If I were a Conservative Chancellor of the Exchequer, I’d want a tax system that delivers growth and doesn’t hold back families and businesses from achieving success. These would be my seven priorities:

1. An end to marginal ratesthat punish work

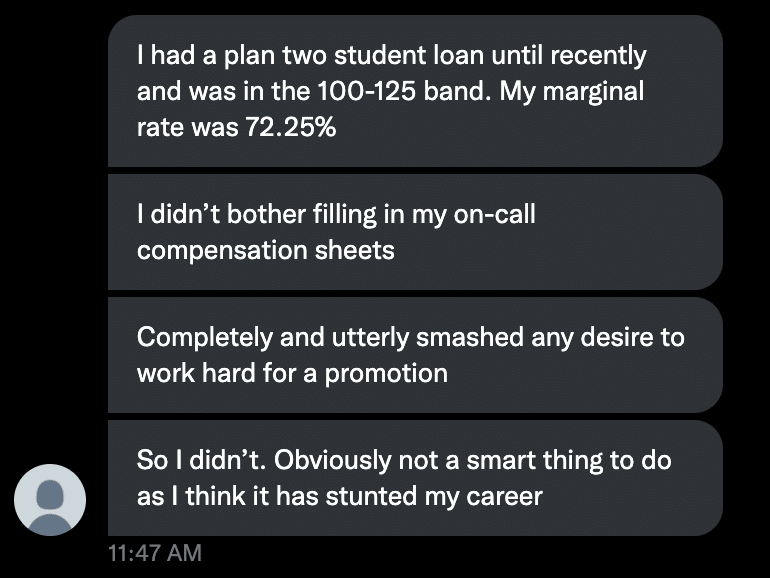

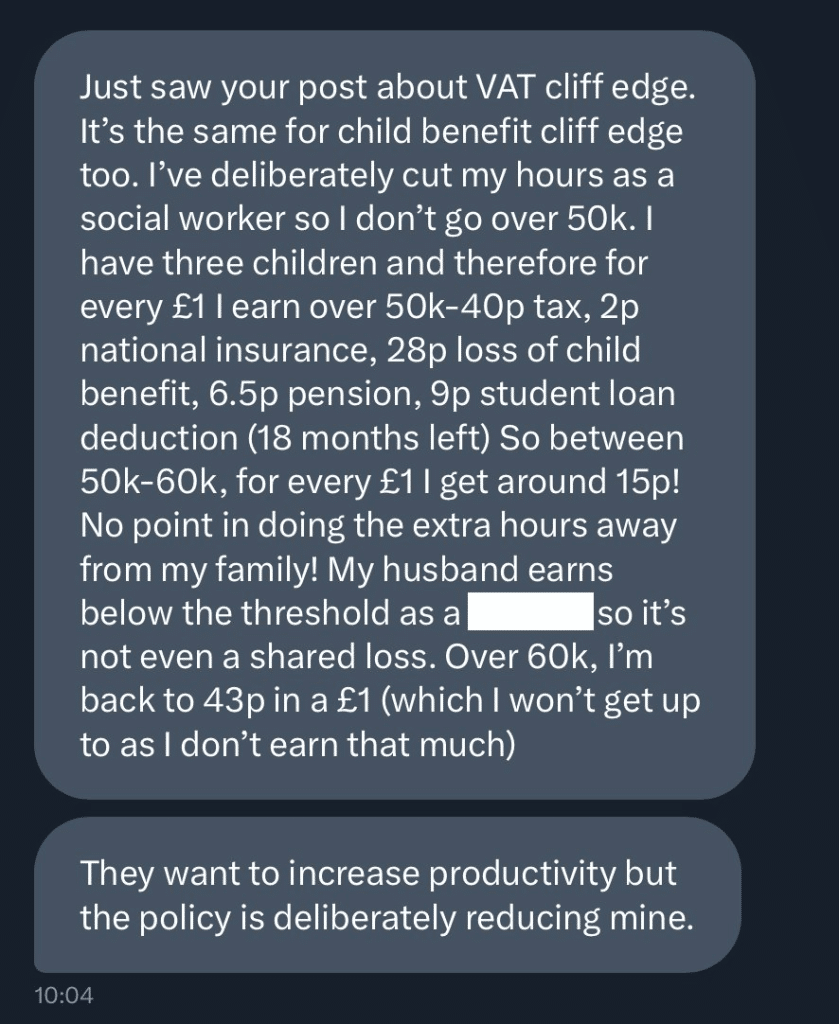

A marginal rate of 50% is unacceptable, but there are social workers earning £50k paying marginal tax rates of 80%. No Conservative should stand for this:

Many of the problems can be immediately fixed with abolition of the child benefit taper (and the Child Benefit High Income Charge) and the personal allowance taper. The cost is likely less than HM Treasury has historically believed, given the widespread taxpayer response of controlling working hours and/or making additional pension contributions. The residual cost could be covered by a small change to the rate and/or thresholds for the highly paid (e..g. by slightly lowering the additional rate threshold).

The impact of student loan repayments on marginal tax rates should be reviewed, together with the impact of the benefit system on marginal rates.1

2. Fix a VAT system that holds business back

No Conservative should accept a VAT threshold which abundant evidence suggests is a brake on the growth of small companies:

There is a well-known solution to this that is both neat and plausible: to increase the threshold. That would, however, only make the problem worse – the threshold would become a brake on the growth of larger companies. The real answer is to drop the threshold, and use the revenues raised to reduce the rate of VAT for everybody.

The practical difficulty for small and micro businesses shouldn’t be understated, in terms of both financial challenges and compliance headaches. The threshold should be frozen for now, with a review and consultation on the way forward, ready for legislation in Finance Act 2024.

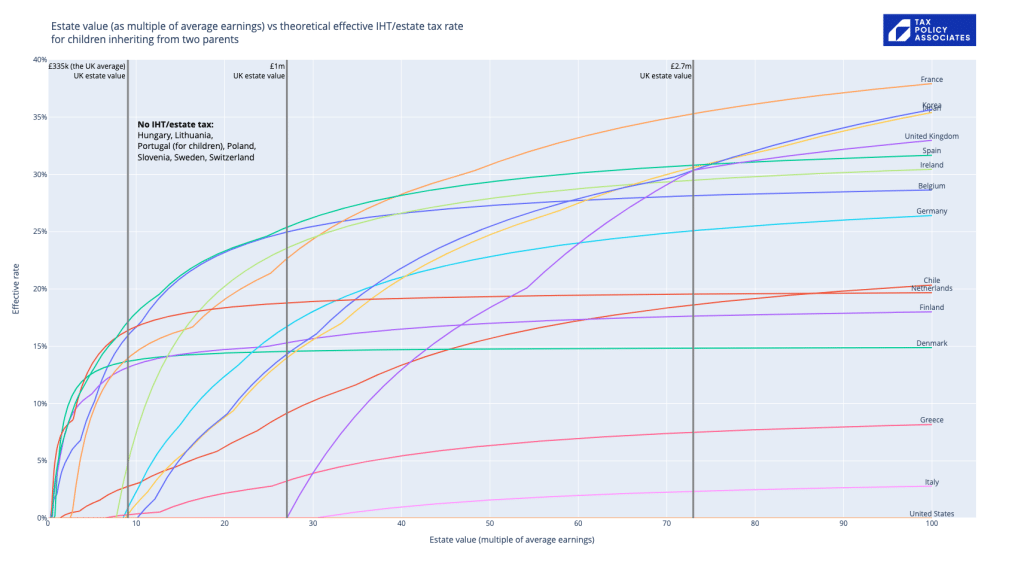

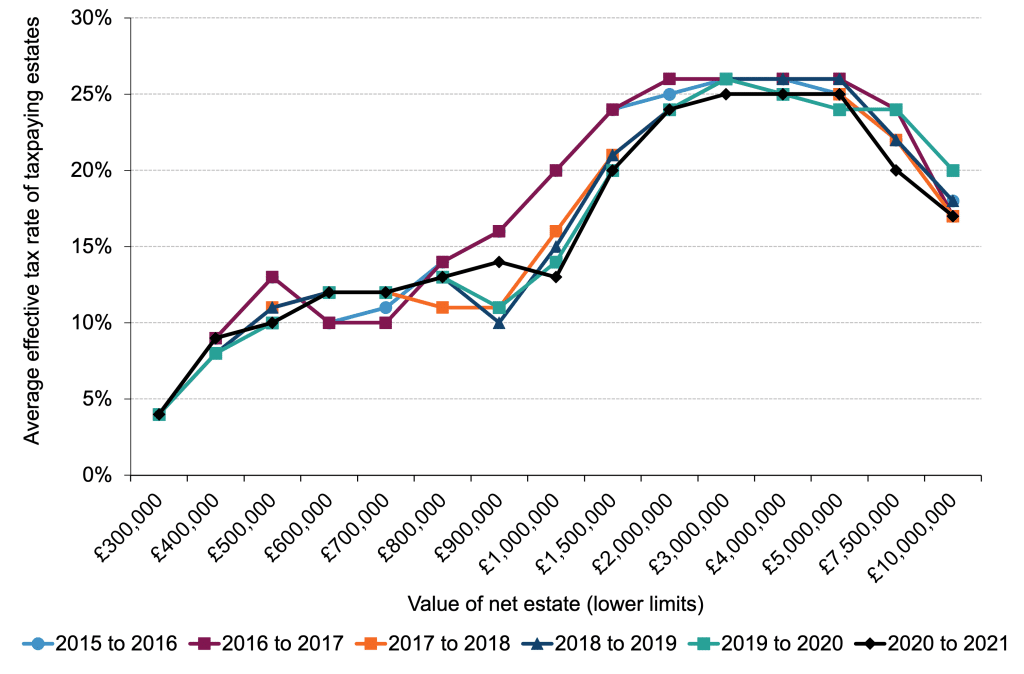

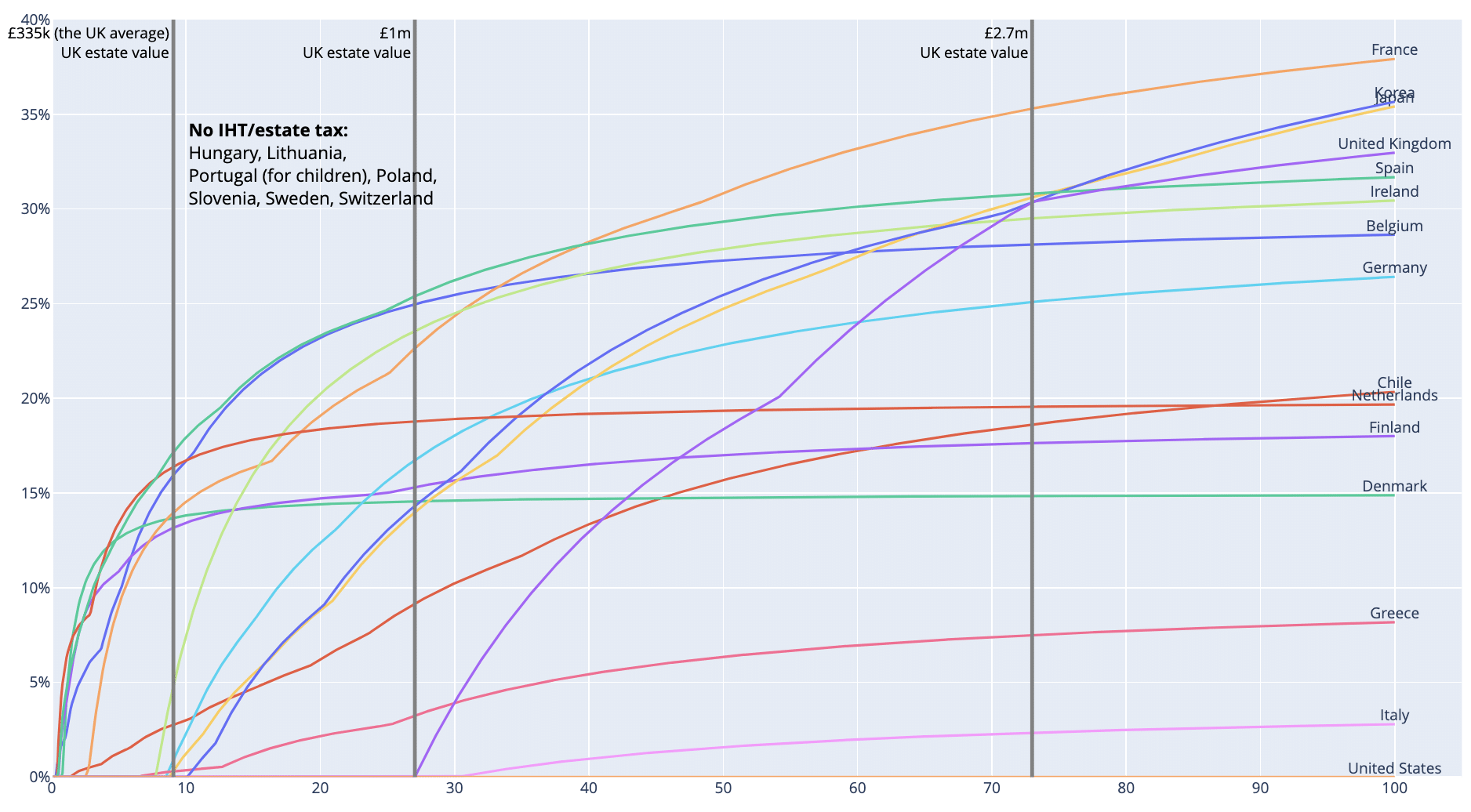

3. Slash the rate of inheritance tax for the middle class

Time to fix both problems. Small business and small agricultural holdings should continue to be protected, but there’s no reason why the middle classes should be paying twice the effective rate of inheritance tax as the seriously wealthy:

The answer: radically cut the rate, paid for by capping exemptions and reliefs.

4. Make full expensing permanent

Last year, the Government introduced “full expensing” – up-front tax relief for investment in plant and machinery. There’s a powerful argument for this – the UK tax system currently has a bias against business investment.

The problem is that, for essentially bureaucratic reasons, full expensing was introduced as a temporary three year measure. Currently it only has two and half years left. This renders it pointless – no business is going to base its long term investment planning on a relief which will disappear by the time spades hit the ground. The Tax Foundation, which has campaigned for full expensing in the US and UK, says this means full expensing currently has no long term impact on UK growth. A missed opportunity.

The Chancellor should have the courage of his convictions, and make full expensing permanent. Then challenge Rachel Reeves to say that Labour will keep it. A long term bipartisan commitment to maintaining full expensing would give business the confidence to invest, boosting wages and economic growth.

The first to go? Stamp duty – not SDLT, but the ancient tax on documents, which still works in much the same way as it did in 1671.

Stamp duty costs business a small fortune in compliance, and likely raises little or no actual revenue. We have modern taxes on securities and land, and we don’t need anything else. I wrote more on that here.

6. Simple simplification

Everyone agrees the tax system is too complicated. But that complication is itself an obstacle to simplification. The Office of Tax Simplification had less impact than many hoped because its recommendations were often too politically difficult to implement.

So we need to look for ways to simplify the tax system which are more modest but still high impact. One is to identify “fossils”: remnants of another area which now serve no real purpose other than complication and cost.

So the Finance Bill should contain a power for tax rules and even entire taxes to be repealed by Regulations, where the OBR agrees that this can be done without a material loss of tax revenue. HMRC and HM Treasury could create a small team working on this full time.

7. Protect the public from tax scams

Tax avoidance used to be the preserve of the wealthy. When it failed – as in recent times it almost always did – the taxpayers could afford to pay the bill.

These days, the wealthy are mostly too well-advised to buy tax schemes. But there’s a largely unregulated industry flogging dodgy tax schemes to people with modest earnings and assets. When it goes wrong, the advisers disappear, often leaving the taxpayers with life-changing bills. It’s a scandal – a mis-selling scandal as much as a tax scandal.

The Government should criminalise unregistered mass-marketed tax schemes (including “refund” schemes such as those discussed here). Promoters (and their directors and owners) should be liable to penalties of twice the fees collected. I’ll be writing more about the details of this soon.

Thanks to WeThink (formerly Omnisis), we’ve conducted some opinion polling on inheritance tax. The polling confirms that inheritance tax really is deeply unpopular, and this isn’t driven by ignorance of how it works. But our polling also suggests that most of the unpopularity is driven by the details, and not the principle, of inheritance tax.

I’ve been curious how much of this polling is led by people not understanding the current over-complicated inheritance tax threshold, which means that inheritance tax in practice usually only applies to a married couple’s assets over £1m. I’ve also been curious whether we’re seeing a principled opposition to inheritance tax in any form, or opposition to inheritance tax as it currently works.

WeThink (formerly Omnisis) very kindly offered to conduct a poll for us without charge. We devised a series of simple questions about inheritance tax that attempted to probe peoples’ views in a reasonably neutral way.

The fairness of the tax

WeThink split the panel into two statistically identical groups.

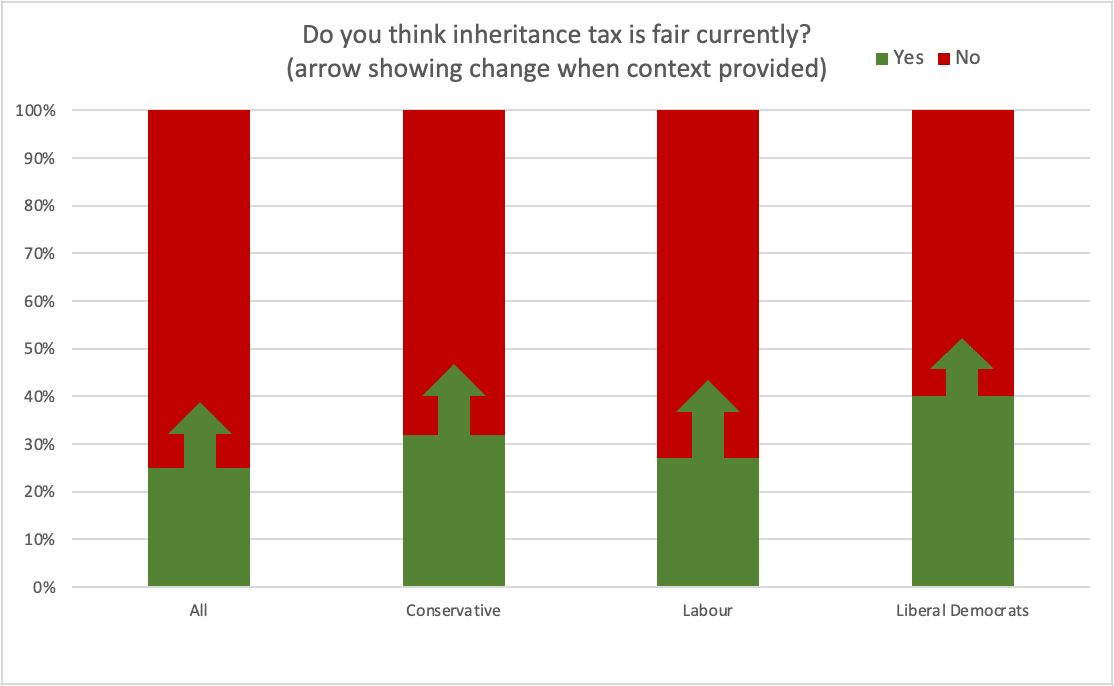

The first set was asked – without any context – a simple question: “Do you think IHT is fair currently?”. The answer was pretty overwhelming:

Surprisingly, Labour voters are even more likely than Conservative voters to believe inheritance tax is unfair.1 Possibly that’s because some of them believe the tax is too low.2

“For most married couples, inheritance tax is only charged where their net assets exceed £1m. The rate is 40%. Do you think IHT is fair currently?“4

That lets us test the hypothesis that people oppose IHT because they wrongly think it will apply to them.

We did indeed see an increase in the percentage believing inheritance tax to be fair, but not a terribly significant increase:

We still see a large majority against the tax; only Lib Dem voters thought inheritance tax fair, even when provided with that context.

I’d conclude from this that we should discard the idea that inheritance tax’s unpopularity is caused by a lack of understanding of the system.

Options for change

Where a respondent said IHT was unfair, we went on to ask what they thought the inheritance tax threshold should be, giving options ranging from no threshold to a £10m threshold. We also included an option for abolition. The intention was to test whether opposition to inheritance tax reflects an absolute principle, or a dislike of the way inheritance tax currently works.

A slim majority – 56% – of the “no context” group preferred changing the threshold to abolition.

An even more slim majority – 53% – of the “context” group preferred changing the threshold to abolition:5

We can draw two conclusions from this. First, some of those saying inheritance tax is unfair believe it unfairly under-taxes estates. Second, at least on this evidence, it’s plausible that if the threshold was set to £2m then only a minority of people would believe inheritance tax to unfairly over-tax.

Finally, for those who said IHT was unfair, but were open to keeping it at a different threshold, we then tested different rates, ranging from 20% to 80%. There was overwhelming support (almost 80%) for reducing the rate to 20%. That was unexpected, and in retrospect we should have given more options below 20%.

Conclusions

Inheritance tax is deeply unpopular – not a surprise.

Some of that unpopularity is caused by a misapprehension as to the level of wealth at which the tax applies. But most of it isn’t – there’s a large majority who believe the tax is unfair even when told that it only applies (broadly speaking) to wealth over £1m.

A much more significant factor appears to be unhappiness with the threshold and/or the rate. It’s plausible that a majority would believe inheritance tax to be fair if the threshold was increased and/or rate reduced. I wouldn’t put it more strongly than that given the limitations of this exercise.

My view remains that we should cut/cap the over-generous reliefs from inheritance tax, and use the revenues to cut the rate. We didn’t ask that in the polling, because I’m unconvinced the complexity of these issues, and the inevitable trade-offs, can be condensed into a one sentence question without pushing an agenda (one way or another). I would prefer that to raising the threshold, because the high (by international standards) 40% rate drives avoidance. A low rate and wide base is the standard boring tax policy response to most problems – and it’s the right one here.

Many thanks to Brian Cooper and Mike Gray at WeThink/Omnisis for their generosity.

Footnotes

I’m not including the breakdowns for the other political parties because the numbers are too small for statistical significance; even the Lib Dem figures should be treated with caution. You can see all the details here. ↩︎

There’s some support for that in the polling detail; about 10% of Labour voters support a rate of inheritance tax of 60% or more; no Conservative voters do. However the statistical validity of individual answers is very low, so I don’t think it’s safe to draw conclusions from this. ↩︎

Note that YouGov gives a “not sure” option and we did not. The question of whether “forced choice” is the best approach has a long history… I have no expertise in this, and was happy to be guided by the experts at WeThink. ↩︎

It’s a very simplified presentation but compressing an explanation of inheritance tax into a sentence is not easy. One obvious criticism is that the question could give the impression that all the assets are taxable the second they hit £1m, and this is a fairly common folk belief about tax thresholds. That was perhaps a mistake on my part. ↩︎

Presumably because people who think inheritance tax is unfair after being presented with the context have already considered and dismissed a £1m threshold ↩︎

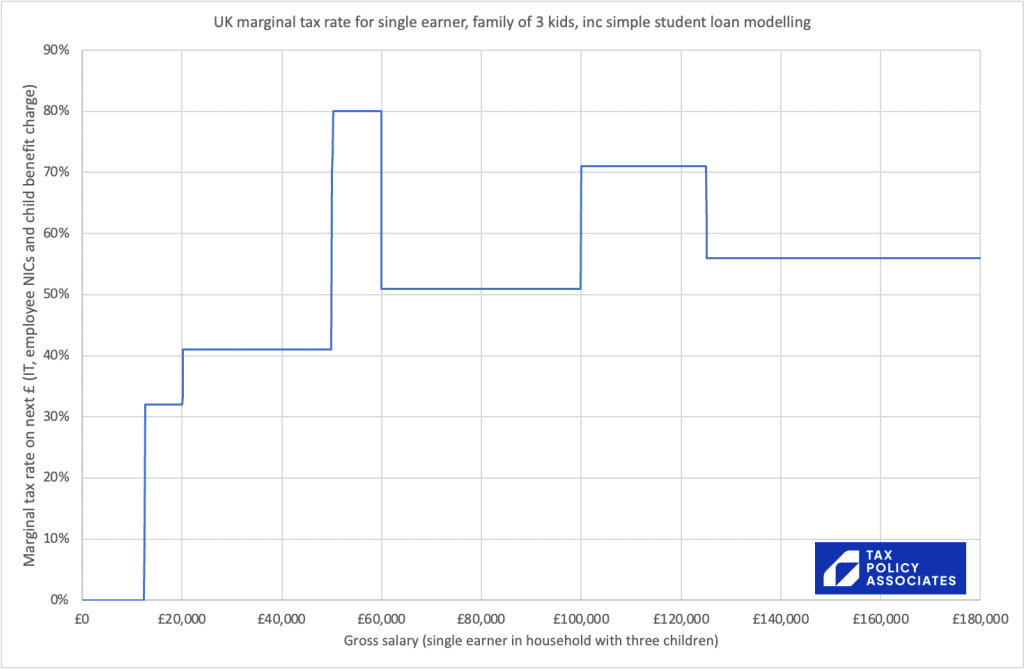

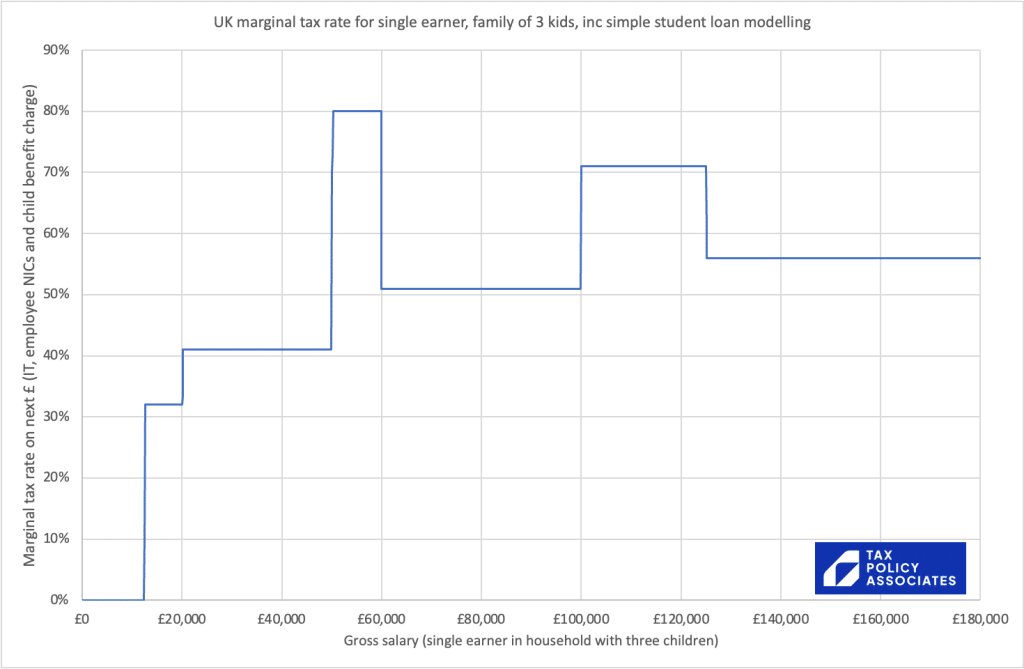

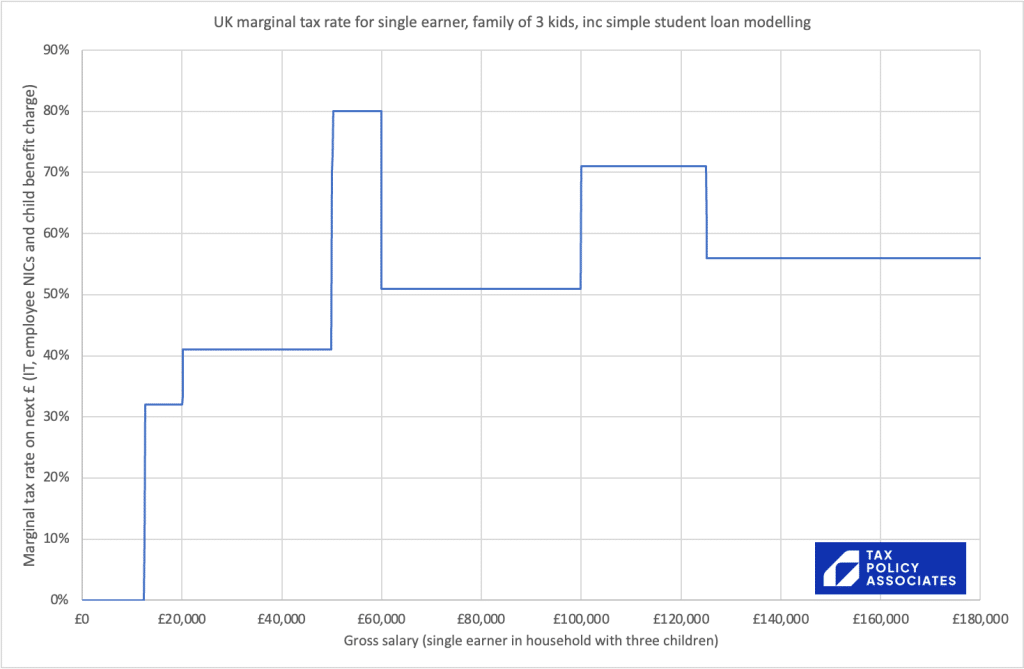

In the last few months we may have given the impression that someone earning £50k, with three children under 18, faced a marginal tax rate of 68%. We may have suggested that this was a disincentive to work, contributed to a shortage of key workers and even held back economic growth. We may have used words like “indefensible” and “disgrace”.

We now realise that our analysis failed to take into account the uprating of child benefit, and in fact the marginal rate in this scenario will be 71%, not 68%. A graduate in this position repaying a student loan can face a marginal rate of 80%.

We also wrongly suggested that someone earning £50k and with six children under 18 faced a marginal rate of 90%. The correct marginal rate is 96%.

We can only apologise for what is an unacceptable error, and would like to make clear for the record that a marginal rate of 71%, 80% or 96% is absolutely fine, and the effect on the individuals involved and the economy as a whole is completely unimportant.

The corrected chart showing the child benefit withdrawal/CBHIC effect:

And including student loan repayments:

The spreadsheet model is available here. Note these figures are for the UK excluding Scotland. The Scottish rates are higher.

The UK’s high marginal tax rates on people earning £50k are a disincentive to work. They’re made worse by the way a large chunk of the tax is collected – the “high income child benefit charge” (HICBC).

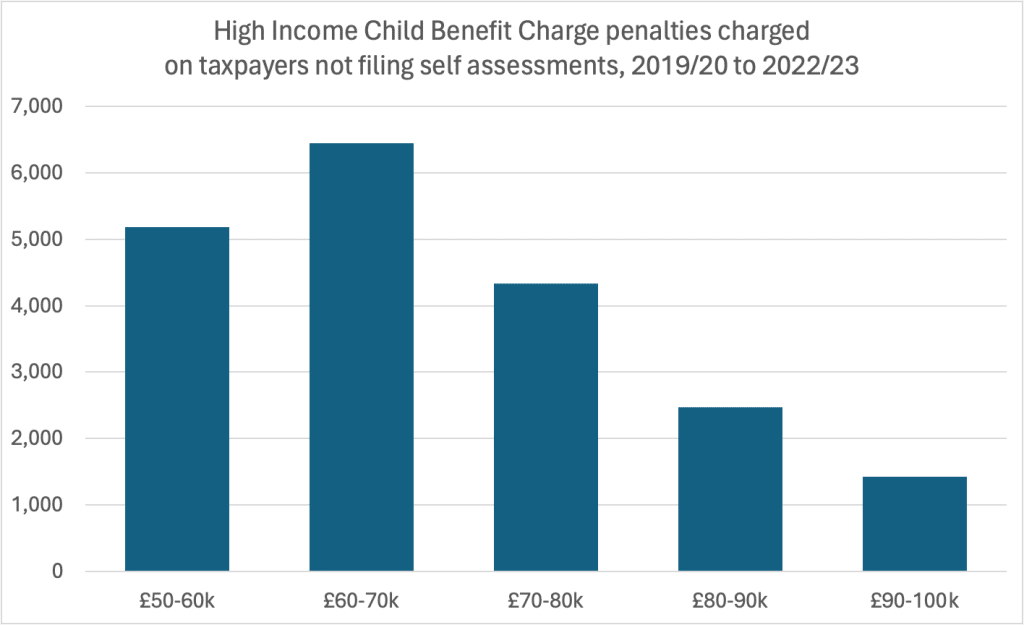

The HICBC creates a “tax trap” for employees who usually wouldn’t file a tax return. If they earn £50k, and they or their partner claims child benefit, they have an immediate requirement to file and pay the HICBC. It’s easy to get that wrong. In the last four years 19,000 did, and were hit with a penalty of up to 30%.

Tax systems shouldn’t have marginal rates of over 70%, and shouldn’t have “traps” that can catch the unwary. The HICBC should be abolished.

UPDATE: note that the income point where child benefit starts to be clawed back was moved from £50k to £60k in the Spring 2024 Budget. That’s an improvement – but all the problems of HICBC we discuss in this article stil remain.

The chart above shows the marginal rate of income tax paid by a UK taxpayer with three children under 18. That’s a 71% marginal tax rate between £50k and £60k.1

The high marginal rate results from George Osborne’s 2013 decision to withdraw child benefit from people earning a “high income” – £50,000. If the £50k threshold had been upgraded with inflation it would be £67,000 now – but it wasn’t. Around one in three households now include someone earning £50,000 – it’s not a “high income”.

How the HICBC works

Whatever we think of the politics of withdrawing child benefit from “high earners”, the way that it was done was a mess.

UK tax generally applies to individuals.2 I’m taxed on my income; my wife is taxed on hers. The benefits system on the other hand, looks at overall household income and capital. The decision was taken to withdraw child benefit based on a mixture of both – if the highest earner in a household hit £50,000 then child benefit would start to be clawed back, and if it hit £60,000 then all child benefit would be withdrawn.3

The challenge was that, whilst HMRC knows how much I earn, it doesn’t have a way to see how much the highest earning person in my household earns. So child benefit couldn’t “automatically” be clawed back.

The highly bureaucratic answer to this challenge was to outsource all the work to taxpayers. Osborne created a new tax – the HICBC – and required people to self-assess it in their tax return. It’s a bad answer because most people earning £50,000 are employees, and don’t file a tax return. So people would have to realise they had to start filing a tax return just because they claimed “too much” child benefit, and notify HMRC.

If your household has children under 18 and someone earning £50k, then you have three choices:

Don’t claim child benefit.

Register for child benefit but opt not to receive it.

Register for child benefit, receive it, and then pay some/all of it back through a special tax, the High Income Child Benefit Charge.

These are difficult choices with not-at-all-obvious outcomes:

The first choice – not claiming child benefit – seems the easiest thing to do, but is actually a mistake, because it means a non-working parent can lose their national insurance entitlement.4 It’s a mistake I made – and as a result my wife lost some pension entitlement. The Government pledged to fix this back in April, but nothing’s happened since.5

The second is the “correct” answer if the highest earner in a household makes £60k+ but not so great an answer if they earn £50-60k, because they’re then giving up all their child benefit unnecessarily.

The third is a pretty bad answer, but if the highest earner makes between £50k and £60k then it’s the only way to receive some child benefit. If you’re already on self assessment and filing online, then paying the HICBC is fairly easy – you just tick a box and type in the amount of child benefit claimed. But if, like most employed people, you’re not on self assessment, then you’ll have to register for self assessment. If you don’t, you’re breaking the law.

These choices all get more complicated if income unexpectedly changes during a year, or a couple separate, or a couple move in together.

And lots of people get it wrong. Sometimes in the Dan’s-wife-loses-some-of-her-pension way. And sometimes in failing to realise you now have to register for self assessment and file/pay the HICBC.

How many people get it wrong?

Almost 20,000 people who weren’t on self assessment were hit with penalties from 2019/2020 to 2022/23 for not realising6 they should be paying the HICBC:7

We don’t have data on the amount of the penalties, but likely it was several hundred pounds.8

This is after an HMRC review of HICBC penalties in 2018 – before then, there were about twice as many penalties issued.9

HMRC has sent millions of letters to people warning them about the HICBC, but not everyone affected has received one. HMRC has pursued people for penalties even when they weren’t adequately informed; tax tribunals have been reasonablysympathetic to taxpayers.10

What should happen?

Marginal rates of over 60% should be regarded as unacceptable. I’d abolish the HICBC on this ground alone.

But the way the HICBC was implemented is an illustration of how a tax system shouldn’t work. A wholly disproportionate level of complication for people on not-very-high incomes doing something as ordinary as having children, where the total amount of tax at stake is so small (likely around £1bn).

The Government has promised to improve things by enabling HICBC to be collected through PAYE, removing the need to file a self assessment form. But taxpayers would still have to notify HMRC this, and still have to make surprisingly difficult choice as to how to proceed.

I’d hope abolishing the HICBC would appeal to both a Conservative Party that regards high marginal rates as an anathema, and a Labour Party that’s always supported the principle of universal child benefit. The amount of money at stake is small, and if the government wished to recoup the cost from people earning £50k, that could be easily done in a less damaging way (for example by upgrading the higher rate income tax threshold slightly more slowly than it otherwise would).

There are a number of cases where it’s more complicated than this. For example: where the high earning parent doesn’t know if the other parent claims child benefit, or where child benefit is claimed by someone outside the household but who provides the household with financial support. I’m going to ignore these issues for now, but they’re important for the people affected. ↩︎

It also means the child won’t automatically receive a national insurance number when they turn 16 ↩︎

Thanks to Miro in the comments for reminding me of this. ↩︎

My assumption is that it was almost always an accident, because I think it would be obvious to most people who understood the system that they would be caught ↩︎

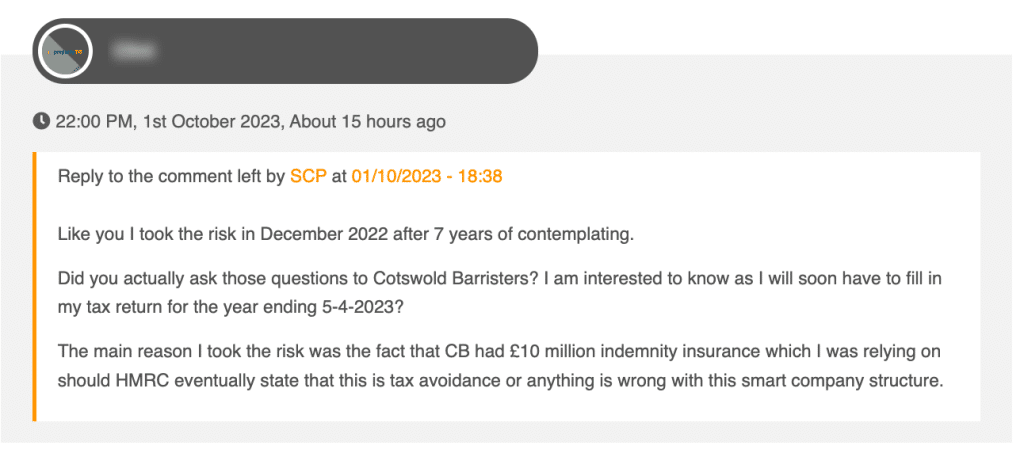

We’ve reviewed multiple Property118 client files to investigate how they implement their tax avoidance scheme. We’ve found that the scheme is implemented so badly that our previous criticism is beside the point – a key drafting error means that the scheme fails immediately. It also appears that their clients receive templated “advice” which fails to identify key issues, or warn clients about the legal and tax risks they are running.

We previously concluded that the structure had significant technical flaws which meant that it likely did not work. However, this analysis assumed the structure was correctly implemented. It isn’t. We have now reviewed complete sets of Property118 advice and documentation, and there are very significant failings in both legal implementation and in Property118’s advice.1

The key problems

Here are the key problems:

The most important document implementing the structure appears to be defective. A trust deed that is supposed to create a bare trust actually reserves rights for the landlord, and so likely creates a taxable settlement. This has complex and highly deleterious consequences for the landlord.

There is another series of drafting errors around the indemnity which supposedly enables a company to claim mortgage interest tax relief. The documents are contradictory, and either don’t create an indemnity at all, or accidentally create a stream of taxable interest payments.

A key tax consequence is whether the structure is disclosable to HMRC under DOTAS. It appears that Property118’s associated barristers chambers, “Cotswold Barristers” never considered this point until we raised it. The head of Cotswolds Barristers, Mark Smith, then published an article that the HMRC official who introduced DOTAS described as “hopelessly wrong”. Our view is that anyone who wrote that article is not competent to advise on tax.

Cotswold Barristers appear to never advise on the application of anti-avoidance rules to their structure.

Cotswold Barristers don’t appear to review their clients’ mortgage terms and conditions, despite promoting their scheme on the basis it is compliant with mortgage T&Cs.

Cotswold Barristers have provided entirely incorrect technical advice to clients they’ve advised to use a “mixed partnership” structure. The advice missed a key section of the legislation.

The documents and advice are almost identical for all clients – Mark Smith and Property118 use very standardised templates.

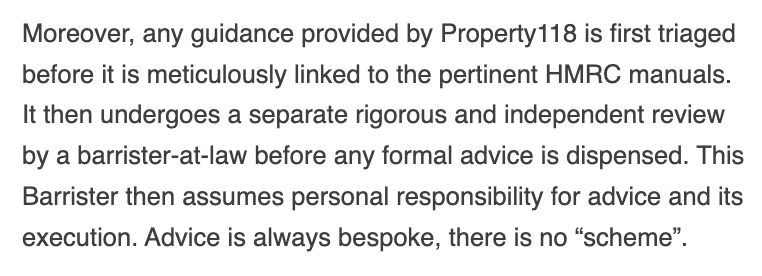

Cotswold Barristers appear to mostly “rubber stamp” advice provided by unqualified “tax consultants” working for Property118. Nevertheless, fees of £30-70k are typically charged for implementing the structure.

Tax advice usually draws clients’ attention to risks, whether large or small. Cotswold Barristers never mention risks of any kind, legal or tax.

Instead, the clients are told that the barristers have £10m of insurance “per client” and therefore the clients are “shielded from financial risk”. This is not true. It’s not £10m “per client” – it’s effectively £10m across all 1,000+ clients. And in any case, professional insurance does not “shield clients from financial risk”. To access the insurance, clients have to successfully sue the barrister for negligence – which is far from straightforward.

It is unclear whether Mark Smith, the only named member of Cotswold Barristers, has the qualifications or experience to advise on tax.

We explain these points further below.

If Property118 have really sold their scheme 1,000 times, and the documents are as standardised as they appear to be, then all 1,000 schemes will have failed. Not just failed because of the technical analysis in our previous article, but failed because of incompetent implementation. We believe many of the clients entered into the scheme on the basis of assurances about Mark Smith’s insurance which were false.

Given the scale of the problem, we believe it’s important that taxpayers and HMRC resolve these issues now, rather than years later, when the situation could become a loan charge-style crisis. We will also be asking the Bar Standards Board to investigate.

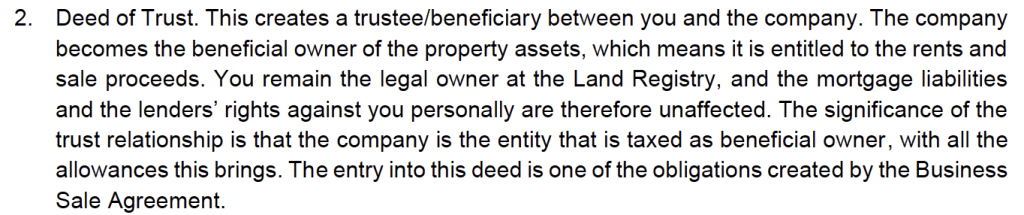

Central to the Property118 scheme is that the landlords declare a trust over their rental properties in favour of a newly incorporated company. Here’s the description of the deed of trust in Mark Smith’s advice:

So this is intended to be a “bare trust” – the company/beneficiary holds absolutely and the landlords are mere trustees. The company would then be taxed more-or-less as if it held the properties directly.

The first operative clause in the trust deed intends to achieve that:

But then, three clauses later, we see this::

This clause has astonished every lawyer who’s seen it. It enables the landlords/trustees to reacquire the property for no payment – but that’s entirely incompatible with a bare trust, where beneficiary absolutely owns the property.2

We have spoken to a range of trust and trust tax experts, and we believe there are three principal possibilities:3

Clause 2.4 gives the landlord/settlor an interest in the trust, which means it is a settlement for tax purposes. This seems the most likely outcome.4

The trust is a bare trust, but Clause 2.4 gives the landlord/trustee an option to reacquire the beneficial interest at any time. We believe this is unlikely given that clause 2.4 is part of the trust, not an ancillary contract.

The trust could be void and/or ineffective for tax purposes. We believe this is unlikely, given that the meaning of the document is clear, even if its tax effect is undesirable.

The first two scenarios result in an up-front capital gains tax charge as if the properties were sold for market value, with no possibility of incorporation relief.5 A settlement would also give rise to complex ongoing tax issues.6. The third scenario might be a welcome one, as possibly it provides a way to take the position that the whole transaction had no effect.7 In all three scenarios there is no possibility of the company claiming a tax deduction for mortgage interest, because you don’t “look through” a settlement in the way you look through a bare trust.

However, regardless of which of these three scenarios apply, none result in the structure intended by Property118 and Cotswold Barristers. The scheme is dead on arrival, and our previous analysis of the structure is no longer necessary (or indeed relevant);8

It is not uncommon for tax avoidance schemes to fail because of incorrect implementation. For example, the Vardy stamp duty/SDLT avoidance scheme involved an unlimited company paying a dividend ‘in specie’ of the real estate itself, and claiming that the dividend was outside SDLT. This was probably destined to fail, but it didn’t even get that far. The dividend wasn’t properly declared and was unlawful.

So far as we are aware, on the basis of the Property118 documents we’ve reviewed and the documents reviewed by advisers we’ve spoken to, this error is present in all Property118 documentation.

We do not believe a reasonably competent tax lawyer would have drafted a trust deed in this manner – it is basic trust law that the beneficiary of a bare trust has an absolute entitlement to the trust property, and no other party has any entitlement. The drafting therefore suggests that Cotswold Barristers may have been negligent.

The misdrafted indemnity

The central point of the structure is to solve the “section 24” limitation on landlords claiming mortgage interest tax relief. The idea is that the landlord continues making interest payments to the mortgage lender, but these are funded by the company, which can claim a tax deduction.

Here is how Mark Smith describes this in the “client care” letter he sends to accompany the draft documents:

The drafting to achieve this is a mess of confused and contradictory provisions.9

First, the Business Sale Agreement contains no indemnity. Instead it says:

The definition of “Liabilities” lists the outstanding mortgages. But law students usually learn in their first contract law class that English law doesn’t permit the purchase of liabilities. In some circumstances you can buy assets in consideration for an assumption of liabilities – but that won’t work here, because the mortgage lender won’t permit the company to assume the liabilities.10

The sale contract for the properties contradicts this:

In other words, the landlords continue to owe the mortgage to the lender (as they must), but the company now owes an equivalent debt to the landlords. That is a sensible approach, but legally different from an indemnity. It creates an obligation for the company to pay a principal amount to the landlord, but doesn’t create any obligation for the company to cover the landlord’s interest payments

There are then three very confusing clauses:

First, an attorney/delegation clause in the trust deed, under which the landlords appoint the company as their attorney to make interest payments on their behalf:

This normally won’t be permitted by the terms of the mortgage; only the borrower can make payments, and as a practical matter a lender would usually reject payments from another party. We don’t know why it’s included.

Then an indemnity in the trust document:

Does this cover the landlord’s mortgage interest payments? Unclear.11

There is then an “agency agreement” with recitals as follows:

Unusually, recital B is the only operative term in the contract12

So, to recap: under the original mortgage, landlord has an obligation to pay interest to the mortgage lender. Under Clause 2.2 of the trust deed, the landlord delegates the making of these mortgage payments to the company. Under the agency agreement, the company then appoints the landlord as its agent to make the same payments – back where it started. We have no idea what the point of this is. Neither provision will have any tax effect – agency/delegation doesn’t normally change the tax character of a payment (because a payment by an agent or delegate is, for most tax purposes, regarded as made by the principal).

It’s a mess.

However, landlords may be better off if these provisions don’t create an obligation for the company to make indemnity payments in respect of the mortgage interest. First, given the debt created by the sale contract, the payments are likely to be “interest”13 for tax purposes, subject to 20% withholding tax, and additional income tax in the hands of the landlord. Second, the payments are unlikely to be deductible for the company (they are probably not payments under a loan relationship; if they are, the existence of a tax main purpose means they will be non-deductible).

In our view, a reasonably competent lawyer would not have drafted such a web of contradictory and confused clauses.

Incompetent advice on DOTAS

As we will discuss below, Cotswold Barristers rarely provide any advice on any tax issue. One of the many issues they do not discuss is DOTAS – the rules requiring a promoter of a tax avoidance structure to disclose it to HMRC.

We criticised this in our original analysis. Six weeks later, Mark Smith responded with an article that provided technical justification for a claim that DOTAS does not apply (link is to an archived version; it’s no longer on the Property118 website). This is important, because it is the only technical analysis we or any of our sources have seen from Mark Smith, and it therefore lets us assess his competence.

Smith’s article was reviewed by Ray McCann, a retired senior HMRC official. When Ray was at HMRC, he led the introduction of DOTAS. Ray described Smith’s article as “hopelessly wrong”.

Smith made the following serious mistakes, which call into question his basic competence.

The article contains a lengthy argument that the scheme is not “tax avoidance”. This is technically irrelevant. DOTAS turns on whether an arrangement’s “main benefits” include obtaining a tax advantage. It is reasonably clear that tax is one of the main benefits of the Property118 structure; indeed it is not obvious what the other benefits are.14 Smith conceded that there is a tax main benefit, but in such a way that a layperson will not notice the importance of the concession.15

Mark Smith said Property118 was not a promoter because “CB is solely responsible for the design of the [structure], in the sense that any issues arising from the design would lead solely to CB being held accountable”. This is not correct. Property118 makes an initial structural proposal to clients, and therefore is “to any extent” responsible for the design of the scheme. Who is “held responsible” is irrelevant (although why Smith thinks Property118 wouldn’t be legally responsible for their own actions is a mystery).

It appears Mark Smith believed that he could not be a promoter because of legal privilege. But there is no absolute DOTAS exemption for lawyers; the question is whether the “prescribed information” required to be delivered under DOTAS would breach legal privilege. Given the generic nature of the scheme, it is possible (depending on the precise facts) that DOTAS reporting would not in fact breach legal privilege, and Cotswold Barrister and/or Mark Smith is a promoter.

Property118 markets, online and in person, a scheme that has a well-established design – and that makes them a promoter. Smith refers to the Curzon case, but that involved a mere administrator – it’s irrelevant. Anyone marketing a scheme will almost always be a promoter for DOTAS purposes.

Smith then concluded the scheme is an “in-house” scheme. This is a complete misunderstanding of the term. An “in-house” scheme is where a company devices and implements its own avoidance scheme. That is not at all what is happening.16

Mark Smith’s analysis therefore contained a series of elementary but serious mistakes. We believe it was incompetent. If Smith’s article is the basis on which he concluded DOTAS didn’t apply, or indeed if he had never previously considered DOTAS, then in our opinion he fell well below the standard of a reasonable tax barrister, and was negligent. It also leads us to believe he is not competent to advise on tax.

Smith’s article was heavily criticised by Ray McCann and others. At some point Smith reacted to this by silently rewriting his article, and removing the hopeless arguments that the scheme had no promoter and was an “in-house” scheme. Smith now relies upon three claims:

The confidentiality hallmark doesn’t apply because they publish the scheme details widely. That’s not what Property118 told us – when we asked about the details of the structure we were told it was “valuable intellectual property”

It isn’t a “standardised tax product” because they look at each case individually. But the documents and advice we’ve seen from Property118 and Cotswold Barristers have been completely standardised.

There isn’t a “premium fee”. That is clearly incorrect for the “bridge loan” structure, where they charge a 1% “arrangement fee”. It also seems incorrect for the rest of their structure, where the fee varies from £30k to as high as £90k based upon the size of the landlord’s portfolio.

HMRC have never raised this point across at least 20 “compliance checks”. We expect that is because they were not presented with the full facts.19. Less Tax for Landlords told us their structure had been seen by HMRC on 40 occasions – but when HMRC became aware of the structure, they concluded it should have been disclosed. In any event, “nobody else has complained” is not a defence in law.

Smith doesn’t mention the “financial product” hallmark. This is a serious error. The bridge loanobviously is a financial product. The indemnity enabling the company to achieve a tax deduction is intended to give rise to a financial obligation for accounting purposes (or there would be no deduction) and is therefore a financial product. The loan and indemnity have the main benefit of creating a tax advantage, and wouldn’t have been entered into but for the tax advantage. The bridge loan and trust/indemnity are contrived and abnormal steps. The financial product hallmark therefore likely applies. We expect Smith failed to consider it because of his misunderstanding of the hallmark (evidenced in his original article).

This is therefore significantly less incompetent than Smith’s original article, but still contains bad errors of fact and law.

The consequence of DOTAS applying is serious for Property118 and (if he is a promoter) Mark Smith – penalties of up to £1m. There are also serious consequences for their clients: HMRC may have up to 20 years to investigate their tax affairs.

There is no 15% rule in that Act or in any HMRC guidance of which we are aware.

The mixed partnership rules also apply – broadly speaking, they counteract the diversion of income to corporate members of partnerships and LLPs. The 15% reference is perhaps meant to suggest that the allocation to the corporate member reflects an arm’s length return on services provided, and is therefore disregarded under section 850C(15) ITTOIA 2005. But where the services are personally provided by an individual member of the LLP then s850C(17) disapplies subsection 15. You can’t, in fact, allocate even 1% to the corporate member.

The failure to consider subsection 17 was in our view incompetent. A reasonable adviser reading the legislation would surely not have made that mistake.20

Advice which is “templated” and fails to cover key points

Cotswold Barristers (which in practice means Mark Smith) advise their landlord client directly under the Bar’s public access scheme.

We have seen no evidence of any of this. The pattern we have seen, again and again, is that Property118 and Cotswold Barristers use standardised documents and provide highly standardised advice.22 In the cases we have reviewed, the written advice consists of four standardised communications:

The initial proposal

The client pays £400 for an initial consultation.

They then receive a document from a “tax consultant” at Property118 (not a lawyer, accountant or CIOT/CTA qualified tax adviser) entitled “Incorporation and Smart Company structuring”.

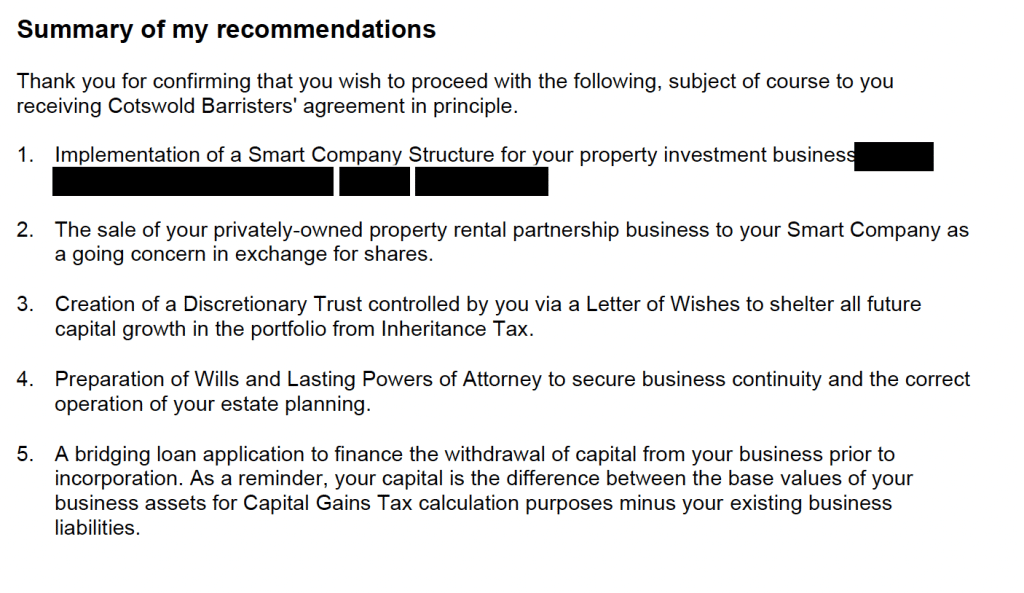

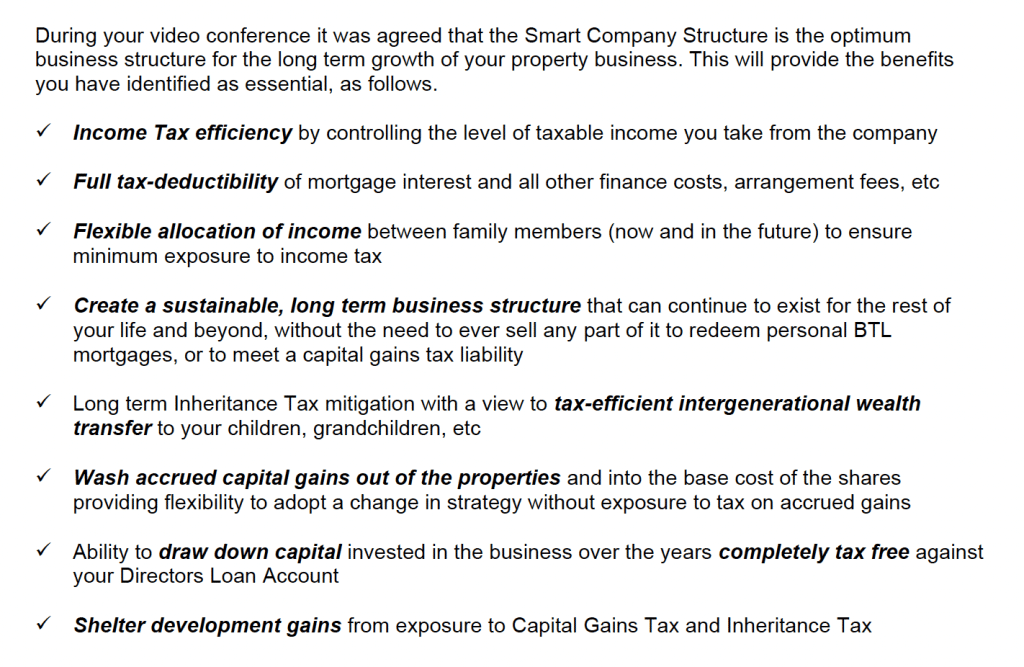

This is a glossy document setting out the proposed structure, in a standardised form, including recommendations almost identical to this:23

It adds:

The document then sells the benefits of the structure, which are almost entirely tax benefits:

The fact there is an obvious tax “main purpose” means a multitude of anti-avoidance rules should be considered; there is no evidence they are considered at all.

The only tax advice contained in the document is a short and generic summary of CGT and SDLT relief upon incorporation.

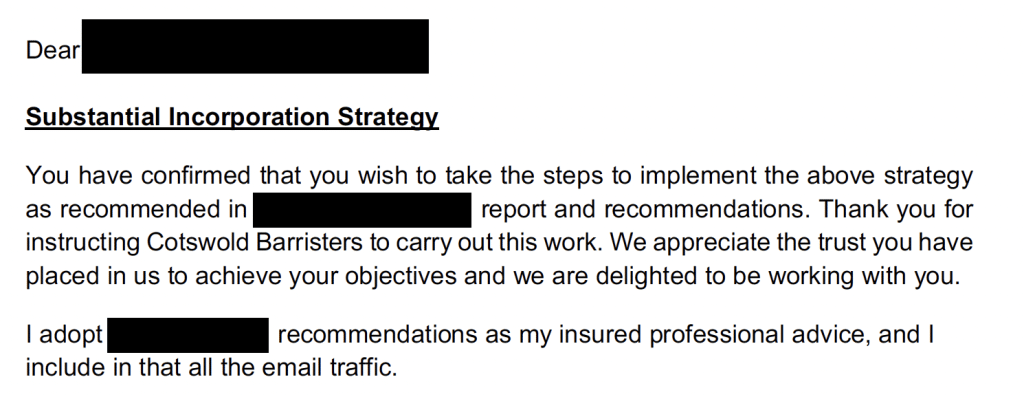

2. Cotswold Barristers confirmation

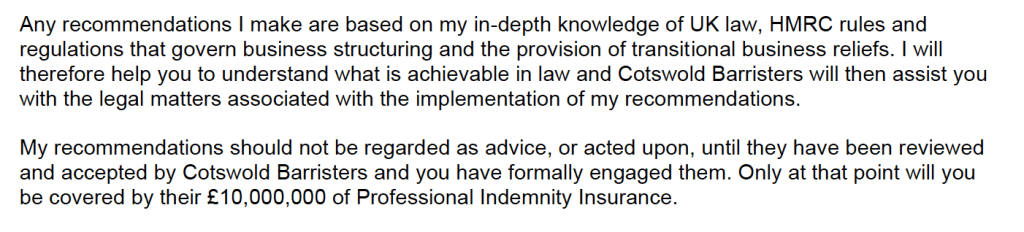

If the client proceeds to instruct P118, they receive a letter from Mark Smith at Cotswold Barristers saying that he agrees with the recommendations in the initial proposal:

The letter then sets out a generic description of the structure and Smith’s terms of business.

There is no advice on any additional points beyond those in the original communication. We are not aware of any case where Mark Smith departs from the original Property118 advice – he appears to always “rubber stamp” the advice of the unqualified “tax consultant”.

3. Draft documents

The client then receives draft transaction documents, plus a one page cover letter entitled “Model client care letter” written by Mark Smith of Cotswold Barristers.

It explains the documents but contains no advice on the tax consequences of the arrangement. We excerpted above the incorrect descriptions of the trust deed and business sale agreement. Similar short descriptions are provided of the other documents.

4. Post-completion letter

After the documents are signed, Mark Smith sends the client another “client care letter” confirming that the transaction has completed. The letter contains a FAQ and an explanation of the structure for conveyancers.

The letter is standardised, and it appears from the documents we have seen that only the salutation at the top of the page changes from client to client. The name of the new company is written as “(company name and number)”. The letter mentions the requirement to submit an ATED return “If any of the properties are worth more than £500,000”, even though Cotswold Barristers know that (in the cases we saw) they are worth significantly more than that.

The most hilarious example of standardisation is:

No advice is provided to the client in this letter.

Missing advice

It’s useful to look again at the original promises for the Property118 structure, made in the first communication:

Very little of this is covered by advice from Property118 or Cotswold Barristers. As far as we are aware, they never provide proper advice on the following key points:

Does the trust default the mortgage?

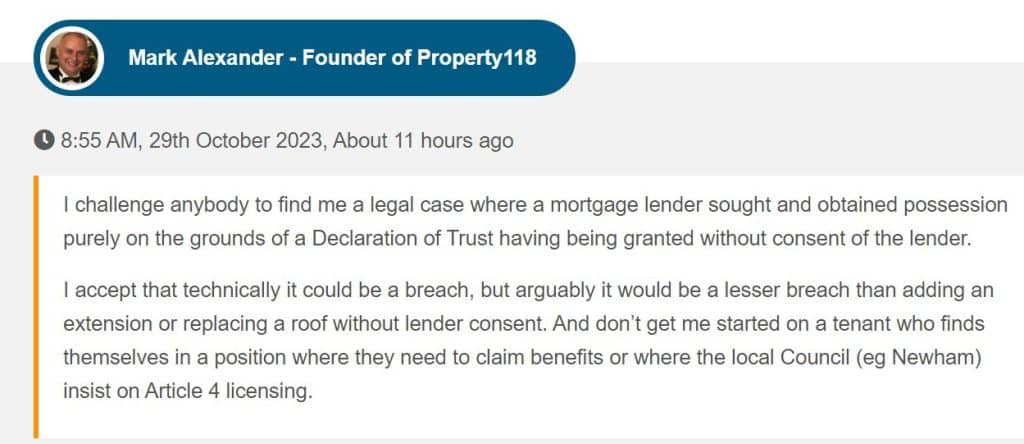

This is a hugely significant point for landlords. Property118 are very reassuring when making presentations, but when it comes to specific clients we have seen no evidence of any advice on this point. Most of their clients have multiple mortgages over different properties. There is no evidence of any review of the mortgage T&Cs in either the original Property118 advice or the Mark Smith letters. Mark Alexander now seems to concede that the structure legally defaults their clients mortgages:

A “technical” breach of mortgage T&Cs will in most cases entitle the bank to call a default and demand repayment.

Does CGT incorporation relief apply?

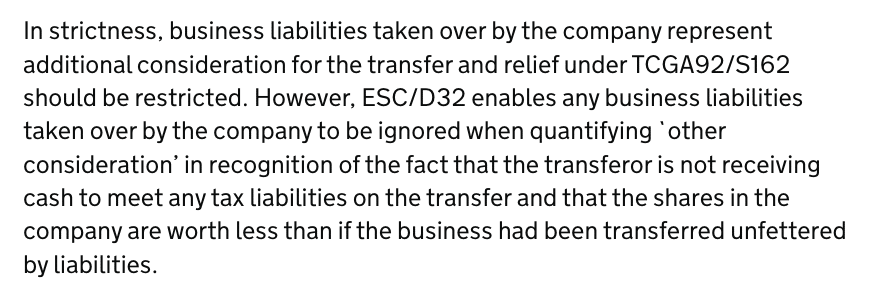

The first letter, from Property118, says it does, based upon a simple analysis of the facts. We would expect a barrister to then consider the technical analysis and, in particular, whether the fact legal title is not transferred means that there is a “sale of a business as a going concern”, and whether ESC D32 can be relied upon given that the transaction is tax-motivated.

There is no evidence of consideration of these points.

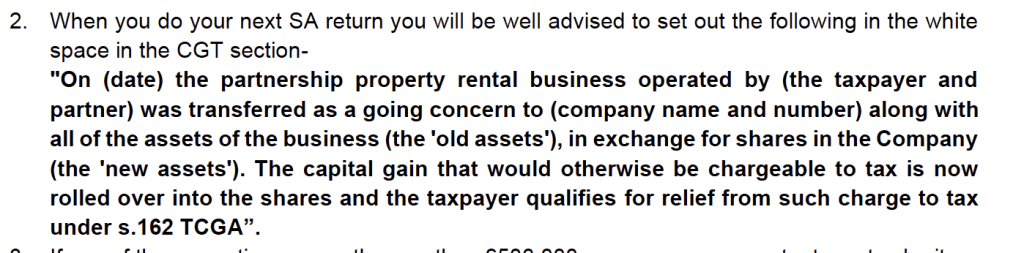

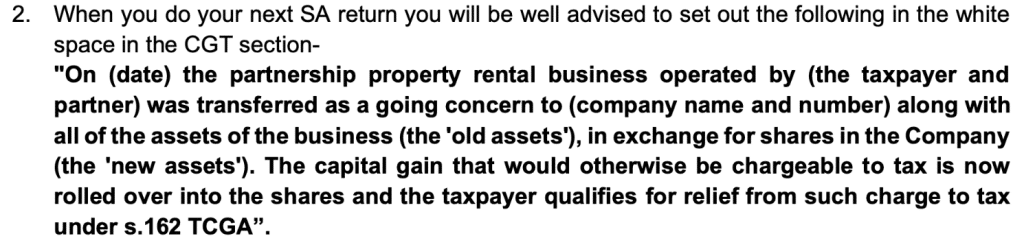

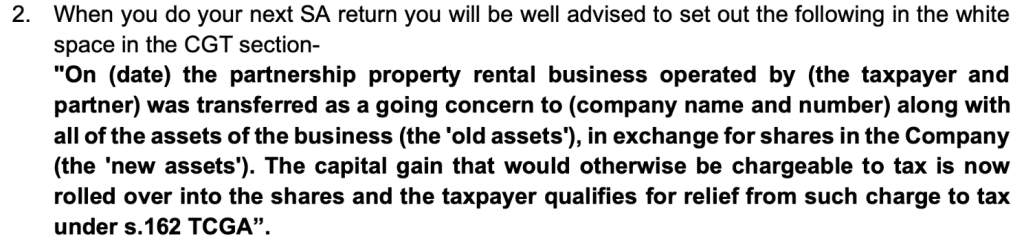

Cotswold Barristers make the serious error of advising clients to include incorrect disclosure in the client’s self assessment return:

This is an entirely incorrect description of the sale agreement, because it is a sale in consideration for shares plus the assumption of debt. That is highly material, because on the face of the legislation it prevents incorporation relief from applying. Reliance could then be placed on an HMRC extra-statutory concession, but that isn’t available in tax avoidance cases.

The description also fails to mention that the business is not being sold conventionally, but rather a trust is being declared.

The most favourable interpretation is that this is a serious error. The less favourable interpretation is that this is intentionally providing incomplete disclosure to HMRC to avoid alerting HMRC to the fact that incorporation relief may not apply.

In any event, the intended incorporation relief position is of merely academic interest given that the trust appears to be a settlement, which means an up-front CGT charge with no prospect of relief.

Does SDLT “partnership relief” apply?

Property118 and Cotswold Barristers claim that in many cases where a married couple jointly run a property rental business, they can retrospectively claim that a partnership always existed, and therefore incorporation benefits from SDLT rules that can provide relief for partnerships incorporating.

Technically it is very doubtful a partnership exists in most normal circumstances.

We see no evidence of Property118 and Cotswold Barristers ever carrying out a fact specific analysis before the strategy is recommended. The “strategy” is always set out in the first standardised advice note prepared by Property118, before Cotswold Barristers are engaged, and before any substantive work is undertaken. We have not seen any evidence of any legal analysis of this point subsequently.

Can the company claim a tax deduction for the mortgage interest?

The first letter, from Property118 says it can (see the second tick mark in the excerpt above). But the basis for this is never explained (and, for the reasons we explain around the misdrafted indemnity, in fact the company can’t claim a deduction).

The fact the trust appears to be a settlement further complicates this; naturally none of the advice from Property118/Cotswold Barristers considers that.

Is it correct that the “growth shares” issued by the company have a valuation of zero?

Property118’s structure involves issuing “growth shares” which carry an entitlement to all future capital gains of the company. The claim is that they initially have a valuation of zero. That is highly questionable. However neither Property118 nor Cotswold Barristers appears to undertake any valuation exercise to justify the claim.

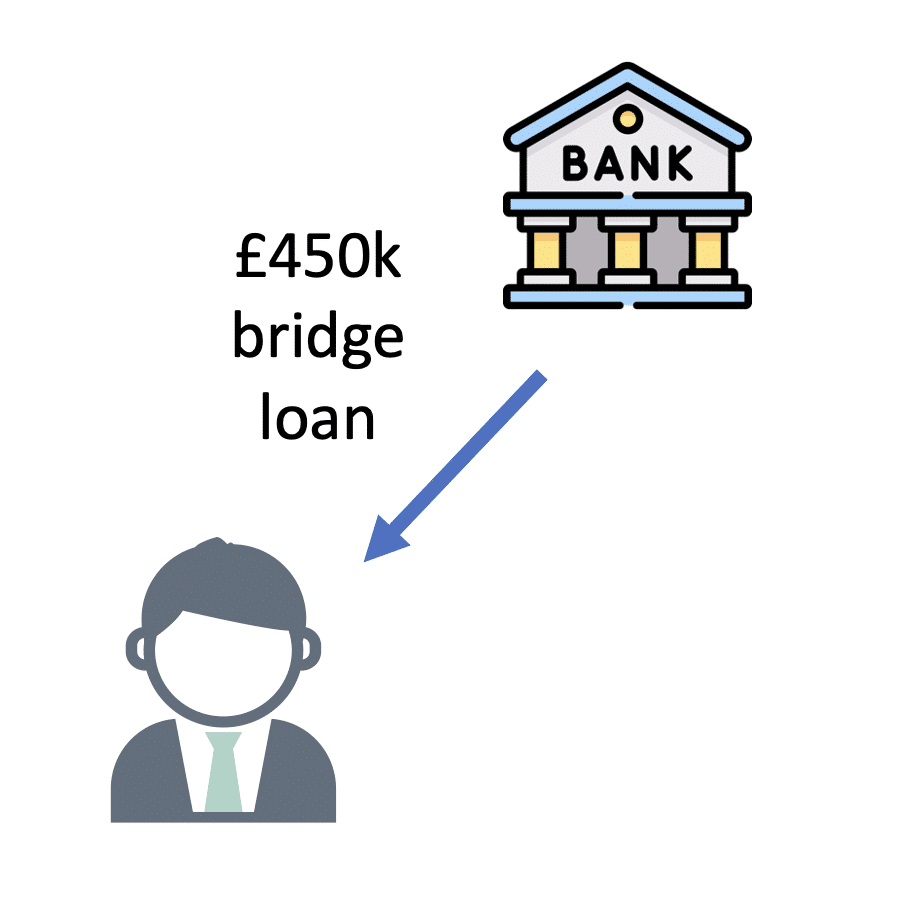

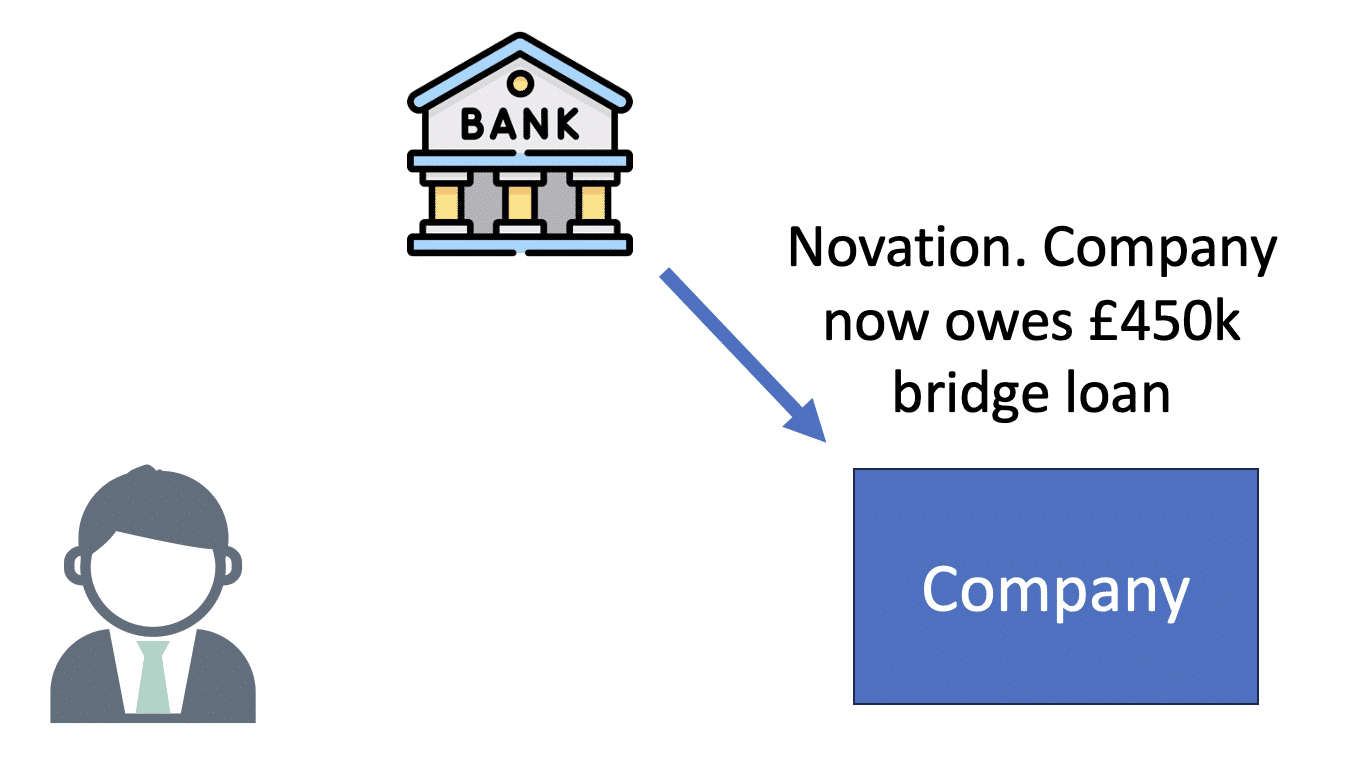

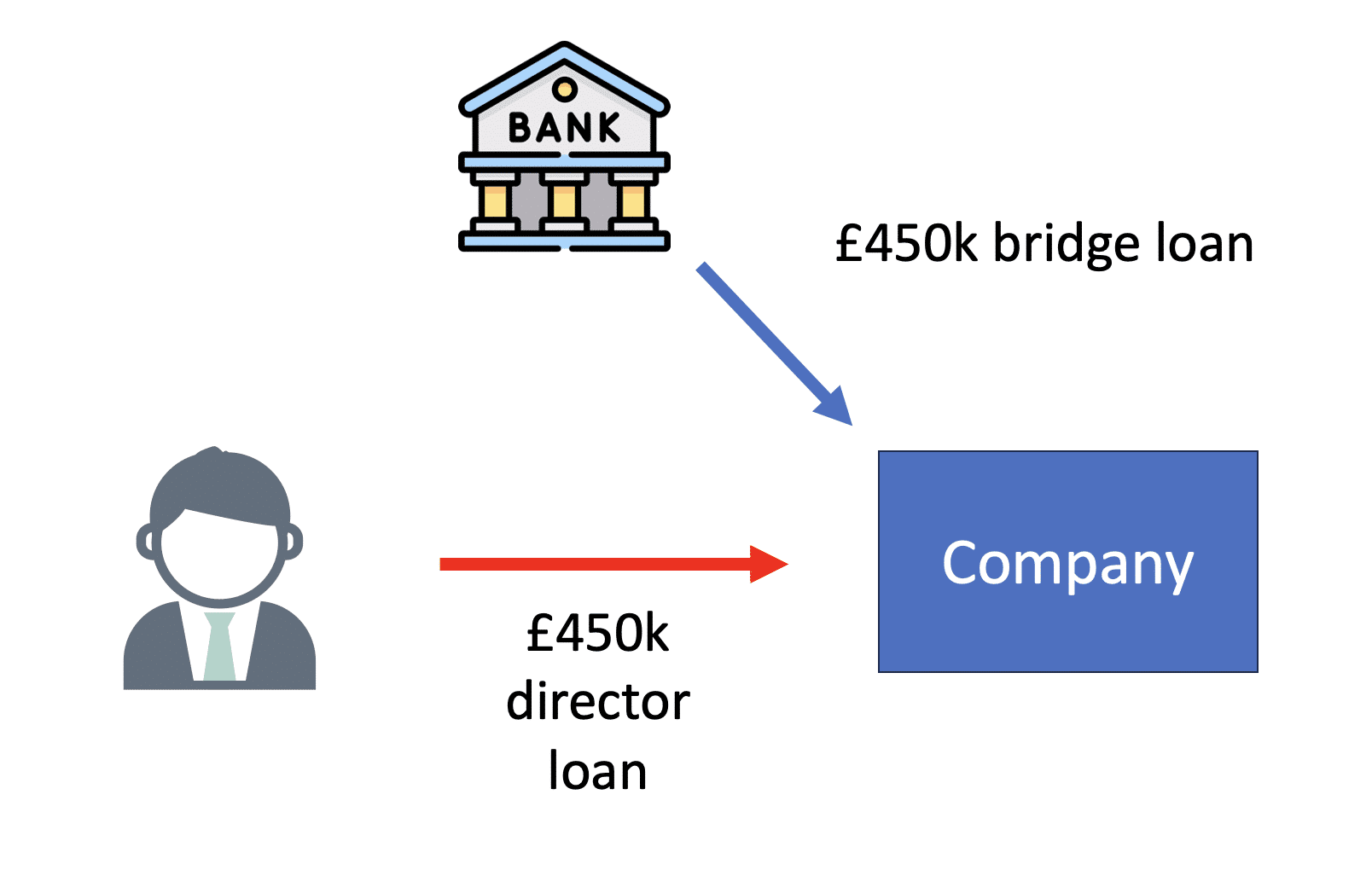

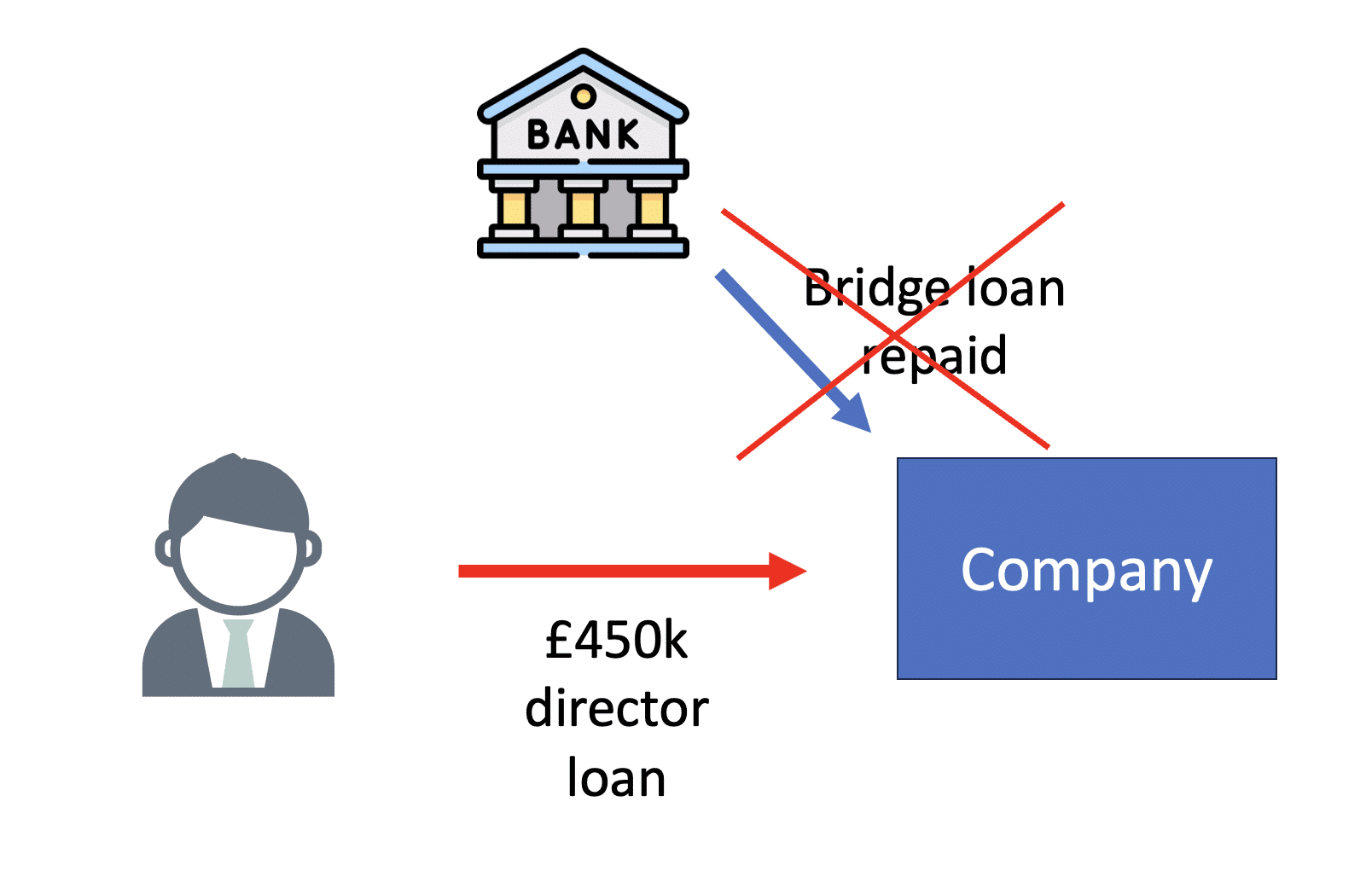

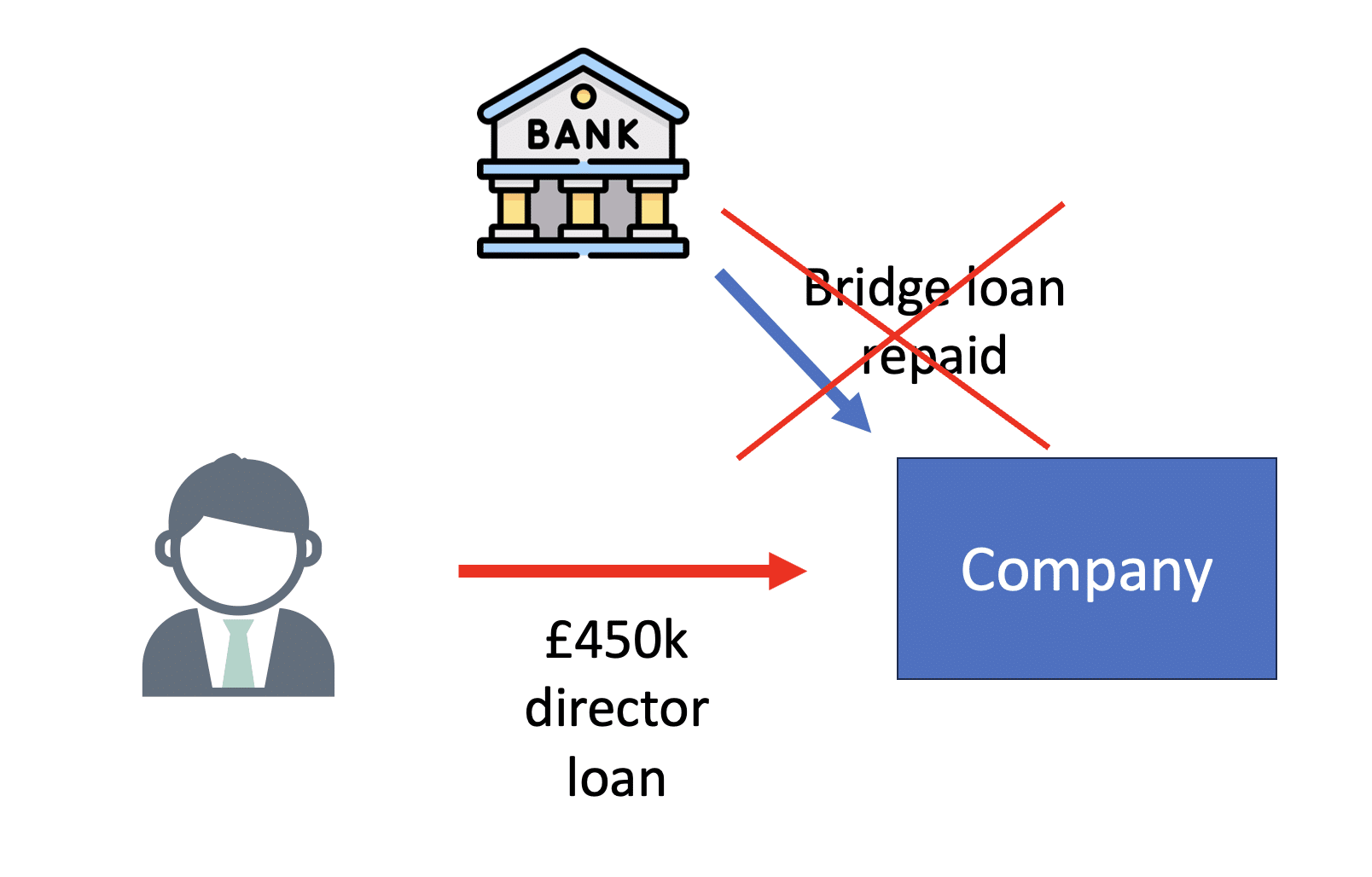

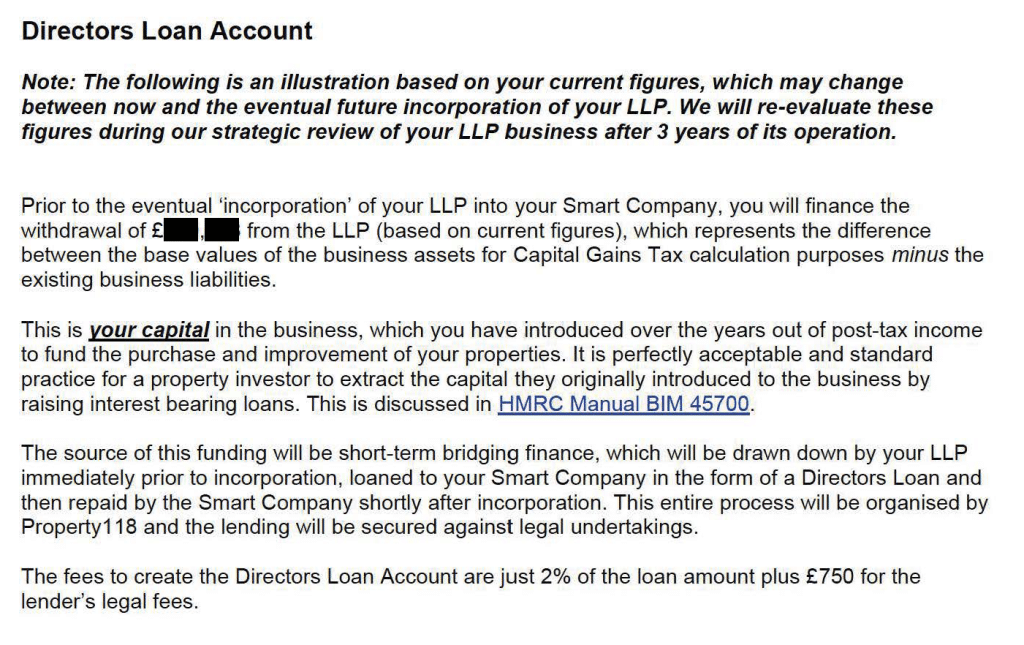

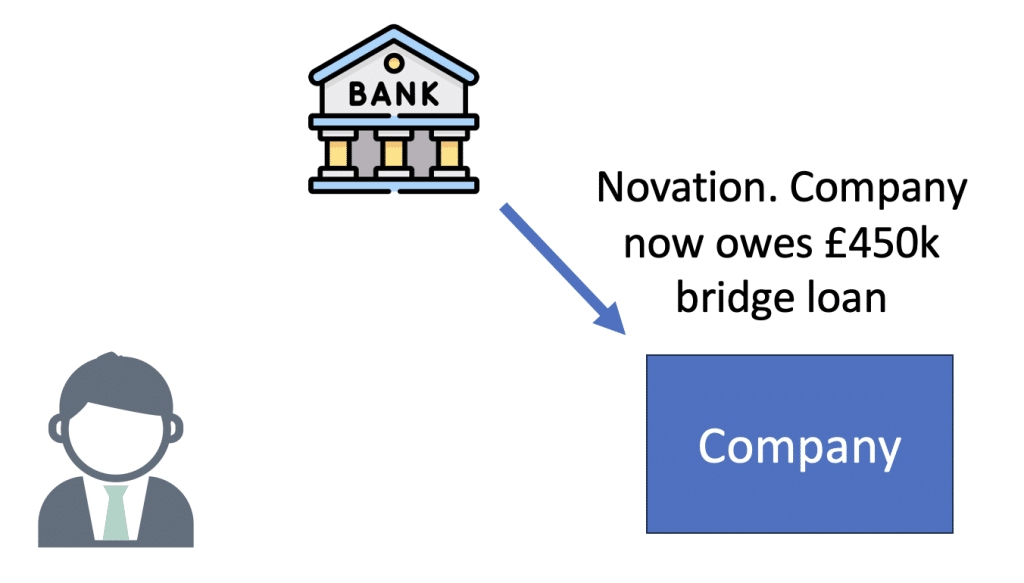

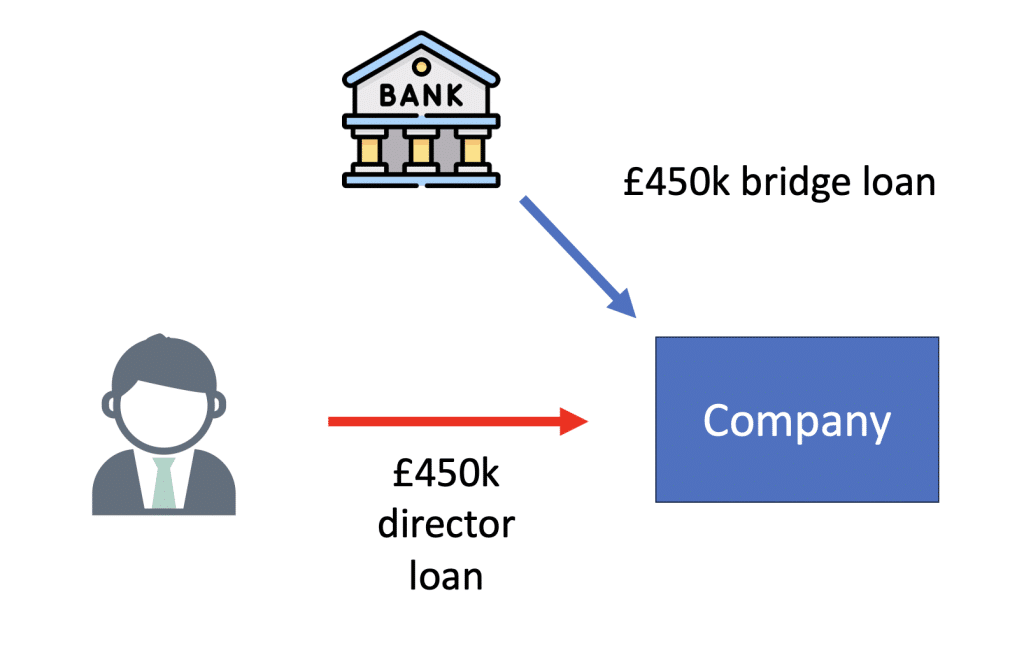

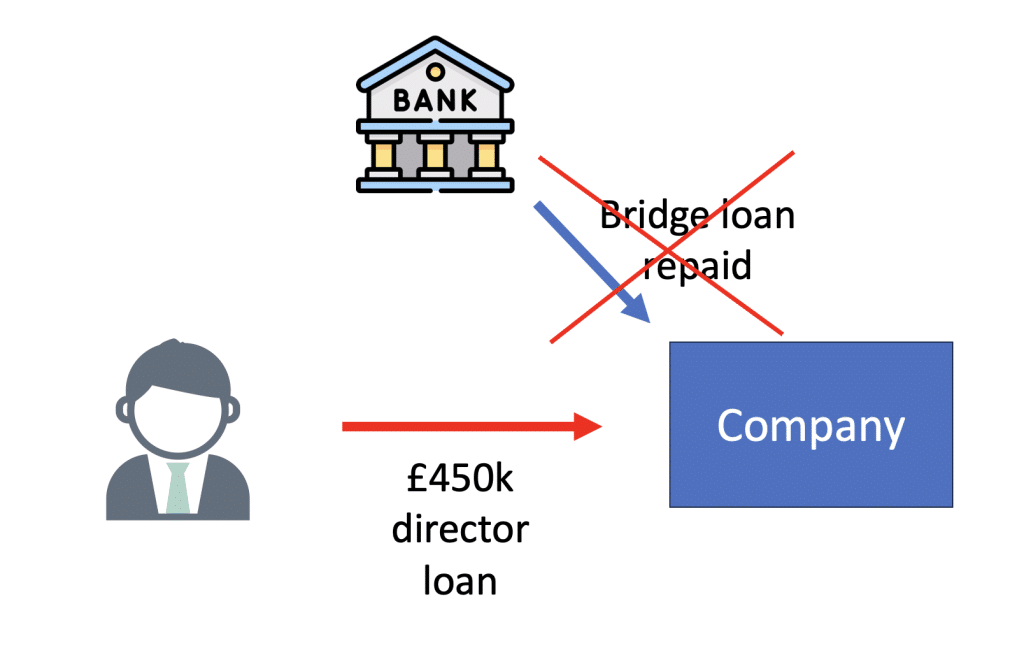

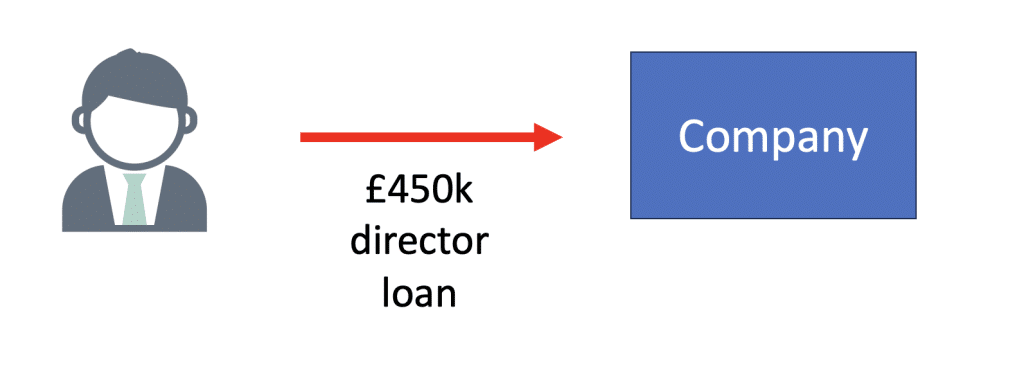

Does the “director loan” structure work?

It’s the director loan which creates the “ability to draw down capital tax free”. It’s achieved using this astonishing structure – a bridge loan that’s put in place for a few hours immediately prior to incorporation, and moves between two escrow accounts without ever being available to the landlord or their business.

In our view the structure prevents incorporation relief applying, with an additional risk that “loan repayments” become taxable. Cotswold Barristers provide no advice at all on the effect of the structure.

Does anti-avoidance legislation apply?

There are a plethora of anti-avoidance rules that are engaged if, as here, a transaction has a “main purpose” or “main benefit” of obtaining a tax advantage: DOTAS, rules denying interest deductibility, GAAR, settlor-interested trust rules etc. Advisers would usually cover these issues even on simple and innocuous structures. We would also usually expect advisers to cover the Ramsay common law anti-avoidance principle.

However, there is no evidence that either Property118 or Cotswold Barristers have considered or advised on any of these issues. As we note above, Mark Smith’s DOTAS article demonstrated a complete lack of understanding of the rules.24

To be clear, most clients don’t want or need detailed technical advice. However in our view a reasonable tax lawyer should always provide advice as to the tax consequences of a transaction, particularly when it is an unusual one – even if the advice is highly summarised.

We cannot explain the templated advice and lack of advice on key points. It is possible that there is detailed advice which all of our sources either missed or have mislaid. However, if that is wrong, it raises serious questions as to Mark Smith’s actions – the clients certainly believe they are receiving specific advice from a barrister.

So why aren’t they?

Inappropriate attitude to risk

Good tax advice on complex structures always contains a discussion of risks, both under current law and the risk of change of law. In 2017, the Court of Appeal found an adviser negligent for failing to warn of the risk of a structure, even when the advice was not itself negligent. This had the obvious effect of making risk warnings more common, even when tax advisers are looking at straightforward arrangements.

There are no risk warnings in the Cotswold Barristers (or Property118) advice we have seen.

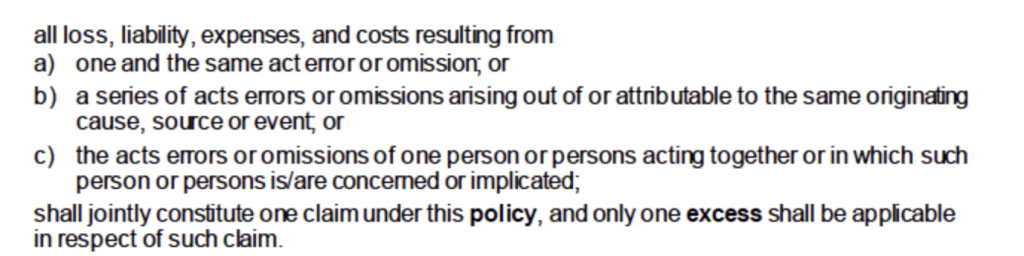

Indeed, the claim is made that their clients are “shielded from financial risk” because the barristers carry £10m of professional indemnity insurance per client.

This is highly misleading.

To access professional indemnity insurance, clients have to successfully sue the barrister for negligence, and that is not straightforward.

David Turner KC, an insurance specialist, was doubtful that Cotswold Barristers really carry £10m of insurance “per client”. His view was that the standard Bar Mutual policy’s “aggregation” clause meant that it would be £10m per “originating cause”. If the Property118 structure is defective then that would likely be one “originating cause”, and the £10m would therefore be shared by all 1000+ clients. Cotswold Barristers subsequently confirmed that David Turner was correct (but tried to stop him publishing that confirmation).

The failure to warn clients of risks may itself amount to negligence. The false claims made about the insurance appear to make the situation more serious.

The only barrister named in the advice sent to clients, or on the Cotswold Barristers website, is Mark Smith26. Smith is a generalist whose practice ranges from general business law, to copyright, to tax, to criminal defence work, to private prosecutions (including one where he was suspended by a month by the Bar Standards Board for acting negligently and “failing to act with reasonable competence“). His profiles in 2017 and 2020 didn’t include tax in his areas of practice.

Tax barristers usually train and practice in a “tax set” – a chambers entirely or partly dedicated to tax law. Mr Smith did not; indeed, in a discussion on LinkedIn, it was not clear Mr Smith had heard the term “tax set”.

On the basis of the documents we have reviewed, it seems plausible that the Property118 scheme fails because of poor implementation, leading to a failure to achieve the intended tax benefits, and significant additional up-front tax. It also seems plausible that Mark Smith and Cotswold Barristers have been serially negligent.

Thanks to SH and D for their trust expertise, and J and K for their invaluable input and review. Thanks to David Turner KC for investigating the insurance position. Thanks to C for input on the indemnity/interest points. Thanks to F and N for technical accounting input. Thanks to G and S for helping locate Property118 advice and documentation, and for their assistance with the technical analysis. Thanks, as ever, to S2 for specialist SDLT input and reviewing after publication. Thanks to James Robertson for the s284 point. Finally, thanks to Ray McCann for his original comments on the DOTAS analysis, and to Patrick Way KC for his insights on a Bell Howley Perrotton LLP podcast (recorded 8 November 2023; not yet broadcast).

Footnotes

It’s relevant to note that a court or tribunal would not necessarily approach the Property118 structure point by point, in the way that we have analysed in our reports. In a recent podcast discussion on the Property118 structure, Patrick Way KC made the important point that, when a structure looks like tax avoidance, the modern judicial approach is to find against it on principled grounds and not undertake the full technical analysis. ↩︎

This is the only meaning we can see “vest absolutely and immediately in the Trustees” can have. It is unclear what “in accordance with their various legal and equitable interests” means, given that a trustee obviously has no equitable interest. Possibly it means that the Trustee takes the same % beneficial ownership as they had before the trust was originally declared.

We have considered whether this could simply be a typo, and 2.4 should be read as meaning that the Property vests “absolutely and immediately in the Beneficiary“, but we don’t think that can be right. First, the property has already vested in the Beneficiary, so it doesn’t make sense to say that the Trustee can by notice vest it again. Second, it would be odd for the Trustee by notice to trigger its own loss of legal title. Third, the “or” clause at the end of the paragraph deals with the scenario where the Beneficiary has called for legal title; why would there be two subclauses doing the same thing? We therefore don’t believe the wording can be ignored, no matter how inconvenient it may be. The drafting is clearly a mistake from a tax perspective, but that doesn’t mean it can be ignored – there is, after all, commercial utility to enabling the landlord to unwind the structure at any time. It might be possible to make an application to the court for rectification on the basis there was a mistake of law and/or mistake of tax law, but this would be far from straightforward. ↩︎

James Robertson added another point we missed in our initial analysis: the potential for an up-front market value CGT charge under s284 TCGA (sale with a right to reconveyance). The interaction between the different provisions would require considerable thought, but likely there would be only one up-front market value CGT charge, whether under the settlement rules, s284 or on the grant of an option. ↩︎

This is the view of our team (including a KC specialising in the tax treatment of trusts), but should not be regarded as the final word; a definitive analysis would require consideration of the full facts and circumstances, and it would be wrong at this stage to preclude the other two possibilities. ↩︎

Including the settlor interested trust rules effectively reversing any potential income tax benefit, and a 6% inheritance tax charge every ten years. Possibly also a 20% entry charge, and the application of the gifts with reservation of benefit rules, although this would need a careful analysis which we have not undertaken. If a settlement arises then it would have to be registered with the Trust Registration Service. Mark Smith takes the view that the intended “bare trust” is not registrable – we are not sure that is correct, but it’s irrelevant if in fact the trust is not bare. ↩︎

This would, however, need careful thought. It would be very inadvisable and perhaps improper to simply proceed on this basis without detailed and case-specific legal analysis. ↩︎

i.e. because our previous analysis was on the assumption that Property118 correctly implemented their structure. We also note that, when Property118 briefly hired a tax KC in an attempt to threaten us with a libel suit, it seems likely that she did not review the transaction documents, as she said specifically that her views were on the basis that the structure was “properly implemented” – see paragraph 13 here. The KC did add that she had reviewed client files, but we expect this was advice and correspondence with HMRC, not transaction documentation – if the KC had reviewed transaction documentation then we believe her opinion would have been very different. ↩︎

In the interests of simplicity, this analysis in this section of our report ignores the first drafting error – the fact the trust is probably a settlement and not a bare trust. In reality the interaction of the two issues would need to be considered, and that is not at all straightforward. ↩︎

And is likely entirely unaware of the transaction. ↩︎

Our team had different views. Some of us believe the clause could be read broadly, given that the trust anticipates the existence of the mortgages. Others don’t agree, because the mortgage payments are not “chargeable on the Property” (rather, they are personal obligations of the landlord), and the mortgage payments do not “arise out of the settlement” (also, what does “payable to them” mean? The word “to” looks like a typo, but it’s included in all the versions of this document we’ve seen). ↩︎

Usually lawyers never put operative provisions into recitals, but where a contract is silent on a point, an operative provision in the recitals will be effective – see the old case of Aspdin v Austin (1844). ↩︎

The fact the indemnity payments are not termed “interest” in the documents is irrelevant (see the Re Euro Hotel case) – economically they are interest on the principal amount created by the sale contract and therefore are interest for tax purposes (see Bennet v Ogston). Probably they would not be interest even if there was no principal amount – our original view (prior to having reviewed the document set) was that they would be either taxable annual payments or capital payments (i.e. sale consideration). ↩︎

This is not the case for a normal incorporation, which achieves other objectives: e.g. segregating liability and obtaining commercial financing – however the Property118 structure does not achieve this ↩︎

And Smith did not then consider any of the many anti-avoidance rules which will be engaged if there is a tax main benefit or tax main purpose ↩︎

Smith misses that there are several ways in which there can be no promoter: (1) in-house schemes, clearly not relevant; (2) the promoter is outside the UK, not relevant; and (3) no promoter. If Smith was right that Property118 wasn’t a promoter then this would be the third scenario, not the first. He makes a bad mistake and is then badly wrong on the consequences of his mistake. ↩︎

And DOTAS looks at the “proposed arrangements”, and therefore the fact that Smith accidentally omits the indemnity is no defence ↩︎

The confidentiality hallmark would also likely apply, given that Property118 refused to disclose details of their scheme on the basis that it is “valuable intellectual property” ↩︎

A “compliance check” is not a tax term, but we are assuming these were “aspect enquiries” and not full enquiries. ↩︎

As an aside, Smith tends to refer almost exclusively to HMRC guidance, and in this case the first guidance appearing on Google doesn’t mention the subsection 17 rule (probably because the guidance pre-dates the legislation). That is speculation; however it is notable that reliance on this out-of-date guidance was one of Less Tax for Landlords’ big mistakes. ↩︎

The reference to HMRC manuals is curious – advisers should be advising on the basis of the law, particularly when a transaction is tax-motivated (as HMRC guidance cannot be relied upon in such circumstances). ↩︎

Which is why we are confident we will not reveal our sources by publishing extracts from Property118 advice and documentation ↩︎

Note in passing that “a discretionary trust controlled by you” is not how discretionary trusts can work if they are to be respected for inheritance tax purposes. ↩︎

It is also notable that Mark Alexander, who runs Property118, appeared completely unaware of Ramsay, thinking a reference to “WT Ramsay” was a mistaken reference to the recent Upper Tier Tribunal Elizabeth Moyne Ramsay case ↩︎

There is no suggestion that Cotswold Barristers was aware of his actions, but Cotswold Barristers does appear to have been responsible for listing him as part of its team. ↩︎

Not to be confused with Mark Smith, the respected extradition barrister. ↩︎

The Law Society has played an exemplary role in calling for libel law reform to prevent abusive SLAPPs – “strategic lawsuits against public participation”. In other words, the use and abuse of legal processes to silence allegations of wrongdoing.

The Society of Media Lawyers is unhappy with this. They’ve written to the President of the Law Society asking the Law Society to stop advocating against SLAPP. Indeed the Society of Media Lawyers don’t seem to accept SLAPP exists – they say there is “not a significant SLAPP problem in the UK”.

They go further: they want Society of Media Lawyers members to be involved in the implementation of the anti-SLAPP provisions of the Economic Crimes Bill, and to be appointed to the Department for Culture, Media and Sport’s SLAPP taskforce.

The Society’s members include the likes of Carter-Ruck – described by David Davis MP as “the go-to law firm for every bad actor seeking to undermine or misuse British justice”. It is clear why Carter-Ruck and friends would want to shape anti-SLAPP rules. It is much less clear why the rest of us would agree to this.

Letter to the President of the Law Society

Dear Nick,

I am a solicitor and the founder of Tax Policy Associates, a think tank established to improve tax and legal policy.

I am aware of a recent letter sent to you by the Society of Media Lawyers. criticising the Law Society’s position on SLAPPs.

The Society of Media Lawyers say there is “not a significant SLAPP problem in the UK” and are unhappy that the Law Society is taking a stand against SLAPP. They ask to be involved in the implementation of the Economic Crimes Bill, and to have a representative on the Department for Culture, Media and Sport’s SLAPP taskforce.

The assertion there is not a significant SLAPP problem in the UK is deeply unserious. To take just a few examples from the last few years:

Schillings acted for Russell Brand, attempting to make the Metro newspaper retract a clearly factual report about a “joke” about sexual assault which Brand had made on live television. Asserting defamation with no legal or factual basis is characteristic of a SLAPP.

An unnamed law firm acted for Russell Brand, and sent an aggressive and intimidating email to an alleged victim of Brand’s, which included an entirely inappropriate allegation of blackmail. The making of unevidenced criminal accusations in correspondence is characteristic of SLAPPs.

Archerfield Partners acted for Russell Brand in an attempt to prevent reporting of accusations of sexual assault by Szilvia Berki. This included defamation letters to newspapers and ultimately a successful application for an an anti-harassment restraining order. If Ms Berki’s allegations were correct (which now seems at least plausible) then this was an outrageous abuse of the legal system to silence her.

Several unnamed law firms acted for PPE Medpro, Michelle Mone and Douglas Barrowman, and wrote to the Guardian saying that any claim that Mone/Barrowman were linked to PPE Medpro was defamatory. The parties have subsequently admitted that Mone/Barrowman are in fact linked to PPE Medpro. Aggressive correspondence based on an untruth is a key characteristic of a SLAPP.

TT Law Ltd acted for William Hay in a defamation claim against Nina Cresswell, who had alleged Hay had sexually assaulted her. Mrs Justice Williams found that Cresswell’s allegations were substantially true. This is part of a very disturbing trend of perpetrators of sexual assault using SLAPPs to silence their victims.

An unnamed law firm acting for an individual accused of sexually assaulting Lucy and Verity Nevitt. The law of confidence was used in a successful attempt to prevent him being named. This is another very disturbing case. Parliament has expressly not given anonymity to those accused of sexual offences, and to attempt to achieve this through secret threats of litigation is an affront to the rule of law.

An unnamed law firm acted for Wirecard against the FT in a defamation action following the FT’s reporting that Wirecard was engaged in fraud. That reporting turned out to be entirely correct. The use of defamation proceedings to silence correct accusations of criminality is characteristic of a SLAPP.

Carter-Ruck acted for Mohamed Amersi in a defamation claim against former MP Charlotte Leslie. Mr Justice Nicklin found for Leslie, and said he had “real cause for concern” that the litigation had an “impermissible collateral purpose”. That is a textbook definition of a SLAPP. It is relevant to note Carter-Ruck’s claim that it has not encountered any SLAPP cases

Discreet Law acted for Yevgeny Prigozhin in a case against journalist Eliot Higgins of investigative website Bellingcat for claiming that Prigozhin ran the mercenary Wagner Group. At the time of Higgins’ report, Prigozhin had been widely reported as running the Wagner Group and had been sanctioned by the US and UK for his role in it. The case was abandoned after Russia invaded Ukraine, and Prigozhin subsequently admitted running the Wagner Group. It is hard to imagine a more obvious SLAPP than bringing a defamation action for a claim that was in fact true, and was widely known to be true at the time.

Taylor Wessing acted for Eurasian Natural Resources Corporation Limited against journalist Tom Burgis. Mr Justice Nicklin found that the passages complained about in Burgis’ book were not defamatory, but noted that the very serious other allegations in the book (that ENRCL was a “corporate front” for criminal activities) were not the subject of a defamation claim. This is a typical SLAPP technique – ignoring the core allegation made and pursuing defamation allegations on an ancillary issue.

Carter Ruck acted for the President of Malaysia’s PAS Islamic Party, Abdul Hadi Awang, in an extraordinarily far-fetched case against Clare Rewcastle Brown with the apparent aim of preventing her reporting about corruption in Malaysia. The case was eventually withdrawn and a settlement agreed in her favour. The far-fetched theory run by Carter Ruck, and the eventual concession, is characteristic of a SLAPP.

An unnamed law firm acted for Jeffrey Donaldson in a defamation claim against OpenDemocracy for their reporting on political donations. The action eventually timed out. Commencing and then eventually withdrawing proceedings is characteristic of a SLAPP.

An unnamed law firm acted for Javanshir Feyziyev against Paul Radu, a Romanian reporter for the Organized Crime and Corruption Reporting Project in relation to allegations of involvement in the Azerbaijani Laundromat. The case was settled in the reporter’s favour shortly before the court date. The decision to bring a claim against an individual journalist rather than the news organisation who published the accusations is characteristic of a SLAPP.

Taylor Wessing acted for Al Wazzan, an investment advisor currently on bail in Kuwait for his role in the 1MDB scandal. Taylor Wessing attempted to prevent Clare Rewcastle Brown from even mentioning that Al Wazzan was on bail. Taylor Wessing abused the law of confidence in an attempt to keep their correspondence from being published.

And from my personal experience:

ACK Media Law wrote to me alleging defamation after I “retweeted” a newspaper article claiming Nadhim Zahawi was under investigation by HMRC. The firm said Nadhim Zahawi was unaware he was being investigated by HMRC. Zahawi had indeed been under investigation, and at that point was in the process of settling the matter. The Prime Minister’s ethics adviser concluded that Zahawi should have understood he was under investigation. Threatening defamation against a member of the public “retweeting” a news article, and not against the newspaper that published the article is characteristic of a SLAPP. Alleging defamation where an accusation is in substance true is characteristic of a SLAPP.

Osborne Clarke acted for Nadhim Zahawi, and accused me of defamation for allegations about Zahawi’s tax position which turned out to be correct. In the course of correspondence, Osborne Clarke stated repeatedly that Zahawi’s taxes were fully declared and paid, a statement that was false, and that Zahawi must have known was false. Osborne Clarke abused the law of privilege and confidence in an attempt to keep their correspondence from being published. Pursuing a defamation claim where the underlying accusation is true; attempting to keep the claim secret; and making false statements in correspondence – all features of a SLAPP.

Brett Wilson LLP acting for a tax avoidance boutique called Property118, accused me of defamation for stating opinions on tax law which are shared by the majority of the profession. A libel action on that basis never had any prospect of success, and the Brett Wilson letter was therefore a SLAPP. Brett Wilson abused the law of copyright and confidence in an attempt to keep their correspondence from being published. Another characteristic of a SLAPP.

All of this presents a disturbing pattern of law firms acting for clients who are using defamation law to inappropriately stifle free discussion and, in many cases, to prevent publication of allegations that are in substance correct. In a number of these cases the lawyers had good reason to know or suspect that the allegations were correct. And these are likely just a small minority of cases: the intention behind most SLAPPs is that they never become public. The stifling of debate by lawyers, through the use of abuse of pseudo-legal arguments and the making of false factual claims, represents a threat to free expression and (in my view) to the rule of law.

I would therefore urge you to continue your current approach to SLAPP, which I am confident has the support of the vast majority of the profession, as well as the general public.

A final point: many of these examples involve members of the Society of Media Lawyers. To say they have a conflict of interest would be a considerable understatement. It would therefore, in my view, be highly inappropriate for the Society of Media Lawyers to involved in the implementation of the Economic Crimes Bill, or to be appointed to the Department for Culture, Media and Sport’s SLAPP taskforce. I would urge you to reject this request.

Baroness Mone introduced a company, PPE Medpro, to the “VIP fast lane” for supplying PPE to the Government during the pandemic. There was copious evidence that she and/or her husband, Douglas Barrowman, ran the company. In December 2020, a lawyer instructed by Mone and Barrowman told the Guardian that “any suggestion of an association” between the Tory peer and PPE Medpro would be “inaccurate”, “misleading” and “defamatory”.

But now a representative of Mone and Barrowman has admitted that Barrowman funded and ran PPE Medpro.

In both cases, a libel threat was made based upon a falsehood.

Were they lying?

I cannot read Mone, Barrowman or Zahawi’s minds, and it is conceptually possible that all were being honest. For example, Mone and Barrowman may have thought that Barrowman’s deep connection to PPE Medpro was not an “association”.3 Zahawi may have not realised he was under investigation.4 It is also possible that they were not aware of the statements being made by their lawyers.5

In my judgment these explanations are less likely than the alternative: Mone, Barrowman, and Zahawi intentionally instructed their lawyers to make false statements, in order to prevent people publishing unfavourable stories about them – stories they knew were substantively true. In my opinion, they likely lied.6

If a libel case proceeds to court, and the claimant lies on the witness stand, then that is perjury, and prominentpeople have been prosecuted for it. But if a claimant lies in libel correspondence, directly or through their lawyers, and the matter never reaches trial, then there is no consequence. Except one: often the lie will be effective, and the story quashed, without ever seeing a courtroom.

This is the “mathematics of libel”.

If you’re faced with a wealthy litigant then it’s usually rational for you to withdraw it and avoid defamation proceedings, even if you’re certain your story is true. Why? Because if you win you will devote perhaps a year of your life to the litigation, and end up out of pocket by a few £100k;7 if you lose, you could be on the hook for £1m or more. Or you could give up now, and hopefully pay nothing. This is the rational choice which – appallingly but inevitably – is forced on people by our defamation law.

So if you want to stop people writing the truth about you, you just need two things: money to pay the lawyers, and the willingness to lie. The mathematics of libel will then do the rest, and force that annoying journalist to back down.8 And in the – usually unlikely – event they don’t, you can just walk away, free from consequence. It’s a one-way bet.

We need to change this calculation.

How?

Any “letter before action” threatening defamation proceedings could be required to be accompanied by a “statement of truth”. The claimant would have to say, under threat of perjury, that the statements in the letter are correct, and that the defamatory statement complained of is false. Lying in correspondence would then have a consequence.9

The new anti-SLAPP law is welcome, but only applies to cases involving economic crime. It wouldn’t have applied to Zahawi, and it’s doubtful it would have applied to Barrowman/Mone. The law could easily be extended to all defamation cases.

The Solicitors Regulation Authority could discipline solicitors who make false factual claims in defamation correspondence without having taken appropriate steps to verify the claims,10 or who remain acting for a client past the point it is clear the client lied.11 I am hopeful they will do so in both the Zahawi and Mone/Barrowman cases.

Or more radical libel reform: the writer Edward Lucas has suggested a speedy and lawyer-free dispute resolution service for defamation cases, much like a small claims court. The best argument against this is that the floodgates would open, and the new court become overwhelmed with claims from ordinary people. But that’s a terrible indictment of the current law – that it’s only viable because only the rich can afford it.

So perhaps we need a change which is equally radical but much simpler: require that public figures can only sue for defamation if they can demonstrate the authors acted maliciously, with knowing or reckless disregard for the truth.12 We could go further, and require that this point is always heard as a preliminary issue before any defamation action can proceed, with the defendant’s costs payable in full13if the claimant fails to demonstrate malice.

One way or another, we need to end the mathematics of libel, and make it rational for people telling the truth to continue to tell the truth.

Footnotes

I believe similar threats were made to other newspapers; the Independent is unique in having published them. ↩︎

There were other false statements in my correspondence with Zahawi’s lawyers. Their first letter made a factual claim about Zahawi’s father having provided startup capital which appears false, as the relevant document was signed much later and back-dated; the other claim about his father being heavily involved in the business was denied by the company and has no supporting evidence. The letter also contained a statement – “Should there be any serious questions to be asked about our client’s taxes, HMRC will no doubt ask them and our client will respond accordingly” – where the use of the conditional tense can only be regarded as highly misleading (given that Zahawi knew that HMRC had already been asking him “serious questions”). And there were repeated subsequent claims that his taxes were fully declared and paid in the UK ↩︎

Unless his advisers were shockingly negligent they would have told him that this was an enquiry or a discovery assessment, and in ordinary English most people would describe that as an “investigation”. Sir Laurie Magnus concluded that Zahawi should have understood he was under investigation; it follows that logically either Sir Laurie is wrong, Zahawi was incompetent in not realising he was under investigation, or Zahawi lied. ↩︎

It would be most surprising, and improper, if a lawyer making factual claims, supporting a serious allegation of defamation, did not do so on the basis of instructions from their client. ↩︎

An important note is that I am assuming the Guardian and Independent’s reporting of the libel threats they received is correct. That seems highly likely; surely otherwise Zahawi/Mone/Barrowman would have said so. ↩︎

Whilst you may expect to get an order to cover your legal costs, the “standard basis” by which costs are awarded means you will usually end up having to pay around 1/3 of the costs yourself ↩︎

Even when a journalist doesn’t back down, the defamation laws have a more subtle effect. They slow down the story, requiring legal input and senior editorial involvement at every step. This can be a considerable benefit to the claimant. ↩︎

I’m not suggesting that correspondence in advance of the “letter before action” would have to include a statement of truth. However I expect that defendants would respond to such correspondence by effectively daring the claimant to produce a letter before action and statement of truth. ↩︎

There is no SRA guidance, caselaw or other authority on what “appropriate steps” would be. My view is that it depends on the nature of the claim being made. If I am accused of shooting JFK, then it is reasonable for my lawyer to deny the claims without requiring anything in the way of evidence from me. If I am accused of robbing a bank last week, it is reasonable for the lawyer to ask me if I robbed the bank. If I am accused of owning my house through a Vanuatu trust document leaked to the Guardian, then it is reasonable for my lawyer to ask me to explain the leaked document, and not accept implausible explanations. ↩︎

As more details emerged about the ownership of PPE Medpro, it was reasonably clear that Barrowman controlled it, and his denials were false. By January 2023, it was reasonably clear that Zahawi had been under HMRC investigations, and that his denials were false. Yet, in both cases, lawyers kept acting. ↩︎

In other words, adopt the US libel standard, following New York Times Co. v. Sullivan. One prominent libel barrister responded to this suggestion by saying that it would make it almost impossible for anyone to sue for libel. That is indeed the point. I don’t see a public interest in giving public figures the ability to bankrupt people for claims that are either true or made in good faith ↩︎

It’s a common complaint that the UK tax system is much too complicated. That complaint is correct.

Some of the complication is inevitable (modern life is complicated). Some is a response to avoidance. Some is driven by policy choices (e.g. VAT exemptions1). But some of the complication really is unnecessary. I’ll try to demonstrate the problem by taking one tax point that faces many companies investing in the UK, and working through each of the overlapping rules the company has to work through.

Judge for yourself how sensible those rules are, and how many are really necessary.

The scenario

Let’s pick a simple scenario that’s realistic – indeed very common:

Waystar RoyCo is a large US business establishing a new UK subsidiary, Waystar UK.

It has a finance company in the US (Waystar Finco) which raises money from the market (borrowing from banks, issuing bonds etc) and then makes it available to group companies.

Waystar Finco wants to provide some of that funding to Waystar UK.

So Waystar Finco makes an “intragroup loan” to Waystar UK, with an interest rate reflecting the cost of Waystar Finco’s funding plus Waystar Finco’s own admin etc costs.

Like most businesses, Waystar UK will expect to get UK corporation tax relief for its interest payments.2 Will it?

From a policy perspective Waystar UK absolutely should get tax relief. It would if it borrowed directly from the market, and interposing Waystar Finco should make no difference (but is likely cheaper/more efficient for Waystar). But that rightly cuts no ice with HMRC – the question is, what do the rules say?

There are many, many, rules that can impact tax relief/deductibility of interest. Here’s how I’d advise Waystar UK on the main ones, with added commentary on whether each of the rules really still makes sense.3

1. Transfer pricing

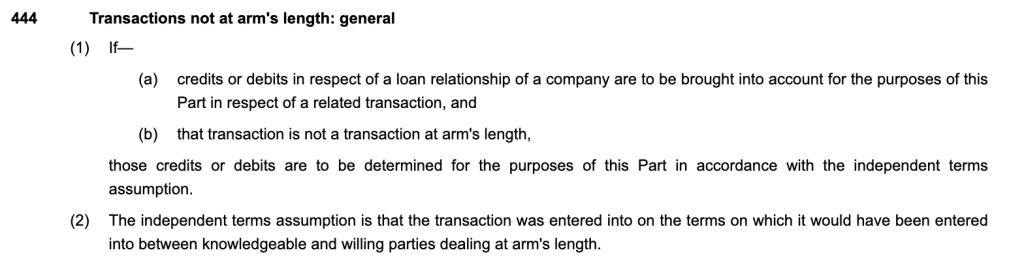

Most countries in the world have “transfer pricing” rules. In broad terms, they say that if a company has an arrangement which isn’t on “arm’s-length terms” and it’s taxed as if it was. So if, for example, current market interest rates are 6%, and Waystar UK borrows from Waystar Finco at 10%, then it will only get a deduction for the 6%. This is pretty sensible.