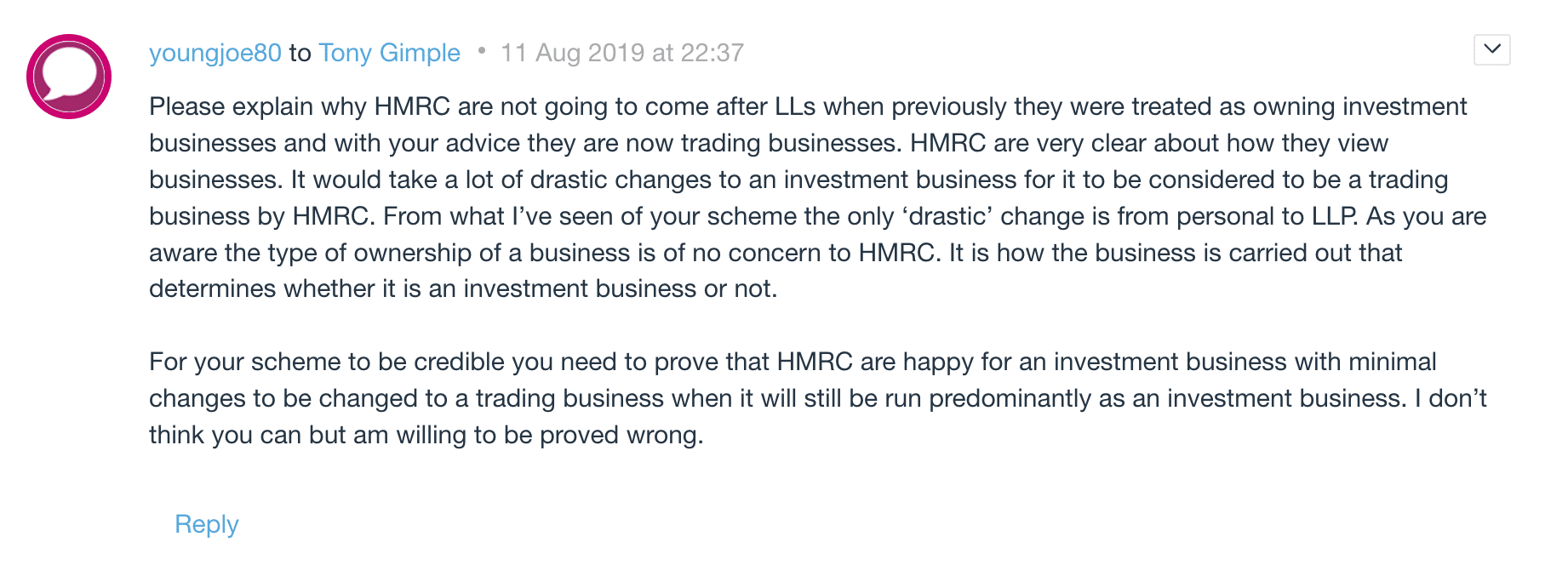

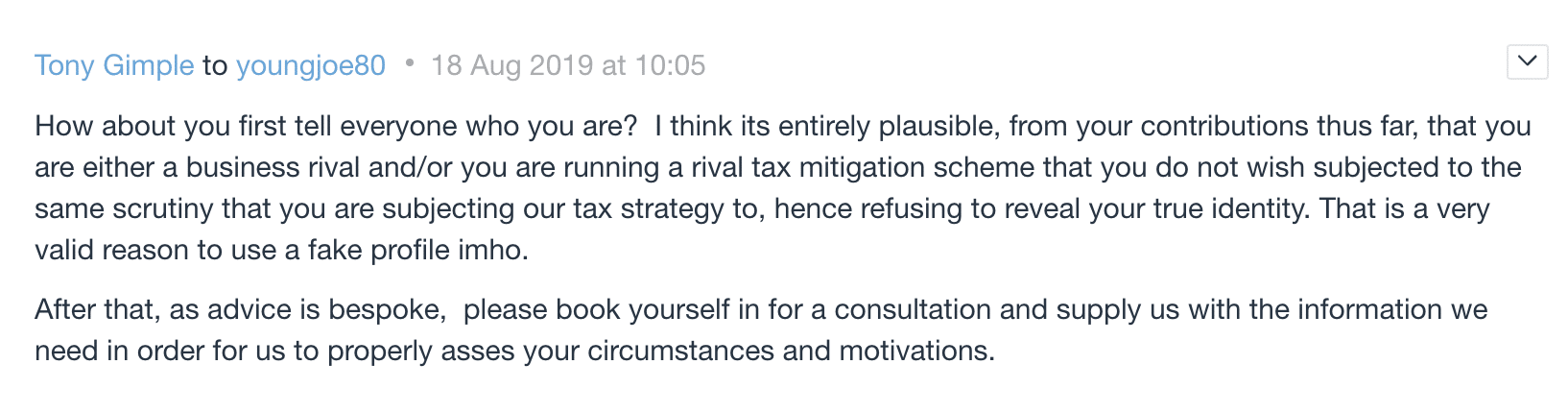

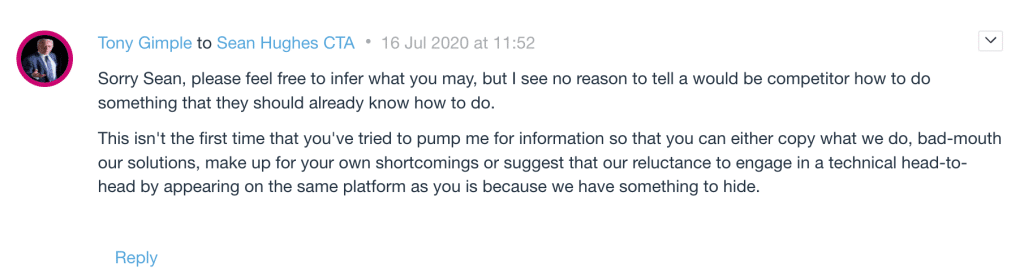

There’s an enormous and largely invisible campaign to use fraudulent notices under the US Digital Millennium Copyright Act to remove critical articles from the internet. We don’t know who is running the campaign, but we do know it’s facilitated by Google’s amazingly trustworthy approach to DMCA complaints made by companies that don’t exist.

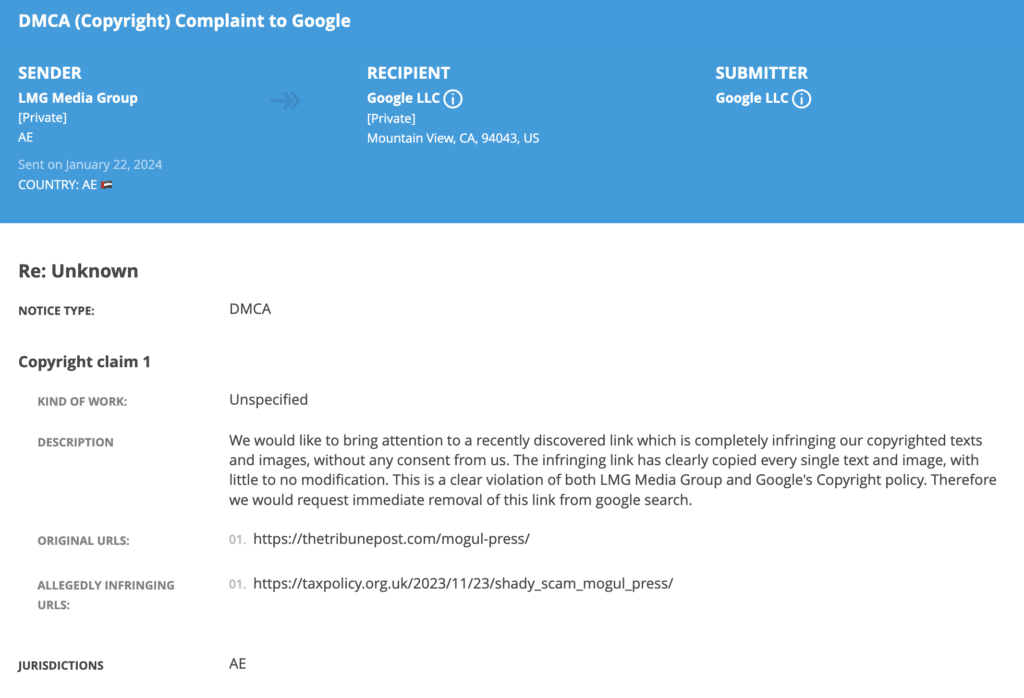

The notice was sent by “LMG Media Group” in the UAE. I don’t believe it exists – but Google rather brilliantly accepts takedown notices without checking if the person filing it exists.

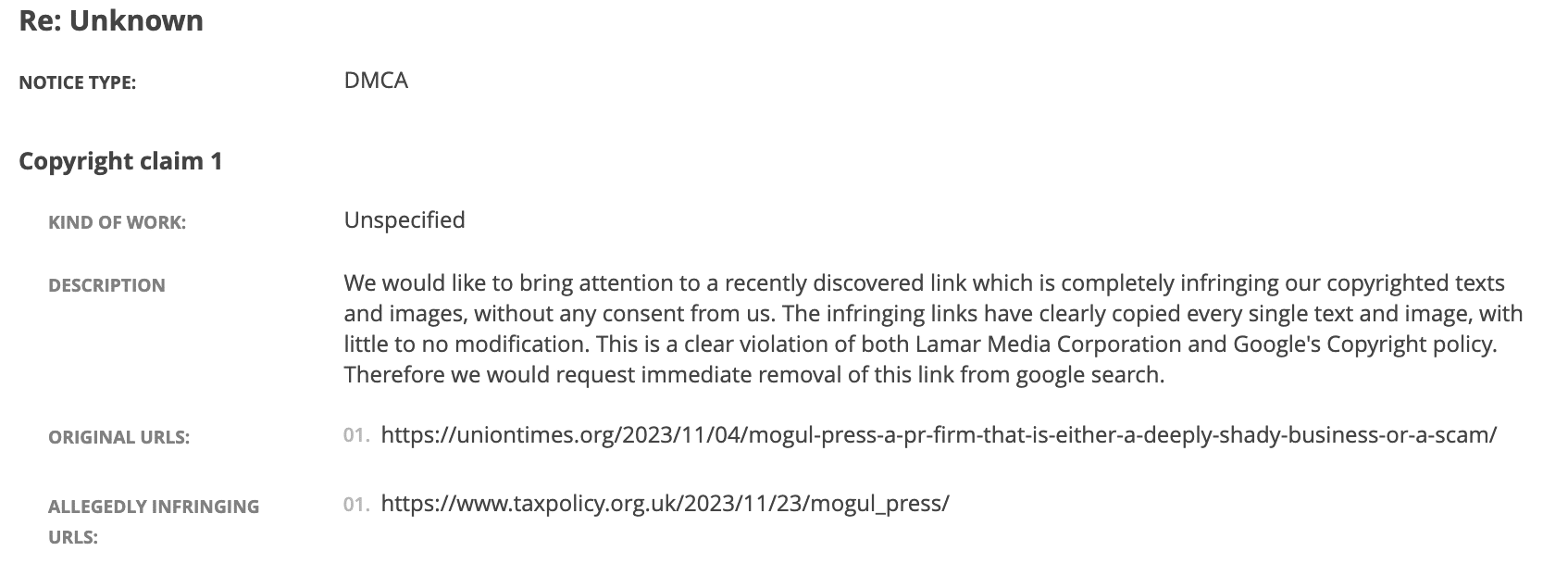

Another identical notice was sent by “Lamar Media Corporation” in the US, which also doesn’t appear to exist:

The intended effect is to remove my article from Google searches.3

Note the unusual wording of the two notices: “completely infringing” (which reads like someone without legal training trying to sound like a lawyer).

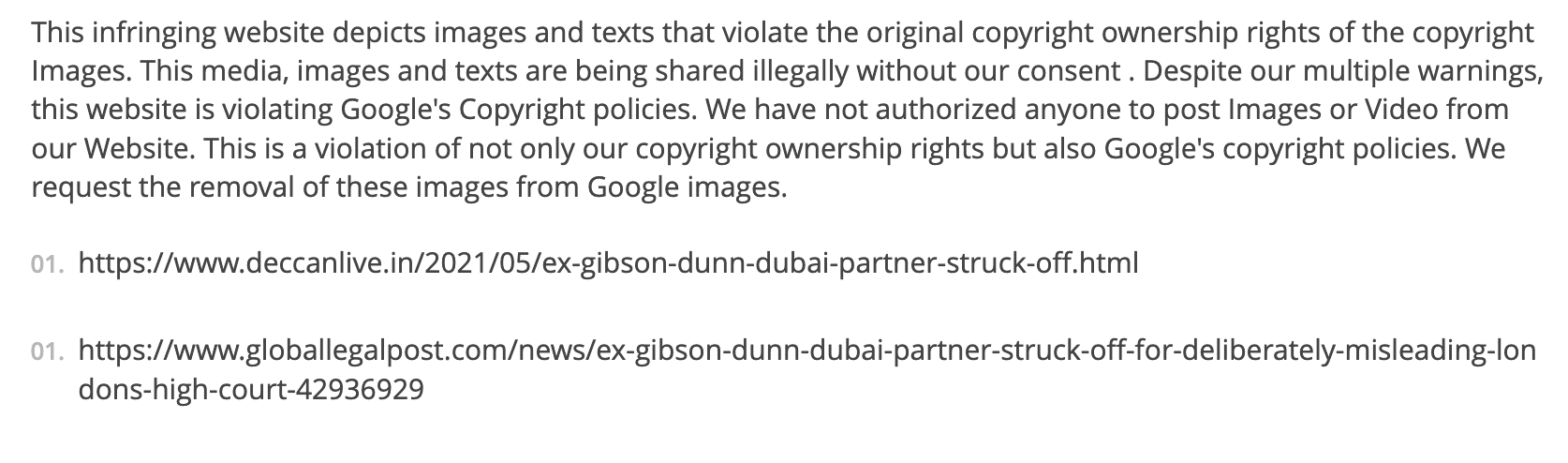

With a duplicate from another made-up company (“Ventuky Media Corporation”), and another from “Bryan Media Corporation”, and another from “Yan Media Corporation”, and another from “Richards Media Corporation”, and another from “Venkata Media Corporation”. There are many more.

The fraudulent companies set up automated systems that can file zillions of complaints instantly. The victim, however, is unlikely to have any automated way to file counter-notices… they’ll have to do so individually. It’s also widely believed that the more reports Google receives, the greater the chance it downgrades the target website in its ranking.

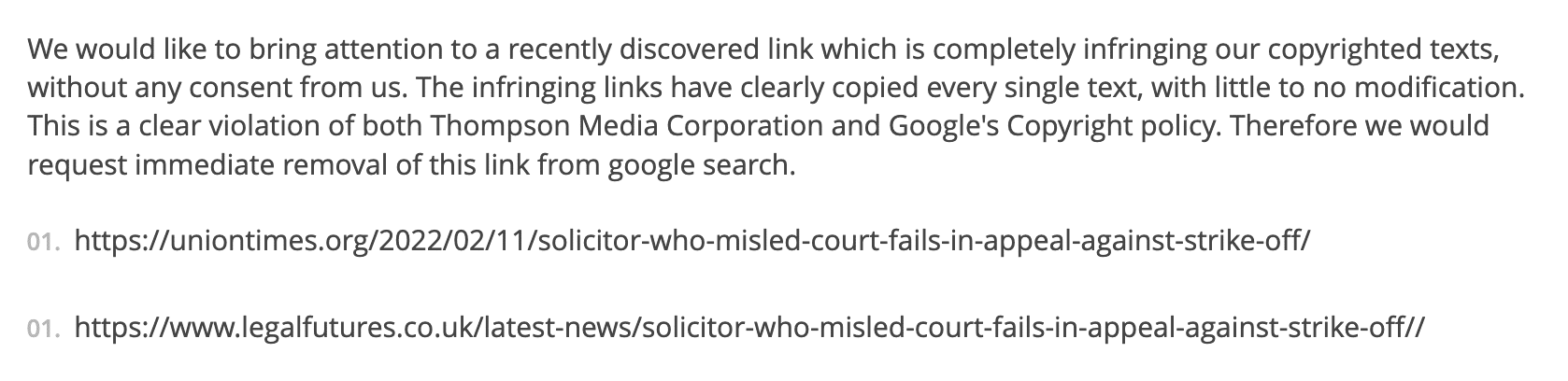

And others have been at this. If you google the name of the solicitor and “striking off” you’ll see some search results, then this:

It claims to be sent by BR Law & Co in Abu Dhabi. BR Law does exist, and has an office in Abu Dhabi, but doesn’t style itself BR Law & Co. I asked BR Law for comment and didn’t hear back.

The former solicitor concerned, his old law firm and his current law firm all deny any involvement in these takedowns. I believe them; even if we ignore the ethics and legality, why take action in January 2024 to remove news from six months earlier? So the identity of those responsible remains a mystery.

Similar searches reveal more attempts to takedown inconvenient reports.

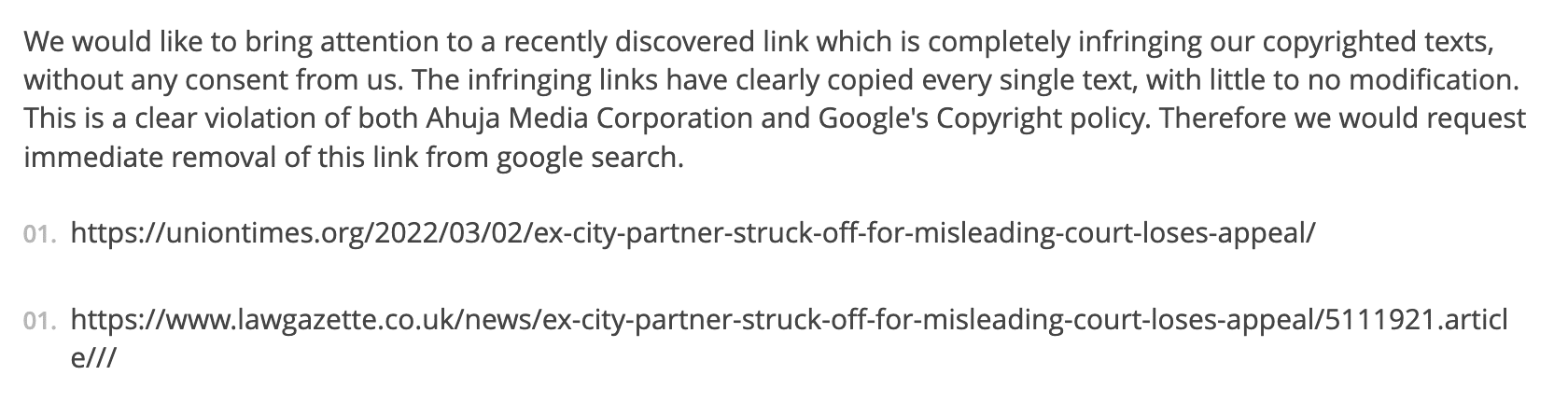

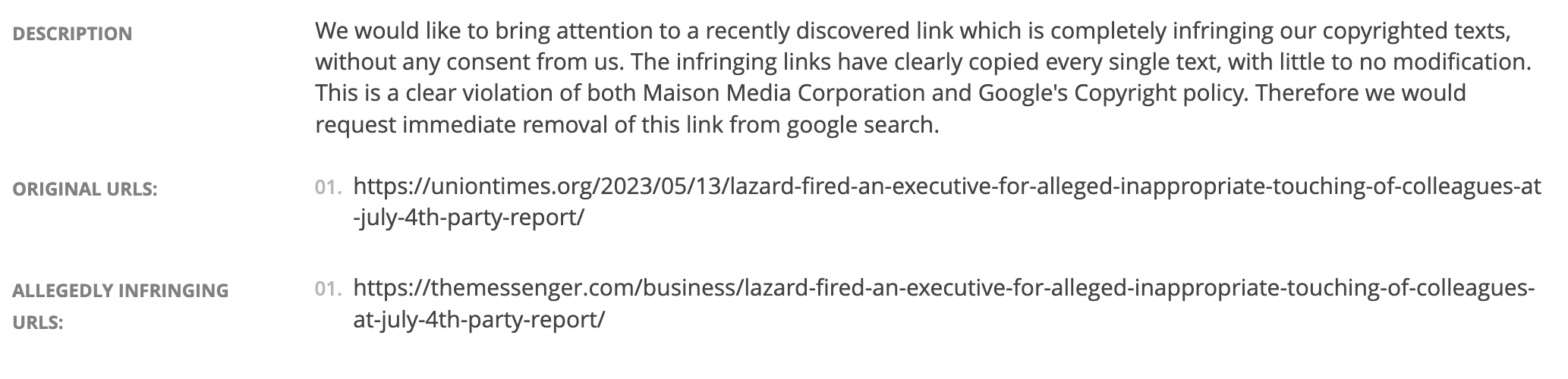

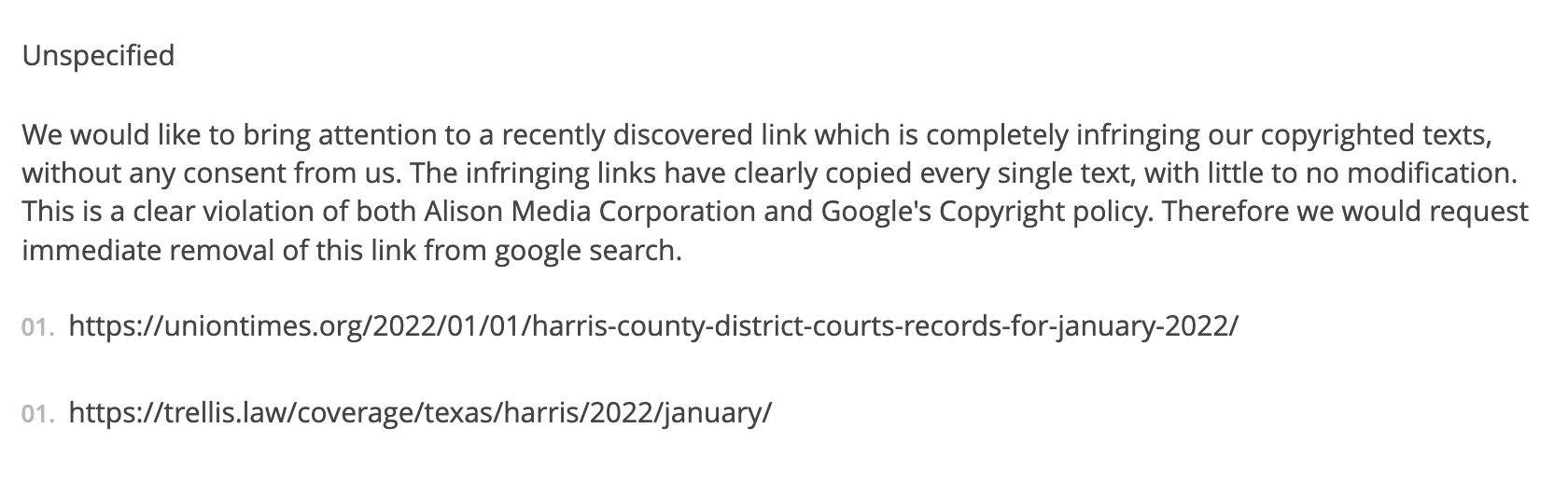

And this – it’s unclear why Alison Media Corporation (which again doesn’t exist) is trying to take down a Harris County court report (link now dead), but they are:

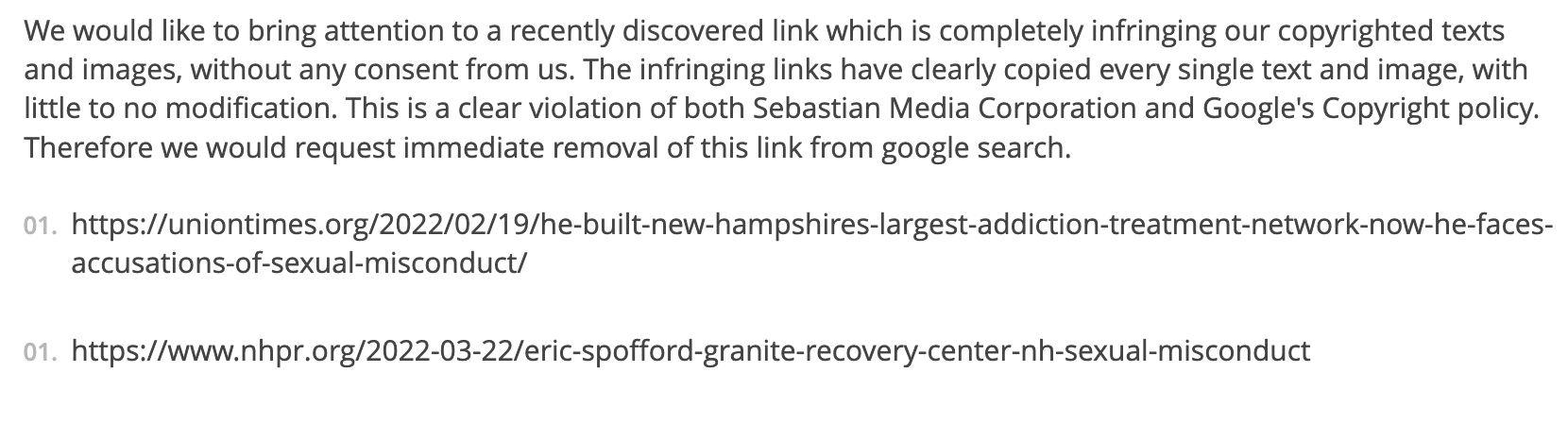

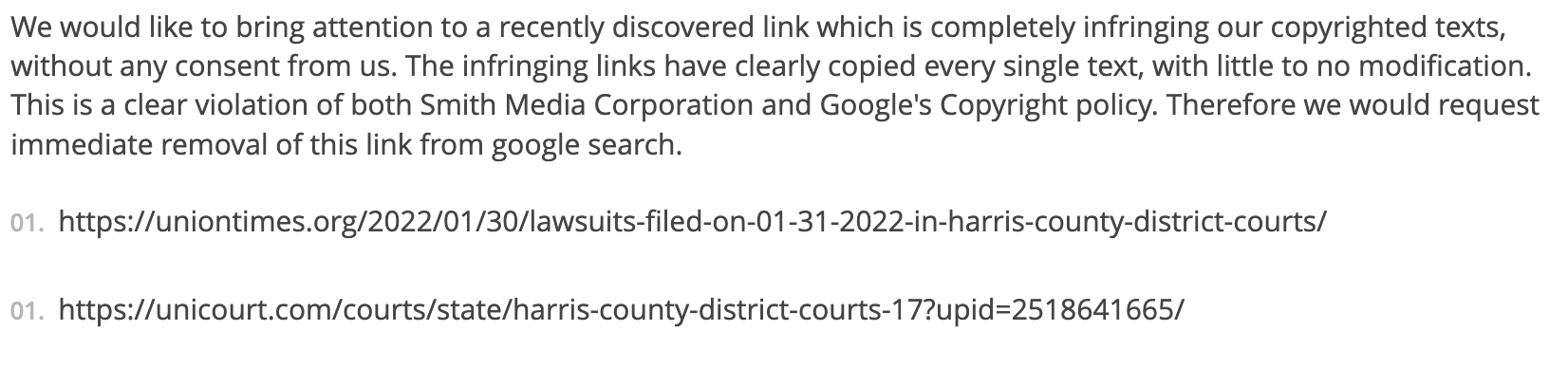

But clearly someone is trying to hide something in Harris County, because here the non-existent Smith Media Corporation is trying to take down another page of court reports:

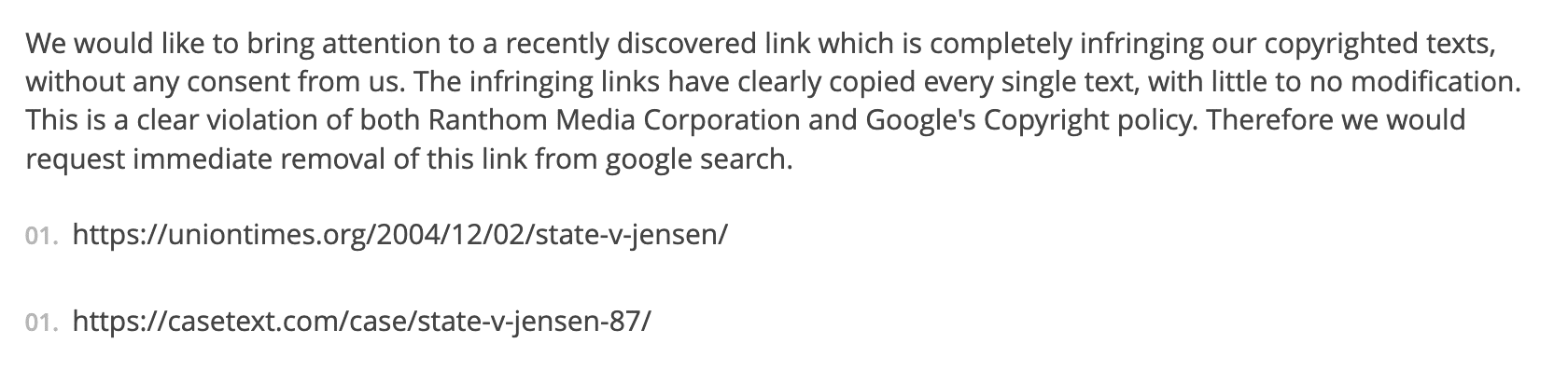

The legal theme continues – here the non-existent Ranthom Media Corporation is trying to take down a Utah case report:

There also appear to be many attempts to take down gambling websites – perhaps by owners of rival websites?

Filing a bad faith takedown notice is a breach of the DMCA; in principle those affected could sue for damages (probably very small) plus attorney fees (potentially large). More seriously, attempting to gain a financial benefit through a fraudulent filing may amount to a criminal offence in the US (wire fraud) and the UK (false representation fraud and/or a breach of the Computer Misuse Act). In both cases, criminal liability could extend to the individual paying for the takedown service, if they were aware that the takedown would be fraudulent (and how could it not be?).

The problem here is that Google assists the frauds, by being amazingly trusting and not requiring any proof of the identity of people submitting takedown notices. I recently “took ownership” of the “knowledge panel” Google displays if someone googles my name. This required an image of my passport and a selfie. It is very unfortunate that Google has much less stringent procedures to file a DMCA takedown notice. Others are more careful.

A Google spokesperson provided this statement:

“We have robust tools and processes in place to fight fraudulent takedown attempts, and we use a combination of automated and human review to detect signals of abuse – including tactics that are well-known to us like backdating. We provide extensive transparency and submit notices to Lumen about removal requests to hold requesters accountable. Sites can file counter notifications for us to re-review if they believe content has been removed from our results in error. We track networks of abuse and apply extra scrutiny to removal requests where appropriate, and we’ve taken legal action to fight bad actors abusing the DMCA.”

Unfortunately this doesn’t seem to be working. Google is accepting takedown notices which have obvious signs of fraud (e.g. multiple companies claiming copyright over the same article, which is highly unlikely). Google could tighten up its existing processes. An additional step would be for Google to require ID verification for people submitting DMCA claims. It’s not at all clear to me why they can’t do that.

Many thanks to Lumen for providing access to their database.

Photo by DALL-E 3 – “a photo of an evil hacker in silhouette at a computer terminal, photorealistic”

Footnotes

Mogul Press’s website T&Cs purport to forbid most third party websites from linking to it, and say “You approve to immediately remove all links to our Website upon request”. Oddly there are a few other websites that contain the same unusual formulation. ↩︎

Everything on this website is licensed under a Creative Commons licence; it can be freely copied, but must be attributed. The fake website doesn’t contain any attribution, and is therefore breaching my copyright. I have therefore submitted a DMCA takedown notice. ↩︎

I filed a counter-notice, which restored my article. In this case that was straightforward; in other cases the sheer volume of automated DMCA takedown notices makes it hard for the victim to respond, particularly if they’re not a large media corporation. ↩︎

You need an account with Lumen to explore these requests in detail. Accounts aren’t generally available, given it’s a non-profit operating a massive database potentially open to abuse, but they do provide access to non-profits and researchers, and kindly provided us with login credentials. ↩︎

As an aside, I don’t understand why Eliminalia hasn’t been prosecuted by the Spanish authorities; its business model appears to rely upon fraud. ↩︎

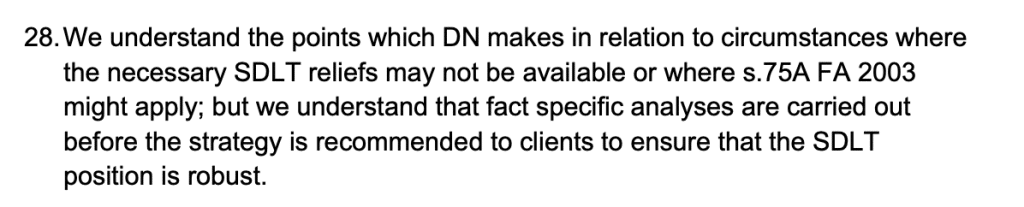

I asked Mogul Press for comment and they didn’t reply, despite having been very chatty previously. I’m therefore seems reasonably likely that the takedown attempt was commissioned by them. ↩︎

Brooks Newmark & Co Ltd, run by former Conservative MP Brooks Newmark, lobbied for foreign PPE suppliers during the pandemic, but didn’t register under the Lobbying Act. It turns out this was entirely legal, thanks to a serious mistake in the drafting of the Act. This has created a loophole which means that lobbyists acting only for foreign clients don’t have to register their lobbying activity. That subverts the purpose of the legislation – the loophole should be closed.

Unfortunately the Lobbying Act turns out to have a significant loophole. The Registrar of Consultant Lobbyists has just ruled that, because Brooks Newmark & Co Ltd only has foreign clients, it doesn’t have to be registered.1

That create the perverse result that a consultant lobbying Ministers on behalf of UK clients has to register the clients, but a consultant lobbying on behalf of only foreign clients does not.

The Registrar’s ruling is, however, technically correct – because of a drafting mistake made back in 2014.

When the Lobbying Act was drafted, the Government took the defensible view that the Lobbying Act registration requirements should only apply to serious businesses, and not e.g. someone lobbying on an informal basis. The Parliamentary draftspeople clearly wondered how to define a “serious business”, and decided to refer to the existing concept of VAT registration. It’s well known that any business with an £85,000 turnover has to be VAT registered, and so they may have thought this was a neat shortcut:

It can, however, be dangerous to borrow legislation created for one purpose and use it for another, unrelated purpose. You run the risk of missing something important.2

One of the nice features of VAT is that it doesn’t discriminate.3 A lobbyist selling consultancy services to a UK business is subject to UK VAT whether the lobbyist is based in Manchester, Monaco or the Moon. A lobbyist selling consultancy services to a French business4 is not subject to UK VAT whether the lobbyist is based in London or Lyon (but in the latter case there probably would be French VAT).

This means that if you’re a UK lobbyist whose only clients are foreign companies, individuals or governments, then you will never charge VAT. You’d normally register for VAT anyway, because that enables you to recover VAT on your costs (“inputs”), but you don’t have to – even if you make many £millions in fees.

The Parliamentary draftspeople unfortunately appear to have missed this5 – they assumed the only scenario where a lobbyist wouldn’t be VAT registered would be where they have less than £85k turnover. This is from the explanatory notes:

And that creates a loophole for consultants who only advise people outside the UK.6 A loophole that Brooks Newmark & Co Ltd qualifies for: because it only has foreign clients, it doesn’t have to register for VAT.

That’s not tax avoidance at all – in fact by not registering, Brooks Newmark & Co Ltd will be over-paying VAT. That makes me think this might have been deliberate Lobbying Act avoidance by Brooke Newmark & Co Ltd (as otherwise, why would they have chosen to pay too much VAT?).7

This now makes it easy for people to secretly lobby for foreign individuals, companies and governments.

If there’s one thing we know from the history of tax, it’s that if a loophole is revealed, and not closed, it will be ruthlessly exploited. If I was a lobbying company thinking of taking on a controversial foreign client, I could establish a new company to act for this one client.8 I’d pay a bit more VAT as a result, but never have to register the lobbying or the client. I’d be amazed if this doesn’t now happen.

But that may be the naive view – it’s possible that the loophole is already understood and exploited in this way.

Many thanks to L for letting me know about this case, which I otherwise never would have come across.

Footnotes

Carter-Ruck were acting for Brooks Newmark; in this case they appear to have been very effective ↩︎

It’s a particularly danger with tax legislation, because it has so many defined terms that appear helpful and straightforward, but are actually anything but. An example I often saw in practice was where a commercial contract had a concept of a company that’s “connected” to one of the contract parties. Someone would inevitably suggest borrowing the corporation tax concept of “connection“. The response from tax lawyers would generally be negative, because of the extreme complication and uncertainty that the tax connection concept would introduce. ↩︎

In the jargon, it is “border-adjusted”, and therefore permitted by WTO rules (see page 144 here) in the way a tax that discriminated against foreign sellers, or in favour of local sellers, would not be. ↩︎

Sometimes the rules are different for non-business customers, but in this case they’re essentially the same↩︎

Richard Thomas has some very well-informed thoughts on this in the comments below; he thinks I may be being unfair ↩︎

The term “loophole” is generally used to mean an unintended result of legislation. The classical example would be where a devious taxpayer finds some way to exploit legislation in a way Parliament never intended, taking advantage of what in essence is a drafting defect. Modern anti-avoidance rules and common law doctrines mean tax loopholes are very unlikely to be found these days (or, more precisely, they are very unlikely to give you a tax advantage if you try to use them). Many thingsdescribed as “tax loopholes” may be viewed by some people as undesirable but they are not unintentional, and so not truly “loopholes” at all. The Lobbying Act loophole, by contrast, absolutely is a good old-fashioned “loophole”. ↩︎

Alternatively it is of course possible they didn’t think it was worthwhile to register for VAT (which feels unlikely, given they appear to have had over £85k in revenue), or alternatively they just simultaneously mistakenly failed to register for VAT and mistakenly failed to go on the lobbying register, and they lucked out that the first mistake cancelled the second. It’s often a good rule of thumb that someone paying too much tax is as noteworthy as someone paying too little. ↩︎

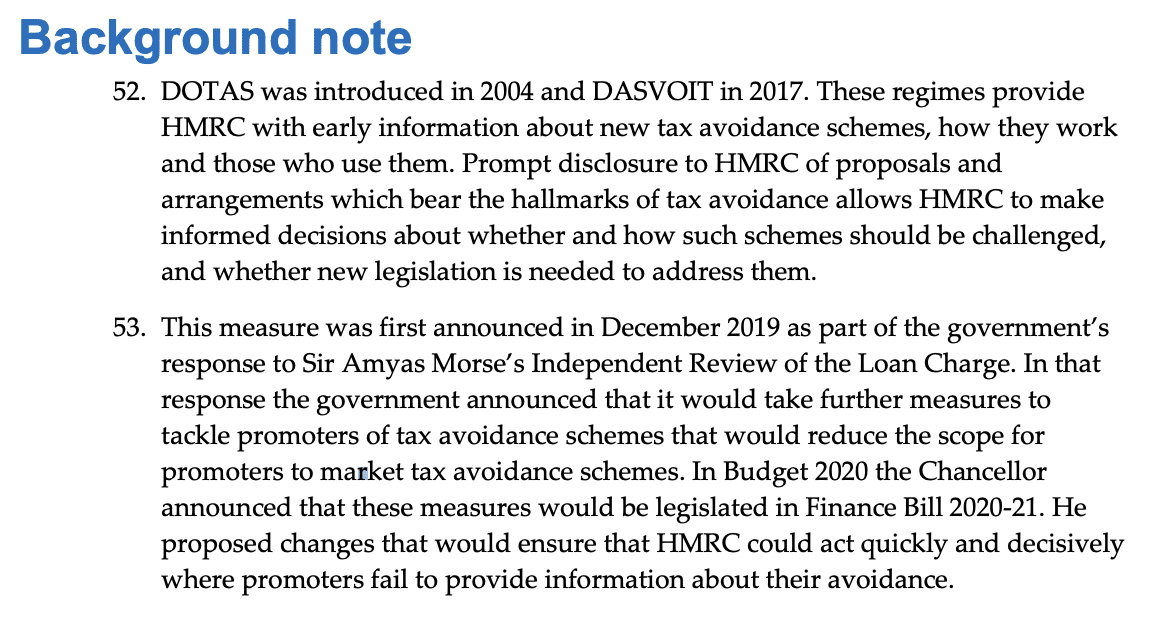

I’d have to keep it outside my VAT group, and there would be irrecoverable VAT costs, including on intra-group supplies – but I suspect in some cases the secrecy advantages will overcome such tax disadvantages… indeed some clients might pay over-the-odds just to obtain secrecy. ↩︎

One could amend the VAT reference to include cases which would be registrable if the supplies were all made within the UK, but it’s much more sensible to drop the link to VAT altogether, and just impose a simple financial de minimis, plus an aggregation rule to prevent lobbying businesses being split into multiple entities to avoid registration. VAT is complicated, and in the future could change unpredictably. And using the VAT rule likely creates other opportunities to evade lobbying regulation, e.g. as Steve Woodward pointed out, splitting a business to multiple VAT registered entities. One of our correspondents, W, has also made the excellent point that it’s not obvious how you apply the current rule to a foreign business. All of which goes to show: it’s best to avoid tying unrelated legislation to a VAT concept. ↩︎

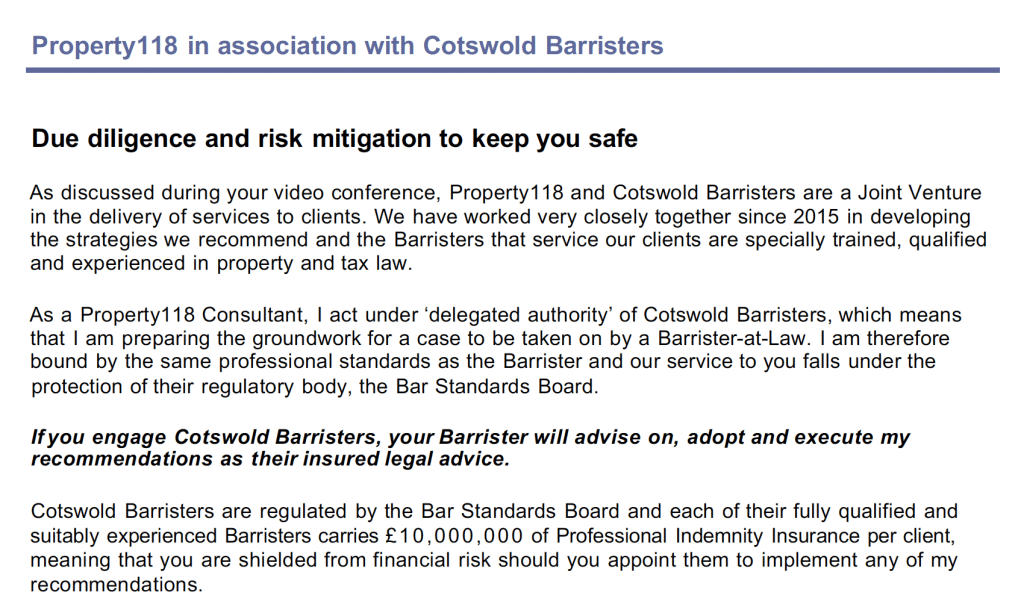

Last year we revealed an inept and dangerous landlord tax avoidance scheme promoted by Property118 and Cotswold Barristers. They responded with a weird campaign of denial, threats and abuse. HMRC then started to investigate, but Property118didn’t tell their clients. HMRC’s conclusion? Property118 had unlawfully failed to notify HMRC they were promoting a tax avoidance scheme. Property118 and Cotswold Barristers’ response? Telling their clients this is a normal procedure for “innovative tax arrangements” and nothing to worry about.

UPDATE 16 February 2024: Property118 have published a defence of their position. Per their usual practice, the article doesn’t contain a single reference to legislation, just a series of irrelevant quotes from HMRC manuals. Competent tax advisers always start with the legislation. HMRC guidance can sometimes be of assistance, but it’s not the law, and legally and practically cannot be relied upon. What you certainly can’t do is try to reach your desired result by citing HMRC guidance as if it’s legislation.

Property118 run a popular landlord website and sell a series of incompetent tax avoidance schemes. Nobody at Property118 has any tax expertise, and they rely heavily on a peculiar barristers chambers (“Cotswold Barristers”) who also appear to have no tax expertise.

We subsequently discovered an even worse element to Property118’s scheme that involved throwing lots of money around in a circle and claiming it created a big tax saving – generating a total of £500k+ in “fees” to a YouTuber who then extensively promoted Property118 without revealing his financial interest.1 And then we went through Property118 client files and found a series of serious errors, as well as evidence that Cotswold Barristers was just “rubber-stamping” standard form advice without giving it any independent thought.

Property118’s initial response

Most of the tax avoidance scheme promoters we’ve reported on simply refuse to comment, and hope that if they stay silent then everything will work out.2

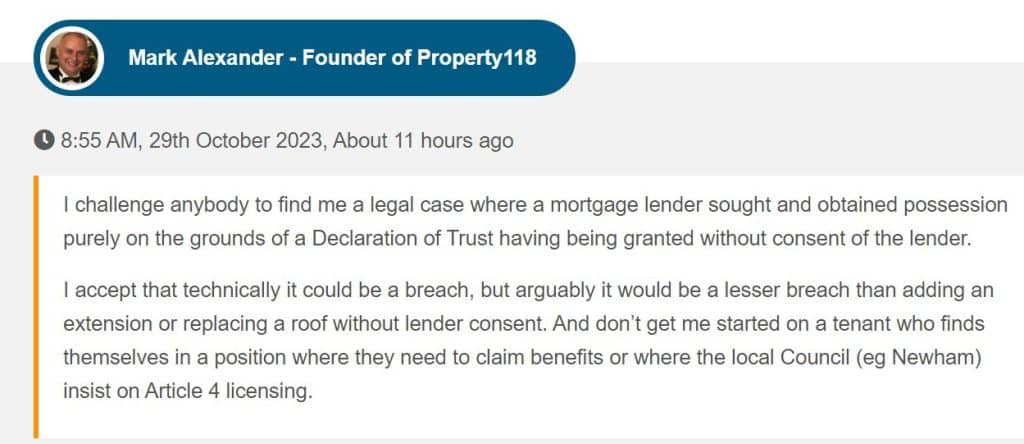

Property118’s response was very different.

They responded aggressively to our requests for comment, and seemed angry that we wouldn’t accept a recorded Zoom call instead of correspondence.

Next, they hired a tax KC to provide an opinion that their scheme worked. More conventional types would have hired a KC who says any old avoidance scheme works. Property118 instead hired a reputable KC, but asked her to advise on largely irrelevant questions instead of the ones that mattered. In particular: was the mortgage defaulted? Was this a tax avoidance scheme that should have been disclosed to HMRC under the “DOTAS” disclosure rules? Did anti-avoidance rules apply? What did Property118’s ineptly drafted documents actually do? None of this was covered.

They then made a series of weird, conspiratorial personal attacks on me, complete with spooky AI generated pictures. They accused me of being unqualified, and said that the many other advisers critical of Property118 were acting out of jealousy for not having thought of these brilliant ideas themselves.

Property118 then referred me to the Solicitors Regulation Authority for being mean to them. I’ve heard nothing further about this – I’d hope the SRA see the referral as an obviously vexatious abuse of the regulatory process to retaliate against a critic.

And finally there were a succession of supposed technical responses to our reports, none of which actually engaged with the substance of what we had said. The peak of this was an article by Mark Smith of Cotswold Barristers claiming that DOTAS didn’t apply (since deleted; this is an archived version), which would be disappointing if handed in by a work experience student.

Then, at some point in November 2023, Property118 went silent, and deleted their main technical response.

Why did they go silent? Because HMRC had started to act.

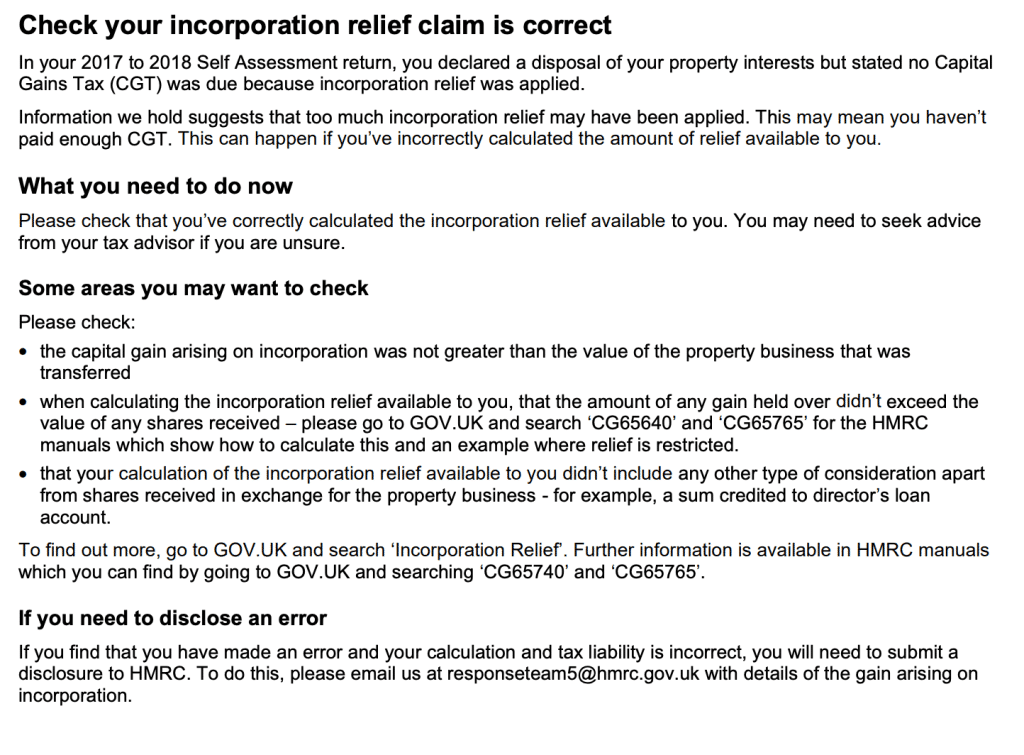

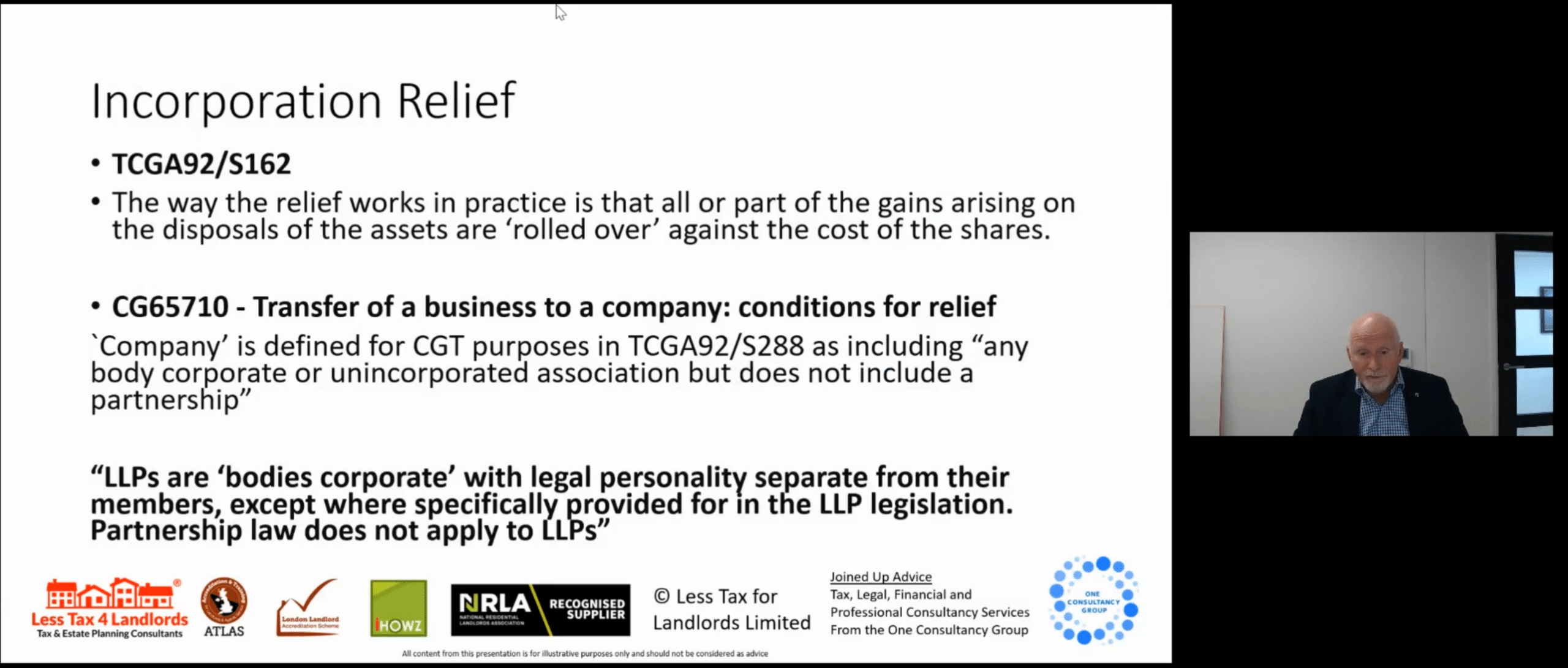

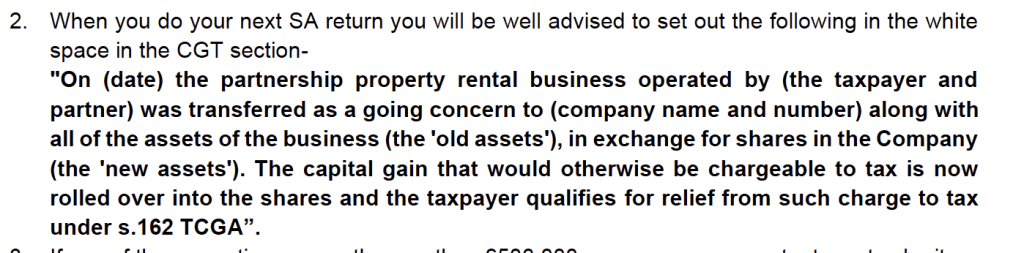

On 16 November 2023, HMRC announced that they’d started to investigate incorporation relief claims from as far back as 2017/18.3. “Incorporation relief” is a tax relief that Property118 relied upon to move landlords’ properties into the structure without capital gains tax. However they got the details badly wrong.

Here’s the key part of a letter which HMRC sent to taxpayers:

It was always reasonably clear that Property118’s schemes should have been disclosed to HMRC under DOTAS – the rules requiring disclosure of tax avoidance schemes. Property118’s denials of this revealed only that they and Cotswold Barristers had a very poor understanding of the rules. Ray McCann, who when at HMRC led the launch of DOTAS, described their responses as “hopelessly wrong“.

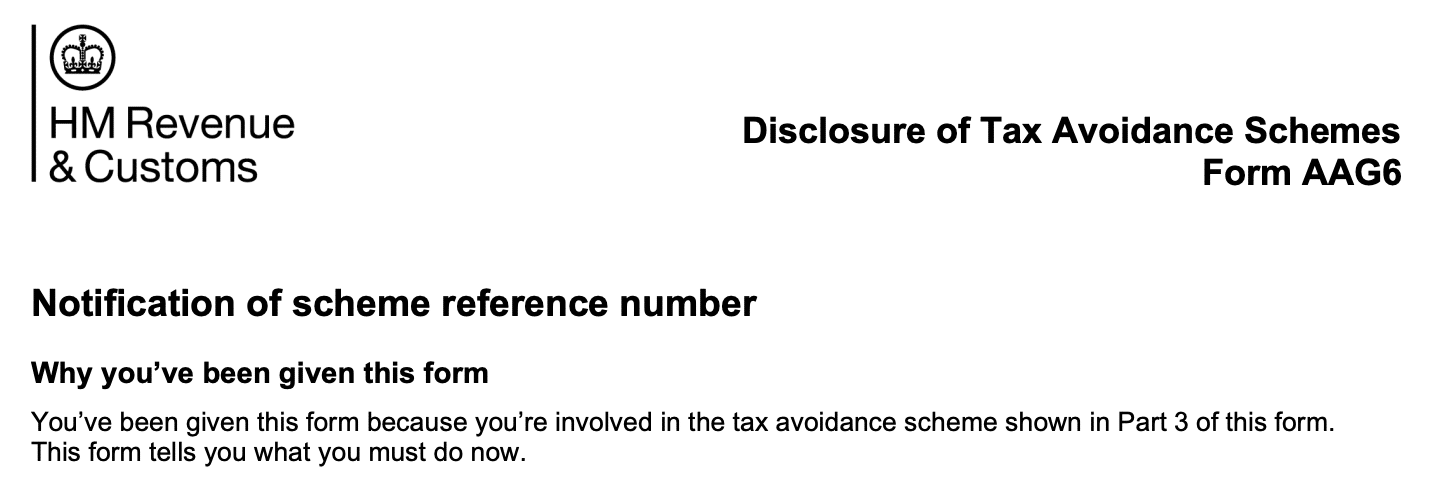

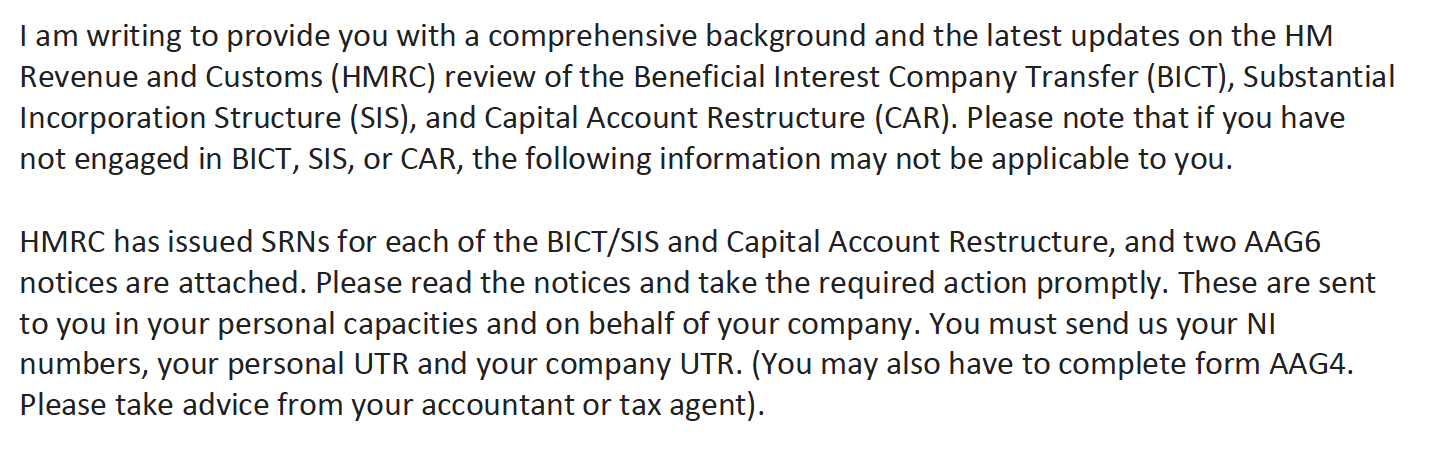

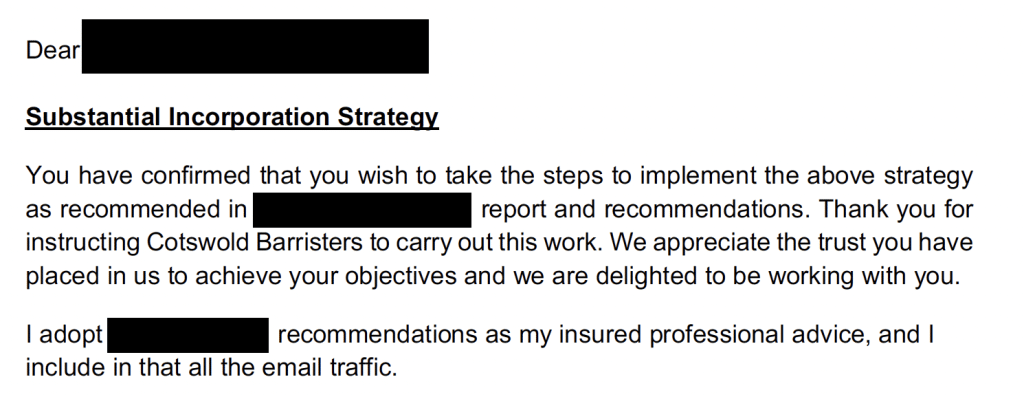

Property118 and Cotswold Barristers should have clearly explained what had happened, and what it means for their client. Instead they decided to mislead their clients with an email which manages not to mention the terms “avoidance” or “DOTAS”:

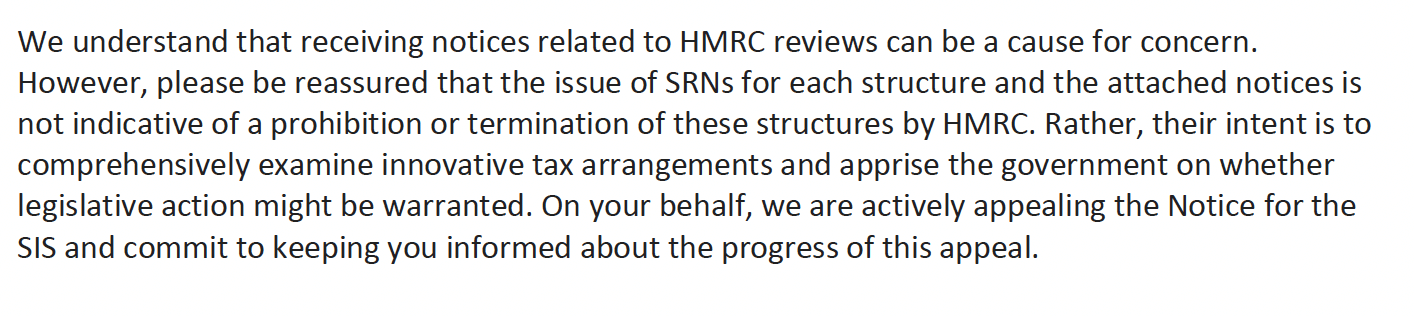

What is an SRN? What is the required action? Why did this happen? Cotswold Barristers don’t say. We’ve uploaded a full copy of the email here.

“You may have to complete form AAG4” is exceptionally unhelpful. Cotswold Barristers should be saying to their clients who used the schemes for past years that they will have to submit this form.

Instead, Cotswold Barristers provide reassurance which is comforting, sympathetic, and completely wrong:

No, the intention of DOTAS is not to enable HMRC to “comprehensively examine innovative tax arrangements”. It’s to enable HMRC to discover tax avoidance schemes as soon as they’re used, so it can decide whether to challenge them and/or ask the Government to enact legislation closing any loopholes. 8 This is well known to all practitioners, and was restated when DOTAS was amended in 2021 to enable SRNs to be issued to rogue promoters:

Anyone reading this will realise the truth: that it’s now likely that Property118’s clients will be the subject of HMRC enquiries, and face large tax liabilities, plus interest and potentially penalties.

It’s sweet that Property118 are appealing HMRC’s decision that the “substantial incorporation structure” is disclosable (good luck with that), but that suggests even they can’t defend the circular “capital account restructure”.9

So why did Cotswold Barristers and Property118 provide that those empty, sympathetic and wrong words of reassurance?

In other circumstances we’d say it’s deliberate deception, but we believe Cotswold Barristers and Property118 are simply unqualified and unable to advise properly on tax.

But whether it’s fraud or haplessness, the question is whether a barrister is permitted to act in this way. That is something we’ll be returning to soon.

Thanks to everyone who contributed to the original Property118 article, particularly those who were happy to be credited by name (when they knew Property118’s reputation for bullying and abuse).

Because, at the time, that was the furthest HMRC could go back. It’s a kind of triage, first attacking the oldest periods, and then (when they’re done and have time) moving onto the newer ones. The approach is absolutely rational for HMRC, but has the considerable disadvantage for taxpayers that it can be years before your avoidance scheme is challenged. The answer is: don’t do avoidance schemes. ↩︎

Our analysis goes further, and says that there are several good reasons to believe the Property118 scheme is completely disqualified from incorporation relief. We expect HMRC will take these points, in the fullness of time, but for now is applying the much easier calculation point, given that it’s just arithmetic. ↩︎

As an aside, there is a rather odd paragraph in the Finance Act 2021 legislation that created the new notice procedure. Subsection 311(9) says: “The allocation of a reference number to arrangements or proposed arrangements is not to be regarded as constituting an indication by HMRC that the arrangements could as a matter of law result in the obtaining by any person of a tax advantage”. Of course the intention is to stop promoters using SRNs as badges of approval from HMRC, but quite what the legal effect is of the subsection, we have no idea. Possibly it has none; possibly it would assist in fraud proceedings against dishonest promoters who did try to use SRNs as promotional material? ↩︎

The version of the Regulations on legislation.gov.uk is unfortunately out of date; however the subsequent amendments aren’t material to the scenario discussed here. ↩︎

DOTAS also means HMRC can, after issuing the SRNs, use its new powers to require Property118 to provide further information about their scheme, including documents and names of clients. We expect this will happen soon, if it hasn’t already ↩︎

It looks like at some point they changed their mind, and decided to appeal that too; quite hard to see what the basis for this will be. ↩︎

Less Tax for Landlords and The Bailey Group1 sold a landlord tax avoidance scheme involving an LLP “hybrid partnership”.2 We reported back in October that the scheme was technically hopeless; HMRC has written to the clients and invited them to settle. Everyone thought the game was up.

How did Less Tax for Landlords respond to being caught? They denied there was anything wrong with their scheme, paid £100,000 to a KC known for writing tax avoidance scheme opinions, obtained an opinion which appears to be worthless, and advised their clients to disregard HMRC’s offer to make a disclosure by 31 January 2024. We expect that, as a result, their clients will incur significant penalties.

At this point the big question is whether Less Tax for Landlords are recklessly incompetent, or conducting a deliberate fraud on HMRC and their clients. Tax advisers and others will form their own view after viewing the evidence we set out below.

It’s often said that the answer to rogue tax advisers is regulation. Less Tax for Landlords’ accounting arm is regulated, by the Institute of Chartered Accountants in England & Wales. But the ICAEW shows no sign of taking any action.

Regulation isn’t working. Rogue tax advisers are taking advantage of HMRC and their own clients. The question is: what can be done?

The LT4L scheme

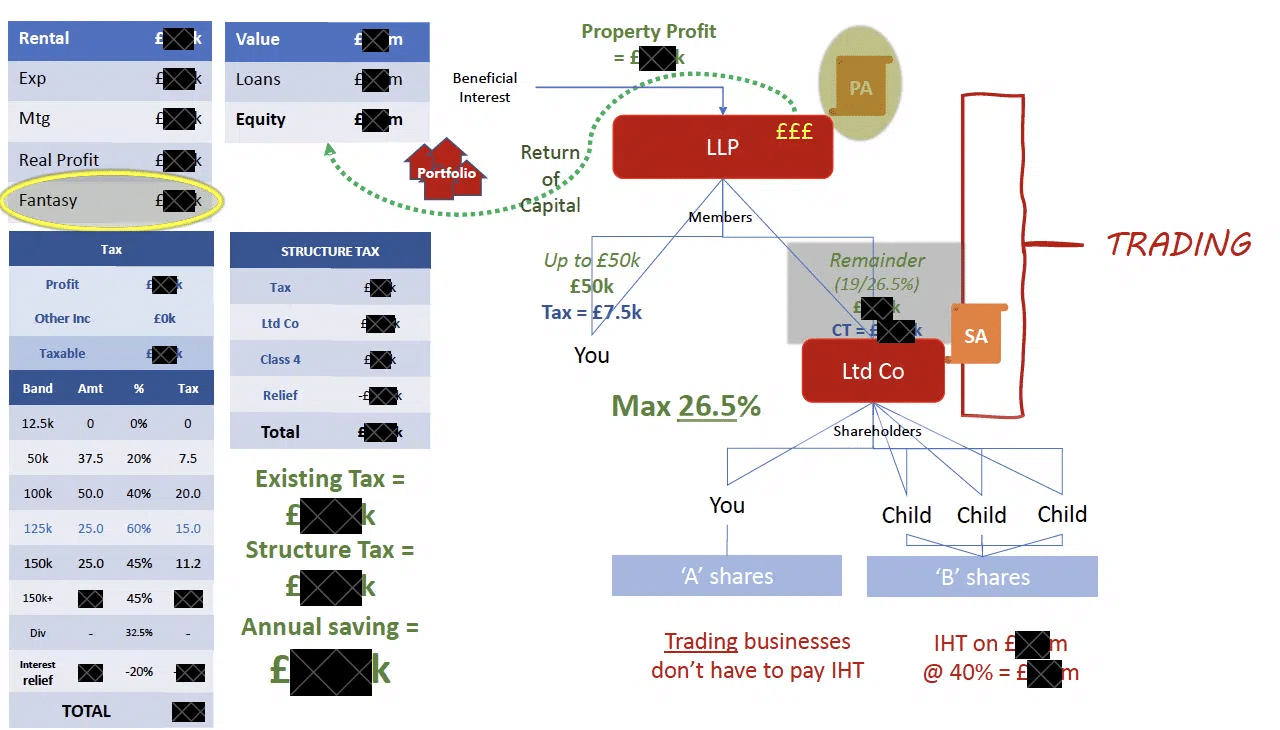

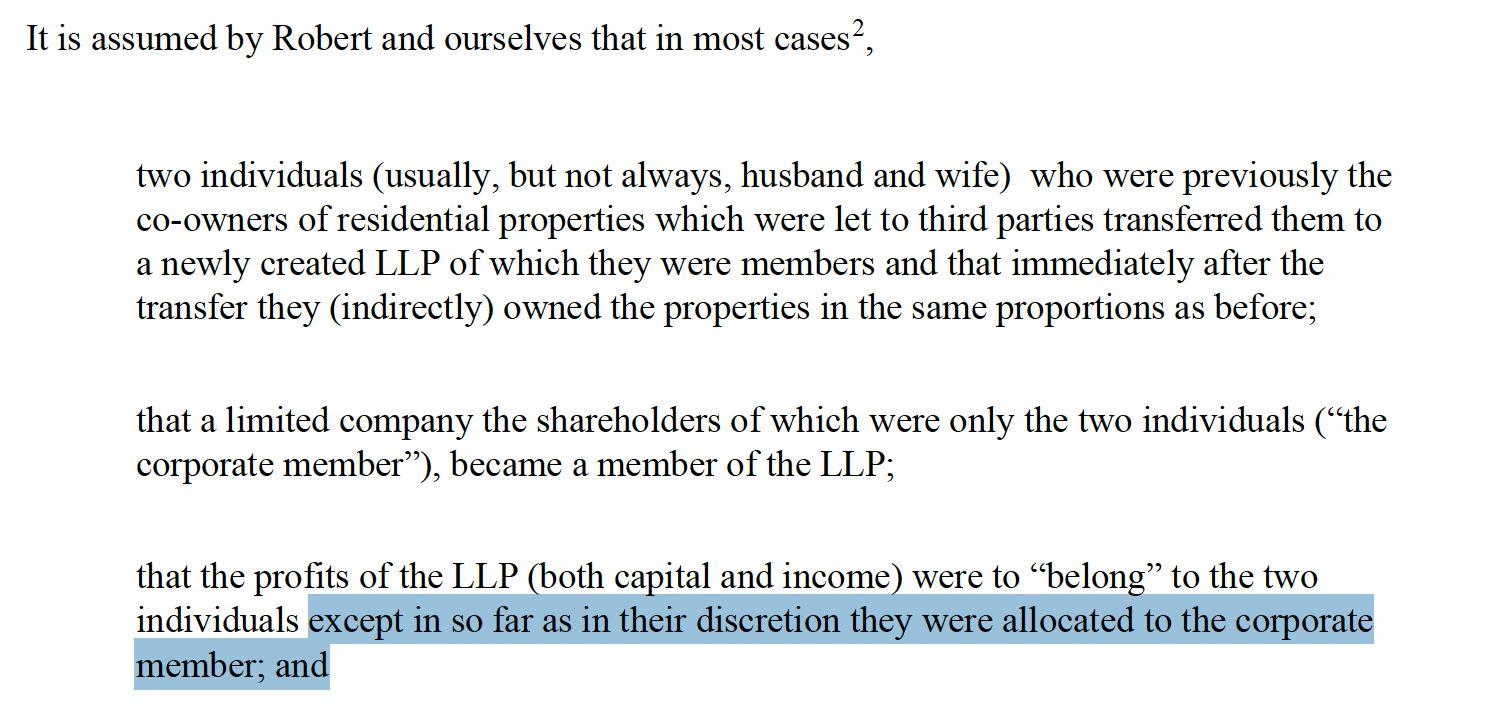

On 4 October 2023 we published a detailed report into a tax scheme marketed by Less Tax for Landlords, the trading name of the One Consultancy Group (OCG). The idea was:

Landlords would declare a trust over their properties in favour of a limited liability partnership (LLP)

The landlord and their spouse would be members of the LLP; there would also be a newly incorporated company as member, owned by the landlord/spouse

The LLP diverts most of its profit to the company.

LT4L made some very impressive claims about the structure:

There was no need to tell the mortgage lender.

After two years, the structure is entirely exempt from inheritance tax thanks to business relief.3

The diversion of LLP profits to the company means rental income is taxed at the corporate rate of 19-25%.4

The trust means the landlords’ obligation to make mortgage payments “shifts to the LLP”, meaning the company as LLP member obtains full tax relief for mortgage interest. The “section 24” restriction on landlords claiming tax relief is avoided.

No CGT or SDLT on establishment, without needing to qualify for any special reliefs.

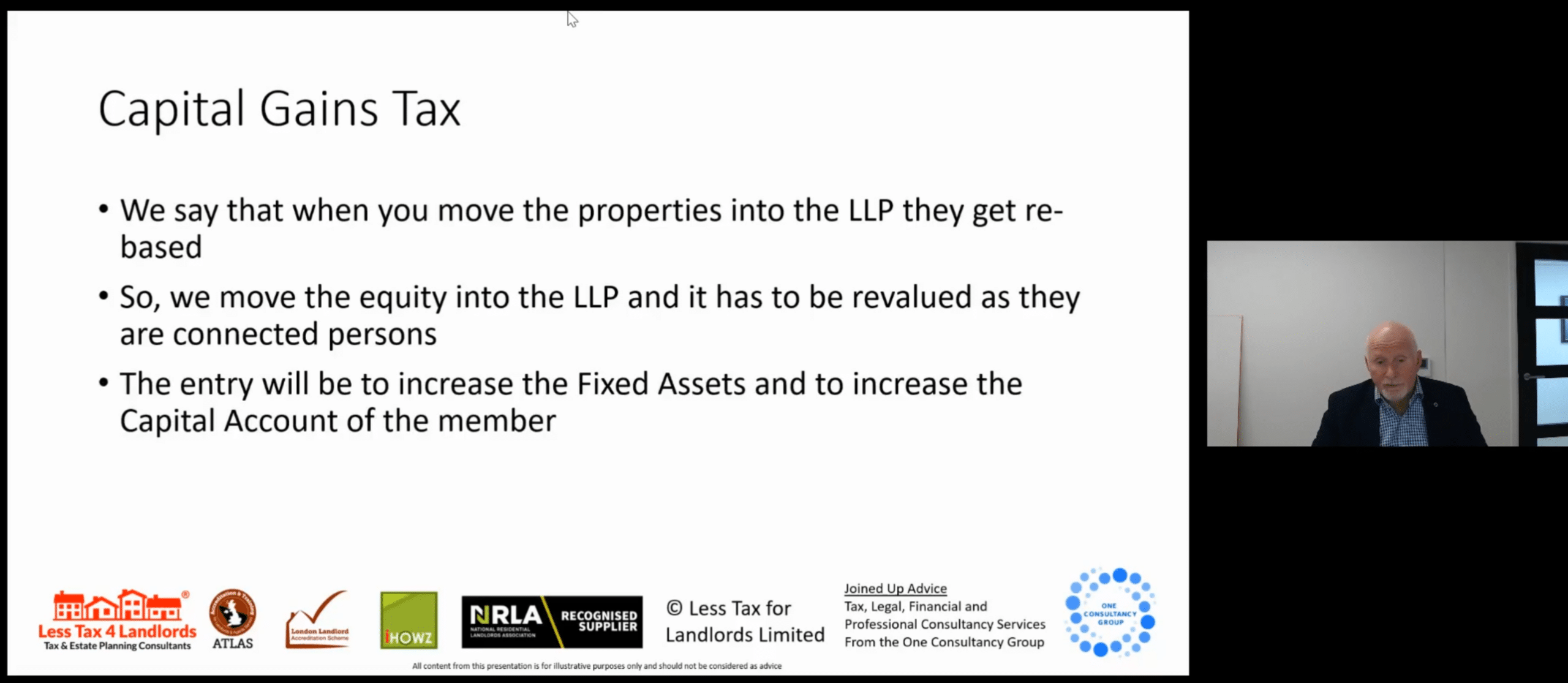

The properties are “rebased” for capital gains tax. In other words, when they’re sold, only the capital gain after incorporation of the LLP is taxed. Pre-incorporation gains disappear.

Instead of taking profits out of the LLP, you can take capital out instead, and you won’t be taxed.

There’s no need to disclose the structure to HMRC.

If the structure triggers unexpected tax, then their clients are protected by an unusual insurance arrangement – LT4L claim they have a “written note” from their insurers stating they are happy to cover all interest, penalties and extra tax payable if HMRC do not agree with the way the structure was set up.

How the LT4L scheme fails

We couldn’t believe the scheme when we first saw it. Every aspect fails:

Declaring a trust over the rental properties without the mortgage lender’s consent (or even telling them) will in most cases default the mortgage. The structure was described to us by an experienced broker as “almost unmortgageable”.

Rental property businesses almost never qualify for inheritance tax business relief. The LLP structure doesn’t change that.

The mortgage obligation doesn’t “shift to the LLP”. It remains with the landlords – who now lose their 20% credit.

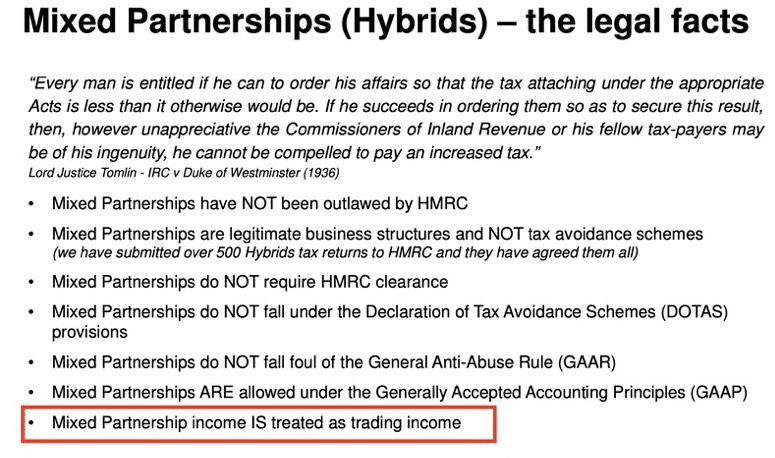

The “mixed partnership” rules mean you can’t get a tax benefit by allocating profits to a corporate partner in an LLP.

The allocation of profits to the corporate partner means there will be up-front capital gains tax. There’s no CGT rebasing.

SDLT will be due at the point that income profits are allocated to the corporate member. LT4L’s unusual structuring potentially results in a higher SDLT liability than would result from a simple incorporation.

The structure can incur additional SDLT every time the profit allocation changes. LT4L’s clients could have unknowingly racked up years of SDLT liabilities.

The structure is disclosable under DOTAS, the rules requiring tax avoidance schemes to be disclosed to HMRC. That is obvious, given that the structure was mass-marketed and its main benefit is to avoid tax.

Members are taxed on profits as they are made; when and how they are taken out is irrelevant. This is a basic principle of LLP taxation.

HMRC do not in fact agree with how the structure was set up, but there is no automatic payout from LT4L’s insurers. That’s because there never was a special “written note”; they just have the usual professional indemnity insurance. To get any benefit from that, an LT4L client has to lose an argument with HMRC, sue LT4L (with the insurers arguing LT4L’s case, not the client’s), and win. This is not easy, even if (as we believe) LT4L’s advice is plain wrong.

Many tax avoidance schemes fail, indeed these days almost all of them do. The unique thing about Less Tax for Landlords is that nobody has been able to explain why they thought their structure worked. It’s not a case where they have an argument, and that argument is wrong. It’s that they don’t appear to have had an argument at all.6

We can illustrate this if we focus for the moment on the claim that the structure is exempt from inheritance tax after two years.

Here are six answers that Less Tax for Landlords provided to clients and advisers asking questions. People familiar with inheritance tax and the tax concept of “trading” will see immediately they are nonsense (The Chartered Institute of Taxation have published a clear summary of the actual position7). But we believe even a non-specialist will see that the explanations given are contradictory:

“[the business] is outside of your estate for inheritance tax, as long as you tick various boxes”

Why?

“because the HMRC recognizes that there is a trading relationship between you all, and that you’ve got a written business plan and that you’re managing it and that your sole purpose is not to avoid tax but to maximize your wealth to tax efficiently as possible, the whole thing becomes inheritance tax free.”

A trading relationship between the participants, a business plan, not having a tax avoidance purpose – all these things are irrelevant to whether inheritance tax applies. There are no “boxes” to tick.

2. The LLP turns into a trading business

If you don’t like that, here’s a completely different explanation:9

“The LLP structure that we set up is not investing in property. It does not own the property. The property is owned by the individuals. The LLP has taken advantage of that ownership and it is available… after two years, that LLP turns into a trading business according to HMRC, not according to us, according to HMRC. And at that point, after two years, the equity of those properties inside that LLP are then outside of the estate for inheritance tax after two years. “

Pure nonsense. The LLP does have beneficial ownership of the property. The LLP does not “turn into a trading business”. HMRC has certainly not said this, or anything like this.

Here’s another version of the same claim from a document LT4L sent to a client, with a badly drawn rectangle supposedly showing that something, somewhere, somehow is trading:10

3. The LLP turns rental income into trading income

Less Tax for Landlords often used this slide:

And sounded very confident:

In reality, an LLP doesn’t transform its income into trading income.

4. Gobbledegook about the equity

Some advisers asking LT4L to explain their structure received this explanation:

“The LLP holds the equity and not the properties – so it cannot be classed as investment. The owner of the properties does not qualify for BR on the properties, but on the equity.”

We have no idea what this means.

5. More trading activity is introduced

When we were researching our report, we asked LT4L how they justified their inheritance tax claims. This was their response:

“We do not work with all landlords, at least not in relation to a Mixed Partnership structure, and for those we do work with, we look to help them commercialise their operation and introduce more trading activity into their business model.”

You can’t “introduce more trading activity” into a rental property business and qualify for business relief.11 So this approach would fail; however we have been unable to find any LT4L clients who were helped to “introduce more trading activity”. This statement may just have been a lie.

6. Aggressive evasion

Over the years, many tax advisers asked Less Tax for Landlords how their scheme magically qualified for business relief. That often went like this:

That confidence has now disappeared, and Mr Gimple’s correspondence with us makes clear he never understood the technical tax basis for the structure. He tells us he relied on Vajahat Sharif who ran the associated law firm (which includes STEP qualified practitioners), and Chris Bailey, who ran the accounting and tax advisory side of the business.

Mr Sharif has told us that he and his staff don’t in fact have any tax expertise, and he never advised on any element of the hybrid partnership structure. We believe Mr Sharif when he says he has no tax expertise, because he promotes himself on LinkedIn as “Head of Terrorism, National Security, Political & Complex Crimes at Tuckers Solicitors”.12 It is impressive that he can combine this with being “Group Head of Legal” and head of compliance for OCG Group (which owns/runs Less Tax for Landlords). We’d assume it’s two different people with the same name, but it isn’t.

Mr Sharif says he had no involvement in the LT4L tax avoidance structure. A letter was recently sent to LT4L’s clients from Sharif and the other directors concerning the structure; Mr Sharif says he didn’t authorise that letter, but hasn’t taken any steps to correct it.

Mr Bailey is a qualified accountant, but from the videos and documentation we have seen, it is apparent that he either has no tax expertise or is lying (we do not know which it is). Bailey was disciplined by the Association of Chartered Certified Accountants in 2020 for failing to provide audit files when requested. He provided a series of excuses for this: he first said he needed more time, then claimed the clients were audit-exempt, then claimed the files were offsite, and finally blamed a software issue. He was found guilty of misconduct. The ACCA accepted that the failure to disclose was not deliberate; it is not clear how they came to this conclusion.

We believe Mr Gimple, and don’t think he was dishonest. However, he had no technical tax qualifications or experience, was selling a scheme he didn’t understand, and aggressively responded to criticism from people who were qualified (without, it seems, ever wondering what precisely was going on). This strikes us as reckless.13

The justifications for the other key elements of the structure were equally nonsensical, with no reasonable basis ever provided for thinking capital gains were rebased, or that the diversion of income to the corporate member would escape the mixed partnership rules. Over the years, many advisers queried the structure – nobody received a coherent explanation.

And the other people who never received an explanation were LT4L’s clients. As far as we are aware, not a single LT4L ever received a technical explanation of why business relief applied, or indeed a technical explanation of any other aspects of the structure.

It is, in short, astonishing.

Why?

The LT4L structure has been the subject of widespread comment by tax professionals. We are not aware of a single adviser, anywhere in the UK, who believes the LT4L structure had any prospect of success.

At this point there are three possibilities.

First, Less Tax for Landlords have alighted on a structure so brilliant that nobody else is able to understand it. They are right and we are all wrong.

Second, LT4L were incompetent and negligent to an astonishing degree.

Third, key personnel at LT4L either knew the structure didn’t work, or were wilfully blind to it not working, but sold it anyway. In other words: they defrauded both HMRC and their own clients.

We are going to discard the first possibility.

To assess the likelihood of the second and third possibilities, let’s look at how LT4L responded to the Spotlight.

LT4L’s response

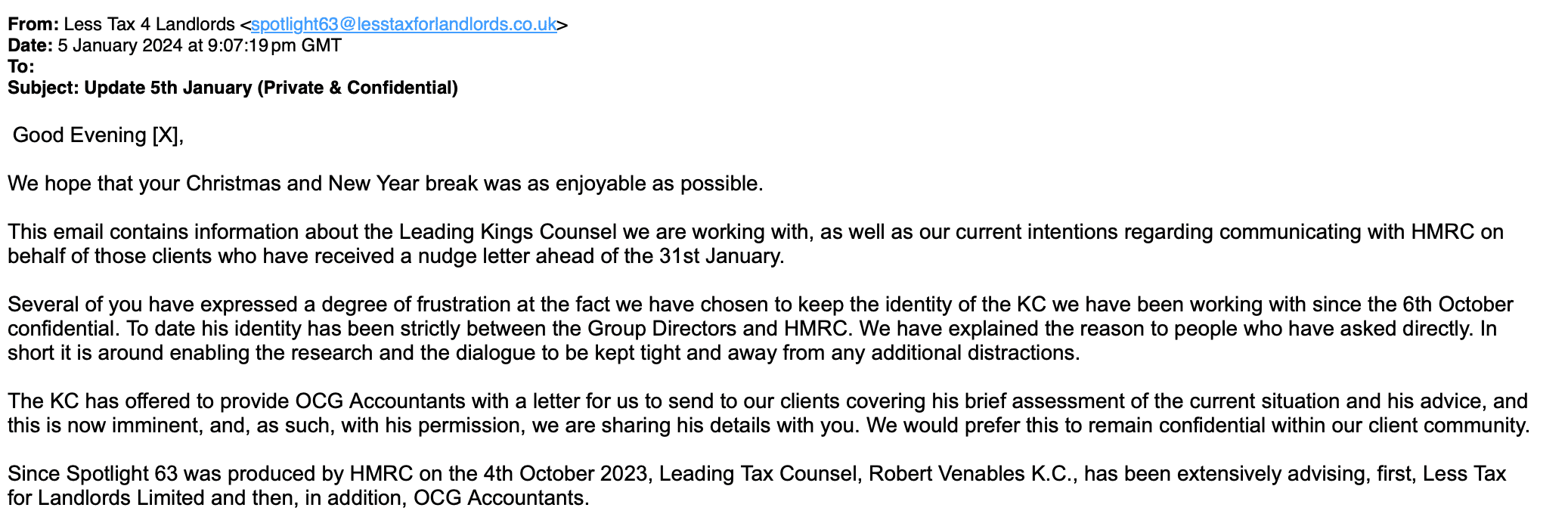

Here’s what LT4L have been up to, since October, in their own words:

Less Tax for Landlords didn’t admit wrongdoing and continued to represent their clients. It’s an impossible conflict of interest.14

LT4L then admitted that the chosen counsel is Robert Venables KC.

This is an illuminating choice. Venables’ reputation is for providing opinions on avoidance schemes.15Jolyon Maugham once wrote an insightful and influential blog about the “boys who won’t say no” – the handful of tax KCs who frequently issue technically dubious opinions on avoidance schemes. Venables is generally considered to be one of those KCs. He’s not the man you go to if HMRC are unreasonably challenging your entirely commercial structure (not least because he has no credibility with HMRC).

We understand from a source that LT4L paid £100,000 for the Venables advice.

LT4L wrote to their clients last month summarising Venables’ opinion. We are publishing a copy of the LT4L letter; it is stated to be confidential, but we believe there is a public interest in publishing it, given it reveals highly unethical behaviour by LT4L. We also believe public scrutiny of LT4L’s actions is in their clients’ interests.

The first and most important thing Venables says is that clients can’t rely on his advice. If Venables gets it wrong, LT4L’s clients are stuffed:

This is standard practice for KCs writing avoidance opinions. The people who actually need to rely on the KC’s advice, can’t. This is why “the boys” happily issue opinions that other advisers wouldn’t touch – it can never come back to them.

The other key reason is that “the boys” will often make assumptions of fact which are unrealistic, and mean they are advising on a structure which is not quite the same as the actual structure. Like this:

This is not how the structure was sold to LT4L’s clients. The whole point was to allocate large amounts of income to the corporate member to obtain a tax benefit. LT4L presentations show almostall the rental income being allocated to the company, leaving the individual LLP members only enough to use up their 20% income tax bracket:

Other advisors, who are merely bad, think there is a 15% limit to the profit that can be allocated to the corporate member.16 LT4L think there is no limit:

So Venables is assuming away the actual structure, either because he has been mis-instructed, or because that’s the only way he can come to the “right” conclusion.17 Everything that follows is therefore worthless.

Mixed partnership rules

These are the rules which undo attempts to allocate income to a corporate member of an LLP/partnership which go beyond a fair return on services or capital provided. Less Tax for Landlords made a series of nonsense claims about these rules. What does Venables have to say?

HMRC have claimed that income which was in fact allocated to the corporate member is deemed to be taxable income of the individuals which should have been declared as such.

HMRC have mentioned the “mixed partnership” rules and the “income stream” rules.

Robert has advised us that he has seen nothing in HMRC’s arguments which justifies the view that taxable income has been under-declared and does not see how their claim can be established on either basis.

There is zero content here.

LT4L were previously very confident the rules didn’t apply as long as your “main reason” for the structure wasn’t tax avoidance and they are “used for business purposes”:

But Venables is silent on LT4L’s original justification, and provides no basis for thinking the structure works. It is possible, again, that he is misunderstanding/misdescribing the structure.

We have heard from a source that LT4L are in fact submitting client tax returns for 2022/23 on the basis there is no allocation of profits to the company. If that is correct it is very disturbing, because it suggests they know their structure is indefensible, and are conceding most/all of the benefit of the structure for future periods, but concealing this from their clients.

Any reallocation of profits can also trigger SDLT charges – more on that below.

Inheritance tax

The prospect of an inheritance tax exemption after two years was the big benefit of the LT4L structure. But on this, Venables provides no advice at all. We are aware of former LT4L clients where HMRC is asserting seven figure inheritance tax liabilities, but all LT4L have to say is:

HMRC have also raised the question of inheritance tax.

To the clients where this is a current issue, separate steps are currently ‘in progress’ with HMRC and unless you have made some gift of your rights over the LLP, Robert sees this as being currently academic. He notes that in any event your self-assessment return has nothing to do with inheritance tax.

Clients who paid thousands of pounds for advice from LT4L which claimed to enable an inheritance tax exemption, should be pretty unhappy that the issue is now described as “academic”. It’s a striking change from their breezy confidence of a few months ago.

Stamp duty land tax

Here’s what LT4L are saying about Venables’ advice:

HMRC have not claimed in their letters to us or to our clients, in the “factsheet” or in Spotlight 63 that any stamp duty land tax should have been paid on the transfers of the properties to the LLP.

Robert had advised us that no stamp duty land tax should have been due on such transfers, except perhaps in exceptional circumstances. We shall be contacting separately our clients whose circumstances may be exceptional.

It’s another bait and switch. The problem isn’t SDLT when the properties go into the structure; it’s SDLT when the profit-sharing ratios change. Every change potentially triggers a tax charge, and the changes are often large.

HMRC didn’t mention this point in Spotlight 63, but we understand they are currently investigating it.

Capital gains tax

Here’s LT4L/Venables:

HMRC appear to accept that there was no capital gains tax payable when the properties were transferred to the LLP.

Robert has advised us that in general that must be correct, although he adds that there may be a small number of our clients who may require more specific contact relating to their specific circumstances.

Once more, a failure to engage with the actual problem: LT4L promised that the structure would “rebase” assets so that, when you sell a property, you’re only taxed on gains since it went into the LLP:

They explained this through gobbledegook:

There is no rebasing when property is moved into an LLP.

One of Bailey’s many errors was to believe LLPs were treated as corporates for capital gains tax purposes:18

The “disclosure of tax avoidance scheme” (DOTAS) rules require promoters of tax avoidance schemes to notify HMRC. HMRC then provides a scheme reference number which the promoter has to give its clients to put on their tax return. This is the kiss of death if you’re trying to market a scheme, so promoters generally find bogus legal rationales for not disclosing.

The LT4L scheme plainly was disclosable, because its “main benefit” was obtaining a tax advantage, and the scheme was mass-marketed and highly standardised.

LT4L didn’t disclose, because they thought their LLP scheme (created wholly for tax reasons) was comparable to the kind of LLP commonly used by accounting and law firms (it isn’t) and “a business structure is not a tax avoidance scheme” (which just ignores the way the rules work).

Spotlight 63 is very clear that HMRC believe DOTAS applies. The LT4L/Venables advice doesn’t mention DOTAS. We would speculate that’s either because LT4L didn’t ask the question, or because they asked the question but didn’t like the answer.

Where does this leave LT4L’s clients?

In a terrible position. They are being advised to do nothing…

“HMRC have suggested that you should amend your self-assessment return for 2021/22.

Robert does not see how it could be to your advantage to do so. He can see that it would very probably be to your disadvantage and to the advantage of HMRC

…

HMRC have suggested that you should make a “declaration” to them and have threatened an enquiry into your self-assessment return for 2021/22 if you do not do so by January 31st 2024. They have not specified what the “declaration” should concern.

Robert does not see how it could be to your advantage to make such a declaration, even if you knew what it was you were supposed to declare. He sees the threat of HMRC making an enquiry into your self-assessment return if you do not do so by January 31st 2024 as a hollow one.”

… but being given no explanation that would let them form a reasonable belief this is a correct course of action.

The likely outcome will be penalties. Robert Venables KC has this to say about penalties:

HMRC have suggested that unspecified penalties might be due from you.

Robert does not see how that can presently be the case.

Again, there is zero content here. Penalties are very likely due for taking all the unsupportable positions we refer to above, and then for failing to correct returns when HMRC has given taxpayers an opportunity to do so.

Why won’t LT4L publish the full opinion?

Often people don’t publish opinions they receive from KCs because that would cause the opinion to lose legal privilege. HMRC could then obtain a copy of the opinion, the instructions and other supporting documentation.

But this ship has likely sailed. By publishing the summary, LT4L probably waived privilege in the opinion itself.19

Another possibility is that the full opinion is embarrassing, particularly if LT4L actually put Chris Bailey’s amazingly wrong technical claims to Venables.

Another is that the opinion would reveal how Venables is being instructed to not actually advise on the key questions.

A taxpayer cannot reasonably proceed on the basis of an empty summary of advice which reveals none of the reasoning, and may indeed be on an entirely incorrect basis. LT4L clients should be demanding the full instructions and opinion. LT4L will probably refuse.

However LT4L will likely be unable to refuse a formal request for the Venables papers from HMRC. Similarly we expect they will be unable to resist disclosing the documents in the (very likely) event they are sued for ngeligence by former clients.

So was it fraud?

We don’t know.

This may have been a case of people acting in good faith, but just getting the tax position extremely wrong. That is quite hard to credit given the number of apparently qualified people working for LT4L, the number of unrelated errors they have made, the number of people who pointed out their errors over the years, and the length of time they sold the structure. Nevertheless, it remains a possibility.

In our judgment the more likely scenario is “wilful blindness” – that Chris Bailey, the qualified chartered accountant who appears to be behind the scheme, had no real expertise in tax, somehow bluffed his colleagues into thinking he did, and pressed on despite all the criticisms made by other advisers. If that’s what happened, then it could amount to fraud against HMRC and LT4L’s clients – that depends on whether a jury would consider Bailey’s actions to be “dishonest”. We discussed how courts approach this question here. In this scenario, those around Bailey were not dishonest, just reckless/negligent.

The people who run LT4L are in greater legal jeopardy now. They have a detailed analysis of their structure which demonstrates it to be hopeless, and they know HMRC agrees. But, instead of admitting error and acting in the best interest of their clients, they are deep in denial, if not cover-up, and continuing to collect £450 per month in fees from around 450 LLPs – i.e. c£2.5m/year. This behaviour may amount to dishonesty even if the earlier behaviour did not.

There is an additional question around LT4L’s repeated claims that they had special insurance which provided complete protection for their clients, with coverage of “£2m per case”:

These claims are almost certainly false,20 and if LT4L knew the claims were false then that could amount to fraud by false representation. We asked LT4L to explain these statements; they declined.

What should LT4L clients do?

LT4L clients should urgently obtain independent tax advice to regularise their tax affairs, plus independent legal advice to preserve their ability to sue LT4L if (as is likely) they have suffered loss.

We can’t recommend individual advisers due to the risk of a conflict of interest, but there are now a number of reputable legal and tax advisers who are familiar with the LT4L scheme and able to act.

However we fear that most LT4L clients will have no way of knowing they are being badly misled.

Who can protect LT4L’s clients?

Right now there is nobody protecting LT4L’s clients from what we believe to be incompetent advice that will cause them significant financial harm.

Who could act?

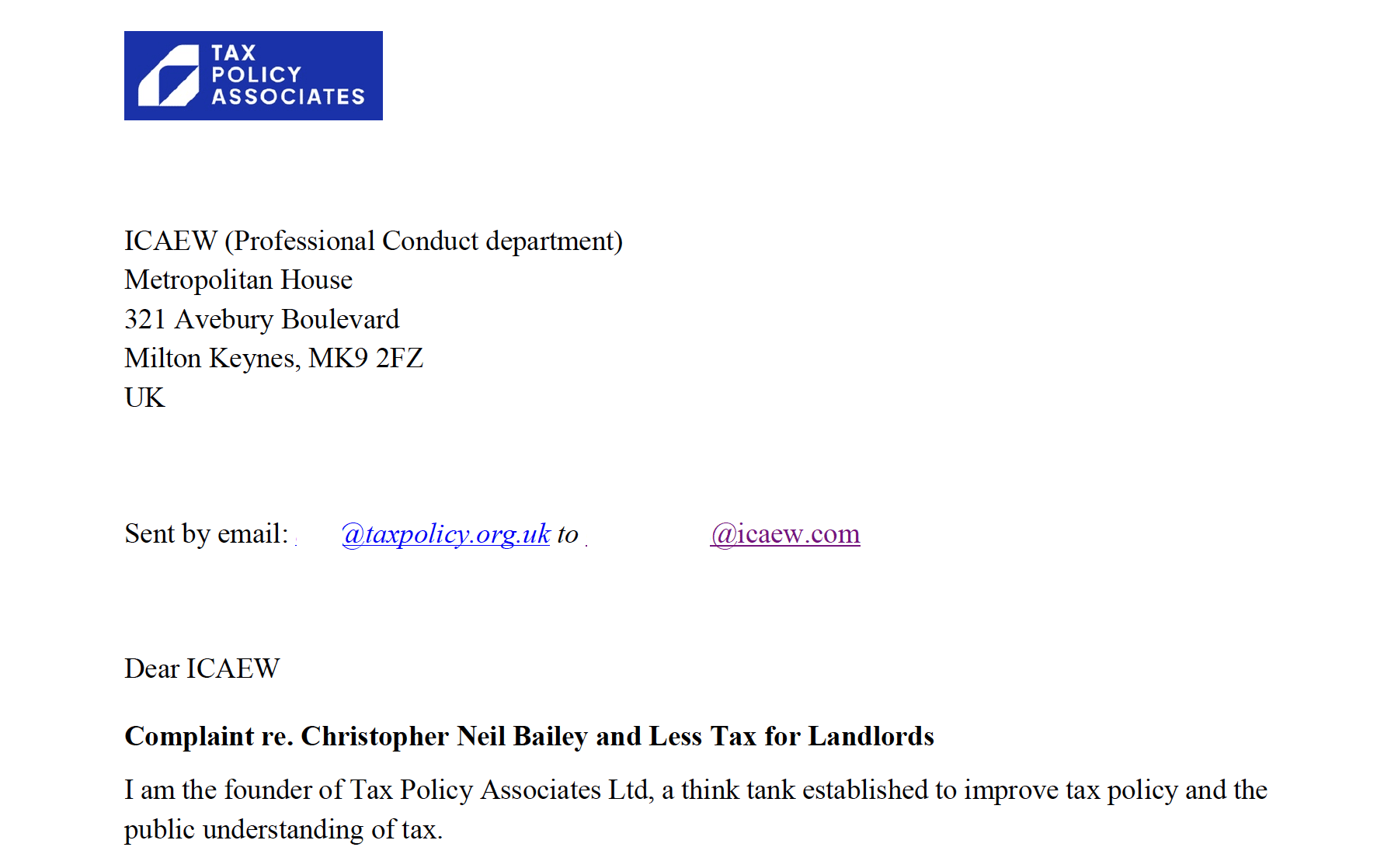

Chris Bailey is regulated by the ICAEW. We reported him to their professional conduct department, and urged swift action to protect LT4L’s clients. It looks like no swift action is being taken. The ICAEW is in danger of completely undermining the concept of self-regulation.

HMRC are enabling LT4L’s behaviour by continuing to treat them as a normal adviser, and allowing or even encouraging them to coordinate their clients’ responses. HMRC should write directly to the clients, warning them that LT4L promoted an undisclosed tax avoidance scheme, and suggesting the clients obtain independent advice.

HMRC should commence a criminal investigation into Chris Bailey and Less Tax for Landlords.

The question is whether the ICAEW and/or HMRC will step up.

Tax Policy Associates is committed to accuracy and we will promptly correct any errors of fact or law in this article. We will not, however, retract our legal opinions in the face of abuse, legal threats and vague non-specific denials.

Thanks to M and L for a helpful discussion on fraud and dishonesty, P for a detailed analysis of the tax evasion caselaw, and K for advice on privilege and collateral waiver. Thanks to S for his insightful review of our original draft. And thanks again to the many people who helped with our original investigation into Less Tax for Landlords.

Footnotes

The Bailey Group was acquired by SKS in September 2020. We understand from SKS that Chris Bailey continued to run the practice until November 2022, and after that point other SKS personnel discovered the nature of the scheme Bailey had been selling. SKS tells us they obtained counsel’s advice and started trying to remedy the position for their clients before the publication of Spotlight 63. So SKS appear to be acting properly and in good faith (although that won’t remove the Bailey Group’s liability for its historic actions). ↩︎

We’ve heard anecdotally that other firms sold similar schemes, but we haven’t seen any evidence to support this. ↩︎

The relief used to be called “business property relief”, and many advisers still refer to it as BPR. This is, however, incorrect – it’s a mistake we made in our original LT4L report, but we will be using the correct nomenclature going forwards. ↩︎

The rate is 19% for profits under £50,000, with a “catch-up rate” of 26.5% on profits up to £250,000, so that the overall effective rate smoothly transitions into the full rate of 25%. ↩︎

This was no small step. HMRC don’t issue a Spotlight for every piece of tax planning which merely doesn’t work; HMRC only Spotlight what they see as particularly egregious and hopeless tax avoidance schemes ↩︎

In this respect Less Tax for Landlords are significantly worse than Property118, whose schemes are poor quality tax avoidance, and who clearly aren’t qualified to advise on tax structures – but we have no reason to suggest they are engaged in intentional fraud. ↩︎

Update 1 March 2024: for some reason the link is down, so we’re linking to an archived version ↩︎

This is from a June 2021 webinar, hosted by Benham & Reeves; they asked us to remove their logo from the video, and we agreed to that. Many people in the landlord real estate world cosseted and promoted Less Tax for Landlords; Benham & Reeves are a long way from being the worst offender. ↩︎

The way they phase the business relief test as referring simply to “trading” is not quite right. A business will usually qualify for business relief unless it consists wholly or mainly of of one or more of dealing in securities or shares, land or buildings, or making or holding of investments”. So what LT4L really need to show is that the insertion of the LLP means that the business no longer consists wholly or mainly of the business of making or holding of investments in land. That is in practice not something they will be able to do. ↩︎

Only in “exceptional” cases will a property rental business qualify for business relief. Taxpayers have failed to qualify for business relief even for an actively managed business of letting holiday cottages; in the words of the recent Grace Joyce Graham judgment, it is only “the exceptional letting business which falls on the non-investment side of the line”. In the Graham case, the deceased “lavished” personal care on guests, including making them home-made food, providing them with fresh crab and fish, arranging linen and towels, making cream teas, and organising weddings and other events. The Tribunal thought this was an “exceptional” case but that, even then, it only “just” qualified for business relief. ↩︎

It is important to note that Mr Gimple cannot be blamed for the actions of Less Tax for Landlords after Spotlight 63 was published, given he retired from the business in 2020. He now runs a firm called “Chancery Law and Tax” which claims to be “one of the UK’s leading providers of Legal Services” but employs no solicitors, barristers or qualified tax advisers. ↩︎

i.e. because it’s probably in their clients’ interests to say that they were mis-sold a scheme which had no technical basis – they may then be able to avoid penalties, or even argue that the scheme should be disregarded. Less Tax for Landlords are obviously not going to run that argument. They’ve a clear incentive to claim that HMRC are wrong and their scheme works, and so keep the clients on their books (paying an annual retainer of around £1,800, which for over 500+ clients is a significant sum) and reduce the risk of negligence claims, or even time them out. ↩︎

The contents of these opinions are generally not publicly available. One exception is the Hyrax case – see in particular paragraph 80 of the judgment. Venables provided an opinion the structure wasn’t disclosable to HMRC under the DOTAS rules. The tribunal had no difficulty coming to the opposite conclusion. ↩︎

The 15% figure used by Property118 and others is, we believe, meant to suggest that the allocation to the corporate member reflects an arm’s length return on services provided, and is therefore disregarded under section 850C(15) ITTOIA 2005. But where the services are personally provided by an individual member of the LLP then s850C(17) disapplies subsection 15. You can’t, in fact, allocate even 1% to the corporate member in such circumstances. ↩︎

There is a question whether it is appropriate for a barrister to advise on the basis of assumptions that are unrealistic, particularly when the barrister knows his advice will be shown to unrepresented individuals. It’s possible of course that Venables did not know the original purpose of the structure; but then, what did he think it was for? ↩︎

Bailey also ignores the fact that incorporation relief requires shares to be issued, which an LLP patently can’t do. ↩︎

Under the doctrine of “collateral waiver”, sometimes described as the “cherry-picking rule”, a summary of the content of advice will generally waive privilege in all of the advice and instructions. See the PCP Capital Partners case. ↩︎

In reality almost all professional indemnity insurance includes an “aggregation clause” which means that the coverage from one error, or series of errors, would be £2m across all their clients. That’s a huge difference. ↩︎

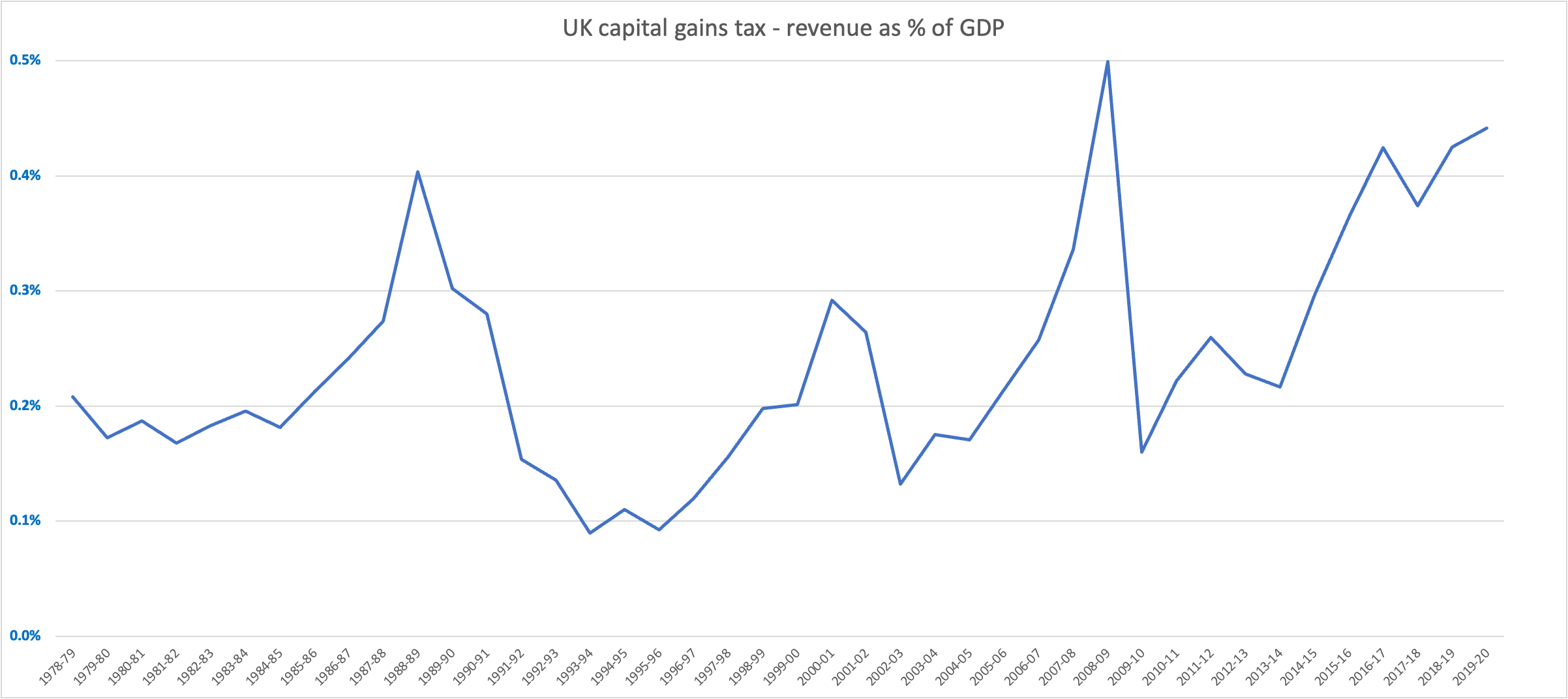

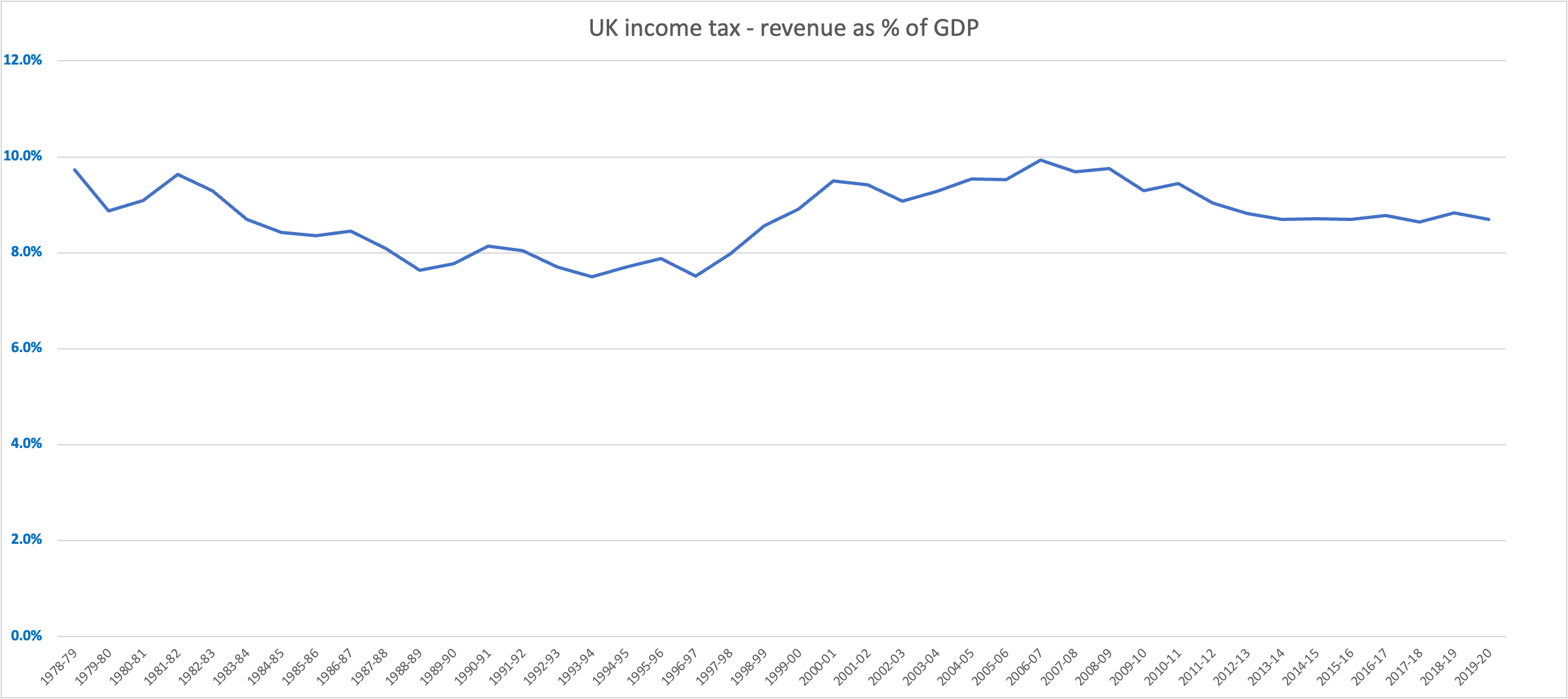

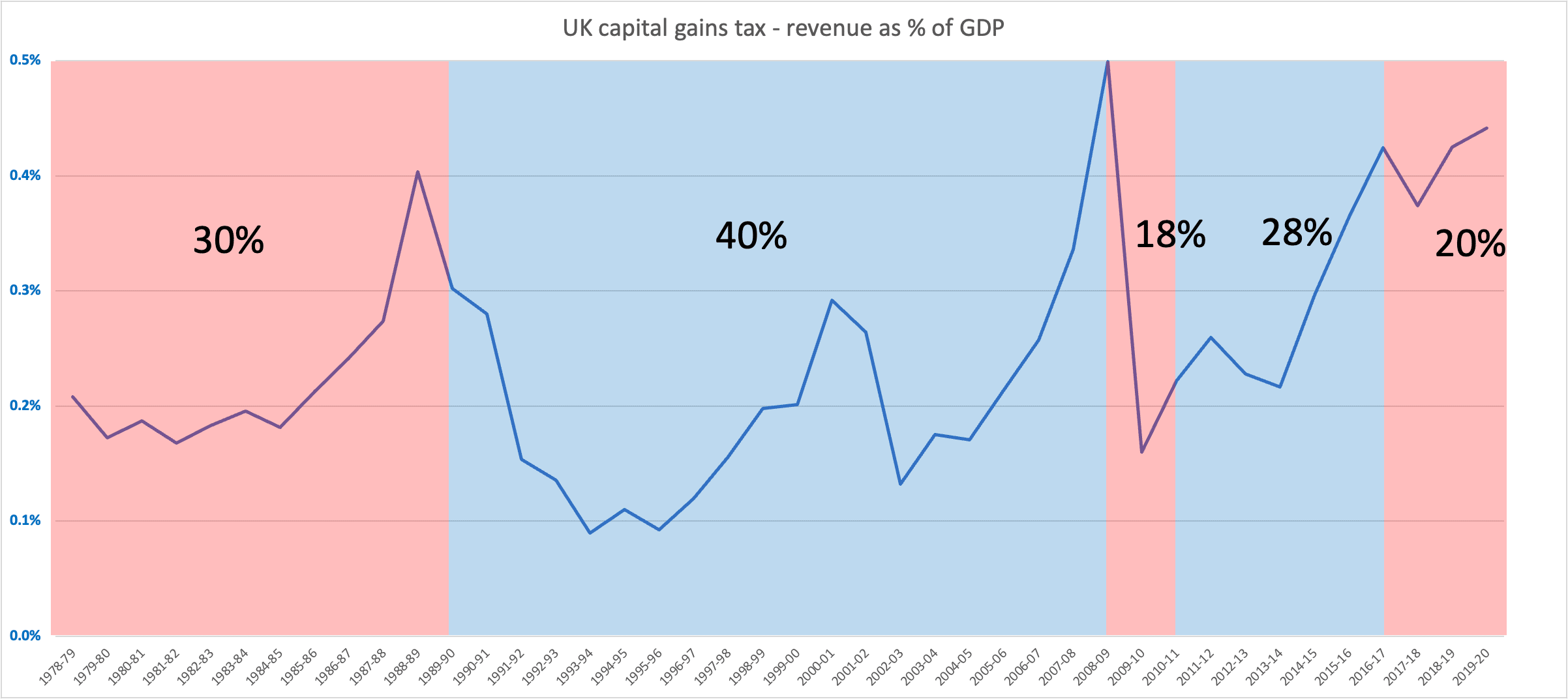

The chart above shows what happens if you plot UK capital gains tax revenues as a % of GDP since 1978. It looks mad.

Income tax revenues, by contrast, look much more sensible:

What on earth is going on?

Politicians fiddling with the rules. Again and again. We start to see it if we overlay the rates:

When the rate is about to go up, people accelerate their sales to benefit from the current lower rate. When the rate is about to go down, people delay their sales until the rate has dropped. I went into some of the history of CGT here.

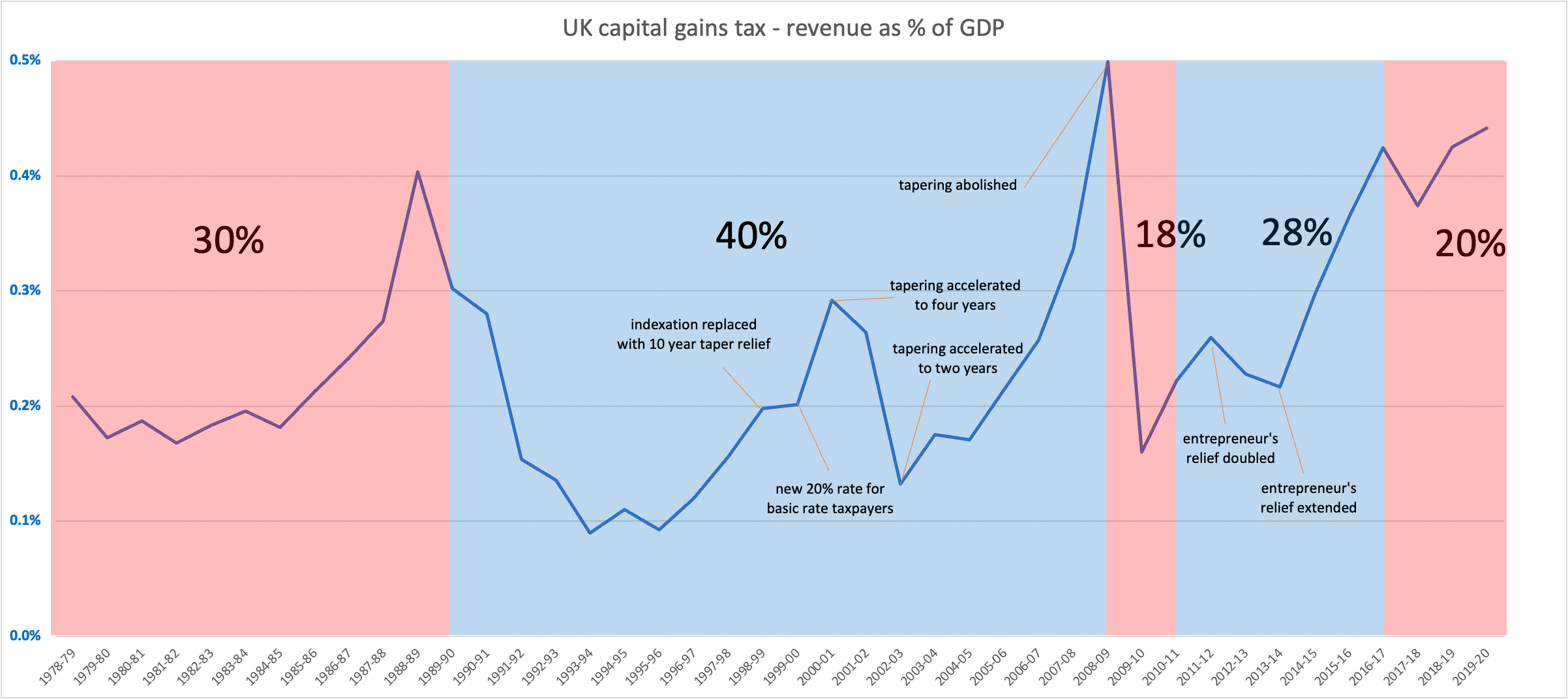

But that doesn’t explain all the peaks in the chart. For that we have to overlay all the constant messing around with the details of the rules:1

At this point some people can get very excited about the Laffer curve, and how the lower rates incentivised economic activity. I’m unconvinced. Even out the peaks and troughs and it’s not obvious there was any net change between 1978 and 2016. And, given the constant changes, it’s not obvious how any rational businessperson could make decisions based on the rate at the time.

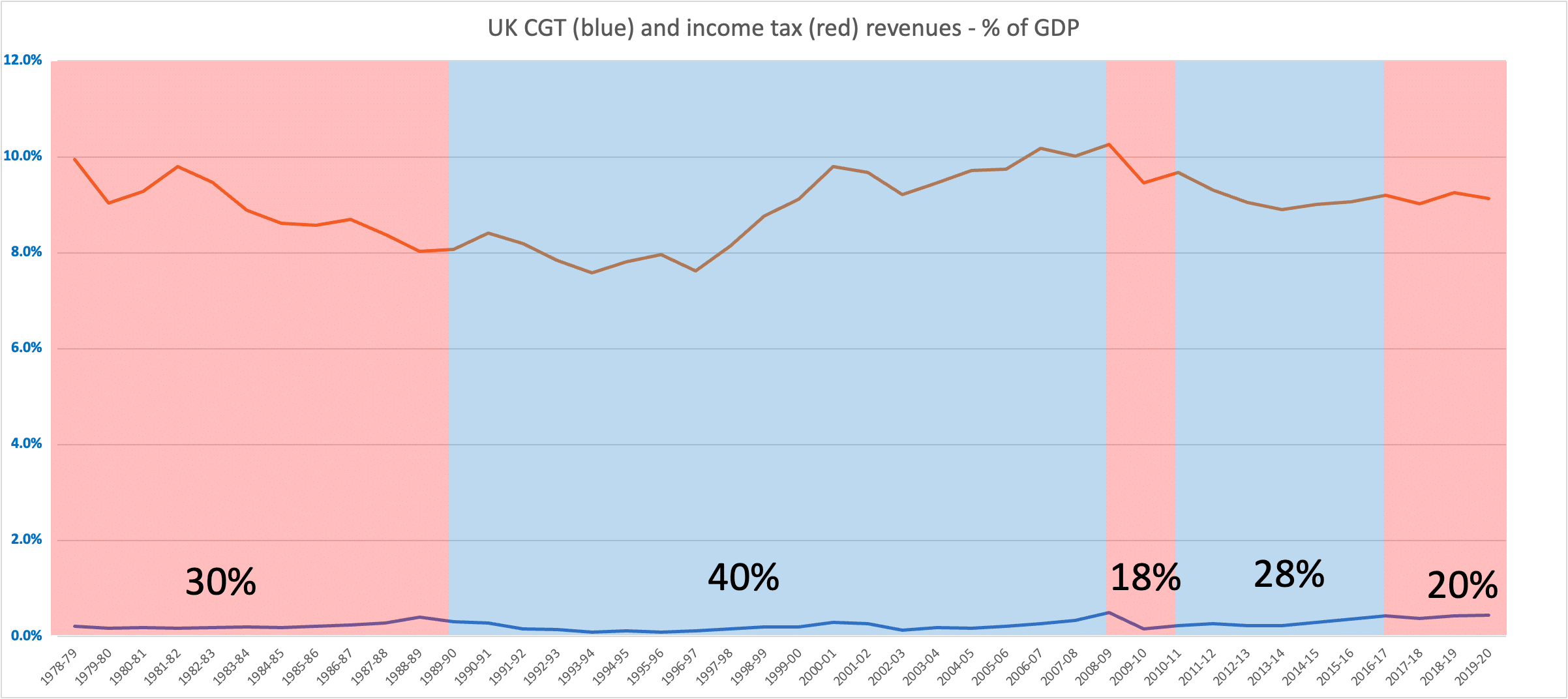

Some other people get very excited about the impact on inequality. I’m unconvinced. Put CGT and income tax onto the same chart, and we see quite how unimportant CGT is, and will always be (regardless of rate):

My view: the current system is dysfunctional. The large gap between the income and capital gains rates creates an unfortunate incentive to convert income (taxed at 45%) into capital (taxed at 20%). On the other hand, there’s no allowance for inflation, so long term investors find themselves taxed on a return that isn’t real. Rewarding avoidance and punishing long-term investment is not a rational outcome.

If some idiot made me Chancellor, how would I fix this?

I’d close or eliminate the gap between CGT and income tax rates, but bring back the “indexation allowance” that stops inflationary gains from being taxed. Nigel Lawson got this right in 1988.

I’d make the change immediate, to prevent a sudden spike in disposals.

And then the important bit: I’d make a big show of announcing I wasn’t going to change any of the CGT rules for the rest of the Parliament. I’d resist the urge to keep bloody changing the rules, and enable investors and entrepreneurs to plan for the long term.

I wrote in more detail about the dysfunctional history of CGT, and the approx £8bn that could be raised by equalising rates, here.

Footnotes

This is greatly simplified. The number of changes when Gordon Brown was Chancellor were particularly egregious ↩︎

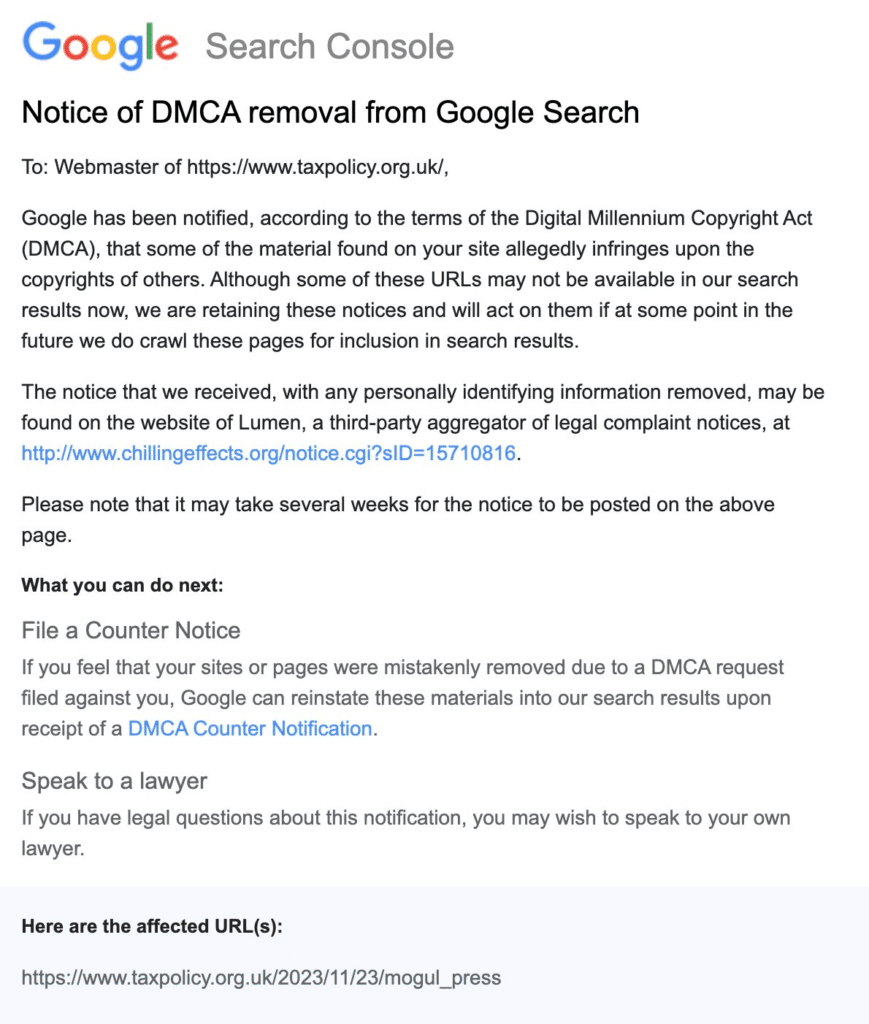

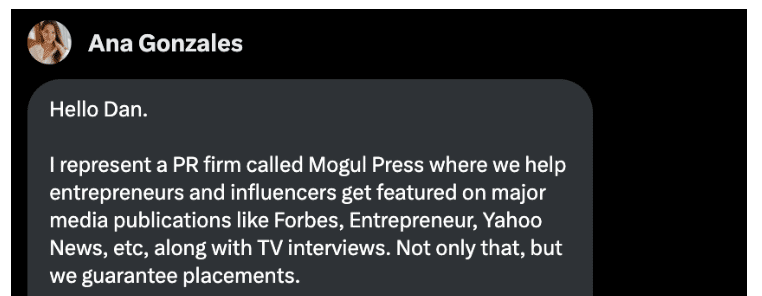

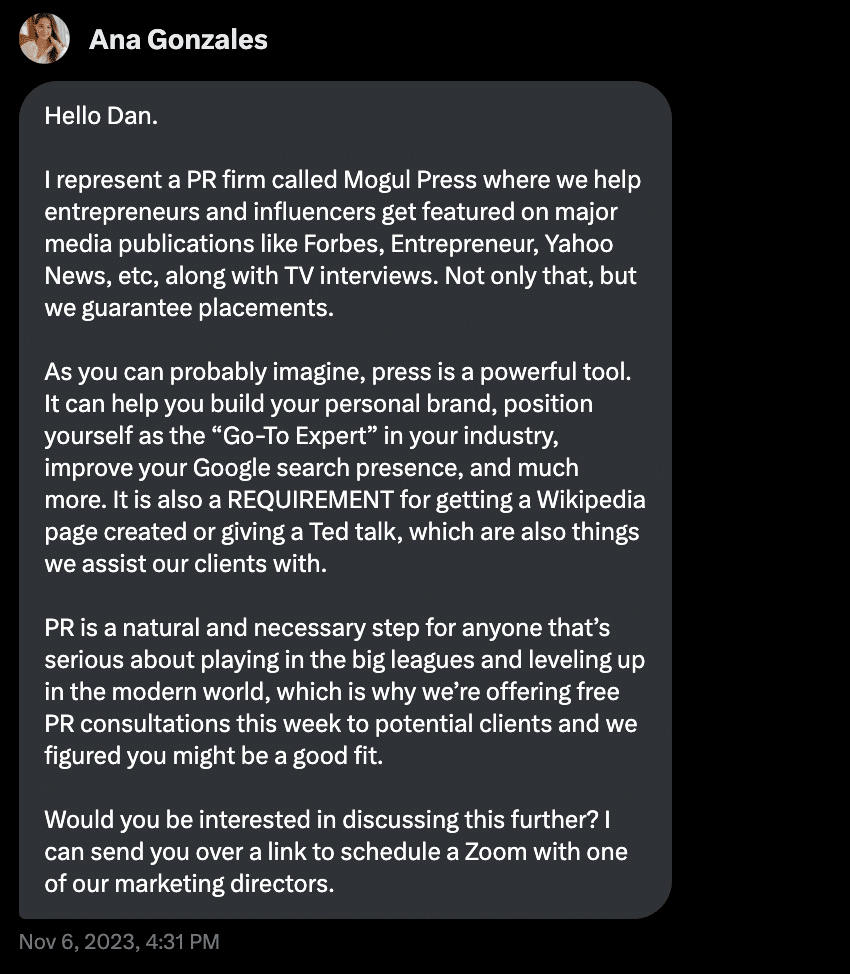

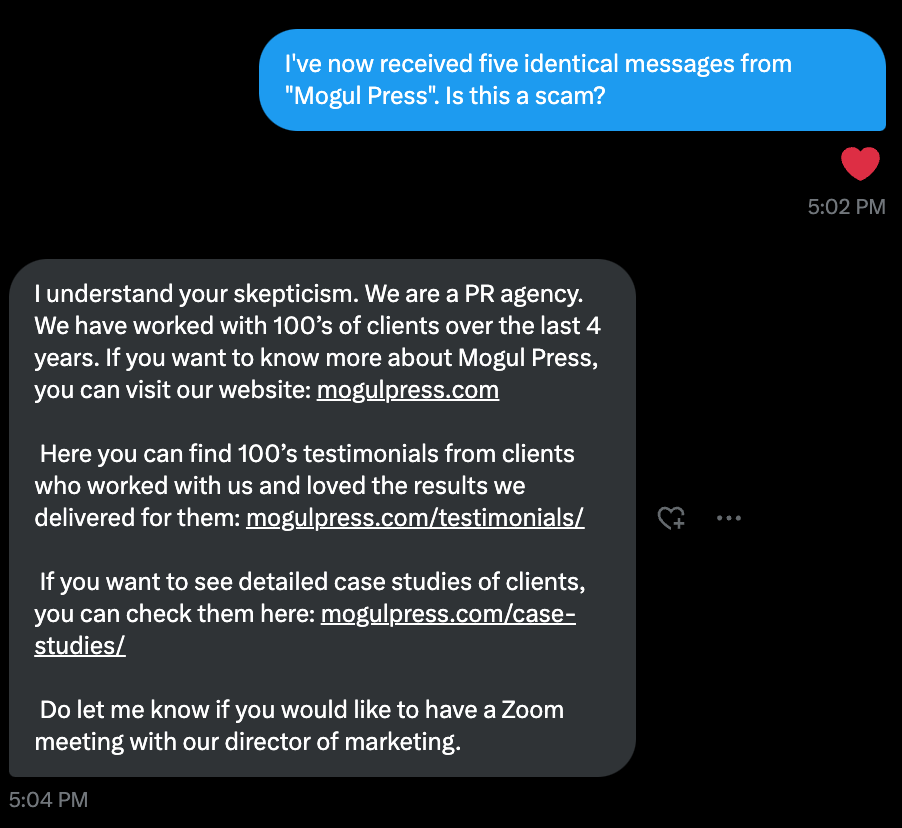

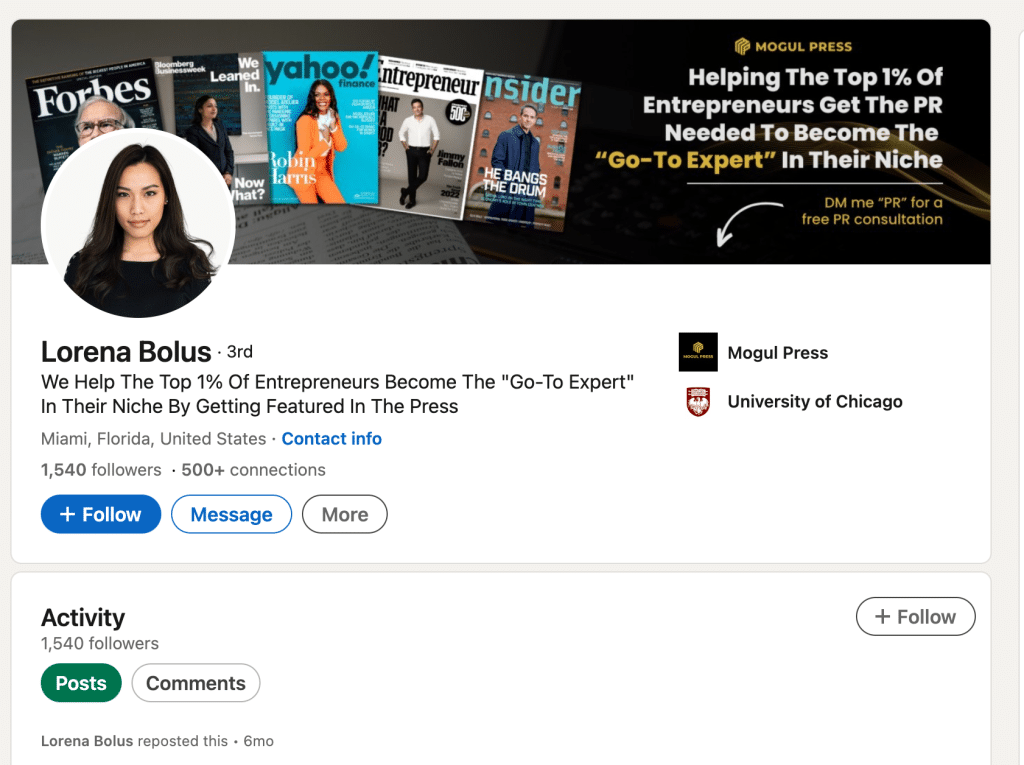

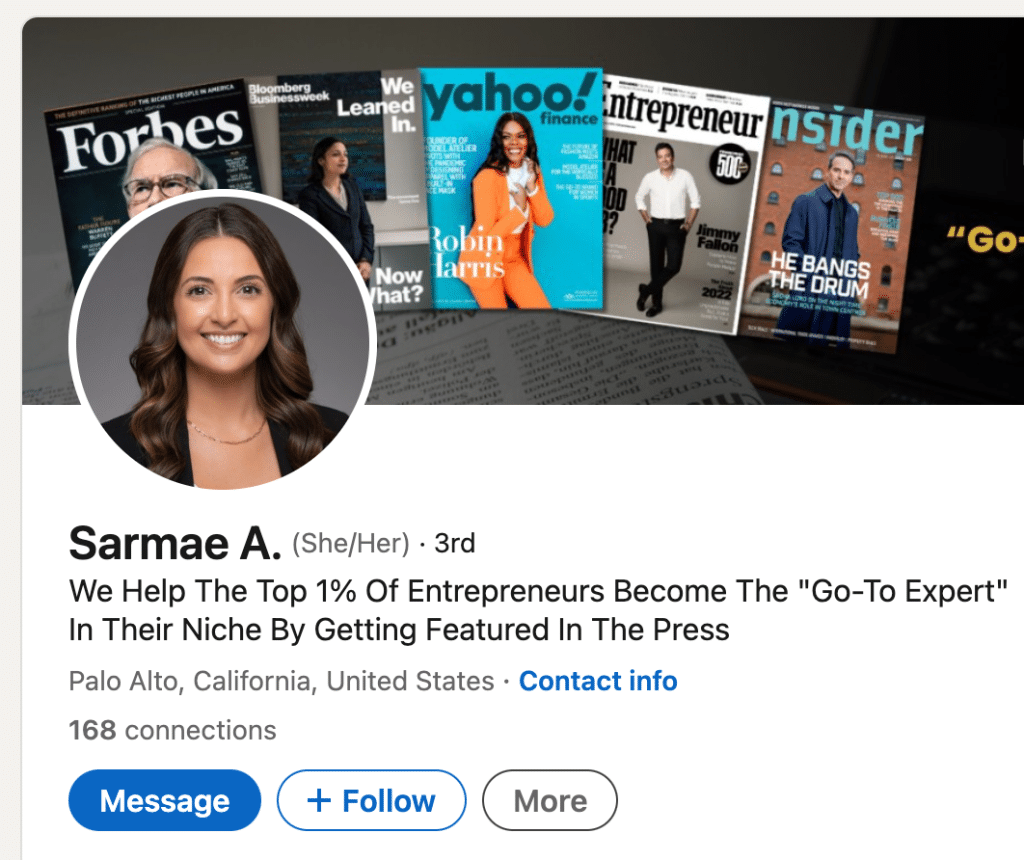

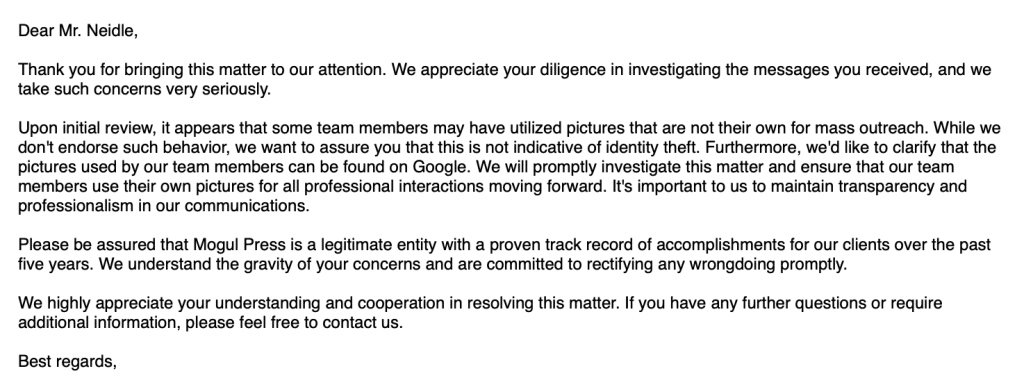

I’ve written previously about a business called Mogul Press, which spams people on social media from fake profiles, often with stolen photos of real people. They claim to be a “PR agency” but their business appears to actually involve charging for paid placements in low quality media.

UPDATE 17 February 2024 – Mogul Press and its associates appear to be in the business of filing fraudulent copyright takedowns. We wrote about it here.

Mogul Press didn’t much like our article. At that point I thought they had several options:

Change their business practices: stop spamming people, stop using fake profiles, and be honest about what their business actually is.

Given they claim to be an “award-winning public relations and communications agency” they could communicate to the world why my article was inaccurate or unfair.

Threaten legal proceedings – although given that my claims were factual, this would always be challenging.

What I didn’t appreciate was that they had a fourth option – fraud.

I received this from Google:

It’s a “takedown notice” under the US Digital Millennium Copyright Act. The idea is that a copyright owner can submit an online form to a service provider, e.g. Google complaining that an indexed page on the internet breaches its copyright. Google will then delist the page and notify its owner. If the owner disagrees there’s a copyright breach then they can file a “counter-notice“. The complainant then has a couple of weeks to begin an actual legal action for breach of copyright; if it doesn’t, the service provider restores access.

I assumed they’d complained about my use of images of their website. These are copyrighted, but I’m perfectly entitled to use them for purposes of comment/criticism under the US “fair use” doctrine. In theory, I could sue Mogul Press for filing a bad-faith takedown notice.

But I was wrong. We can now see copies of the actual complaints and they aren’t incorrect, or bad faith. They’re simply fraudulent:

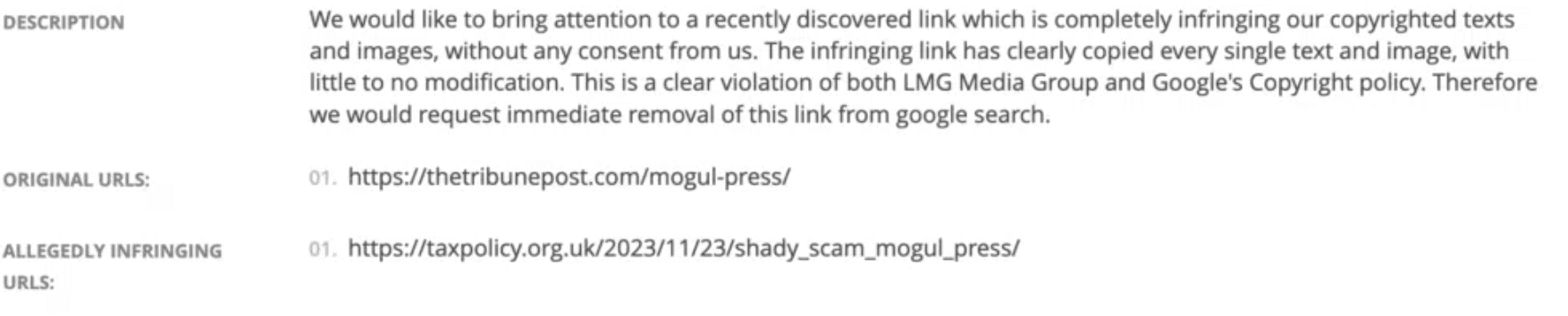

The “tribunepost.com” link (archived version here) is just a direct copy of our article. Mogul Press created it (naturally breaching our copyright) and then filed a DMCA notice claiming that we’d copied them. This is, very obviously, just fraud.1

Given the likelihood Mogul Press and its CEO, Nabeel Ahmad, are just scammers with no easily-traceable assets, it’s probably not worth spending time suing them. I’ll probably hurt them more financially by publishing this article – and that would be an entirely fair outcome.

I asked Mogul Press what they were up to, and they didn’t reply – so I think we can discard the possibility that someone else did this without telling Mogul Press ↩︎

Labour seems set to introduce VAT on private school fees. We thought it would be helpful to set out the ways some private schools might try to avoid VAT, and our assessment of their prospects of success. We’ve identified some approaches which we’ve categorised as “good” (likely to succeed), “bad” (likely to fail) and “ugly” (highly inadvisable and maybe even criminal).

Please note two important caveats:

We’ve written this to help advance the debate, and inform private schools and parents of the issues they may wish to consider. This is not legal or tax advice, and anyone considering implementing any of the approaches we discuss should speak to a suitably qualified tax professional.

The question as to whether VAT should be charged on private school fees is a political question on which we take no position. The question as to the wider impact of charging VAT on the private and state sectors is an education policy question where we have no expertise (we wrote about the issues here). This article focuses solely on the question of how the VAT could be avoided.

Why VAT planning is high risk for private schools

Here’s the big problem: if a school takes any steps to reduce the overall VAT it charges parents, and that goes wrong, the school would have a very large liability.

The reason is that, if a private school doesn’t charge VAT, and HMRC disagrees, then HMRC will have at least four years to challenge the position. HMRC can then assess the school to VAT and it will then immediately have to pay.1

The school would be able to appeal but, unlike income tax and other direct taxes, the school would have to pay up-front first, and then spend likely at least two years in an appeal process.

This creates a very significant practical risk for schools engaging in any VAT planning. The planning could appear to succeed and the school hear nothing for four years; then a sudden HMRC enquiry could result in it having to pay four years’ worth of VAT, plus interest, plus legal fees, all in one go. In other words, an amount broadly equal to one full year of fees (plus potentially penalties too).

In principle the school may be able to recover this from parents. That would however require specific wording in schools’ contract with parents, providing for an indemnity in the event HMRC asserts the school charged VAT incorrectly. The current standard form school contract doesn’t do this2.

Even if the contract in principle enabled recovery from parents, the practicalities would be difficult. Some parents would be abroad. Others may not be able to pay. Many would have left the school. All will likely be unhappy. Parents may be able to argue that they are not bound by an indemnity, for example because the school did not fully disclose the risks, and the indemnity is therefore unenforceable (the Consumer Rights Act applies to private schools’ contracts with parents).

We therefore conclude that it is imprudent for any school to engage in VAT planning beyond the extremely simple and vanilla (the “good” items we identify below). Anything further presents a risk that any prudent school should regard as unacceptable.

Note that it doesn’t matter what advice a school obtains – accounting firms, KCs, whatever. If HMRC challenge the arrangement (and if it’s one of the ugly ones below, they will) the tax will have to be paid up-front. And in our view HMRC will win any appeal on these structures.

The good – a year’s fees in advance

Say the election is held in October 2024. What if parents pay a full year’s fees in September 2024 rather than, as is more normal, paying for each term shortly before it starts?

From a VAT point of view, VAT will be charged at the point an early payment is made. So the applicable VAT rules would be those in September 2024, and there would be no VAT. If there was an October 2024 Budget imposing VAT on private school fees, then that wouldn’t ordinarily change the VAT chargeable the previous month.

We say “ordinarily” because, in principle, Government could legislate retrospectively, so that fees paid in advance prior to the Budget became subject to the new 20% rate. That would be unusual, and we would be surprised if it were to happen. A prudent school may, nevertheless, wish to explicitly reserve the right to charge VAT if the legislation is retrospective.

On the other hand we will almost certainly see “anti-forestalling” rules. The Government might announce very quickly after the election that it will apply 20% VAT to private school fees. However the actual legislation would take some time to finalise and pass, particularly if (as would be wise) there is a consultation on the detail.3 That creates a protracted period during which people could seek to pay months and even years of fees in advance. A wise Government would therefore announce that any payment of more than a term’s fees in advance, from the date of the announcement, will be subject to VAT. This approach has been previously adopted for other VATchanges.

Hence it would be sensible for any advance payment of fees to be made well in advance of any announcement.

The theoretically good – several years’ fees in advance

In principle paying several years’ fees in advance of an election should be just as good as paying one year’s fees in advance.

However it seems less likely to happen, for several reasons:

There will be a limited subset of people who can both afford to pay several years in advance, and care enough about the VAT cost to try to escape it.

Schools may be wary about locking in the current level of fees for several years, particularly in a relatively high inflation environment.

What if parents have to move out of the area, or otherwise withdraw their children from the school – would they get the fees back?

If that’s wrong, and we did see widespread payment of multiple years’ fees in advance, then the odds of retrospective legislation would increase. It may be unwise for private schools to push advance fee payments too far. It would certainly be a good idea for them to explicitly reserve the right to charge VAT if in fact legislation is retrospective.

UPDATE – November 2024. What we in fact saw was widespread prepayment but often structured really badly, so the “prepayments” in many cases weren’t actually prepayments at all. We wrote more about this here.

The also good

There are other reasonably uncontroversial ways schools can respond to VAT on their fees:

Schools will be able to recover VAT on their “input” costs, for example IT equipment, rent (not relevant to most schools) and the cost of building/maintaining buildings. This may require updating their accounting systems.

Under the “capital goods” scheme, schools will be able to recover some VAT for capital projects paid for in the previous ten years – previously these VAT costs would have been entirely non-recoverable.

Some school clubs have historically been run by external providers, invoicing separately (e.g. music lessons during school or after-school clubs). Where the providers aren’t subject to VAT (because they are exempt, zero rated, or their turnover is too small to attract VAT) then this will likely continue after school fees become subject to VAT. But see “unbundling” below.

There would be nothing wrong with schools responding to the VAT change by trying to increase parents’ charitable donations (as Labour do not currently plan to end charitable status). Charitable donations aren’t subject to VAT; they also provide school and parents with gift aid (effectively adding up to 80% to the donation). In principle, the more donations a school receives, the less fees it needs to charge.

None of these are avoidance.

The bad – legal challenges

We may see attempts to challenge the imposition of VAT on private school fees.

Provided the legislation is enacted competently, we see no realistic basis on which such a challenge could be made:

EU law would have made it unlawful to simply scrap the VAT exemption for private school fees.4 However, post-Brexit the UK faces no such constraints.

EU law principles such as fiscal neutrality might also have been used to argue that the imposition of VAT on private school fees is unlawful (we are sceptical); but post-Brexit such principles can no longer override UK law.

One might argue that the abolition of the private schools VAT exemption infringes the Human Rights Act/ECHR. However, even in principle, the Human Rights Act cannot override primary legislation – all a successful challenge would do is provide a “declaration of incompatibility“, asking Parliament to think again. And in practice, Courts have deferred to Parliament on tax questions, and no ECHR challenge has ever resulted in tax legislation behind held to be incompatible with Convention rights (even in the case of retrospective legislation). Any argument around private school fees would in our view be weaker than previous failed challenges.

We would therefore caution parents and schools against wasting large sums of money on legal challenges with little or no reasonable prospect of success.

The bad – unbundling

It’s been suggested some services such as boarding school accommodation, after-school clubs, sports activities and transport (e.g. school buses) could be “unbundled” and charged separately, and continue to be VAT exempt.

We are doubtful this will work. The technical question is whether there are two separate “supplies” for VAT purposes (e.g. accommodation with VAT at 0% plus education at 20%) or one supply (education at 20%). The courts have held that the key question is whether the two supplies are “distinct and independent”, but added that a single economic transaction should not be “artificially split”. HMRC have a useful summary of the issues here.

The issues are illustrated by the BPP case. One company provided tuition, with VAT charged at 20%. Another company in the same group provided textbooks intended to be used as part of the tuition, with VAT charged at 0%. BPP argued these were two separate supplies. It succeeded because the supplies were truly independent – a significant number of students bought the books without attending the course, and a significant number attended the course but bought the books elsewhere (and it would have succeeded even if the same company had provided both tuition and books).

Private schools will struggle to show that “unbundled” supplies are really independent – it is unlikely they will be purchased separately from the education. The most obvious example is boarding: it’s usually only available to pupils at the school, and is often part of the history and ethos of the school. Eton is not realistically going to open up boarding to people attending other schools (and if they did so in theory, with nobody taking it up, that would not assist them). Furthermore, any “unbundling” faces the significant challenge that it will clearly have been arranged in response to the VAT change.

There may be some cases where “unbundling” succeeds, but (as we note above) the risk will be on the school, and it’s a risk we believe prudent schools will not take.

Nevertheless, it may be wise for a Labour Government to introduce specific unbundling anti-avoidance rules, to serve as a clear “stay off the grass” warning sign.

The ugly – avoidance schemes

We can imagine a variety of different types of planning/schemes people might employ to avoid or reduce fees. We don’t believe any of these will work, and some could even result in prosecution:

Any attempt to tie donations to the provision of education would likely make that “donation” a fee, subject to VAT. If schools went further, and disguised a fee as a donation, then could potentially amount to criminal tax evasion.

For example, a school could try to game donations by quietly hinting that the children of people making large donations would receive full scholarships. But then the donation is, realistically, a fee, and subject to VAT. If the arrangement is hidden from HMRC then it could again be regarded as criminal.

A few people have suggested creating offshore entities owning the schools. That wouldn’t change anything. VAT is charged based on where the school “belongs” which impact means where the education takes place. So if a school actually moves to Ireland, with teachers in Ireland and children educated Ireland, then that would indeed escape UK VAT. But just moving the company achieves nothing.

A parent’s employer might think it could pay for their children’s education, and therefore recover the VAT cost. That doesn’t work, because the supply from a VAT perspective is from the school to the parent (reimbursed by the employer). The employer cannot recover the VAT. A variant on this would involve a company owned by the parents themselves – that risks heading into criminal territory.

A variant on this: school could hint that if a parent’s company sponsors an event or building then their children would receive full scholarships. The company would ordinarily be able to recover VAT when it buys advertising/sponsorship. However again it would be clear the “sponsorship” is really the payment of school fees for the benefit of the parents. If hidden from HMRC the arrangement could be regarded as criminal.

We don’t think unbundling is a very good idea, but an even worse idea would be to load a disproportionate amount of value into the unbundled items, for example charging thousands of pounds for textbooks or school uniforms, and asserting the 0% VAT rate applies. This again risks prosecution.

Schemes where parents appear to pay several years of fees in advance, but in reality don’t. They keep the money and the school only gets it slightly ahead of each term, as it normally would. For example, you pay say five years’ of schooling up front with no VAT, but funded with a loan from the school. You pay the loan back over time with interest, and the payments just happen to equal the fees you would have paid normally. Any such scheme would be highly vulnerable to challenge (particularly if, as may be inevitable, failing to keep up with the interest payments means that your child can no longer go to the school – it is then clear that this is not interest, but a fee).

We can imagine even more aggressive structures – for example a school moving to a model similar to hairdressers or a strip club, where each teacher/sports coach is an self-employed independent contractor sharing premises. The school provides billing and coordination services but the teachers don’t work for the school. Most of the teachers are under the VAT threshold (or the private tuition exemption applies), so all the teachers’ fees would be free of VAT. This, however, seems wildly impracticable – we doubt most schools could be run consistently with this model, although possibly very small schools could (e.g. with just two or three teachers).

Independent special schools would likely be exempt from the new rules. There is a designation process for these schools – it is possible some schools might try to obtain a special school designation that should not be applicable to them. Again that could amount to criminal tax evasion.

A school could split into multiple separate companies, each below the £85k threshold. There is specific anti-avoidance legislation to stop this, and it’s an area where HMRC is very active.

We might even see “structured” solutions, such as converting a school into an company with parents subscribing for shares – the subscription of shares is not normally subject to VAT. Or perhaps an LLP with teachers and parents as members. All such structures are highly unlikely to succeed given the obvious reality of the arrangement – that the parents are paying to receive a service.

We don’t think specific rules are necessary to prevent any of these schemes, as we believe all would clearly fail. There will probably still be some people who try them, but that would be the case regardless of what anti-avoidance is introduced.

The bottom line

Whenever engaging in any tax planning, or indeed any legal transaction of any kind, a good question to ask is: “What’s the worst that could happen, and what would my liability be?”. The answers in this case suggest that trying to avoid VAT on private school fees will almost always be a bad idea.

Thanks to C for the first draft of this article and V for HRA/ECHR input. Thanks to Q for reading through the final draft. Most of all, thanks to all the people who contributed avoidance ideas on my original Twitter and LinkedIn threads.

It’s slightly more complicated than this; taxpayers have the right to first seek an internal HMRC review, but in practice that almost never changes the outcome. ↩︎

There’s optional language saying fees are exclusive of tax, but that’s not enough to create a four year indemnity ↩︎

The usual timeline would be draft legislation published for consultation say in January, to go into the Finance Bill in March/April and obtain Royal Assent in July. ↩︎

Although the conditions in Article 133 of the VAT Directive could have been imposed, which in practice would probably have amounted to the same thing ↩︎