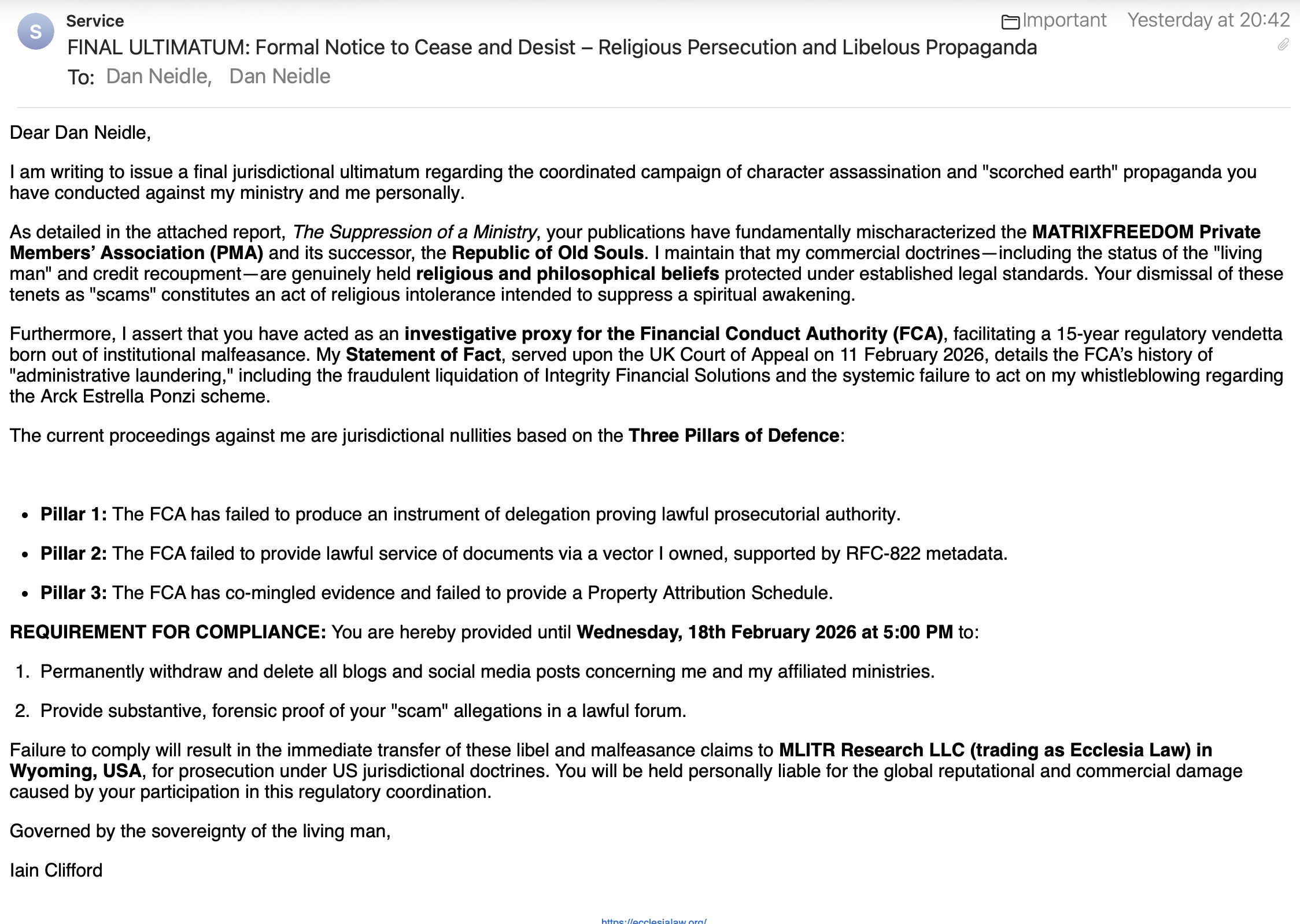

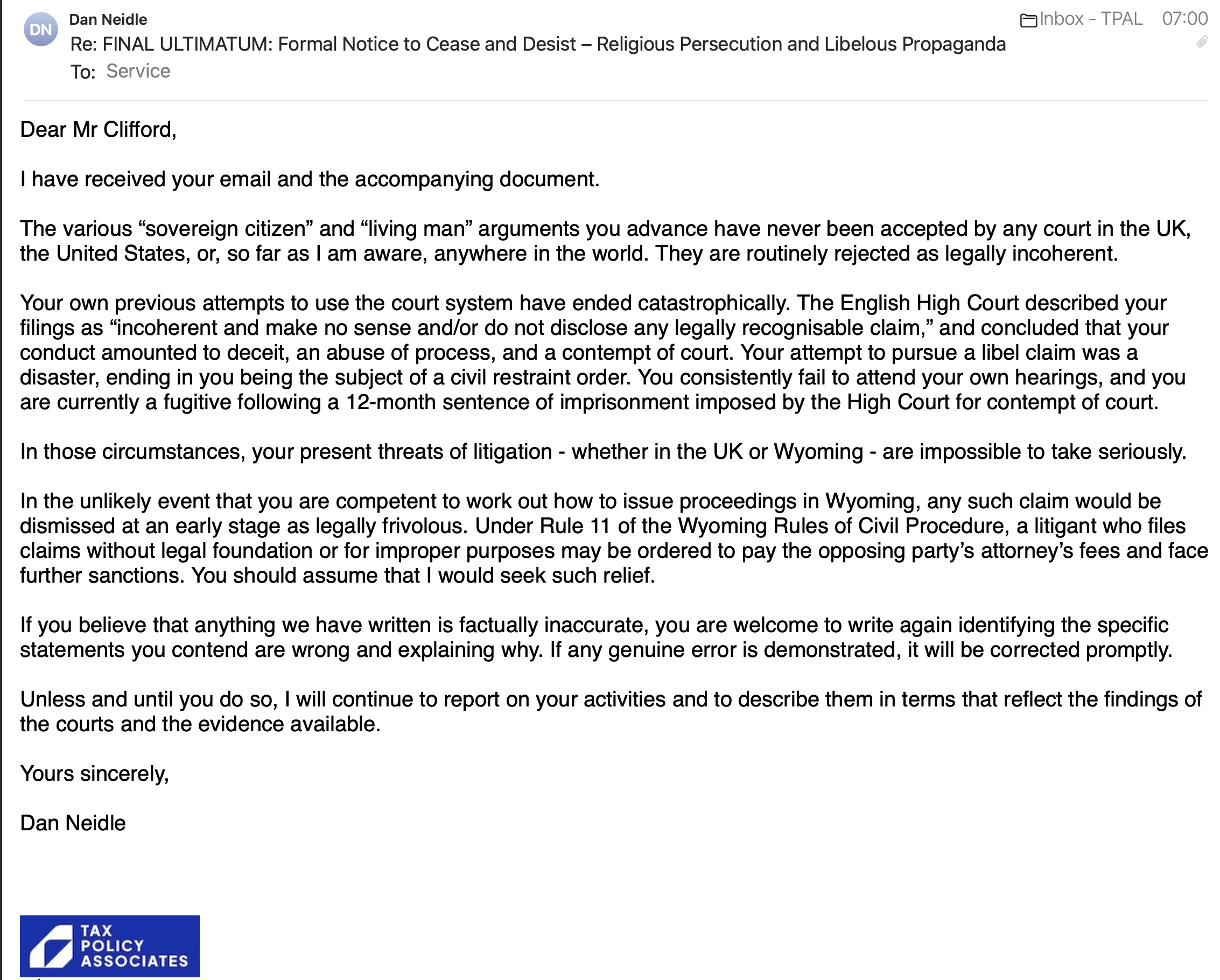

The UK loses £1bn each year to fraudulent claims for research and development (R&D) tax relief. We revealed last week that one of the largest firms in the market, Green Jellyfish (and its associated firm Kirby & Haslam), made fraudulent claims. We can now reveal in detail how the fraud worked. We believe they’re responsible for over £100m of fraudulent claims.

Unqualified sales people cold-called businesses with no R&D (like carpenters and care homes), and promised them R&D relief would be available. “Technical writers” – none of whom had any relevant experience or qualifications, and many of whom had creative writing degrees – wrote reports justifying the relief. The employees were given briefings with examples of supposedly valid claims. But those briefings were false – none of the example projects actually qualified.

We are today publishing the details of how Green Jellyfish, Kirby & Haslam and other “Impact Group” companies worked from the inside, together with their internal briefing documents.

Update: there have now been arrests. Comments on this post are closed.

The claim: an expert team

Green Jellyfish promised their clients they had a team of expert R&D specialists.

This is from a promotion sent by Green Jellyfish to care homes in 2022, talking about their team of “Tax Specialists”:

This is from their website and LinkedIn pages (as of 23 August 2024) – “we are the R&D tax experts”, a “team of specialists” and “a team of Research and Development Tax Specialists”:

And this email to a client (in 2022) talked about “an FCA regulated team of experienced experts in this field”.

The reality – zero expertise

We have not found a single Green Jellyfish or Kirby & Haslam employee with any background in tax, accounting, law, science, or technology.1

We identified ten Green Jellyfish technical writers using open source materials, and metadata from our dossier of the company’s R&D claims. In most cases they were hired straight from university. In other cases they had unrelated previous experience.

Here are typical examples:2

The cold-calls to clients, in which clients are assured that R&D tax relief will be available, came from “business development executives” (BDEs). Successful leads were passed to “business development managers” (BDMs) who would have telephone meetings with the clients.

This was a large team with high turnover- we’ve identified over 50 individuals who worked in this role for Green Jellyfish from 2021. They typically had a sales background, but none had any expertise in any legal, accounting, tax or technical area:3

So this was a team with zero expertise. Clients were lied to.

The employees’ story

We have been speaking to current and former Green Jellyfish employees. We have verified their employment from LinkedIn, historic emails, and document metadata.

Their stories are consistent, and paint a picture of a business that worked like this:

The sales teams

- The business development executives (BDEs) cold-called clients and sent follow-up emails which (without exception, as far as we’re aware) said the BDE was confident a claim could be made.

- They would target different sectors on different days, obtaining company details from Companies House and then looking up phone numbers on Google. For example: two days electricians, then plumbers, then bricklayers, groundworkers, pubs etc. The one thing these sectors had in common was that they were highly unlikely to qualify for R&D tax relief. Two sources have told us they believe that was intentional: it meant Green Jellyfish wouldn’t be competing with other advisers.

- Potential leads were passed to business development managers (BDMs) for follow-up calls. There were about 15-20 BDEs at any one time, and 10-15 BDMs. As we note above, none of the BDEs or BDMs had any technical background or experience.

- The BDMs asked clients about their business in very general terms, and were supposed to identify “innovative projects”. The BDMs were given lists of example qualifying R&D expenditure (see below), but in practice BDMs almost always said R&D relief was available.4

- The BDMs sent a follow-up email to the client confirming that relief would be available, and asking for copies of the client’s accounts and corporation tax return. There would normally be nothing in writing from the client or the BDM setting out the details of the project.

- The BDEs and BDMs saw this purely as a sales job, and had no understanding of the legal requirements, or the consequences of wrongly claiming tax relief.

- Several BDMs/BDEs have told us they were given the initial explanation that almost everything qualified for R&D tax relief if you worded the claim correctly.

- BDEs and BDMs were under huge pressure to meet sales targets. There was rapid turnover of the BDE and BDM teams (unusually high even by the standards of junior sales jobs).

- Some of the BDMs relied heavily on ChatGPT to write their notes.

- That was particularly the case when, later on, BDMs were hired in the Philippines and South Africa – they heavily (one source thought “exclusively”) wrote to the technical report team using ChatGPT.

The numbers

- The BDMs would put numbers together for the tax relief claims based on the clients’ accounts and corporation tax returns.

- Sometimes this followed a discussion about potential R&D projects. Often it didn’t.

- We have seen multiple emails from BDMs to clients saying that they would establish the qualifying R&D expenses by looking through the company’s accounts and tax returns. Qualifying R&D expenses cannot be calculated in this way – individual projects must be identified.

- Several sources5 have told us that the BDM team would have “industry standards” of the amount they could claim for each sector – for example 20% for care homes. Later they would adjust percentages slightly so the numbers didn’t look too round, for example 20.21%. Later still, different percentages were used for different categories of expense. If our sources are correct, this would be blatant fraud. We would, however, caution that (unlike most of the other information provided to us by our sources) we have no documentary evidence to directly support this claim, and our sources could be mistaken or exaggerating. However we have noted many of the claims in our dossier are almost-round percentages of the company’s expenses.

- Our sources have different views on the total volume of claims made by Green Jellyfish, but they all agree the total must be more than £100m. We believe that’s consistent with Green Jellyfish’s accounts. 6

- HMRC are now very alert to refund claims. Several sources told us Green Jellyfish had been “blacklisted” by HMRC, and no refunds would be made when Green Jellyfish was the agent. One solution was to use affiliated entities. Another was to find businesses who were about to submit corporation tax returns, and make last minute changes to add large amounts of R&D tax relief – HMRC would then have no idea any R&D agent had been involved. (We would caution accountants to be alert to this.)

The technical team

- Sometimes a BDM sent a note of their call with the client to the team of “technical writers” to prepare a report.

- A report was required after August 2023, when HMRC tightened claim procedures. Before that, the technical team were only involved in some cases (we believe, but aren’t sure, it’s where there was a more realistic identifiable R&D project). More often, the claims were like Sophie’s, where a claim was submitted without a report (but a report produced much later if there was an HMRC enquiry).

- The technical writers were formally employed by Kirby & Haslam, not Green Jellyfish, but in practice the two companies operated as one business.

- As we note above, most of the “technical writers” were hired straight out of university with no prior experience. Many had English literature and creative writing degrees; a few had other Arts degrees. None had any prior R&D, legal, accounting or tax experience.

- Two of the “technical writers” were referred to as “R&D Tax Specialists” by BDEs on client calls within a few weeks of starting work for Green Jellyfish.

- The technical writers realised quite quickly that there was nobody around with any tax qualifications. The BDMs and BDEs sometimes did not realise this, and one we spoke to appears to have genuinely believed that the technical writers were experts.

The reports

- We have seen images of notes sent by BDMs to the technical writers. We aren’t publishing them because of the risk our sources could be identified – but we would describe the text as poorly written half-descriptions of a standard care home business. We believe we can link one to a case where a six figure sum was claimed from HMRC (and later had to be refunded, with penalties).

- It was made very difficult for the technical writers to refuse to write reports based on the BDM’s notes. If they could not write a report, the claim would go to HMRC anyway, pre-Aug 2023 (after that, the rules were tightened and additional information specifying the R&D had to be provided to HMRC).

- The technical writers were dissuaded from telling BDMs that claims did not qualify for tax relief – this was considered “aggressive language”.

- Some of the BDMs referred to the technical writers as the “sales prevention department”.

- We have now seen many reports prepared by the technical writing team. We have not seen one which actually meets the conditions for R&D tax relief.

The group structure

- The business was run day-to-day by Daniel Robinson and Scott Herd, with Steve Christophi known to be involved at board level, but rarely seen.

- Several of our sources commented on the obscure group structure, with the BDMs in a different company from the technical writers. They thought this to make it easier for the technical writers and BDMs to blame each other for poor quality claims.7

- There was also a “legal team” made up of recent law graduates. They were called “paralegals” but this was not accurate – the term “paralegal” usually means someone with legal training working under the supervision of a qualified lawyer. So far as we are aware, there were no qualified solicitors or barristers working for Green Jellyfish or any of the associated entities.8 The paralegal team got involved when HMRC opened an enquiry into a Green Jellyfish claim. We have also seen a number of legal letters and emails drafted by the “paralegal” team. The letters rely heavily on Google and show signs of being written by ChatGPT or a similar LLM.

The junior personnel working for Green Jellyfish had an appalling experience in a very hostile environment. We don’t see them as morally or legally responsible for the false R&D tax claims. At least two made anonymous reports to HMRC. The blame lies with those who hired staff with no experience and fed them false information, knowing that clients would be misled.

The fake training materials

Green Jellyfish gave the business development and technical writing teams examples of what they said were valid R&D relief claims; these were sometimes also given to clients to “help them identify” qualifying projects.

The legal position is that R&D tax relief is only available for “research and development”. That term is defined in guidance published by BEIS/DIST and given statutory force under the Corporation Tax Act 2010. HMRC accurately summarise the rules as follows:

Here’s Green Jellyfish’s list of examples of R&D projects run by care homes (PDF here):

As a general proposition, the prospect of any care home having qualifying R&D relief is highly unlikely. A care home and its staff may be very innovative in how they plan and deliver care, but it is hard to see how they will ever look for “advances in science and technology”.

But, despite this, care homes were a key market for Green Jellyfish. Two of our sources estimated that care homes made up 40% of Green Jellyfish’s business and 25% of the group companies’ business.

In our view it is clear that none of the examples in this list are valid:

- Some are not science and technology at all: e.g.: “Manage and control symptoms of dementia through a wide range of interior and exterior designs” and “Management of a specialised outdoor garden design to mitigate common dementia symptoms”

- Others are just using existing technology, e.g. “new software… installation of sensors… to optimise the delivery of care services and… in particular, the detection of symptoms relating to diabetes, addiction, and dementia”, or “create a data analysis tool that can detect and recognise dementia traits”.

- Some of the projects would qualify, but it’s implausible a care home would ever have the expertise, resources or facilities to carry them out. Seeking to “advance the field of clinical neuroscience” or “advance the scientific field of neurology” are realistic objectives for a hospital or laboratory, but not a care home.

Green Jellyfish also gave their staff and clients this document, again focusing on care homes (PDF here):

The summary of the qualification criteria are reasonably accurate. We believe anyone with an accounting, tax, legal or technical background reading these paragraphs will realise immediately that care homes usually won’t undertake “research and development”. But nobody in the business development or technical writing team had that background.

In our opinion the examples are, once more, all clearly invalid:

- “Developments in care plans” are not an advance in science and technology. Green Jellyfish seem aware of this, by adding the caveats “if the specific care plan is an advance in science or technology” and “and is not easily deducible by a competent professional within the field”. But we don’t believe any care plan can be an advance in science or technology, and given it’s devised by professionals in the ordinary course of their business, it will be “easy deducible”. The caveats look like someone was trying to cover their back.

- “IT software designed by organisation for bespoke needs of clients/ carers”. Software will only in exceptional cases be an “advance in science or technology”.9 Realistically, care homes will use existing platforms and technology with minor modifications.10

- “Use of AI for service standardisation, operations, and capture of new symptoms within patients”. We doubt any care home will develop its own AI systems. It is much more likely it uses existing platforms such as OpenAI/chatGPT – and that will not be an “advance in science and technology”.

- “Development and implementation of biosensors and trackers in clothing of residents and carers to monitor changes in health”. We very much doubt the care homes are developing biosensors/trackers. They will be buying off-the-shelf products. That is not an advance.

- “Technology suppliers in the sector (e.g., Birdie) during COVID-19: e.g. partnering… with NHSX for Techforce19 to build the NHS111 symptom tracker into the Birdie app”. Integrating an existing service into an app is obvious, and not an advance in science or technology.

- “Revolutionising technology relating to medicine (trying to mitigate medicine waste)”. It is not plausible a care home has the equipment, resources or staff to “revolutionise technology”.

- “Improving or creating technology to address a specific scientific or technological problem within the care sector”. This is so vague as to be meaningless.

- “R&D within risk assessments – creating a plan that is able to reduce the potential for harm or risk”. Creating a plan is not a scientific or technical advance.

- “Innovation in approaches to Dementia care (or other neurological conditions), especially the use of activities and tools to aid recollection”. Using activities and tools is not a scientific or technological advance.

The more detailed “specific client examples” in the documents are, again, invalid:

Implementing behaviour strategies is not an advance in science and technology. Developing a computer programme is not usually an advance in science and technology (unless e.g. it goes “far beyond routine adaptation of existing technologies“). “Recording a person’s behaviour in real time” sounds routine, and not much like an advance at all.

Video interviews and streamlining recruitment are not advances in science and technology.

Designing gardens for people with dementia is not an advance in science and technology, and a garden designer is not a competent professional in the field of neurology.

Advancing the scientific fields of neurology and neurobiology absolutely could be a scientific advance qualifying for R&D relief, but we are very doubtful any care homes have the resources, expertise or budget for neurology research.

The game is given away by the second bullet point. A highly experienced nurse is providing care; he or she is not making scientific advances, and is not a competent professional in the fields of neurology and neurobiology.

The use of the term “neurobiology” is particularly silly. Neurobiology is the study of nerve cells at the molecular level, requiring a sophisticated laboratory. We expect the author didn’t know what the term meant.

These examples corroborate what we were told by current and former Green Jellyfish employees – that they were instructed that almost everything qualifies for R&D tax relief, provided the claim is worded correctly.

These instructions, and the lists of examples misled Green Jellyfish staff and their clients. We think this was intentional.

Who ran Green Jellyfish?

The different entities involved in the business have a variety of different owners, in some cases changing entity and owners over time. Back in 2023, all were listed as part of the “Impact Group”; today they are more shy about admitting that the entities are linked.

Three names come up again and again when we speak to current and former employees.

- Steve Christophi, who owns Kirby & Haslam. He is not listed as a shareholder or director of Green Jellyfish, but he was described as a “stakeholder” in internal communications, and our sources report that he was one of those running it. It is notable that, when Paul Rosser wrote about Green Jellyfish, it was Steve Christophi who went to talk to Paul about it (Christophi’s version) or intimidate him (Paul’s version).

- Daniel Robinson was listed as “managing director” of the Impact Group in 2022 and 2023. He was the registered owner of the previous Green Jellyfish entity and today, according to our sources, acts as the CEO of the group. He is currently the owner of Impact Business Partnerships Ltd, which appears to act as a kind of holding entity for the group.

- Scott Herd was listed as the “Non-Executive Chair” of the Impact Group in 2022 and 2023, and described as “a crucial board member at one of the leading R&D tax credit firms in the UK”. He was previously a director of the current Green Jellyfish entity.

Others are undoubtedly responsible. Paul Rosser researched a structure diagram which reveals other names; we will be writing more on this soon.

Green Jellyfish’s response.

We asked Green Jellyfish to comment on the documents and the evidence of their unqualified staff and unethical business practices. We also warned Messrs Robinson and Herd that we would be naming them in this article:

Green Jellyfish’s lawyers, Fladgate, are still acting. However, despite the seriousness of the allegations, we received a response from Green Jellyfish rather than from their lawyers. This is surprising given the seriousness of the allegations we are making.

The response complains about our timetable, makes a series of irrelevant claims about Steve Christophi’s peculiar visit to Paul Rosser, demands that we review a recording of that visit (we are unaware a recording exists), and demands “specific, detailed questions and concrete evidence to substantiate [our] claims”. They refuse to respond until we do this.

Our response was as follows:

Evidence of fraud

One explanation is that this was all an accident. That those running Green Jellyfish and its other affiliates were acting in good faith, but completely misunderstood the law. They thought all innovations qualified for R&D Tax relief, hired the wrong staff, created wrong examples, and so forth. It would follow that, whilst they were responsible for a large number of incorrect R&D tax relief applications – they did not know that would be the outcome, and no question of fraud arises.

We find this explanation implausible on its face.

As we have mentioned above, we believe that anybody with any appropriate experience would realise that the guidance provided to the staff was (and Steve Christophi, one of those who run the company, is a chartered accountant).

And even if we (charitably) assume Christophi, Herd and Robinson started out acting in good faith, they surely would have realised something was going on when they started to see HMRC challenge their claims and explain very clearly why the claims were being challenged.

At this point an honest person would stop and ask whether there was something in their procedures which was resulting in so many failed claims.

But there is no sign that this happened. Our sources suggest that things actually got worse, not better, as HMRC tightened up its procedures. Even by the sorry standards of cowboy R&D claims firms, this was extraordinary.

It is therefore our view that those in charge of Green Jellyfish (who we believe were Christophi, Robinson and Herd) knew that false R&D claims were being made, and knew that they were misrepresenting the nature of their team to clients. If they were “dishonest” then this amounts to a fraud on their own clients, and on HMRC.

Dishonesty

Whether Green Jellyfish’s leadership team were actually dishonest is a question for a jury.

The jury would be asked to decide whether their conduct was dishonest by the standards of ordinary decent people (regardless of whether the individuals in question believed at the time they were being dishonest).11 The leading textbook of criminal law and practice, Archbold, says:

“In most cases the jury will need no further direction than the short two-limb test in Barton “(a) what was the defendant’s actual state of knowledge or belief as to the facts and (b) was his conduct dishonest by the standards of ordinary decent people?”

We expect that, presented with the evidence we have published to date, most ordinary decent people would say the behaviour of those running Green Jellyfish was dishonest. However, ultimately that is something for a jury to decide.

In our view there is more than enough evidence to justify a criminal investigation of Green Jellyfish’s leadership team, which we believe includes Christophi, Robinson and Herd.

Thanks above all to the current and former employees of Green Jellyfish for telling us their stories. Given Green Jellyfish’s history of legal and physical intimidation, this involved considerable bravery on their part.

Many thanks to K and T for their R&D tax relief expertise, and to P for additional research. Thanks, as ever, to S for his review and technical suggestions.

Thanks to Mark Strafford, of Sedulo Forensic Accountants and his R&D tax colleagues for their high level forensic accounting review of Green Jellyfish’s accounts.

Paul Rosser of R&D Consulting reviewed a late draft of this article – Paul deserves full credit for discovering and pursuing this story over the last couple of years.

Some images and text © GJ2020 Limited, and used here in the public interest and for purposes of criticism.

Footnotes

Two exceptions. First, Steve Christophi, who is a chartered accountant. Christophi was one of those managing the business and perhaps had ultimate ownership of it, but he played no part in day-to-day advice. Second, the web design and IT staff, who had obvious technical ability but played no role in the R&D tax relief claims ↩︎

After the events of the last few days, many Green Jellyfish employees and former employees have removed their profiles from LinkedIn and/or removed Green Jellyfish from their online CVs. We would discourage others from trying to identify junior Green Jellyfish personnel; we don’t think it’s fair to hold them responsible for the misdeeds of the business. ↩︎

“Complete Care Advisory” is another firm associated with Green Jellyfish; it provided services to care homes including false R&D tax relief claims. We do not know if its other services were bona fide or not. ↩︎

Possibly this should say “always”; nobody we spoke to was aware of a case where a client was rejected. The very poor quality of the projects that were identified by the BDMs suggested that few if any were rejected. ↩︎

Current/former employees of Green Jellyfish and its affiliates ↩︎

Because trade debtors are shown as £2.3m at December 2021 and £3m at December 2022. We can conservatively assume clients paid within 90 days, which implies over £25m of fee income, which (given their 20% fee) implies £125m of tax benefit claimed before the business became much harder in August 2023. Update – 27 August: Mark Strafford, of Sedulo Forensic Accountants and his R&D tax colleagues kindly conducted a high level review of these accounts for us, pro bono, and they agree that this is the right ballpark figure. (Although they believe 60 days would be more typical for this kind of business, implying that the true figure of Green Jellyfish claims may be higher than our previous estimate). ↩︎

We are not sure that’s right; the scattered group structure looks more like an attempt to hide the true ownership of the business and segregate liability. But we do not know for sure, and we could easily be wrong. ↩︎

Nor were any of the “paralegals” registered with the (voluntary) Professional Paralegal Register. We see the use of the job title “paralegal” as a cynical way to hire law graduates and hold out the false promise that this is the start of a legal career. ↩︎

See the Get Onbord case where an “impressive” machine learning/AI system created by a tech startup was found to qualify. The judgment says that a “massive amount of new code was written as part of the project, which goes far beyond “routine” adaptation of existing technologies”. ↩︎

One can imagine a scenario where a care home commissioned a tech company to develop a very sophisticated AI system, but we haven’t seen any examples of this in our Green Jellyfish dossier, or heard about any such case from our industry contacts. ↩︎

The subjective element of the test for dishonesty (see Ghosh (1982)) was removed by Ivey [2017] for civil cases, and that decision was confirmed to apply to criminal cases in Barton [2020]. The fact that a defendant might plead he or she was acting in line with what others in the sector were doing, and therefore did not believe it to be dishonest is no longer relevant if the jury finds they knew what they were doing and it was objectively dishonest. ↩︎

Comments are now closed for legal reasons. Our apologies.

{kind=link}

{kind=link}

.jpg){kind=link}