We keep talking about marginal rates, but rarely stop to explain exactly what they are, and why they matter. Here’s a short explainer, to accompany our interactive marginal rate charts.

There is an updated article on marginal rates here.

The marginal rate is the percentage of tax you’ll pay on your next £1 of income. It therefore affects your incentive to earn that £1.1.

If you doubt that, imagine that you pay tax at 20% on your income, but the next £1 you earn, or indeed the next £10,000 you earn, will all be taxed at a marginal rate of 100%. Would you work extra hours for zero after-tax pay? I think most people would not.

That seems a silly example (although we can find worse ones in our own tax system – see below). But a marginal rate below 100% will also change your incentives.

Perhaps you are only just managing to afford childcare, and every hour you earn increases your childcare costs. A marginal rate of 70% might mean your take-home pay is less than the childcare cost.

Or it may just be that you value your own time so that, if your take-home pay from working additional hours drops below a certain point, it’s not worth it to you.

We should look at some examples.

Marginal rates – a boring example

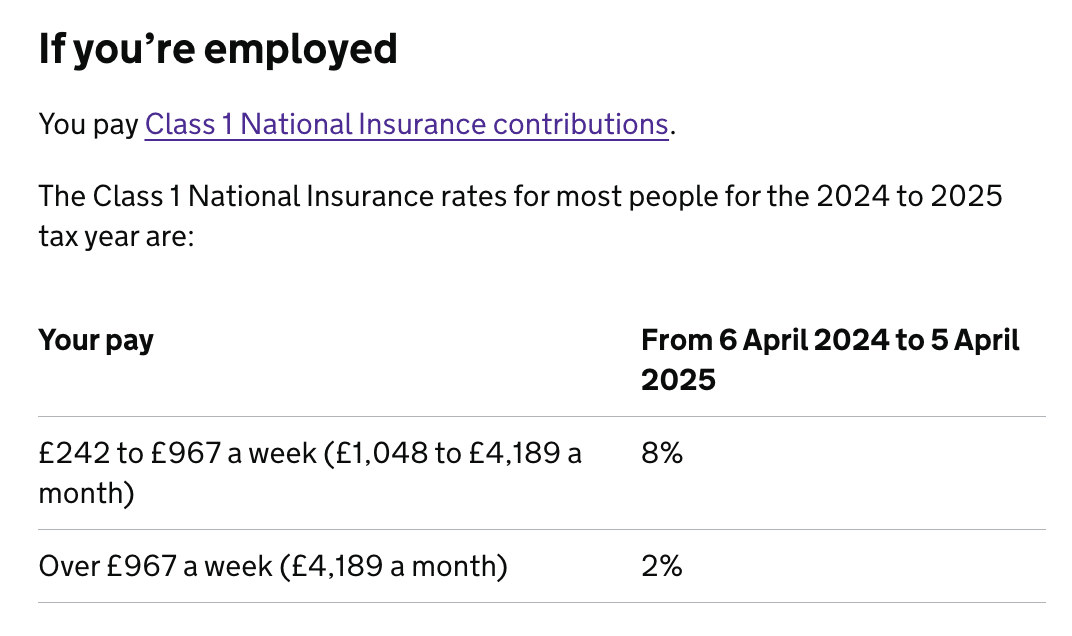

In the current, 2024/25 tax year, combined income tax and national insurance rates for an employee look like this:2

- No tax on incomes below the £12,570 personal allowance.

- £12,570 to £50,270 – a combined income tax and employee national insurance rate of 28%

- £50,271 to £125,140 – a combined rate of 42%3

- Above £125,140 – a combined rate of 47%.

It’s important to realise that the different tax brackets only apply to income in that bracket. If you earn £50,271 you’re in the higher tax bracket, but you only pay 42% tax on £1. You still pay 28% tax on everything you earned before above the personal allowance. This is unfortunately not very well understood.

Imagine Bob is an employee earning £12,570. None of his income is taxed. Bob has the opportunity4 to earn an additional £1,000, putting him in the 28% tax bracket.5

There are three ways we could describe Bob’s position after earning that £1,000.

- The applicable headline rate. Bob is a basic rate 28% taxpayer.

- The overall effective tax rate. This is the total tax paid divided by Bob’s income. Total tax paid = £1,000 x 28% = £280. Income = £13,570. So effective tax rate is 280/13570 = about 2%.

- The marginal rate – the percentage tax you’re paying on that new £1,000. This is 280/1000 = 28%.

Each of these has their uses.

The first figure is simple.

The second is useful for assessing how much tax Bob pays overall. If a political party proposed a sweeping set of tax reforms, Bob would be very interested in the impact on his effective rate.

But the third – the marginal rate – is important, because it affects Bob’s incentive to earn the additional pound. Right now it’s the same as the headline rate – but that’s not always the case…

Marginal rates – a less boring example

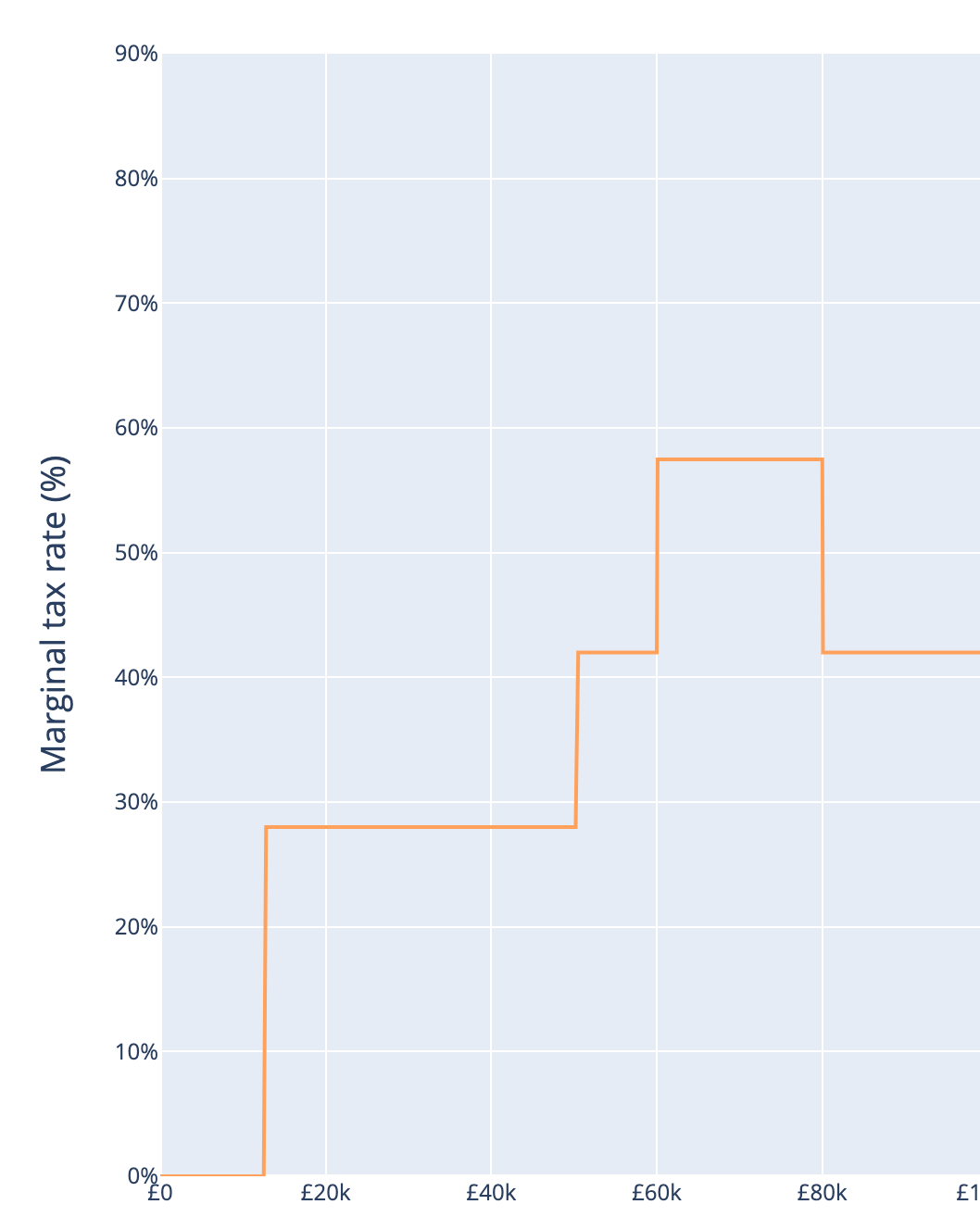

Jane is earning £60k and claiming child benefit for three children. That’s worth £3,094.

She’s now in the 42% tax band.6 Jane still pays basic rate tax for her income between £12,570 and £50,270, but now pays 42% tax for everything over that. So her total tax bill is (50270 – 12570) * 28% + (60000-50270) * 42% = £14,643 and Jane takes home £45,357.

Jane is thinking of working a few more hours to earn another £1,000. She’s still in the higher tax band – so in a sane world she’d expect another £420 of tax, and a marginal rate of 42%.

But that is not the result. Once Jane’s income hits £60,200, the “High Income Child Benefit Charge” starts to apply to claw back her child benefit – 1% for every £200 of earnings.

So that £1,000 of additional earnings costs Jane HICBC of £154.70, on top of the £420 of “normal” tax. A total of £565.

So how do we describe Jane’s position after earning that £1,000?

- The applicable headline rate. Jane is a higher rate 42% taxpayer.

- The overall effective tax rate – the total tax paid divided by Jane’s income. That’s 15207/61000 = about 25%.

- The marginal rate – the tax Jane is paying on that new £1,000. This is 56.5% – and we will have the same result for all incomes between £60k and £80k. 7

As I mentioned at the start, there can be practical reasons for people to turn down work if the marginal tax rate gets too high – but there are also psychological factors. For many people, 50% feels like a high rate.

Oh, and if Jane’s a student repaying her student debt, then the marginal rate goes up by 9% to 66%.

And if the Green Party formed a government they’ll raise this to 72%.8

The big picture

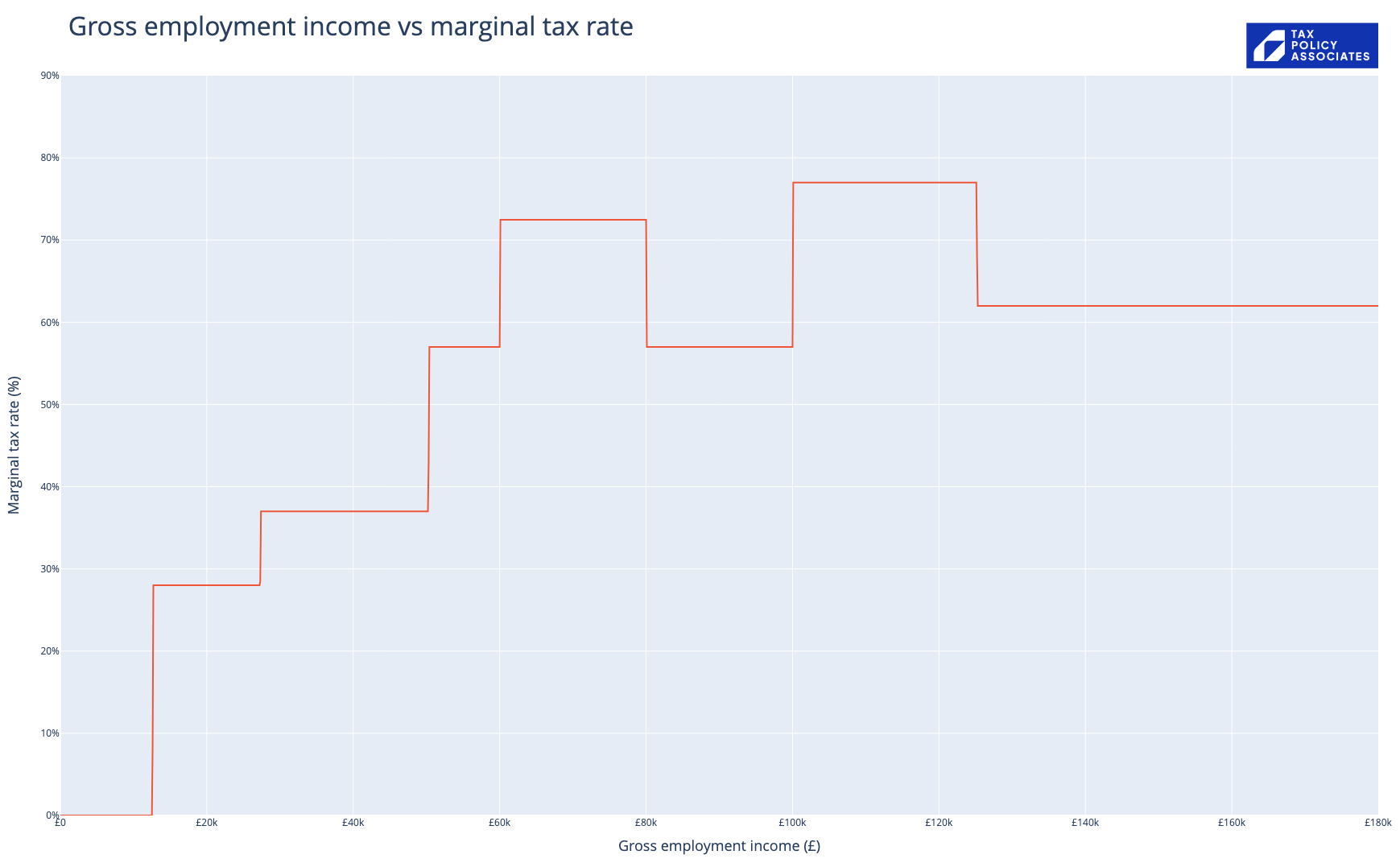

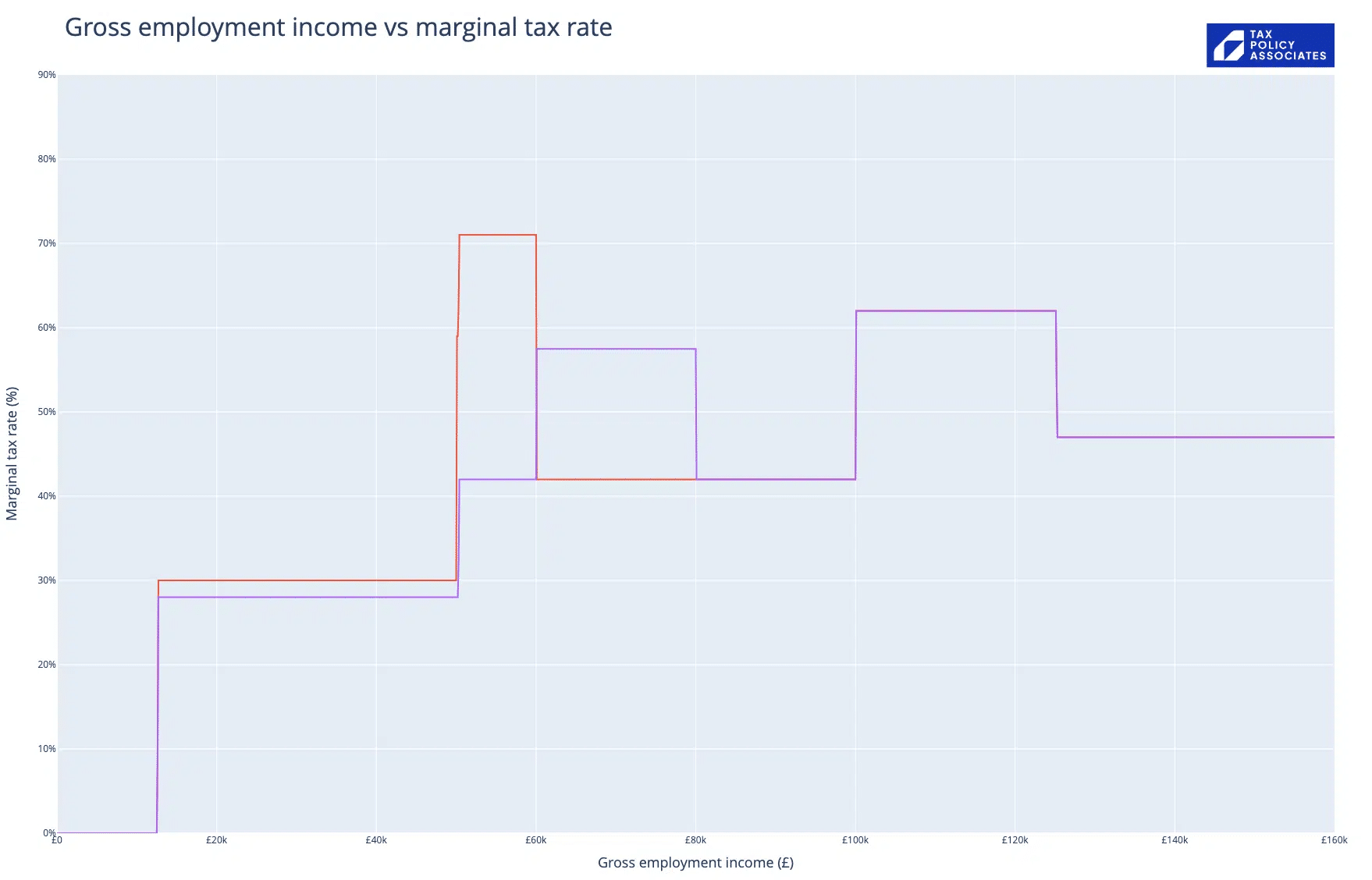

We can chart Jane’s marginal rate for each income she could earn. Incomes along the bottom, marginal rate along the top:

You can see the HICBC as the “tower” between £60k and £80k, which should be a smooth 42% plateau. Instead it hits 57%. (I’m hiding what happens after £100k)

The HICBC is a gimmick which enabled George Osborne to somewhat-surreptitiously raise tax on people on high incomes without raising the tax rate itself.

It’s a really bad policy:

- It means that Jane pays a higher marginal rate rate than someone earning £90k, or indeed £900k. Where’s the logic in that?

- The way in which HICBC works creates a nasty trap for the unwary, with thousands of people accidentally incurring HMRC penalties.

The politics are nice and intuitive – surely it’s not right for people on high incomes to receive child benefit? But the reality is that this logic inexorably leads to a high marginal rate, and a cumbersome and sometimes unjust collection mechanism.

Can it get worse?

Very much worse.

George Osborne’s HICBC was copying a trick invented by Gordon Brown to clawback the personal allowance for people earning £100k.

Again, the politics are nice, but the consequences are a mess.

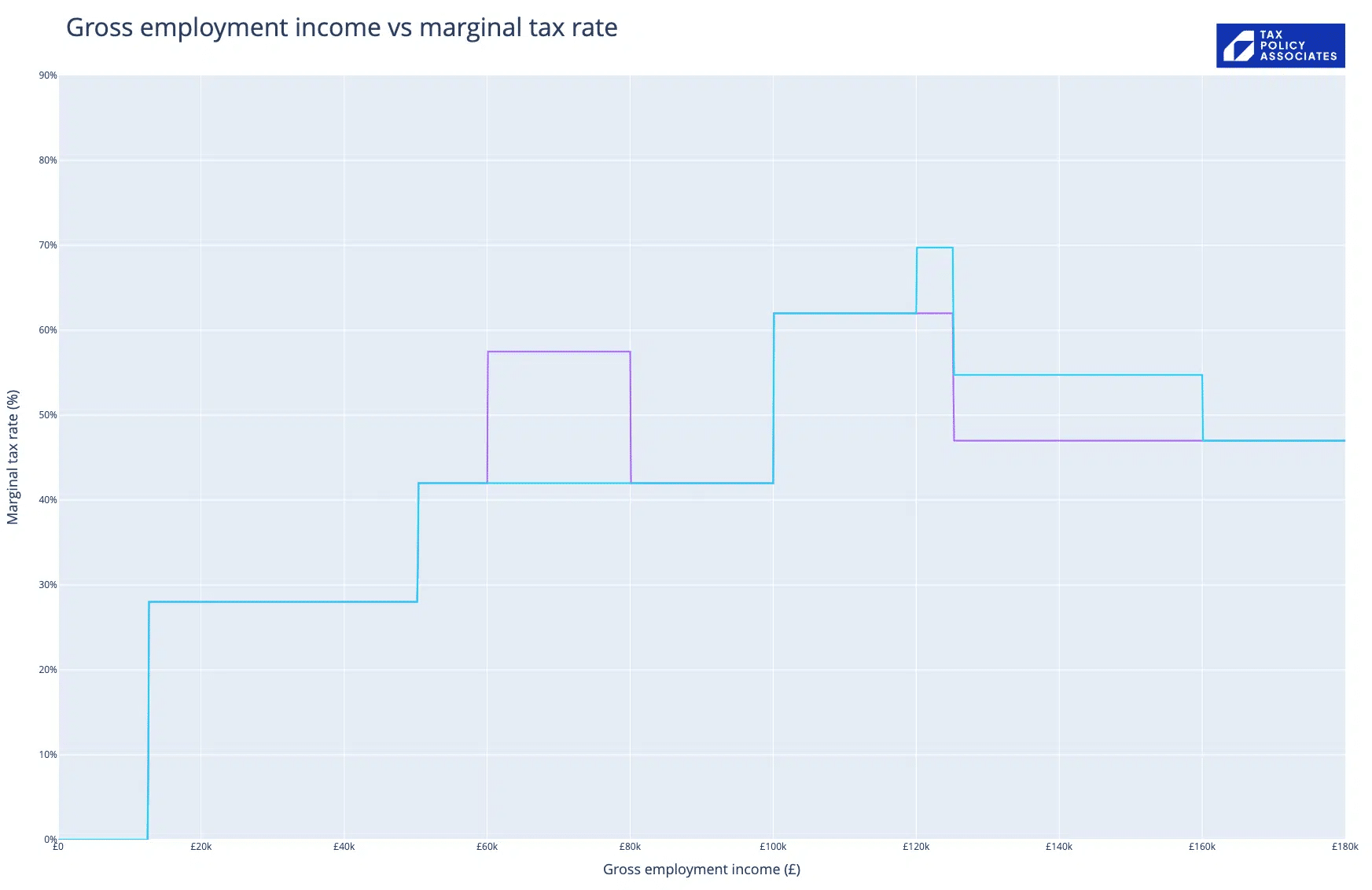

If Jane starts earning between £100k and £125k then she faces a marginal tax rate of 62%. It then drops to 47% from £125k. Her marginal rate chart looks like this:

62% is a very high rate. And if she has a student loan, that will add on 9% to the marginal rate, taking her total marginal rate, between £100k and £125k, to 71%.

We’ve received many reports saying that high marginal rates affecting senior doctors/consultants are an important factor in the NHS’s current staffing problems – exacerbated by the fact that the starting salary for a full time consultant is just under £100,000. But it’s important not to just focus on the impact on jobs that we think are of particular societal importance. It’s also problematic if an accountant, estate agent or telephone sanitiser turns away work because of high marginal rates – it represents lost economic growth and lost tax revenue.9 Sometimes people take the work, but use salary sacrifice or additional pension contributions so their taxable income doesn’t hit the threshold. But that doesn’t work for everyone; sometimes they’ve hit the pensions allowance; sometimes it doesn’t always make sense to work harder now, for money that they can’t touch for years.

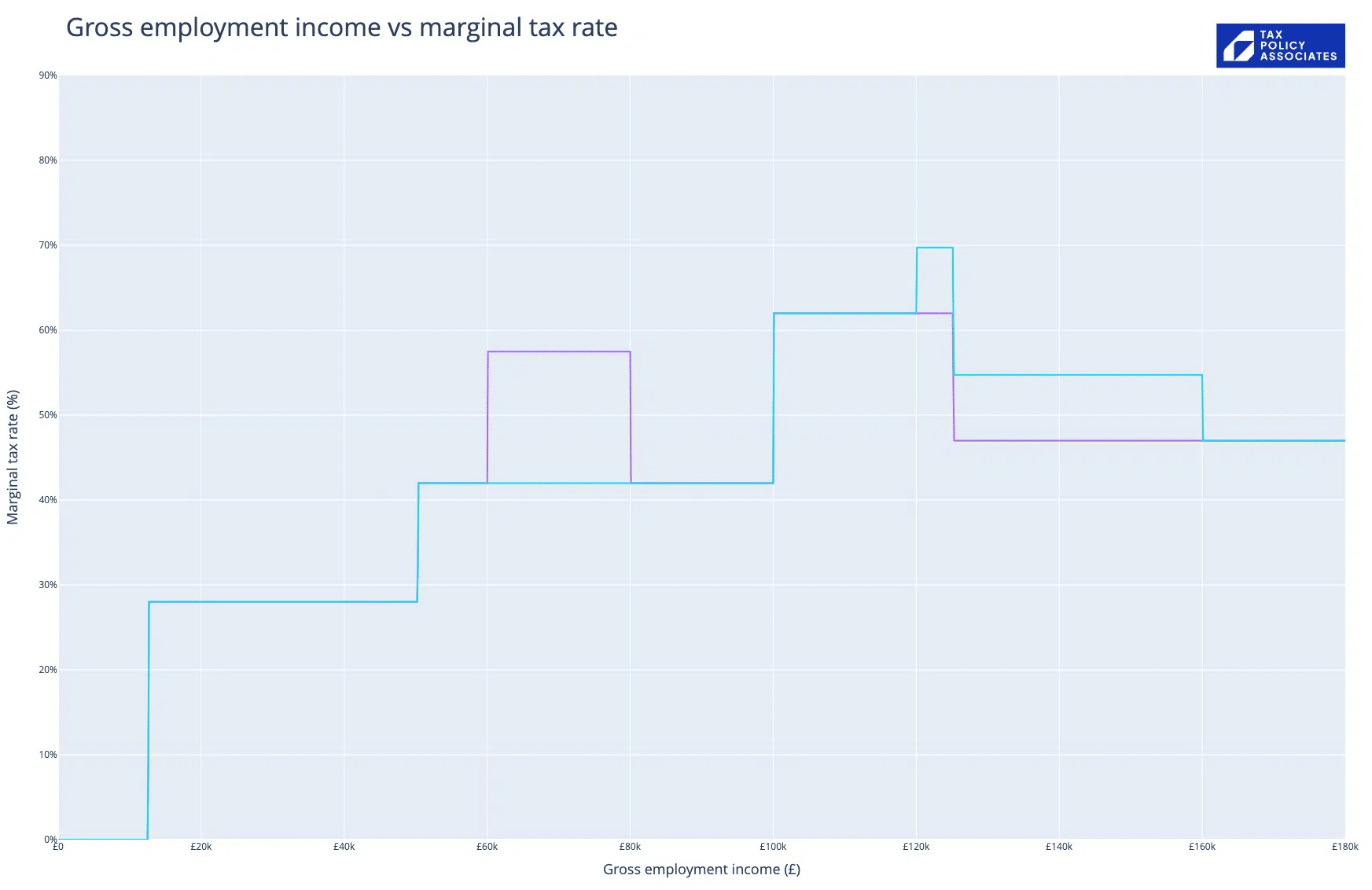

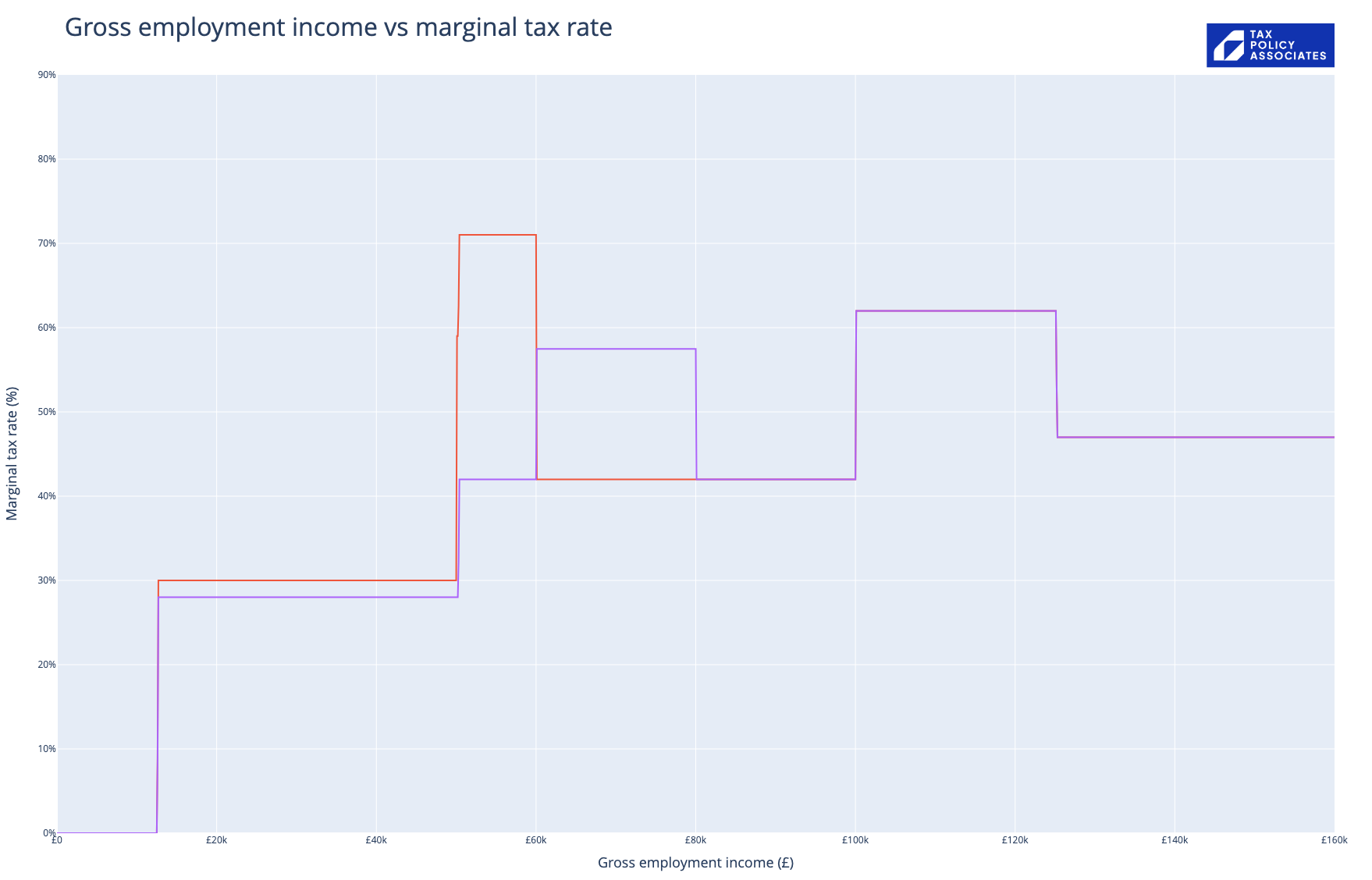

The Conservative Party election manifesto pledges to move the HICBC from £60-80k to £120-160k. That helped Jane on £60k but now creates a nasty problem. When she’s earning £120k, and almost out of the personal allowance clawback, she gets the full effect of both the child benefit clawback and the personal allowance clawback:

(Purple is how things are now; blue is the Conservative manifesto proposal)

That’s a marginal rate of 70%. And then, when she hits £125k, she’ll have a marginal rate of 55% all the way to £160k.

It’s a mystery to me why the Conservative manifesto didn’t set the new HICBC at £125k – you’d still have a 55% marginal rate beyond that, but at least you’d avoid 70%. The most plausible reason is that they were defeated by the complexity of the system.

And worse?

There are other similar features I’m skating over. The £1,000 personal savings allowance drops to £500 once you hit the higher rate band, and to zero once you hit the additional rate band. That can create high marginal rates at these points.10 The marriage allowance lets a non-working spouse transfer £1,260 of their unused personal allowance to their partner, if they’re earning less than the £50,270 higher rate threshold. So it’s worth £252 – and it disappears once the higher rate band is hit.

And worse?

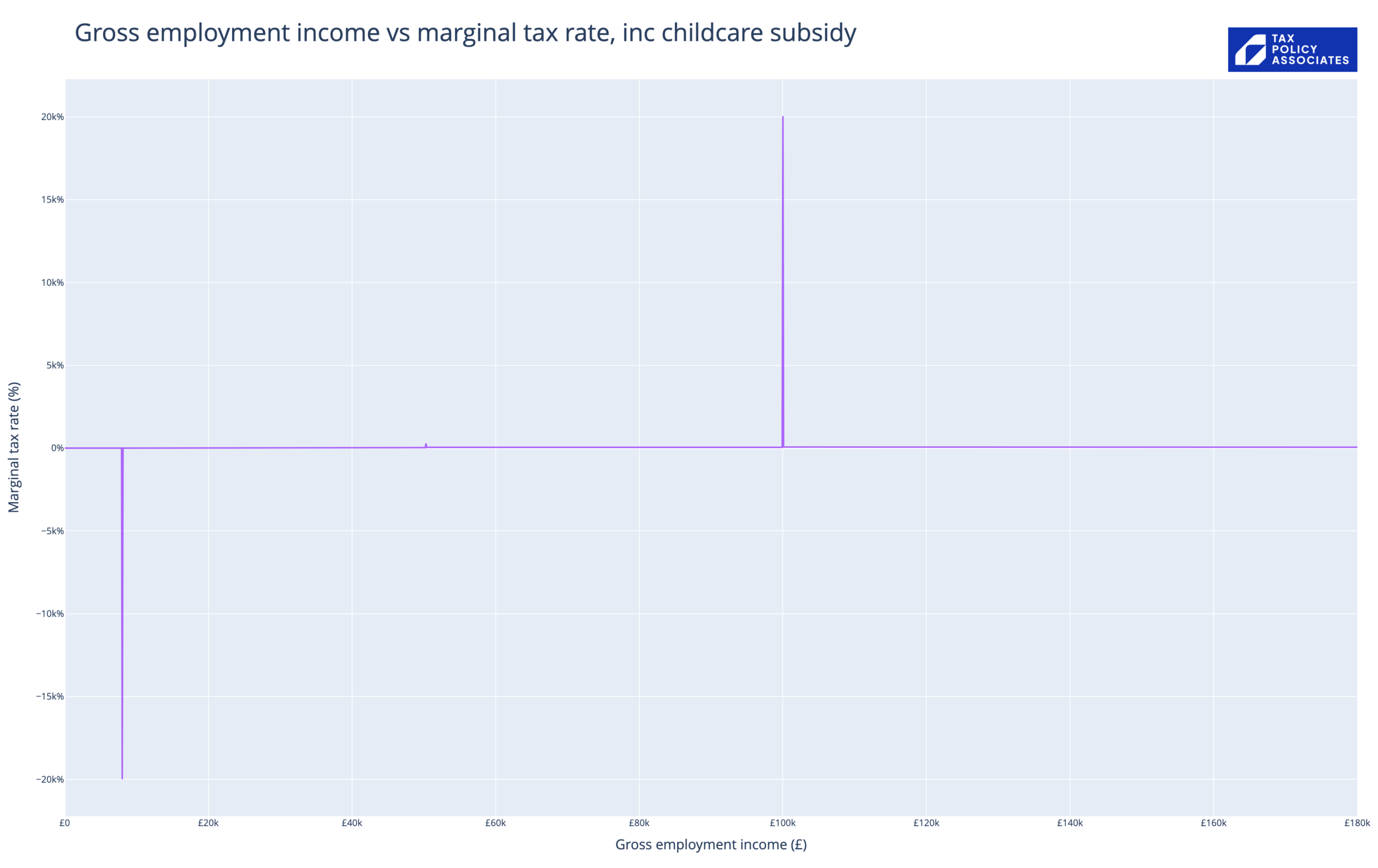

The Government keeps creating generous childcare schemes that are removed suddenly when your wage hits £100,000. That creates a marginal rate that can only be described as “insane”.

This year, the Government created a new childcare support scheme for parents with children under 3. This could be worth £10,000 per child for parents living in London. And it vanishes completely once one parent’s earnings hit £100k. Here’s what that does to the marginal tax rate:11

The 20,000% spike at £100,000 is absolutely not a joke – someone earning £99,999.99 with two children under three in London will lose an immediate £20k if they earn a penny more.12 And the negative spike at £8,668 is because it’s at that point you qualify for the scheme – you have a huge negative marginal tax rate (which has the potential to create obvious distortions of its own).

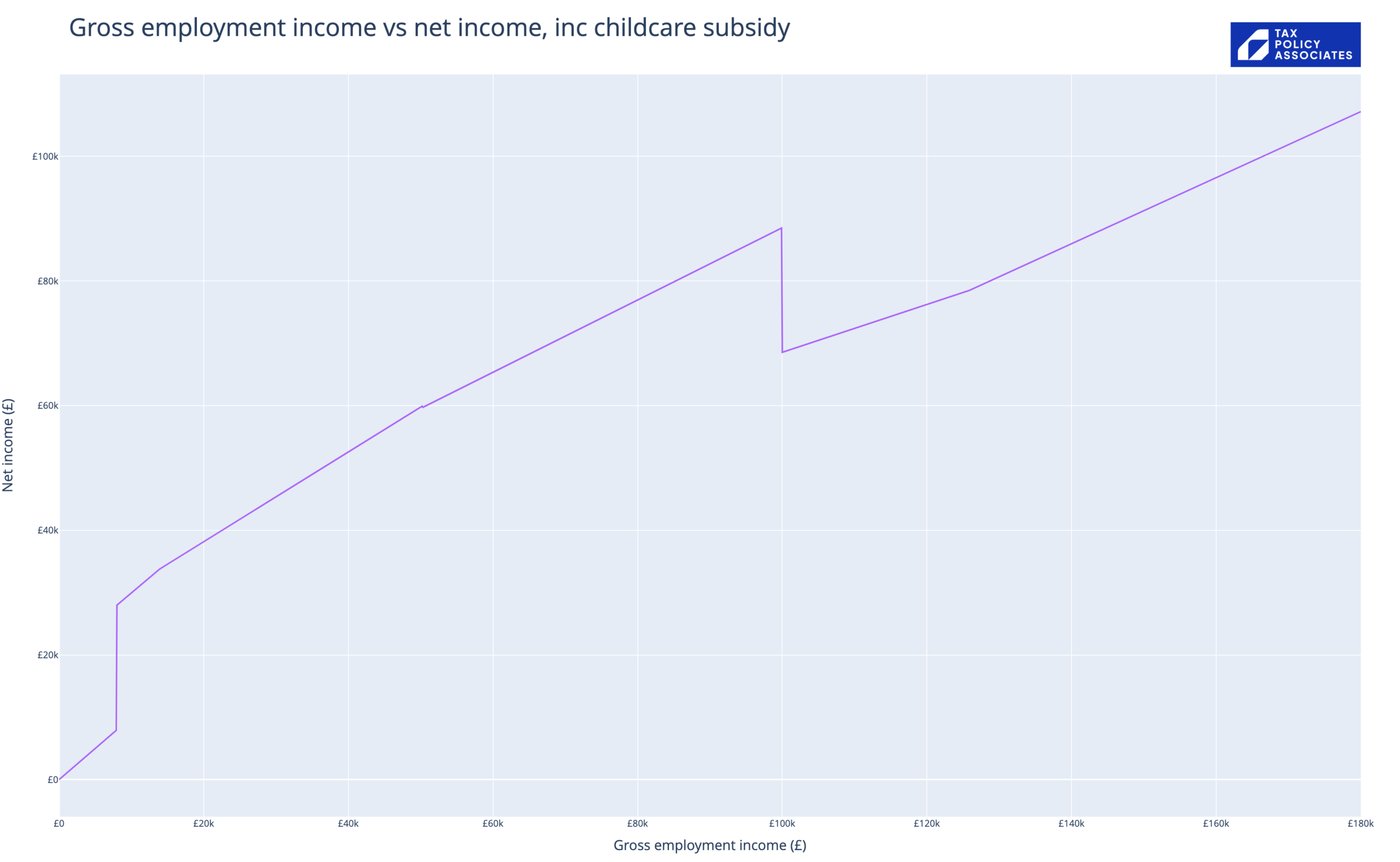

The practical effect is clearer if we plot gross vs net income:

After-tax income drops calamitously at £100k, and doesn’t recover to where it was until the gross salary hits £145k.

This is ignoring the pre-existing tax-free childcare scheme, which also vanishes at £100k. The amounts are less (usually under c£7k/child) so the curve would look less dramatic. However, as the scheme applies to children under 11, taxpayers feel these effects for many more years.

But don’t worry

If Jane started earning beyond £145k, all of these problems go away, and she has a nice straightforward marginal rate of 47% forever.13

What kind of tax system creates complexities and high marginal rates for people earning £50-125k, and simplicity and lower marginal rates for peopel earning more than £125k?

What’s the solution?

But these problems are going to get worse over time, as more and more people get dragged into the thresholds that trigger these high marginal rates. When the HICBC was initially set at £50k, that was a fairly high salary. By 2025/26, around 21% of taxpayers will earn £50k – and that’s likely what motivated Jeremy Hunt to raise it to £60k. But in these inflationary times, £60k will be the new £50k relatively soon.

In theory it’s easy: don’t add tricks and gimmicks into the tax system. If you want to raise more money from people on high incomes, raise rates or lower thresholds so you raise more money from people on high incomes.

In practice it’s hard. Scrapping these rules and making child benefit, the personal allowance, and childcare subsidies universal, would be expensive (somewhere between £5-10bn, depending on your assumptions). And the obvious way of funding that – increasing income tax on high earners, appears to have been ruled out by all main parties.

Let’s hope whoever is the next Chancellor can see these problems clearly, doesn’t make them worse, and – ideally – looks for smart solutions.

Photo by Osman Köycü on Unsplash

Footnotes

Everything interesting happens at the margin. For more on why that is, and some international context, there’s a fascinating paper by the Tax Foundation here ↩︎

Ignoring Scotland for the moment. I’m sorry, Scotland – you are included on the charts, but I can’t lie to you… it’s not pretty ↩︎

That’s the headline rate – the actual rate is different… for which see further below. ↩︎

Perhaps he is self-employed and chooses which clients/work he takes on. Perhaps he is employed, and can choose how much overtime to work, or whether to accept a promotion. Perhaps he is going back to work after time spent looking after young children. Many people have the ability to work additional hours if they wish. ↩︎

Strictly that doesn’t exist – you’re paying basic rate tax plus Class 1 employee national insurance contributions. But realistically this amounts to 28% tax. I’m going to count income tax and national insurance as if they’re one tax throughout this article. ↩︎

Strictly that doesn’t exist – she’s paying 40% higher rate tax plus 2% Class 1 employee national insurance contributions. Realistically this is 42% tax. ↩︎

Note that the marginal rate will vary depending on how we calculate it, and the size of the “perturbation” we calculate the marginal rate over. Most textbooks define the marginal rate as the % tax on the next pound/dollar of income. Say that we looked at the tax Jane paid on £60,199 of income – that would be £14,726. A £1 pay rise takes her to £60,200, and tips her into the HICBC – she now pays £0.42 more higher rate tax, plus an additional HICBC charge of 1% of your child benefit – £30.94 (assuming you have three kids). So the marginal rate is 100 * (£31.63/£1) = 3,163%. This is not very meaningful, as nobody’s incentives are going to be affected by the consequence of a £1 pay rise. It also creates the silly result that the marginal rate on her next £1 pay rise will be 42%, because the HICBC won’t increase until she gets to £60,400. So it’s better to use a more realistic figure like £1,000. The practical consequence is that the 56.5% figure isn’t *the* correct answer, but it’s a sensible and useful one, and it’s important to check that weird marginal rates aren’t just an artifact of the chosen perturbation. Our charts use a £100 marginal rate for convenience, but then “smooths” the HICBC formula so the marginal rate doesn’t leap up and down. ↩︎

I think this is an unfortunate consequence of the Green Party having a policy to forgive all student loans, and another policy to increase national insurance by 6% for everyone earning £50k+. That would be a net win for someone paying off a student loan. However at some point during the manifesto process, they relegated student loan forgiveness to a “long term objective”, but didn’t change their national insurance plan. ↩︎

Particularly when the economy is running at very little spare capacity; it would be different if there was high unemployment/plenty of spare capacity, because the work that was turned away would (at least in theory, in the long term) be undertaken by others ↩︎

The £5,000 starting rate for savings is also phased out, but very slowly, and the phasing-out seems unlikely to be relevant to many people. ↩︎

The chart is for a single earner, but if they have a partner, the partner would also need to be earning at least £8,668 (the national minimum wage for 16 hours a week) ↩︎

The 20,000% figure is a consequence of the code that produces the chart incrementing the gross salary by £100 in each step. It would be a mere 2,000% if we used the same £1,000 perturbation as above. ↩︎

Ignoring pensions, which create a marginal rate problem all of their own… ↩︎

{kind=link}

{kind=link}