BBC Merseyside is reporting on a ludicrous attempt to avoid business rates using snails. It is so stupid that I cannot do justice to it – please read the story (radio version here).

This is, however, just one of many stupid schemes to avoid business rates. And the bizarre thing is that historically they have mostly worked. Here’s why – and how the Government should step in.

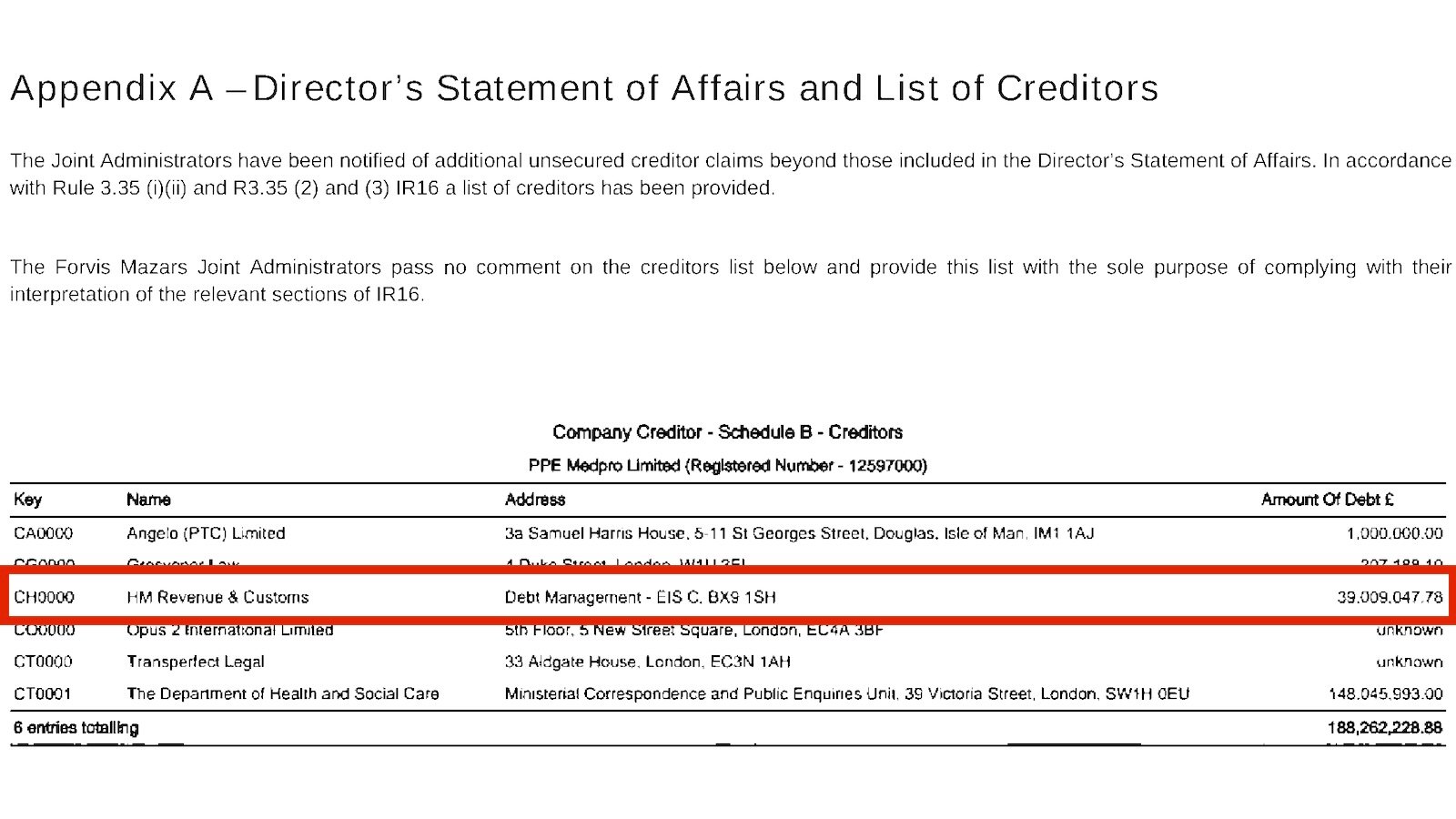

Cardboard boxes

There is a whole industry devoted to “business rates mitigation” – i.e. avoidance.

The most well-known scheme doesn’t involve snails – it’s all about cardboard boxes.

The idea is that landowners grant a lease to a tax avoidance firm. The firm stores a few boxes in the property for six weeks1, then leaves and terminates the lease. This is claimed to be “occupation” and so, after the short lease terminates, the landowner claims “empty property relief” from business rates for the next three months.2 The landowner pays 20% of its tax savings to the tax avoidance firm. And then does the whole thing again when the three months ends. And again.

It’s called “box shifting” and has been widely reported⚠️.

To a tax lawyer, this looks laughable. It’s an artificial scheme where the only purpose is tax avoidance – and the courts have spent the last 25 years striking down almost every tax avoidance scheme they’ve seen. This one isn’t even clever. I think most tax lawyers would expect the courts to shred box-shifting schemes in minutes.

But in fact the courts have repeatedly approved these schemes.

In the Principled case from 2013, the judge ruled for the landowner, saying:

“I cannot see any good reason why, if ethics and morality are excluded from the discussion, the thing of value to the possessor should not be the occupancy itself. The verb “occupy” and the nouns “occupation”, “occupancy” and “occupier” are, in the end, ordinary English words. Their meaning has developed in case law to give them a sensible construction, but they have not been given technical statutory definitions.”

And the same judge, in the Public Health England case from 2021, applied judicial reasoning from 1949:

And then one of his “propositions of law”:

“it does not matter if the possessor’s predominant or sole motive is mitigation of or exemption from rates liability“

(I’m appalled that a government body would not only buy a tax avoidance scheme, but then cause government money to be spent on both sides of litigation defending it.)

The reason this is so surprising to tax lawyers is that it’s not how modern statutory interpretation of tax law works. Following the Ramsay case in 1982, and the Furniss v Dawson case a year later, the courts began to apply tax law purposively, interpreting terms in light of their realistic purpose. There is an excellent summary of the law here, from law firm Norton Rose Fulbright. So when a judgment starts off by using the words “tax avoidance”, the result is almost always that HMRC wins, and the taxpayer loses.

Except business rates. As this article says, the courts seemed to accept that “rate mitigation schemes” were legal and proper practice.

The result was an explosion in business rates avoidance, driven by a mini-industry of “business rates mitigation advisers” charging 20% of the tax saving.

Box-shifting was the most common scheme, but there were numerous variants – my favourite (upheld🔒 by the High Court) involved the entirely tax-motivated installation of “blue tooth3 equipment”. The snail scheme seems particularly egregious, but it’s not insane to suggest it would have worked.4

Why did the schemes succeed?

So why was it that the courts have been merrily striking down every tax avoidance scheme they see, but approving business rates avoidance schemes? There’s no reason to think that business rates are any different from any other tax.

Informed observers5 have suggested three key reasons:

- HMRC has had massive success litigating avoidance schemes in the last 25 years, and lost very few cases.6 However, business rates cases are usually litigated by local authorities, who don’t have this experience or expertise.

- The lawyers acting for the local authorities tended to be planning and local government lawyers, not tax specialists. Undoubtedly they are very able, but they did not run the cases as tax avoidance cases. So in the Principled and Public Health England cases, Ramsay was not even argued.7

- Cases don’t come before tax tribunals and tax judges, who would have disposed of these schemes in fifteen minutes. Instead they usually end up as judicial reviews8, and (very unsatisfactorily) these courts did not apply the modern approach to interpretation of tax law.9

In other words: not enough tax lawyers.10

The Supreme Court brings some common sense

This all changed in 2021 with the Hurstwood case, when a particularly aggressive business rates avoidance case hit the Supreme Court.

Things are looking bad for the landowner when we get to the fourth paragraph of the judgment:

“The liquidation version of the scheme (in the form described in this judgment) has already been judicially branded an abuse of the insolvency legislation in proceedings for the winding up in the public interest of a company which promoted and managed such a scheme: see In re PAG Management Services Ltd [2015] EWHC 2404 (Ch); [2015] BCC 720. As will appear, the dissolution version of the scheme is no less an abuse of legal process and may in certain circumstances involve the commission of a criminal offence.“

And, as often happens, particularly bad facts result in a significant change of judicial approach that will affect everybody.

The Court jumped straight to the Ramsay principle five paragraphs later, saying that it had “reached a state of well-settled maturity“.

And then it only took one paragraph to reach the obvious conclusion:

“In our view, Parliament cannot sensibly be taken to have intended that “the person entitled to possession” of an unoccupied property on whom the liability for rates is imposed should encompass a company which has no real or practical ability to exercise its legal right to possession and on which that legal right has been conferred for no purpose other than the avoidance of liability for rates. Still less can Parliament rationally be taken to have intended that an entitlement created with the aim of acting unlawfully and abusing procedures provided by company and insolvency law should fall within the statutory description.“

When it comes to tax avoidance schemes, the common-sense result is usually the correct legal result. The taxpayer lost.11

So how come the High Court, and the Court of Appeal had come to the opposite conclusion? Because, said the Supreme Court, the local authorities and their lawyers had been rubbish at arguing their case. I paraphrase only slightly:

“The courts below appear to have received little assistance from counsel for the local authorities as regards the purpose of the rating legislation; and the same was true in this court. It is perhaps unsurprising that in these circumstances the judge and the Court of Appeal did not adopt a purposive approach to interpreting the relevant statutory provisions and considered that the “owner” as defined in section 65(1) of the 1988 Act must invariably and even on the assumed facts of these cases be identified as the person who is entitled to possession of a hereditament as a matter of the law of real property.“

They should have hired a tax lawyer – and then the local authorities wouldn’t have spent a fortune on taking a simple case all the way to the Supreme Court.

But aren’t business rates an unfair burden on many businesses?

Not as much as is often claimed. The evidence suggests that most of the economic burden of business rates falls on landowners, not retailers/tenants. This is a counter-intuitive result, and retailers often argue strongly that it’s they who are paying. They are, however, wrong – retailers pay the tax, but in the long term the burden is passed to landowners in the form of lower rents, with 75% of the cost of business rates passed onto landowners after three years.

There are certainly problems with business rates, not least that the slow five year cycle of revaluations means that retailers can be caught paying business rates that are out of all proportion to their rent.

Labour are committed to abolishing/reforming business rates, but in an unspecified way.

We’ve suggested abolishing business rates, council tax and stamp duty – all dysfunctional taxes – and replacing them with a modern land value tax.

What should the Government do?

The Sunak Government ran a consultation last year on business rates avoidance. The 2024 Spring Budget announced three outcomes:

- The Finance Act made box-shifting a bit harder, by requiring premises to be reoccupied for 13 weeks rather than six weeks.

- The Government said it would consult on extending the general anti-abuse rule (GAAR) to business rates.

- There would be communications to warn landowners off cowboy “mitigation” firms.

This doesn’t go far enough.

The Hurstwood judgment should end all the avoidance schemes, but experience suggests that the avoidance firms will continue to flog schemes, take their 20% fees, and then disappear when – years later – the courts strike them down.

The Government should do three things.

First, drag business rates into the 21st century, and make sure all modern anti-tax avoidance rules apply to business rates. That means:

- Introduce a targeted anti-avoidance rule (“TAAR”) for business rates. We see TAARs in most modern tax rules, and they work like this: if you do something artificial which has the sole or main benefit of reducing or eliminating your business rate liability, then it has no tax effect. Scotland has already done this; the rest of the UK should follow their lead.

- Business rates should be covered by DOTAS, the rules that require tax avoidance schemes to be disclosed to HMRC.

Second, and more controversially, consider fixing the administrative problems that led to ten years of stupid avoidance schemes:

- Everyone involved will hate this proposal; but Government should give serious consideration to requiring all non-valuation business rates litigation to be delegated to HMRC. Or, if that’s too unpopular, or administratively difficult, require HMRC to be consulted on business rates appeals involving points of law.

- Another unpopular proposal: the Government should consider a new right of appeal to tax tribunals for non-valuation business rate disputes. Tax tribunals are far better placed to hear what are in reality tax disputes. The risk would be a large increase in poor quality appeals, taking up both tribunal and local authority time – one way to avoid that would be to charge higher fees for business rate tribunal appeals.

- And: local authorities, when you’re dealing with tax avoidance, please hire lawyers who have expertise in tax avoidance.12

Finally, none of these technical measures will deter cowboys like the snail promoter:

So the Government should crack down on promoters of hopeless schemes – business rates as well as other tax avoidance schemes.

- Make failure to comply with DOTAS a criminal offence.

- Make it a criminal offence to promote a scheme or tax position which is so unreasonable no reasonable adviser would think that it works.

- And impose tax-geared penalties on advisers, and their directors/shareholders, when they promote a scheme or tax position that is so unreasonable no reasonable adviser would think that it works.

Business rates need to grow up and be treated like other taxes. And the Government should empower HMRC to go after promoters, not the taxpayers they exploit.

Rachel Reeves vs the snails shouldn’t be a close fight.

Many thanks to W, Faisel Sadiq⚠️, Chris Grose, K and F for their business rates expertise.

Image by FLUX.1 schnell “A photo of a large snail crawling on a desk. The desk has the word “tax” written on it in chalk.”

Footnotes

Now thirteen – see below ↩︎

Six months for industrial and warehouse properties. ↩︎

That is how the court spelt it. Draw your own conclusions. ↩︎

Until Hurstwood – see below ↩︎

Meaning: not me. I am a tax avoidance expert but not a business rates specialist, and this article leans heavily on people who are business rates specialists ↩︎

Their failures have been in failing to challenge schemes early enough). ↩︎

See para 76 of Principled: “[The Ramsay doctrine] is not relied on in the present case and [it is something] which I will not attempt, at my peril, to paraphrase.” ↩︎

Most business rates disputes are around the value of the property and these go to the Valuation Tribunal; but there is no route for appealing technical business rates points other than judicial review ↩︎

Para 117 of Principled suggests the judge didn’t understand Ramsay at all – he said “The cases on sham transactions, those founded on the Ramsay principle, and those founded on lifting of the corporate veil, do not provide the answer either. There is no question here but that the transactions are genuine and produce the legal results for which, by the wording of the documents, they provide.”. That is not the test in Ramsay – the genuineness of the transactions and the absence of sham does not prevent it applying. The judge should have required the parties to present arguments on Ramsay and other common law anti-avoidance caselaw. ↩︎

Although, in fairness, the not tax lawyers did occasionally beat the tax lawyers, although an appeal is pending. Many thanks to H (a tax lawyer) for bringing this to my attention just after publication. ↩︎

The Hurstwood judgment came just a few weeks after Public Health England, which must be regarded as wrongly decided. ↩︎

I accept no fee-paying work and have no interest in any law/accounting firm, so I can say this without a conflict of interest. ↩︎

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Tax barristers and fraud: how the Bar responded to our allegations

Rogue barristers are enabling a billion pound tax fraud – and the Bar won’t act

Samuel Leeds: the “property guru” and his bogus tax loopholes

Leave a Reply