The Conservative Party has just proposed moving the point at which child benefit is phased out from income of £60k to £120k. This will greatly reduce the marginal rate for parents earning £60-80k. But it means that a parent earning £120k who has three children will face a 70% marginal rate. And they’ll face a long stretch of earnings (£100k to £160k) with a marginal tax rate of over 50%.

The Conservative Press was released at 10.30pm on Thursday 6 June 2024 – we’ll link to it if it’s published online, but for the moment there’s a copy at the end of this article.

Our income tax system is a mess of awkward gimmicks, bodges and compromises. One of the worst is the “high income child benefit charge” (HICBC), which claws back child benefit once your income hits a certain threshold.

The HICBC

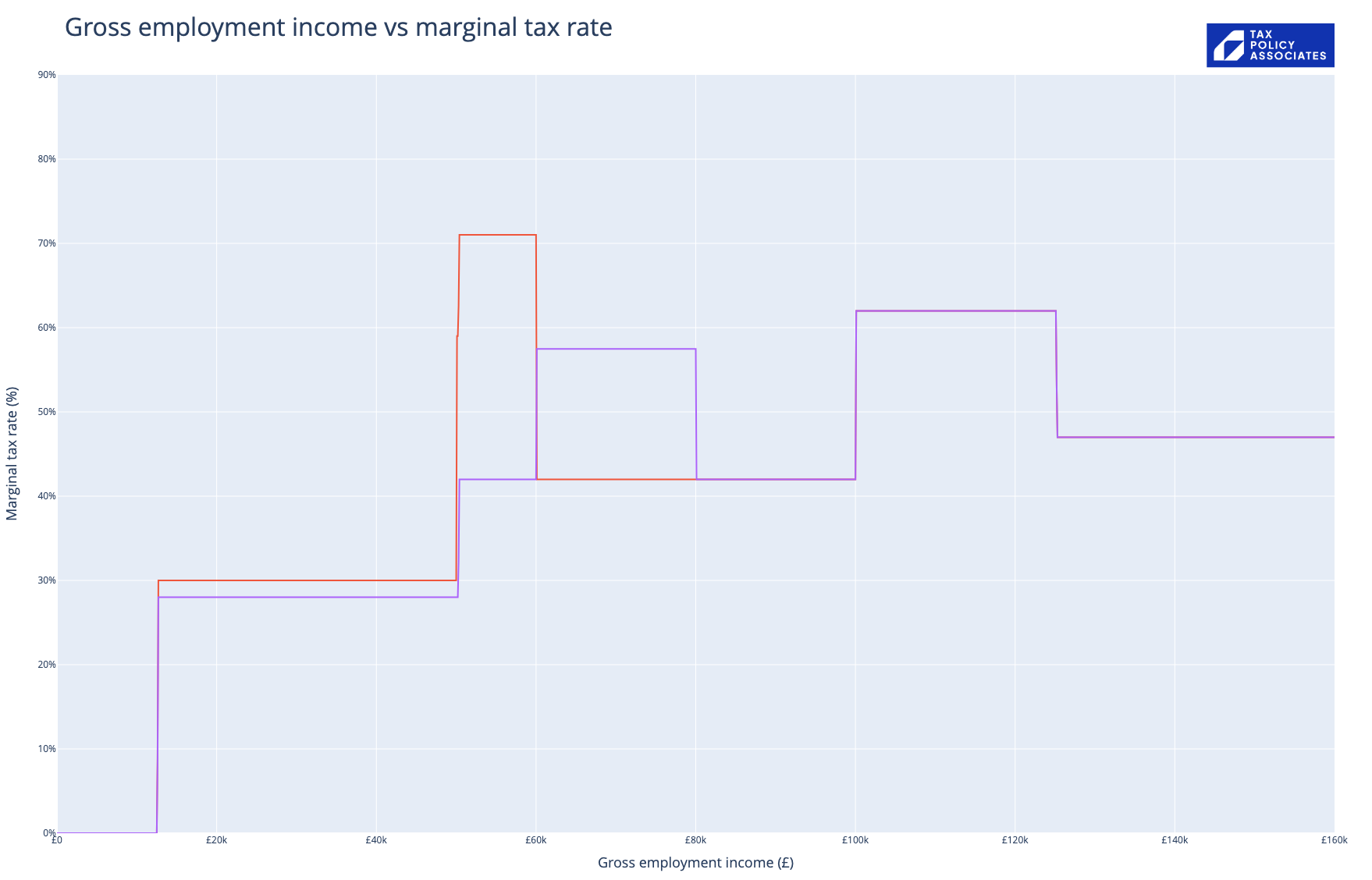

Until the 2024 Budget, the HICBC meant that a family with three children where the highest earner was on £50k faced a marginal rate of tax of 68%.

The “marginal rate” is the rate of tax on the next £ earned – it’s important because it affects the incentive to work. It’s slightly counter-intuitive, but marginal rates can be more important than headline rates and overall/effective rates. If my overall rate of tax is 20%, but I’ll be taxed 100% on the next £1,000 I make then I’m unlikely to want to work for that extra £1,000.

The HICBC was, therefore, a problem (with other serious practical issues too, which we discuss here). So Jeremy Hunt deserves credit for making it significantly less awful in this year’s Budget. He moved the HICBC phasing so instead of applying on incomes from £50k to £60k, it applies from 6 April 2024 to incomes from £60k to 80k. That reduced the marginal rates for a parent with three children under 18 to from 71% to 57%:

Red is before the Budget; purple is after.

There’s a more readable interactive version here, that lets you play with and compare all the rates discussed in this article – you can click on the legend to select different scenarios, finger/mouse over to see exact figures, and zoom in/out of details of the chart. The code that creates the marginal rate charts is available on our github.

The new Tory proposal

The Conservatives have just put out a press release (copied below). They say their manifesto will move the HICBC phasing out to £120k-£160k. That’s good news for people earning £60k – their marginal rate drops right back down to 42%.

However, this creates a new and very high marginal rate of 70% for parents with three children under 18 earning between £120k and £125k:

(Purple is after the Budget; blue is today’s announcement)

Why? Because the personal allowance clawback already creates a 62% marginal tax rate for everyone earning between £100k and £125k. And the Tories are moving the child benefit clawback so it partially overlaps with the personal allowance clawback.

The 70% rate is bad but temporary. The more serious effect is that, once earnings get past the £125k point, there’s a 55% marginal tax rate all the way up to £160k (after that, the marginal rate reverts to the standard 47%). Of course these rates will be less for people with less than three children under 18, and higher for people with more.

This all feels like a big mistake.

They also want to move the HICBC so instead of applying by reference to the highest earner in the household, it applies to the overall household income. This isn’t a surprise – the Government announced it in the Budget. Problem is, the tax system doesn’t track household income. Married couples used to be taxed on their joint income – that was scrapped⚠️ following a decades-long feminist campaign for independent taxation. There’s an almost unanimous view amongst tax policy wonks that this change will be technically complex and in some cases cause hardship.

It’s true that applying HICBC to the highest earner is often unfair – a couple each earning £49k aren’t caught, but a couple with one not working, another earning £60k are caught. But any change needs to fully think through the new unfairnesses that it will create, and I fear the Government, and the Tories, haven’t done this.

So what?

Why does it matter if people earning £120,000 pay a 70% marginal tax rate, and those earning £125k-£160k pay a 55% marginal tax rate?

- First, because going past the 50% mark is psychologically significant, and this change creates a long stretch of the tax system (£100k to £160k) where the marginal rate is over 50% for people with three children under 18.

- Second, because it’s irrational. It’s perfectly reasonable to support a 55% tax rate on high earners. It’s not reasonable or rational to have a 70% or 55% marginal tax rate on a particular segment of high earners earning £120k-£160k, but 47% on those earning more than £160k.

- And both these factors mean that some high earners, who often have control over how, when and where they work, have a reduced incentive to work in the UK. That’s not good for growth.

This is the problem with gimmicks like the child benefit and the personal allowance clawback. They’re introduced as cute tricks to avoid increasing the headline rate of tax. They then become more and more significant over time, capturing more and more taxpayers… and therefore become more expensive to remove. And tweaking them without repealing them altogether is complicated by all the other gimmicks in the system.

The answer is to end the gimmicks.

Original text of Conservative Party press release

EMBARGOED STRICTLY NO APPROACH: 2230 Thursday 06 June 2024

Conservatives pledge £1,500 tax cut for parents

· Threshold at which families pay the Child Benefit Tax Charge will rise from £60,000 to £120,000

· Major reform to the Child Benefit system to make it fairer by treating parents as households rather than individuals

· 700,000 families will benefit by an average of £1,500 from this tax cut

The Conservatives will cut taxes for 700,000 families by an average of £1,500 as Labour continue to refuse ruling out tax rises of £2,094 per working household to plug their financial black hole.

We will do this by raising the threshold at which people start to pay the High Income Child Benefit Tax Charge (HICBC) to £120,000, up from £60,000 currently.

And to end the unfairness that means single earner households can start paying the tax charge when a household with two working parents and a much higher total income can keep Child Benefit in full, we will move to a household rather than individual basis for assessing the tax charge.

Single-earner households and households where one individual earns substantially more than the other will be the biggest beneficiaries.

The announcement underlines the Conservatives’ commitment to rewarding aspiration, boosting households’ financial security and incentivising work by allowing hard-working families keep more of what they earn.

It builds on our tax-cutting plan announced in April to raise the threshold at which individuals start to pay the Child Benefit tax charge from £50,000 to £60,000.

These changes have taken 170,000 families out of paying the tax charge, and mean that almost half a million families gain an average of £1,260 to help with the cost of raising their children this year.

Chancellor of the Exchequer, Jeremy Hunt said:

“Today we have announced a £1,500 tax cut for parents to boost families’ financial security and give them more money to spend on the things that matter most.

“Raising the next generation is the most important job any of us can do so it’s right that, as part of our clear plan to bring taxes down, we are reducing the burden on working families.

“There is a clear choice for voters at this election: bold action to cut taxes for working families under the Conservatives, or a £2094 tax rise to fill Labour’s £38.5 billion spending black hole”.

The pledge is fully funded, paid for by clamping down on tax avoidance, which is expected to raise a total of £6 billion. Labour have said they would raise a similar amount from tax avoidance, but have said they will spend it on other things.

Notes to Editors:

Costing and funding

· Our policy to end the unfairness of the High Income Child Benefit Charge has been fully funded and costed. Increasing the threshold to £120,000 and the taper rate to £160,000 will cost £1.3bn in 2029/30. It will be paid for by our previously announced plan to raise £6 billion from further clamping down on tax avoidance and evasion. So far, of this £6 billion we have committed:

o £1 billion for National Service

o £2.4 billion for the Triple Lock Plus

o £60 million for 30 news towns

· The Labour Party has said it will raise £5.1 billion from tax avoidance and evasion by the end of the Parliament. It has decided to spend this money on other things.

In April 2024, the Conservatives reformed the High-Income Child Benefit Charge, cutting tax for half a million families:

· In April, the Conservatives reformed the High-Income Child Benefit Charge, cutting tax for nearly half a million families. As of April 2024, the Conservatives raised the threshold for the High-Income Child Benefit Charge from £50,000 to £60,000 and halved the rate so that it is not paid in full until you earn over £80,000 – estimated to support nearly half a million families with an average gain of up to £1,260 in 2024-25 towards the costs of raising their children (HM Treasury, Spring Budget, 6 March 2024, link).

· Reforms to the High Income Child Benefit Charge are predicted to boost economic growth and support jobs across the country. The OBR estimated that the changes to the HICBC we introduced this year will increase economic growth and increase the average hours worked by workers employees by an amount equivalent to 10,000 full-time employees (Office for Budget Responsibility, Economic and Fiscal Outlook, March 2024, link).

However, the current system is still unfair, which is why the Conservatives have set out a clear plan to deliver the support working families across the country need:

· We will end the unfairness of the High-Income Child Benefit Charge by moving to a system based of households, cutting taxes for 700,000 households by an average of £1,500 per year. We will ensure that the High-Income Child Benefit Charge is only paid by households with a combined income of more than £120,000 per year and increase the threshold at which Child Benefit is fully withdrawn to £160,000 per household.

· Following consultation, we will legislate and deliver these changes by Autumn 2025. Moving to a household basis requires significant reform to how HMRC administers the High-Income Child Benefit Charge and so we will first launch a consultation to resolve the key design issues to deliver the new system by April 2026.

Image by DALL-E 3⚠️ – “a children’s buggy overflowing with pound notes”

A tax reform agenda for tomorrow’s Chancellor

Our take on the Reform UK manifesto

Our take on the Labour manifesto

Our take on the Green Party manifesto

Leave a Reply