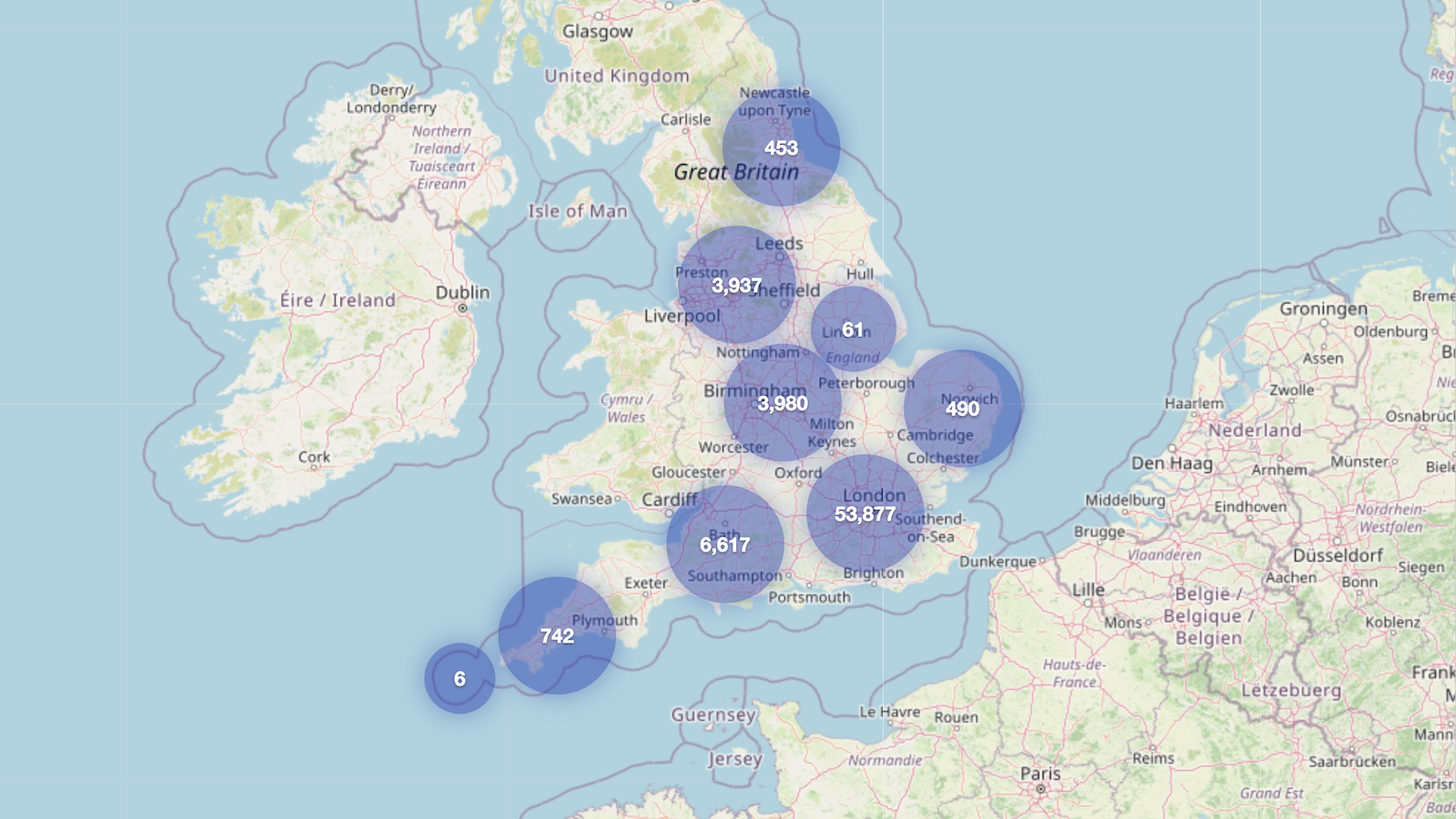

Regional breakdown

Here’s where a £1.5m mansion tax’s revenue would come from (you can hover for the detail, or click to zoom in):

And, this is a heatmap of Parliamentary constituencies – you can pan/zoom with your finger/mouse and hover/touch individual constituencies for details:

As you’d expect, it’s mostly London and the South East. The effect is extreme – residents of Camden would pay more mansion tax than everyone in the Midlands and North put together. Residents of Kensington would pay more than twice as much.

The main effect of the £1.5m band is to pull in more of the commuter belt: constituencies such as Esher and Walton, Twickenham, and Harpenden and Berkhamsted each gain close to two thousand newly-caught homes. The £1.5m band reaches Greater Manchester too, though more modestly – we estimate around 2,400 homes across the ten boroughs would be in scope, concentrated in Altrincham and Sale West. Even then, Greater Manchester would only account for around 1% of the properties subject to the tax.

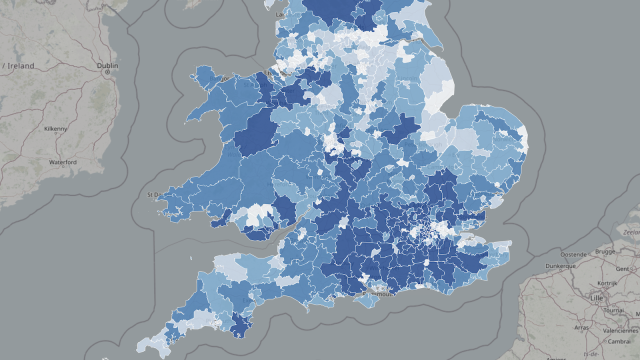

Where are the properties?

This interactive map shows every postcode containing properties we estimate would fall within a £1.5m mansion tax:

You can view the map fullscreen here. The markers sit at the centre of each postcode3 and do not represent individual properties.

The overall yield

The tax announced in the November 2025 Budget applies a charge of £2,500 a year on homes worth £2m-£2.5m, rising in steps to £7,500 above £5m. As we explained above, we think a £1.5m band wouldn’t make sense if it was charged at a lower rate than this. So we assume that the lowest £2,500 rate would apply to the new £1.5m band, with each of the other charges shifting down one band, creating a new £10,000 top rate:

| Band (April 2026 value) | Announced £2m tax | Our £1.5m scenario |

|---|---|---|

| £1.5m – £2m | — | £2,500 |

| £2m – £2.5m | £2,500 | £3,500 |

| £2.5m – £3.5m | £3,500 | £5,000 |

| £3.5m – £5m | £5,000 | £7,500 |

| £5m+ | £7,500 | £10,000 |

We can estimate the revenue impact by taking the Office for Budget Responsibility’s costing approach and applying it to two scenarios: a new £1.5m band at £1,500/year, and our base case – a new £1.5m band at £2,500/year that “pushes up” each of the other bands. We set out the methodology below.

| Budget proposal (£2m threshold) | Add £1.5m band at £1,500 (other bands unchanged) | Add £1.5m band at £2,500 with higher other bands (our base case) | |

|---|---|---|---|

| Static revenue, 2028-29 | £605m | £830m | £1,235m |

| Dynamic revenue, 2028-29 (after taxpayer responses and the extra valuation and administration cost) | £400m | ~£510m | ~£775m |

Methodology and limitations

The code for the analysis and webapp is available on our GitHub.

The methodology is the same as our original post, with refreshed data throughout. We take every transaction in the Land Registry price paid database that looks residential4 (now running to May 2026), and adjust/uprate each price to April 2026 – the date the tax will actually value properties – using the change in median detached house prices in each constituency, bridged from the latest ONS quarter to April 2026 with the England detached-house index from the UK House Price Index.5

The limitations are as before, and mostly mean our results are an under-count: we miss properties that haven’t sold since 1995; we de-duplicate repeat sales of the same property, conservatively (so may accidentally eliminate real sales); we can’t reliably screen out commercial property, farms sold with farmhouses, or portfolio deals that span multiple postcodes; we can’t account for improvements or conversions after a sale; and constituency-level inflation misses variation within a constituency. Our original post sets these out in full.

On the announced £2m tax, our refreshed model estimates static revenue of around £495m.6 Our figure is below the OBR’s static estimate of £605m (which it reduces to £400m after behavioural effects – see the table above), likely because of the limitations identified above (our Land Registry method counts about 127,000 homes over £2m against the OBR’s whole-stock estimate of 165,000). We don’t have our own dynamic analysis but borrow and extrapolate the OBR’s approach.7 So treat the individual numbers as approximate and lower-bound; the overall picture – which postcodes and constituencies pay, relative to each other – should be reasonably accurate.

For our revenue table, Column 1 reproduces the OBR’s certified costing for 2028-29 exactly: a static yield of £605m, reduced to £400m once behavioural responses are taken into account — a fall of about a third (OBR, Costing of high value council tax surcharge, 2 April 2026, Table 1.5). For columns 2 and 3 we extrapolate that method. The OBR’s static base is 165,000 properties above £2m, from a commercial automated-valuation model covering the whole housing stock; our own Land Registry model — which only sees properties sold since 1995, and is therefore a lower bound — finds about 127,000. We gross up our estimate of the £1.5m-£2m band (around 116,000 properties) by that same factor (165 ÷ 127 ≈ 1.30), giving roughly 150,000 additional properties on the OBR’s basis — close to the “more than 150,000 families” figure reported in the press. Static revenue is each band’s property count multiplied by its annual charge. The dynamic figures then apply the OBR’s aggregate behavioural retention rate (£400m ÷ £605m ≈ 66%), which on the OBR’s own numbers captures price capitalisation, bunching below thresholds, reduced new supply, non-payment, inability to pay, appeals, the low-income support scheme, and knock-on losses to stamp duty, capital gains tax and other taxes. This is a pretty crude approach, but suffices for a rough approximation.

An element of particular significance for the £1.5m band is to deduct the extra cost of the valuation exercise. The OBR’s £400m is the surcharge’s tax line only; the Valuation Office’s valuation work and councils’ administration are funded separately (the government has said local authorities will be “fully compensated”), so they sit outside the OBR figure. Lowering the threshold to £1.5m roughly doubles the properties in scope — from about 165,000 to about 315,000 — and so roughly doubles the valuation and collection workload. There is no published cost figure, but HMRC is recruiting up to 1,000 valuation officers, around a third of them for this surcharge – we would estimate that amounts to an overall cost of around £40m a year8, so extending to £1.5m adds roughly £40m a year (and more in the 2026-28 set-up and at each five-yearly revaluation, plus the cost of appeals on around 150,000 newly-caught homes). We deduct this ~£40m from columns 2 and 3 — it is the same for both, because they value the identical £1.5m base and differ only in the charge. Column 1 is held to the OBR figure (without an adjustment for valuation costs).

Another element more relevant to the £1.5m band is that we have applied house price inflation for detached properties. We did that because valuation specialists we spoke to thought detached-house price growth was a reasonable proxy for high-value property growth. It will not be perfect, particularly in London where many £1.5m-plus properties are flats or terraced houses, and house price inflation can vary widely between and within individual streets. However we don’t think any of this will impact the broad geographic pattern.

There are, finally, two sources of error for the £1.5m band which we expect will work in opposite directions. Our undercount is probably worse at lower values, so the new band could be nearer 165,000-170,000 properties, lifting columns 2 and 3 by around 3%. Against that, behavioural leakage is likely proportionately larger at £1.5m than at £2m — far more homes sit just above the threshold, and more are owned by asset-rich but income-constrained households — so borrowing the £2m retention rate probably flatters the dynamic figures. Figures are rounded to the nearest £5m, following the OBR’s approach.

The OBR’s original costing carried a “high” uncertainty rating. Our extrapolation is – obviously – much more uncertain than that.

Contains HM Land Registry data © Crown copyright and database right 2026, licensed under the Open Government Licence v3.0⚠️. Also contains Office for National Statistics house-price and postcode data, Valuation Office Agency council tax statistics, and Ordnance Survey and Royal Mail data, all © Crown / Royal Mail copyright and database right 2026 and licensed under the Open Government Licence v3.0. Revenue estimates draw on the Office for Budget Responsibility’s published costing.

Thanks to K for help with the code, and T, D and S for their property and valuation insight.

The mansion tax map: where the money comes from

What would a land value tax actually do?

Has Britain run out of “other people” to tax?

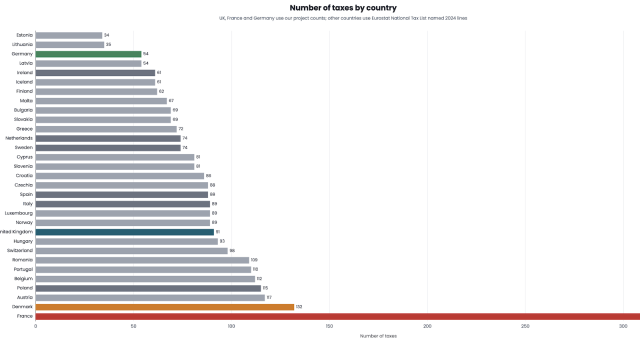

The UK has 90 different taxes. France has 348. Germany has 60. Why?

Why does Britain have more taxes than at any time since 1834?

90 UK taxes. On one chart.

Footnotes

The tax first applies in April 2028, but on values as at April 2026, revalued every five years. Our original post uprated to the most recent data then available; this version uprates to April 2026, using the latest ONS constituency price data (year ending September 2025) plus the England detached-house index from the UK House Price Index, which now runs to April 2026 (so no extrapolation/forecasting is required). ↩︎

All figures are our lower-bound estimates from Land Registry data – see the methodology section. On the same refreshed data, the announced £2m version catches around 127,000 properties and raises around £495m a year. ↩︎

Strictly the address-weighted centre, not the geometric centre. ↩︎

i.e. labelled detached, semi-detached, terraced or flat/maisonette. Almost all of those are residential. Some of the “Other” category will be residential too, but we’ve no way to screen those using only Land Registry data. ↩︎

The ONS constituency series currently runs to the year ending September 2025; from there to April 2026 we apply the England-wide detached-house index, over which prices moved by only about 1%. We also display 2025 council tax data on the map. ↩︎

Our original post estimated £510m using data to mid-2025; the update to April 2026 values and six more months of transactions moves it to £495m – a negligible difference given the approximate nature of this exercise. ↩︎

The OBR assumed clustering just below the thresholds and losses to other taxes, chiefly stamp duty. A £1.5m threshold puts far more ordinary-if-expensive family homes just inside scope, exactly where behavioural effects concentrate. ↩︎

This is a back-of-the-envelope estimate from discussions with former HMRC personnel. We take average gross employment cost of £70k per person and multiply by 300 officers = £21m. We then assume that systems and other associated costs will roughly double that figure. ↩︎

Leave a Reply