The UK loses £1bn each year to fraudulent claims for research and development (R&D) tax relief. We can reveal that one of the firms responsible is Green Jellyfish – one of the largest firms in the market. Green Jellyfish says it’s a specialist in research and development tax relief, and that they help companies claim an average of £32,000 in tax refunds from HMRC. But they claim tax relief that doesn’t exist, and then cover it up with the help of an affiliate, Kirby & Haslam. They’re making £3m a year in profits from ripping off the taxpayer and their own clients.

Update: there have now been arrests. Comments on this post are closed.

R&D tax relief costs the UK about £8bn each year, of which more than £1bn has been identified by HMRC as fraudulent1. This has all been widely reported, but, until now, nobody has publicly named the people responsible for the false claims.

We can identify that one of the largest R&D firms in the market has submitted a series of fake and potentially fraudulent R&D tax relief claims: Green Jellyfish. We have a dossier of clearly fake2 R&D tax relief claims made by Green Jellyfish and its associates. This article focuses on one – where Green Jellyfish’s client/ victim was Sophie3, who runs a small therapy business.

Green Jellyfish promised Sophie a “no win no fee” R&D tax relief claim, but there was never any basis for it, and when HMRC challenged it, Sophie was left with large bills. We believe she was defrauded. In other cases, where HMRC didn’t spot Green Jellyfish’s false claims, it will be the taxpayer who was defrauded.

We believe there is enough evidence for HMRC and the police to commence a criminal investigation, shut down Green Jellyfish’s business, and protect both their clients and the wider public interest.

R&D tax relief

R&D tax relief was created to encourage small companies to invest in research and development. It gives profit making companies a tax deduction which reduces their corporation tax bill, or in the case of loss-making companies the ability to surrender their losses for a cash payment from HMRC.

The term “research and development” is defined in guidance published by BEIS and given statutory force by the Corporation Tax Act 2010⚠️. HMRC summarise the rules as follows:4

The Times reported in 2022 about highly questionable R&D tax relief claims, with restaurants being encouraged to claim R&D relief for vegan menus. In our view, claims like this have no legal basis and may be fraudulent.

HMRC has been proactively investigating historic R&D tax relief fraud and making it harder for new fraudulent claims to be submitted. Sadly this has had knock-on effects on bona fide claimants.

Sophie’s story

Sophie runs a small therapy business. In 2021 she had £46k of revenue. She paid herself a salary of £12k, and had a profit of £18k (after other costs and corporation tax).

In 2022, Sophie was cold-called by Green Jellyfish, who said they thought her business could claim R&D tax relief.

As Sophie puts it:

“GJF from the start were persistent but very friendly and approachable, they seemed to know exactly what R and D was about, whereas I had never heard of it before. They were confident that my business could claim and after initial doubts I naively put my trust and faith in them.”

After the call, Green Jellyfish sent a follow-up email to Sophie saying this:

There is and was nothing on Sophie’s website that suggested any R&D activity. Green Jellyfish was at no point FCA-regulated. 5

And they explained their process:

We don’t believe anyone who’d even casually perused the HMRC website could “safely say that [Sophie would] easily fall within the parameters of the scheme”.

Sophie had no financial or tax background, and trusted that Green Jellyfish knew what they were talking about. She took up the offer of a telephone consultation. During the call, Green Jellyfish asked Sophie about her business and whether she thought it was “innovative”. Sophie said it was6, but didn’t provide much detail about what she did

Green Jellyfish didn’t ask about whether there were any specific R&D projects – it’s pretty obvious there weren’t, and couldn’t be, when Sophie’s business had one employee/director who was a therapist, not a researcher or engineer.

The evidence of fraud

Green Jellyfish then asked for Sophie’s accounts and corporation tax return:

And off the back of that, with no information about any R&D activity, Green Jellyfish submitted an R&D tax relief claim.

We believe this was likely fraudulent for two reasons.

First, Green Jellyfish had no basis for making a claim, because Sophie gave them no basis. They never provided her with any statement of what precisely the claim would be for, much less the kind of report you’d expect from an R&D firm. As Sophie put it to us:

“I remember chatting to Andrew about my business on the phone but I still don’t know what he was claiming for!“

This therefore isn’t a case of Green Jellyfish staff misunderstanding the legislation or guidance. There’s no evidence they paid any attention to the rules at all.

Second, Green Jellyfish claimed Sophie’s entire staff costs as qualifying R&D expenditure.

Here’s Sophie’s accounts for 2021 – we’ve blanked out the last three digits to preserve her anonymity:

Note the staff costs of £12k – the only staff member was Sophie herself. And Green Jellyfish claimed all of that as qualifying R&D expenditure:

This doesn’t survive five second’s scrutiny. Nobody in the business of filing R&D tax credit claims could seriously think Sophie spent absolutely all of her time on qualifying research and development activity.

So why did they claim the entire £12k? We expect that’s because the only way an R&D relief claim for a company of this size would make sense, and justify Green Jellyfish’s fee, is if they claimed 100% of staff costs.

We should add that we can be certain from this evidence that a false R&D tax relief claim was made, but we cannot be certain that a fraud was committed. That depends on whether those involved were dishonest to the criminal standard, which ultimately would be decided by a jury. We set out the criminal standard for fraud by false representation here, and for tax evasion (“cheating the revenue”) here.

But the evidence is in our view sufficient to merit a criminal investigation.

HMRC’s response

Green Jellyfish filed false R&D tax credit claims for Sophie for 2021 and 2022. HMRC immediately paid the refund, and Green Jellyfish took their fee.

A year later, HMRC told Sophie they were opening “compliance checks” into her R&D tax relief claims. That would mean Sophie would have to refund HMRC – and she’d remain out of pocket for Green Jellyfish’s fees.

Why does it work like this? Why couldn’t HMRC have checked the claim before paying the refund?

Because HMRC generally operate a “refund now, check later” policy. It’s a rational approach in a world of normal taxpayers and normal advisers. If HMRC checked first then refunds would take months. And who would put in a fake refund claim knowing that the consequence of getting it wrong would mean paying back the refund, plus interest and penalties?

But, unfortunately, “refund now, check later” creates a loophole for bad actors to exploit. Rogue R&D tax relief firms can file hopeless claims knowing that they keep their fees whatever happens, and that the risk sits with their poor clients like Sophie.

Kirby & Haslam

Sophie told Green Jellyfish she’d received a compliance check, and they passed her to an associated firm7, Kirby & Haslam.

At this point Sophie realised there was something very strange going on. Andrew had left Green Jellyfish, and the firm had no documentation for her claim. There was no report identifying the qualifying R&D expenditure, and not even a summary of her business activity. So Kirby & Haslam wrote to her asking the kind of questions that Green Jellyfish should have asked right at the start (but didn’t):

At this point an honest and competent firm would have realised that Sophie had no qualifying R&D expenditure. Kirby & Haslam took a different approach. They used Sophie’s responses to construct a response to HMRC which tried to claim that running remote therapy sessions during the Covid-19 lockdown was an “advance in science and technology” qualifying for R&D relief:

The idea this was an “advance in the field” is ridiculous, particularly at a time when almost every service business was finding ways to work remotely. We don’t believe any R&D tax expert would believe this claim had any prospect of success.

But the more serious problem is that it was entirely created after-the-event by Kirby & Haslam.

The consequence for Sophie

HMRC unsurprisingly rejected the Kirby & Haslam justification for her R&D tax relief claim (and another made subsequently for 2022). They sent Sophie a letter which explained why in some detail. For example:

This left Sophie with an unexpected bill of over £7,500 to repay to HMRC. That stung – because she’d only received a £4,500 refund… the rest had been taken by Green Jellyfish as their fee.

Sophie says:

“Just before Christmas I received a notice from HMRC that not only was I going to have to pay back the full amount of the first claim made by GJF, they had also found the second claim to be non-compliant, and I would also need to pay this back. I had no idea that HMRC were evaluating both claims so this came as a huge shock. I remember rushing over to my friend’s house in a state of distress, crying at the injustice of the situation and terrified about how I could pay the money back when it had already been absorbed into my business. At this stage my anxiety sky rocketed, and I spent a few days over Christmas feeling sick and stressed. I tried to put on a brave face around my children over Christmas as I did not want them to worry. The situation impacted on my mental health and triggered many negative emotions of fear, anxiety, isolation, anger, hopelessness and despair.”

The lies to escape penalties

At this point it looked likely Sophie would be hit with penalties for submitting a tax return that was “careless”.

Kirby & Haslam wrote representations to HMRC on Sophie’s behalf.

A normal firm in Kirby & Haslam’s position would have been appalled at Green Jellyfish’s original claim, and the representations would have described how Sophie had in essence been defrauded.

Instead, Kirby & Haslam wrote representations to HMRC which lied about the background. Here’s an email from them “correcting” Sophie’s initial answers to HMRC:

None of this was true. Sophie had relied entirely on the claim submission company. Andrew at Green Jellyfish (to whom Sophie had been speaking) was a “Business Development Manager”, not a tax specialist. She didn’t have a “thorough discussion” regarding her project, because she never discussed a project. Sophie had made no effort to understand the R&D tax relief claim criteria because they were never mentioned to her; she didn’t know what they were, or that they even existed.

Sophie was very uncomfortable with Kirby & Haslam’s proposed responses. She told us:

“Kirby and Haslem were pushing to avoid penalties from HMRC, and in my state of fear, I allowed them to talk me out of telling HMRC what I really wanted to say about GJF and their unscrupulous process. I was constantly told that as a company director I was expected to know about R and D and to have paid due diligence to the claim. I am a clinical professional, working in therapy. I am not a tax specialist and I’m rubbish at maths, so of course I couldn’t know the ins and outs of R and D. I had been led by the group of so called “specialists”. But apparently this was not good enough. Kirby and Haslem made me take responsibility for the claim without blaming GJF. I was so angry but felt alone with the problem, so saw no option but to take their guidance.“

Sophie escaped penalties. We think that’s a fair outcome under the circumstances – but it’s deeply unjust that Green Jellyfish and Kirby & Haslam aren’t subject to penalties themselves.

Could it just have been a mistake?

Not according to Green Jellyfish. When Sophie complained to them, they told her their “approach in preparing and submitting claims is always meticulous, based on the information provided to us and to the highest standards of care and skill”.

They refunded their fees for the 2021 claim, but not the 2022 claim (despite their “no win no fee” promise).

And it wasn’t a one-off either. We have a dossier of similar cases, often for much more money: R&D tax relief claims being made by Green Jellyfish on the basis of absolutely nothing, by businesses who realistically could never qualify. And then in these cases we again see Kirby & Haslam coming in after the event, and inventing rationales for the original claim. But at least in Sophie’s case the Kirby & Haslam document described her actual activity; we’ve seen other Kirby & Haslam letters which invent entirely fictitious R&D projects.

Green Jellyfish is not a small operation. Its accounts show that in 2022 it had 38 employees and made a profit of at least £3m.8

How much of Green Jellyfish’s business consists of genuine R&D claims, and how much fake claims? We can’t know. The size of our dossier convinces us there are many fake claims – but we can’t know if it’s 10% of their business or 100%.

We would, however, speculate that what we’ve seen is Green Jellyfish’s standard approach. We say that for several reasons:

- Green Jellyfish’s advertising consistently⚠️9 says that all you need for a claim is your corporation tax return and accounts.

- Sophie’s experience, and the other businesses we’ve spoken to, was consistent with that. No analysis of any projects, just the numbers in the accounts and tax return.

- Green Jellyfish doesn’t appear to employ any tax advisers. Only salespeople and business development officers. This isn’t how you build a legitimate R&D tax relief business – R&D tax relief is highly technical.

- Kirby & Haslam didn’t seem to think there was anything strange about the absence of any records from Green Jellyfish, or the fact that they were constructing entirely original arguments for R&D tax credit relief.

- Sophie’s complaint was the opportunity for a bona fide company to look at its processes and consider whether her tax relief claim had been properly handled. They instead just lied to her (“meticulous”).

Even if most/all of Green Jellyfish’s R&D tax relief claims are false, we expect some of their clients will be very happy. HMRC are unlikely to be able to identify all the false claims, and some clients will inevitably keep their refunds (even if there’s a criminal investigation).10 In those cases, it’s HMRC and the wider body of taxpayers that lose out.

Paul Rosser

This report only exists because of years of work by Paul Rosser.11

Paul is an R&D tax specialist. He’s often asked by non-specialist accountants to check R&D claims, particularly when they’re prepared by outside firms who the accountants don’t know. In 2020 he started to see claims prepared by Green Jellyfish which he thought were clearly invalid. Paul had been writing about the dubious end of the claims industry. Paul now wrote specifically about Green Jellyfish on LinkedIn, and named the firm.

On the evening of 25 April 2024, Sotiris Christophi arrived unannounced at Paul’s home and threatened him. He said Green Jellyfish had been through Paul and his wife’s social media accounts, and was preparing to release some unfavourable information about Paul to the public. Paul immediately told him to leave. Christophi then made a series of calls to Paul’s wife’s personal mobile phone.

We asked Christophi about this back in April: he responded saying he regretted his actions, and asking to speak to us in person. We said we would prefer if Christophi could put his position in writing;12 we never heard back.

The tip of the iceberg

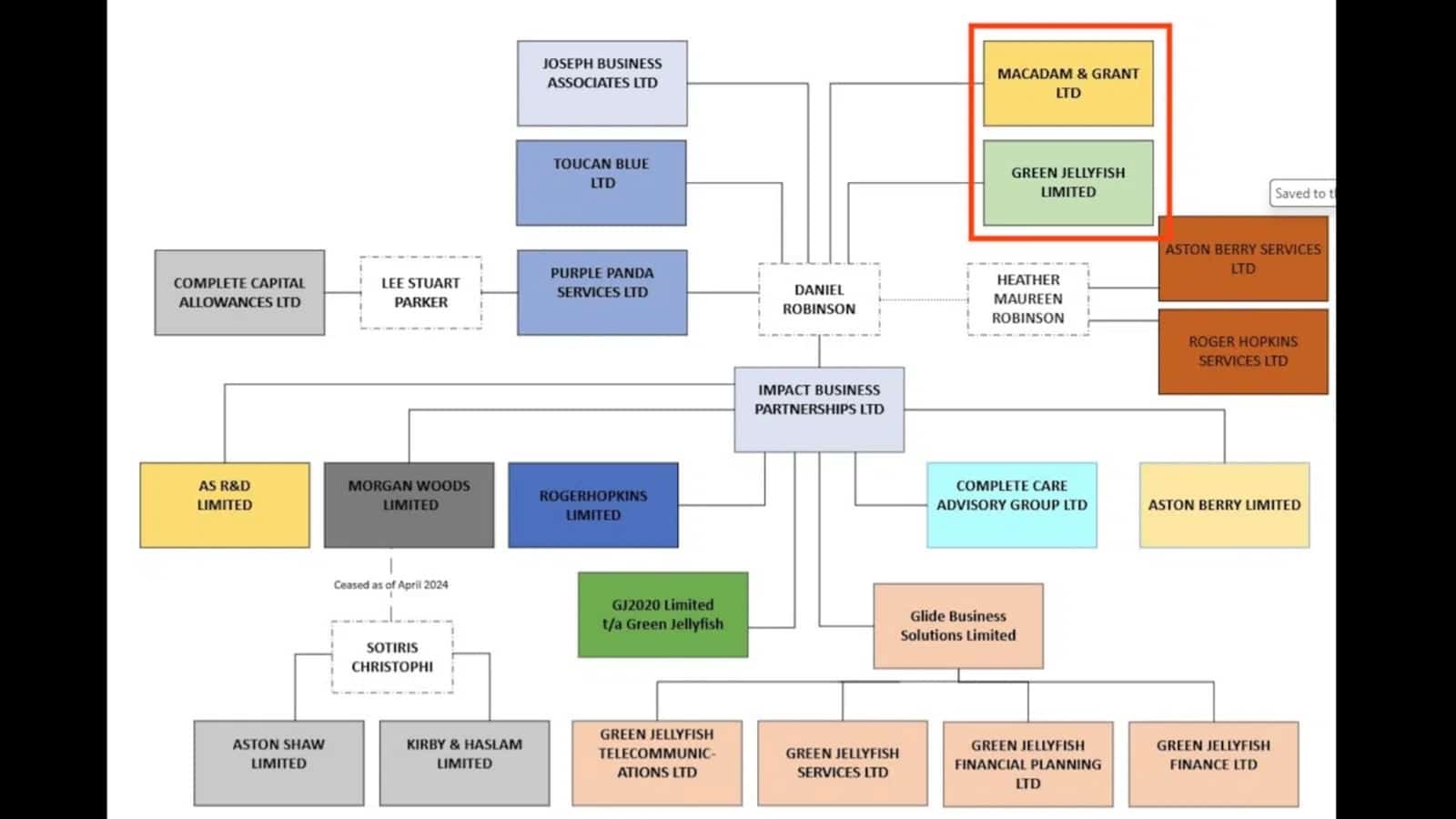

There is a large network of companies associated with Green Jellyfish:13

Notable companies in the network are:

- GJ2020 Limited – the Green Jellyfish business; it was called Green Jellyfish Ltd but changed its name in September 2023.14

- Purple Panda Services Ltd, which runs the Purple Panda⚠️ business. This appears to have a similar business and branding to Green Jellyfish.

- Kirby & Haslam⚠️ – a more seriously-branded R&D firm

- Aston Shaw, an accounting firm.

The precise links between the companies aren’t clear but there is clearly a close relationship between Green Jellyfish and Kirby & Haslam. An adviser acting at arm’s length would have advised Sophie to tell HMRC she was misled by Green Jellyfish. A normal adviser would not accept repeated referrals of improper claims. The letter from Green Jellyfish responding to Sophie’s complaint was (according to the metadata) written by a paralegal working for Kirby & Haslam.

Kirby & Haslam and Aston Shaw are owned by Sotiris/Steve Christophi, an accountant regulated by the Association of Chartered Certified Accountants (ACCA).15 Christophi denies a connection to Green Jellyfish, but he certainly seemed to be speaking for Green Jellyfish when he visited Paul Rosser’s home to threaten him.

We have a dossier of other apparently fraudulent tax relief claims made by these companies, and will be writing more about them soon.

Green Jellyfish’s response

Last week we wrote to Fladgate LLP, who act for both Christophi and Green Jellyfish.

We put to Fladgate that Green Jellyfish submits R&D claims with no technical basis, and all it does is review a company’s corporation tax returns and accounts. We also put to them that Kirby & Haslam invent justifications for Green Jellyfish’s claims after the fact.

There were several curious features to Fladgate’s response:

- The Fladgate letter was labelled as “confidential”. It wasn’t. Solicitors are not permitted to falsely label letters as confidential, and one solicitor is currently appearing before the Solicitors Disciplinary Tribunal as a result of such a mislabelling.16

- Most of Fladgate’s letter to us is taken up with allegations of an “unlawful means conspiracy” against Green Jellyfish by former employees, rival R&D advisers, and an individual who Christophi is currently suing. We have no interest or understanding of any of this (we’re confident that Sophie’s story is real). It is, however, most unusual for a solicitor to put in correspondence what amounts to a conspiracy theory.

- Fladgate deny that Green Jellyfish or Kirby & Haslam is behaving improperly, but the denial is very non-specific.

- Specific denials are then included in a separate email from Christophi (on behalf of Kirby & Haslam) and an unknown individual representing Green Jellyfish, which Fladgate forwarded to us. The evidence above (and other evidence we have collated) shows these denials to be false.

- The Christophi/Green Jellyfish email rather deceptively ducks our allegation that it’s improper for Green Jellyfish to claim that care homes, restaurants and childcare companies can often claim R&D relief. (“The legislation is very clear and does not exclude a company from making an R&D claim based solely on the sector.“)17

We responded to Fladgate saying that we had evidence of actual fraud; we have not heard back.

Fladgate is a fine firm with a good reputation. We think there will be widespread disquiet amongst its partners that it’s acting for a business that is widely suspected of fraud, denying that fraud in the face of public evidence, and repeating their client’s wild conspiracy theories.

Everyone, guilty or innocent, deserves a criminal defence, and no criminal lawyer should be criticised for acting for any defendant, no matter how repugnant their crimes. However, defamation is very different. There is no professional or moral duty for a solicitor to write defamation threats on behalf of a business when there is good reason to believe it is carrying on a fraud. Particularly when the consequence of acting is that the solicitor will be facilitating the fraud.

HMRC’s response

HMRC is prohibited from commenting on individual taxpayers, but told us:

“With R&D claims, public money is at stake and taxpayers rightly expect us to scrutinise them, which is why we have increased compliance activity. We do that thoroughly and fairly, and the overwhelming majority of valid claims are paid on time.

Any customers who have a concern about an R&D claim they have made, or may have been made on their behalf, should email: [email protected] They should title the email as ‘For the attention of the R&D Anti Abuse Unit’“

What should happen to Green Jellyfish?

Sophie has been deeply affected by what happened to her:

“I contemplated closing my business, as it does not make a huge turnover and I wondered if all this pressure was worth it. I used most of my savings paying back the requested amount and I am still trying to build my savings back up.

I always follow the rules and trust others to do the right thing, and it felt like I had been taken for an idiot. I don’t understand the mentality of people who act like this and I feel let down by what I’ve experienced.“

We don’t think Sophie should blame herself. She was the victim of what looks like a fraud. Those responsible should pay the price.

We will be referring Christophi to the ACCA, although we don’t have much hope – the ACCA unaccountably is refusing to investigate Christophi’s threat to Paul Rosser. We will also be reporting Green Jellyfish’s false claim of FCA regulation to the FCA.

And the evidence presented in this article suggests that Green Jellyfish and the individuals who run it have defrauded both their own clients and HMRC.

We believe there should be an immediate criminal investigation.

We hope the authorities can move quickly; past experience is that Green Jellyfish and those behind it may not stick around to face the consequences of their actions.

How to stop the tax cowboys

Green Jellyfish are not the only tax firm defrauding their clients and HMRC.

The previous Government thought the answer was regulation – they ran a consultation on “raising standards in the tax advice market“.18 We don’t agree. Green Jellyfish weren’t regulated, but acted with total disregard for the law – they’d disregard regulation too. And Kirby & Haslam was regulated.

So it’s not at all clear that regulation is the answer. It would, however, come with a cost – a new regulatory edifice to be created for currently unregulated advisers, most of whom do a good job. That means cost for them, cost for their clients, and cost for the taxpayer.

The better answer is a simpler and more powerful one: change the incentives. Right now, the reward of churning out fake tax claims is large, and the risk of serious sanctions, or criminal prosecution, is perceived to be low. That needs to change.

Our suggestion: create a new criminal offence of promoting tax schemes, or technical tax positions, that are so unreasonable that no reasonable adviser would think they were correct.19 The offence would be accompanied by civil tax penalties equal to 100% of the tax in question, chargeable on the companies involved and the people behind them.

The challenge is to shape the new rules so that the cowboys are pushed out of the business, but legitimate advisers have nothing to be concerned about. That’s hard, but not impossible. And it’s been achieved before. When the General Anti-Abuse Rule was introduced in 2013, some feared it could apply to “normal” tax planning – in practice it hasn’t.

That’s what we’re proposing – a GAAR-style rule that’s carefully aimed at the cowboys, and with very serious consequences when it applies.

Many people’s instinctive response is that we should “make tax avoidance illegal”. That can’t, and shouldn’t be done, because we can’t rigorously define “tax avoidance”.

But we can rigorously define “trying to avoid tax by taking a position that isn’t in fact legally correct, and is so unreasonable that no reasonable adviser would have taken it”. And then make that a criminal offence.

It would be more effective than a new regulatory framework, and an awful lot simpler.

Full credit to Paul Rosser of R&D Consulting for discovering and pursuing this story over the last couple of years. It’s an extraordinary story of a tax professional doing the right thing despite considerable professional, legal and even physical risk. This article wouldn’t exist without Paul.20

Thanks above all to Sophie (and other clients/victims of Green Jellyfish) for telling us their stories. We’ve anonymised Sophie’s details but she’s aware that Green Jellyfish and K&H may identify her; in the unlikely event they’re stupid enough to threaten her, we will take full responsibility for her defence.

Many thanks to K and T for their R&D tax relief expertise, to P for additional research, and as ever to S for his invaluable review and insights. Thanks to J for picking up an accounting error in the original draft.

Some images and text © GJ2020 Limited, and used here in the public interest and for purposes of criticism.

Corporate structure diagram © Paul Rosser.

Footnotes

Hopefully the figure will be much smaller going forward, following new rules requiring much more detail in applications from 1 August 2023 ↩︎

By which we mean not just technically wrong, but indefensible ↩︎

Sophie is not her real name. For the reasons we set out below, we will not be identifying any of our sources for our Green Jellyfish investigation, except Paul Rosser. We have hidden Sophie’s name, and the details of her business, but not changed anything material to her story. ↩︎

The guidance in 2021 on this point is the same – you can see the 2021 version via the Internet Archive here. The main link is to the current HMRC website because we know some people cannot easily access the Internet Archive⚠️. ↩︎

Prior to 2 July 2021, Green Jellyfish was owned by Glide Business Solutions, which was FCA-regulated. However that is irrelevant to the status of Green Jellyfish and its staff, and in any event Glide wasn’t the shareholder when the email was sent to Sophie in 2022 ↩︎

We agree; the way Sophie carried on her therapy business during lockdown was “innovative” in the normal business meaning of the term; but that’s very different from having qualifying R&D expenditure. ↩︎

The precise nature of the association isn’t clear; more on that below ↩︎

The accounts show £558k of corporation tax owing to HMRC; the corporation tax rate at the time was 19% – this implies taxable profit of £558k/19% = £3m. The P&L reserve increased by £2.6m from 2021 to 2022, implying that taxable profits were lower then accounting profits by at least £150k. Some of this was likely due to capital allowances, as there was a c£200k addition to plant and machinery. Dividends may also have been paid. And we would not be surprised if the company artificially depressed its taxable profit, given how cavalier Green Jellyfish was with its clients’ tax position. Note that there was an accounting error in the original version of this footnote; many thanks to J for picking this up. ↩︎

Click “What documentation do I need to prepare my claim” ↩︎

Although, given this appears to be a case of deliberate false claims, HMRC will have 20 years to investigate such clients. ↩︎

It is important to add, however, that the contents of this report were written by Tax Policy Associates independently, and the only element which relies solely on evidence from Paul Rosser is the tale of Christophi’s unexpected visit. Christophi has, however, admitted that the event took place. ↩︎

The subjects of our investigation often ask to speak in person; standard journalistic practice is that responses should be in writing, and we believe there are numerous reasons why that is the only sensible approach. ↩︎

Many thanks to Paul Rosser for the diagram, which is a product of considerable research by him. The group structure has since changed slightly. ↩︎

There is something odd going on with its directors, who keep resigning and being reappointed. We don’t understand why that would happen. ↩︎

Christophi is also sometimes known as Sotos Christophi, and you can find him under that name on the ACCA website. He is referenced in this rather curious press report from 2019 about a council being “hindered” (in an unspecified way) from collecting business rates. ↩︎

Fladgate subsequently told us that they labelled the letter as “confidential” because they mention a police investigation. They have no first hand knowledge of that investigation and don’t appear certain it exists. We have no idea why they thought the repetition of what is little more than a rumour would be “confidential”. ↩︎

Technically it is highly unlikely for businesses of this type to be eligible for R&D relief, but there is little point in debating the law when there is evidence of fraud. We don’t intend to go into this point any further with Christophi/Green Jellyfish. ↩︎

It closed shortly before the election, and so we haven’t had a response or any follow-up, but we believe officials are still proceeding on the assumption this will be the way forward. ↩︎

There would have to be a fair defence for cases where a mistake was made by genuine accident, or where a rogue employee acted despite compliance measures being put in place. ↩︎

But, as ever, Tax Policy Associates Limited takes sole responsibility for the content of this article. ↩︎

“GDPR tax credit” fraud, from the people behind Green Jellyfish

The British fugitive, his $600m US tax fraud, and its 3,000 victims

Liberty Rock’s claim that a magic cheque can pay your tax

Inside a fake tax refund factory

Finance Monthly fabricated an interview with me

Herran Finance – another fake bank at Companies House

Comments are now closed for legal reasons. Our apologies.

39 responses to ““Green Jellyfish”: we reveal one of the firms responsible for the £1bn cost of fraudulent R&D tax relief claims.”

It should be quite obvious to those using Green Jellyfish that they probably weren’t entitled to free money for R&D Credits if they weren’t actually doing any R&D. I’m struggling to be sympathetic towards their plight as they’ve allowed Green Jellyfish to help them make fraudulent claims and then suffered the consequences. This has happened time and time again and will no doubt continue to until the system is robust enough to stop it.

GJ were/are brilliant salespeople. The businesses were usually very small, and had never heard of R&D tax relief at all. So when they have someone telling them that their innovative business qualifies for the relief, and that’s the intention, I understand they they believed it.

where do we go from here?

Complete Care Advisory ltd is part of the cabal fradulantly claiming R&D payments from HMRC.

Mark Daniel Robinson, Also of Green Jellyfish one of the main protaganists.

This is superb – great investigation as well. Trying to help companies is great but doing it properly, sensibly and more responsibly needs to the way forward. Thanks to Dan and Paul for their monstrous work. Those of us trying to do it properly often get overlooked as the big firms promise the earth and deliver nothing.

Amazing investigation and reporting. Sadly I am another victim of Green Jellyfish’s fraud. Similar to Sophie’s story, I have had to pay everything back to HMRC, including the huge commission that Green Jellyfish took, plus significant interest payments. I have tried to contact Green Jellyfish to complain and request some of their commission back, but they never respond to me.

I run a small business and we cannot afford to lose the many, many thousands that Green Jellyfish took as part of this scam. I have documented evidence of what they sent to HMRC and it’s fraudulent, false and explicitly makes claims that I said are not true (such as plans to sell software to the market, which is total nonsense – there are other examples too). I never got to see the report or approve it before it was sent to HMRC, I just suddenly received an email from Green Jellyfish saying HMRC had approved the claim.

I am tempted to take legal action as Green Jellyfish won’t respond to me, but we’ve lost so much money in this scam, it would be difficult to finance.

Martin there is a class action being prepared by lots of their clients owed money.

I believe it’s on a no win, no fee basis so if you want to look at joining the solicitor is Nick Ashcroft at Addleshaw Goddard [edited by TPAL to remove his email address for spam protection]

Cheers

Paul

Great work Dan.

The Great Train Robbery team stole £70million of public money in today’s prices. A serious police team went after the crooks and chased them to the ends of the planet. Just saying.

We are also defrauded by Complete care advisory group limited and director at that time now is a director of Green jelly fish limited. They submitted report on our behalf which was totally bogus. They took £17800 from HMRc . HMrC later removed the claim as a fraudulent claim and now asking for the money back . CCA not giving the money back and asking me to re-claim . I refused as they are liars, cheaters and Fraudsters . Problem is no one taking action against them . I have now hired a law firm to take action against them . I like to know if more people can also join as we must do whatever we can to expose these sham companies.My email is REDACTED

I had green jelly fish constantly badgering me about projects and how we were eligible because we were in social care to claim back money and how they would do all the work for us wouldn’t have to do anything, kept saying no thanks. Then we had I’m sure a different firm that had 4 “projects” you could pick from and they would claim the money back off the tax so nearly signed up to that one but got my accountant to check through the contract first there was info we felt was suspect luckily I never signed it

Good work Dan and Paul.

We have to stand up to these people. I had one trying sell a ludicrous scheme based on the GDPR regulations

They seem to move around so perhaps keep tabs on them and publish their new companies

Thank you Mike.

Ahh yes the old GDPR data breach tax scam, well know and called out by HMRC as totally fraudulent.

I think that HMRC does what it can with the resources available to it – they were enormously helpful to myself, and my company, when I inadvertently got sold tax credits as a “government incentive scheme to assist companies post pandemic” – not a “bounce back scheme”, rather, a genuine “thanks for getting the country through this” type of scheme – as long as you had genuinely gone to extraordinary lengths not to be a burden, and displayed some innovation in the face of adversity.

Yes, of course I was mugged off by these charlatans and now have a debt to pay but I’d rather pay for my stupidity and sleep easy. I didn’t get charged a penalty fortunately.

The last I heard I was being threatened with legal action but I’ve heard nothing for a tear or so now. Bring it on I say because I have all the emails they sent – “I can confirm that you will be paid even if the claim is challenged because you have chosen option B”. Jeez how can I have been so stupid?

Anyway, my claim went through Roger Hopkins Limited – essentially the same company.

Refreshing to see some sunlight shone on this merky area of tax. Sadly HMRC appear to have been asleep at the wheel and clearly have evidence in their records to spot trends and act far more promptly to close down these cowboys.

I agree that regulation won’t achieve anything other than policies and bureaucracy for bona fide tax advisers… the cowboys will continue to ignore … unless they are in the cross-hairs. Like Money Laundering – massive amounts of bureaucracy for all regulated firms etc. But the crooks and ‘bent’ firms sidestep and disregard. I entirely agree the crooks need to be held accountable with penalties to match tax and fees and exceed such for repeat offenders… with some threshold (20 cases?) Sufficient to trigger immediate action to freeze accounts pending a prompt and timely investigation with confiscation of all proceeds of crime.

Lastly much of this sector initially sought clients by significant referral fees (classic pyramid selling) from lawyers and accountants – PCRT requires full disclosure of such commissions and the various professional bodies need to consider if they have done enough to advise their members and protect them and public from these charlatan firms as well as policing compliance… should Sophie’s advisers been more curious?

We had similar with a client persuaded to made a claim for 2 years by RDI Solutions. HMRC paid out, to RDI Solutions, but then rejected the claim, just as RDI Solutions called in the administrators.

This was back in March, client has not heard anything and no idea where £65K went.

Below is all we know

RDI Solutions has called in insolvency practitioners and told clients they will have to wait a month for any kind of update

Clients of the research and development (R&D) claims firm have been left hanging as RDI Solutions called in Absolute Recovery Limited to review whether the business will have to go into administration or can be restructured. The licensed insolvency practitioner at Doncaster based Absolute Recovery is Stephen Richard Penn.

This follows the closure of the R&D company earlier this week when the RDI Solutions’ website was taken down, leaving only a notice online that the business was ‘not in operation’, having effectively suspended all activity.

A brief holding message on the RDI Solutions website has now been updated, stating that the company email has been disabled and is no longer available.

Any existing customers have been told they will have to wait minimum 30 days before they are contacted by the insolvency practitioner.

The company is run by owner and sole director Naim Mahmud through Mahmud Group Holdings and was set up in 2019; earlier this month the only four remaining directors resigned.

When it was up and running, RDI claimed it handled monthly R&D claims worth around £20m in tax relief, representing a sizeable annual claim book of £240m, and had ‘3,000 clients’. Accounts at Companies House show extensive director loans and intergroup loans are outstanding.

In a statement, RDI Solutions said: ‘The company is currently seeking advice from an insolvency practitioners to assess the company’s financial position and the best course of action moving forward for the business while it attempts to restructure.

‘There is currently no access to the company emails, for any enquiries, please contact Michael at Absolute Recovery Limited and he will assist with your query.

‘If your query can wait, Absolute Recovery Limited will be in touch in the next 30 days.’

Unfortunately the statement of affairs for RDI contains some concerning news regarding it’s assets

https://www.linkedin.com/posts/paul-rosser-3979514_since-the-sudden-closure-of-rdi-solutions-activity-7204394900161748992-S7gr

For the morally bankrupt, any chance to get ‘free money’ if HMRC adopt a pay now, ask later approach is just too tempting. More fool HMRC for thinking that leopards change spots, same with Covid loans, more free money. They never ever do.

There should be a post office style enquiry about HMRC and the taxpayer funds they have handed over to these tax crooks, starting with Harra.

From my personal knowledge of the accounting firm, who have a terrible reputation in Norfolk, I’d say it is highly probably that all of these ‘yellow brick (taxpayer funds) roads’ lead to them and their owner.

Fascinating story.

Several “rogue” companies offering help to SMEs who want to claim R&D tax credits were set up because the original scheme was so generous and scrutiny of claims seemed so lax. Paying companies that were making losses was the icing on the cake.

It seemed that Government wanted to be seen to be helping small firms invest. They even adjusted the national figures for investment to include the credits given under the scheme.

Similar misuse of the Entrepreneurs Tax relief scheme took place when 10% tax relief was available for up to £10 million.

Keep up the good work.

If you have a system which dangles a carrot to a wide boy, the wide boy is going to chase the carrot. One such system is HMRC cash repayments for R&D claims.

To make matters worse, the client pool of the likes of Jellyfish includes not only the greedy man looking to get one over on HMRC, but the unsuspecting small business who don’t even know what R&D is.

An impressive piece of investigative journalism, Dan and Paul – well done.

Another approach to tackling the rogue R&D tax advisers is to leverage the ‘Dishonest Tax Agent’ civil penalties introduced under Schedule 38 of the Finance Act 2012. These penalties can reach up to £50,000 and include the publication of the agent’s details. Operating under a civil standard and the balance of probabilities, HMRC only needs a ‘reason to believe’ to impose them, rather than the establishment of proof beyond reasonable doubt. Despite being woefully underutilised, these penalties would be ideally suited for situations like this, with the added bonus of granting HMRC access to the R&D adviser’s working papers and files, giving HMRC a deeper insight into any potential web of deceit. Greater use of these penalties is something we’ve advocated for with HMRC and HMT. We should also increase the upper-level amount now that the legislation is more than a decade old. I’ve put a link to the relevant guidance below:

https://www.gov.uk/guidance/dishonest-conduct-by-tax-agents

Thanks Jonathan.

I totally agree, HMRC should be looking at penalties for those behind Green Jellyfish, as the amounts they have generated in fees alone is eyewatering and there should be some negative consequences to act as a deterrent for others considering defrauding the taxpayer.

Good to see you having the bravery to out a firm like this and highlight the serious question of why HMRC haven’t taken steps to shut them down before now (by refusing to accept claims from them etc) given what they obviously know. Keep up the good work and hopefully HMRC will eventually step up and be much more proactive in this space.

Thanks Dan, always producing amazing articles. I know you covered a lot on LessTax4Landlords and how they were corporate sponsors at the National Landlords Show. There’s also a company by the name of Comprehensive Tax Planning that still exhibits at the show they also seem to claim R&D as the “most generous corporate tax relief”.

Thank Dan and Paul for helping the victims of GJF to get the truth out but importantly publicising this huge scam at the cost of the tax payer and SME.

It’s funny how Dan Robinson (CEO of Impact) has taken dividends but refuses to pay the staff their redundancy wages. If you want a story on this – get in touch, I’ll happily provide proof.

thanks – I’m aware there are various stories going round about Impact potentially being wound up, but I’ll leave that to others and focus on the tax.

I was one of those GJF put a claim in for and I had to pay it back like Sophie.

The scale of losses here is breathtaking. I agree with what you say about the desirability of paying valid claims quickly and the potential solution. That said in economic terms the relief was poorly designed, HMRC were slow to spot the truly incredible growth in claims by small businesses and traditionally one of HMRC’s tools was identifying and monitoring suspected “rogue” advisors to direct scrutiny toward claims from that source. Equally criminal sanctions applied to such professionals. These cowboy “advisors” are far from professional but bringing together a group of people and going out to make claims which look fraudulent seem to me to have the makings of conspiracy charges.

I’m surprised this otherwise excellent article doesn’t appear to refer to the Claims Notification regime which was introduced last August to cut these cowboys off at the knees.

Admittedly I’m not sure whether it is applicable to SMEs as well as those claiming the RDEC, but it seems to me to be an excellent way of making cowboy claims redundant, as it would no longer permit the making of last minute claims from those companies who had never made a prior claim.

I believe this is just the first article in a series.

Yes, the measures HMRC have put in recently such as pre-notification and the Additional Information Form (AIF) are helping reduce fraud, however historically billions of taxpayer funds have been lost before HMRC did very much to stop it.

To be fair I can see that this is covered within one of Dan’s hyperlinks.

Lesson for every Taxpayer , don’t go on blind dates following call from supposedly reputable firms offering their services while claiming FCA regulated. Simple call to FCA verify their registration details. Do your research and request fee quotes in writing from several firms together with draft letter of engagement.Do they hold PI insurance. Finally my main reason for contacting you is the surprise Barclays Bank have Debenture and Cross Company Guarantee registered 26 March , given the adverse publicity and commentary from various professional individuals does Barclays ignore social media posts such as Linkedin . Banks claim they lend to people, well with the myriad of director resignations and reappointments then surely this another red flag or perhaps they are good at giving plausible stories to their senior lenders !

I think I talked to Green Jellyfish not long after they were established. From memory they were wanting us to refer our clients. Luckily for us we didn’t make any referrals because I wasn’t sufficiently satisfied with what they had told me.They also seemed to have an awful lot of staff for a start up. Looks like we dodged a bullet.

Did Sophie’s company not have accountants drawing up the accounts and initial CT600 return. Surely she could have asked then for advice about the claim?

A client of mine had the same issue with G.Jellyfish. GF changed and resubmitted accounts and CT600s that I prepared as accountants without my knowledge or consent.

they told her they weren’t specialists and don’t seem to have checked it at all. A shame.

Great work keep it up.

There must be an argument for HMRC to tell similar stories in real time. I know they can issue warnings in real time and report after prosecution but this so much more impactful. More legislation to pull back further the rules that enable these people to operate in the shadows.

The email linked in the sentence “Specific denials are then included in a separate email from Christophi” (under the section Green Jellyfish’s response) appears to actually be TPA’s response to Fladgate, not their reply – just FYI.

thanks – think this is now fixed!

Brilliant work Dan. Hope you are as well regarded by Ms Reeves et alas you should be.