There has been a huge amount of controversy over the inheritance tax changes in last year’s Budget. They raised £500m, but hit some small farms and small businesses unfairly – whilst not stopping much existing inheritance tax avoidance. There’s a new proposal from CenTax which seems to do the impossible: protect small farms and businesses, counter tax avoidance more effectively, and double the yield to £1bn.

CenTax are proposing a “minimum share rule”. Where a farm/business forms at least 60% of an estate, there would be full relief from inheritance tax up to £5m per person (so £10m for a married couple). For £5m-10m per person there would be 50% relief. After £10m, no relief.

I’m convinced this proposal would be fairer for small farms and businesses, tougher on avoidance and raise more tax.

Inheritance tax – the background

If someone dies then their estate1 pays inheritance tax (IHT) at 40% on all their assets over the £325k “nil rate band” (NRB).2 A married couple automatically share their nil rate bands, so only marital assets over £650k are taxed.

Transfers to spouses are usually completely exempt from inheritance tax. So, for a married couple, in most cases there’s only inheritance tax when the second spouse dies.

The Cameron government introduced an unnecessarily complicated additional “residence nil rate band” (RNRB) where the main residence is passed to children. This is £175k per person, and again automatically shared between married couples. So for most married couples, only marital assets over £1m are taxed. The RNRB starts to be withdrawn (“tapers”) for assets over £2m (with planning, a married couple can keep the RNRB with joint assets of over £2m3).

Before the Budget

Before the Autumn 2024 Budget, private businesses and farms were often completely exempt from inheritance tax (IHT).

Agricultural property relief (APR) removed the IHT charge on the agricultural value of farmland, farm buildings and usually most of the farmhouse.

Business relief (BR) removed the IHT charge on businesses – including farm businesses and farm assets such as machinery and livestock.

In practice, qualifying APR/BR assets were entirely exempt with no cash cap. This protected small farms and small businesses. However it went further than that:

The exemptions had no limit. What made sense for a policy perspective for a small farm or family business doesn’t really make sense for a £7bn business – but the exemption covered it just the same.

The exemption doesn’t apply to shares in listed/quoted companies, for the very good reason that you can easily fund the tax by selling the shares in the market. But shares in alternative markets like AIM aren’t considered “quoted” for this purpose, even though you can easily fund the tax in precisely the same way. So there’s a large market in AIM portfolios designed solely to save inheritance tax. This has no public benefit – it reduces tax take, distorts investment, and artificially inflates AIM valuations (hence reducing yield).

The Budget 2024 changes

The Budget put a combined cap of £1m per person on agricultural property relief and business relief. Up to that cap, there was still a complete exemption from inheritance tax (except for AIM shares).

Above the cap, relief was cut to 50% – so the marginal IHT rate on qualifying farm/business assets beyond the cap became 20%, not 40%.

That sits on top of the standard IHT thresholds: the £325k nil-rate band (NRB), the £175k residence nil-rate band where a home passes to direct descendants, and the usual spouse exemption.

The Budget changes apply from April 2026 and raise raises £500m per year by 2029/30 (more in earlier years).

Why most farms and small businesses wouldn’t be taxed…

The upshot for farmers and owners of small businesses:

For a single farmer who has no material assets other than his or her farm and farmhouse, and plans to leave everything to their children, the new APR/BR cap plus the nil rate band plus the residence nil rate band comes to a maximum of £2m.4

For a married couple who plan to leave everything to each other and then their children, the new cap plus nil rate band plus residence nil rate band comes to a maximum of £4m with some basic planning.5

For farms/businesses larger than this, the answer in principle is to gift property above the £2-4m limit. Provided they live for seven years, the gift will be entirely outside inheritance tax and, if the owner/farmer is still relatively young (say no older than 70) it will be relatively inexpensive to insure against the risk they died early.

… and why some farms and small businesses would

In practice that £4m figure may not be achieved. Some farmers are unmarried; some married farmers’ spouses aren’t involved in the business.

And the “gifting plus insurance” strategy doesn’t work for everyone.

An owner/farmer may be elderly, and not expected to live for seven years (so gifting won’t work and insurance is unavailable or expensive). This is why the Office for Budgetary Responsibility costings show the IHT changes yielding the most revenue in the first few years, from the “too old to gift” cohort. After that point, gifting/planning is expected to reduce revenues.6

Many small farmers have no material income or assets other than their farm, and expect their “retirement” to be funded through farming income. So it won’t be always be easy for them to make a significant gift to their children (and a gift has to be real to count as a gift for IHT purposes).

All of this means that the consequence of the Budget changes are more nuanced than most media coverage (on both sides) suggests:

Only a few hundred small farm estates will end up paying significant amounts of inheritance tax. The CenTax report has more data and details on this.7

Other farms will spend time/money putting planning in place so they don’t pay significant amounts of tax.

This will be a source of worry and stress for many people, even if their estates don’t end up paying tax.

Why should we care about someone with £5m of assets?

An obvious response to the above is: everyone else pays inheritance tax. Why should farms and small businesses be any different, particularly if they own assets worth millions of pounds?

It’s helpful to compare the position of someone inheriting £5m of cash/securities and someone inheriting a £5m farm or small business.

This doesn’t seem a particularly harsh outcome. After all, I’d have paid at least 40% tax (or more) if I earned £5m – it’s not clear why there should be less tax when I’m getting the money for nothing. And most people could live very comfortably for the rest of their lives on £120,000 of passive income.

Now let’s look at what happens if I inherit a £5m farm or small business, and ignore the house and other assets for now. If my parents put simple planning in place, £2m will be fully covered by APR/BR, and the rest benefit from 50% APR/BR. Meaning the tax bill is £600,000 – 20% of £3m.

I probably can’t sell £600,000 worth of the farm/business to pay this. It’s hard to sell part of a small business, and farms cease to be viable below a certain size.

Nor can I easily fund the tax by borrowing. HMRC lets me pay the inheritance tax over ten years and interest free – i.e. £60,000 per year. That means I need the business to generate a 1.2% return to cover the cost of the tax.

Many small businesses would be able to do this – but many small farms will not. The profit from farming often represents a very small percentage of the value of the land. I’ve spoken to farmers who own land worth £5m whose net income is around £50,000. That seems economically contradictory, even impossible, but it’s nevertheless the case.11

The result would be that the heirs would be forced to sell the farm to pay the tax. The farm as a unit would be unviable. That is undesirable – not just for the family directly affected, but for the local community.

The problems with the Budget changes

This illustrates an obvious problem with the Budget changes: in a small but significant number of cases, small farms bear a cost they cannot afford, and will end up being broken up.

There’s a second problem: the changes don’t remove the tax avoidance opportunities of BR/APR. I can acquire (for example) woodland purely to avoid inheritance tax, and it’s still completely effective for the first £1m, and worthwhile (50% relief, so an effective 20% inheritance tax rate) for the rest.

The question is how we fix this.

Our proposal: clawback

Last year we spoke extensively to farmers and farm tax advisers, and proposed a solution – “clawback“.

We suggested keeping full APR/BR for genuine farm succession but clawing it back if heirs sell the farm within a long, tapering period. That would make farmland useless as a bolt‑on IHT shelter: if your children cash out, the tax is reinstated.12

Since we were only seeking to protect small farms, we suggested there should be a £20m ceiling on the exemption.

This had two effects:

Someone inheriting a small farm and continuing to farm it (or lease it to a tenant farmer) would continue to benefit from a complete inheritance tax exemption

Someone inheriting farmland/woodland acquired for inheritance tax planning purposes would likely want or need to sell it (given the low yield); but they then wouldn’t benefit from the inheritance tax exemption.

The proposal therefore was tougher on tax avoidance than the Budget proposal, whilst also protecting small farms.

Clawback was widely supported by farmers and the National Farmers’ Union. However it has failed to achieve any traction with Government. I believe the main reason is that there is simply no data that lets HMRC or HM Treasury model the revenue impact of clawback. There may also have been a concern that it wasn’t possible to design and implement clawback by April 2026.

It therefore doesn’t look like there is any realistic possibility of clawback being implemented.

The idea is that, to get agricultural property relief or business relief , a minimum share of the estate must be made up of qualifying farm/business assets. If farming/business is what you do, you hold more than the minimum share, and get relief up to a generous allowance. If you’re a wealthy household that bought some farmland/woodland to save inheritance tax, you don’t.

CenTax present various possible scenarios, but the one I think is most workable is as follows:

A minimum share set at 60%. All the small farmers I’ve spoken to would easily clear this hurdle – their farmland, business and farmhouse amount to around 90% of their overall assets. Most small businesses would too.13

If the value of the farm/business is at or over the minimum share, APR/BR provide a complete exemption up to a £5m combined APR/BR allowance. This is per-person, so a married couple should benefit from a combined £10m allowance. The allowance should transfer between spouses, in the same way as the nil rate band and residence nil rate bands currently do. Above the £5m per-person allowance, there would be 50% APR/BR relief, i.e. a 20% effective inheritance tax rate.

If the value of the farm/business is below the minimum share, APR/BR is not available, so the full 40% IHT rate applies.14

There would then be a £10m (per person) upper limit to any APR/BR relief. After that, inheritance tax would apply at the usual 40% rate.

I believe this is a better solution than clawback.

It protects small farms just as effectively than clawback (but without the complexity of worrying that subsequent unplanned sales of land/assets could trigger a large IHT charge).

It counters artificial use of APR/BR for avoidance purposes more effectively than clawback, because it’s not reliant on a subsequent event the timing of which would be uncertain. And it does this much more effectively than the Government’s proposal, because tax planners no longer get a £1m exemption to play with.

It should be possible to implement by April 2026, although some of the detail (and anti-avoidance) would need careful thought.

Most importantly from HM Treasury’s perspective, existing IHT data can be used to estimate the revenue impact. Here’s CenTax’s figures:

My favoured scenario is in the bottom right – the central estimate is that this doubles the revenue from the Government’s IHT reform. So instead of raising £500m by 2029/30, it raises £1bn.

I won’t try to reproduce CenTax’s full technical design here – their paper isn’t short – but the policy principle is a simple one: relief should reflect how far the estate is genuinely a farm business or small business. That’s hard to game, easy to administer off the existing data model, and it avoids pushing viable farms into “sell land to pay the tax” decisions that the Budget proposal inevitably creates.

I think it’s a very good idea – I hope Government and representatives of farmers and small businesses give it careful consideration.

Thanks to the farmers, advisers and policy folk who commented on a draft of this note. Any errors are mine.

Footnotes

The “estate” here has a different meaning from the way the word is often used, e.g. “landed estate”. The “estate” is the legal fiction that springs up when someone dies – the executors manage the estate, and inheritance tax is charged on (usually) the estate. ↩︎

The estate pays as a legal matter, but realistically the burden of inheritance tax falls on the heirs – they’d (obviously) receive more if there was less/no IHT. ↩︎

In principle the RNRB could be retained in full with joint assets up to £4m, but in practice changes in asset values between deaths make this very unlikely. ↩︎

This is because of the order in which reliefs apply. The first £1m is completely relieved by APR/BR. The remaining £1m benefits from 50% relief, leaving £500k. That £500k is covered by the NRB/RNRB. ↩︎

That works as follows. The first of the couple to die leaves £1m of farm/business assets to their children, completely relieved by APR/BR – so no IHT, and the rest to the surviving spouse. The second to die leaves £3m to their children. £1m of that is completely relieved by APR/BR. The remaining £2m has 50% relief, leaving £1m. That £1m is covered by both spouses’ combined NRB/RNRB. But the residence nil rate band tapers, so in practice the full £4m will not be available in all cases. ↩︎

CenTax concludes that, amongst farm estates worth less than £2.5 million, only 15 estates per year would face an increase larger than 5%. All of the 25 farm estates per year facing an increase larger than 15pp are valued at over £7.5 million. See Figure 12 on page 50. ↩︎

Let’s assume a simple 40% flat rate here; perhaps I inherit a house as well, some/all of which is covered by the nil rate band and residence nil rate band. ↩︎

That is of course not an investment recommendation, but in a “I take no liability” sense I strongly recommend investing in an index-tracker ETF. ↩︎

Although there is a tax gotcha here – the return on the portfolio is taxable but the cost of the borrowing is usually not deductible. So a 7% return after tax will be very similar to the 5% cost of the borrowing ↩︎

Why? Some mixture of: farmland prices reflect development potential, even if the chances of planning permission are very low; farmland prices reflect demand from people owning large houses who’d like to acquire the neighbouring fields; and – not least – they also reflect demand from people looking to avoid inheritance tax. ↩︎

The fact their house doesn’t qualify for relief means that their business assets typically form a smaller percentage of their overall assets. ↩︎

This would be a “cliff edge”, with 0% relief switching straight to 100% relief at the 60% point. Cliff edges are usually undesirable features of a tax system, but the reasons explained in the CenTax report, it’s probably the best way for the minimum share rule to apply. ↩︎

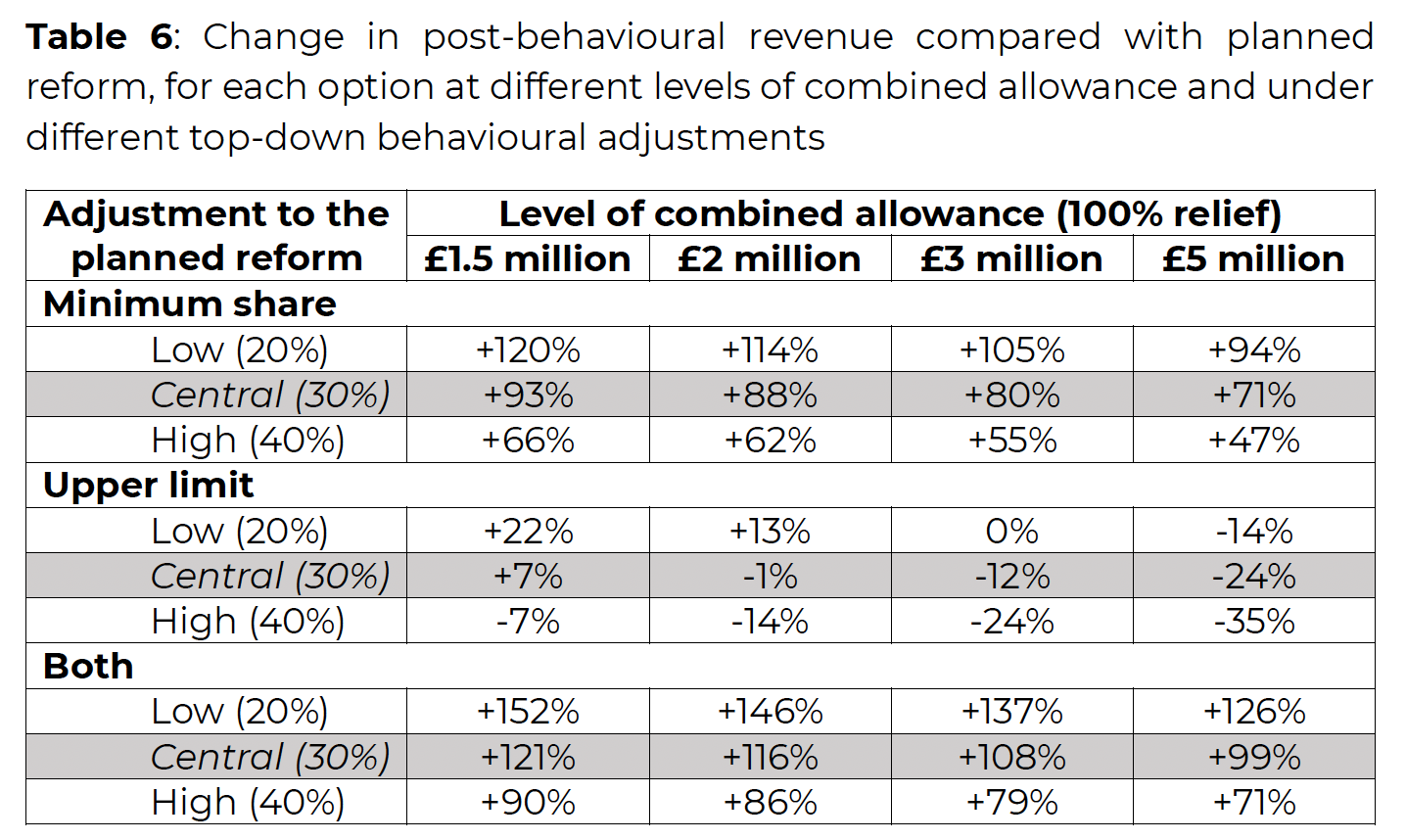

The Institute for Public Policy Research (IPPR) has proposed large increases in gambling taxes to raise £3bn. The £3bn would be used to remove the two-child benefit limit and the household benefit, “lifting around half a million children out of poverty overnight”.

However there’s a gap between how the proposal is being pitched – taxing gambling companies on their large profits – and the reality. According to the IPPR itself it would be gamblers, not gambling companies, paying the price.

There’s also a gap in the IPPR’s calculations. This is a very large proposed tax increase – with the largest tax, remote gaming duty, rising 138%. But the IPPR’s calculation is “static” – it simply multiplies current gambling profits by the new rates. The IPPR justifies this with illustrative calculations showing gambling companies worsening their odds to maintain their profits. But there’s a point beyond which gambling companies can’t do that, and the IPPR’s proposal may go well past this point.

If the IPPR are wrong, and the tax can’t be passed on, then the revenues raised would be much less than £3bn – potentially half.

This is always the problem with “sin taxes”. We can use them to raise revenue. We can use them to deter the “sin”. But we need to be clear what we’re trying to achieve. And we need to be honest and admit that most of the tax is realistically paid by the sinners, not the companies selling the sin.

The proposal

The UK has a confusing array of different taxes on gambling. The IPPR paper proposes large increases in the most important ones:

Remote gaming duty increased from 21% to 50%. This applies to online gaming supplied to UK customers, wherever in the world the supplier is, and is expected to raise about £1.1bn this year.

Machine gaming duty increased from 20% to 50%. MGD applies to e.g. fruit machines, quiz machines, and fixed odd betting terminals. The tax raises about £600m this year.

General betting duty increased from 15% to 25%. This applies to sports betting and most other gambling (except horse racing, which already pays an additional 10% levy). The tax raises around £700m.

The £2.4bn raised by these taxes would increase to about £5.6bn. This would probably be the rare case of a popular tax increase – Portland Communications found that, if they asked the public which taxes should be increased, gambling taxes topped the table.

In many cases we’d expect so large an increase in tax to reduce the gambling companies profits and, as these taxes apply to profits, result in only a small increase in revenue – or even a decrease in revenues (a “Laffer curve” effect). However, previous increases in gambling taxation have not had this effect: the rate of remote gaming duty went up by 40% from April 2019, and the result was a 33% increase in revenue.

That suggests there is potential to raise gambling taxes and raise revenue – but the IPPR’s increase is much larger – up to 138% for remote gaming duty. It therefore can’t just be assumed that history is a guide to what will happen. So it’s disappointing that the £3bn estimate is “static” – it doesn’t take account of “Laffer” effects. Instead, the IPPR justify the figure through an illustrative calculation.

The IPPR’s illustrative calculation, and what it means

“It is only fair, therefore, that these companies, which are exempt from any form of VAT and often based overseas, contribute more to help wider social aims where they can – and the industry is booming.“

I think the reader would assume from this that it’s the gambling companies who end up paying the tax. That is, however, not necessarily the case. It’s usually thought that gambling companies respond to increases in gambling taxes by passing the cost on to gamblers, in the form of worse odds. Or, as an economist would say, the “legal incidence” of gambling taxes is on gambling companies – they pay the tax to HMRC, but the “economic incidence” of gambling taxes largely falls on gamblers.

The IPPR report relies on this, because it means profits aren’t hit, and so “Laffer” effects are limited:

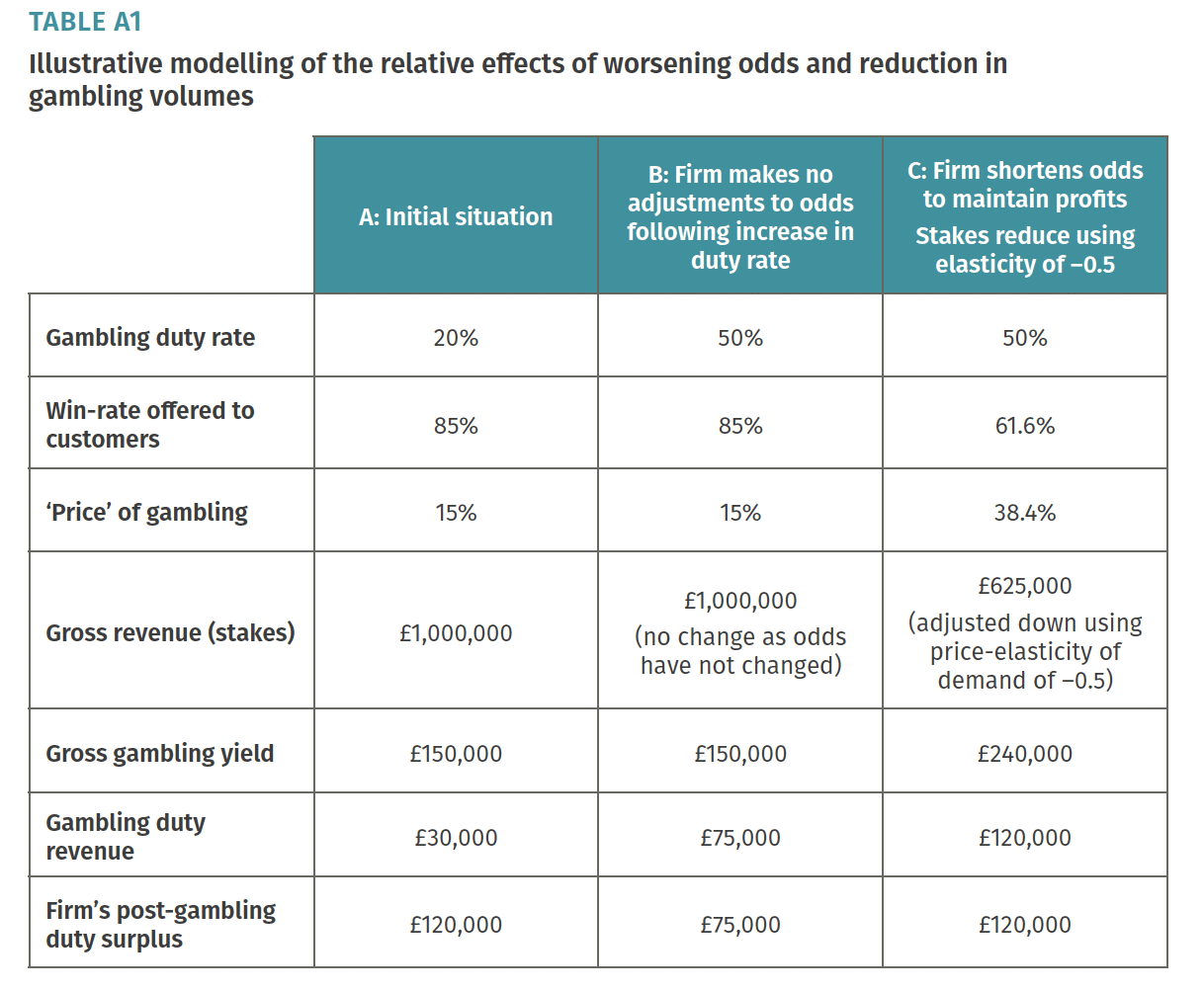

This approach is justified by an illustrative example which shows how the incidence falling on gamblers means that tax revenues increase, even when the rate rises significantly:

The first column is how things are now.

The second column is where the gambling company simply absorbs the increased gaming duty (with its post-tax profit dropping by about 40%).

The third column is what the IPPR thinks will happen: the gambling company protects its margin by worsening odds. Its revenue reduces by 40% but its profit remains the same. The increase in duty has, in economic terms, been entirely paid by gamblers.

This is a simplistic illustrative calculation. I doubt gambling companies would be able to pass all the cost of increased duties to gamblers (particularly for online gaming, where the odds across different platforms serving different countries are very visible).

We should, however, expect a good part of the burden of the tax will economically be borne by gamblers. Whether that is an acceptable outcome is a political question. Personally I find it troubling because, as the IPPR report says:

And there is evidence from a Finnish study that the incidence of gambling tax may be particularly focussed on lower income gamblers.

What happens if the IPPR are wrong?

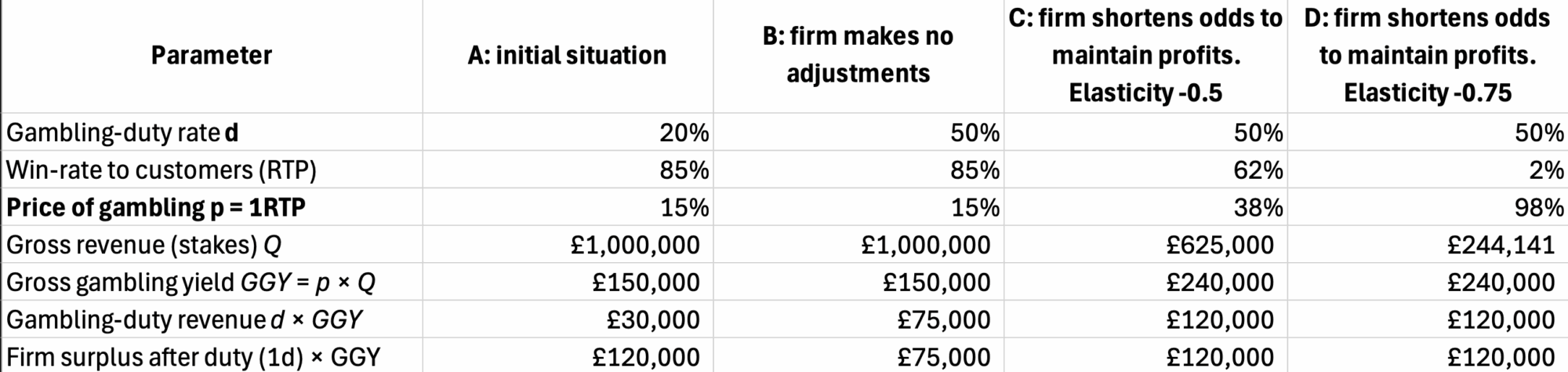

The figure in the IPPR’s illustrative table is based upon a “price elasticity of demand” of -0.5. In other words, that a 10% increase in the “price” of gambling (the odds) will result in a 5% decrease in the gambling revenue. This is a large effect, but IPPR’s illustrative figures show that gambling companies can (in principle) still protect their margins by worsening odds, and so making a greater percentage profit from that reduced revenue.

However there is a point where this stops working.

As the price elasticity rises beyond -0.5, gambling firms have to make the odds worse and worse to keep their margins. But there’s a limit – eventually the odds become impossible.

Here’s what happens if we add a column D to the IPPR’s table, with elasticity of -0.75:1

At that point, margins can only be maintained if customers’ win-rate drops from 85% (as at present) to 2%. It’s unlikely anyone would gamble in such a scenario. And beyond -0.75, it becomes impossible to maintain margins with this strategy.

Gambling companies could, in principle, take the opposite approach, and maintain their margins by greatly increasing sales. It’s unclear if that’s possible, but I expect most people would consider it an undesirable outcome.

So the IPPR’s simple “illustrative” approach only makes sense if its estimate of a -0.5 elasticity is roughly correct. Beyond that point, their simple assumption that profits can remain broadly static fails, and a more complex analysis is required.

The calculation above is absolutely not a proper analysis – it merely identifies an important limitation of the IPPR’s illustrative calculation. There are numerous real-world factors which complicate matters,2 and the real-world limit of the IPPR’s approach will not be -0.75 – a detailed analysis would be required to determine where it lies.

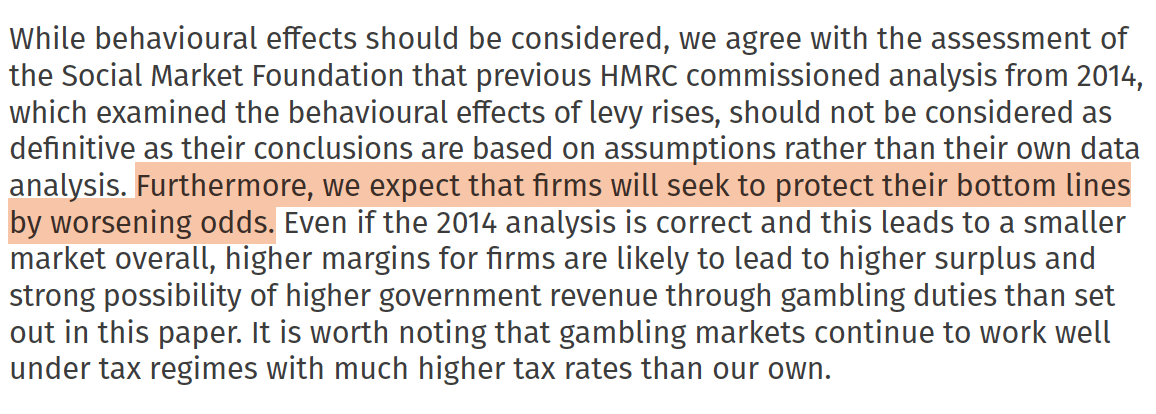

Earlier this year, the Social Market Foundation published a proposal to increase gambling taxes (more modestly than the IPPR’s proposal). The SMF were critical of the figures in the HMRC report, saying that much of it rests upon questionable assumptions rather than empirical evidence. The IPPR say they agree with the SMF.

The HMRC and SMF documents are both serious and considered pieces of work, and I and our team have not assessed the merits of the two positions.

But the point is of critical importance to the IPPR paper. if the HMRC/Frontier figures were correct then, applying the -1.8 (rather than -0.5) elasticity to IPPR’s numbers cuts the extra remote gaming duty revenue by about two-thirds. Because RGD is the single biggest component of the £3bn package, that alone would mean the whole yield would fall to about £1.5bn – half the expected £3bn.

Given the dependence on the -0.5 figure, it is therefore unfortunate that the IPPR present only one scenario. It would be preferable to admit the uncertainty and discuss the range of possible outcomes.

Conclusion

We need to be careful about trying to raise additional revenue from “sin” taxes. The revenue may be less than we expect, and what revenue we do receive may (in economic terms) come from customers rather than the businesses making the sale.

Personally I see compelling arguments for reducing the harms caused by gambling; but I’m unconvinced tax is a good tool for doing that. Regulation may be a better approach.

A tax increase may still be worth doing as a revenue-raiser. But any argument for an increase needs a more robust revenue estimate than the IPPR’s use of a static calculation and illustrative tables. And it needs to acknowledge who is actually paying the price.

The win rate/price of gambling is assumed; it of course varies for different forms of gambling. Firms could cut costs, alter marketing spend, shift product mix, or accept lower margins temporarily. For online gambling in particular, cross-border supply could constrain odds-worsening even before we hit the -0.75 threshold, because consumers could use VPNs etc to use foreign untaxed platforms. And, critically, elasticity is not constant – elasticities from smaller price changes don’t necessarily apply to very large price changes. ↩︎

Thanks to H for a discussion on elasticities and help with the modelling.

In July 2022, I wrote that I thought Nadhim Zahawi had lied about his taxes. I was right. Nadhim Zahawi lied repeatedly about his tax affairs, and continued to do so until it became public in January 2023 that – at the same time he was saying he’d always paid taxes in full – he was negotiating a £5m settlement with HMRC, including back-taxes plus penalties. Mr Zahawi was then sacked by the Prime Minister.

Nadhim Zahawi’s solicitor, Ashley Hurst, emailed me that July demanding that I retract my allegation, with the implicit threat of libel action if I did not. He went further: he claimed that the email was “without prejudice” and confidential, and that I was not permitted to publish it or even refer to it. He said it would be a “serious matter” if I did. I took that to be another threat.

In December 2024, the Solicitors Disciplinary Tribunal found that the email was improper, and agreed that it contained an implicit threat of action against me if I disclosed the existence of the email. Mr Hurst was fined £50,000 and had to pay the SRA’s costs of £298,391, as well as his own costs of £908,172.1

Mr Hurst is now appealing to the Administrative Court. Here are his grounds of appeal:

Here is the SRA’s response:

My take: if Mr Hurst wins this appeal, then solicitors will have a green light to claim their libel threats cannot be published, or even referred to. The “secret SLAPP” will have become blessed by the courts.

That would be a terrible result for everybody who cares about free speech.

Footnotes

Although I expect Osborne Clarke are paying these – the firm has backed Mr Hurst throughout. ↩︎

Chancery Law & Tax is “one of the UK’s leading providers of Legal Services”. It appears to have no employees or directors with any legal or tax qualifications. It’s owned by a man called Tony Gimple.

Mr Gimple’s previous firm, Less Tax for Landlords (aka the One Consultancy Group) promoted a landlord tax avoidance scheme. Mr Gimple sold the scheme very successfully for years – but it was an incompetent disaster, was shut down by HMRC, and has left hundreds of landlords in a dire financial position.

Mr Gimple has learned nothing. Chancery Law & Tax is going down the same path – advising landlords but getting the basics badly wrong. If the new proposed regulation for advisers doesn’t put him out of business, it isn’t working.

LT4L advised landlords to move their properties into an “hybrid partnership” LLP. Mr Gimple said this somehow enabled an inheritance tax exemption (it didn’t) and that LLP income was “trading income” (it isn’t). These were elementary mistakes that a trainee accountant would spot.

This was false – professional indemnity insurance does not work this way. And, sure enough, HMRC did not agree with the way the scheme was structured, and says it should have been disclosed as a tax avoidance scheme. No landlord has received a penny from LT4L’s insurers.

Mr Gimple now says he never understood the structure, and trusted LT4L’s accountant, Chris Bailey, to get the tax right. But listen to one of his interviews – he’s talking at length, with great confidence:1

Or this presentation:

Almost everything he says in the interview and the presentation is dangerous nonsense.

Someone with so little understanding of UK tax should never have been selling a tax scheme, and certainly shouldn’t be running a tax firm now. But he is.

Chancery Law & Tax

Mr Gimple’s new firm has just published a guide to incorporating a property business.

Incorporating therefore creates a potentially significant ongoing tax benefit for landlords.

But there is a big risk. Incorporation of a landlord’s business can easily trigger capital gains tax and stamp duty land tax. These will often be very large liabilities, much larger than the ongoing tax saving. Great care needs to be taken.

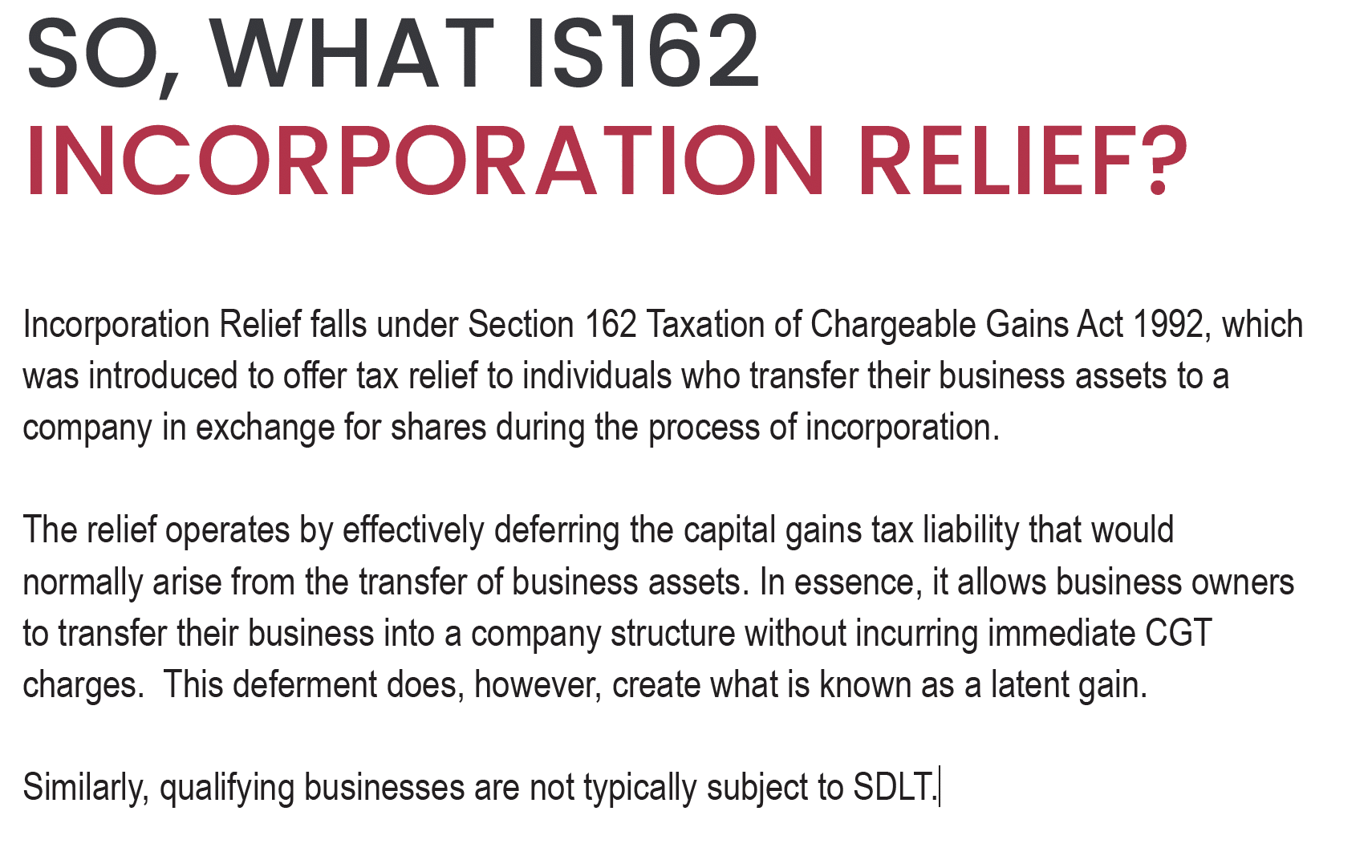

Mr Gimple’s guide mainly discusses the section 162 TCGA “incorporation relief” from capital gains tax. However it claims that section 162 also applies to stamp duty land tax:

This claim is simply wrong. Section 162 does not apply to SDLT in any manner.

This isn’t a one-off mistake. The guide goes on to say that “qualifying businesses are not typically subject to SDLT”:

It’s another serious error. In all cases where an individual is incorporating a property rental business, there will be an up-front SDLT charge – potentially a very high one given current rates.

If the individual is carrying on a property rental business in partnership then the complex rules in Schedule 15 Finance Act 2003 may apply to prevent an SDLT charge – but specialist advice is required. There is zero connection between s162 and Schedule 15 (or indeed any aspect of SDLT).

These errors suggest that Mr Gimple and Chancery Law & Tax lack a basic understanding of SDLT.

The Less Tax for Landlords connection

Mr Gimple is promoting incorporation to the very landlords who were sold the failed Less Tax for Landlords scheme. There are some highly complex SDLT consequences of the LT4L scheme2, and on the evidence of this guide, Mr Gimple’s firm lacks the expertise to deal with them. Given his track record, we would strongly advise affected landlords to instead seek independent advice from an adviser with tax qualifications.

Is it legal to call the firm “Chancery Law & Tax”?

Chancery Law & Tax obviously have the word “Law” in the title, and say they’re “one of the UK’s leading providers of Legal Services”. They claim to provide a Will writing service.

Finally, the Advertising Standards Authority may have a view on how reasonable it is for a small unregulated firm with a dismal history to say it is “one of the UK’s leading providers of Legal Services”.

Who should landlords turn to for advice?

Landlords, and anyone else needing tax advice, should use a regulated firm, and only deal with regulated professionals. If you’re speaking to a salesman like Mr Gimple, with no legal or tax qualifications, then our view is that you’re making a mistake, and potentially a very expensive one.

In particular the complex “sum of the lower proportion” rules which apply where the beneficial interest in a property has been partnership property of this kind of property investment partnership. The matter is further complicated by changes in the LLP members’ entitlement to income, and potentially also by the paragraph 12A elections rules. ↩︎

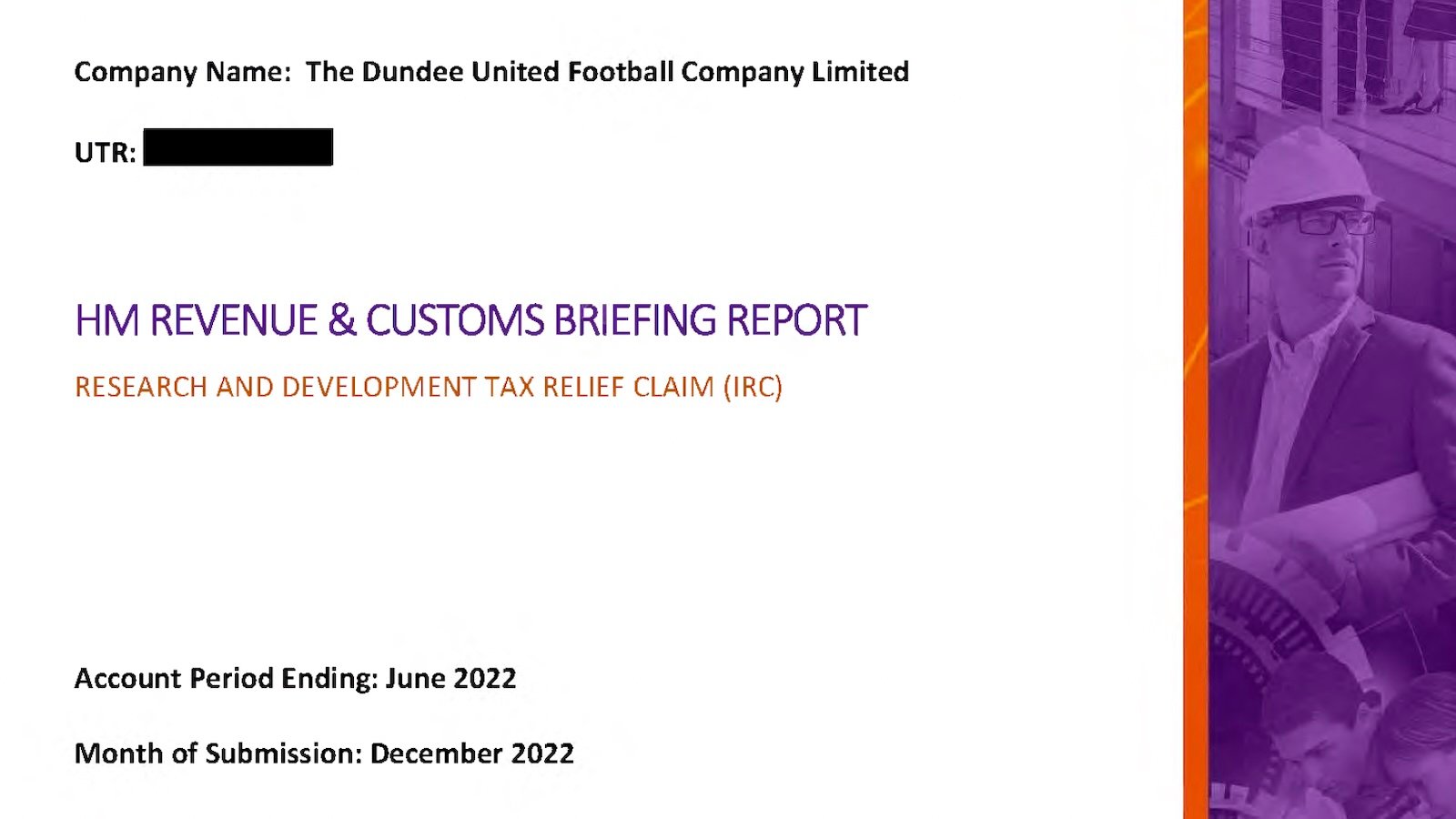

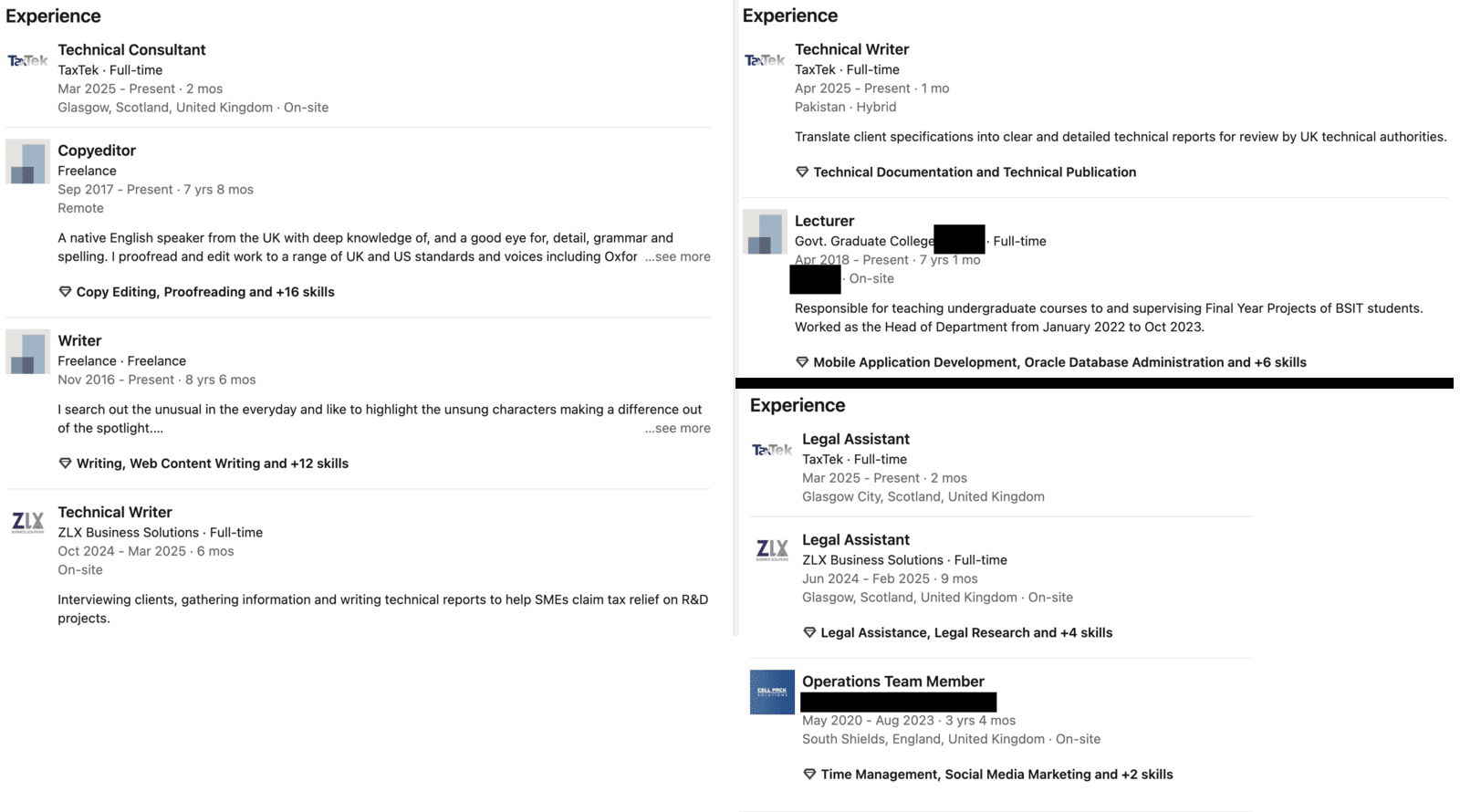

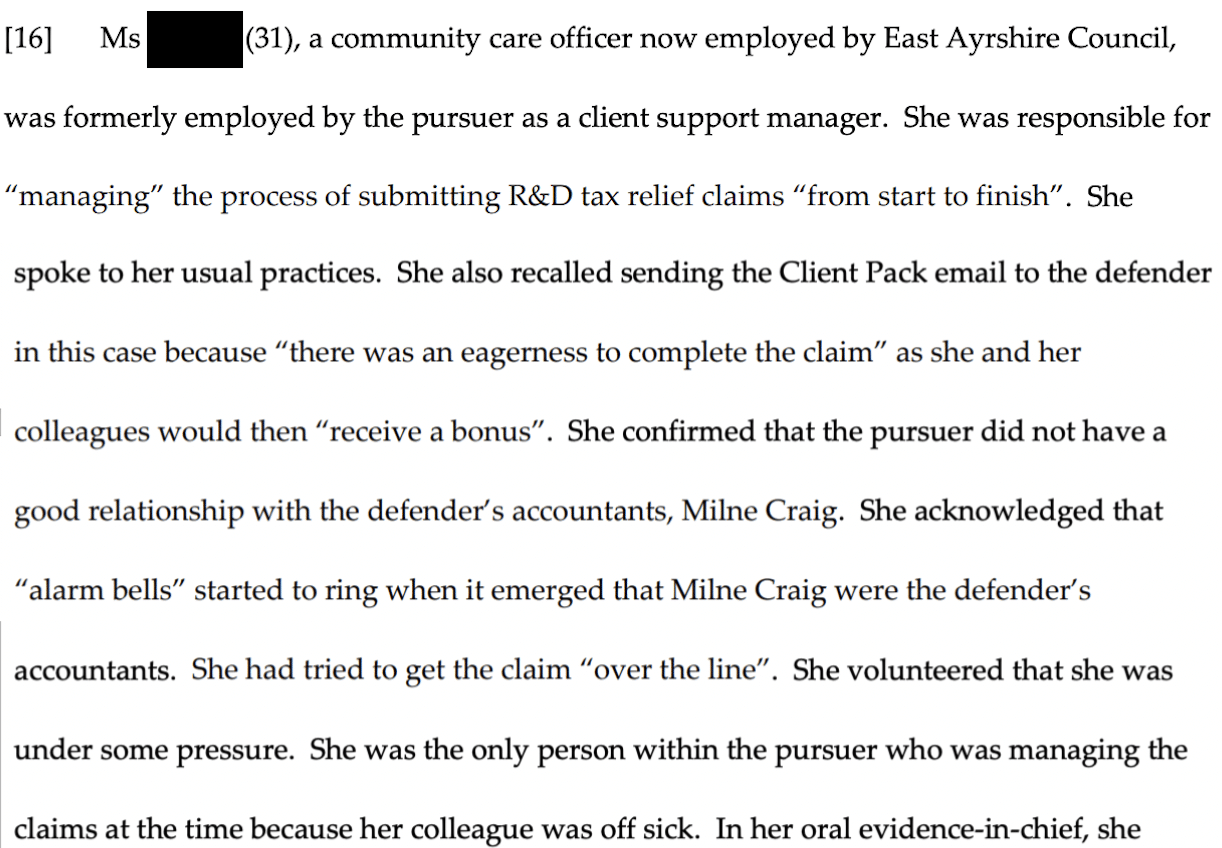

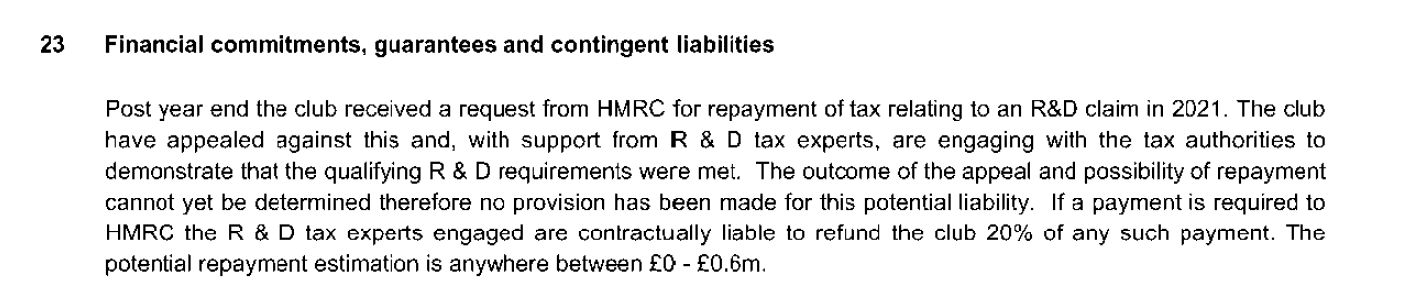

As The Times has reported, there’s evidence that Dundee United claimed R&D tax relief for a quarter of its players’ wages. HMRC – and therefore all of us – may have subsidised the club’s wage bill.

The Times‘ article was based on an R&D tax relief claim document we obtained – we’re publishing it in full below. We’re publishing the document because it’s not just invalid – it is outrageous. R&D tax relief is intended to incentivise innovation. It applies to businesses seeking an “advance in science or technology”. It was never intended to apply to the wages of football players, and in our view it’s clear that it cannot apply in this way.

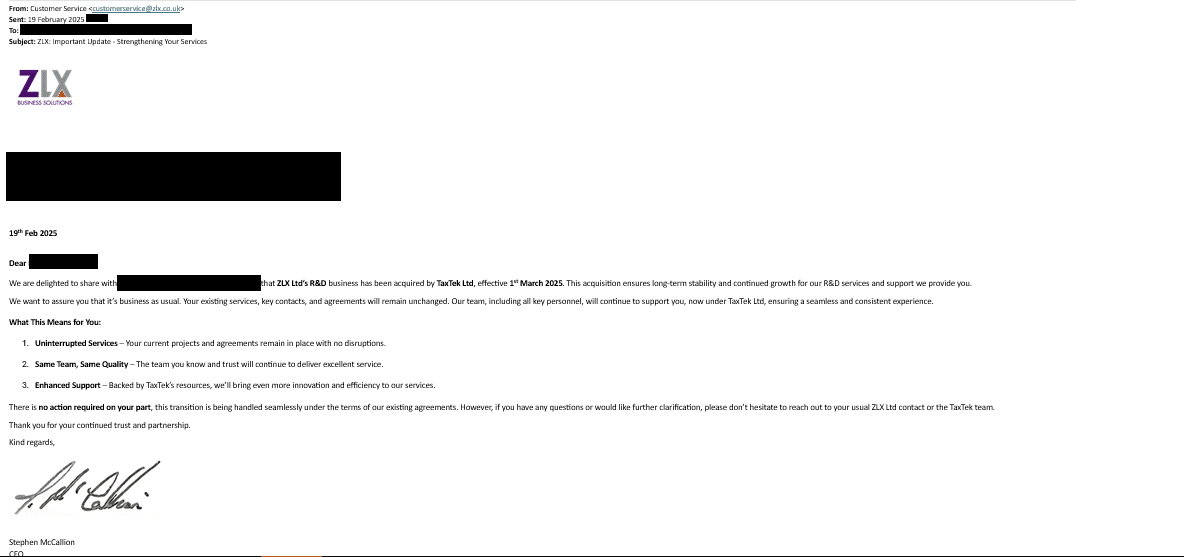

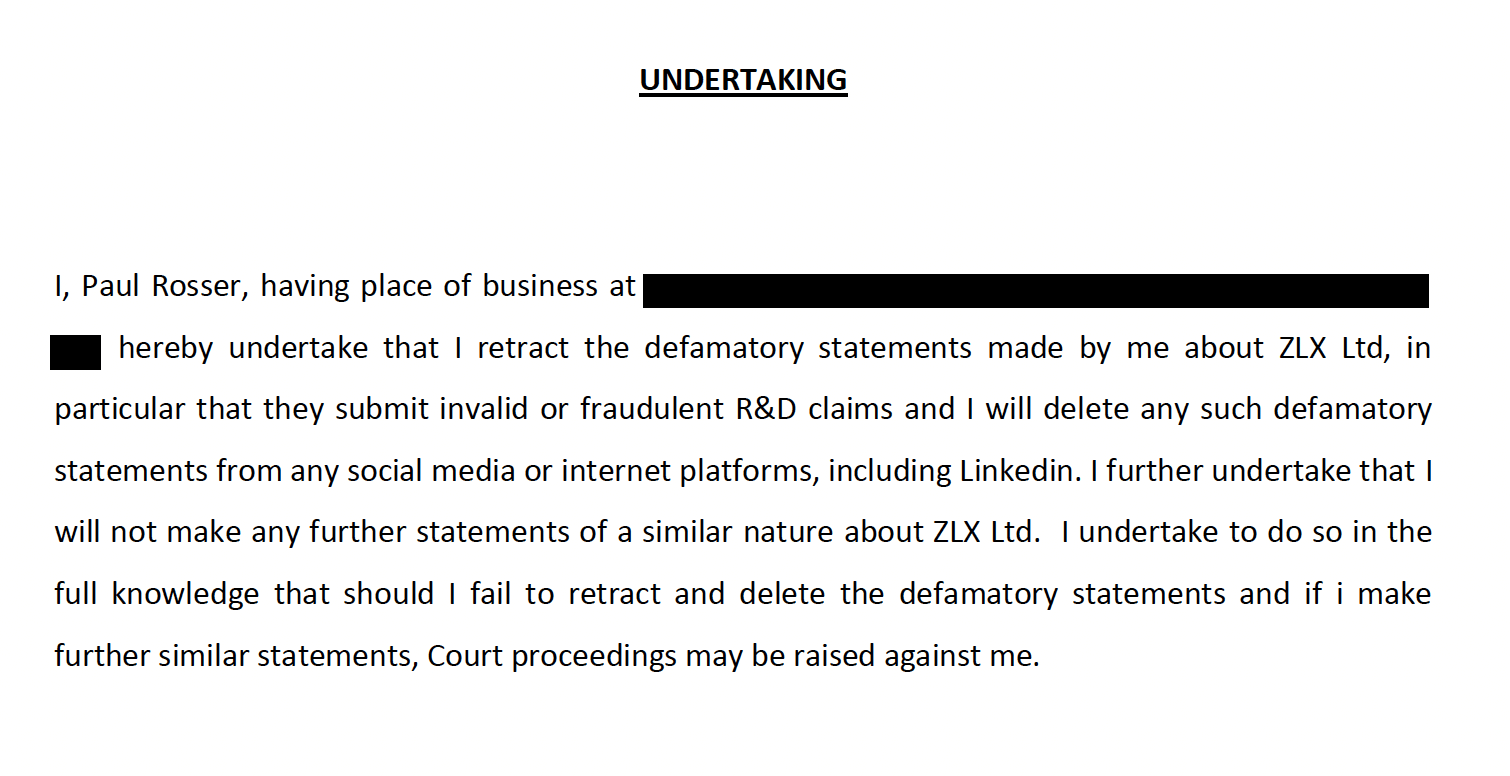

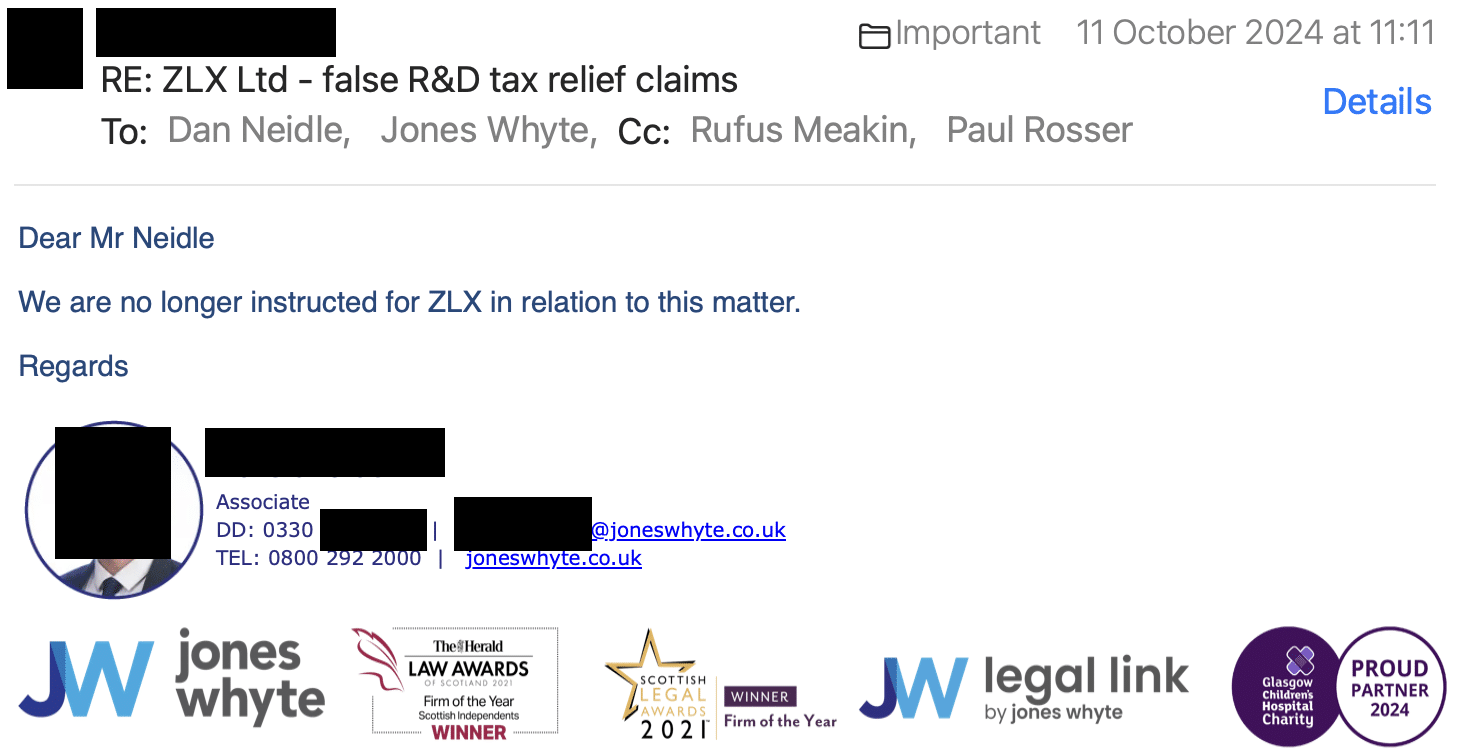

Dundee United have refused to comment. The firm that drafted the document, ZLX, denied that this document was sent to HMRC, but were unable to explain why it was created, or why it was signed by Dundee United’s finance director and a director of ZLX.

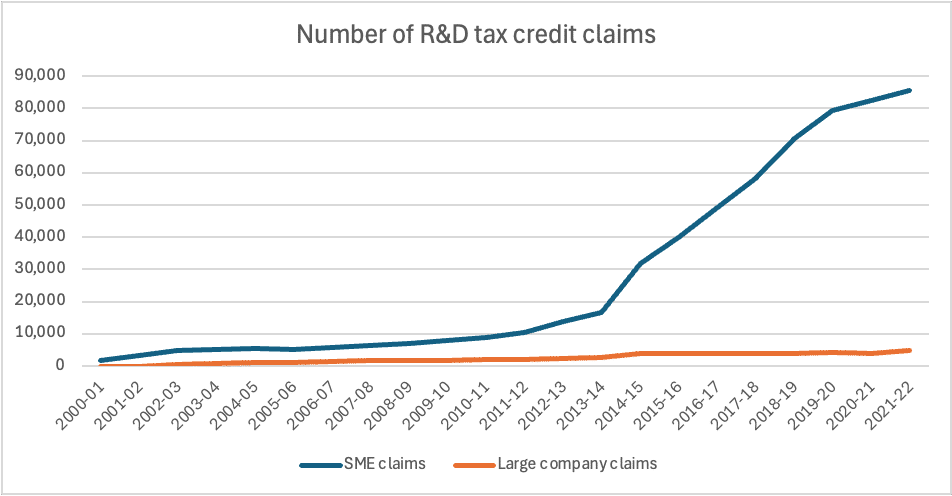

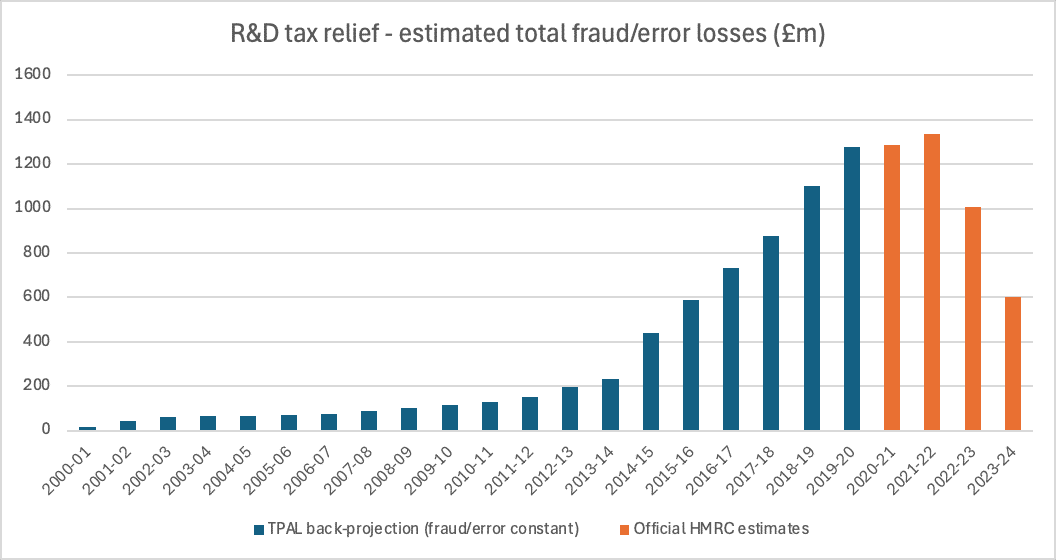

We believe this is part of a wider problem. The Times previously reported that 33 football clubs are being investigated by HMRC. And we have previously reported that the total cost of invalid and fraudulent R&D tax credit claims could be £10bn.

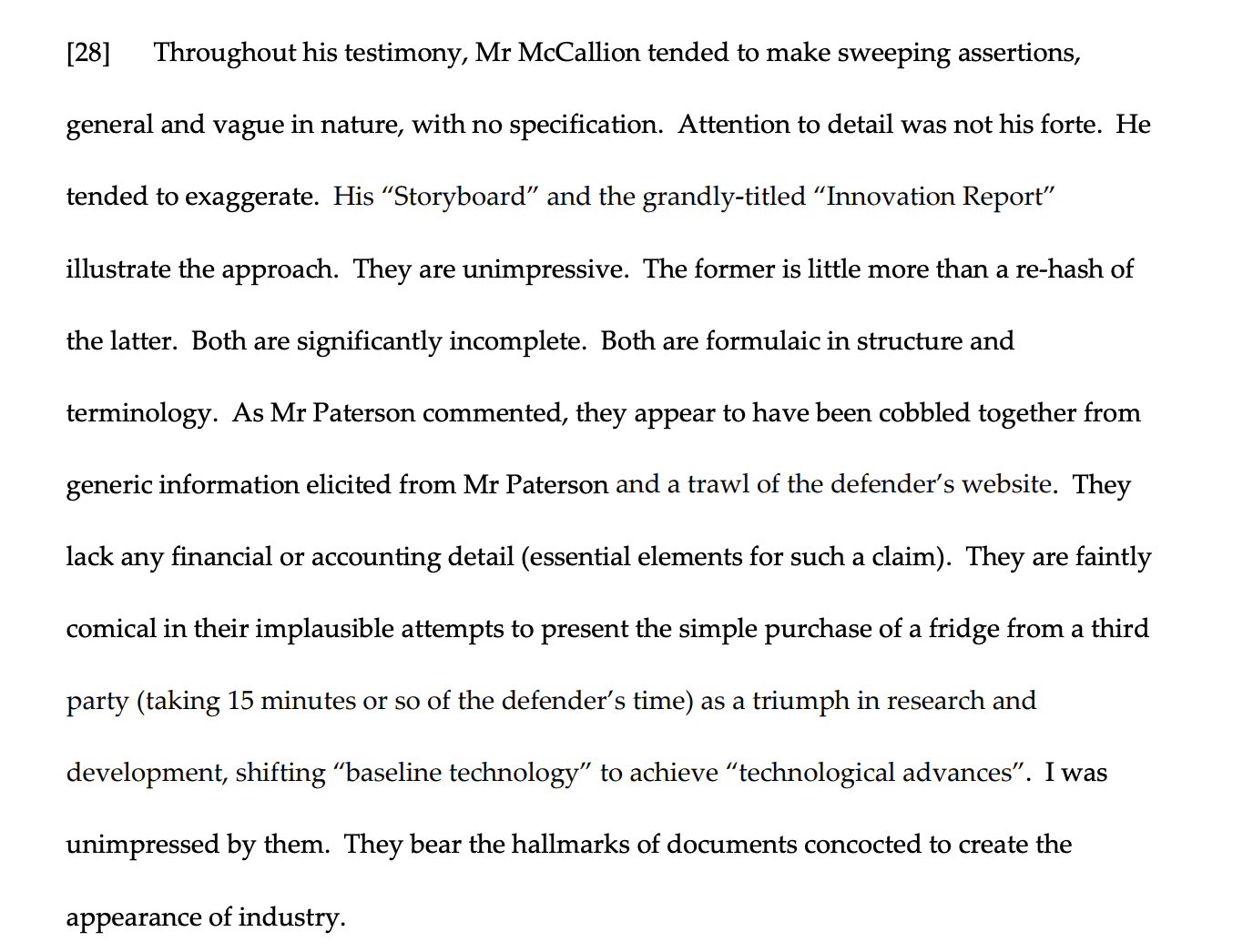

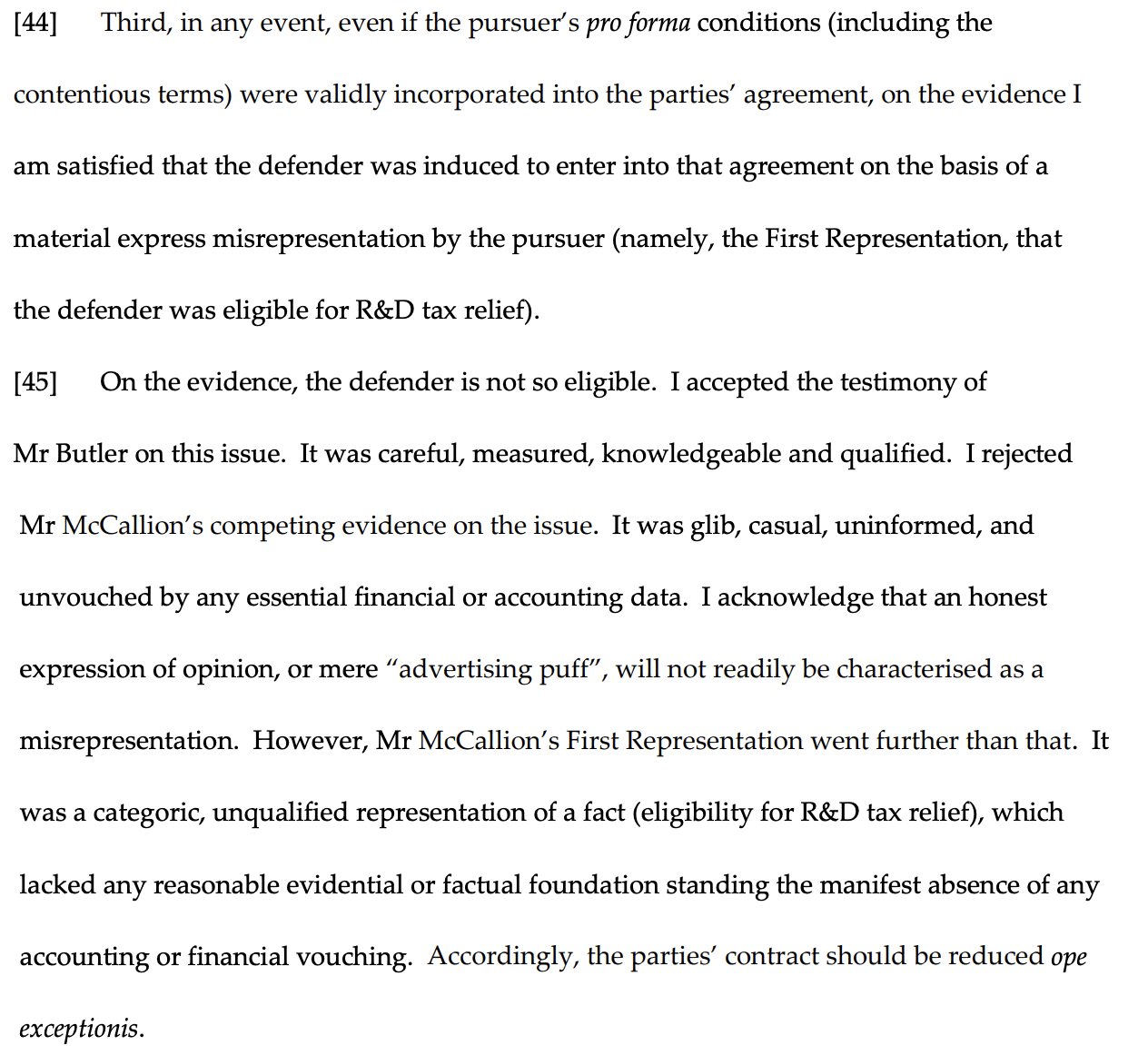

UPDATE: The Courierpublished an article on 10 October 2025 in which a former director of Dundee United says that the document is genuine. And – critically – the Courier obtained emails from Abertay University which suggest that the research project described in the ZLX document never existed, and Abertay University confirmed that in a statement. Paul Rosser has found a research paper which may be the genesis what appears to be a false claim by ZLX/Dundee United. If the ZLX/Dundee United claim we publish below was submitted to HMRC, but the research it describes never existed, then anyone involved who knew they were submitting a false document may have committed tax fraud. We put this point to Stephen McCallion, CEO of ZLX, but his only response was a vague denial; he was unable or unwilling to explain the ZLX document and the Abertay emails.

Here’s the document supporting a claim for £1.4m of R&D tax relief. It’s signed by Dundee United’s finance director and a director of ZLX:

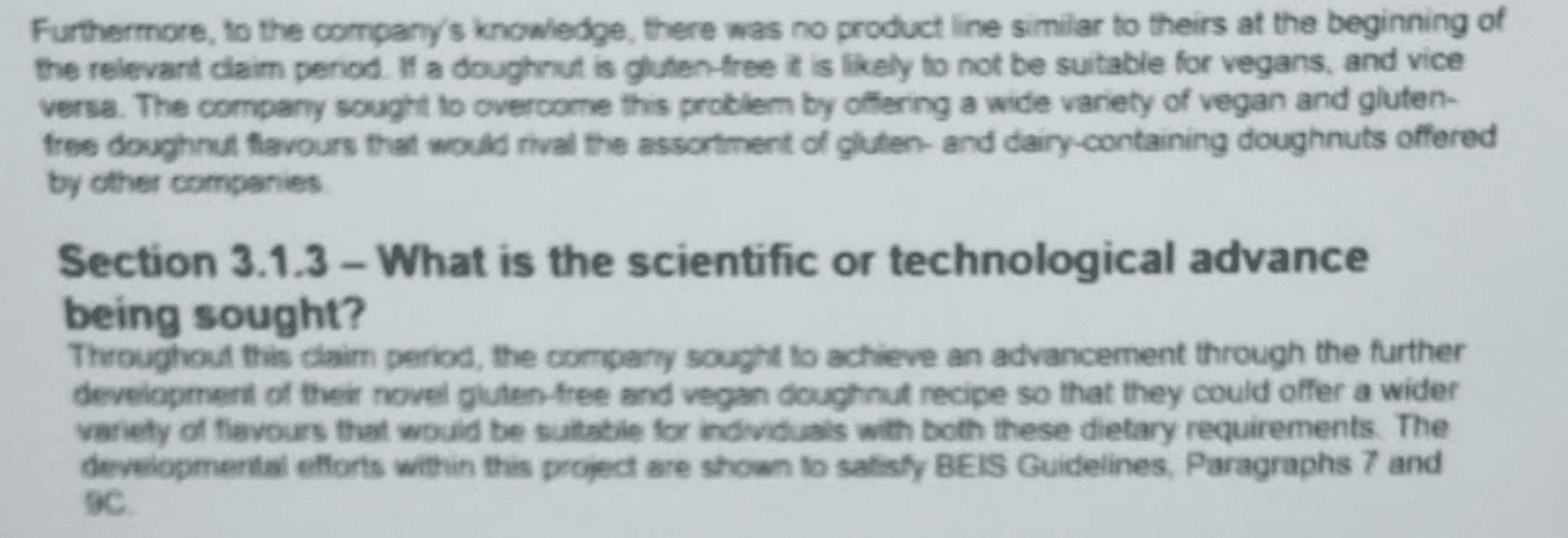

Does the Dundee United document describe valid R&D tax relief claims?

It does not. We spoke to three leading R&D tax advisers, and all were amazed that anyone could consider such a claim legitimate.

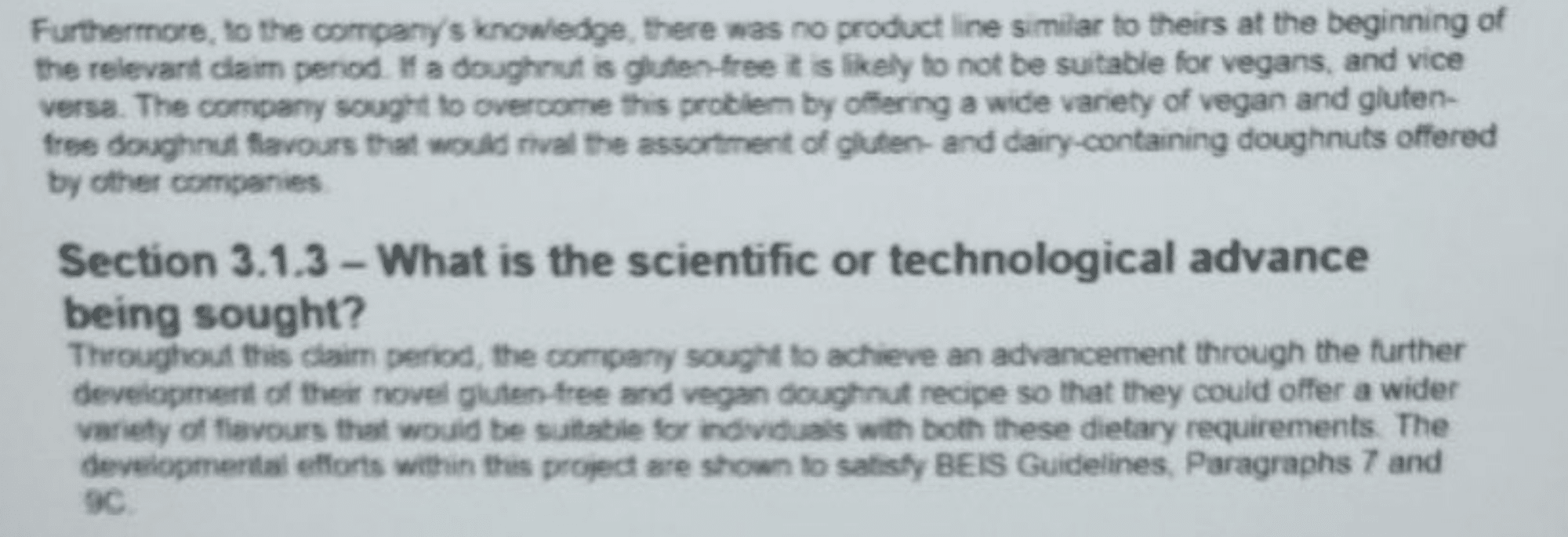

The document covers three obvious things that any sports team would do – training, diet and analytics. This is all dressed-up in pseudo-technical language such as “position-specific carbohydrate periodisation” (meaning changing players’ diets based on their activity). All the verbiage cannot hide the fundamental problem with the three projects: if something is widely known about by clubs, then a club simply doing the same is not attempting to create an “advance in science/technology”, and no relief is available.1

The document is therefore invalid on its face, but what’s more troubling is the expenses that the document says are claimed for tax relief:

24% of their players’ wages – as if the players were carrying out scientific/technical research. That is a huge amount of money, and in our view is indefensible. Even if the R&D projects were real, and qualified for relief, the players would be the subjects of that research, and their wages would not qualify for relief.

80% of their chef’s wages – and whilst he appears to be an excellent chef, it seems most unlikely he spent 80% of his time on an R&D project. Even if he did, supporting activities of a non-technical nature are not eligible for relief.

90% of the wages of their “head of tactical performance“. Even if he was a professional engaged in R&D, we are doubtful he spent 90% of his time on this.

21% of their heating and lighting costs, implying that 21% of the use of their premises was for R&D projects. This seems implausible.

The document is for a 2022 claim; Dundee United also claimed £1.27m for 2020 and 2021.

Who would make such a claim?

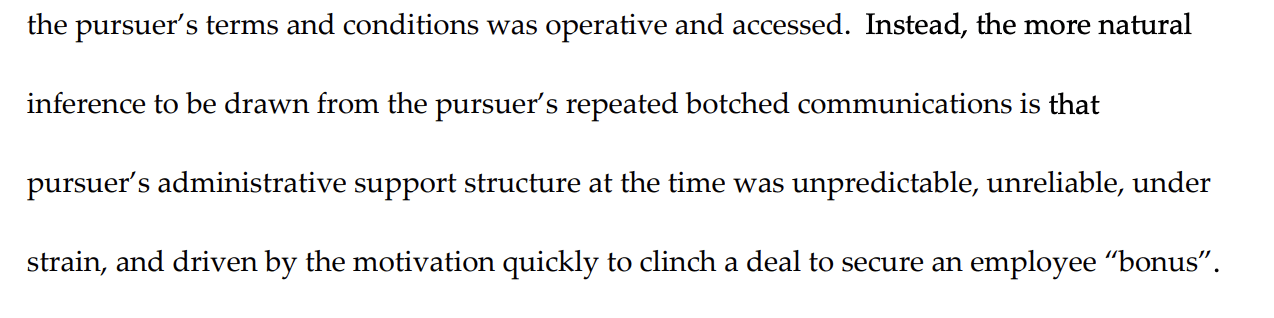

The document was prepared by ZLX – the R&D tax firm notorious for suing a client who wasn’t willing to put in a comical R&D tax claim for installing a fridge.ZLX was an official partner of Dundee United and, as The Times reported, the club made an R&D tax relief claim worth £600k.

ZLX’s owner, Stephen McCallion, told us that it is “not a document that was submitted to HMRC and the contents were not submitted to HMRC”. However he was unable to explain why the document was created and signed, and he did not deny (to us or The Times) that Dundee United’s claimed R&D tax relief for a large percentage of its player’s wages.

We and The Times asked Dundee United for comment; we didn’t hear back.

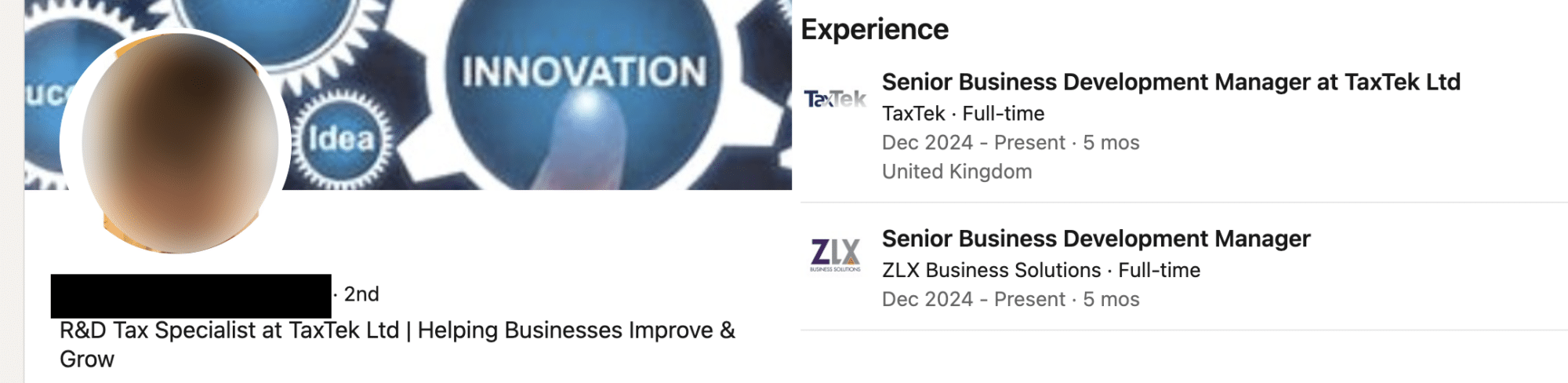

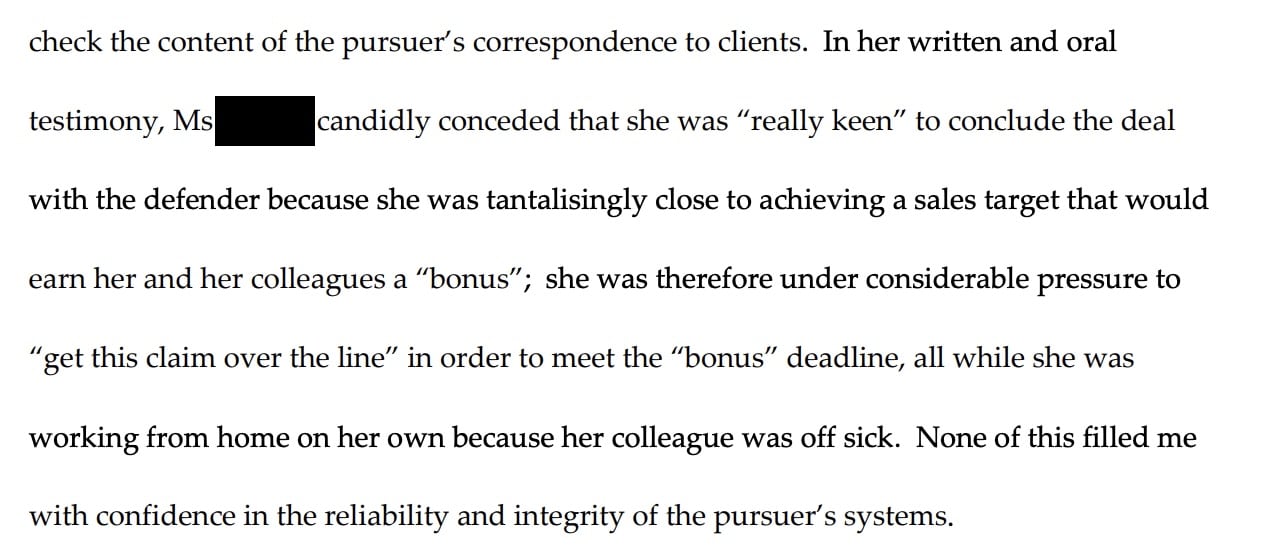

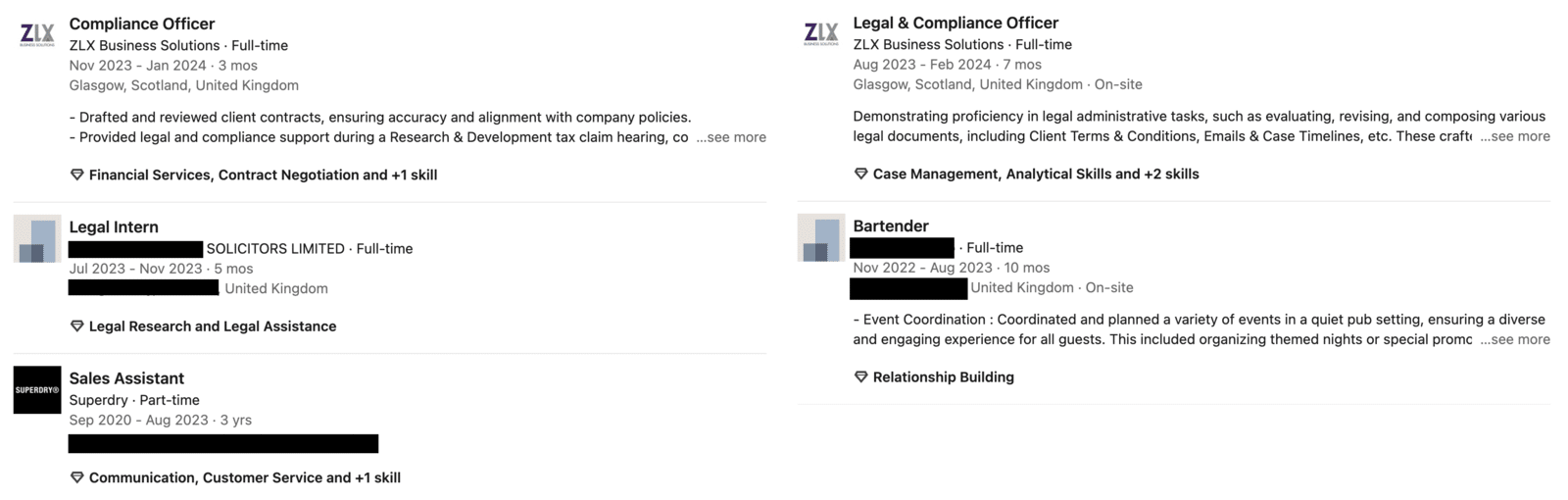

We previously reported that ZLX appeared to employ nobody with any tax qualifications. In 2024, ZLX had two people in its compliance team – their previous experience was as a bartender and sales assistant. It is therefore to be expected that ZLX would make invalid claims. The question is whether this was merely reckless, or whether it crosses the line into criminality on the part of ZLX’s management.

Mr McCallion objects to our previous reporting – but has not identified any specific errors.

We don’t believe any reasonable adviser would have thought this claim was valid, or that any reasonable business would have submitted it. We expect HMRC will charge Dundee United penalties.

If ZLX/Dundee United did make R&D tax relief claims described on the basis of the document we reviewed (or substantively similar claims) then we believe ZLX should be the subject of a criminal investigation.

Henley & Partners’ 2025 Wealth Migration Report says 16,500 UK millionaires will leave this year. That’s a very small percentage, which is surprising when the OBR expected 25% of the wealthiest non-doms to leave the UK.1 And many private wealth industry figures have told us that many of the figures in the Henley & Partners reports don’t make sense. Wealth specialists in business and academia have told us they doubt that it’s possible to do what Henley & Partners claim.

Our team has therefore conducted a full statistical and forensic review – which shows that the Henley & Partners reports can’t be trusted:

Definitions change, numbers don’t. The report dropped all property wealth between 2023 and 2025, yet its millionaire counts barely moved. That is impossible if the published methodology were real. And when the FT asked about this, New World Wealth (who write the report) admitted that property was never actually included in the analysis, although before 2025 their reports all said that it was.

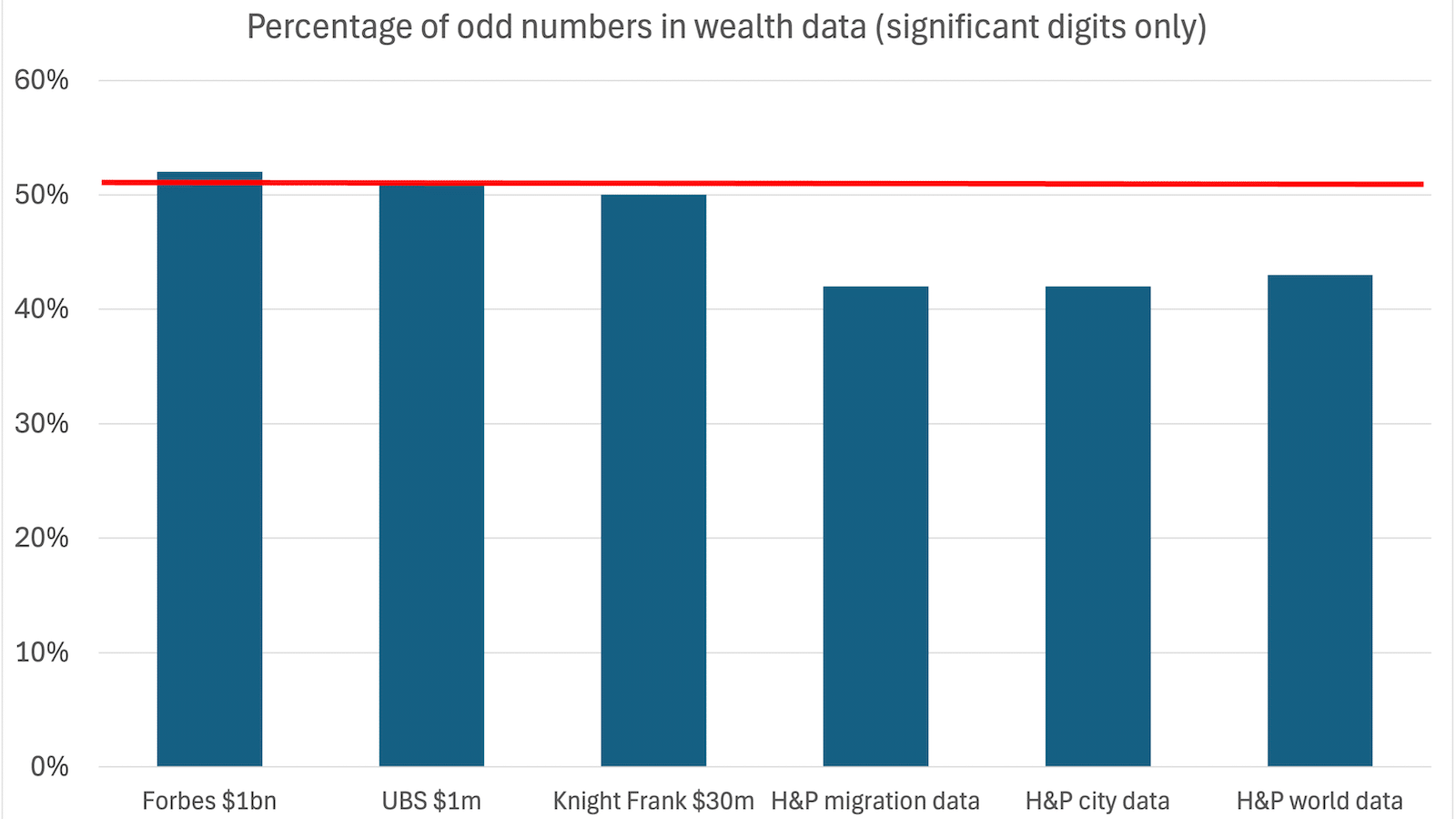

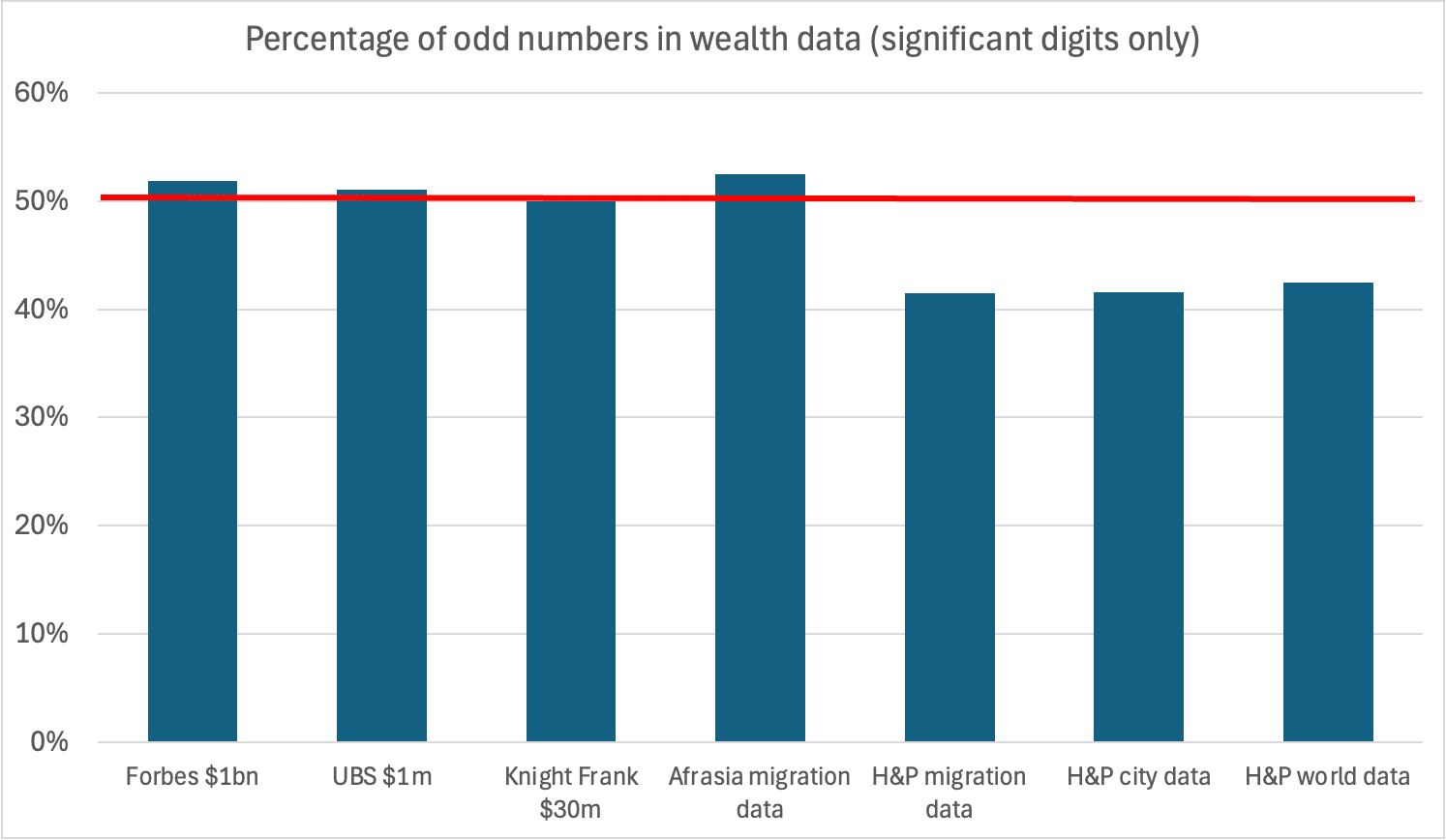

Too many even numbers. Wealth reports from Knight Frank, Forbes and UBS have as many odd numbers as even numbers – which is what you’d expect. But the Henley & Partners wealth and migration figures have too many even numbers – the chance of that occurring naturally is 2%. It’s classic evidence of numbers typed, not measured.

Digit patterns look “made‑up”. Trailing digits cluster on 0s and 5s, with almost no 1s. Statistically, the chance of that occurring naturally is about 1 in 240,000. More evidence that the numbers are manually created or adjusted.

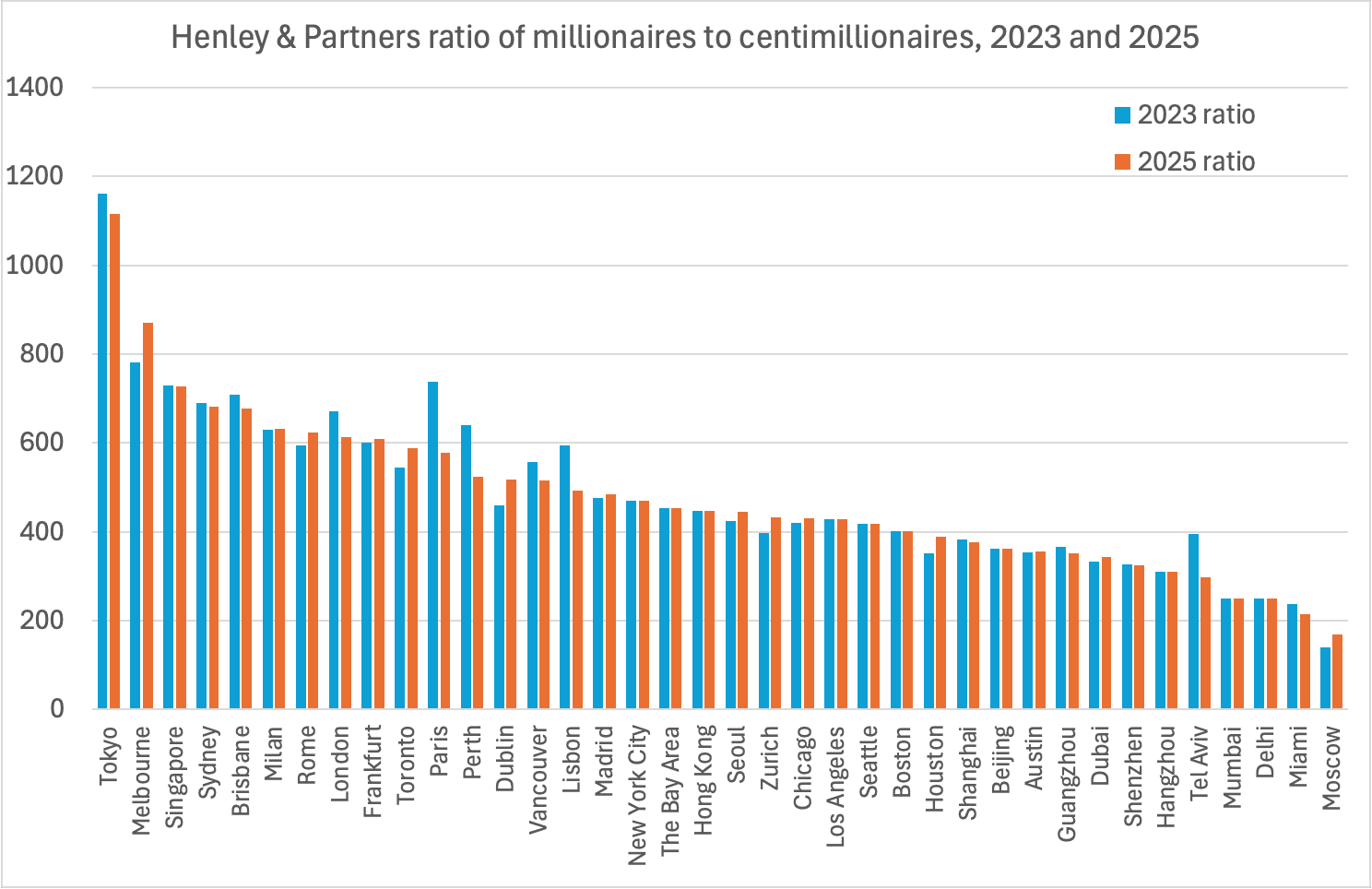

Millionaire/centimillionaire ratios are “frozen.” In 2023‑25, 14 of 38 cities show a less than 1 % change in the ratio of millionaires to centimillionaires (people with $100m of net wealth). Five of the world’s largest and most dynamic cities showed a change of less than 0.1 %. Our model gives only a 0.03% likelihood of such stability arising from chance. The likely explanation: a single growth/shrink factor is applied to both brackets: another sign the figures are engineered, not observed.

A one‑man firm says it tracks 150,000 fortunes – right down to investments, cash and crypto – and nets off their debt. That simply can’t be done. Not even by tax authorities.

Official data flatly contradicts the Henley & Partners figures. UK millionaires ($1m+) are overstated by almost 100 %, while UK centimillionaires ($100m+) are understated by around 70 %.

No statistical controls. As was first reported by Tim Harford in 2024, the report uses no statistical controls of any kind. Even if it did what it claimed, it’s just a survey, no more scientific than a Twitter poll.

Until an independent audit is carried out, the Wealth Migration Report should be treated as marketing material, not evidence.

Henley & Partners are a firm which sells migration services. They have no statistical expertise. They told us that New World Wealth doesn’t share the details of its methodology with them. We accept that, if there was fabrication, Henley & Partners are unaware of it.

The methodology changed dramatically. The data didn’t.

The Henley & Partners reports count numbers of millionaires ($1m+), centimillionaires ($100m+) and billionaires ($1bn+) by their “net wealth”. This was originally defined to include real estate. The Henley & Partners 2023 report said “wealth” means “property, cash and equities less any liabilities”. It added “the bulk of the average high-net-worth individual’s wealth is tied up in residential property and equities.”2

The 2024 USA report says they are measuring “wealth” defined as “listed company holdings, cash holdings, and debt-free residential property holdings” (our emphasis). That’s a small but important difference – because now they don’t just net off property debt, they ignore mortgaged property altogether.34

There was then a further change in 2025. The 2025 report said “wealth” only includes “listed company holdings, cash, bonds, gold, and crypto5 holdings”.6 The 2025 USA report says explicitly that “real estate assets are excluded”.

We should therefore see a change in the Henley & Partners figures between 2023 and 2024, and then another between 2024 and 2025.

Over the period 2023 to 2025, the fall in the number of millionaires should be dramatic. In large cities like London and New York, where one-third of a dollar millionaire’s net wealth is tied up in the home,7 eliminating property wealth should cause the number of millionaires to fall by around 20%.8

We don’t see any effects like this.

The data doesn’t change

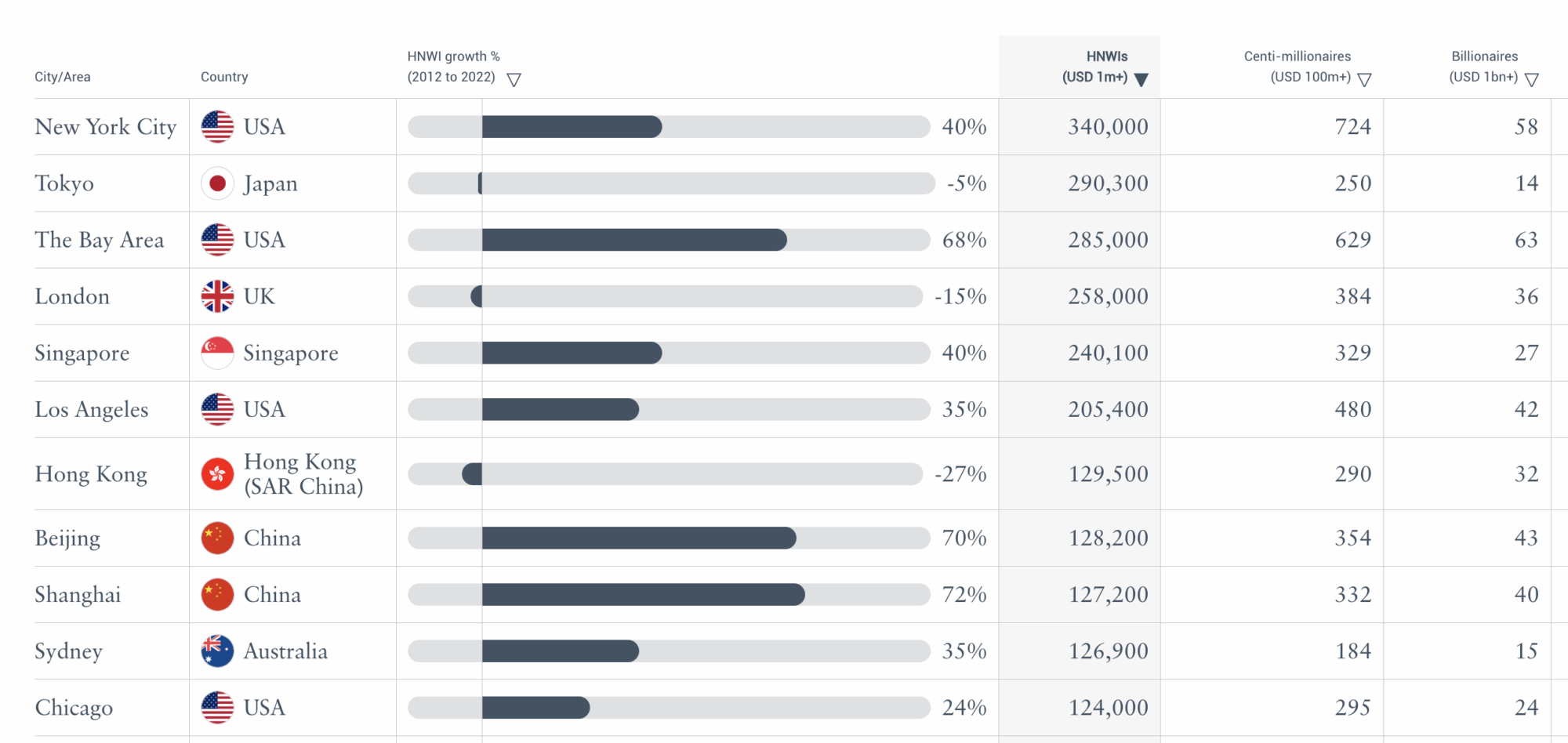

This is the Henley & Partners 2023 list of the world’s wealthiest cities. At this point the definition of wealth in the reports clearly included property – and these are cities where property is a big component of wealth:

The 2024 figures should show all mortgaged property dropping out of the data. A large amount of wealth should have disappeared, with the number of dollar millionaires dropping significantly (and a smaller effect on centimillionaires).

There should have been a particularly large effect in (for example) New York, the Bay Area and London, where large numbers of people are millionaires based solely upon their net property wealth.

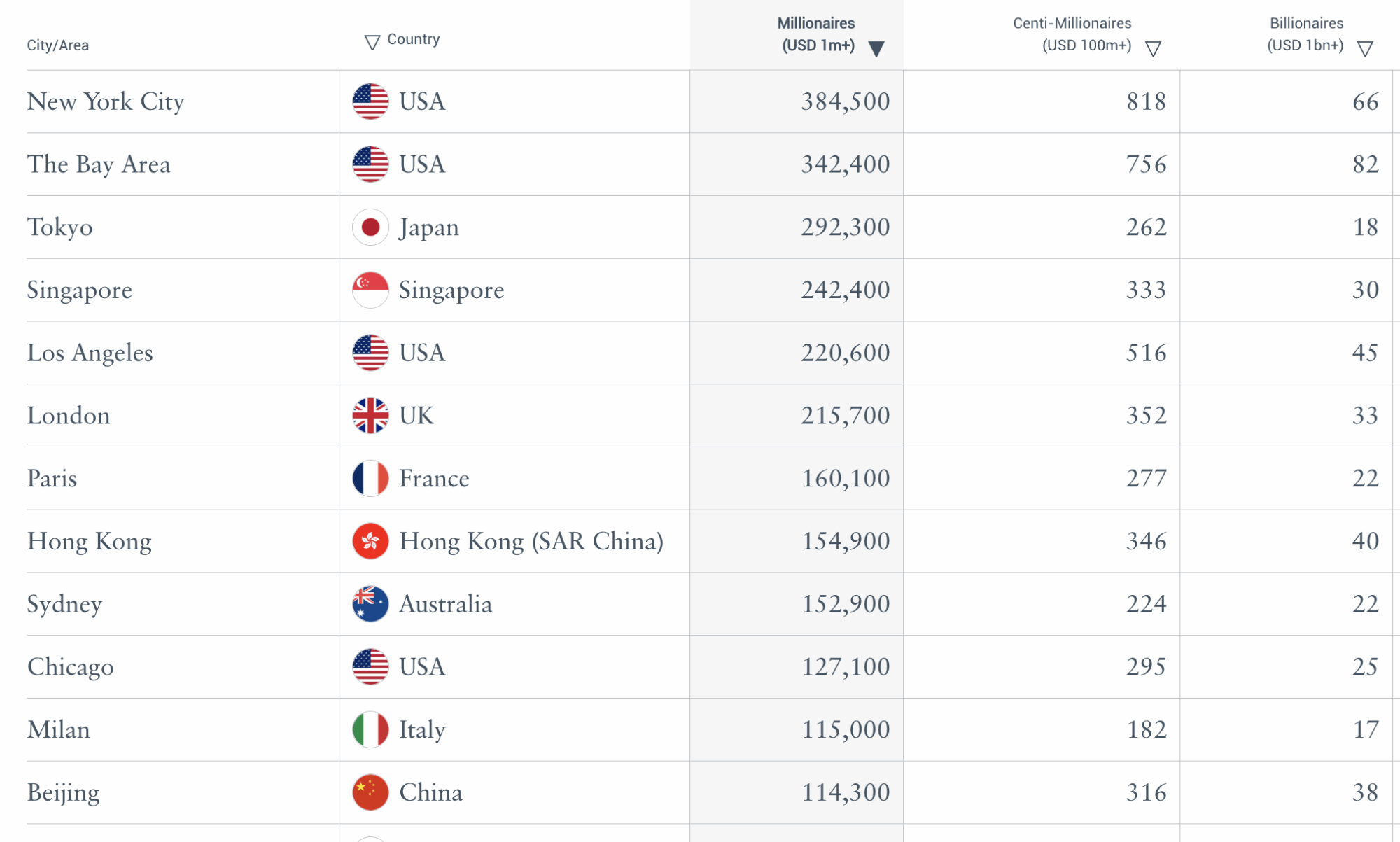

Then, when the final change in 2025excluded all real estate, we should have seen a further change, and overall a drop of around 20% in millionaire numbers in cities with high house prices. We don’t see anything like that:

And everything is presented as if the figures are comparable year-to-year.

It’s as if nothing happened.

What this means

New World Wealth ignored our questions – but when the Financial Times asked, the founder conceded that the model has never counted property wealth at all, even though the published “methodology” said it did.

New World Wealth then told the FT that the wording of the methodology was changed because there had been “a lot of question marks about why our numbers were so much lower than these Credit Suisse numbers . . . we probably had to refine the methodology to explain that”. This is revealing: when the data was criticised, their response wasn’t to revisit the data, but to change the stated methodology.

This could be deliberate deceit; it could also be a small firm out of its depth and acting out of panic. We don’t know – but it means we don’t believe any of the methodology can be trusted.9

There are suspicious patterns in the data

The Henley & Partners data is supposed to be the output of a model/calculation. We used standard forensic accounting techniques to detect whether this was the case.

Odd numbers

A common method used by forensic accountants is checking what percentage of numbers in a list of figures are odd. For many datasets it should be 50%, but humans often have a subconscious preference for even numbers.

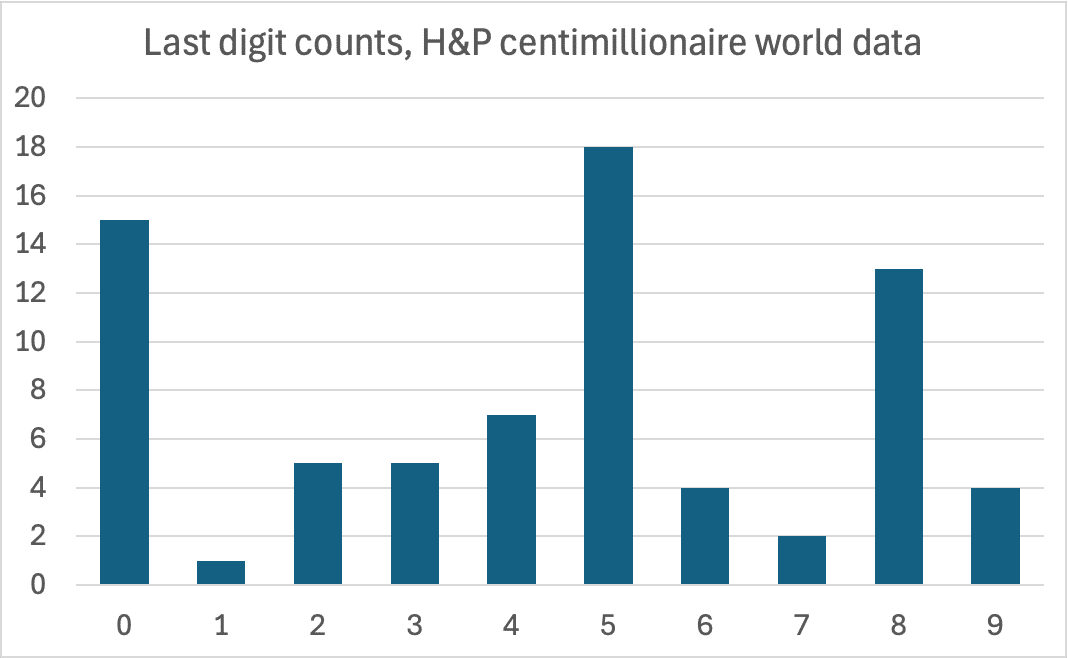

So we looked at the Henley & Partners data from 2022 to 202510 and checked the last significant digit in the counts of millionaires, billionaires (ignoring cases where the number is zero11), and centimillionaires:

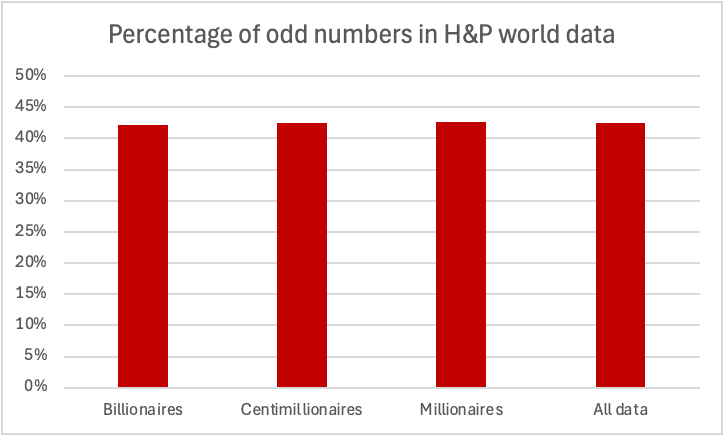

We’d expect to see as many odd as even numbers – but we don’t.12 There are many fewer odd numbers that we would expect: 42.5% out of 299 datapoints. The chance of such a result (or fewer) occurring by chance is 0.5%.13

The fact we are seeing such a similar percentage of odd numbers across the $1m, $100m and $1bn data (42.7%, 42.5% and 42.2%) suggests that the same process/person is responsible.

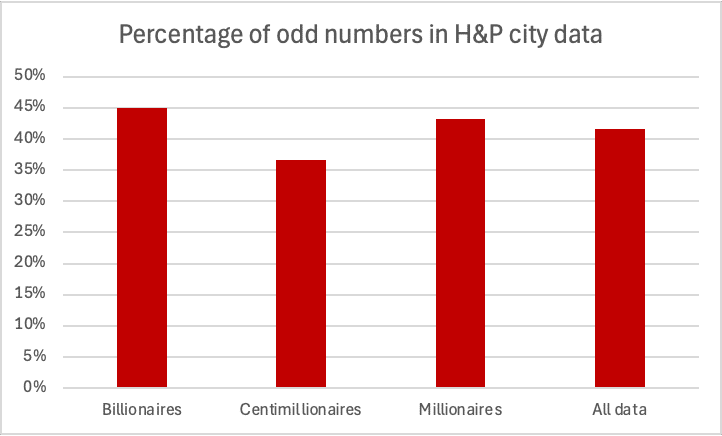

The city data is even more anomalous, with the centimillionaire data having only 37% odd numbers out of 210 datapoints – the probability of that being chance is 0.01%.14

We checked the last significant digit of the 159 migration‑flow numbers Henley published for 2022 to 2025. 41.5% of these were odd. That’s only 2% likely to have happened from chance.15

Distribution of digits

Another well-established technique for detecting rigged numbers is to count the last digits.

Imagine you’re investigating an election, and you suspect that the figures for the number of voters in each constituency have been faked.

Computers are pretty good at generating random numbers. Humans are surprisingly bad – we have funny biases. So you could go through all the voting figures and count how many times the last digit is a 1, how many times it is a 2 etc. You’d expect all the digit counts to be roughly the same – because for practical purposes the last digit is random, and so there’s a one in ten chance each digit comes up.

If you find that (say) most of the last digits are 0s, 5s and 8s, and there’s only one 1, then you’d have strong grounds for suspecting foul play.

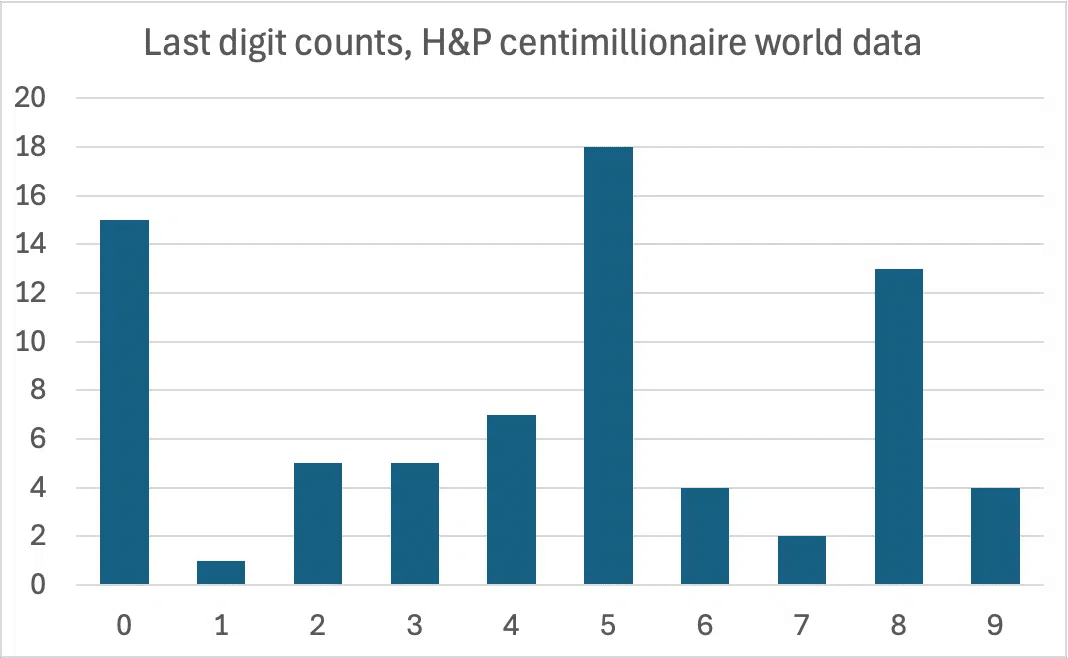

We did just that with the Henley & Partners data on the centimillionaires ($100m+) in each country,16 counting the last digits.17 And it turns out most of the digits are 0s, 5s and 8s, and there’s only one 1:

We can calculate how likely it is that this just happened through chance.

The probability of getting no more than one 1 is 0.4%.18 That’s unlikely – but the probability of the entire distribution being so peculiar is even less likely: 0.00042% or roughly one in 240,000.19

Forensic accountants often scrutinise datasets for this type of pattern, as it suggests that numbers were not the result of a direct count or measurement but were instead estimated or rounded to convenient figures. While this is common in budgets or forecasts, it is a serious anomaly in a dataset that purports to be a precise count of individuals. The additional spike in the digit 8, coupled with the near-total absence of the digit 1, further strengthens the case for artificial number generation.

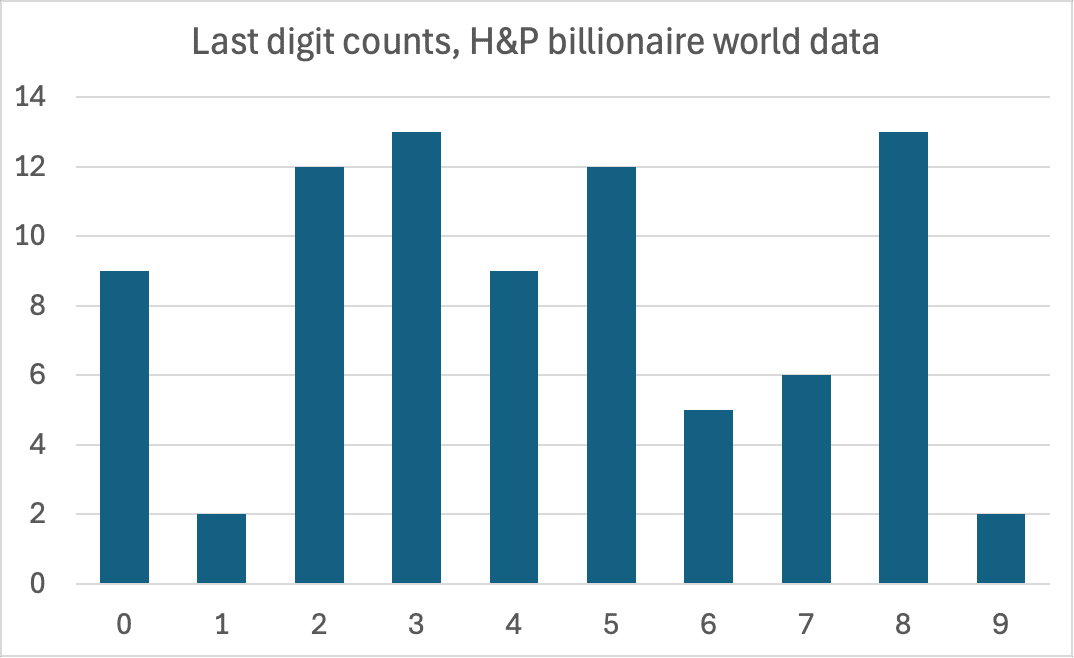

We also see a suspicious pattern in the billionaire data:

Again a lack of 1s. This isn’t as anomalous as the centimillionaire data, but still only a 2% likelihood such a distribution would arise through chance.20 This time rounding is not a good explanation, because there is no excess of 0s and 5s.

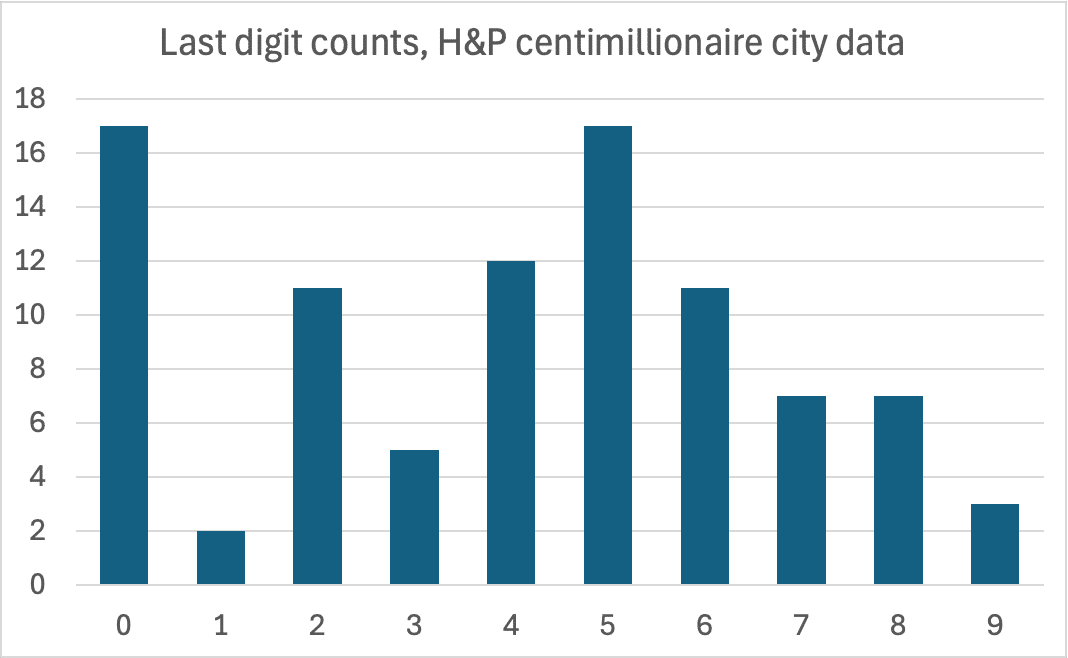

We then ran the same analysis on the Henley & Partners data for the number of centimillionaires in each city, again looking at the last digit:

Yet again, few 1s, and a spike of 0s and 5s. The probability of this distribution being chance is 0.1%.21

The city billionaire data has too many repeated entries for us to be able to obtain a statistically valid result.

Interestingly, we didn’t see similar statistically significant anomalous patterns in the city or country millionaire data. 22. We also can’t apply these statistical techniques to the migration flow data, as there isn’t enough variation between the numbers – they’re smaller and rounded.

Do other wealth reports have similar anomalies?

We ran a series of statistical tests on the UBS Wealth Report counts of millionaires.23

Here’s the last digit count, which shows the kind of random distribution we’d expect,24:

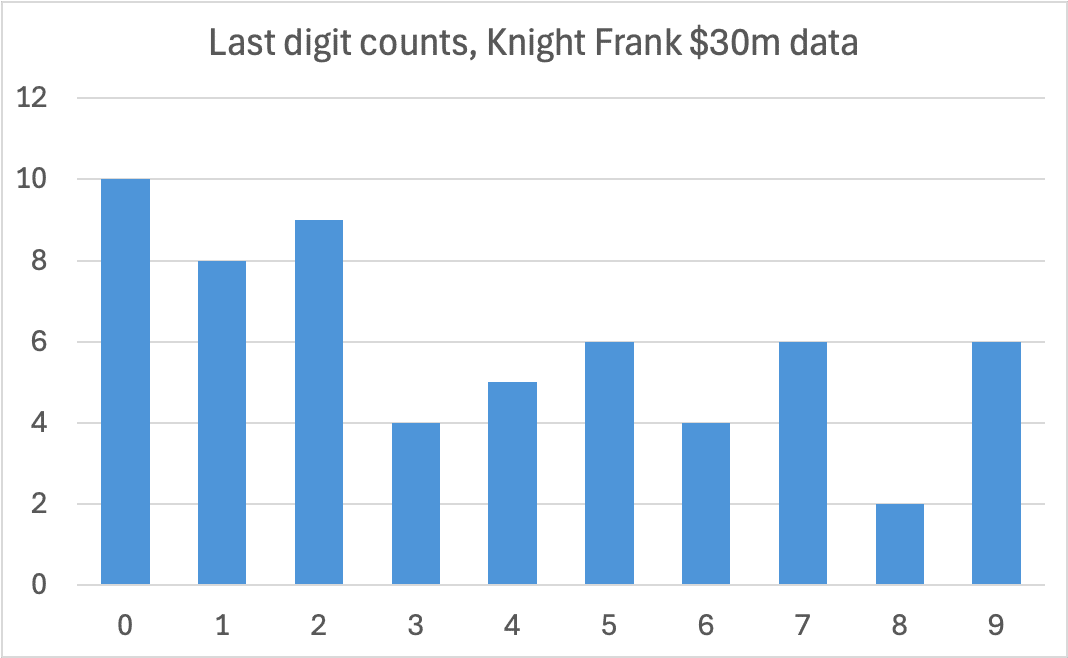

We also looked at data on the $30m population from Knight Frank.25 The smaller number of datapoints mean the distribution is “bumpier”, but it’s well within what we expect from random chance:26

We ran odd number checks against the UBS and Knight Frank numbers, as well as the most recent Forbes count of billionaires by country. All were in the expected range:27

Before the Henley & Partners reports, New World Wealth created migration reports for AfrAsia Bank for 2018, 2019 and 2020. The stated methodology is very different, and so we didn’t pool these with the Henley & Partners data. However, the format of the migration datapoints is very similar, and the data “looks” similar – so it’s noteworthy that when we run exactly the same tests on the AfrAsia Bank migration data as we did on the Henley & Partners migration data, we don’t see anomalous patterns in the AfrAsia Bank data.28

The even-number bias in the Henley & Partners data therefore looks unique:

Taken together, five independent sources – UBS, Knight Frank, Forbes, and the NWW AfrAsia migration reports – show digit patterns fully consistent with chance. The anomalies are unique to the Henley & Partners series.

Our analysis shows it is statistically almost impossible for the published centimillionaire and billionaire numbers to be the direct, untampered-with output of a financial dataset or model. The over-representation of figures ending in 0 and 5, and significant excess of even numbers, is a sign of human intervention.

The Henley & Partners migration data also looks highly anomalous, with an even-number bias that can’t be explained by normal processes.

We found a total of nine positive results, out of the 27 tests we ran. The likelihood of this being a coincidence is extremely low – many millions to one.29

This leaves two possibilities. The numbers could be fabricated. Alternatively, and probably more likely, raw numbers are taken from a calculation or model and then manually adjusted for unknown reasons before publication.

If these numbers are fabricated or manually adjusted, then it’s prudent to assume that all the other numbers may be too, particularly given the importance that the Henley & Partners methodology attaches to people with higher levels of net wealth. We’re just fortunate that the centimillionaire, billionaire and migration adjustments revealed themselves statistically; this won’t always be the case.

The remarkably steady millionaire/centimillionaire ratio

There are other oddities in the Henley & Partners city data. The ratio of millionaires to centimillionaires is curiously stable from 2023 to 2025:

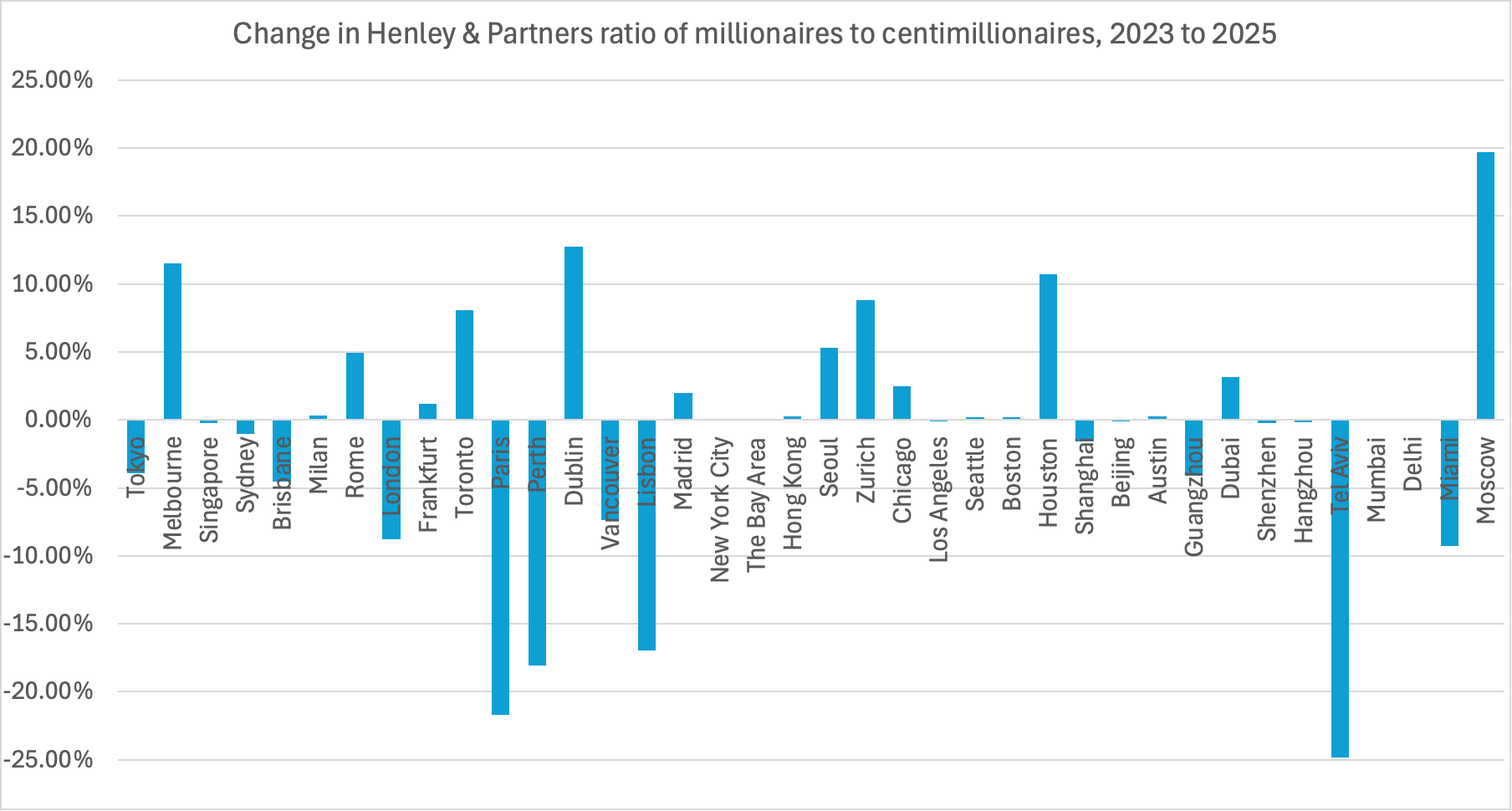

If we focus on the change in the ratio:

We see fourteen cities (38%) with a change in the ratio of less than 1%. Five (13%) show a change of less than 0.1%, with the numbers of millionaires and centimillionaires just happening to move by almost exactly the same percentage, so that the ratio was largely unchanged.

What’s even stranger is that these five are some of the world’s most economically dynamic cities: New York (0.09%), Los Angeles (-0.09%), the Bay Area (-0.04%), Delhi (0.01%) and Mumbai (0.07%).30 This adds to our sense that the data is artificial.

In reality we should see random noise in the millionaire and centimillionaire data. So an interesting question is: if millionaire and centimillionaire head‑counts are measured quantities that are correlated, but also wiggle around through ordinary economic forces, how often would the ratio between them end up almost perfectly unchanged?

We can answer this with a “Monte Carlo” simulation – running a million iterations on a computer in which we keep the millionaire/centimillionaire counts highly correlated, but add a degree of random noise (with the amount of noise taken from other wealth reports). We can then count how many of those million runs saw five or more cities with a change in ratio of 0.1% or less. This gives us a robust estimate of the likelihood of this occurring through sheer chance.

The result: only a 0.03% chance that five cities would see so small a change in ratio. The most obvious explanation: New World Wealth are applying an assumed common growth/shrinkage rate for some of the numbers, not a measurement.

The credibility of the Henley & Partners report rests upon it being able to identify millionaires, and then track them.

We don’t believe either is possible.

The description of the methodology for both 2024 and 2025 is extremely thin. There are significant changes between years, with additional data sources cited in 2025, but the consistency of the last three years’ results suggest that the methodology itself has not changed.

The firm that created the report, New World Wealth, has one employee. It’s plausible that one man could use public sources to identify CEOs and other prominent wealthy individuals, and then scrape LinkedIn data to find less prominent individuals in high-earning professions. However, other aspects of the methodology do not seem possible for even a large team to accomplish, much less one man:

Determining listed company holdings for CEOs is reasonably straightforward. For the very wealthy with a public profile, public estimates of wealth are available. Estimating wealth for less public people, on an individual (rather than population) level, is not possible. The idea that investment holdings, cash, and (in particular) crypto holdings can be identified on an individual is far-fetched. HMRC can’t see cash holdings – how can New World Wealth?

Determining property holdings (until they were excluded in 2024) is again not possible – either individually or at scale. Even those countries with public land registries, like the UK, don’t let you carry out reverse searches (i.e. finding where a named person lives).

The report also claims to assess net wealth, i.e. deducting levels of debt. We are unaware of any technique that can, either individually or at scale, determine a person’s level of debt.32

The methodology claims to track investment migration program statistics. However, these statistics are usually not available.33

There are then oddities like claiming to use “statistics from high-end international removal firms”. We don’t believe this could be integrated into migration data in a useful way.

The report claims to determine the “true” location of high net worth individuals (particularly investors with net worth of over $30m) using “LinkedIn and other business portals”. That is not possible. LinkedIn data is not reliable.

NWW also claims to use “company registers — with a focus on filings by directors that indicate a change in country of residence”. However company registries are not openly accessible in most countries and, when they are, residence is usually not kept up-to-date.34

Even where high net worth individuals could be identified on LinkedIn, linking that data to other data about the same individual is not trivial. Even linking one name to UK Companies House entries is notoriously difficult. Yet New World Wealth would have to do this for 150,000 individuals worldwide. We don’t believe it’s possible, and certainly not for a one-man firm. So if even they could track millionaires, and could track migration, they wouldn’t be able to marry the two datasets up.

For the very wealthiest, determining the place of residence is often not possible even conceptually: they often have multiple homes in multiple countries, and spend no more than a few months in each one. Even tax authorities can struggle to assess residence.

The author of the study claimed in an interview with Tim Harford that NWW “track people on LinkedIn and other business portals” and that “the bulk of the database is between $20m and $100m in assets”. We don’t believe LinkedIn can be used to identify 75,000+ people who have more than $20m in assets.

There is a suggestion in the report that the true methodology is to estimate salaries35 and then assume that someone with a salary of $200,000 will typically have a million dollars in net liquid assets. If so, this is a bad mistake – the assumption is not correct. HMRC and ONS data suggests that about 3% of UK taxpayers earn £150k/$200k, but only about 1% of UK taxpayers have net financial wealth of £850k/$1m. The reason is obvious: if you earn £150k then your take-home pay is around £91k. It’s certainly possible to save $1m on that income, but it will take decades rather than years.

Before New World Wealth created reports for Henley & Partners, its client was AfrAsia Bank. These reports present apparently comparable (and very similar) migration data but the only cited sources are investor visa programme statistics (which, as noted above, are very limited), interviews with HNWI intermediaries, and tracking HNWI media reports of migrations and property purchases. All of that LinkedIn data appears to have made little change to the results.

If New World Wealth really did track 150,000 individuals’ on LinkedIn they would have to be registered under GDPR in the UK and at least one EU country. New World Wealth are not registered in the UK and we haven’t located any EU registration.

One experienced wealth researcher told us:

“The only asset class for which I would believe they might have semi-reliable info is major shareholdings of listed companies – which is what most of the Sunday Times Rich List relies on. Anyone claiming they have good public data on any other asset class is making it up; it simply does not exist.“

The H&P reports contradict other data

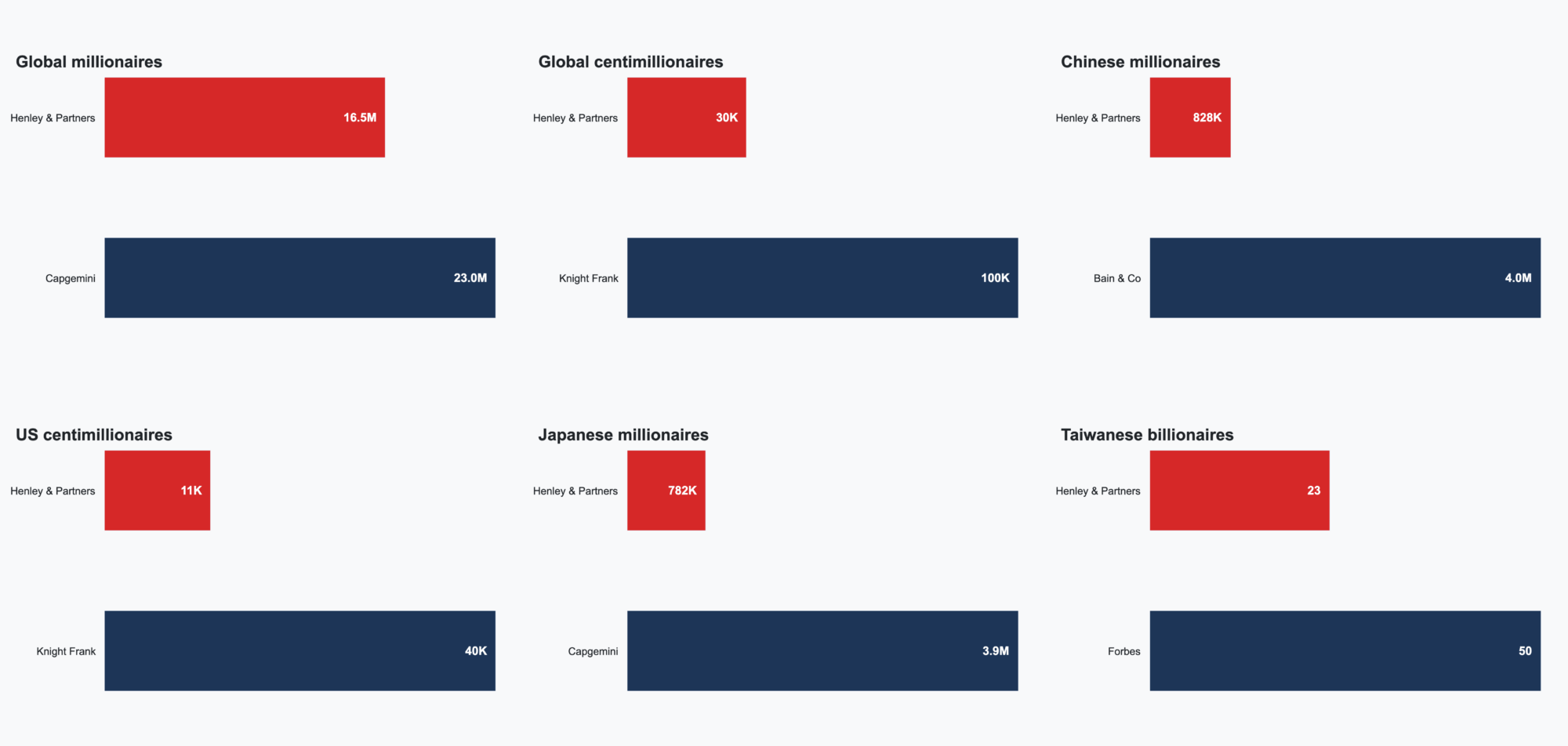

The number of UK millionaires and centimillionaires in the Henley & Partners reports contradict official statistics:

The stated number of dollar millionaires in the UK – 578,400 – is too high. We have reasonably reliable data from the ONS, which shows that about 1% of UK taxpayers have net financial wealth of £850k/$1m, i.e. around 300,000 people.

Conversely, the stated number of dollar centimillionaires in the UK – 730 – is much too low. HMRC data suggests the correct number is around 3,400.36

Given there are about 3,400 centimillionaires in the UK, the idea there are only 10,000 in the USA, and only 30,000 in the world, seems far-fetched.

There are numerous other results that look odd. Checking almost any figure with other reports (e.g. Bain & Company, Knight Frank, Capgemini, Forbes) makes Henley & Partners look like an outlier:37

The results aren’t representative

When we want to investigate something about a large population – voters, shoppers, or millionaires – we usually can’t speak to everyone. So we survey a subset called a sample.

For the survey’s conclusions to be trustworthy, that sample must be representative: its members should mirror the broader population’s key characteristics (age, income, geography, attitudes, and so on) in roughly the same proportions. Sometimes you can achieve this by picking people randomly (for example when conducting an exit poll). Often you can’t, because the way you are picking people will skew the results (people who answer a landline are likely more elderly than people who don’t).

A well-designed study therefore begins by defining the population clearly, selecting participants who reflect that population (as best you can), and then applying statistical weights or other adjustments to correct any imbalances that remain. Bigger samples help reduce random error, but sheer size cannot fix systematic bias: if the people you reach are untypical, larger numbers merely give you a very precise answer to the wrong question.

The Henley & Partners report claims to survey 150,000 people (assuming for the moment this is true). The methodology says there is a “special focus” on those with over $30m of listed company holdings, and the “primary focus” (50% of the database) is on company founders. These are two different things. But all the published data talks about “millionaires” (defined to mean $1m liquid wealth). These are different groups of people, and conclusions about one group do not apply to another. That suggests that the sample is highly unrepresentative.

Economic journalist Tim Harford interviewed the author of the report last year, and asked why he didn’t use a representative sample. The response was: “Well I would argue it is a representative sample. 150,000 people, that’s a lot… polls are normally done on less than 1,000. So 8,000 [the number surveyed in the UK] is quite a big number”. This is not how statistics work – an unrepresentative sample does not become representative as it gets larger.38

It is very surprising that the author of so widely cited a report has never heard of statistical sampling.39

One might conclude from this that the survey places an unrepresentative weight on the very wealthy, and so over-estimates $1m millionaire movement, but provides a good guide to $20m+ millionaire movement. We don’t think that would be correct, because even if the report really surveys the $20m+ population accurately, the people sampled are not representative of that population.4041

Tax Justice UK recently published a paper critiquing the Henley & Partners report.42 We agree with many of the statistical and methodological criticisms made by TJN. We don’t agree with TJN’s subsequent use of the report as evidence that that only 0.3% of millionaires are leaving the UK and therefore there is no “exodus”. The 0.3% figure would be wrong even if Henley & Partners were right43 but, more importantly, if a report has no statistical validity then the correct answer is to say that no conclusions can be drawn from it.

Henley & Partners’ response

We put the issues identified in this report to Henley & Partners. They haven’t seen any more detail on the New World Wealth data than is visible on their website, and they don’t appear to have anyone with statistical expertise on their staff. If the report is fabricated, they don’t know it.

Henley & Partners did say that the consistency of the report, and the fact it showed trends that matched their practical experience, made them believe it was real. But it’s hardly a surprise that the report matches Henley & Partners’ experience, because it uses client data from Henley & Partners.

Nor is “consistency” an answer to our criticisms. The reports may be consistent44 – but it seems likely they are consistently wrong. And the “consistency” is itself problematic when the methodology changed so dramatically from 2023 to 2025.

We wrote to New World Wealth for comment on two occasions before publishing this report, but did not receive a response. As noted above, they admitted to the FT that the methodology had never included property (even though it said it did). They didn’t respond to the FT regarding the other irregularities in the data.

New World Wealth’s founder and sole employee, Andrew Amoils, did provide comments to Spear’ Magazine. These are illuminating:

“In response to the claims made about the removal of property wealth from the methodology, Amoils said that only a very little amount of debt-free investment property was included previously and so the ‘impact of stripping it out was small’”

This looks like an evasion. Until 2024, New World Wealth claimed to include all real estate in their figures. In 2024 they removed indebted property. In 2025 they removed all property. These changes should have resulted in a c20% fall in millionaires in London, New York, and other cities where real estate makes up a significant component of wealth.

“On being the only person at his firm, Amoils said: ‘The “one-man firm” argument sounds good in print. However, the truth is even the big market research houses of 500 plus employees don’t put their whole team on a wealth report. They would typically put three people max.’”

This again looks like an evasion – Mr Amoils is not actually denying that he is the sole author of the New World Wealth reports. As for his claim that other firms only name three people as authors of wealth reports, this is from the 2025 CapGemini wealth report:

And:

“He added that the quantity of even numbers was a consequence of the rounding system he employed, where figures are rounded to the nearest 50, 100 or 1,000 depending on the report. ‘It is important to remember that our figures are not exact, they are modelled estimates, which is why we round them,’ he says.”

Mr Amoils either hasn’t read this report or hasn’t understood it. We looked at the last significant digit. What we saw wasn’t rounding, but something much more suspicious, for example:

The many anomalies in the report mean that we consider the 16,500 figure to be meaningless. There’s also a more fundamental problem: figures on millionaires leaving cannot be translated easily into figures on non-doms. There are around 300,000 people in the UK with net liquid assets of $1m, but only about 21,000 non-doms (many of whom are not millionaires).45

The OBR expects 25% of the wealthiest non-doms to leave (those who use trusts) and 12% of other non-doms.46 The private wealth advisers we speak to estimate that perhaps 5% to 10% have left already. That’s fewer than 2,000 people – they’ll be invisible in even accurate estimates of the total numbers of “millionaires” leaving the UK.47

Our conclusion

The Henley & Partners reports do not do what they say they do. They do not count millionaires, centimillionaires and billionaires by reference to their “liquid investable wealth”. They don’t track migration. The stated methodology isn’t applied, and is probably impossible to apply. There are, at the least, significant manual adjustments to the figures, for whatever reason. The figures contradict authoritative data.

We believe Henley & Partners should withdraw their reports until they have been audited by a suitably qualified independent third party. In the meantime, they shouldn’t be relied upon by policymakers, journalists, or anyone seeking to understand global wealth or migration trends.

Many thanks to B and K for their help with this report, D and I for their statistical and methodological analysis, P and C for their forensic accounting expertise, Y for country advice, and all the private wealth experts who spoke to us.

Our spreadsheet with the forensic analysis and statistical calculations can be found here. All data from Henley & Partners/New World Wealth, UBS/Credit Suisse, Knight Frank, Forbes and Cap Gemini is their respective copyrights, and reproduced here for the purposes of criticism and review, and in the public interest.

Footnotes

At the end of this article we discuss what the actual migration figures may look like. However we note this point up-front because we don’t want this report to be used to suggest that non-doms are not leaving the UK. We believe it’s clear that they are (and also clear that this is what the OBR expected). ↩︎

Earlier reports were consistent with this. The 2022 Global Citizen reports said “private wealth” includes property (there were multiple reports that year and they are consistent). The Africa report from 2022 says “It should be noted that the average HNWI worldwide has the bulk of their wealth tied up in residential property and equities, so large movements in these two segments impact heavily on the total private wealth held in a country”. The earlier NWW reports for AfrAsia Bank included property. ↩︎

So, for example, someone who borrowed $1m against their $5m penthouse will have had $4m of wealth identified in the 2023 report which disappeared from the 2024 and 2025 reports. Mortgaging property is common even for the very wealthy, either to avoid “locking up” cash in non-yielding assets, or for tax purposes. Similarly, real estate held for investment (even by the very wealthy) will normally be leveraged, because it increases the yield. ↩︎

The main 2024 report is a little more ambiguous – it doesn’t define the term “wealth”, but says that property has a “significant impact on wealth”. ↩︎

There are various public lists of large crypto investors; they are unreliable and only reflect a small proportion of the overall population. ↩︎

Although, when interviewed by Tim Harford, the author of the report said he “mainly” surveyed “listed company holdings and some cash holdings”. ↩︎

If we give households the full benefit of a 30 % equity rally over this period, and (generously) assume they are one-third invested in equities, the elimination of property wealth means anyone worth $1m to $1.2m in 2023 would cease to be a millionaire in 2025 (because $1.2m x (1/3 x 1.3 – 2/3) is less than $1m). A Pareto distribution with α ≈ 1.35 implies around 54,000 people in London fall in that range – roughly 20% of all millionaires. ↩︎

There are also undocumented changes in methodology. The 2022 “Global Citizen Report” figures are substantially different from the 2023 figures, with the number of UK millionaires falling by 12% and the number of Japanese millionaires falling by 30%. Possibly the Global Citizen report is using a different approach – but the lack of any published methodology means we don’t know what. We have excluded the Global Citizen data from our report, although it may bear further analysis. ↩︎

The 2021 Henley & Partners reports don’t contain any detailed data. For earlier years, New World Wealth reports were published by AfrAsia Bank in 2018, 2019, 2020. The stated methodology is very different (see further below), so we didn’t pool this with the Henley & Partners data. However we did check for odd/even numbers and did not see anomalies in this dataset – see below. There was no data for 2020/21 because of lock‑downs and border closures. ↩︎

We were pooling different years’ of data, which is appropriate provided the odd numbers across the data are independent. This is generally the case, with the exception of the billionaire data, where three countries had a repetition year-on-year. We removed the repetitions from the datasets (but retaining the repetitions does not materially change the result). ↩︎

There’s an important but subtle point to watch when applying these techniques. Rounding can produce outputs which are skewed towards even trailing digits if a rounding mode known as “round-to-even” or “banker’s rounding” is used. Spreadsheets generally don’t use round-to-even rounding, but most programming languages do. Great care therefore needs to be taken when applying forensic techniques to data which (for example) was created by a computer programme which rounded a pre-existing dataset containing figures to one decimal point. In such a case, banker’s rounding of random numbers would only be expected to produce 45% odd trailing digits. The likelihood of observing 127 odd numbers in a sample of size 299 would therefore be 20.6%. However, the issue becomes much less significant where the underlying dataset has more than one decimal point (as 2.5 would round to 2, while 2.51 or 2.501 would still round to 3). We therefore don’t believe banker’s rounding explains the results found in this report. ↩︎

One-tailed binomial test, p = 0.0054. The individual results are not significant: p = 0.094, p = 0.066 and p = 0.084 respectively; however given all the results are independent outputs of one process, it is appropriate to pool them together. ↩︎

Centimillionaire result, p = 0.000068, millionaire result p = 0.035, billionaire result p = 0.084, overall result p = 0.000018, but obviously that is dominated by the centimillionaire result. There are repeated datapoints in the billionaire set so, even if we had found a significant result, we would have regarded it with scepticism. ↩︎

p = 0.019. Most of the migration flow numbers are given to the nearest hundred, and so we divide by 100 to obtain the last significant digit. However in 2025 (but not earlier years) numbers under 500 are rounded to the nearest 50. For the 2025 dataset only, we therefore divided all numbers under 500 by ten. We were concerned this might have introduced an element of subjectivity and therefore double-checked by instead binning all migration numbers under 1000 for all years. That left only 58 numbers, of which 38% had an odd last significant digit (p = 0.0060). We are therefore reassured that we did not inadvertently bias the data (and 58 is still high enough for validity). The curious consequence of binning numbers below 1,000 may indicate a higher level of manipulation for larger countries. ↩︎

We used all their data from 2023 to 2025 – as we note above, the 2022 data appears to use a different methodology (for an unknown reason), and we don’t think it’s appropriate to assume that the earlier AfrAsia reports are comparable. For many statistical tests one wouldn’t put different years together, because that means the datasets aren’t independent. However for this test it’s different, because we’re looking at the last digits. None of the centimillionaire number counts remain the same year-on-year, and so we can regard them as independent and pool the years. The first digits however would not be independent (because it’s likely the first digit of the millionaire count would be the same year on year), and so we did not test for first digit frequency. ↩︎

But only where there are three digits in the data, because otherwise you get a Benford-style distribution. For trailing digits, Benford converges to uniform as soon as we get past the first two positions. ↩︎

There are 74 last digits. The chance that none are a 1 is 0.90 ^ 74 = 0.00041. The chance that only one is a 1 is 74 x 1/10 x (9/10) ^ 73 = 0.0038. Adding them together = 0.4%. ↩︎

We used a chi-squared test – this is a statistical test that compares an observed frequency with an expected frequency, and calculates the likelihood that the difference is due to chance. ↩︎

vs a uniform distribution, p = 0.016. A Benford test is unlikely to be appropriate here, but we ran as a check, and p = 0.015. ↩︎

We can’t use the last digit, because the data is rounded to the nearest hundred, so we looked at the “thousands” digit instead. That found no anomalies. A Benford-style test on the first or second digit doesn’t give a statistically significant result, because the number of datapoints in any one year is too small, and combining years is not appropriate because (unlike last digits) first (usually) and second (often) digits are consistent from one year to the next – the datasets aren’t independent. ↩︎

Full data is available for 2020 and 2019 to 2025. The UBS definition of “millionaire” is different from Henley & Partners’, because it isn’t limited to liquid wealth, but that’s not relevant for the purpose of these forensic tests. ↩︎

51% of the 180 UBS numbers are odd (binomial p = 0.42), 50% of the sixty Knight Frank numbers (p = 1), and 52% of the 81 Forbes billionaire counts (p = 0.41). ↩︎

52% of the 61 AfrAsia migration datapoints were odd, p = 0.40. ↩︎

When running several different tests against multiple data sources there is always a risk of achieving positive results solely through chance. More cynically, a researcher can keep running different tests against different subsets of data until eventually finding significant results (i.e. cherry-picking or “p-hacking“). It is therefore important that we disclose all the tests that we ran, with positive and negative outcomes. There were seven H&P datasets – millionaires, centimillionaires and billionaires for cities and the world, plus the migration data. On each of these datasets we tested first and (except migration) second digit Benford’s law, last digit distribution and last significant digit odd/even. That’s a total of 27 tests, of which nine were positive (p <= 0.02). If the data was in fact not anomalous, we’d (on average) expect to run 50 tests before chance gave us a p = 0.02 positive. The chance of fluking nine or more positives under a binomial (n = 27, p = 0.02) model is 1.7 × 10⁻⁹ (≈ 1 in 600 million, but this understates quite how unlikely it is, given that in most cases our results were more significant than p = 0.02). ↩︎

This can’t be down to rounding, because NWW give precise centimillionaire numbers and millionaire numbers to the nearest hundred (so for e.g. London that’s four significant figures. ↩︎

We deliberately used low‑ball volatility (5 % vs the 8 to 15 % many surveys record) and a high 0.7 correlation between centimillionaire and millionaire numbers; even under those gentle assumptions, the odds of five major cities seeing <0.1 % ratio movement are ≈ 0.03 %. Tougher but still realistic parameters drive that probability essentially to zero. If we go the other way, and make the correlation unrealistically high – 0.95 – the probability of seeing five cities with so little change remains well below the usual significance level: 0.5%. ↩︎

Nor do we believe it would be possible to use rules-of-thumb, e.g. average levels of debt, and obtain a meaningful result. ↩︎

There are some exceptions. The UK, US, Portugal and Greece publish data (e.g. Portugal attracted around 2,000 high net worth individuals over ten years). Italy published figures in the numbers taking advantage of its flat tax scheme for wealthy migrants: from 2017 to 2023, around 4,000 people used the scheme. The numbers are small and (even where available) have little impact on country migration figures. ↩︎

For example by scraping job titles/employer from LinkedIn and then using other sources like Glassdoor and Payscale to estimate the salary. ↩︎

In this document, HMRC says there are 5,000 people with £50m+ of assets and 2,500 people with £100m+ of assets. We understand these are more than estimates, and that HMRC actively monitors this population individually. We can use these figures and the number of millionaires from ONS data to estimate the number of people with £73m/$100m of assets. Note that there are credible studies showing that the wealth of the very wealthiest is systematically under-counted, and therefore not always visible to HMRC – HMRC doesn’t know the number of billionaires in the UK. Hence the true figure for the number of centimillionaires may well be higher than the 3,400 figure. ↩︎