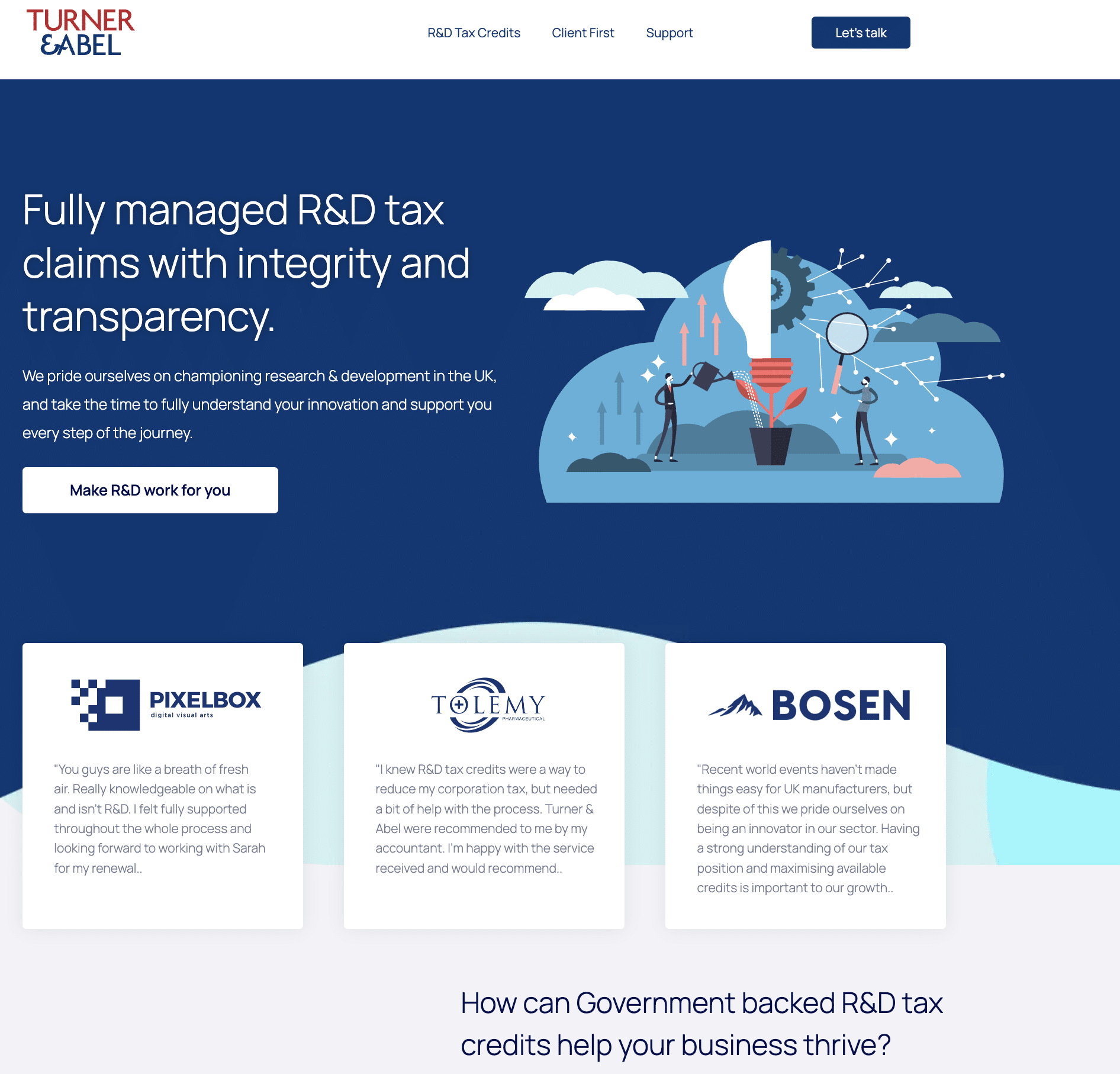

The company was created in July 2024.1 But fair enough – people start new firms all the time.

The website lists no staff. That’s very odd for an accounting firm – it’s a business where reputation and client relationships are everything. Firms often start with barebones websites, but the website hasn’t been updated since it was created in July.

Despite the “let’s talk” button, there’s no phone number.

The Turner & Abel website says “You’re paying for qualified finanical (sic) and legal experts to build the best possible case for your innovation”. We can’t identify any qualified legal or financial professionals working for the firm.

In fact we can’t identify any staff at all. No staff are visible on LinkedIn. Someone gave Turner & Abel a LinkedIn account, but didn’t do anything with it. Zero followers. Zero employees. No text. That’s not how people launching a new firm normally behave.

The website has three testimonals, from Pixelbox, Tolemy Pharmaceutical and Bosen. We can find no evidence any of these companies exists. There is a Ptolemy Pharmaceutical and a Tolemy Bio, but they have different logos (and of course slightly different names). There is no manufacturing company called “Bosen” (there’s a Bosen Ltd, but it’s a mail order company). Pixelbox also doesn’t appear to exist, except in Wisconsin.

The three companies’ logos are also curious. The Pixelbox logo is taken from a stock image library – and, astonishingly, the name also comes from the stock image. The Tolemy logo comes from an image stock library. The Bosen graphic is in a few places on the internet, e.g. this blog. All three logos are all in the same colour.2Reverse images searches don’t find the three logos anywhere else on the internet.

The privacy page is unfinished, with template “suggested text” left in place throughout.

It’s not just coincidence. The website code shows that Turner & Abel has the same webmaster as Green Jellyfish’s affiliate, Kirby & Haslam.3

And we’ve heard the full story from sources at Green Jellyfish. The company made hundreds of fake R&D tax relief refund claims, claiming thousands of pounds for businesses that didn’t actually do R&D. At some point HMRC identified this, and started blocking refunds where Green Jellyfish was the agent.

So the answer was to create Turner & Abel and use it to make the claim. That’s what Turner & Abel did, and perhaps still does.

Who owns Turner & Abel?

On paper, the company is owned and run by Matthew Woolham. But we understand he’s just a junior sales manager who doesn’t make any business decisions. People should be more careful before they agree to become a company director, but in the circumstances of this group, Woolham’s ownership of a fraudulent company doesn’t necessarily make him a fraudster.

Green Jellyfish and its associates appear to intentionally hide the true ownership of their companies. That’s a criminal offence – but the individuals behind these companies (particularly Scott Herd, Daniel Robinson and Steve Christophi) probably have more serious problems than this right now.

Coleman Clarke’s website is similar to Turner & Abel’s, and similarly suspicious. Again the website illegally doesn’t provide the registered addressl it doesn’t even provide the legal name of the entity. However the registered address at Companies House gives the game away. Again the owner has no obvious connection to Green Jellyfish.

Clearview has been extensively used by Green Jellyfish and its affiliates but is hard to spot. The registered address is different, and there’s another owner with no obvious connection to Green Jellyfish. The company appears to have undertaken legitimate business; but more recently it’s been used as a “name” by Green Jellyfish staff, for making calls to clients, and for submitting claims to HMRC.

Comments are now closed for legal reasons. Our apologies.

The Turner & Abel users.json file shows that the Turner & Abel has the gravatar hash 18f89a4653223cd15cfcde8eea0c3cb7. The webmaster of Kirby & Haslam has the same gravatar hash. ↩︎

We frequently receive tip-offs from accountants and lawyers who’ve seen firms promoting dubious tax schemes.

This often requires a large amount of analysis from us to work out exactly what’s going on, and what the true tax consequence is.

But sometimes it’s obvious that what’s being proposed is wildly improper, even fraudulent. We’re going to start publishing cases like this as “tax scam of the day” – documents and links plus a short explanation of why what’s proposed is a scam.

We hope that this helps warn potential clients off dangerous scams, and prompts HMRC and other authorities to be more proactive identifying and closing down cowboy tax advisers.

What’s the claim?

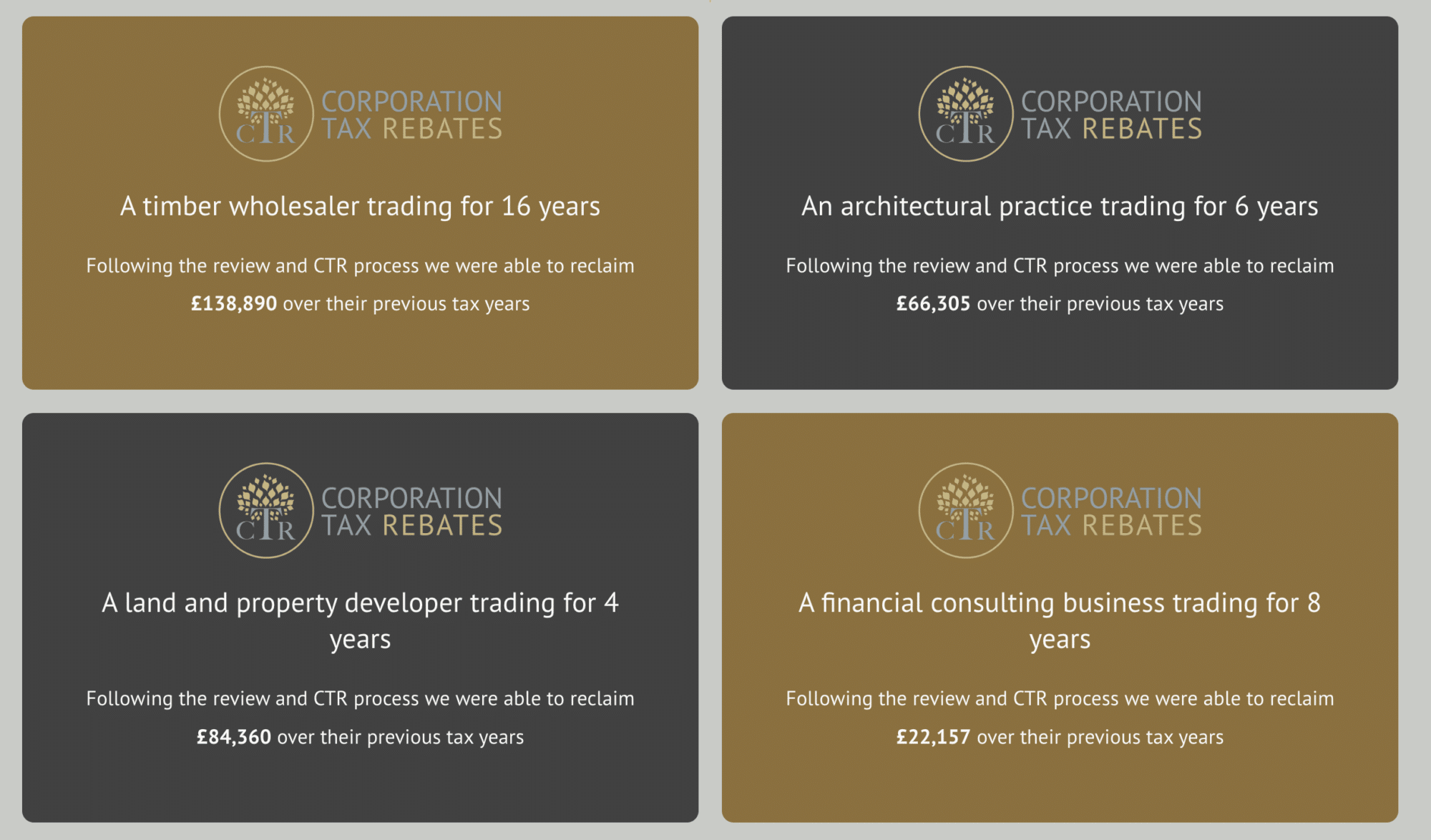

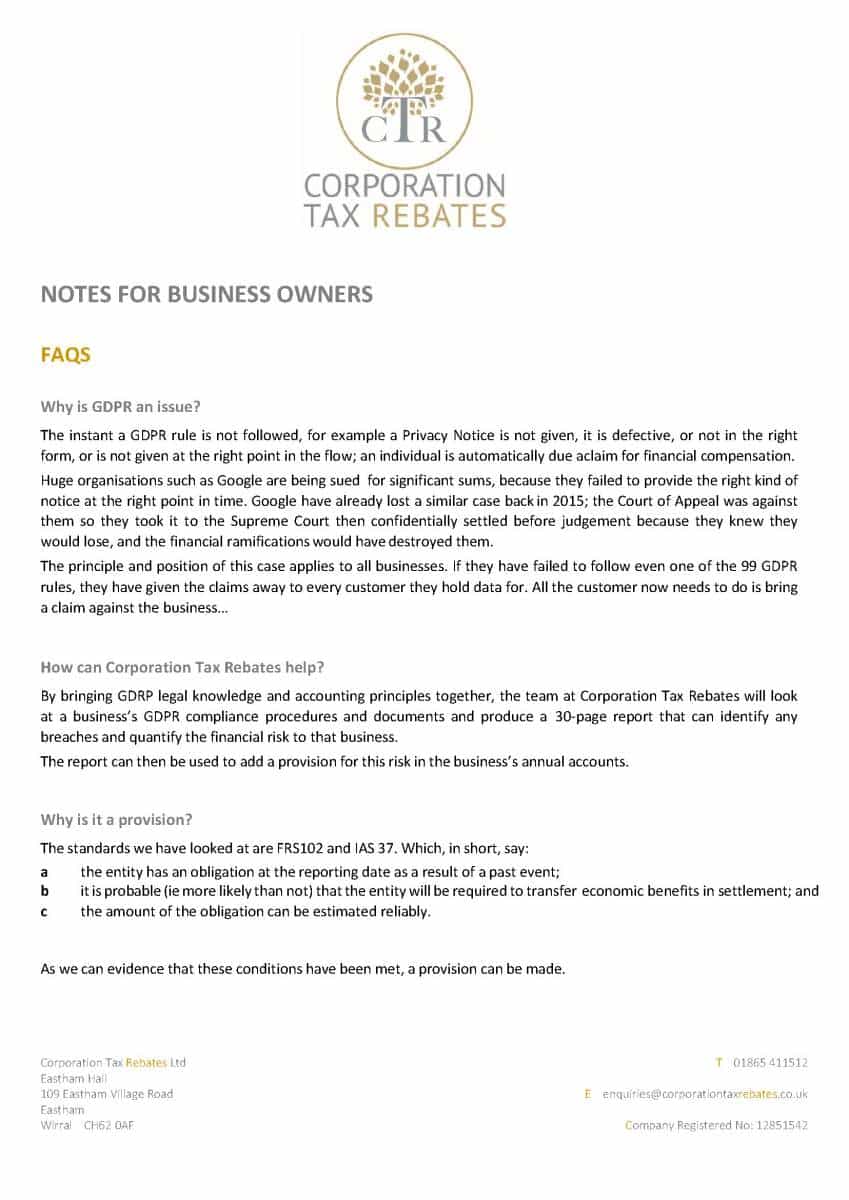

Corporation Tax Rebates’s website says they’re the “UK’s First Corporation Tax Recovery Service Based on Data Risk Compliance”. The pitch is that GDPR can lead to large claims against businesses, so accounting rules permit companies to make large provisions against future liabilities, resulting in tax rebates.

If Corporation Tax Rebates Ltd is the “first” company offering this service, that’s for the very good reason1 that you can’t recover corporation tax based on vague thoughts that you might have to pay GDPR fines/damages at some point in the future. We explained why here but, in short, the fines/damages have to be probable and quantifiable, and for almost all small businesses this won’t be the case.

We can see no proper basis for timber wholesalers, architects, land developers or financial consulting business to have six figure provisions for GDPR damages. The obvious way to test this: how many companies in these sectors have had six figure damages awards against them? The answer is: hardly any. Civil damages awards are rare and small.

The danger for Corporation Tax Rebates’ clients is that this scam will appear to work. If you amend your corporation tax return then you may just get a refund automatically (although even this isn’t straightforward – see Richard Thomas’ comment below).

If HMRC become aware that a company’s doing this, we are confident they would open an enquiry, and the consequences for the company are likely to be bad. Any HMRC enquiry could come up to a year after the refund scheme… and, if it all goes wrong, good luck recovering your fee from Corporation Tax Rebates.

The documentation

There are many websites pushing GDPR tax credits, but most appear highly amateurish, and our suspicion is that they’re just low-level scams. Corporation Tax Rebates Ltd is different. The company and its introducers send out glossy publicity material that goes into some detail.

Ian Andrew Sinclair-Ford is listed as the “person with significant control” of the company 3 and the document metadata shows him as the author of the “confidential briefing note”. He gives his profession as “solicitor”.

We believe anyone with legal, tax or accounting training should know this scheme is improper. We therefore believe it should be investigated as criminal tax fraud, not as tax avoidance. We have reported Sinclair-Ford to the SRA

Many thanks to M for the original tip, and to Trevor Fenton for sending us the documents and looking into the Companies House materials.

We note that the documents are asserted to be confidential. They are not; they were sent to our source without any prior agreement of confidentiality, pre-existing business relationship or any other circumstances under which it is reasonable to expect a duty of confidence to arise. Even if they were confidential, there is a public interest in disclosure, and the iniquity rule means that there is never confidentiality in a fraud. ↩︎

Although it’s not clear that’s correct – each of the three holds 1/3 of the company. There are other oddities in the Companies House filings, with share capital of £105 but only one £1 share ever alloted/issued. ↩︎

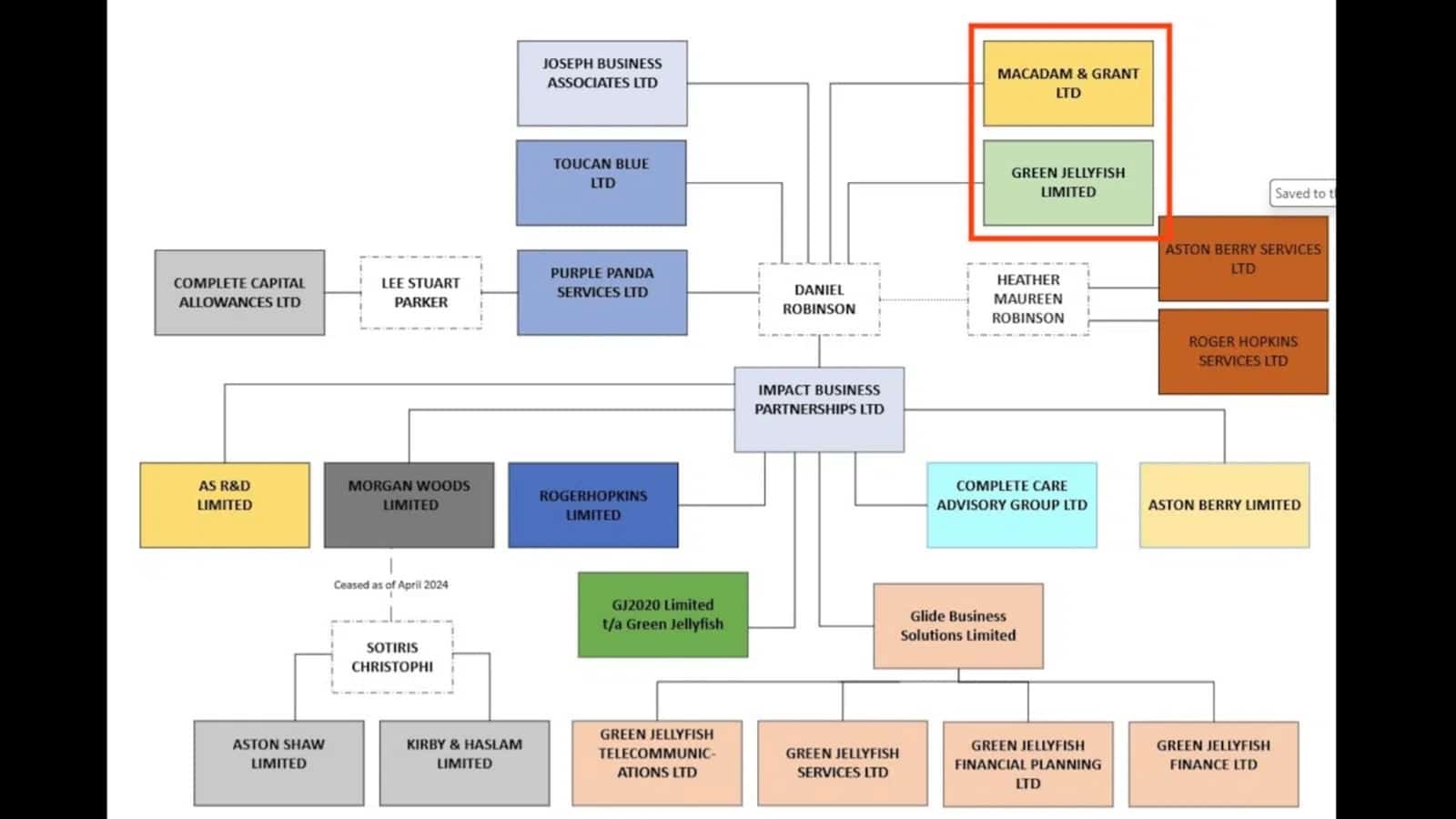

R&D tax fraud outfit Green Jellyfish is part of a complex group of companies. Two of those companies, Macadam & Grant and Toucan Blue, promote “GDPR tax credits”. There is no such thing. It’s plain tax fraud.

We wrote last year about firms advertising that they’d help businesses claim “GDPR tax relief”.

The idea is that the Information Commissioner is very scary, and can slap large fines on businesses who breach GDPR, you might suffer massive damages. So it’s only prudent to amend your accounts for last year to put a reserve in place – reducing your profits and resulting in a tax refund.

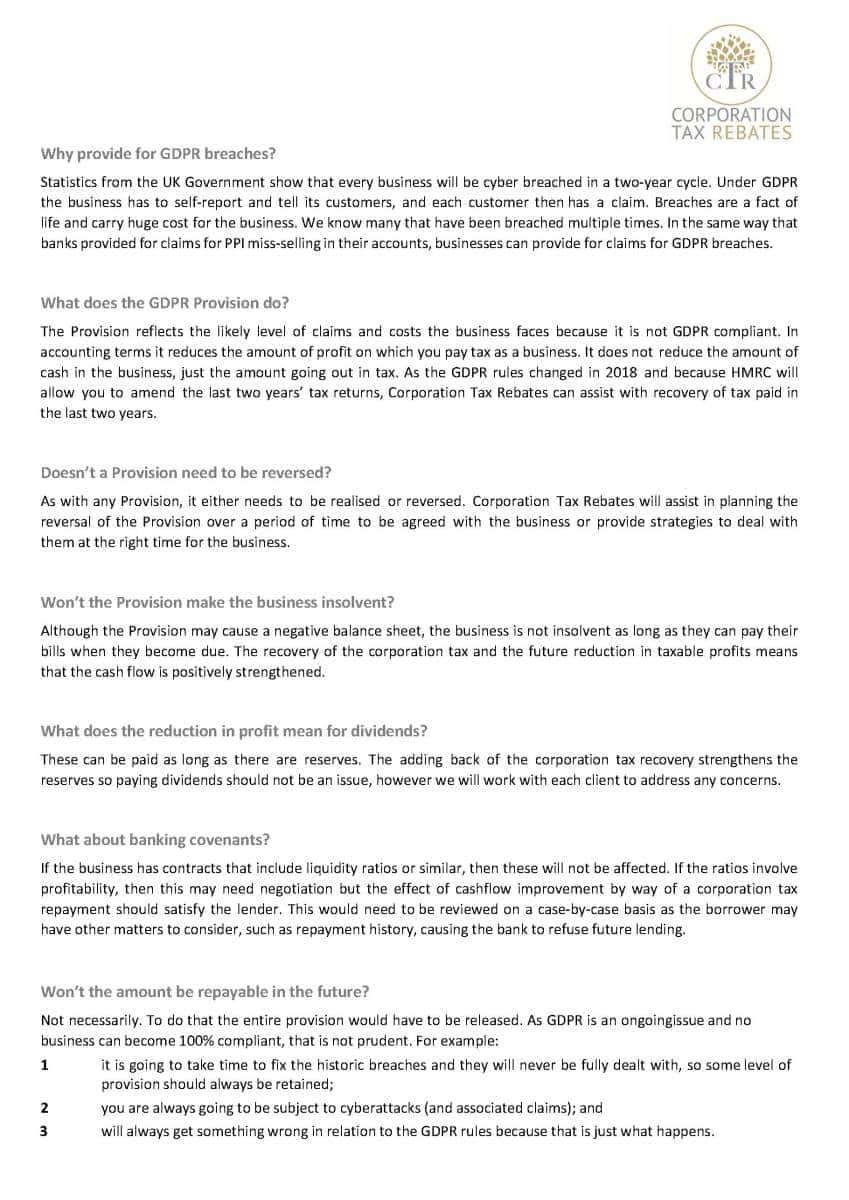

But that’s wrong in three different ways. Only on rare occasions would accounting principles actually permit such a reserve – the liability has to be “probable”. Very few businesses ever suffer material fines or damages as a result of data privacy breaches.1 Civil damages awards are rare and usually small. The really big liabilities would be fines or punitive damages – but (aside from being unlikely) they’re not tax-deductible.23 And a reserve isn’t a “credit” – a credit is forever, but a reserve will be reversed over time.

A junior accountant would spot these issues in five minutes. In fact, one did – Yisroel Sulzbacher originally brought this to our attention.

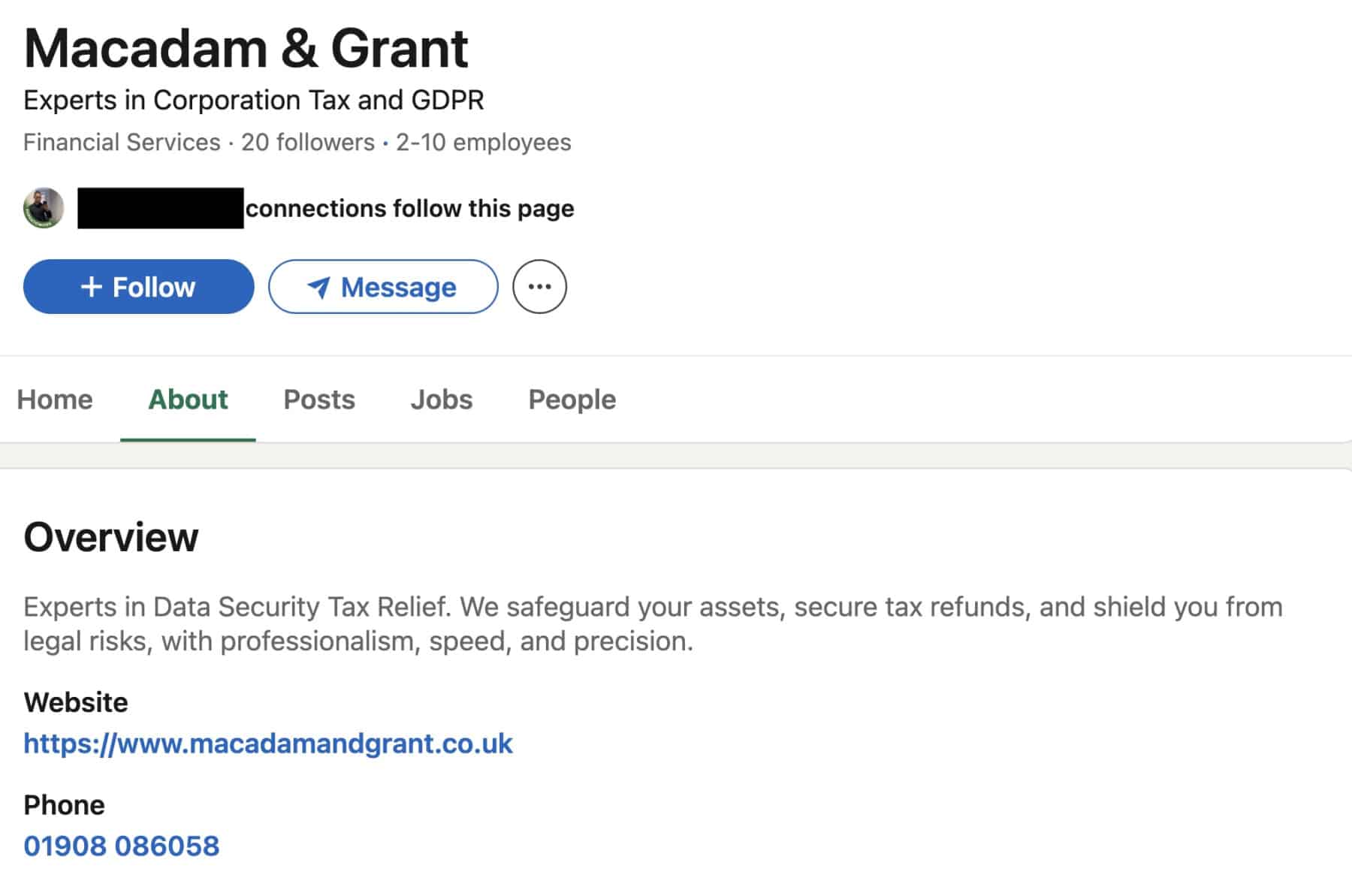

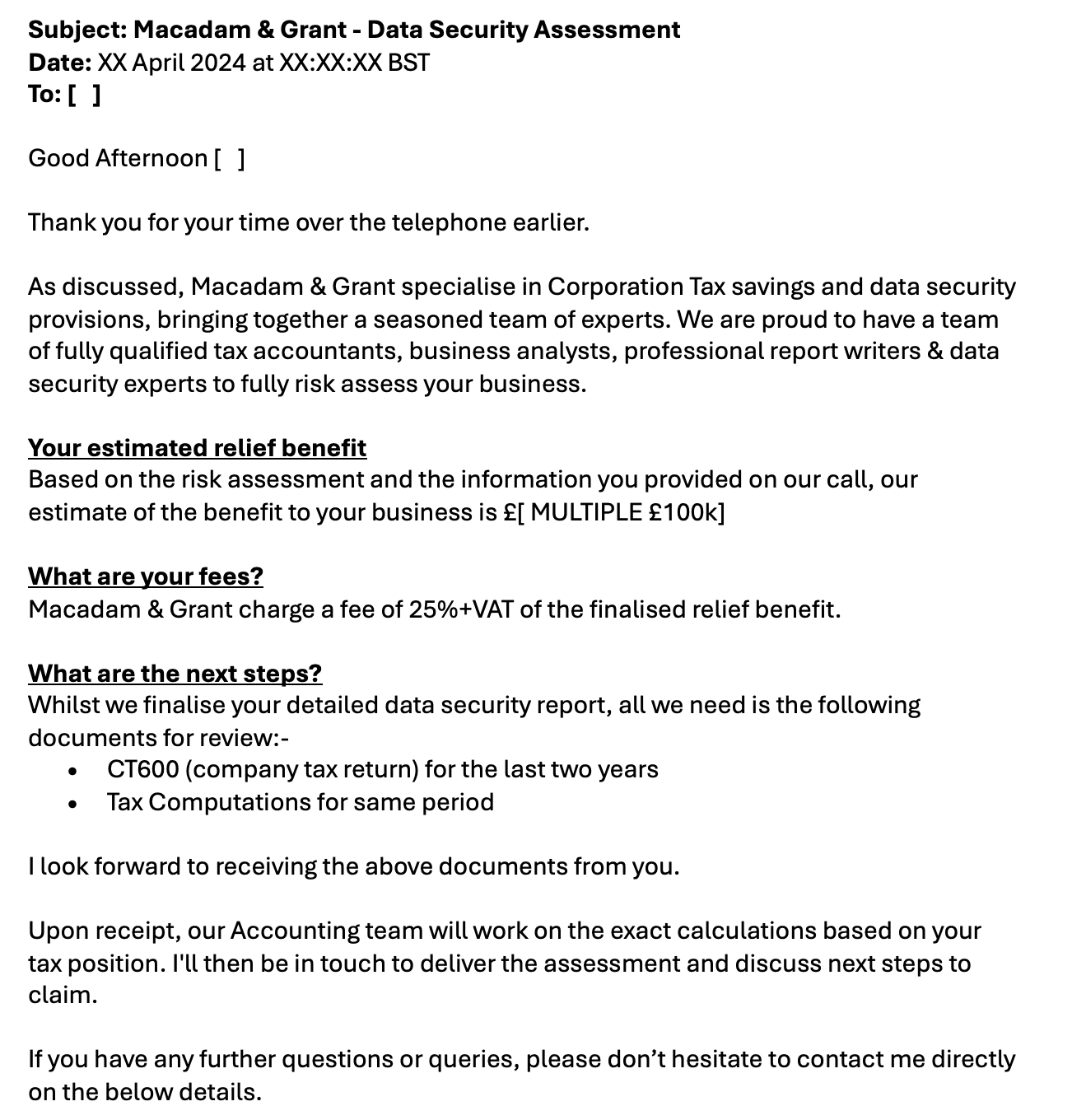

One of the companies promoting the GDPR tax relief scam was Macadam & Grant:5

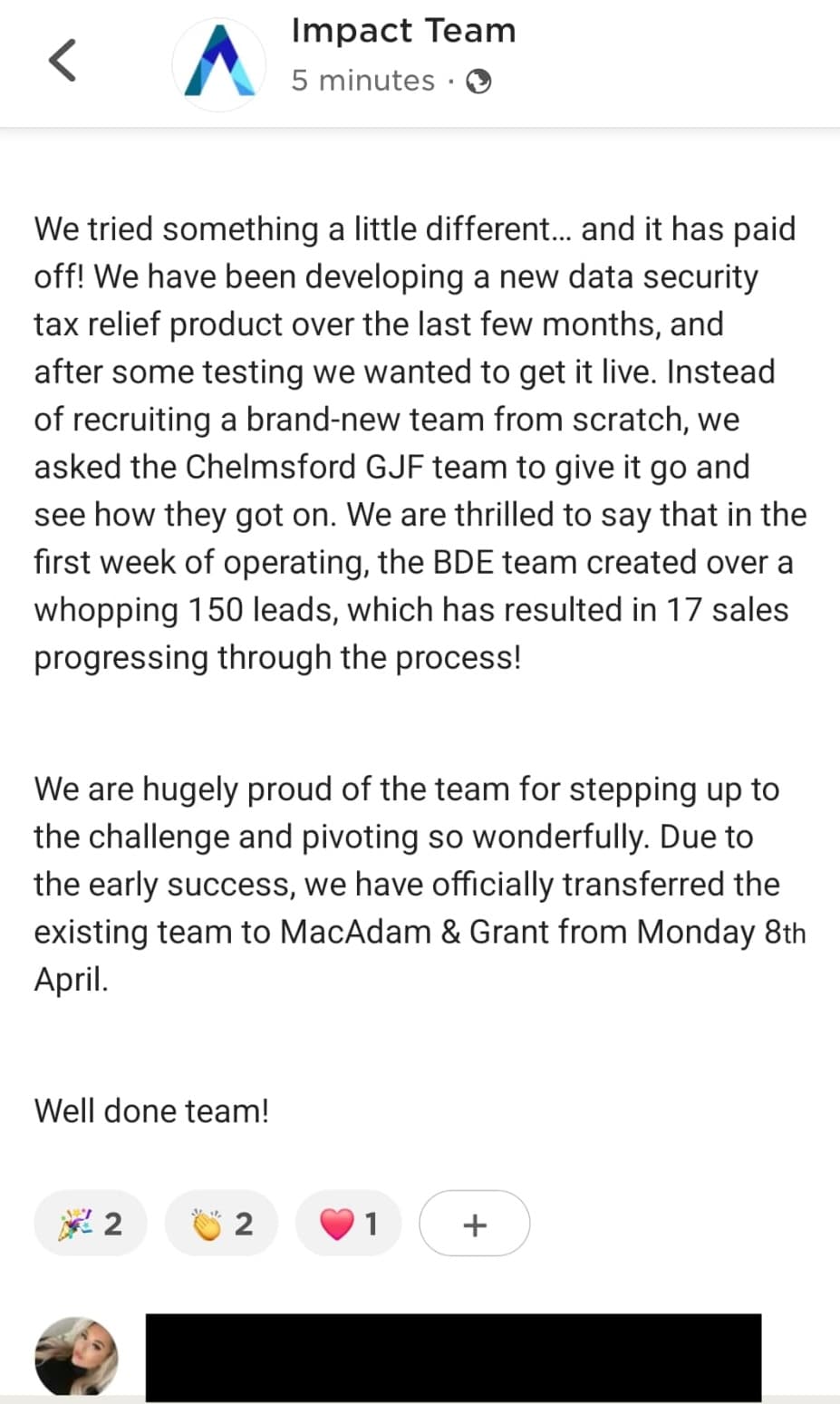

The launch of this product was seen as a big success by those running this business:6

And here’s Daniel Robinson, CEO of the Impact Business Partnership Group7 that owns Green Jellyfish and Macadam & Grant. Robinson says (at 1:40 in the video): “we also tested Macadam & Grant, which is our GDPR tax relief scheme business, which we’re currently taking to market at full scale during Q1 [2024]”:8

It’s jarring to see a bland corporate quarterly results presentation for a fraudulent business. Of course it’s possible that Robinson doesn’t understand that “GDPR tax relief” doesn’t exist. However, we know that employees raised concerns about this “business” with the board and were brushed aside.9 So it seems to us that, at the least, Robinson and the others were reckless

The hard sell

Macadam & Grant operated in exactly the same way as Green Jellyfish. Cold-calls from the BDEs (“business development executives”) and then follow-up emails promising massive tax refunds.

Here’s an example email from Macadam & Grant, forward to us by an outraged tax adviser:10

Like Green Jellyfish’s R&D claims, the figures bear no relation to reality. The idea any company, other than the very largest, faces six figure GDPR fines/damages is laughable. But this is worse than Green Jellyfish – at least R&D tax relief is real. Macadam & Grant was promoting a tax relief that doesn’t exist. This email was fraudulent on its face.

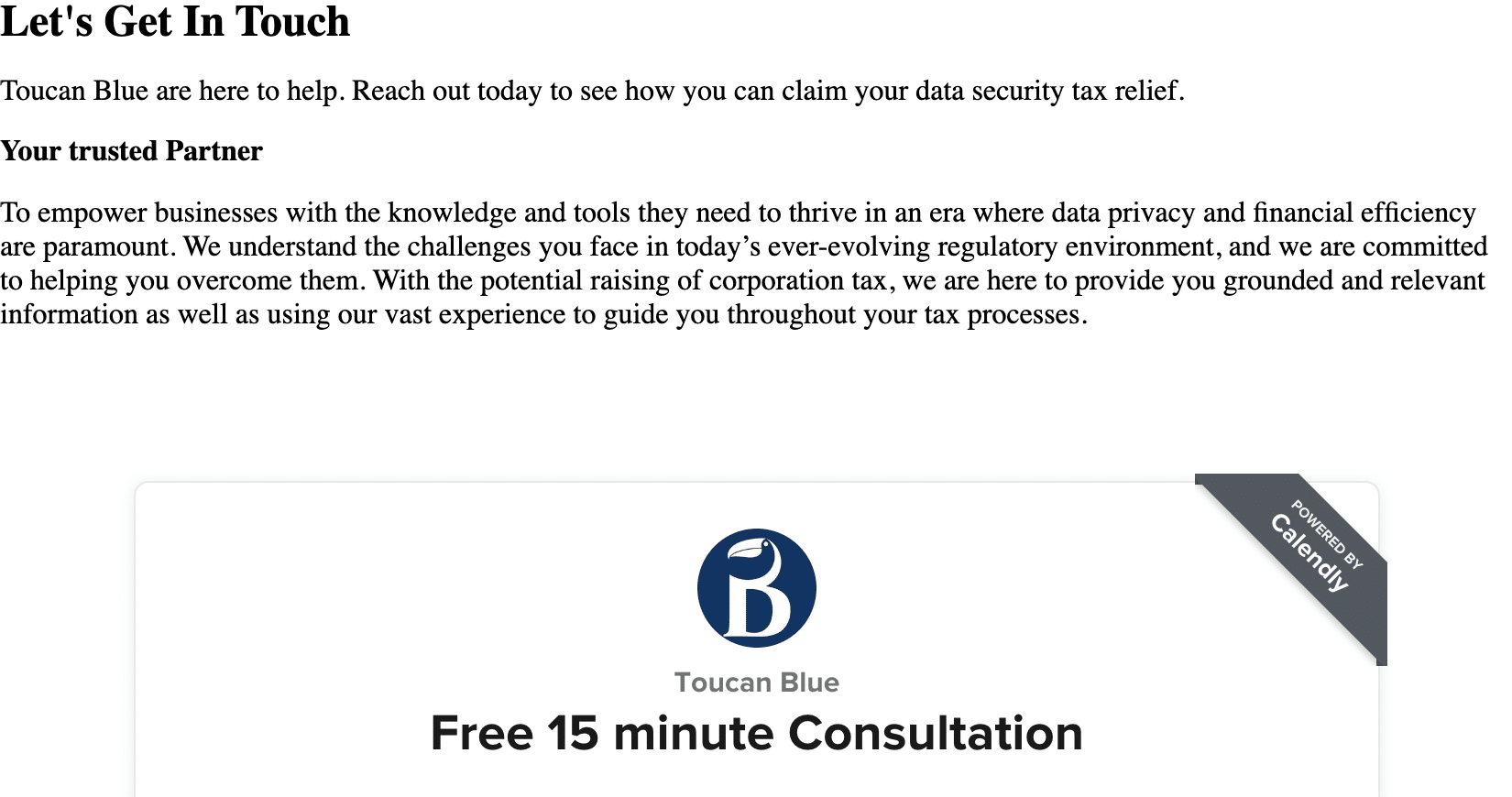

Here’s a promotional video posted by Toucan Blue on LinkedIn. They avoid the term “GDPR tax credits” and talk about “data security relief”, but it’s clearly the same fraudulent product:

And a website:

Toucan Blue appears to have soldother tax products – we are highly suspicious of how genuine those products are.

Toucan Blue is registered to the same address as Macadam & Grant and the other Impact/Green Jellyfish companies. It was owned by Daniel Robinson until June this year. Between then and 27 August 2024, the sole director, and sole “person with significant control”11 was Trudi Duncombe. Ms Duncombe ceased to be a director on 27 August, two days after we published this article, but is still listed as a PSC.

Who else is flogging this scam?

There are other companies flogging this. We believe all are fraudulent, including:

However there are significantly fewer people pushing this than when we first wrote on the subject – many of the companies we listed then have taken down or amended their websites.13

Green Jellyfish’s response

We wrote to Daniel Robinson on 22 August, and said that we believed these companies’ GDPR relief claims were fraudulent.

We received no substantive response, but the Toucan Blue website was taken offline shortly afterwards.

The Impact Group

Most R&D tax fraud is carried out by individuals or small companies. It’s very unusual to see a reasonably sophisticated group of companies (the Impact Group) involved in something like this. To see them involved in another unrelated fraud suggests a systemic problem with the group.

We hope there is a criminal investigation of all involved.

Many thanks to Paul Rosser for the chart, to M for the tip-off about Macadam & Grant, and to the current and former Impact Group employees who’ve bravely spoken to us.

And thanks to Yisroel Sulzbacher for the original tip about the non-existent relief.

Comments are now closed for legal reasons. Our apologies.

Footnotes

FRS 102 says a company can only recognise a provision if the liability is “probable” and can be “estimated reliably” ↩︎

A GDPR fine or punitive damages claim is non-deductible for corporation tax purposes, even if it reached by way of settlement. Damages paid out in a civil claim that compensate for actual loss (as opposed to punitive damages) may be deductible, but such claims are unlikely (and the figures would for most companies be small). ↩︎

Even if you manage to book a reserve and get a deduction, you still fail, because reserves created primarily for a tax benefit aren’t deductible anyway (and neither are the adviser’s fees). A tax tribunal recently used that principle to deny a business a tax benefit from a reserve created for unfunded pension liabilities – which were much more real than these fictional GDPR liabilities. ↩︎

We’d missed the Forbes Dawson and Justin Bryant pieces when we wrote our first article; full credit to them for spotting the issue. ↩︎

This is from an Impact Group internal communication sent to us by a source. ↩︎

There are many companies/groups called “Impact” – please be wary about drawing conclusions about any similarly named company, unless it operates from Rose Lane in Norwich ↩︎

Video kindly provided to us by a source, and authenticity confirmed with other sources. ↩︎

There appears to have been significantly more internal resistance to their GDPR tax relief business than to their R&D tax relief business. We expect the reason is that some technical knowledge is required to know that their R&D tax relief business was fraudulent; however one Google search reveals the problem with GDPR tax relief. ↩︎

We have redacted identifying information, but none of the text is changed. This was sent to us before we started investigating Green Jellyfish, and we only belatedly made the connection. ↩︎

It’s unclear why, as no Companies House documents show Ms Duncombe holding any shares; possibly there is a trust arrangement behind the scenes? ↩︎

Possibly defunct; the website’s security certificate is out of date. Not to be confused with the reputable and unrelated Osborn Knight Solicitors↩︎

None responded to us last year when we wrote asking how they justified advertising a relief that did not exist. We’ve written to the four above. We found a few others, but the websites appeared to be broken/abandoned – the above four appear live. ↩︎

The UK loses £1bn each year to fraudulent claims for research and development (R&D) tax relief. We revealed last week that one of the largest firms in the market, Green Jellyfish (and its associated firm Kirby & Haslam), made fraudulent claims. We can now reveal in detail how the fraud worked. We believe they’re responsible for over £100m of fraudulent claims.

Unqualified sales people cold-called businesses with no R&D (like carpenters and care homes), and promised them R&D relief would be available. “Technical writers” – none of whom had any relevant experience or qualifications, and many of whom had creative writing degrees – wrote reports justifying the relief. The employees were given briefings with examples of supposedly valid claims. But those briefings were false – none of the example projects actually qualified.

We are today publishing the details of how Green Jellyfish, Kirby & Haslam and other “Impact Group” companies worked from the inside, together with their internal briefing documents.

Green Jellyfish promised their clients they had a team of expert R&D specialists.

This is from a promotion sent by Green Jellyfish to care homes in 2022, talking about their team of “Tax Specialists”:

This is from their website and LinkedIn pages (as of 23 August 2024) – “we are the R&D tax experts”, a “team of specialists” and “a team of Research and Development Tax Specialists”:

And this email to a client (in 2022) talked about “an FCA regulated team of experienced experts in this field”.

The reality – zero expertise

We have not found a single Green Jellyfish or Kirby & Haslam employee with any background in tax, accounting, law, science, or technology.1

We identified ten Green Jellyfish technical writers using open source materials, and metadata from our dossier of the company’s R&D claims. In most cases they were hired straight from university. In other cases they had unrelated previous experience.

The cold-calls to clients, in which clients are assured that R&D tax relief will be available, came from “business development executives” (BDEs). Successful leads were passed to “business development managers” (BDMs) who would have telephone meetings with the clients.

This was a large team with high turnover- we’ve identified over 50 individuals who worked in this role for Green Jellyfish from 2021. They typically had a sales background, but none had any expertise in any legal, accounting, tax or technical area:3

So this was a team with zero expertise. Clients were lied to.

The employees’ story

We have been speaking to current and former Green Jellyfish employees. We have verified their employment from LinkedIn, historic emails, and document metadata.

Their stories are consistent, and paint a picture of a business that worked like this:

The sales teams

The business development executives (BDEs) cold-called clients and sent follow-up emails which (without exception, as far as we’re aware) said the BDE was confident a claim could be made.

They would target different sectors on different days, obtaining company details from Companies House and then looking up phone numbers on Google. For example: two days electricians, then plumbers, then bricklayers, groundworkers, pubs etc. The one thing these sectors had in common was that they were highly unlikely to qualify for R&D tax relief. Two sources have told us they believe that was intentional: it meant Green Jellyfish wouldn’t be competing with other advisers.

Potential leads were passed to business development managers (BDMs) for follow-up calls. There were about 15-20 BDEs at any one time, and 10-15 BDMs. As we note above, none of the BDEs or BDMs had any technical background or experience.

The BDMs asked clients about their business in very general terms, and were supposed to identify “innovative projects”. The BDMs were given lists of example qualifying R&D expenditure (see below), but in practice BDMs almost always said R&D relief was available.4

The BDEs and BDMs saw this purely as a sales job, and had no understanding of the legal requirements, or the consequences of wrongly claiming tax relief.

Several BDMs/BDEs have told us they were given the initial explanation that almost everything qualified for R&D tax relief if you worded the claim correctly.

BDEs and BDMs were under huge pressure to meet sales targets. There was rapid turnover of the BDE and BDM teams (unusually high even by the standards of junior sales jobs).

Some of the BDMs relied heavily on ChatGPT to write their notes.

That was particularly the case when, later on, BDMs were hired in the Philippines and South Africa – they heavily (one source thought “exclusively”) wrote to the technical report team using ChatGPT.

The numbers

The BDMs would put numbers together for the tax relief claims based on the clients’ accounts and corporation tax returns.

Sometimes this followed a discussion about potential R&D projects. Often it didn’t.

We have seen multiple emails from BDMs to clients saying that they would establish the qualifying R&D expenses by looking through the company’s accounts and tax returns. Qualifying R&D expenses cannot be calculated in this way – individual projects must be identified.

Several sources5 have told us that the BDM team would have “industry standards” of the amount they could claim for each sector – for example 20% for care homes. Later they would adjust percentages slightly so the numbers didn’t look too round, for example 20.21%. Later still, different percentages were used for different categories of expense. If our sources are correct, this would be blatant fraud. We would, however, caution that (unlike most of the other information provided to us by our sources) we have no documentary evidence to directly support this claim, and our sources could be mistaken or exaggerating. However we have noted many of the claims in our dossier are almost-round percentages of the company’s expenses.

Our sources have different views on the total volume of claims made by Green Jellyfish, but they all agree the total must be more than £100m. We believe that’s consistent with Green Jellyfish’s accounts. 6

HMRC are now very alert to refund claims. Several sources told us Green Jellyfish had been “blacklisted” by HMRC, and no refunds would be made when Green Jellyfish was the agent. One solution was to use affiliated entities. Another was to find businesses who were about to submit corporation tax returns, and make last minute changes to add large amounts of R&D tax relief – HMRC would then have no idea any R&D agent had been involved. (We would caution accountants to be alert to this.)

The technical team

Sometimes a BDM sent a note of their call with the client to the team of “technical writers” to prepare a report.

A report was required after August 2023, when HMRC tightened claim procedures. Before that, the technical team were only involved in some cases (we believe, but aren’t sure, it’s where there was a more realistic identifiable R&D project). More often, the claims were like Sophie’s, where a claim was submitted without a report (but a report produced much later if there was an HMRC enquiry).

The technical writers were formally employed by Kirby & Haslam, not Green Jellyfish, but in practice the two companies operated as one business.

As we note above, most of the “technical writers” were hired straight out of university with no prior experience. Many had English literature and creative writing degrees; a few had other Arts degrees. None had any prior R&D, legal, accounting or tax experience.

Two of the “technical writers” were referred to as “R&D Tax Specialists” by BDEs on client calls within a few weeks of starting work for Green Jellyfish.

The technical writers realised quite quickly that there was nobody around with any tax qualifications. The BDMs and BDEs sometimes did not realise this, and one we spoke to appears to have genuinely believed that the technical writers were experts.

The reports

We have seen images of notes sent by BDMs to the technical writers. We aren’t publishing them because of the risk our sources could be identified – but we would describe the text as poorly written half-descriptions of a standard care home business. We believe we can link one to a case where a six figure sum was claimed from HMRC (and later had to be refunded, with penalties).

It was made very difficult for the technical writers to refuse to write reports based on the BDM’s notes. If they could not write a report, the claim would go to HMRC anyway, pre-Aug 2023 (after that, the rules were tightened and additional information specifying the R&D had to be provided to HMRC).

The technical writers were dissuaded from telling BDMs that claims did not qualify for tax relief – this was considered “aggressive language”.

Some of the BDMs referred to the technical writers as the “sales prevention department”.

We have now seen many reports prepared by the technical writing team. We have not seen one which actually meets the conditions for R&D tax relief.

The group structure

The business was run day-to-day by Daniel Robinson and Scott Herd, with Steve Christophi known to be involved at board level, but rarely seen.

Several of our sources commented on the obscure group structure, with the BDMs in a different company from the technical writers. They thought this to make it easier for the technical writers and BDMs to blame each other for poor quality claims.7

There was also a “legal team” made up of recent law graduates. They were called “paralegals” but this was not accurate – the term “paralegal” usually means someone with legal training working under the supervision of a qualified lawyer. So far as we are aware, there were no qualified solicitors or barristers working for Green Jellyfish or any of the associated entities.8 The paralegal team got involved when HMRC opened an enquiry into a Green Jellyfish claim. We have also seen a number of legal letters and emails drafted by the “paralegal” team. The letters rely heavily on Google and show signs of being written by ChatGPT or a similar LLM.

The junior personnel working for Green Jellyfish had an appalling experience in a very hostile environment. We don’t see them as morally or legally responsible for the false R&D tax claims. At least two made anonymous reports to HMRC. The blame lies with those who hired staff with no experience and fed them false information, knowing that clients would be misled.

The fake training materials

Green Jellyfish gave the business development and technical writing teams examples of what they said were valid R&D relief claims; these were sometimes also given to clients to “help them identify” qualifying projects.

Here’s Green Jellyfish’s list of examples of R&D projects run by care homes (PDF here):

As a general proposition, the prospect of any care home having qualifying R&D relief is highly unlikely. A care home and its staff may be very innovative in how they plan and deliver care, but it is hard to see how they will ever look for “advances in science and technology”.

But, despite this, care homes were a key market for Green Jellyfish. Two of our sources estimated that care homes made up 40% of Green Jellyfish’s business and 25% of the group companies’ business.

In our view it is clear that none of the examples in this list are valid:

Some are not science and technology at all: e.g.: “Manage and control symptoms of dementia through a wide range of interior and exterior designs” and “Management of a specialised outdoor garden design to mitigate common dementia symptoms”

Others are just using existing technology, e.g. “new software… installation of sensors… to optimise the delivery of care services and… in particular, the detection of symptoms relating to diabetes, addiction, and dementia”, or “create a data analysis tool that can detect and recognise dementia traits”.

Some of the projects would qualify, but it’s implausible a care home would ever have the expertise, resources or facilities to carry them out. Seeking to “advance the field of clinical neuroscience” or “advance the scientific field of neurology” are realistic objectives for a hospital or laboratory, but not a care home.

Green Jellyfish also gave their staff and clients this document, again focusing on care homes (PDF here):

The summary of the qualification criteria are reasonably accurate. We believe anyone with an accounting, tax, legal or technical background reading these paragraphs will realise immediately that care homes usually won’t undertake “research and development”. But nobody in the business development or technical writing team had that background.

In our opinion the examples are, once more, all clearly invalid:

“Developments in care plans” are not an advance in science and technology. Green Jellyfish seem aware of this, by adding the caveats “if the specific care plan is an advance in science or technology” and “and is not easily deducible by a competent professional within the field”. But we don’t believe any care plan can be an advance in science or technology, and given it’s devised by professionals in the ordinary course of their business, it will be “easy deducible”. The caveats look like someone was trying to cover their back.

“IT software designed by organisation for bespoke needs of clients/ carers”. Software will only in exceptional cases be an “advance in science or technology”.9 Realistically, care homes will use existing platforms and technology with minor modifications.10

“Use of AI for service standardisation, operations, and capture of new symptoms within patients”. We doubt any care home will develop its own AI systems. It is much more likely it uses existing platforms such as OpenAI/chatGPT – and that will not be an “advance in science and technology”.

“Development and implementation of biosensors and trackers in clothing of residents and carers to monitor changes in health”. We very much doubt the care homes are developing biosensors/trackers. They will be buying off-the-shelf products. That is not an advance.

“Technology suppliers in the sector (e.g., Birdie) during COVID-19: e.g. partnering… with NHSX for Techforce19 to build the NHS111 symptom tracker into the Birdie app”. Integrating an existing service into an app is obvious, and not an advance in science or technology.

“Revolutionising technology relating to medicine (trying to mitigate medicine waste)”. It is not plausible a care home has the equipment, resources or staff to “revolutionise technology”.

“Improving or creating technology to address a specific scientific or technological problem within the care sector”. This is so vague as to be meaningless.

“R&D within risk assessments – creating a plan that is able to reduce the potential for harm or risk”. Creating a plan is not a scientific or technical advance.

“Innovation in approaches to Dementia care (or other neurological conditions), especially the use of activities and tools to aid recollection”. Using activities and tools is not a scientific or technological advance.

The more detailed “specific client examples” in the documents are, again, invalid:

Implementing behaviour strategies is not an advance in science and technology. Developing a computer programme is not usually an advance in science and technology (unless e.g. it goes “far beyond routine adaptation of existing technologies“). “Recording a person’s behaviour in real time” sounds routine, and not much like an advance at all.

Video interviews and streamlining recruitment are not advances in science and technology.

Designing gardens for people with dementia is not an advance in science and technology, and a garden designer is not a competent professional in the field of neurology.

Advancing the scientific fields of neurology and neurobiology absolutely could be a scientific advance qualifying for R&D relief, but we are very doubtful any care homes have the resources, expertise or budget for neurology research.

The game is given away by the second bullet point. A highly experienced nurse is providing care; he or she is not making scientific advances, and is not a competent professional in the fields of neurology and neurobiology.

The use of the term “neurobiology” is particularly silly. Neurobiology is the study of nerve cells at the molecular level, requiring a sophisticated laboratory. We expect the author didn’t know what the term meant.

These examples corroborate what we were told by current and former Green Jellyfish employees – that they were instructed that almost everything qualifies for R&D tax relief, provided the claim is worded correctly.

These instructions, and the lists of examples misled Green Jellyfish staff and their clients. We think this was intentional.

Who ran Green Jellyfish?

The different entities involved in the business have a variety of different owners, in some cases changing entity and owners over time. Back in 2023, all were listed as part of the “Impact Group”; today they are more shy about admitting that the entities are linked.

Three names come up again and again when we speak to current and former employees.

Steve Christophi, who owns Kirby & Haslam. He is not listed as a shareholder or director of Green Jellyfish, but he was described as a “stakeholder” in internal communications, and our sources report that he was one of those running it. It is notable that, when Paul Rosser wrote about Green Jellyfish, it was Steve Christophi who went to talk to Paul about it (Christophi’s version) or intimidate him (Paul’s version).

Scott Herd was listed as the “Non-Executive Chair” of the Impact Group in 2022 and 2023, and described as “a crucial board member at one of the leading R&D tax credit firms in the UK”. He was previously a director of the current Green Jellyfish entity.

Others are undoubtedly responsible. Paul Rosser researched a structure diagram which reveals other names; we will be writing more on this soon.

Green Jellyfish’s response.

We asked Green Jellyfish to comment on the documents and the evidence of their unqualified staff and unethical business practices. We also warned Messrs Robinson and Herd that we would be naming them in this article:

Green Jellyfish’s lawyers, Fladgate, are still acting. However, despite the seriousness of the allegations, we received a response from Green Jellyfish rather than from their lawyers. This is surprising given the seriousness of the allegations we are making.

The response complains about our timetable, makes a series of irrelevant claims about Steve Christophi’s peculiar visit to Paul Rosser, demands that we review a recording of that visit (we are unaware a recording exists), and demands “specific, detailed questions and concrete evidence to substantiate [our] claims”. They refuse to respond until we do this.

Our response was as follows:

Evidence of fraud

One explanation is that this was all an accident. That those running Green Jellyfish and its other affiliates were acting in good faith, but completely misunderstood the law. They thought all innovations qualified for R&D Tax relief, hired the wrong staff, created wrong examples, and so forth. It would follow that, whilst they were responsible for a large number of incorrect R&D tax relief applications – they did not know that would be the outcome, and no question of fraud arises.

We find this explanation implausible on its face.

As we have mentioned above, we believe that anybody with any appropriate experience would realise that the guidance provided to the staff was (and Steve Christophi, one of those who run the company, is a chartered accountant).

And even if we (charitably) assume Christophi, Herd and Robinson started out acting in good faith, they surely would have realised something was going on when they started to see HMRC challenge their claims and explain very clearly why the claims were being challenged.

At this point an honest person would stop and ask whether there was something in their procedures which was resulting in so many failed claims.

But there is no sign that this happened. Our sources suggest that things actually got worse, not better, as HMRC tightened up its procedures. Even by the sorry standards of cowboy R&D claims firms, this was extraordinary.

It is therefore our view that those in charge of Green Jellyfish (who we believe were Christophi, Robinson and Herd) knew that false R&D claims were being made, and knew that they were misrepresenting the nature of their team to clients. If they were “dishonest” then this amounts to a fraud on their own clients, and on HMRC.

Dishonesty

Whether Green Jellyfish’s leadership team were actually dishonest is a question for a jury.

The jury would be asked to decide whether their conduct was dishonest by the standards of ordinary decent people (regardless of whether the individuals in question believed at the time they were being dishonest).11 The leading textbook of criminal law and practice, Archbold, says:

“In most cases the jury will need no further direction than the short two-limb test in Barton “(a) what was the defendant’s actual state of knowledge or belief as to the facts and (b) was his conduct dishonest by the standards of ordinary decent people?”

We expect that, presented with the evidence we have published to date, most ordinary decent people would say the behaviour of those running Green Jellyfish was dishonest. However, ultimately that is something for a jury to decide.

In our view there is more than enough evidence to justify a criminal investigation of Green Jellyfish’s leadership team, which we believe includes Christophi, Robinson and Herd.

Thanks above all to the current and former employees of Green Jellyfish for telling us their stories. Given Green Jellyfish’s history of legal and physical intimidation, this involved considerable bravery on their part.

Many thanks to K and T for their R&D tax relief expertise, and to P for additional research. Thanks, as ever, to S for his review and technical suggestions.

Paul Rosser of R&D Consulting reviewed a late draft of this article – Paul deserves full credit for discovering and pursuing this story over the last couple of years.

Two exceptions. First, Steve Christophi, who is a chartered accountant. Christophi was one of those managing the business and perhaps had ultimate ownership of it, but he played no part in day-to-day advice. Second, the web design and IT staff, who had obvious technical ability but played no role in the R&D tax relief claims ↩︎

After the events of the last few days, many Green Jellyfish employees and former employees have removed their profiles from LinkedIn and/or removed Green Jellyfish from their online CVs. We would discourage others from trying to identify junior Green Jellyfish personnel; we don’t think it’s fair to hold them responsible for the misdeeds of the business. ↩︎

“Complete Care Advisory” is another firm associated with Green Jellyfish; it provided services to care homes including false R&D tax relief claims. We do not know if its other services were bona fide or not. ↩︎

Possibly this should say “always”; nobody we spoke to was aware of a case where a client was rejected. The very poor quality of the projects that were identified by the BDMs suggested that few if any were rejected. ↩︎

Current/former employees of Green Jellyfish and its affiliates ↩︎

Because trade debtors are shown as £2.3m at December 2021 and £3m at December 2022. We can conservatively assume clients paid within 90 days, which implies over £25m of fee income, which (given their 20% fee) implies £125m of tax benefit claimed before the business became much harder in August 2023. Update – 27 August: Mark Strafford, of Sedulo Forensic Accountants and his R&D tax colleagues kindly conducted a high level review of these accounts for us, pro bono, and they agree that this is the right ballpark figure. (Although they believe 60 days would be more typical for this kind of business, implying that the true figure of Green Jellyfish claims may be higher than our previous estimate). ↩︎

We are not sure that’s right; the scattered group structure looks more like an attempt to hide the true ownership of the business and segregate liability. But we do not know for sure, and we could easily be wrong. ↩︎

Nor were any of the “paralegals” registered with the (voluntary) Professional Paralegal Register. We see the use of the job title “paralegal” as a cynical way to hire law graduates and hold out the false promise that this is the start of a legal career. ↩︎

See the Get Onbord case where an “impressive” machine learning/AI system created by a tech startup was found to qualify. The judgment says that a “massive amount of new code was written as part of the project, which goes far beyond “routine” adaptation of existing technologies”. ↩︎

One can imagine a scenario where a care home commissioned a tech company to develop a very sophisticated AI system, but we haven’t seen any examples of this in our Green Jellyfish dossier, or heard about any such case from our industry contacts. ↩︎

The subjective element of the test for dishonesty (see Ghosh (1982)) was removed by Ivey [2017] for civil cases, and that decision was confirmed to apply to criminal cases in Barton [2020]. The fact that a defendant might plead he or she was acting in line with what others in the sector were doing, and therefore did not believe it to be dishonest is no longer relevant if the jury finds they knew what they were doing and it was objectively dishonest. ↩︎

Comments are now closed for legal reasons. Our apologies.

BBC Merseyside is reporting on a ludicrous attempt to avoid business rates using snails. It is so stupid that I cannot do justice to it – please read the story (radio version here).

This is, however, just one of many stupid schemes to avoid business rates. And the bizarre thing is that historically they have mostly worked. Here’s why – and how the Government should step in.

The most well-known scheme doesn’t involve snails – it’s all about cardboard boxes.

The idea is that landowners grant a lease to a tax avoidance firm. The firm stores a few boxes in the property for six weeks1, then leaves and terminates the lease. This is claimed to be “occupation” and so, after the short lease terminates, the landowner claims “empty property relief” from business rates for the next three months.2 The landowner pays 20% of its tax savings to the tax avoidance firm. And then does the whole thing again when the three months ends. And again.

To a tax lawyer, this looks laughable. It’s an artificial scheme where the only purpose is tax avoidance – and the courts have spent the last 25 years striking down almost every tax avoidance scheme they’ve seen. This one isn’t even clever. I think most tax lawyers would expect the courts to shred box-shifting schemes in minutes.

But in fact the courts have repeatedly approved these schemes.

In the Principled case from 2013, the judge ruled for the landowner, saying:

“I cannot see any good reason why, if ethics and morality are excluded from the discussion, the thing of value to the possessor should not be the occupancy itself. The verb “occupy” and the nouns “occupation”, “occupancy” and “occupier” are, in the end, ordinary English words. Their meaning has developed in case law to give them a sensible construction, but they have not been given technical statutory definitions.”

And the same judge, in the Public Health England case from 2021, applied judicial reasoning from 1949:

And then one of his “propositions of law”:

“it does not matter if the possessor’s predominant or sole motive is mitigation of or exemption from rates liability“

(I’m appalled that a government body would not only buy a tax avoidance scheme, but then cause government money to be spent on both sides of litigation defending it.)

The reason this is so surprising to tax lawyers is that it’s not how modern statutory interpretation of tax law works. Following the Ramsay case in 1982, and the Furniss v Dawson case a year later, the courts began to apply tax law purposively, interpreting terms in light of their realistic purpose. There is an excellent summary of the law here, from law firm Norton Rose Fulbright. So when a judgment starts off by using the words “tax avoidance”, the result is almost always that HMRC wins, and the taxpayer loses.

Except business rates. As this article says, the courts seemed to accept that “rate mitigation schemes” were legal and proper practice.

The result was an explosion in business rates avoidance, driven by a mini-industry of “business rates mitigation advisers” charging 20% of the tax saving.

Box-shifting was the most common scheme, but there were numerous variants – my favourite (upheld by the High Court) involved the entirely tax-motivated installation of “blue tooth3 equipment”. The snail scheme seems particularly egregious, but it’s not insane to suggest it would have worked.4

Why did the schemes succeed?

So why was it that the courts have been merrily striking down every tax avoidance scheme they see, but approving business rates avoidance schemes? There’s no reason to think that business rates are any different from any other tax.

Informed observers5 have suggested three key reasons:

HMRC has had massive success litigating avoidance schemes in the last 25 years, and lost very few cases.6 However, business rates cases are usually litigated by local authorities, who don’t have this experience or expertise.

The lawyers acting for the local authorities tended to be planning and local government lawyers, not tax specialists. Undoubtedly they are very able, but they did not run the cases as tax avoidance cases. So in the Principled and Public Health England cases, Ramsay was not even argued.7

Cases don’t come before tax tribunals and tax judges, who would have disposed of these schemes in fifteen minutes. Instead they usually end up as judicial reviews8, and (very unsatisfactorily) these courts did not apply the modern approach to interpretation of tax law.9

This all changed in 2021 with the Hurstwood case, when a particularly aggressive business rates avoidance case hit the Supreme Court.

Things are looking bad for the landowner when we get to the fourth paragraph of the judgment:

“The liquidation version of the scheme (in the form described in this judgment) has already been judicially branded an abuse of the insolvency legislation in proceedings for the winding up in the public interest of a company which promoted and managed such a scheme: see In re PAG Management Services Ltd [2015] EWHC 2404 (Ch); [2015] BCC 720. As will appear, the dissolution version of the scheme is no less an abuse of legal process and may in certain circumstances involve the commission of a criminal offence.“

And, as often happens, particularly bad facts result in a significant change of judicial approach that will affect everybody.

And then it only took one paragraph to reach the obvious conclusion:

“In our view, Parliament cannot sensibly be taken to have intended that “the person entitled to possession” of an unoccupied property on whom the liability for rates is imposed should encompass a company which has no real or practical ability to exercise its legal right to possession and on which that legal right has been conferred for no purpose other than the avoidance of liability for rates. Still less can Parliament rationally be taken to have intended that an entitlement created with the aim of acting unlawfully and abusing procedures provided by company and insolvency law should fall within the statutory description.“

When it comes to tax avoidance schemes, the common-sense result is usually the correct legal result. The taxpayer lost.11

So how come the High Court, and the Court of Appeal had come to the opposite conclusion? Because, said the Supreme Court, the local authorities and their lawyers had been rubbish at arguing their case. I paraphrase only slightly:

“The courts below appear to have received little assistance from counsel for the local authorities as regards the purpose of the rating legislation; and the same was true in this court. It is perhaps unsurprising that in these circumstances the judge and the Court of Appeal did not adopt a purposive approach to interpreting the relevant statutory provisions and considered that the “owner” as defined in section 65(1) of the 1988 Act must invariably and even on the assumed facts of these cases be identified as the person who is entitled to possession of a hereditament as a matter of the law of real property.“

They should have hired a tax lawyer – and then the local authorities wouldn’t have spent a fortune on taking a simple case all the way to the Supreme Court.

But aren’t business rates an unfair burden on many businesses?

Not as much as is often claimed. The evidence suggests that most of the economic burden of business rates falls on landowners, not retailers/tenants. This is a counter-intuitive result, and retailers often argue strongly that it’s they who are paying. They are, however, wrong – retailers pay the tax, but in the long term the burden is passed to landowners in the form of lower rents, with 75% of the cost of business rates passed onto landowners after three years.

There are certainly problems with business rates, not least that the slow five year cycle of revaluations means that retailers can be caught paying business rates that are out of all proportion to their rent.

The Sunak Government ran a consultation last year on business rates avoidance. The 2024 Spring Budget announced three outcomes:

The Finance Act made box-shifting a bit harder, by requiring premises to be reoccupied for 13 weeks rather than six weeks.

The Government said it would consult on extending the general anti-abuse rule (GAAR) to business rates.

There would be communications to warn landowners off cowboy “mitigation” firms.

This doesn’t go far enough.

The Hurstwood judgment should end all the avoidance schemes, but experience suggests that the avoidance firms will continue to flog schemes, take their 20% fees, and then disappear when – years later – the courts strike them down.

The Government should do three things.

First, drag business rates into the 21st century, and make sure all modern anti-tax avoidance rules apply to business rates. That means:

Introduce a targeted anti-avoidance rule (“TAAR”) for business rates. We see TAARs in most modern tax rules, and they work like this: if you do something artificial which has the sole or main benefit of reducing or eliminating your business rate liability, then it has no tax effect. Scotland has already done this; the rest of the UK should follow their lead.

Business rates should be covered by DOTAS, the rules that require tax avoidance schemes to be disclosed to HMRC.

Second, and more controversially, consider fixing the administrative problems that led to ten years of stupid avoidance schemes:

Everyone involved will hate this proposal; but Government should give serious consideration to requiring all non-valuation business rates litigation to be delegated to HMRC. Or, if that’s too unpopular, or administratively difficult, require HMRC to be consulted on business rates appeals involving points of law.

Another unpopular proposal: the Government should consider a new right of appeal to tax tribunals for non-valuation business rate disputes. Tax tribunals are far better placed to hear what are in reality tax disputes. The risk would be a large increase in poor quality appeals, taking up both tribunal and local authority time – one way to avoid that would be to charge higher fees for business rate tribunal appeals.

And: local authorities, when you’re dealing with tax avoidance, please hire lawyers who have expertise in tax avoidance.12

Finally, none of these technical measures will deter cowboys like the snail promoter:

So the Government should crack down on promoters of hopeless schemes – business rates as well as other tax avoidance schemes.

Make failure to comply with DOTAS a criminal offence.

Make it a criminal offence to promote a scheme or tax position which is so unreasonable no reasonable adviser would think that it works.

And impose tax-geared penalties on advisers, and their directors/shareholders, when they promote a scheme or tax position that is so unreasonable no reasonable adviser would think that it works.

Business rates need to grow up and be treated like other taxes. And the Government should empower HMRC to go after promoters, not the taxpayers they exploit.

Rachel Reeves vs the snails shouldn’t be a close fight.

Meaning: not me. I am a tax avoidance expert but not a business rates specialist, and this article leans heavily on people who are business rates specialists ↩︎

Their failures have been in failing to challenge schemes early enough). ↩︎

See para 76 of Principled: “[The Ramsay doctrine] is not relied on in the present case and [it is something] which I will not attempt, at my peril, to paraphrase.” ↩︎

Most business rates disputes are around the value of the property and these go to the Valuation Tribunal; but there is no route for appealing technical business rates points other than judicial review ↩︎

Para 117 of Principled suggests the judge didn’t understand Ramsay at all – he said “The cases on sham transactions, those founded on the Ramsay principle, and those founded on lifting of the corporate veil, do not provide the answer either. There is no question here but that the transactions are genuine and produce the legal results for which, by the wording of the documents, they provide.”. That is not the test in Ramsay – the genuineness of the transactions and the absence of sham does not prevent it applying. The judge should have required the parties to present arguments on Ramsay and other common law anti-avoidance caselaw. ↩︎

Although, in fairness, the not tax lawyers did occasionally beat the tax lawyers, although an appeal is pending. Many thanks to H (a tax lawyer) for bringing this to my attention just after publication. ↩︎

The Hurstwood judgment came just a few weeks after Public Health England, which must be regarded as wrongly decided. ↩︎

I accept no fee-paying work and have no interest in any law/accounting firm, so I can say this without a conflict of interest. ↩︎

The UK loses £1bn each year to fraudulent claims for research and development (R&D) tax relief. We can reveal that one of the firms responsible is Green Jellyfish – one of the largest firms in the market. Green Jellyfish says it’s a specialist in research and development tax relief, and that they help companies claim an average of £32,000 in tax refunds from HMRC. But they claim tax relief that doesn’t exist, and then cover it up with the help of an affiliate, Kirby & Haslam. They’re making £3m a year in profits from ripping off the taxpayer and their own clients.

We can identify that one of the largest R&D firms in the market has submitted a series of fake and potentially fraudulent R&D tax relief claims: Green Jellyfish. We have a dossier of clearly fake2 R&D tax relief claims made by Green Jellyfish and its associates. This article focuses on one – where Green Jellyfish’s client/ victim was Sophie3, who runs a small therapy business.

Green Jellyfish promised Sophie a “no win no fee” R&D tax relief claim, but there was never any basis for it, and when HMRC challenged it, Sophie was left with large bills. We believe she was defrauded. In other cases, where HMRC didn’t spot Green Jellyfish’s false claims, it will be the taxpayer who was defrauded.

We believe there is enough evidence for HMRC and the police to commence a criminal investigation, shut down Green Jellyfish’s business, and protect both their clients and the wider public interest.

R&D tax relief

R&D tax relief was created to encourage small companies to invest in research and development. It gives profit making companies a tax deduction which reduces their corporation tax bill, or in the case of loss-making companies the ability to surrender their losses for a cash payment from HMRC.

The Times reported in 2022 about highly questionable R&D tax relief claims, with restaurants being encouraged to claim R&D relief for vegan menus. In our view, claims like this have no legal basis and may be fraudulent.

Sophie runs a small therapy business. In 2021 she had £46k of revenue. She paid herself a salary of £12k, and had a profit of £18k (after other costs and corporation tax).

In 2022, Sophie was cold-called by Green Jellyfish, who said they thought her business could claim R&D tax relief.

As Sophie puts it:

“GJF from the start were persistent but very friendly and approachable, they seemed to know exactly what R and D was about, whereas I had never heard of it before. They were confident that my business could claim and after initial doubts I naively put my trust and faith in them.”

After the call, Green Jellyfish sent a follow-up email to Sophie saying this:

There is and was nothing on Sophie’s website that suggested any R&D activity. Green Jellyfish was at no point FCA-regulated. 5

And they explained their process:

We don’t believe anyone who’d even casually perused the HMRC website could “safely say that [Sophie would] easily fall within the parameters of the scheme”.

Sophie had no financial or tax background, and trusted that Green Jellyfish knew what they were talking about. She took up the offer of a telephone consultation. During the call, Green Jellyfish asked Sophie about her business and whether she thought it was “innovative”. Sophie said it was6, but didn’t provide much detail about what she did

Green Jellyfish didn’t ask about whether there were any specific R&D projects – it’s pretty obvious there weren’t, and couldn’t be, when Sophie’s business had one employee/director who was a therapist, not a researcher or engineer.

The evidence of fraud

Green Jellyfish then asked for Sophie’s accounts and corporation tax return:

And off the back of that, with no information about any R&D activity, Green Jellyfish submitted an R&D tax relief claim.

We believe this was likely fraudulent for two reasons.

First, Green Jellyfish had no basis for making a claim, because Sophie gave them no basis. They never provided her with any statement of what precisely the claim would be for, much less the kind of report you’d expect from an R&D firm. As Sophie put it to us:

“I remember chatting to Andrew about my business on the phone but I still don’t know what he was claiming for!“

This therefore isn’t a case of Green Jellyfish staff misunderstanding the legislation or guidance. There’s no evidence they paid any attention to the rules at all.

Second, Green Jellyfish claimed Sophie’s entire staff costs as qualifying R&D expenditure.

Here’s Sophie’s accounts for 2021 – we’ve blanked out the last three digits to preserve her anonymity:

Note the staff costs of £12k – the only staff member was Sophie herself. And Green Jellyfish claimed all of that as qualifying R&D expenditure:

This doesn’t survive five second’s scrutiny. Nobody in the business of filing R&D tax credit claims could seriously think Sophie spent absolutely all of her time on qualifying research and development activity.

So why did they claim the entire £12k? We expect that’s because the only way an R&D relief claim for a company of this size would make sense, and justify Green Jellyfish’s fee, is if they claimed 100% of staff costs.

We should add that we can be certain from this evidence that a false R&D tax relief claim was made, but we cannot be certain that a fraud was committed. That depends on whether those involved were dishonest to the criminal standard, which ultimately would be decided by a jury. We set out the criminal standard for fraud by false representation here, and for tax evasion (“cheating the revenue”) here.

But the evidence is in our view sufficient to merit a criminal investigation.

HMRC’s response

Green Jellyfish filed false R&D tax credit claims for Sophie for 2021 and 2022. HMRC immediately paid the refund, and Green Jellyfish took their fee.

A year later, HMRC told Sophie they were opening “compliance checks” into her R&D tax relief claims. That would mean Sophie would have to refund HMRC – and she’d remain out of pocket for Green Jellyfish’s fees.

Why does it work like this? Why couldn’t HMRC have checked the claim before paying the refund?

Because HMRC generally operate a “refund now, check later” policy. It’s a rational approach in a world of normal taxpayers and normal advisers. If HMRC checked first then refunds would take months. And who would put in a fake refund claim knowing that the consequence of getting it wrong would mean paying back the refund, plus interest and penalties?

But, unfortunately, “refund now, check later” creates a loophole for bad actors to exploit. Rogue R&D tax relief firms can file hopeless claims knowing that they keep their fees whatever happens, and that the risk sits with their poor clients like Sophie.

Kirby & Haslam

Sophie told Green Jellyfish she’d received a compliance check, and they passed her to an associated firm7, Kirby & Haslam.

At this point Sophie realised there was something very strange going on. Andrew had left Green Jellyfish, and the firm had no documentation for her claim. There was no report identifying the qualifying R&D expenditure, and not even a summary of her business activity. So Kirby & Haslam wrote to her asking the kind of questions that Green Jellyfish should have asked right at the start (but didn’t):

At this point an honest and competent firm would have realised that Sophie had no qualifying R&D expenditure. Kirby & Haslam took a different approach. They used Sophie’s responses to construct a response to HMRC which tried to claim that running remote therapy sessions during the Covid-19 lockdown was an “advance in science and technology” qualifying for R&D relief:

The idea this was an “advance in the field” is ridiculous, particularly at a time when almost every service business was finding ways to work remotely. We don’t believe any R&D tax expert would believe this claim had any prospect of success.

But the more serious problem is that it was entirely created after-the-event by Kirby & Haslam.

The consequence for Sophie

HMRC unsurprisingly rejected the Kirby & Haslam justification for her R&D tax relief claim (and another made subsequently for 2022). They sent Sophie a letter which explained why in some detail. For example:

This left Sophie with an unexpected bill of over £7,500 to repay to HMRC. That stung – because she’d only received a £4,500 refund… the rest had been taken by Green Jellyfish as their fee.

Sophie says:

“Just before Christmas I received a notice from HMRC that not only was I going to have to pay back the full amount of the first claim made by GJF, they had also found the second claim to be non-compliant, and I would also need to pay this back. I had no idea that HMRC were evaluating both claims so this came as a huge shock. I remember rushing over to my friend’s house in a state of distress, crying at the injustice of the situation and terrified about how I could pay the money back when it had already been absorbed into my business. At this stage my anxiety sky rocketed, and I spent a few days over Christmas feeling sick and stressed. I tried to put on a brave face around my children over Christmas as I did not want them to worry. The situation impacted on my mental health and triggered many negative emotions of fear, anxiety, isolation, anger, hopelessness and despair.”

The lies to escape penalties

At this point it looked likely Sophie would be hit with penalties for submitting a tax return that was “careless”.

Kirby & Haslam wrote representations to HMRC on Sophie’s behalf.

A normal firm in Kirby & Haslam’s position would have been appalled at Green Jellyfish’s original claim, and the representations would have described how Sophie had in essence been defrauded.

Instead, Kirby & Haslam wrote representations to HMRC which lied about the background. Here’s an email from them “correcting” Sophie’s initial answers to HMRC:

None of this was true. Sophie had relied entirely on the claim submission company. Andrew at Green Jellyfish (to whom Sophie had been speaking) was a “Business Development Manager”, not a tax specialist. She didn’t have a “thorough discussion” regarding her project, because she never discussed a project. Sophie had made no effort to understand the R&D tax relief claim criteria because they were never mentioned to her; she didn’t know what they were, or that they even existed.

Sophie was very uncomfortable with Kirby & Haslam’s proposed responses. She told us:

“Kirby and Haslem were pushing to avoid penalties from HMRC, and in my state of fear, I allowed them to talk me out of telling HMRC what I really wanted to say about GJF and their unscrupulous process. I was constantly told that as a company director I was expected to know about R and D and to have paid due diligence to the claim. I am a clinical professional, working in therapy. I am not a tax specialist and I’m rubbish at maths, so of course I couldn’t know the ins and outs of R and D. I had been led by the group of so called “specialists”. But apparently this was not good enough. Kirby and Haslem made me take responsibility for the claim without blaming GJF. I was so angry but felt alone with the problem, so saw no option but to take their guidance.“

Sophie escaped penalties. We think that’s a fair outcome under the circumstances – but it’s deeply unjust that Green Jellyfish and Kirby & Haslam aren’t subject to penalties themselves.

Could it just have been a mistake?

Not according to Green Jellyfish. When Sophie complained to them, they told her their “approach in preparing and submitting claims is always meticulous, based on the information provided to us and to the highest standards of care and skill”.

They refunded their fees for the 2021 claim, but not the 2022 claim (despite their “no win no fee” promise).

And it wasn’t a one-off either. We have a dossier of similar cases, often for much more money: R&D tax relief claims being made by Green Jellyfish on the basis of absolutely nothing, by businesses who realistically could never qualify. And then in these cases we again see Kirby & Haslam coming in after the event, and inventing rationales for the original claim. But at least in Sophie’s case the Kirby & Haslam document described her actual activity; we’ve seen other Kirby & Haslam letters which invent entirely fictitious R&D projects.

Green Jellyfish is not a small operation. Its accounts show that in 2022 it had 38 employees and made a profit of at least £3m.8

How much of Green Jellyfish’s business consists of genuine R&D claims, and how much fake claims? We can’t know. The size of our dossier convinces us there are many fake claims – but we can’t know if it’s 10% of their business or 100%.

We would, however, speculate that what we’ve seen is Green Jellyfish’s standard approach. We say that for several reasons:

Sophie’s experience, and the other businesses we’ve spoken to, was consistent with that. No analysis of any projects, just the numbers in the accounts and tax return.

Green Jellyfish doesn’t appear to employ any tax advisers. Only salespeople and business development officers. This isn’t how you build a legitimate R&D tax relief business – R&D tax relief is highly technical.

Kirby & Haslam didn’t seem to think there was anything strange about the absence of any records from Green Jellyfish, or the fact that they were constructing entirely original arguments for R&D tax credit relief.

Sophie’s complaint was the opportunity for a bona fide company to look at its processes and consider whether her tax relief claim had been properly handled. They instead just lied to her (“meticulous”).

Even if most/all of Green Jellyfish’s R&D tax relief claims are false, we expect some of their clients will be very happy. HMRC are unlikely to be able to identify all the false claims, and some clients will inevitably keep their refunds (even if there’s a criminal investigation).10 In those cases, it’s HMRC and the wider body of taxpayers that lose out.

Paul Rosser

This report only exists because of years of work by Paul Rosser.11

Paul is an R&D tax specialist. He’s often asked by non-specialist accountants to check R&D claims, particularly when they’re prepared by outside firms who the accountants don’t know. In 2020 he started to see claims prepared by Green Jellyfish which he thought were clearly invalid. Paul had been writing about the dubious end of the claims industry. Paul now wrote specifically about Green Jellyfish on LinkedIn, and named the firm.

On the evening of 25 April 2024, Sotiris Christophi arrived unannounced at Paul’s home and threatened him. He said Green Jellyfish had been through Paul and his wife’s social media accounts, and was preparing to release some unfavourable information about Paul to the public. Paul immediately told him to leave. Christophi then made a series of calls to Paul’s wife’s personal mobile phone.

We asked Christophi about this back in April: he responded saying he regretted his actions, and asking to speak to us in person. We said we would prefer if Christophi could put his position in writing;12 we never heard back.

The tip of the iceberg

There is a large network of companies associated with Green Jellyfish:13

The precise links between the companies aren’t clear but there is clearly a close relationship between Green Jellyfish and Kirby & Haslam. An adviser acting at arm’s length would have advised Sophie to tell HMRC she was misled by Green Jellyfish. A normal adviser would not accept repeated referrals of improper claims. The letter from Green Jellyfish responding to Sophie’s complaint was (according to the metadata) written by a paralegal working for Kirby & Haslam.

Kirby & Haslam and Aston Shaw are owned by Sotiris/Steve Christophi, an accountant regulated by the Association of Chartered Certified Accountants (ACCA).15 Christophi denies a connection to Green Jellyfish, but he certainly seemed to be speaking for Green Jellyfish when he visited Paul Rosser’s home to threaten him.

We have a dossier of other apparently fraudulent tax relief claims made by these companies, and will be writing more about them soon.

We put to Fladgate that Green Jellyfish submits R&D claims with no technical basis, and all it does is review a company’s corporation tax returns and accounts. We also put to them that Kirby & Haslam invent justifications for Green Jellyfish’s claims after the fact.

The Fladgate letter was labelled as “confidential”. It wasn’t. Solicitors are not permitted to falsely label letters as confidential, and one solicitor is currently appearing before the Solicitors Disciplinary Tribunal as a result of such a mislabelling.16

Most of Fladgate’s letter to us is taken up with allegations of an “unlawful means conspiracy” against Green Jellyfish by former employees, rival R&D advisers, and an individual who Christophi is currently suing. We have no interest or understanding of any of this (we’re confident that Sophie’s story is real). It is, however, most unusual for a solicitor to put in correspondence what amounts to a conspiracy theory.

Fladgate deny that Green Jellyfish or Kirby & Haslam is behaving improperly, but the denial is very non-specific.

Specific denials are then included in a separate email from Christophi (on behalf of Kirby & Haslam) and an unknown individual representing Green Jellyfish, which Fladgate forwarded to us. The evidence above (and other evidence we have collated) shows these denials to be false.

The Christophi/Green Jellyfish email rather deceptively ducks our allegation that it’s improper for Green Jellyfish to claim that care homes, restaurants and childcare companies can often claim R&D relief. (“The legislation is very clear and doesnot exclude a company from making an R&D claim based solely on the sector.“)17

Fladgate is a fine firm with a good reputation. We think there will be widespread disquiet amongst its partners that it’s acting for a business that is widely suspected of fraud, denying that fraud in the face of public evidence, and repeating their client’s wild conspiracy theories.

Everyone, guilty or innocent, deserves a criminal defence, and no criminal lawyer should be criticised for acting for any defendant, no matter how repugnant their crimes. However, defamation is very different. There is no professional or moral duty for a solicitor to write defamation threats on behalf of a business when there is good reason to believe it is carrying on a fraud. Particularly when the consequence of acting is that the solicitor will be facilitating the fraud.

HMRC’s response

HMRC is prohibited from commenting on individual taxpayers, but told us:

“With R&D claims, public money is at stake and taxpayers rightly expect us to scrutinise them, which is why we have increased compliance activity. We do that thoroughly and fairly, and the overwhelming majority of valid claims are paid on time.

Any customers who have a concern about an R&D claim they have made, or may have been made on their behalf, should email: [email protected] They should title the email as ‘For the attention of the R&D Anti Abuse Unit’“

What should happen to Green Jellyfish?

Sophie has been deeply affected by what happened to her:

“I contemplated closing my business, as it does not make a huge turnover and I wondered if all this pressure was worth it. I used most of my savings paying back the requested amount and I am still trying to build my savings back up.

I always follow the rules and trust others to do the right thing, and it felt like I had been taken for an idiot. I don’t understand the mentality of people who act like this and I feel let down by what I’ve experienced.“

We don’t think Sophie should blame herself. She was the victim of what looks like a fraud. Those responsible should pay the price.

We will be referring Christophi to the ACCA, although we don’t have much hope – the ACCA unaccountably is refusing to investigate Christophi’s threat to Paul Rosser. We will also be reporting Green Jellyfish’s false claim of FCA regulation to the FCA.

And the evidence presented in this article suggests that Green Jellyfish and the individuals who run it have defrauded both their own clients and HMRC.

We believe there should be an immediate criminal investigation.

We hope the authorities can move quickly; past experience is that Green Jellyfish and those behind it may not stick around to face the consequences of their actions.

How to stop the tax cowboys

Green Jellyfish are not the only tax firm defrauding their clients and HMRC.

The previous Government thought the answer was regulation – they ran a consultation on “raising standards in the tax advice market“.18 We don’t agree. Green Jellyfish weren’t regulated, but acted with total disregard for the law – they’d disregard regulation too. And Kirby & Haslam was regulated.

So it’s not at all clear that regulation is the answer. It would, however, come with a cost – a new regulatory edifice to be created for currently unregulated advisers, most of whom do a good job. That means cost for them, cost for their clients, and cost for the taxpayer.

The better answer is a simpler and more powerful one: change the incentives. Right now, the reward of churning out fake tax claims is large, and the risk of serious sanctions, or criminal prosecution, is perceived to be low. That needs to change.

Our suggestion: create a new criminal offence of promoting tax schemes, or technical tax positions, that are so unreasonable that no reasonable adviser would think they were correct.19 The offence would be accompanied by civil tax penalties equal to 100% of the tax in question, chargeable on the companies involved and the people behind them.

The challenge is to shape the new rules so that the cowboys are pushed out of the business, but legitimate advisers have nothing to be concerned about. That’s hard, but not impossible. And it’s been achieved before. When the General Anti-Abuse Rule was introduced in 2013, some feared it could apply to “normal” tax planning – in practice it hasn’t.

That’s what we’re proposing – a GAAR-style rule that’s carefully aimed at the cowboys, and with very serious consequences when it applies.

Many people’s instinctive response is that we should “make tax avoidance illegal”. That can’t, and shouldn’t be done, because we can’t rigorously define “tax avoidance”.

But we can rigorously define “trying to avoid tax by taking a position that isn’t in fact legally correct, and is so unreasonable that no reasonable adviser would have taken it”. And then make that a criminal offence.

It would be more effective than a new regulatory framework, and an awful lot simpler.

Full credit to Paul Rosser of R&D Consulting for discovering and pursuing this story over the last couple of years. It’s an extraordinary story of a tax professional doing the right thing despite considerable professional, legal and even physical risk. This article wouldn’t exist without Paul.20

Thanks above all to Sophie (and other clients/victims of Green Jellyfish) for telling us their stories. We’ve anonymised Sophie’s details but she’s aware that Green Jellyfish and K&H may identify her; in the unlikely event they’re stupid enough to threaten her, we will take full responsibility for her defence.

Many thanks to K and T for their R&D tax relief expertise, to P for additional research, and as ever to S for his invaluable review and insights. Thanks to J for picking up an accounting error in the original draft.

Hopefully the figure will be much smaller going forward, following new rules requiring much more detail in applications from 1 August 2023 ↩︎

By which we mean not just technically wrong, but indefensible ↩︎

Sophie is not her real name. For the reasons we set out below, we will not be identifying any of our sources for our Green Jellyfish investigation, except Paul Rosser. We have hidden Sophie’s name, and the details of her business, but not changed anything material to her story. ↩︎

Prior to 2 July 2021, Green Jellyfish was owned by Glide Business Solutions, which was FCA-regulated. However that is irrelevant to the status of Green Jellyfish and its staff, and in any event Glide wasn’t the shareholder when the email was sent to Sophie in 2022 ↩︎

We agree; the way Sophie carried on her therapy business during lockdown was “innovative” in the normal business meaning of the term; but that’s very different from having qualifying R&D expenditure. ↩︎

The precise nature of the association isn’t clear; more on that below ↩︎