The recent publication of Rishi Sunak and Keir Starmer’s tax returns brought into focus the large difference between the marginal rates of tax on employment income (47%) and capital gains tax (20% for shares; 28% for real estate). Many people propose closing this gap. But how unusual is it in an international context? What do we see if we look across the rest of the OECD?

The UK rate of income tax on dividends tops out at 39.35%, but the rate of capital gains tax on sales of shares is 20%.1 This is a large gap, and encourages significant avoidance – so I’ve suggested closing it. Some people responded by saying that other countries also had a large gap between CGT and income tax, and the UK would be an outlier if we closed it. My initial reaction was that this was wrong, but I don’t think it’s wise to ever propose tax policy changes without looking at what the rest of the world does.2 This short article therefore compares rates across the developed world.3

CGT vs income tax on dividends

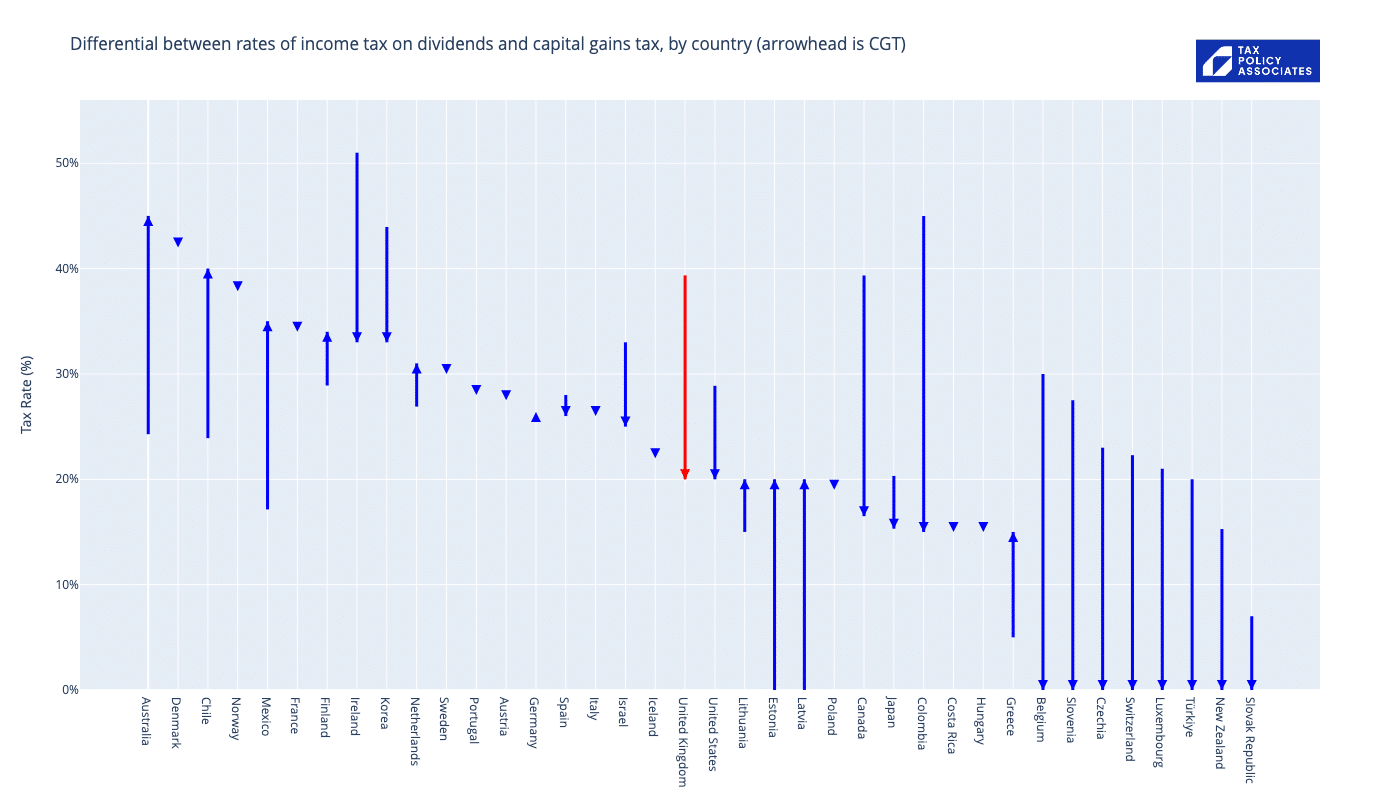

Here’s a chart showing, for each country in the OECD, the highest marginal rate of income tax on dividends and the highest marginal rate of capital gains tax on share sales. The arrowhead is the CGT rate. The tail of the arrow is the income tax rate. The chart is sorted by CGT rate.

In other words, this shows us the size of the CGT/income tax gap:

The position is rather nuanced:

- The big Continental economies – France, Germany, Italy, Spain, have CGT rates more-or-less equal to income tax rates. In that sense the UK is an anomaly.

- However whilst the UK has a slightly below average rate of CGT on shares, it has one of the highest rates of income tax on dividends. Higher than France, Portugal, Italy, Spain. Which is surprising.

- Quite a few countries have no CGT at all (arrowheads on the 0% line), although one could probably make a fair case that none of those are particularly comparable to the UK.4 I’d expect those countries have a lot of avoidance, with people manufacturing gains rather than taking dividends from private companies.

- Two countries have no income tax on dividends at all (arrow tails on the 0%) line – Latvia and Estonia. Curiously they charge CGT on shares, so I’d expect there is a lot of avoidance by taking dividends rather than selling shares in private companies.

So is it true to say the UK has an unusually large gap between the rates of income tax and capital gains tax? Somewhat, depending on whether you think the comparison should be focussed on the big Continental economies or drawn more widely.

This differential between the income tax rate on dividends and the CGT rate on shares is important when we’re thinking about the potential for avoidance, given how easy it is for owners of private companies to shift their return from dividends to capital gains. That was Nigel Lawson’s point back in 1988.

But if we increased the UK CGT rate to match the dividend income tax rate of 39.35% it would be one of the highest in the world, with only Denmark and Australia higher (and the Australian rate is halved where an asset is owned for a year or more). That shouldn’t rule out such a change, but it should make us hesitate.5

And I suspect it would be politically highly controversial to follow France, Germany, Italy and Spain, equalise the rates of income tax and CGT on dividends/shares at around 30%. It would be seen by many as a tax cut for the rich, and that would probably be correct.6

CGT vs income tax and NI/SS on employment income

As a tax lawyer, I start by looking at the problems of avoidance and economic distortion caused by a large income tax/GGT rate differential. However, often people are making a more political point: that it’s inequitable to tax capital gains so much less than employment income. That’s most often an argument associated with the political Left, but even a technocratic centrist like James Mirrlees argued that the combined rates of corporate and shareholder taxation should equal the tax rates on employment income.7

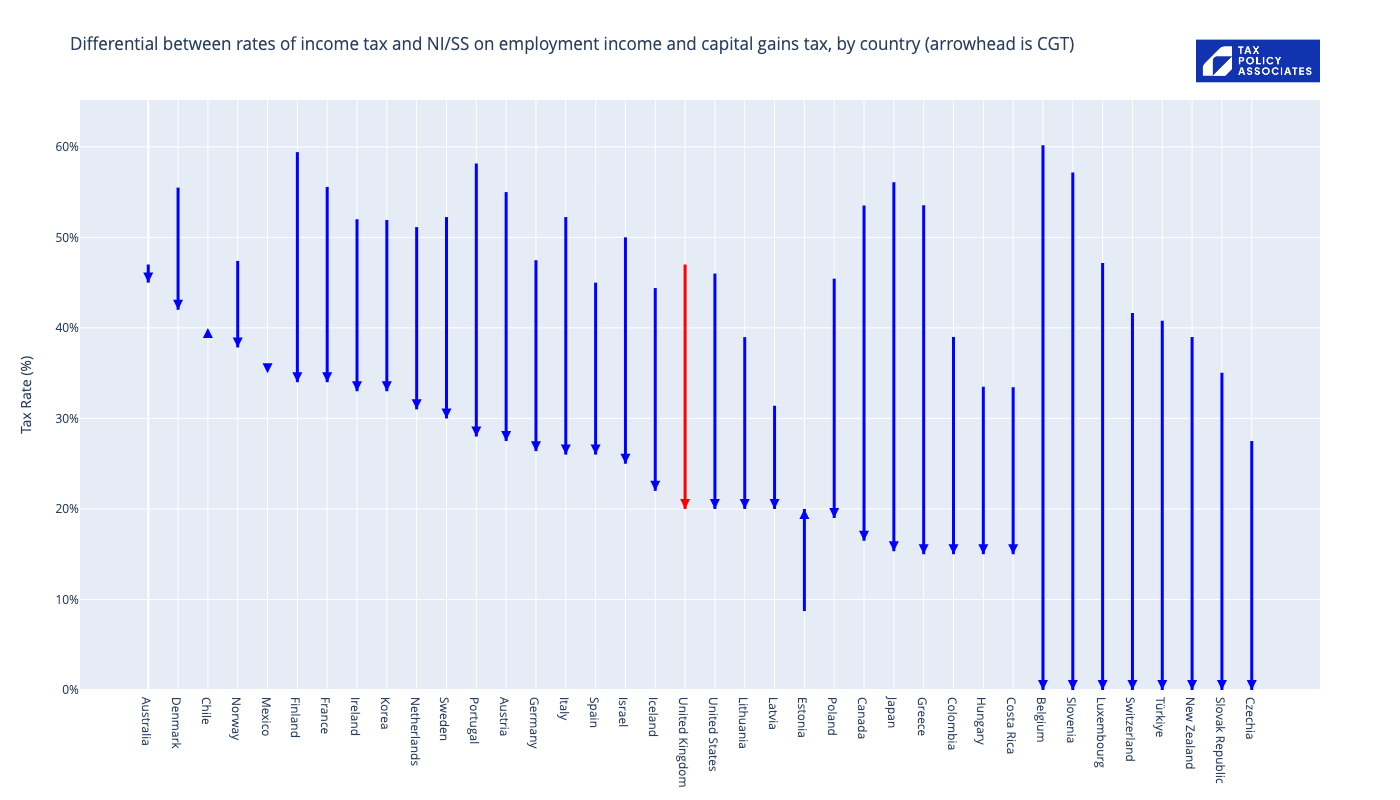

What if we take the chart above, but instead of comparing CGT with income tax on dividend income, we compare it with tax on employment income, i.e. income tax and national insurance/social security?

This is a dramatically different picture, as almost all countries tax employment income significantly higher than investment income, and therefore almost all the OECD has a big differential between CGT and tax on employment income.8 Once we include national insurance/social security, the UK’s differential looks unexceptional (particularly compared to the likes of Belgium – 0% CGT vs 60% tax on employment income!).9

The UK would therefore be an outlier if we equalised CGT and income tax on dividends at the employment income marginal rate of 47%. We’d have the highest rate of CGT in the developed world, which doesn’t feel like a great idea. I find this an uncomfortable conclusion, given the avoidance and distortion that results from taxing different types of income at wildly different rates.

I still believe we should increase the rate of UK capital gains tax, but I’d probably be cautious at going much above 30%, although if indexation (allowance for inflation) is reintroduced then perhaps we have more scope.10 But in a world full of crazy and inequitable tax systems, perhaps we have to be careful not to be too sane.

The data and code that created the charts is here.

Notes on the underlying data:

- The tax rate on dividends is the highest marginal combined national/state rate taking account of imputation systems, tax credits and tax allowances. Source is the wonderful OECD tax database, column K.

- The tax rate on labour income is the highest marginal rate of combined national/state, including employee social security/NI (but not employer rates). Again the OECD tax database is the source – see the “all in rate” column F.

- The CGT rate is the highest marginal combined national/state rate on shares. Source: this helpful table from PwC and Tax Policy Associates research.

- Note that these are rates for local residents. Some countries (e.g. France) in principle tax foreigners on local gains (although tax treaties mean in practice this rarely applies). Other countries like the UK/US only tax local residents on gains in stock/shares.

Footnotes

In principle both rates reflect the fact that a company’s profits are subject to tax at 25% – that means the effective rate of tax on dividends from a UK company can be as 54%, if the dividend is entirely paid out of taxable profits. However using the 54% figure would be misleading for two important reasons. First, dividends aren’t always paid out of taxable profits (in some circumstances you can borrow to pay a dividend). Second, UK resident individuals receive dividends from countries all over the world. The 54% is relevant only to where a UK resident individual receives a dividend from a UK company. This will in practice be a minority of cases. The same is true for most other countries, and therefore it would be misleading to present each country’s rate of tax on dividends adjusted to reflect that same country’s rate of corporate tax. ↩︎

Both in terms of being informed by their experiences and because of the inevitable-if-controversial spectre of tax competition. It is absolutely possible to make the case that the UK should have a tax system that’s very different from the rest of the world but, if one does so, it’s important to understant that this is what you are doing, and consider the implications. ↩︎

It therefore doesn’t include countries like Singapore and the tax havens, who are not OECD members. ↩︎

Switzerland is interesting, because whilst it has no CGT it does have a wealth tax, raising about 1% of GDP – by comparison the UK raises about 0.5% of GDP from CGT, and most countries raise much less. Given the concentration of financial wealth in Switzerland it is likely that the Swiss system as a whole ends up significantly under-taxing wealth. ↩︎

It’s sometimes proposed we increase the rate to 57%. That would be significantly higher than any other country. ↩︎

i.e. because I expect the revenue gains from increasing the rate of CGT would be smaller than the revenue losses from reducing dividend tax. ↩︎

See e.g. Tax by Design, page 474. ↩︎

It’s even more dramatic if you bring employer national insurance into it. On the face of it that would make sense, given that in the long run most of the economic incidence of employer national insurance falls on employee wages. But in the short term it doesn’t, and therefore marginal rates (and the charts in this article) don’t include employer taxes. Suffice to say that for almost all countries including employer taxation would materially expand the delta between rates of tax on labour income and CGT ↩︎

Anecdotally, this leads to a large amount of planning/avoidance by those on high incomes, so that the apparently high income tax rate in France, Belgium etc tends to be paid by the middle classes and not the very wealthy. However I am not aware of any data on the subject (and anecdotes from tax lawyers are inevitably unrepresentative and should be treated with caution). ↩︎

People used to complain indexation was too complicated; in the days of online tax return that should no longer be an issue. The advantage of a higher rate plus indexation is that we are (effectively) reducing the rate for “real” longer term investors, but not for people who magically turn income into gains. The analysis really requires us to look at how inflation is catered for in other countries’ tax system; I believe most countries don’t have any indexation allowance, but I’m not aware of any centralised resource on the subject. So this would be a reasonably sized project, but one which is worth doing. ↩︎

What would a land value tax actually do?

What if Andy Burnham lowered the mansion tax threshold to £1.5m?

The history of UK capital gains tax in five charts

Has Britain run out of “other people” to tax?

The UK has 90 different taxes. France has 348. Germany has 60. Why?

Leave a Reply