Blog

-

Updated: do Brits pay more or less tax on our wages than people in other countries?

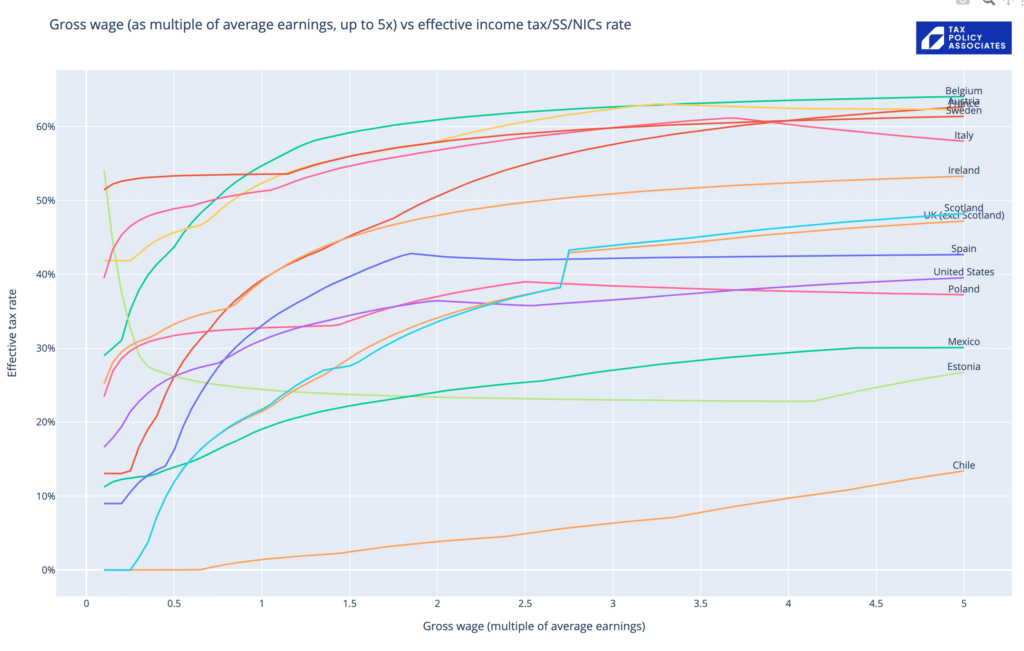

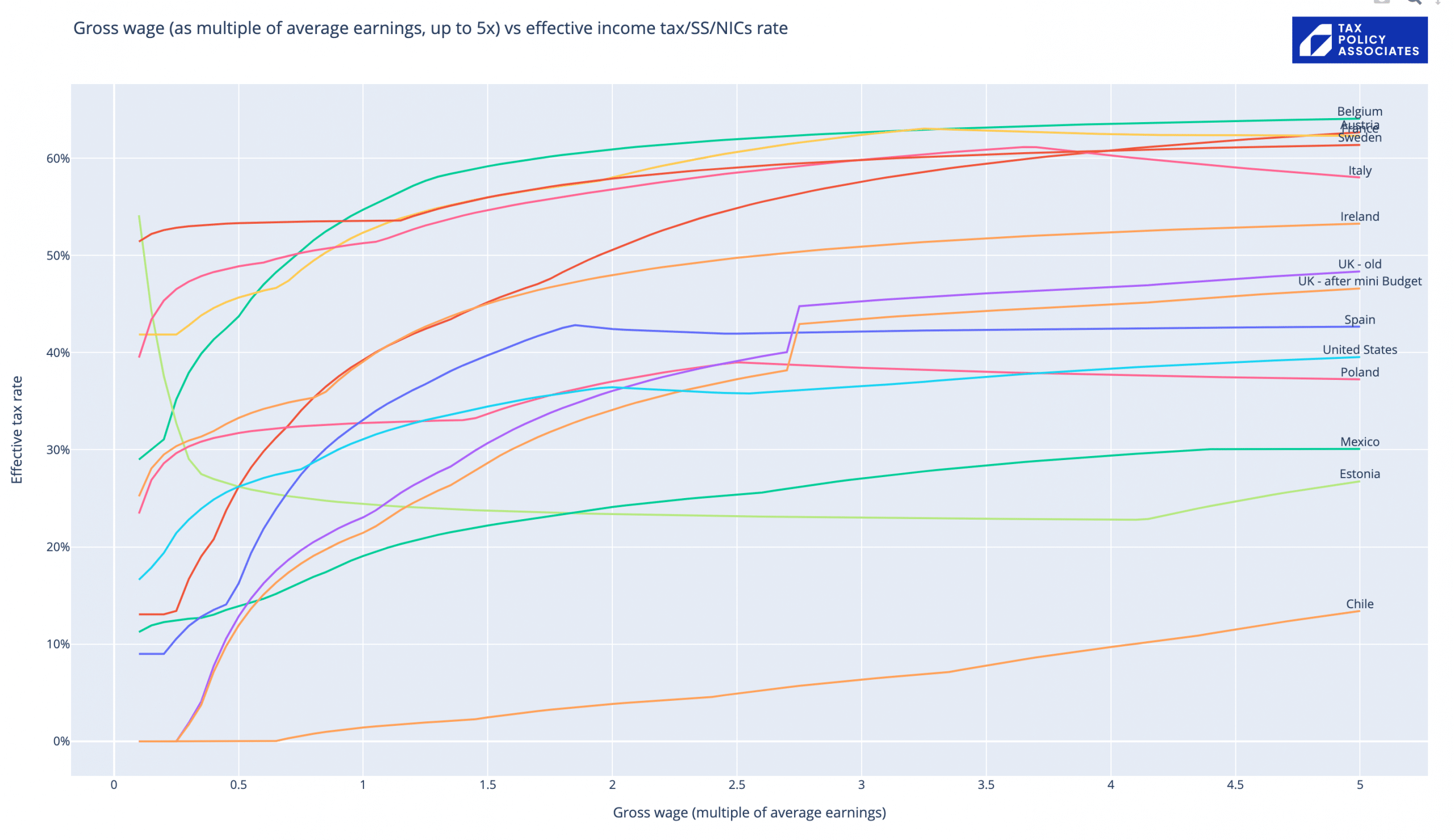

How do UK/Scottish taxes on wages compare with other countries’? It’s a simple question – but not straightforward to answer.

Looking just at rates is misleading. This chart1, for example, suggests that the top rate of UK tax is comparable with the US. That’s not really right. In the US, the top rate of Federal income tax (and, often, state income tax) kicks in at $523,600. The top UK rate – now 45% – applies from £125,140. So for most reasonably high-earning people, tax rates in the US are significantly less.

A better question is, what’s the effective tax rate – the “tax wedge” on any given amount of income?

My answer is this chart – and you can click on it for an interactive version that lets you add/remove countries:

Some immediate conclusions:

- The UK/Scotland has a much lower effective tax rate on average wages, and lower than average wages, than almost every other developed country.

- This then starts catching up quite quickly once we approach twice the average wage. And once we’re on high incomes, UK effective rates look a bit more average. Less than the expansive Continental welfare states. More than smaller countries, the US, and other countries with much less generous welfare states.

- So a good case can be made that the UK is undertaxed by international standards. That’s not something many people in the UK believe, but it doesn’t stop it being true…

Quick notes on where the data in the chart comes from:

- The chart is generated by some simple code, that takes worldwide data for tax rates and threshold (from the wonderful OECD tax database), applies it to different income levels.

- The effective tax rates include employer national insurance/social security.2 We don’t see employer wage taxes in our wage slips, but evidence suggests it is mostly borne by workers.3

- The x axis isn’t an absolute dollar amount, as realistically we can’t compare taxes on £100k in the UK with £100k in Costa Rica. Instead, the x axis is a multiple of average wages – so we are comparing tax on (e.g.) the UK average wage with tax on the Costa Rican/French/etc average wage.4

- The chart doesn’t take account of tax reliefs/deductions – these are generally quite limited in Europe, but very generous in the US… so again the chart overstates the actual tax Americans pay.

- The data is now updated for the 2023/24 UK and Scottish rates, but other countries are not updated (I have no good source for the data). Given the wider economic circumstances, it’s plausible that taxes will be going up worldwide, and so this chart may make the UK/Scotland rates look relatively higher than they actually are.

- See my previous post for more detail on the methodology and a complete list of caveats and limitations.

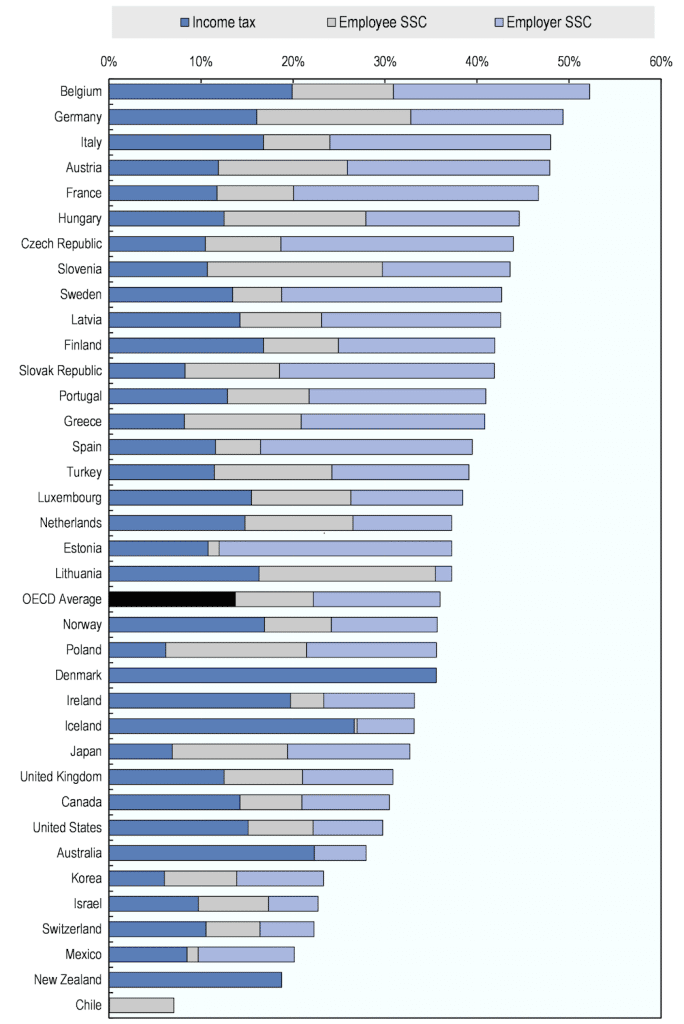

And if you don’t want to believe my chart, here’s the OECD’s own chart showing the effective rate of tax on average incomes:5

I continue to think that, if we want a Scandinavian level of public services, then most people have to pay similar levels of tax to most people in Scandinavia. Sorry about that.

Photo by Javier Miranda on Unsplash

Footnotes

This combines income tax and employee national insurance/social security, and for countries (like the US) where there are state taxes as well as national taxes, it adds in the average state tax. ↩︎

But not the apprenticeship levy because it’s kinda sorta hypothecated… you could definitely make a case it should be included ↩︎

i.e. because the employer has an amount they’re willing/able to pay as wages, and employer NICs come out of that). ↩︎

But the UK and Scottish figures just use the UK average wage, because my feeling is that this is the comparison people are interested in ↩︎

-

A legal analysis: did Douglas Barrowman commit a criminal offence?

9 June 2023 update: the Companies House entries still fail to disclose Douglas Barrowman as the ultimate beneficial owner. PPE Medro was updated on 11 May to show Arthur John Lancaster as the owner of the company. Lancaster is a trust accountant/tax adviser for Barrowman’s group – it is unlikely he actually controls the companies himself. 1 The PSC entry for LFI Diagnostics Limited is unchanged.

Given the failure to correct the entries, it is now hard to see how this can be an innocent mistake. Companies House should be seriously considering a prosecution of the directors.

UPDATE 13 August 2023: this has been overtaken by new evidence. See our new report here.

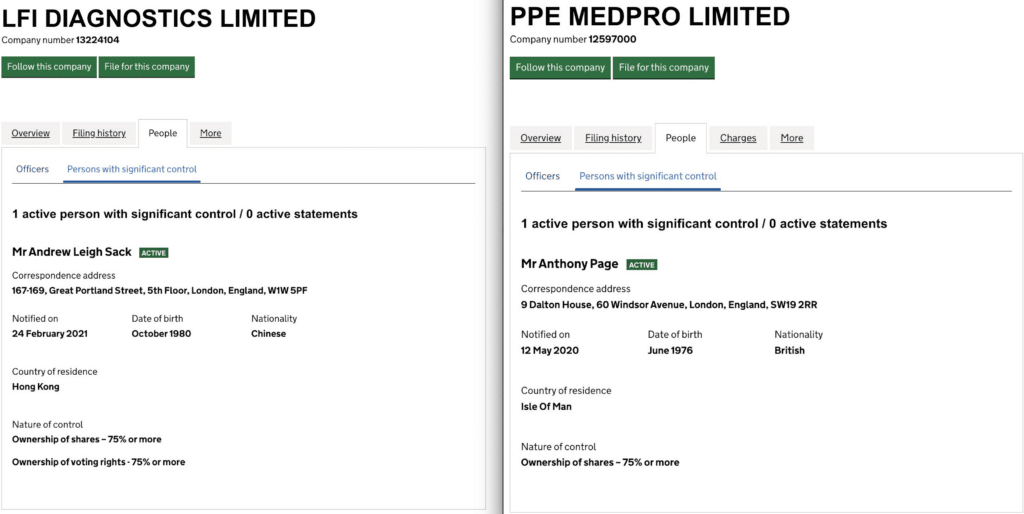

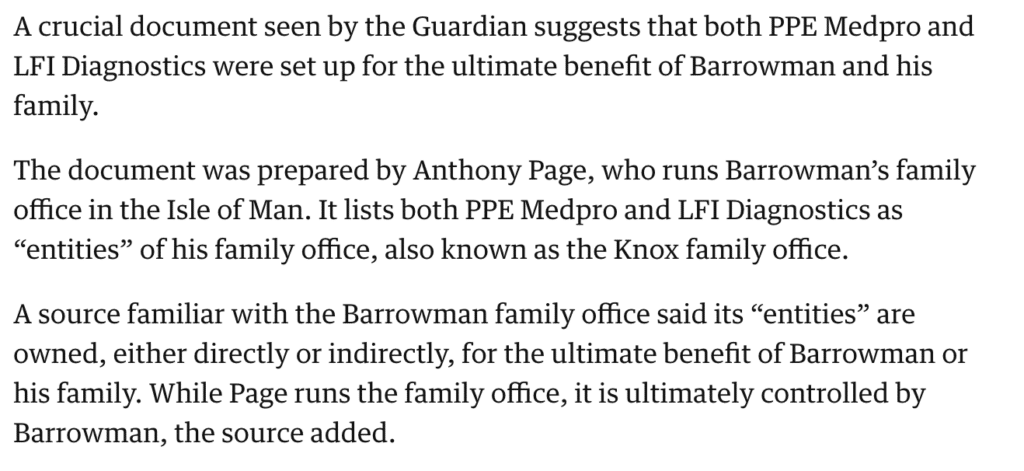

The Guardian recently reported that two UK companies ultimately controlled by businessman Douglas Barrowman were the subject of PPE contract lobbying by his wife. I’ve no expertise or interest in the PPE lobbying issue. But I am interested2 in the fact that, while the Guardian says Barrowman controls the companies, their Companies House entries3 say no such thing:

I’m fairly sure these are the right companies4. So my immediate view is that either the Guardian was wrong, or the Companies Act rules requiring registration of “persons with significant control” were broken. I haven’t seen the document on which the Guardian relies, and I can’t know for sure if their story is correct but, given the stupidity of English libel law, and the willingness of Barrowman to use it, I expect the Guardian was very careful.

What are the “persons with significant control” rules?

Back in the day, Companies House showed who the shareholders of a company were, but stopped there. So if, for example, a company was owned by a tax haven holding company, you wouldn’t be able to ever find out who the ultimate shareholder was.

This all changed in 2016 – rules were put in place requiring companies to identify their “persons with significant control” – meaning the actual humans who were able to tell the company what to do.5 Normally this would be the ultimate shareholder – but sometimes there would be someone who wasn’t a shareholder, but who nevertheless could ensure that the company always adopted the activities they desired. They too would be a “person with significant control”.

So, let’s say I’m a secretive oligarch. I set up a UK company with some local directors. The shares in the company are held by a Panamanian company, and that in turn is held by my personal chef, who I throw money at and therefore always does what I ask. Pre-2016, your Companies House search stopped dead in Panama. But today, the company should register me (not the Panamanian company, and not my chef) as the “person with significant control”.

And that’s the whole point of the rules – to enhance corporate transparency and help stop the abuse of companies for nefarious purposes.

If the Guardian report is accurate, who is the “person with significant control” of the two companies?

The definition of a “person with significant control” is set out in Schedule 1A of the Companies Act. In our case, the relevant section is paragraph 5: where a person (not necessarily a shareholder) has a right to exercise, or actually exercises, significant influence or control over a company.

This passage in the Guardian article is key:

If indeed the companies are “ultimately controlled” by Barrowman then he has “significant influence or control” and is therefore the “person with significant control”, regardless of whether he holds any shares.67

What should have happened?

A company is required to identify and then register its “persons with significant control”.

Section 790D of the Companies Act requires a company to take reasonable steps to find out who controls it.

For a small part of a big international corporate group that might be hard on the poor UK directors, and so there are procedures for the directors to essentially send out begging letters to its immediate shareholders to find out who controls them. But in the PPE Medpro case there are no such complexities – the sole director is Anthony Page, who helps run Barrowman’s private office.

So if Barrowman really controls PPE Medpro, it would be surprising (but I suppose not impossible) if Page didn’t know that.

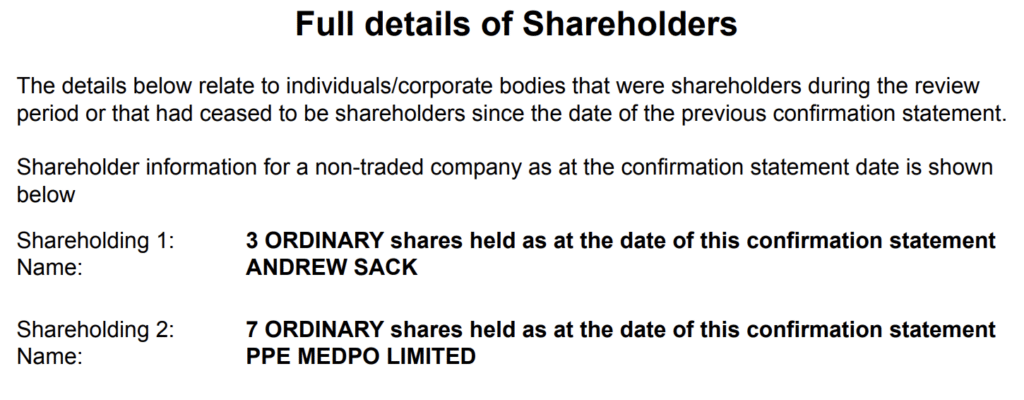

Since we know nothing about the LFI Diagnostics directors, Andrew Sack and Chan Chen, we can’t say anything about the likelihood they knew about Barrowman’s involvement – but surely they knew that they were not the actual controllers? Andrew Sack wasn’t even the majority shareholder:

There are similar problems with other Barrowman UK companies. Just looking up companies where Page is a director we see Neo Space (Douglas) Limited, PPE Medical Protection Limited, Neo Space Aberdeen Limited, and a few more. All of them list Page (and sometimes other directors) as the “persons with significant control”. It seems most unlikely this is correct.

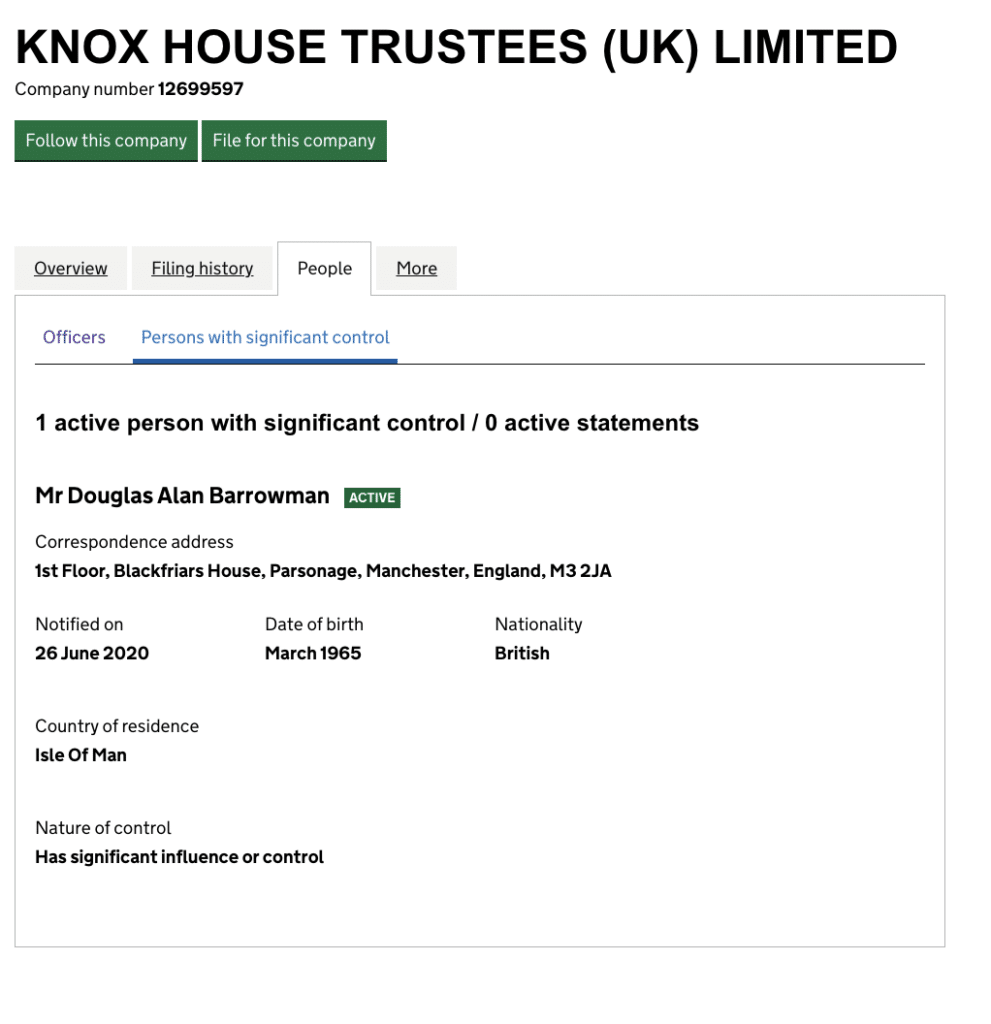

There’s just one exception I can find, Knox House Trustees Limited, which correctly discloses Barrowman as the “person with significant control”:

Why are they getting this wrong?

I don’t know. It could be incompetence. It could be obsessive secrecy. It could be related to some kind of tax planning, perhaps linked to arguments that the groups are not in fact under common control (Barrowman’s group has a history of shady tax behaviour).

Does it matter?

The ownership disclosure rules are there for a reason: so that it’s easy to see who really controls a company. In this case the failure to comply could have had serious consequences, if it meant that civil servants assessing a PPE bid were unaware of the connection between the bidding companies and Barrowman, and hence the link to Mone. I’ve no idea if that happened – but it’s the potential for this to happen (whether in this scenario or a different one) which is why the rules are there.

What are the criminal offences applicable to directors?

There’s a specific offence for breach of section 790D, committed by the company itself, and every director responsible. On conviction, the director faces up to two years in jail and an unlimited fine.

And there’s a general Companies Act offence of knowingly or recklessly delivering a false statement or document to Companies House. Again, up to two years in jail and an unlimited fine.

So if Barrowman controls the companies, and Page knew (but didn’t register) then in principle he should be very worried.

And Sack and Chen clearly got this wrong – how could Sack, a minority shareholder, have thought he controlled the company? But perhaps the prospect of a prosecution doesn’t bother them, given they’re based in Hong Kong.

What are the criminal offences applicable to Barrowman?

There’s a specific requirement that, where someone knows they control a company, but they haven’t received a notice from the company requiring them to provide information, then they have to tell the company that they do in fact control it. And if they don’t do this, then they commit an offence – again, with up to two years’ imprisonment, and an unlimited fine.

What does this mean for Barrowman?

It all means that, in my opinion, Barrowman may have committed a criminal offence if:

- The Guardian summary of the internal “crucial” document is correct, and the Guardian’s source is correct that Barrowman “ultimately controls” the private office.8

- The correct legal analysis is that Barrowman actually exercised “significant influence or control” over either or both companies (which, if the Guardian summary and source are correct, will likely be the case).

- Barrowman knew, or ought reasonably to have known, that he should have been registered as a “person with significant control”.

- The companies never sent him a formal notice asking for him to confirm control.

- He never notified the companies of his status as a “registrable person”.

Points 1, 4 and 5 are straightforwardly factual. 2 is legal, but doesn’t seem too challenging.

The most difficult point for a prosecution, and the most obvious “out” for Barrowman, is 3. Barrowman could say he had no idea the company was incorporated. Or that he didn’t know the rules worked this way, and it’s not reasonable to say he ought to have known.

Pleading ignorance as to the existence of the company may be challenging given the significance of the contracts the companies were reportedly involved with – but whether such a defence could be sustained turns on the facts and, in particular, what kind of paper-trail would emerge, and how credible people are on the witness stand.

The “I couldn’t be expected to know the rules worked this way” defence would be successful in many cases, and is one of the reasons why prosecutions of these offences are so hard. The difficulty Barrowman has is that he’s a highly sophisticated businessman, who runs a group of companies that provide technical tax and legal services to private offices – in fact he is, in my view, exactly the sort of person who ought reasonably to know that the rules work this way. So this would plausibly be a harder defence for him than for the average businessman.

If breaching these rules is a criminal offence, why do people do it?

Because they think they won’t be prosecuted, and historically that’s been a very safe bet. So there is widespread failure to comply with the law.

Part of the answer is a high profile prosecution or two.

But another important part is to have effective civil penalties, which don’t require the expense and uncertainty of a criminal trial, and which deter shareholders, directors, corporate services providers, and advisers from participating in filing false information. I’ll be writing more about that soon.

Footnotes

It is relevant to note that Lancaster was heavily criticised by a tax tribunal, in the context of one of Barrowman’s avoidance schemes, for providing evidence that was “seriously misleading”. ↩︎

Disclosure: I am an experienced commercial lawyer, but I am not a company law expert. However, I know many people who are; this article reflects my reading of the legislation, informed by their experience and expertise. Any errors, however, are solely mine ↩︎

PPE Medpro is easy; Anthony Page is definitely the right person. LFI Diagnostics is slightly more difficult; I’ve no idea who Andrew Sack and the other director, Chan Chen, are, but Companies House shows it as majority owned by “PPE Medpo Limited”, and the incorporation date lines up with the Guardian article. So, absent an amazing coincidence, this is the right company too ↩︎

The legislation starts here, and is fairly easy to read – there’s also useful (statutory) guidance ↩︎

Although LFI Diagnostics Limited may be majority held by PPE Medpro Limited (its name is shown as “PPE Medpo Limited” in the LFI confirmation statement; that could be a different company but I’m guessing is a simple typo). If that’s correct, then the correct approach should be for LFI Diagnostics Limited to report that it’s held by PPE Medpro Limited, as the “relevant legal entity”. The reason is that we can then look at the disclosure for PPE Medpro Limited and see who the ultimate owner is – but of course we can’t, because that is wrongly reported ↩︎

There can be more than one “person with significant control” – so, for example, it could be that Page and Barrowman both fall in this category. ↩︎

It would be a very strange private office if he didn’t ultimately control it ↩︎

-

Nadhim Zahawi’s lawyers referred to regulator for abusing libel law to shut down debate

I reported in July that Nadhim Zahawi, then Chancellor of the Exchequer, had founded YouGov using a tax avoidance structure. Zahawi provided an explanation which my detailed analysis showed to be false. Zahawi then shifted immediately onto a different explanation. In my opinion this showed that his first explanation was a lie – and I said so.

Zahawi had a media profile and resources dwarfing a small tax think tank – but instead of using these to explain himself, he instructed Osborne Clarke to write to me demanding that I retract. And their letter claimed that I could not publish the letter, or even tell anyone I’d received it. It was an attempt to silence criticism which had no basis in law, and for which Zahawi and his lawyers should be ashamed.

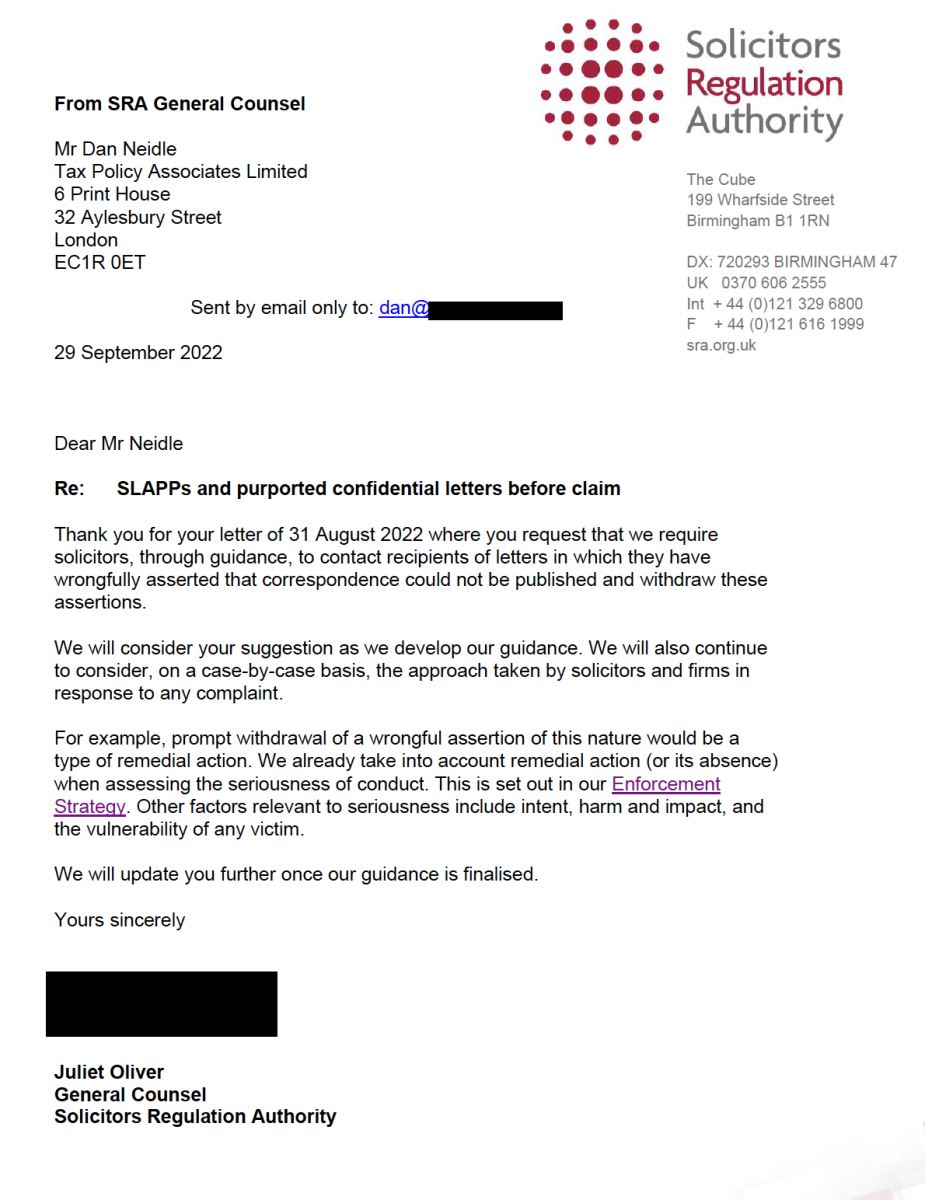

The Solicitors Regulation Authority this week issued a “warning notice” making clear that this kind of behaviour is unacceptable. I have therefore referred Zahawi’s lawyers, Osborne Clarke, to the regulator.

I’m also asking the SRA to investigate Osborne Clarke more widely. In the end, their actions cost me some legal fees but otherwise failed. But I know there are many others, without my legal background, contacts or financial resources, who have received letters like this (on behalf of Zahawi and others) and been silenced. If the SRA find that people have been silenced by deception and intimidation, then this needs to be put right.

I’ve copied below the text of my letter, with links to the referenced documents. If you prefer a PDF, that is here (but without links).

And more on Mr Zahawi coming soon…

SRA General Counsel

The Cube

199 Wharfside Street

Birmingham B1 1RN

1 December 2022

Sent by email

Dear Ms Oliver

Osborne Clarke – SLAPP – breach of SRA Principles

1. Many thanks for your publication on 28 November 2022 of the new warning notice on SLAPPs. In light of that notice, I wish to make a formal referral to you of Osborne Clarke for several significant breaches of SRA Principles. I believe you will be already aware of a number of the breaches, but you may not be aware of others.

The background

2. I retired from commercial practice in May 2022, and founded Tax Policy Associates; a think tank which works to improve both tax policy and the public understanding of tax. In July 2022, I wrote several articles and social media posts about Nadhim Zahawi. At that time, Mr Zahawi was the Chancellor of the Exchequer.

3. The essence of my writings was that, when Mr Zahawi founded YouGov in 2000, the founder shares (which ordinarily would have been issued to Mr Zahawi) were instead issued to a Gibraltar company, Balshore Investments Limited. I said this looked like tax avoidance. Mr Zahawi’s team responded by briefing several journalists that the reason for Balshore receiving the shares (which I will call the “first explanation”) was that Mr Zahawi’s father, who owned Balshore, had contributed startup capital to YouGov.

4. I investigated the accounts and Companies House filings and found that the startup capital was contributed by another investor, Neil Copp. Balshore had contributed only a token amount (£7,215). I therefore wrote that either I was mistaken, the filings were wrong, or Mr Zahawi was lying. The key Twitter thread can be found at https://taxpolicy.org.uk/evidence (attached in PDF format as tweet1.pdf).

5. Immediately after this, Mr Zahawi’s team started briefing a different explanation (which I will call the “second explanation”): that Mr Zahawi’s father received the shares in recognition of the significant advice and assistance he had provided to the business. The fact that Mr Zahawi was no longer defending his first explanation suggested to me that I had not made a mistake; in my opinion it suggested that the first explanation had been a lie. I said so. I did not say that the second explanation (“advice and assistance”) was a lie (although it seemed highly implausible). The key Twitter thread can be found at https://taxpolicy.org.uk/lying (attached as tweet2.pdf).

6. On Saturday 16 July 2022, I received an unsolicited direct message on Twitter from Ashley Hurst, a partner at Osborne Clarke (see attachment SRA1). Mr Hurst sought to speak to me on a without prejudice basis. I responded that he should put what he had to say in writing, and that I did not accept without prejudice correspondence.

7. Later that day I received an email from Mr Hurst (see attachment SRA2) asking me to retract my accusation by the end of that day, or I would receive an open letter on Monday.

8. I did not retract. On Tuesday 19 July I received a letter from Mr Hurst (see attachment SRA3).

Breaches of SRA Principles

9. The Osborne Clarke correspondence bears several of the hallmarks of strategic lawsuits against public participation (SLAPPs) which are identified in your warning notice.

Labelling

10. The email (SRA2) is marked “confidential and without prejudice”. It says:

“I have marked this email without prejudice because it is a confidential and genuine attempt to resolve a dispute with you before further damage is caused. Our client wants to give you the opportunity to retract your allegation of lies in relation to our client.

That would not of course stop you from raising questions based on facts as you see them.

You have said that you will “not accept” without prejudice correspondence. It is up to you whether you respond to this email but you are not entitled to publish it or refer to it other than for the purposes of seeking legal advice. That would be a serious matter as you know. We recommend that you seek advice from libel lawyer if you have not done already.”

11. However, the letter cannot possibly be “without prejudice”, for three (independent) reasons. First, I had specifically told Osborne Clarke I would not accept “without prejudice” correspondence. Second, even if I hadn’t done so, their email was not a genuine attempt to resolve an existing dispute – it offered no concessions, and was therefore not an attempt at settlement. Third, there was no dispute – as became subsequently clear, Mr Zahawi never had any intention of instigating a claim.

12. The claims that the email SRA2 and subsequent letter SRA3 were confidential were equally false. The content of the email and letter lacked the quality of confidence (as all the information in the documents was already public or obvious). There was nothing in our relationship which suggested that a duty of confidence could be imputed to me – the letter was unsolicited. Even if the letter had contained confidential information, there was a clear public interest in the matters under discussion (which would override the duty of confidence).

13. Hence the claims that the email was “without prejudice” and the email and letter were “confidential” were without merit, an attempt to mislead, and a breach of the SRA Principles.

Aggressive and intimidating threats

14. The email asserts that the “without prejudice” rule prevents me from publishing or even referring to the letter. This is entirely false. It is often tactically unwise for a party to publish without prejudice correspondence, but the “without prejudice” rule is a rule of evidence and does not prevent publication. This was, again, false, and an attempt to mislead. However, it is more serious than that: it is an aggressive and intimidating threat (“That would be a serious matter as you know.”).

15. The second Osborne Clarke communication, SRA3, also seeks to intimidate me into not publishing the letter. It asserts that doing so would be “improper” (paragraph 1.3) but does not give a legal rationale for this claim – most likely because there is no such rationale.

Advancing meritless claims – false allegations

16. As you identify in your warning notice, a common characteristic of SLAPP pre-action correspondence is that it advances meritless legal claims.

17. The entirety of the first Osborne Clarke email (SRA2) is meritless. The central allegation is:

“You have relied on comments attributed to YouGov by The Times today to support your view that our client was lying about the extent of involvement of our client’s father in the very early days of YouGov when it was set up in 2000.”

18. This misrepresents the comments I had made. I had specifically alleged that Mr Zahawi lied when he claimed that his father provided startup capital to YouGov (his first explanation). I did not allege that Mr Zahawi’s subsequent explanation was a lie (the second explanation – that Balshore Investments acquired its shareholding because Mr Zahawi’s father was so involved in the running of the business).

19. It is hard to imagine a more meritless defamation action than complaining about an allegation that was not in fact made.

20. The Osborne Clarke email (SRA2) at no point attempts to respond to my actual allegation. The closest it comes is by saying I omitted to reference that Mr Zahawi’s father paid £7,000 for his second tranche of shares. But I clearly did mention this, in both my Twitter thread (https://taxpolicy.org.uk/evidence) and my longer article (https://taxpolicy.org.uk/zahawi-capital/). The lack of attention Osborne Clarke paid to the facts evidences recklessness and/or a lack of interest in the merits of the case, both of which are identified in the SRA “conduct in disputes” guidance as unacceptable behaviour.

Advancing meritless claims – no legal basis

21. Your risk warning specifically mentions cases where a solicitor pursues a claim despite knowing that a legal defence to their claim will be successful.

22. At the time, Nadhim Zahawi was Chancellor of the Exchequer. It is hard to imagine a topic of higher public interest than an accusation that the Chancellor of the Exchequer had avoided tax and lied about it. Hence Osborne Clarke would have known that a public interest defence under section 4 of the Defamation Act 2013 would likely have been successful. It is notable that their communications do not mention the public interest defence.

Advancing false factual claims

23. Another common element of SLAPP pre-action letters is for the solicitor to advance factual claims by their client which are false, and which the solicitor should know are likely false. As your guidance notes, solicitors should take reasonable steps to satisfy themselves that a claim is properly arguable before putting it forward.

24. In this instance, both Osborne Clarke communications (SRA2 and SRA3) assert that Balshore provided £7,000 of startup capital for the YouGov shares it acquired in 2000. See, for example, paragraph 2.4 of SRA3.

25. However, the Companies House form for the share issuance shows that it was signed in October 2002, but backdated to 2000 (see attachment SRA8). My review of YouGov’s accounts and other Companies House filings confirm that the £7,000 was paid in 2002, not 2000 (I can supply evidence of this if that would be helpful).

26. Hence the key factual component of the Osborne Clarke letters was false. Osborne Clarke cannot have made any attempt to verify the matter (given that a cursory review of the Companies House form would have immediately revealed the backdating).

27. There is no duty on a solicitor to conduct detailed due diligence to fully investigate a client’s factual assertions. However, where the solicitor is going to assert factual matters in a letter to a third party, as a central part of a threatened claim against the third party, the solicitor should have some proper basis for doing so. The solicitor’s duty to the third party and the rule of law mean that the solicitor cannot simply advance any factual assertion made by his or her client, without the slightest investigation. A solicitor is not a mere post-box, particularly when serious allegations of defamation are being made. The failure of Osborne Clarke to make any checks on the claim was reckless and a breach of the SRA Principles.

28. The breach subsequently became more serious. I drew Osborne Clarke’s attention to the falsehood of the £7,000 claim, but (now knowing it was likely false) they did not correct the record. At that point Osborne Clarke became complicit in misleading me. I discuss this further below.

No intention of actually commencing litigation

29. A further common characteristic of SLAPPs (mentioned in your guidance) is where a solicitor is acting in a public relations capacity, with a legal veneer but no actual legal content. One example of this is where a solicitor makes a threat of a defamation lawsuit which is a “bluff”. The solicitor and client have no intention of filing an actual defamation claim, either because the client’s case is too weak (for example because the honest opinion or public interest defences will apply), or because the claimant would not want to run the risk of pre-trial disclosure or cross-examination during trial. The solicitor therefore engages in purported pre-action correspondence with the aim of intimidating the recipient into withdrawing their accusation. This is abusive behaviour, damaging to the rule of law. When combined with mislabelling, the overall effect is that people are silenced, with no way for the public or the judicial system to ever know about it.

30. It will often be hard to judge whether a solicitor’s correspondence falls within this category. This, however, is an unusual case where we can be confident that it does. The key sentence in Osborne Clarke’s email (SRA2) reads:

“Should you not retract your allegation of lies today, we will write to you more fully on an open basis on Monday.”

31. The natural reading of this is that, if I did not retract, Osborne Clarke would send me a pre-action letter, with a view to subsequently commencing defamation proceedings. However when I did not retract, I did not receive a pre-action letter. Osborne Clarke’s subsequent letter (SRA3) is explicit that it is “not a threat to sue for libel”. And when I still did not retract, I received no further correspondence (and no libel claim has been forthcoming).

32. Hence, the evidence suggests that Osborne Clarke was bluffing: this was pre-action correspondence as an end itself – a SLAPP, and a breach of the SRA Principles. It was, perhaps, not pre-action correspondence at all – but Osborne Clarke acting in a “reputation management”/“public relations” capacity of the kind that your 28 November warning identifies.

33. It may be that, if you review Osborne Clarke’s files, you will find that Mr Zahawi had told Osborne Clarke he had no intention of commencing proceedings.

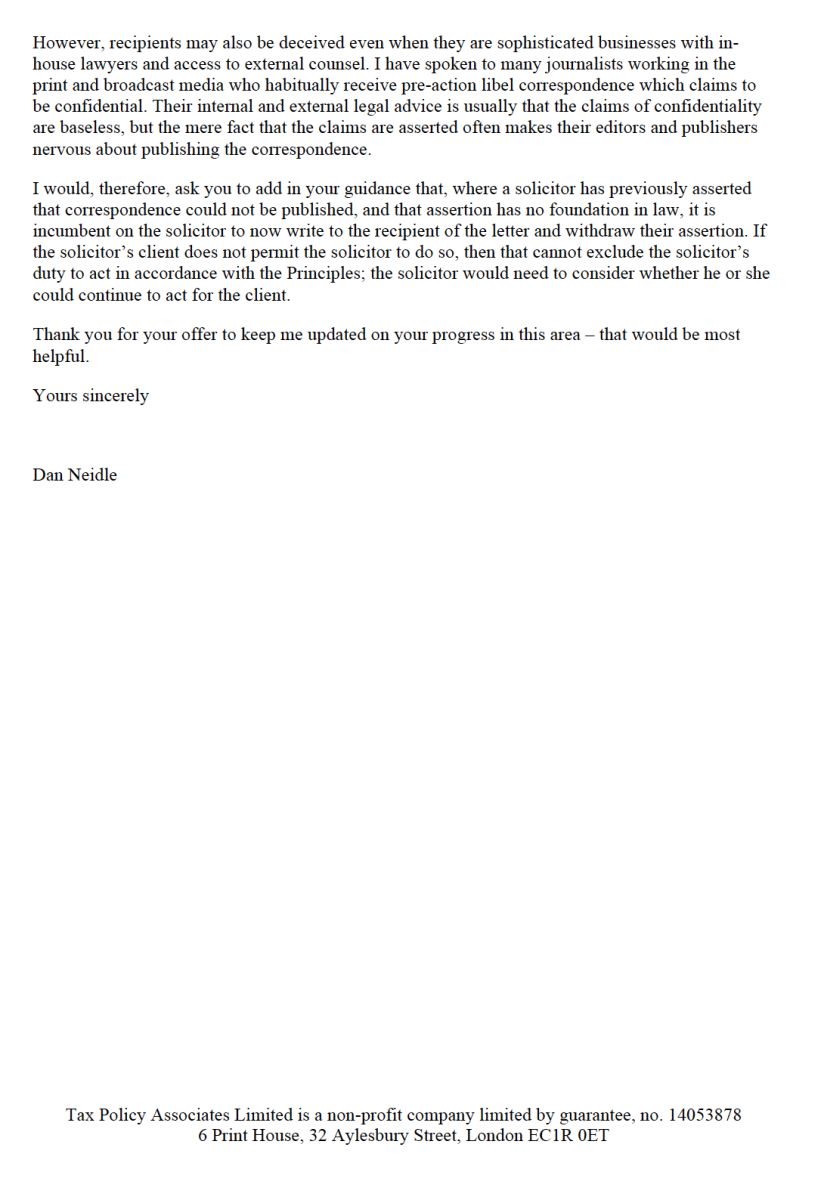

Reason for writing

34. I had not intended to make a formal complaint about Osborne Clarke. However, their behaviour since I called their “bluff” has evidenced a serious misunderstanding of a solicitor’s professional duties and obligations:

35. I wrote to Osborne Clarke on 19 August 2022 (attachment SRA4) alerting them to the fact that their central claim about the £7,000 was false, and inviting them to correct the record.

36. Their response on 25 August 2022 did not address the point (attachment SRA5).

37. I responded on 31 August 2022 (attachment SRA6) making clear that I expected Osborne Clarke to address the three falsehoods in their correspondence: the false claim Balshore had provided £7,000 of capital, the false claim of confidentiality, and the false claim that the “without prejudice” rule prevented publication. I invited them to justify or withdraw their claims, and pointed out that it was not open to a solicitor to make a false statement and, knowing it was likely false, fail to correct it. Whilst Osborne Clarke may originally have made a mistake, or been reckless, in presenting the false £7,000 claim, at the point they realised it was likely false, and failed to correct the record, they became complicit in misleading me.

38. Osborne Clarke responded on 8 September (attachment SRA7). On my first point (the £7,000 of capital), Osborne Clarke simply said that their professional conduct rules prohibit them from discussing client confidential matters. This is a non-sequitur. If the solicitor becomes aware that he or she has (intentionally or unintentionally) misled a third party then the solicitor must correct the record – otherwise the failure to correct is itself a breach of the SRA Principles. Client confidentiality will in most cases not prevent such a correction (the duty of confidence will not apply if the solicitor is being asked to perpetrate a falsehood). But if there is a conflict then client confidentiality does not simply override other SRA Principles; the solicitor is then faced with a serious ethical dilemma which the solicitor may only be able to resolve by ceasing to act for the client. Osborne’s Clarke’s response was unacceptable.

39. On my second point (the false assertions of confidentiality and without prejudice), Osborne Clarke said that they would address their responses to the SRA. Again, this is a non-sequitur. A solicitor’s duty not to mislead a third party is not owed to the SRA; it is owed to the third party.

40. I had hoped Osborne Clarke would correct the record of their own accord, and I would not need to refer the matter to you. Unfortunately, it is clear they will not do so – it is for that reason I have written this letter.

Wider implications

41. It is my understanding that the key features of Osborne Clarke’s correspondence are commonplace: false assertions of confidentiality and “without prejudice”; an attempt to intimidate the recipient into not publishing the letter; basing a libel threat on a client’s assertion of facts without any attempt to very if those facts are correct.

42. I would, therefore, ask you to review other defamation matters where Osborne Clarke was instructed, to ascertain if they have indeed breached the SRA Principles on other occasions (it may be that this is already underway as part of your thematic review into SLAPP).

43. You will appreciate that I was a very atypical recipient: as a former partner in a large law firm I had the legal knowledge to identify that the claims being made were false, the contacts to obtain expert advice, and the financial resources to pay for that advice. Osborne Clarke’s actions caused me to incur unnecessary legal fees, but had no other adverse consequences and I was not, in the end, silenced.

44. I expect many other recipients of these letters did not have those advantages, and were silenced by meritless claims of confidentiality. The damage to the profession and the rule of law can only be undone if these letters can be identified, and Osborne Clarke and/or the SRA then writes to the recipients making clear that the confidentiality assertions were false. Whether Osborne Clarke’s client permits them to do so is irrelevant: a solicitor’s public interest obligations override their duty to their client.

45. If there is indeed a pattern of behaviour of Osborne Clarke falsely labelling as confidential/without prejudice letters to unrepresented parties, making meritless claims, and making false assertions of facts, then I would ask that you bring Solicitors Disciplinary Tribunal proceedings against Osborne Clarke, and seek the most serious sanctions against those involved.

46. Do please let me know if I can be of any further assistance. I would ask that you contact me by email rather than by post.

Yours sincerely

Dan Neidle

Photo of Nadhim Zahawi by Richard Townsend

-

The SRA stops secret libel letters

The SRA has warned solicitors to stop sending libel letters which falsely claim to be confidential, and mustn’t be published. This should dramatically change the landscape for everyone from large newspapers to individual tweeters and bloggers. It’s now up to us to take advantage of it.

Back in July, the Chancellor of the Exchequer instructed lawyers to write to me, accusing me of libel and requiring me to withdraw my allegation that he had lied. They claimed their letters were confidential, and warned me of “serious consequences” if I published them. This was tosh. I did not retract, and I published the letters.

I don’t think of myself as particularly naive, but was shocked to discover that fibbing about the confidentiality of libel threats is standard practice in the libel world. It has a chilling effect on free speech in this country – the rich and powerful can silence their critics so completely that we don’t even know they’ve been silenced. It’s a hallmark of SLAPPs – “Strategic Lawsuits Against Public Participation” – which have become distressingly common.

It may come as a surprise to many people, but solicitors are not allowed to tell fibs. The Solicitors Regulation Authority requires solicitors to behave in accordance with the SRA Principles: to act with honesty, integrity, independence, and to uphold the rule of law. Intimidating people into not publishing letters they are perfectly entitled to publish is the very opposite of these Principles.

So I wrote to the Solicitors’ Regulation Authority, asking them to end the practice of solicitors making phoney claims of confidentiality in libel letters. The SRA sent me a promising initial response. At the same time, the Anti-SLAPP Coalition have been pushing for both strong SRA guidance and a change in law – so I am playing a small part in a much wider campaign1

Yesterday the SRA published their final guidance on SLAPPs – and it could not be clearer. Lawyers cannot attempt to prevent the publication of their libel letters by claiming the letters are “confidential” or “without prejudice” without very good reason.

Here’s the key section:

We expect you to ensure that you do not mislead recipients of your correspondence, and to take particular care in this regard where that recipient may be vulnerable or unrepresented.

One way this can happen in this context is by labelling or marking correspondence ‘not for publication’, ‘strictly private and confidential’ and/or ‘without prejudice’ when the conditions for using those terms are not fulfilled.

We accept that marking a letter with such terms might be necessary if (for instance) an individual needs to disclose private and confidential information in order to disprove facts intended for publication [Dan note: these cases are rare – there was a reason my example involved a rampaging rhinoceros]. If so, it might also serve a purpose in ensuring correspondence is not read by an unintended recipient and/or to inform the recipient that they cannot rely on the defence of consent if they choose to publish any of the relevant material. Recipients might also properly be warned as to the legal risks of publication of such correspondence (which may include aggravation of any damages payable).

However, you should carefully consider what proper reasons you have for labelling correspondence in these ways, and whether further explanation is required where the recipient might be vulnerable or uninformed. Such markings cannot unilaterally impose a duty of privacy or confidentiality where one does not already exist. Clients should be advised of this and warned of the risks that a recipient might properly publish correspondence which is not subject to a pre-existing duty of confidence or privacy.

…

Equally, correspondence should not be marked as ‘without prejudice’ if that correspondence does not fulfil the conditions for that label. You should consider whether the communication represents a genuine attempt to compromise an existing dispute. There should ordinarily be no need to apply it to correspondence which does not offer any concessions and only argues your case and seeks concessions from the other side.

Now compare this with what I received from Zahawi’s lawyers, Osborne Clarke:

“It is up to you whether you respond to this email but you are not entitled to publish it or refer to it other than for the purposes of seeking legal advice. That would be a serious matter as you know.”

And then:

“You have said that you will not accept without prejudice correspondence and therefore we are writing to you on an open, but confidential basis. If your request for open correspondence is motivated by a desire to publish whatever you receive then that would be improper. Please note that this letter is headed as both private and confidential and not for publication. We therefore request that you do not make the letter, the fact of the letter or its contents public.”

I have given Osborne Clarke several opportunities to retract these false claims, and they have declined. I will therefore be writing to the SRA to make a formal complaint. I would urge everybody who’s received a libel letter falsely labelled as confidential/without prejudice to take similar action. This is whether you received the libel letter this morning or ten years’ ago, and whether you’re the Financial Times or a Twitter account with 20 followers2. And what action should someone in this position take, particularly if they don’t have access to legal advice? There’s very good news on that front coming soon – I’ll be writing on this in the next few days.

The point isn’t to be vindictive, it’s to change the whole risk/reward calculation for libel lawyers and their clients. Once the wealthy and powerful know they can’t stop a libel threat being published, and there’s a high risk it will receive more publicity than the original accusation, then suddenly the whole idea of sending it becomes less appealing.

If you want to threaten someone with libel: fine3. But you’ll have to face the consequences of everyone knowing what you’re up to.

But this only works if we – the recipients of these letters – act. And that’s about to become a whole lot easier. More to follow!

Photo from the Anti-SLAPP Coalition conference on 28 November 2022, where I was kindly invited to speak on a panel.

Footnotes

And also important to thank everyone who has personally helped me – tax accountants, lawyers, QCs, academics, experts on confidentiality and privilege etc etc – a huge amount of generosity from a large number of people, most of whom I cannot name, but all of whom I’m immensely grateful to. ↩︎

This is not a theoretical example; after my experience, I was inundated with messages from people with small blogs and Twitter followings who had been at the receiving end of SLAPP letters ↩︎

Actually not fine; I tend to think libel law should only apply to the most serious of deliberate lies ↩︎

-

Autumn Statement proposals: ten good, three bad, three meh

If some idiot was to make me Chancellor, I’d do something like this, none of which are likely to actually happen:

- Announce that, when fuel prices return to normal, there will be a retrospective windfall tax on the energy sector raising a target £30bn. But absolutely don’t announce any further details. More on the design principles here.

- Follow Nigel Lawson’s lead, and raise the rate of capital gains tax so it is equal to the rate on income. Raises at least £8bn.

- Abolish the non-dom regime and replace it with a straightforward exemption on foreign income/gains for the first three years after people come to the UK. Will be more useful to the workers we want to attract than the current mess, but won’t enable oligarchs and oil sheikhs to live in the UK tax-free. Plausibly raises £2bn.

- Close the stamp duty loophole that means most commercial real estate is bought and sold inside “special purpose companies” so that no stamp duty is paid. Will probably raise at least £1bn.

- Raise the annual tax on homes held in companies – ATED. Should yield £200m.

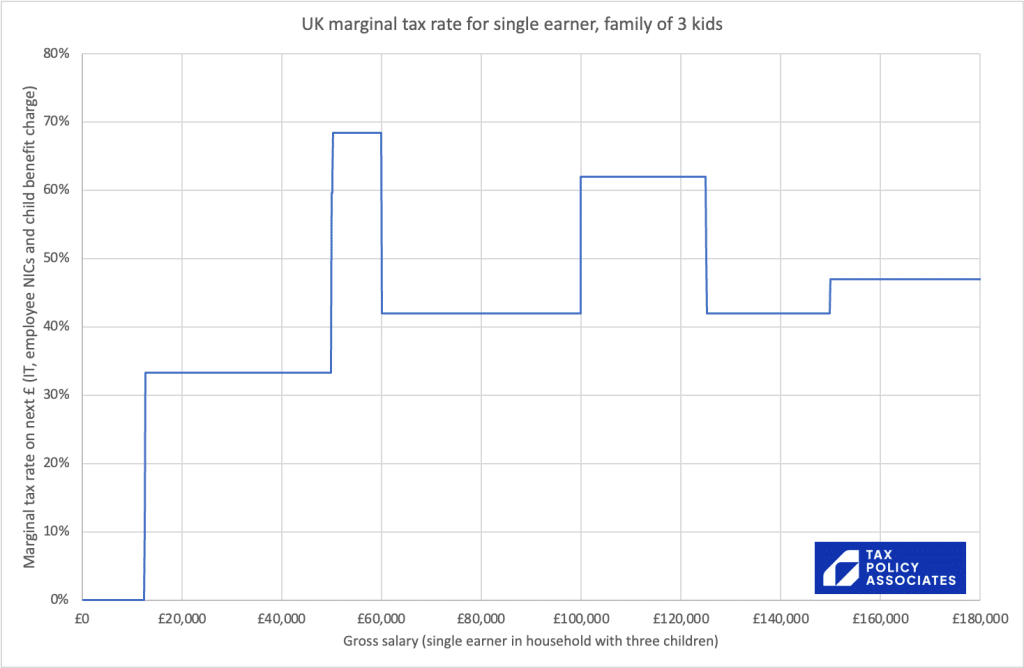

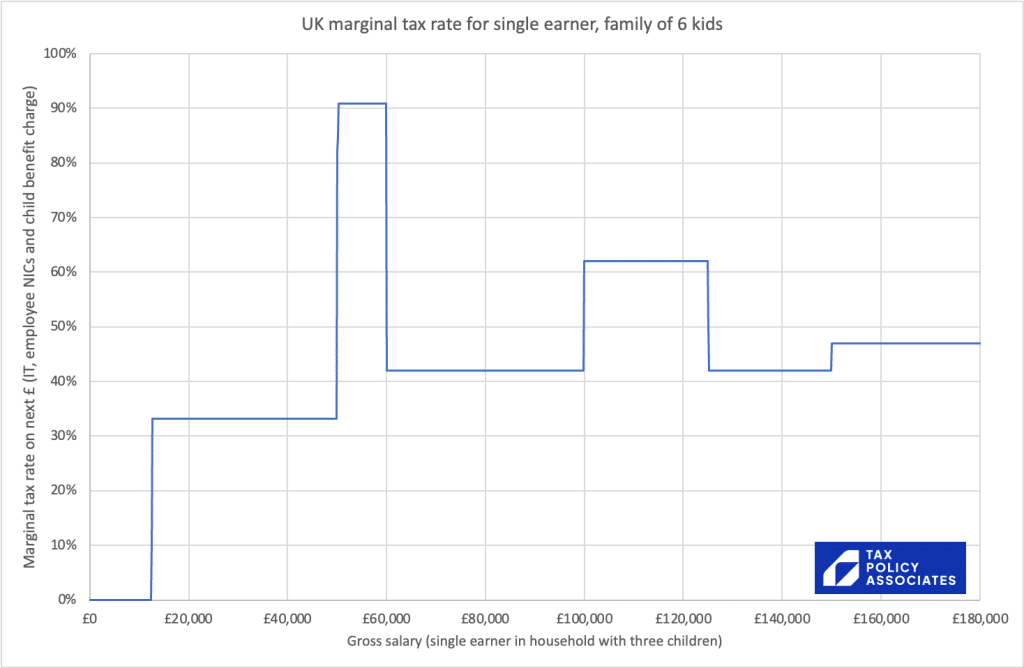

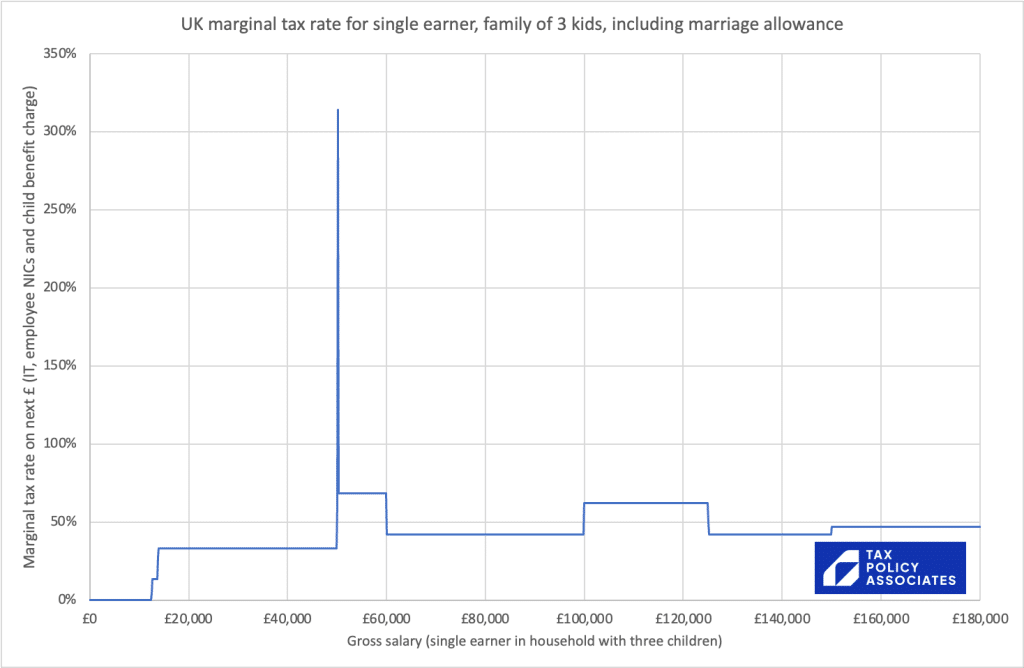

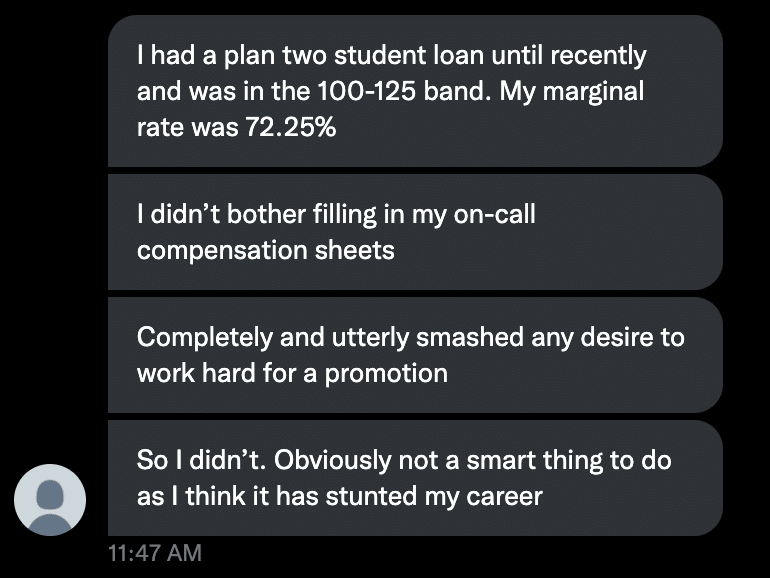

- Eliminate the tapers and clawbacks that result in anomalously high marginal income tax rates of well over 50% and sometimes higher than 90%. Pay for it by increasing the additional 45p rate, or reducing the threshold at which it applies.

- Scrap/cap over-generous inheritance tax exemptions, and use the revenues to reduce the rate from 40% to around 25%.

- Pensions tax relief costs over £48bn, with most of the benefit going to highest earners. Capping relief at 30% should raise at least £2bn1.

- Announce the long-term objective of ending employer’s national insurance, so that all income is taxed at the same rate. This will mean tax-cuts for employees, and tax rises for others – but it will benefit the economy as a whole.

- Start a review of other features of the tax system that penalise growth: top of the list, the high VAT threshold and the never-ending changes to corporation tax rates and reliefs.

On the other hand, here are some things the Chancellor will probably do, and which are neither brilliant nor terrible:

- Let fiscal drag collect an additional £30bn of tax with minimum political pain. The easiest way to collect lots of tax is to tax everyone, and this certainly does that. And conventional wisdom is that voters don’t notice fiscal drag; but until this year it was also conventional wisdom that voters don’t notice rises in national insurance.

- Lower the threshold at which the 45% additional rate applies. As Arun Advani points out here, this is something of a “poll tax” on moderately high earners, as it has the same cash impact on someone earning £150k as it does on someone earning £1m.

- Slight expansion of the existing windfall tax, perhaps extending it past 2025. It’s a poorly designed tax, and we’d be better off replacing it, but the case for taxing people who’ve obviously made a windfall is politically and practically irresistible.

And here are some things we absolutely shouldn’t do:

- Change the tax treatment of already-existing pensions or ISAs. People used these products believing they worked a particular way. It’s unfair, and will damage faith in the tax system and savings vehicles as a whole, if we change the rules of the game after people start playing.

- Introduce a wealth tax. Almost all previous wealth taxes around the world have failed, raise little/no revenue, or both. Most wealth tax proposals ignore this, and can be discarded as unserious populism. The few that are intellectually rigorous end up being politically unfeasible (because they tax pensions and homes).

- Create more points in the income tax/national insurance system where the marginal rate is over 50%. Chancellor Neidle would impose a 200% wealth tax on anyone proposing tax changes without saying precisely what they mean in terms of marginal rates.

Any other suggestions?

Image by DALL-E: “a tree in autumn, with its branches covered in brown leaves and one dollar bills, digital art”

Footnotes

Source: HMRC statistics and my napkin ↩︎

-

The first thing we do, let’s tax all the lawyers.

The UK taxes high-earning lawyers less than bankers. That’s irrational – and illustrates a wider problem with the tax system. It’s hard to change, but we’d all benefit if we taxed all income in the same way.

Here’s the problem:

- A City law firm has £100m of profits to share between 100 partners.1 The tax consequence: each partner has gross income of £1m on which they pay £435k income tax2, plus £35k national insurance3. So the lucky partners take home £530k4, and lucky HMRC collects £47m.

- A bank has £100 million of profits to share between 100 traders. The tax consequence: the bank pays employer’s 13.8%5 national insurance, leaving £87.9m for the bankers.6 So each banker has a gross income of £879k, on which they pay £380 income tax and £21k national insurance. So the poor bankers take home £477k, and even more lucky HMRC collects £52.3m.

The lawyers have an overall effective tax rate of 47%; the bankers’ rate is 52.3%. That is an odd and irrational result.

Why does it happen? The simple reason is that partners in a law firm are not employees, and so there’s no 13.8% employer’s national insurance.7 This isn’t tax avoidance, or even tax planning8 – it’s an inevitable consequence of the fact that our tax system puts so much weight on whether a person is an employee.

The question is whether we should change the law and tax partners in law firms and other large professional firms the same way as employees.

How much tax could we raise?

The Lawyer has crunched the numbers on large law firms, and reckon that the top 50 UK law firms and top 50 US law firms have a combined UK profit of £6.3bn, implying that if they were subject to employer’s national insurance, that would yield an additional £870m of tax.

The top 75 UK accounting firms have a profit of around £3bn, implying an extension of employer’s national insurance would yield an additional £400m of tax.

Add in management consultants, investment managers, and other large professional partnerships (whether in partnership or corporate form) and it’s realistic to think we’d be looking at between £1.5bn and £2bn of revenue.9

Should we do it?

Given the economic mess we currently find ourselves in, it’s hard to defend £1m lawyers paying less tax than other comparable professionals.

As Catrin Griffiths, editor of The Lawyer, says:

All the data points to the fact that commercial law is a highly successful UK sector that relies on an infrastructure of education, training and technology. In a climate of rising taxes for all, law firms will be increasingly challenged to consider their own financial contribution to the public finances.

Politicians may find the prospect of an easy £2bn of additional revenue tempting.

And yet I pause at the idea of creating a headline tax rate of over 50%. On the one hand, that’s already what happens – the bankers in my example above have an effective rate of 53.5%. But – and this is important – they probably don’t feel like they do.

And taxing partnerships/partners differently from companies/shareholders would be unprincipled and asking for trouble (meaning: unfair distortion and avoidance).

Wider implications – and solutions

It’s not just lawyers. The same distortions and difficulties arise throughout the economy.

We tax employment income much more than other types of income, and that creates distortion, uncertainty, and tax avoidance. I’ve no doubt that employer’s national insurance is a Bad Tax and we should end it.

But if we immediately abolished national insurance, and rolled it into income tax, then I fear many people would be aghast at how much tax they were paying (even if employers passed-on the benefit of the employer national insurance cut, which is distinctly optimistic). Tax psychology is a thing, and (on the basis of no evidence) I worry about the overall economic and fiscal effects of people feeling like they’re paying more in tax than they take home. That’s not a reason not to act, but it’s a reason to be very cautious.

This is a hard problem.

There are two things that might make it easier:

- First, make the change mostly revenue-neutral. We’d be greatly expanding the base of people paying the 13.8% tax. So we don’t need the rate to be as high as 13.8% to collect the same amount. My feeling (and tax policy needs more than a feeling) is that nobody should be paying a marginal rate of over 50%.

- Second, mandate that employers pass on the savings. This would be a highly unusual thing to do, but in this circumstance, it might be realistically achievable10

This would have two effects. People who aren’t employees would see a tax rise, but it would be less than the full 13.8%. Employees would see an actual tax cut. It’s just about possible this could make the whole proposal politically feasible. Maybe.

Much better to actually fix the underlying problem than to pick on one particular sector – more principled, and much less susceptible to avoidance.

All we need is a suitably courageous politician.

Image by DALL-E: “a statue of lady justice, with a stack of dollar bills in her hand, digital art”

Footnotes

Some people unfamiliar with City law firms may be shocked at how large these figures are; some people who work in City law firms may regard this as a poor level of profitability, and possibly a failing firm. ↩︎

i.e. tending towards the 45% top marginal rate ↩︎

Tending towards the 2% marginal rate ↩︎

It will usually be less than this, because law firms – like most businesses – have non-deductible expenditure… in practice that will raise the effective tax rate by a couple of % ↩︎

There’s a good argument I should add the 0.5% apprenticeship levy, because it does behave just like another 0.5% employer’s NI. But, given it’s semi-hypothecated, I decided to leave it out. If you disagree with me on this, then that means my bigger argument has 0.5% more force. ↩︎

I made a bad mistake here, and added the 13.8% employer’s NI to the £100m. That makes no sense, because the bonus pool was stated to be £100m – the bank is going to have to use that to pay the bonuses and the employer’s NI. Now corrected! ↩︎

Some people will complain at this point that the bankers aren’t paying employer’s national insurance – so why include that in their effective tax rate? The answer is that the economic evidence suggests that, in the long run, the economic incidence of employer’s national insurance largely falls on wages. In my example it’s particularly clear – the bank has a bonus pool, and the employers are going to get what’s left after employer’s national insurance is paid – so it is directly reducing their income. ↩︎

Except when it is – see the smart comment from ‘Tigs’ below regarding salaried “partners” ↩︎

There would certainly be difficult edge cases; this post is about the principle rather than the practicality. Similarly, lots of points to think about re. non-deductible expenditure, which for some large partnerships already takes the effective rate over 50%. ↩︎

The usual problem is this: when the 5% “tampon tax” was abolished, we couldn’t legally require that prices were cut by 5%, because retail prices move all the time, and it’s not possible to disentangle the tax cut from other price changes. Wages are different. It might (and this would need a lot of thought) be possible to require employers pass on an employer’s national insurance cut. That wouldn’t be a perfect solution, because an employer could pass on the cut, but at the same time scrap a wage rise that otherwise would have been paid. But it could (particularly in a time of low inflation) ensure that most of the benefit went to employees in the short term, and there’s good reason to believe that it will go to employees in the long term regardless of what we do. ↩︎

-

How the abolition of the “tampon tax” benefited retailers, not women

5% VAT applied to tampons until January 2021 – then it was abolished. Many were hoping that the savings would go to women, in reduced tampon prices. Our analysis of ONS pricing data shows that no more than 1% of the VAT savings was passed to consumers; the rest – and very possibly all the saving – was retained by retailers.

Our report is available in PDF format here. An interactive chart demonstrating our conclusions is here. The Guardian report on our paper is here and the FT here.

A web version of the PDF report follows below:

Executive Summary

5% VAT applied to tampons and other menstrual products until January 2021. Then, following the high-profile “tampon tax” campaign, it was abolished. Many expected that the benefit of the tax saving would go to women, in the form of reduced prices.

However, an analysis of ONS data by Tax Policy Associates demonstrates that the 5% VAT saving was not passed onto women. At least 80% of the saving was retained by retailers (and very possibly all of it).

The key piece of evidence is this chart showing price changes before and after the abolition of the “tampon tax” on 1 January 2021. Ignoring the large spike in December 2020, average prices after the change are only slightly lower than before the change. For reasons explained further below, this likely reflects normal market movements rather than the passing on of the VAT saving.

Interactive charts that illustrate this in more detail are available here.

Background

Campaigners had been pushing for years for the 5% VAT on menstrual products to be scrapped[1]. EU law prevented this, but in 2016 the then-Government obtained in-principle agreement with the EU[2] that this would change. In the event, these discussions were overtaken by Brexit, and it was not until January 2021 that the tax was abolished. [3]

There will be widespread interest in who benefited from the abolition of the tampon tax – consumers or retailers. And there is also an important tax policy point. We have recently seen proposals that VAT or duties be reduced or removed from particular products or services (e.g. VAT on the tourism industry, VAT on petrol or fuel duty on petrol/diesel). However, these campaigns often assume that the benefit of the tax cuts will be passed onto consumers. The “tampon tax” provides further evidence that this will often not be the case.

Analysis

We used Office for National Statistics data to analyse tampon price changes around 1 January 2021, the date that the “tampon tax” was abolished. We were able to do this because the ONS includes tampons (but not other menstrual products) in the price quotes it samples every month to compile the consumer prices index. Since 2017, the ONS has published the full datasets for its price sampling. [4]

We set out our methodology below.

Qualitative analysis

Our methodology results in the above chart of tampon prices before and after 1 January 2021. The data is normalised to December 2020, i.e. the price on December 2020 is set at 100% for ease of reference – this facilitates easy comparisons between different products.

Or, over a longer period:

The charts show a 6% fall in tampon prices in January 2021 – that is largely a reversal of a 4% increase the previous month; there is then a 2.5% increase in February 2021. Overall, the average price for the period after the VAT abolition is about 1.5% less than it was beforehand.

The December 2020 price spike

It could be suggested that the 4% price rise in December 2020 was a deliberate strategy to make it look as though the 5% VAT cut was being passed to consumers the next month. However, we regard that as highly unlikely. It would require astonishing cynicism on the part of retailers. It would also suggest a degree of coordination between a large number of retailers that would be difficult to arrange in practice, as well as a flagrant breach of competition law.

As we will show below, other products also show price spikes at a variety of different times, which we expect are driven by a complex and unpredictable mixture of seasonal and situational supply/demand factors. This seems the more likely explanation. However, the fact that the December 2020 price was a “spike” means that it would be incorrect to conclude from the December and January data that tampon pricing fell by 5% when VAT was abolished.

Comparison with other products

It is insufficient to look at tampon pricing in isolation. For example, if many other consumer products were materially increasing in price in January 2021, then the absence of an increase in tampon pricing could be consistent with the benefit of the VAT abolition being passed to consumers. However, the evidence does not show this.

Our analysis includes price movements for thirteen other products that would likely be subject to similar supply and demand effects to tampons – toiletries and products made of cotton. It is important to note that none of these projects were subject to VAT changes over the period in question. Hence, if the benefit of the VAT abolition was passed on to consumers, we would expect to see a significant divergence between price changes in tampons and price changes in the other products. We do not.

This chart compares price changes in tampons (the red dotted line) with price changes in tissues (the blue line).

The two datasets seem reasonably correlated on either side of 1 January 2021 (with the exception of a large spike in tissue pricing in December 2019, and another spike at the start of the data in December 2017). If the benefit of the tampon VAT abolition was passed onto consumers we would expect a divergence between the two datasets after 1 January, as tampon prices fell but tissue prices did not. However, we see no such effect.

This chart compares tampon pricing (red dashed line) with t-shirts (cyan line). T-shirts are largely, but not entirely, made of cotton, and therefore are in principle subject to similar demand factors:

While t-shirt pricing seems much more volatile than tampon pricing, there is again no evidence of prices diverging after 1 January 2021.

There is an interactive version of the chart here that lets the user compare tampon price movements with the other toiletry and cotton products included in the CPI, as well as the CPI itself (which, towards the end of the period covered by the chart, increases steeply as energy costs etc start to rise). Clicking on the legend on the right-hand side will add/remove additional products.

Quantitative analysis

Comparing the average change in tampon prices for the six months before the abolition to the six months after confirms what we see in the above charts – the change in the price of tampons is broadly in line with other price changes we see in products where the VAT treatment did not change:

A similar picture is apparent over a longer period:

This implies that none of the VAT abolition was passed to consumers in the form of lower prices.

What if, in the interests of prudence, we ignore the other products that showed a drop in price, and look at tampon pricing in isolation? How likely is it that the apparent 1.5% drop in price is a real effect, and not just a function of the high variability of the pricing of all of these products? Our statistical analysis (see the “methodology” section on below) suggests that, at most, 1% of the price reduction was a real effect

Conclusions

Consumers did not in fact get the full benefit of the abolition of the 5% VAT “tampon tax”. At most, tampon prices were cut by around 1%, with the remaining 80% of the benefit retained by retailers. More likely, the retailers took all the benefit – amounting to £15m each year.[5]

It is open to any retailer contesting the figures in this report to publish full data showing their pricing on either side of the 1 January 2021 abolition.

footnote Our analysis is of ONS data across retailers as a whole. It is, therefore, possible that some retailers did pass on the benefit of the VAT cut, and provided lower prices than the average figure in the data. That would, however, imply that other retailers provided higher prices. And where, as happened in at least one case, a retailer[6] announced tampon price cuts ahead of the actual abolition of the tax, that retailer should be able to demonstrate that the price cut happened, and as a result their prices remained diverged from other retailers up to (and perhaps beyond) 1 January 2021.It is our hope that the power of the “tampon tax” campaign means that public pressure will cause retailers and suppliers, at this late stage, to pass on the full benefit of the tampon tax abolition to consumers.

Policy implications

This is an unusual case where a product is specifically included in ONS data. Prices changes are not normally so visible; nor are they normally subject to this degree of political pressure.

The public and policymakers should therefore be sceptical of those making proposals for cuts in VAT and duties, particularly if claims are made that this will benefit consumers, and/or those on low incomes (that was generally not the case for the “tampon tax” campaign, which was largely argued on a point of principle). If we want to support those who can’t afford to pay, then the answer is to put cash directly in their hands (through the tax and benefits system), or in some cases (perhaps such as this) provide free or subsidised products. We should be cautious before lowering tax rates in the hope that benevolent retailers and suppliers will pass the savings on to those who need it. The evidence from the “tampon tax” is that they won’t.

Methodology

Source of data

The Office for National Statistics compiles detailed monthly price quotes for a large variety of products, and then calculates price indices for each of those products. Since 2017, this data has been published.

To assess the change in tampon prices, we extracted the ONS data from December 2017 (When the data starts) through to April 2022,[7] and consolidated the index data for tampons and another thirteen broadly comparable products. We ended in April 2022 because after that point inflation effects start to dominate (see here).

We then wrote a short python script to analyse and chart the data. This is freely available on GitHub here. For clarity, all the price indices are normalised to 31 December 2020.

T-test

The bar charts above provide a reasonably clear indication that nothing exceptional happened to tampon pricing on the six months either side of January 2021. Whilst the average price after this date was higher than the average price before, there were greater differences in most other comparable products.

Apply statistical techniques to these datasets is not straightforward given the limited number of datapoints and very high degree of volatility. It was, however, thought appropriate to run an unequal variance one-sided t-test (using the python SciPy library) to compare the pricing datasets for the six months before 1 January 2021 with those for the subsequent six months. The null hypothesis would be that the price did not change; the alternative hypothesis was that the price was lower on and after 1 January 2021.

This resulted in the following set of p-values:

Product p-value (six month t-test) Tissues-Large Size Box 0.00001 Women’s Basic Plain T-Shirt 0.00627 Boys T-Shirt 3-13 Years 0.00709 Sheet Of Wrapping Paper 0.03236 Men’s T-Shirt Short Sleeved 0.09442 Toilet Rolls 0.10948 Tampons 0.14045 Kitchen Roll Pk Of 2-4 Specify 0.53249 Disp Nappies Spec Type 20-60 0.89392 Baby Wipes 50-85 0.95865 Toothpaste (Specify Size) 0.99270 Plasters-20-40 Pack 0.99694 Razor Cartridge Blades 0.99831 Toothbrush 0.99847 As expected, the p-value for tampons is not significant (> 0.05). More significant p-values were achieved for six other products, four of which were actually significant at 5%. Those products did not receive any change in VAT treatment over the period in question so, absent other unknown factors, this should be regarded as a product of the volatility of pricing decisions in a complex market environment, as well as potentially unknown supply and demand factors.

If we look at longer periods than six months then the p-value for tampons becomes more significant (because, although the average does not change, the number of datapoints increases, and significance becomes “easier” to attain). At eight months, a significant result is achieved (p-value=0.03201), although given that more significant results are (again) obtained for other products, this result should be treated with caution.

Nevertheless, if the tampon pricing results are viewed in isolation, they are compatible with the price having decreased after 1 January 2021. We can estimate the maximum likely extent of that decrease by constructing a synthetic tampon pricing sequence, identical to the actual tampon pricing sequence but with an increase of x% from 1 January 2021. If a t-test of that synthetic pricing sequence does not provide a significant p-value then that implies that the statistically significant difference between the pre-January 2021 pricing and post-January 2021 pricing is limited to a tampon price reduction of x%.

Testing different values of x, the p-value ceases to be significant with x at 1% (p-value equal to or greater than 0.0935 for any given range of months) (the precise methodology utilised can be seen in the GitHub code).

Hence, we can conclude that there is only weak evidence of any change in tampon pricing reflecting the cut in VAT, with the greatest realistic extent of any price reduction being approximately 1%.

Limitations

The analysis in this paper is subject to a number of important limitations:

- The ONS adopts a methodology that is designed to produce statistically rigorous results across consumer prices as a whole. It is not necessarily intended to provide robust figures for changes in the price of one product. Nevertheless, around 250 tampon prices[8] are sampled each month[9].

- The prices of tampons and the other consumer goods considered in this paper will be affected by numerous factors – the supply of raw materials, energy costs, and sheer random happenstance. It is therefore unsurprising that we see a large amount of month-to-month variation in prices; this makes it difficult to identify separate real trends from noise. More sophisticated statistical methods than a t-test are therefore not helpful (difference-in-difference and synthetic control methods were attempted, but did not produce meaningful results).

- The January 2021 VAT change applied to all menstrual products,[10] however ONS data only covers tampons. It is therefore possible in principle that the benefit of VAT abolition was passed to consumers of e.g. sanitary towels, although it is not obvious why that would be the case.

Acknowledgments

Thanks to Arun Advani of the University of Warwick for his advice on statistical techniques, to Gemma Abbott for her advice on the background to the “tampon tax” campaign, and to Laura Coryton for her help and advice. Any errors in our analysis are the sole responsibility of Tax Policy Associates, as are the conclusions we draw from it.

And many thanks to the Office for National Statistics for publishing the data at a level of detail that facilitates this kind of analysis, and also for responding swiftly and helpfully to our queries.

[1] Technically VAT on tampons was not abolished – the rate was reduced to 0%. This is different from an exemption, because an exemption would mean that retailers can’t recover the cost of purchasing tampons from wholesalers, and would therefore probably result in higher consumer prices. However, in the interest of clarity, this report refers to “abolition”.

[2] See, e.g. https://www.theguardian.com/money/2016/mar/18/tampon-tax-scrapped-announces-osborne

[3] See the 1 January 2021 Government announcement: https://www.gov.uk/government/news/tampon-tax-abolished-from-today

[4] The ONS datasets can be found here: https://www.ons.gov.uk/economy/inflationandpriceindices/datasets/consumerpriceindicescpiandretailpricesindexrpiitemindicesandpricequotes

[5] Extrapolating from the £47m figure in the Government press release https://www.gov.uk/government/news/tampon-tax-abolished-from-today

[6] See https://www.expressandstar.com/news/uk-news/2017/07/29/tesco-beats-tampon-tax-with-5-price-cut/

[7] Most of that date is here, except the 2019 data which is here

[8] The full set of price quotes obtained in January 2021 is available here: https://www.ons.gov.uk/file?uri=/economy/inflationandpriceindices/datasets/consumerpriceindicescpiandretailpricesindexrpiitemindicesandpricequotes/pricequotesjanuary2021/upload-pricequotes202101.csv

[9] There are complex issues around sampling error in CPI which are outside the scope of this paper (see, for example, Smith (2021)). However, with 250 samples, the sampling error ought to be very much less than the 5% VAT reduction.

[10] The VAT term is “sanitary products” – details are in HMRC VAT Notice 701/18 – see https://www.gov.uk/guidance/vat-on-womens-sanitary-products-notice-70118

Image by DALL-E – “a pound sterling sign, £, made of tampons, digital art, on a blue background”

-

The real reason your work doesn’t let you remote-work from abroad, and how to fix it

We’re delighted to publish an article on the underreported subject of tax and remote working, by Leonard Wagenaar, an M&A tax and international tax professional[1] whose insightful analysis is usually posted on LinkedIn here. This is the first in an occasional series of articles by outside tax experts – we won’t necessarily agree with every word, but we will agree that the subject is important and not currently getting enough attention.

Since the pandemic, remote work has become common. Some countries now try to attract remote workers to settle in their country, so they can work remotely internationally. Of the 27 EU countries, 11 have implemented or are considering special ‘digital nomad visas’[2]. Two of them – Greece[3] and Spain[4] – also couple this with special tax breaks for remote workers, triggering fears of a race to the bottom on personal taxes.

Although most of us can’t imagine a working environment without remote work, international remote work is still rare. New visa rules are unlikely to change that. Within the EU, there were never any visa restrictions on remote work for EU citizens. A culture of international remote work could transform the labour market. But the biggest obstacles are tax systems, even those from supposedly supportive countries.

Right now, no sensible employment contract will leave the employee free to work from wherever they want, as a travelling employee could easily trigger tax for the employer wherever they travel. That’s because countries generally tax the foreign companies as soon as they have a ‘permanent establishment’ (or “PE” for short). Generally, a PE will be triggered if someone does business for the employer through a ‘fixed place of business’. This is a concept that’s over a hundred years old and though it has developed over all those years, it clearly wasn’t designed with the digital age in mind. For instance, could a desk in your holiday home be a fixed place of business? Or the kitchen table of your friend’s uncle? How about the table in the local coffee shop? Or could the ‘fixed place’ even be within the work phone you carry around?[5] No one really knows.

There are plenty of guidance notes, published tax rulings and case law, but these are highly fact dependent and go in different directions. Being stranded abroad against your will in a global pandemic probably doesn’t trigger a PE, provided you at least tried to get back home[6]. If the company demands that you work remotely in another country, that’s likely a PE[7]. Having an office abroad and not using it is not a PE[8]. But the typical basic remote worker fact pattern? No one really knows. Countries can apply other tests to answer this question, such as “is the home office at the disposal of the employer?” or “does the employer have the ability to exclude people from the home office?”. But generally, these tests replace one obscure question with another.

The longer a fact pattern continues, the higher the risk of a “fixed place of business” PE. The threshold is usually set at three months. But there are exceptions to this too, especially if the activities abroad repeat themselves after interruptions. And if one remote worker leaves the country, but another enters around the same time, does that reset the clock? Does it matter whether the second employee visits the same place or does similar activities? Again, no one really knows.

Most of the time, having or not having a PE would not impact the tax due for the employer all that much. But a PE would require the employer to register locally, run a local payroll and run expensive transfer pricing analyses to figure out just how much profit should be allocated to the PE. Any position they take will displease either their home tax authority or the foreign tax authority, meaning they will live with a significant risk of challenge. So, usually, employers don’t bother and just require that they can control the employee work location, even if that’s outside the office. In the Netherlands, an employer can’t unreasonably deny a request for remote work, but they can deny such a request if someone wants to work remotely from another country.

So, in short, archaic tax rules are holding back a modern labour market. Political discussions are dominated by images of ‘digital nomads’ backpacking their way between work, the beach and travel. But the best opportunities are for people who now struggle to find suitable work due to their location. If employers could hire remote employees internationally with minimal disruption, the biggest opportunity is for areas that have been left behind economically. Remote work – including international remote work – is a tool for levelling up.

So far, countries have not felt empowered to solve this problem, but they have all the tools to do so. The definition for PE has been fixed in many double tax treaties. A multilateral solution would be most efficient, but will take a very, very long time, especially now that all international tax debate seems to be consumed by other topics[9]. In the meantime, there is plenty countries can do unilaterally. Tax treaties give countries the right, but not the obligation, to tax PEs. So, countries can apply higher thresholds than tax treaties. In other words, host countries can choose not to tax foreign companies with remote workers by issuing clear binding guidance that a home office does not trigger a PE and neither do workspaces in hotels, Airbnbs, coffee places or on smart devices, etc. [10] It would not bring the company’s overall tax burden down (not by much at least), but it would greatly reduce their compliance burden. And if it stops companies from trying to control where their employees are working from, I’m sure they won’t complain either.

This simple measure could very well be more effective in attracting international remote work than new visa categories or even personal income tax breaks. Countries can adopt this simple step without a potentially damaging tax competition that comes with offering lower personal income taxes. After all, they can still collect all personal income taxes from the remote workers. It is all possible. But is the political will there?

Photo by Glenn Carstens-Peters on Unsplash.

[1] All views are in personal capacity and do not necessarily represent those of any employer, remote or local.

[2] https://www.euronews.com/travel/2022/10/23/want-to-move-to-europe-here-are-all-the-digital-nomads-visas-available-for-remote-workers

[3] https://visaguide.world/digital-nomad-visa/greece/#:~:text=Taxes.,a%2050%25%20reduction%20tax%20program.

[4] https://www.schengenvisainfo.com/news/spain-introduces-new-visa-for-foreign-start-ups-digital-nomads-reduces-taxes-for-them/#:~:text=Digital%20nomads%20will%20also%20be,for%20up%20to%2012%20months.