Many “tax avoidance schemes” are in fact just tax fraud. We have been investigating one in detail, involving a company splitting its business between 10,000 companies, and using social media to hire 10,000 Filipino individuals who it can pretend are the shareholders/directors.

The scheme was facilitated by an opinion from a well-known tax KC, Giles Goodfellow. Mr Goodfellow was surely not aware the scheme would end up being a fraud, but he should have been. His opinion was in our view one that no reasonable tax lawyer should have given.

This is part 1 of our report – it introduces the scheme, how it worked, why it cost the UK at least £50m, and why we believe it should be described as fraud and not tax avoidance.

Part 2, with the KC opinion is here.

Part 3, with another KC’s opinion, is here.

The background

Elements of the scheme have been reported before, but we believe this is the first time the full picture has been put together.

Back in 2016 and 2017, Simon Goodley at the Guardian reported on a tax avoidance scheme involving the Anderson Group.1 Simon’s articles are here, here and here, and File on Four later ran a programme on the schemes, summarised here. The scheme companies later went bust, leaving HMRC out of pocket. Our founder, Dan Neidle, said at the time that this looked more like criminal tax evasion than tax avoidance, and that is also HMRC’s view of these structures.

Seven years on, we now have much more information on the scheme and the people running it. We know that a director of a company involved faced serious legal consequences, and admits the scheme was a fraud. We also have a copy of the scheme opinion from a senior tax barrister/King’s Counsel (KC) – it’s been described by other KCs as “shocking”, “appalling”, “mind-blowing” and “deeply irresponsible”. But before we go through the KC opinion, we will set out the detail of the scheme:

The players

The usual kind of contracting arrangement looked like this:

- A contracting business employed thousands of agency workers using a company in its group (an “umbrella company” in the jargon of the trade, because it covered numerous contractors).

- When they signed up a worker, the worker became employees of the umbrella company.

- Another business needing temporary workers would pay the contracting business a daily rate for those workers. There would be 20% VAT on this.

- The contracting business would then pay the VAT to HMRC, retain some of the daily rate as its profit, and pay the rest to the umbrella company to enable it to pay the salary of the workers (after applying employer’s national insurance and deducting income tax and employee national insurance).

This was a sensible and entirely normal arrangement, which avoided no tax.

The scheme

At some point in 2016, unknown parties, including an outfit called the Aspire Business Partnership LLP, and another entity (“AA”) implemented this avoidance scheme:

- AA established a large number of new UK companies. The Guardian article said there were 2,000, but we now have good evidence there were at least 10,000.

- When AA signed up a worker, they would become an employee of one of these new companies, with one or two employees per company. So instead of one “umbrella company” there were many “mini umbrella companies”, or “MUCs”.

- Central to the scheme was a company called Contrella. It is unclear whether Contrella was the historic “umbrella company” or was new to the business.

- A business needing temporary workers still paid AA a daily rate. AA paid it to Contrella. But Contrella now in turn made payments to each MUC, and it was the MUC that paid the workers.

- The MUCs did nothing themselves. They appointed AA as their agent to manage everything to do with their operations

Then this astonishing and outrageous additional step:

- each of the 10,000 MUCs’ shares were acquired by a different individual living in the Philippines, and that individual also became the sole director.

It is hard to over-state just how bizarre and deeply suspicious that final step is. Our team of tax experts have worked on complicated structures for some of the largest and most complex businesses in the world. None of us have seen anything remotely like this.

Who was the end client for the scheme? The Guardian said it was the Anderson Group.2 Anderson denies that, and the CEO of Anderson continues to deny that to us today, but the Guardian report had good evidence to the contrary, and see below for more details on the links between the companies and Anderson).

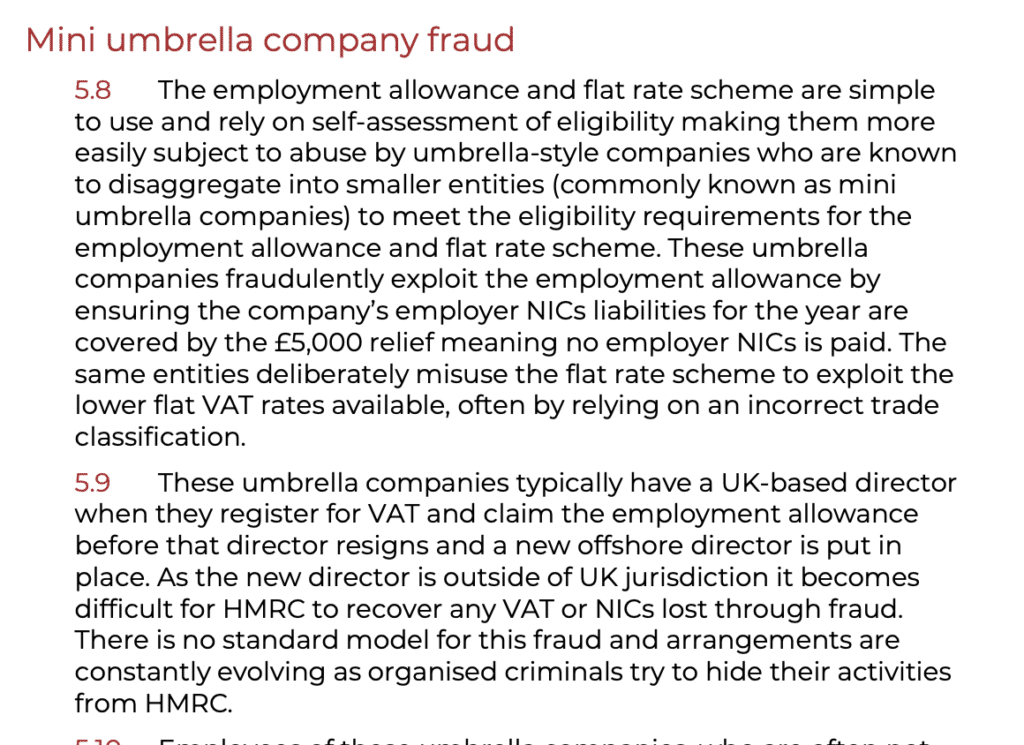

It’s important to note that there is plenty of other tax avoidance/evasion that goes on involving mini-umbrella companies, such as paying the MUCs’ employees via loans or other arrangements which supposedly don’t attract income tax and national insurance (but really do). Or simply just deducting tax/NI from payments to employees and then never accounting for it to HMRC. HMRC has warned about these issues here. We are not alleging that the MUCs involved in this scheme did any of this.

The “avoidance”

Small companies at the time benefited from two special government incentives: a flat rate VAT scheme (that in practice meant they got to keep about half the VAT that would normally be handed over to HMRC) and a national insurance employment allowance (worth about £3,000 at the time). AA and Contrella normally wouldn’t get either of these, because they weren’t small companies.

The intention of the scheme was that each of the 10,000 MUCs could claim the small companies’ VAT scheme and employment allowance.

We can estimate the minimum amount of tax avoided by the scheme if we assume each company has an employee for which it charges out £20,000 in fees (almost certainly it would be more than that). There is then a £3,000 tax benefit from the employment allowance, plus £2,000 from the VAT flat rate scheme (i.e. half the 20% VAT on £20,000). That’s a total of £5,000 per company, across 10,000 companies – i.e. £50m per year (and the companies ended up lasting about a year on average).

This is very much a minimum, because the VAT flat rate scheme qualification conditions go up to £150k per company, and so the theoretical maximum tax benefit avoided by the scheme would be if each company charged out £150,000 in fees – the total figure then is £180m.

And the 10,000 companies are the tip of the iceberg: Richard and Gillian have found more than 55,000 other companies that look to be part of similar schemes – most likely sold by Aspire (or other promoters) to other employment agencies. That implies a total loss to HMRC of at least £300m, even on our very cautious £5,000 per company estimate.

The Filippino “directors”

An obvious question is: how did they find 10,000 people in the Philippines willing to be shareholders and directors, and how did they coordinate them?

The amazing answer: by advertising on Facebook and YouTube to recruit Filippino directors:

The “director/shareholders” were paid £150 per year. In principle, they were acquiring the companies for £1 each (and that’s what the Companies House filings show). But in practice, they weren’t asked to pay anything (“We will never ask you for a single centavo”):3

In return, the directors “managed” their company by clicking through to an online portal which prompted them to click an “authorise” button whenever the people managing the scheme wanted the company to do something:

The scare quotes around “directors” and “shareholders” is because the individuals were clearly not really directors or shareholders in more than name. The people running the scheme really owned the shares (were “beneficial owners” as a legal matter) and were the real directors (“shadow directors” from a company law perspective). But none of that was disclosed to HMRC when VAT/national insurance returns were made. And the Companies House “persons with significant control” entries failed to show who was really running the show.

The company mentioned in the videos, Compass Star, is connected to Alan Nolan, who founded Aspire, the company which appears to have promoted/arranged the scheme.4 The connection between Compass Star and Aspire/Nolan is clear in this BVI court judgment, and also in this video. Aspire seems to have established multiple schemes for different groups, but all appear to have been run the same way. Aspire were the “Instructing Agent” when the KC provided his opinion – which likely means they were the promoter.

Was this really avoidance – or criminal tax evasion?

HMRC say these schemes are tax evasion – which is a crime – and not tax avoidance. See here from 2021, and this very clear statement from a consultation document published on 7 June 2023:5

We agree that the schemes are likely fraud. Our reasoning is as follows:

- The trick of splitting your business into lots of little businesses is an obvious one, so there are rules to stop this, for both VAT and the employment allowance (plus common law and statutory anti-avoidance principles and rules). A year before this scheme was implemented, HMRC had published a Spotlight stating clearly that HMRC believe such schemes did not work.

- The KC’s opinion provided various arguments that the scheme worked despite all these rules. In our view, these arguments were very poor, and we’ll discuss them in our next report. However, the KC’s advice was on the key assumption that each company was to be organisationally independent and had as much autonomy over its business as practical. We think it was improper for him to make that assumption, but for the moment let’s put ourselves in the position of his client who (if we are being charitable) took his opinion, and the assumption, seriously.

- The way the companies were established completely disregarded that key assumption. The way directors were recruited, and the automated portal created for them to authorise documents, meant that there was zero independence and zero autonomy.

- Hence, even on the KC’s view, the flat rate VAT and employment allowance benefits were not available, because his fundamental assumption that the companies were independent/autonomous turned out to be very far from correct.

- In light of the arrangements put in place to coordinate the Filipino directors, we believe any competent tax adviser would have known that this scheme would fail (even without reading the KC opinion). Anyone (tax adviser or informed layperson) reading the KC opinion would have expected the scheme to fail.

- And it looks like no care was taken to prevent the same individuals acting as directors of multiple companies.6 This means that even if the directors genuinely had been independent of each other and Anderson/Aspire, and even if the KC’s opinion had been correct, the scheme still failed. Given we can find this after a few minutes of checking a spreadsheet, it’s curious that the promoter didn’t identify and stop duplication. The fact they didn’t check, or didn’t care to check, suggests a level of recklessness which may itself reach the point of criminality.

The fundamental difference between tax avoidance and tax evasion is that many people may disapprove of tax avoidance, but as long as it doesn’t involve dishonesty then it’s not a crime. If there’s dishonesty then it is a crime – criminal tax evasion. The modern test for dishonesty in a criminal trial looks at whether a person’s conduct is dishonest by the standards of “ordinary decent people”. Typically in a tax context that means hiding things from HMRC, or deceiving HMRC as to the true nature of things.

It is our view that either we are mistaken, misunderstanding some key aspect of what was going on, the people implementing this scheme were astonishingly incompetent (e.g. they forgot about the KC opinion), or they deliberately claimed tax benefits they had been advised would not be available. If the latter, then the scheme was tax evasion.

We do not know which individuals were responsible for the tax evasion, and hence cannot comment on where criminal liability might lie. We cannot believe the KC had any idea that implementation would be as described above, and hence there is no question of him attracting criminal liability.

We have written more about the distinction between tax evasion and tax avoidance here.

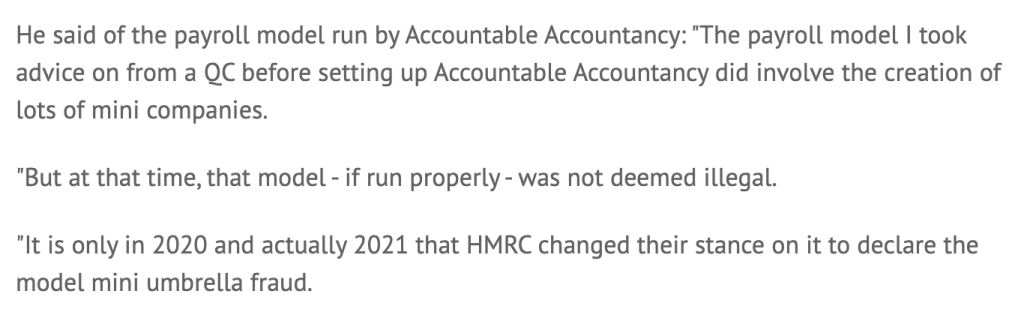

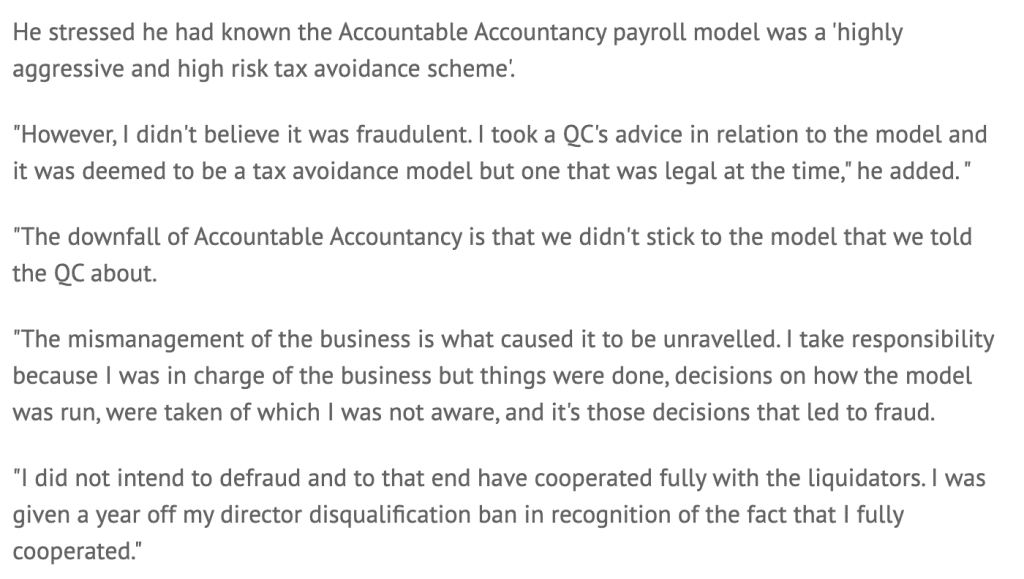

At least one person involved, the director of Contrella, has already faced serious legal consequences. He admits the scheme was a fraud, but his justification is interesting:

and:

So there are two different explanations here. One, that we can dismiss, is that the structure wasn’t fraud when it was put in place, but because fraud due to HMRC “changing its stance”. That is clearly not correct.

The other is that the QC advice was not followed – perhaps for the reasons we identify above.

There is of course a third possibility: that the scheme would always in practice have involved fraud, because an element of deception is essential to it – the claim that the companies are independent, when they cannot possibly be.

Can we really be sure there were 10,000 companies?

Some amazing work was done on this by Richard Smith, a freelance investigative journalist, and Gillian Schonrock, a fraud investigator. You can read about it in more detail, and work through the evidence yourself, on this website (the tongue-in-cheek presentation belies the seriousness of what it shows).

Richard and Gillian’s have identified 10,000 mini-umbrella companies associated with the Anderson Group, which they’ve very kindly shared with us. Graham Barrow, an expert in investigating Companies House abuse, very kindly spent time independently investigating the Anderson Group MUCs, and (with no prior communication as to the methods of the previous work) independently reached almost identical conclusions. Tax Policy Associates also independently verified the results of both sets of research.

Hence we are very confident that 10,000 is the correct figure. We should stress that the legal conclusions drawn in this article are ours and ours alone – Richard, Gillian and Graham are not lawyers and make no claims about the legality of the practices they have documented.

Richard and Gillian have kindly let us publish the full list of Anderson-affiliated companies here. Around 10,000, and all likely connected with the Anderson Group. You can click through to Companies House and check each one out yourself.

There are a few different signs that point to each of these companies being connected to Anderson:

- Anderson Legal Services as a member. Controlled by Adam Fynn, who owns Anderson. Subsequently renamed to Varon Services Limited, then dissolved (company number 08274743).

- Anderson Company Solutions Limited either as agent in the original incorporation documents (the first document filed with Companies House) or as a creditor. Adam Fynn was a director at the time. Renamed to Balance Professional Services Limited, and is in the process of being struck off (company number 08123110).

- Alona Varon becoming a director to strike the companies off. She did this a lot – over 4,400 times. Varon was a director of Anderson Legal Services/Varon Services Limited.

- Samantha Forbes appointed as company secretary. She also did this a lot (although Companies House doesn’t link her roles so they’re harder to find, but there again appear to be over 4,400). Forbes is a director of Fynn’s other business, the Drinks Experience Group.

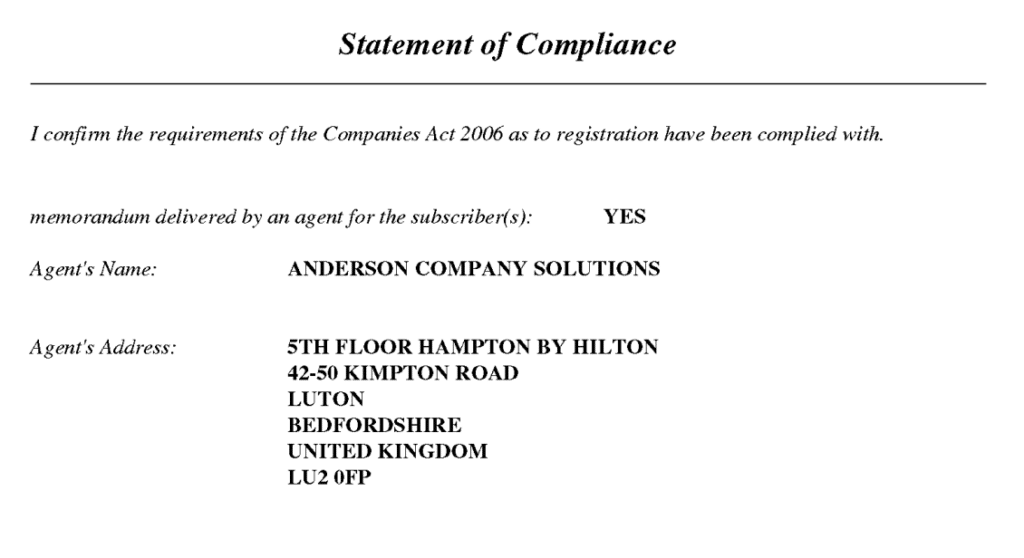

So, for example, take Labour Supply PP380 Limited. Its incorporation documents show Anderson Company Solutions Limited as agent:

Initially there was one Filipino director, Pa Dii. Then another a few days later, Keizah Estrera. Then Alona Varon was appointed as director three months later to strike it off. So it’s reasonably clear it was part of the Anderson scheme.

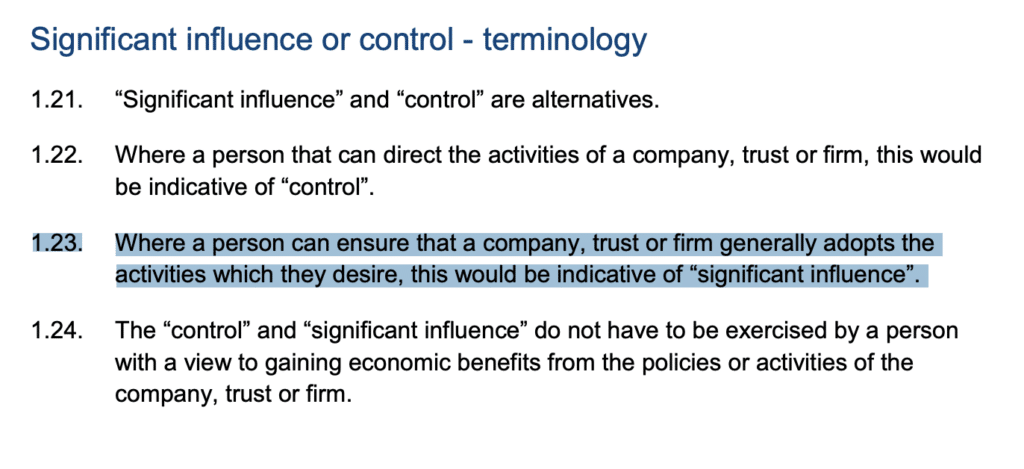

Note that the “persons with significant control” entry solely shows Pa Dii: That cannot be right given that the promoters, or whatever other people were directing the website were, at the very least, exercising “significant influence” over the company – and that required them to be registered. The statutory BEIS guidance is clear:

This was an industrial-scale breach of the PSC rules, and action can and should be taken against those responsible.

What is HMRC doing about the scheme?

HMRC is subject to very strong duties of taxpayer confidentiality, and so can’t and won’t comment on what it’s doing about the Anderson Group and Aspire. There are, however, signs that they are actively pursuing those involved, and moving to close down these schemes. There is some evidence for this:

- The director of Contrella faced serious legal consequences, and admits the scheme was fraudulent.

- We know from Companies House filings that HMRC was actively involved in the liquidation of 1,796 of the companies in June 2016, claiming that it was owed £35m – actual cash recovered was only £700k. That implies a much higher overall loss from the 10,000 companies than the £50m we have estimated.7

- Most of the other companies have been dissolved too, either by a voluntary liquidation or by a striking off, but without apparent HMRC involvement – one possibility here is that it’s just not worth the time/cost for HMRC to pursue liquidators for scraps.

- We can speculate that HMRC are involved in litigation against the promoter, Aspire Business Partnership LLP, and/or associated people and companies. Aspire stopped trading in 2018 and applied for a voluntary striking-off in 2018, which it then voluntarily withdrew. Aspire continues to file accounts with Companies House, even though it has no trade and has zero assets and zor liabilities. It’s unusual for an entity to continue to exist and file in such circumstances: one explanation is that it is a party to litigation.

- Contrella entered a voluntary insolvency process in 2016.

- A court decision in the British Virgin Islands tells us that, in March 2018, HMRC used an international treaty to require the BVI tax authorities to obtain accounts and other details from Compass Star Limited. Compass Star spent four years trying to fight HMRC in the BVI courts, and eventually lost. We don’t know what HMRC did with the information that it presumably received.

- HMRC have published unusually strongly worded guidance around mini-umbrella companies, clearly stating that they view the attempt to claim the VAT flat rate and employment allowance as tax evasion.

- The flat rate VAT rules were changed in 2017, which greatly reduced the benefit from these schemes.

- There have been large-scale HMRC efforts to de-register MUCs from VAT, and block them from the employment allowance.

- HMRC is attempting to place responsibility for hiring fraudulent MUCs on the ultimate end-users (e.g. in the case of this scheme, the construction company that engages Contrella to provide subcontractors, and ends up hiring an employee of one of the MUCs). This can be very rough justice on that company, but does create an incentive on end-users to police their supply-chains.

- Research from Pinsent Mason found that an astonishing 700% increase in the number of cases awaiting tax tribunals was significantly caused by a large number of mini-umbrella company cases.

- Recent Tax Tribunal statistics show a decline in these cases, saying that this suggests “a possible winding down of the trend started in Q2 2021/22 when Treasury and HMRC increased action against umbrella companies employing potentially fraudulent VAT schemes”,

- HMRC, HM Treasury and the Department of Business and Trade called for evidence last year on the whole of the umbrella company market. It’s now published a summary of the responses received, and a consultation document with various proposals for change. These include a variety of tax proposals, including mandating due diligence, making end-users responsible for debts of umbrella companies, and even moving the entire PAYE responsibility to the end-user.

- The same document proposes other changes to nullify the tax benefit of the fraud, such as requiring a company benefiting from the national insurance employment allowance to have a UK director. The document also hints that the VAT flat rate scheme may be abolished.

- Here’s our response to the consultation:

Part 2

Part 2 of this report will look at the KC opinion, which other KCs have described as “shocking”, “appalling”, “mind-blowing” and “deeply irresponsible”. We’ll be proposing changes to prevent such opinions being issued without consequence.

Thanks to Simon Goodley at the Guardian for the original reporting on this, and Richard Smith, Gillian Schonrock and Graham Barrow for their amazing investigative work (again noting that they draw no legal conclusions; the legal conclusions are the sole responsibility of Tax Policy Associates Ltd).

Thanks to R, P, T, C, M and B for their help with our tax analysis, to K for assistance with the confidential information and privilege elements, to Michael Gomulka for a useful discussion of the barristers’ Code of Conduct, and to A for finding the reference to umbrella schemes in recent tax tribunal data. Thanks to JK for her insight on umbrella companies

Footnotes

Not to be confused with the Anderson Group that’s active in construction, or Andersen LLP/Andersen Tax – a well-respected accounting and tax firm ↩︎

Again, not to be confused with the unrelated construction group or the unrelated tax advisory group ↩︎

You can see the text that accompanied the original YouTube video here. ↩︎

Nolan is an interesting character, who apparently worked for HMRC at one point. He was found by an appeal tribunal in 2012 to have “sought to avoid telling the truth” ↩︎

By which time the national insurance employment allowance had been increased from £3,000 to £5,000, making the schemes more lucrative ↩︎

A cursory check through the data reveals many duplications. Raquel is the director of over 300 companies. Manuel, 9. Lourdes, 8, and so on. Many of these companies carry clear signatures of being related to Anderson. ↩︎

See page 6 of this document. How can HMRC claim £35m from 1,796 companies, when we’ve estimated the total tax avoided from 10,000 companies was £50m? Very possibly our £20k/company fee estimate is too conservative, and the true figure is nearer out £180m top end estimate. Alternatively/in addition the companies didn’t account for VAT and PAYE/NI at all. Possibly HMRC is charging penalties for carelessness, wilful default and/or failure to disclose a tax avoidance scheme. Or perhaps some other factor ↩︎