I posted some charts yesterday on how the UK tax system compares to other countries when we look at tax as a % of GDP. One response was to say: “well, I don’t care about tax as a % of GDP… I care about the tax I pay”. Which is fair enough.

How can we fairly compare the tax actual people pay?

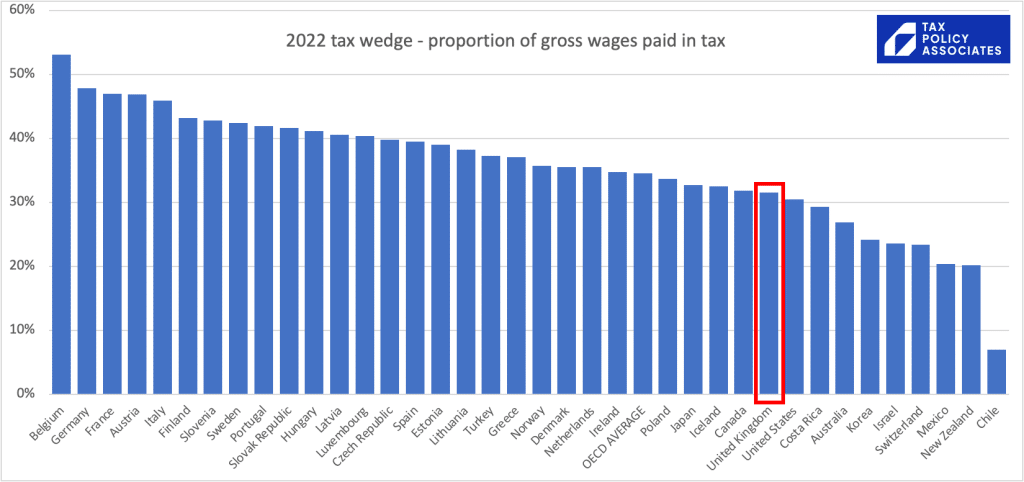

Tax wedge

The “tax wedge” is the tax paid by the average single worker divided by the gross wages.1 It’s the best way I know to make a fair (or somewhat fair) comparison of the burden on tax on wages across the world.

I think many people will be surprised, even disbelieving, at where the UK places here.

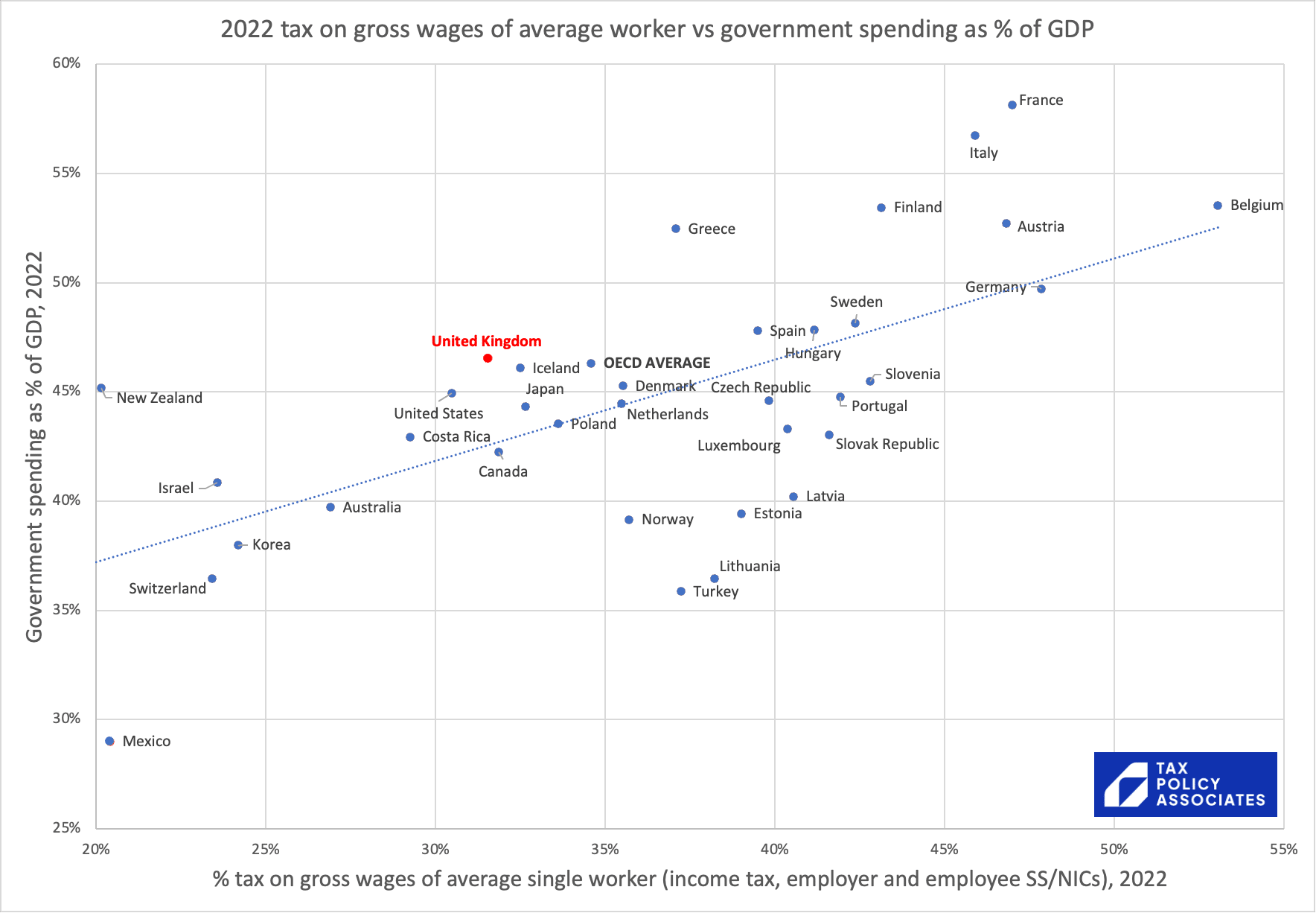

Clearly there are some very different social models, with Belgium (for example) having a much more expansive welfare state than Chile. So it’s useful to add in that wider context (again from OECD data):

So in general terms, if you’re an average worker, you get what you pay for.

Or, if we want to annoy lots of people, we can point out that there’s no country where the average worker pays less tax than the UK on their wages, but which has higher government spending.

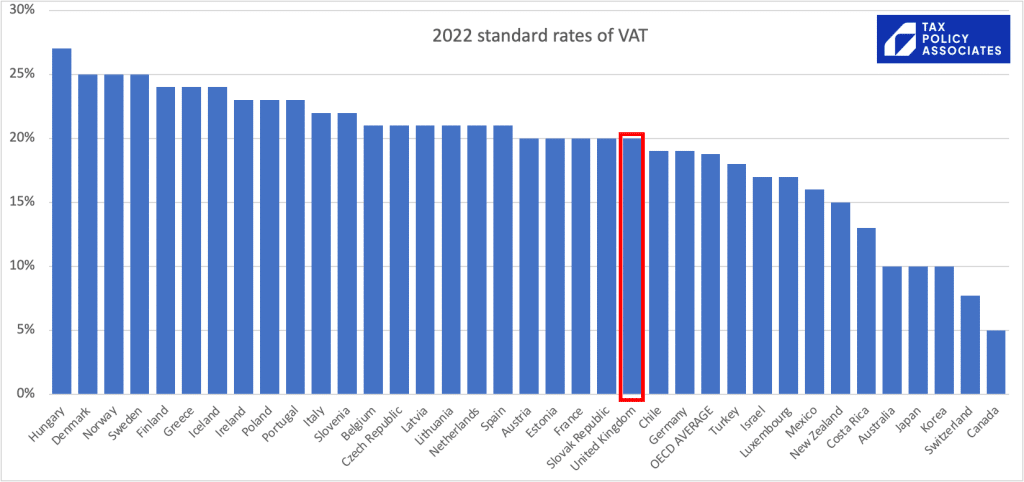

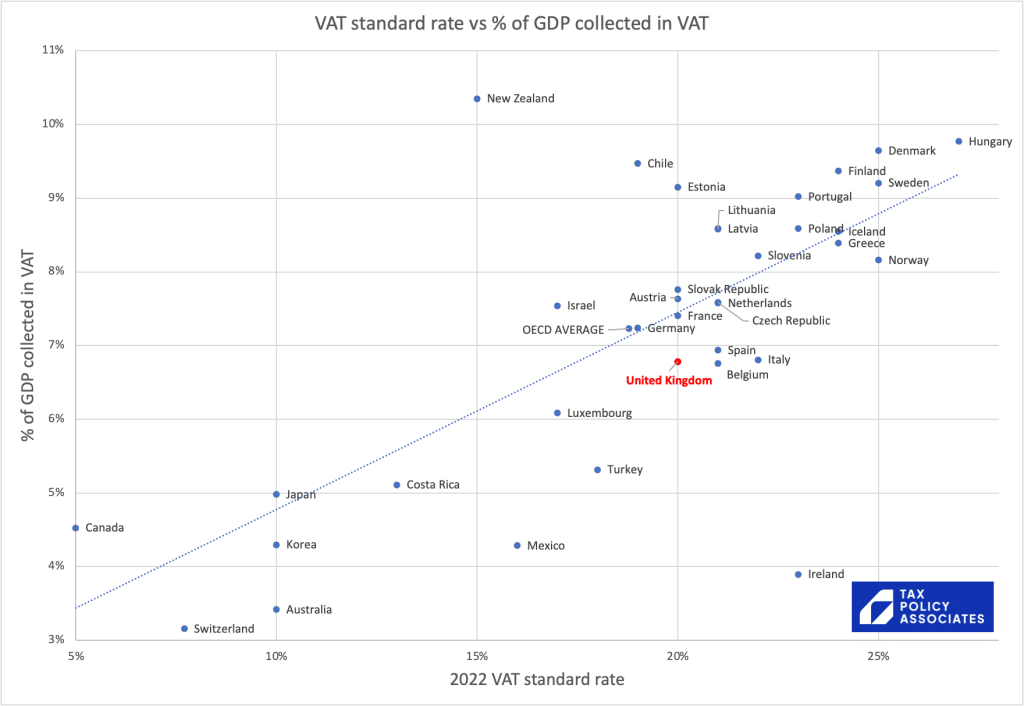

What about VAT?

If we just look at the standard rate of VAT in each country:

On the face of it the UK again looks very average.2

But we can’t just compare the standard rate. Some countries apply the standard rate to almost everything; others have widespread exemptions and special rates.

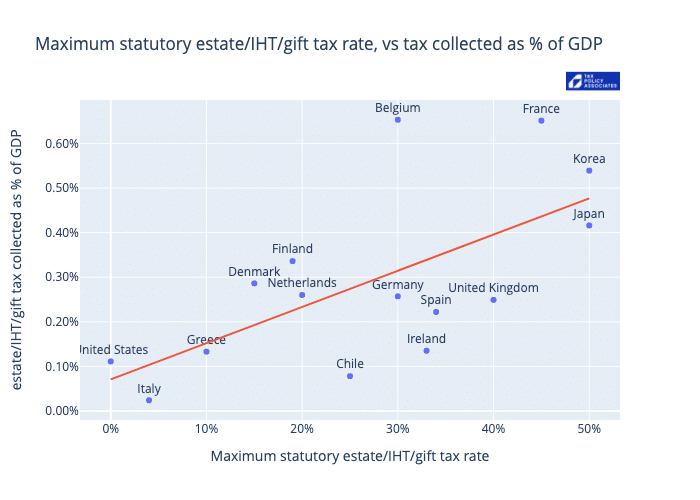

We can get a sense of this if we plot the rate of VAT against the amount of tax VAT collects, as a % of GDP:3

The chart suggests the UK collects a bit less VAT (as a % of GDP) than you might expect from its rate.4

The bottom line is that there is no evidence that the average Brit is over-taxed by international standards.

The spreadsheets with the data and charts are available here.

Footnotes

In other words, this takes into account the income tax and national insurance/social security paid by the worker him or herself, and also the national insurance/social security paid by the employer (because there is good evidence that in the long run this is economically paid by the employee in the form of reduced wages). ↩︎

There’s no USA on the chart, because the US has no VAT. Many states have sales taxes, but they’re nothing like VAT – the rate is much less (averaging around 5%) and the goods/services covered are much more limited. ↩︎

Bear in mind the usual caveats about comparing different systems in different countries, and (as usual) ignore Ireland, because its reported GDP is distorted by multinational [HQ locations]/[tax avoidance] (delete per your preference). ↩︎

Actually it’s worse than that, because VAT compliance in the UK is pretty good, and so masks what is a very limited VAT base (i.e. wide exemptions/lower rates) by international standards. Rita de la Feria, perhaps the world’s leading VAT academic, has written convincingly on this. ↩︎

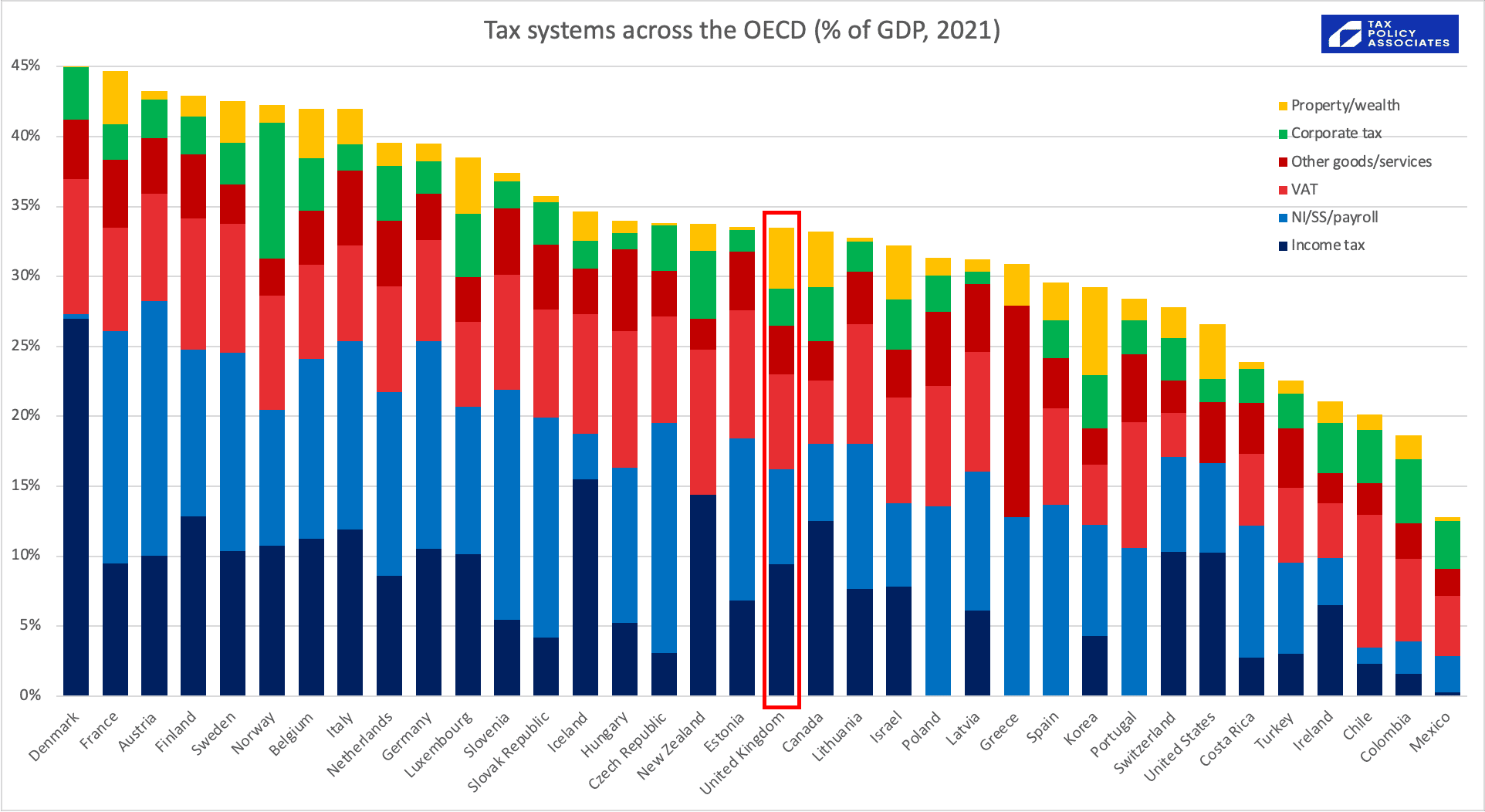

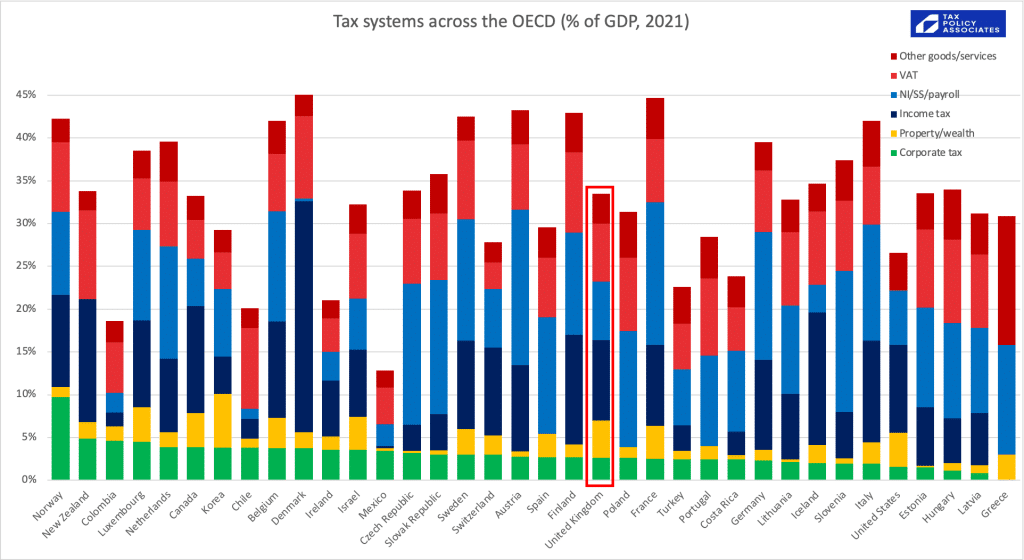

We now have the latest OECD tax data, showing tax as a percentage of GDP across the developed world.

The UK looks rather average:

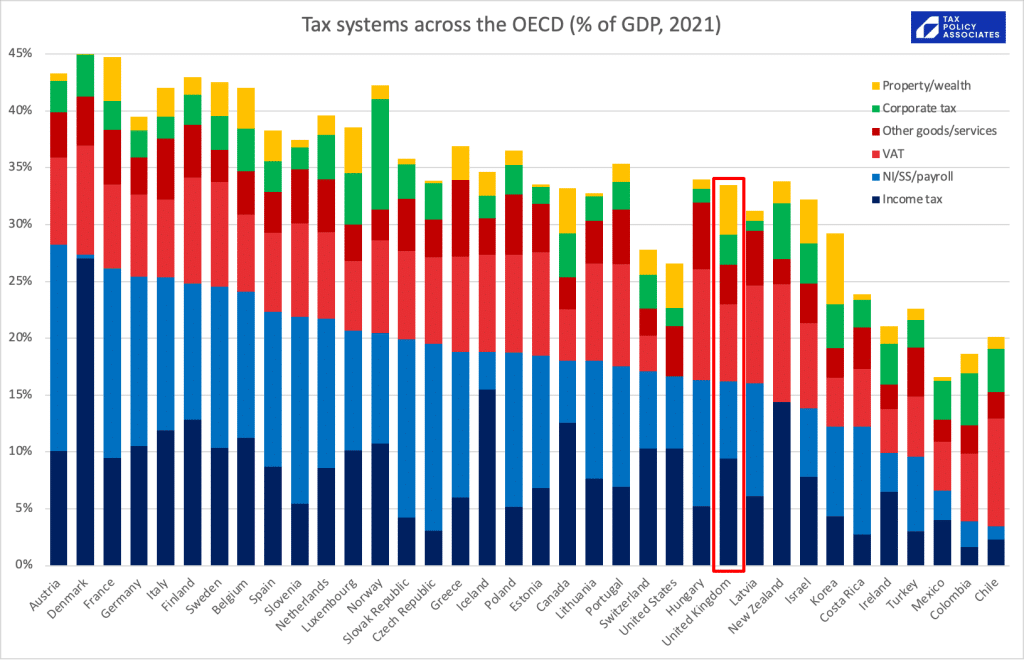

If we order by personal tax (income tax and national insurance etc), we see that UK income tax/NI is a somewhat lower % of GDP than average:

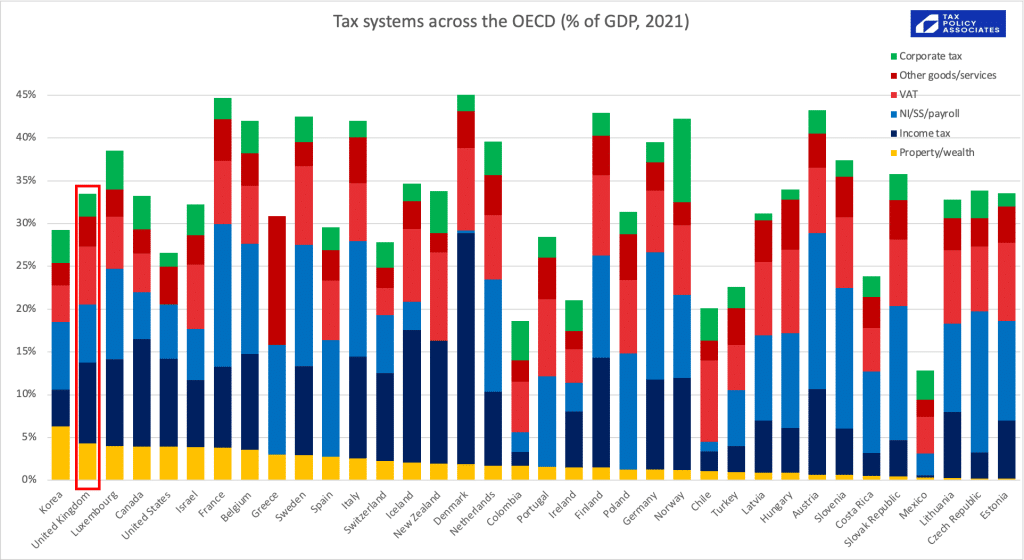

If we order by property/wealth tax, the UK surprisingly raises one of the highest %s of GDP in the world (although we should be careful about comparisons here; please see caveats below):

Corporate tax, the UK raises a bit less than average (although this is before the increase from 19% to 25%, which will put the UK in the top quartile):

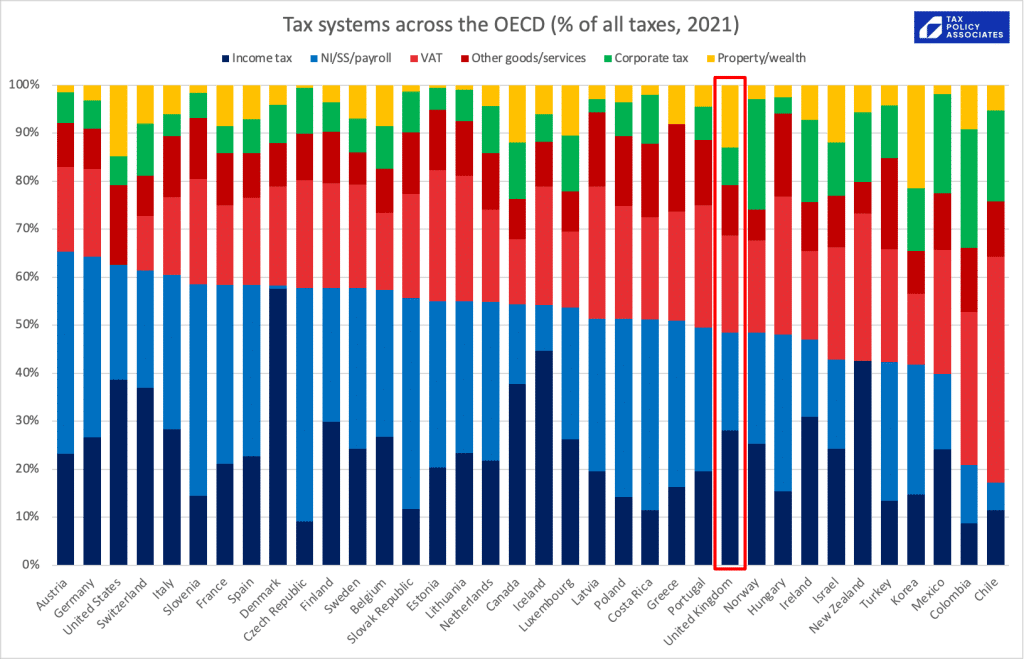

Another way to look at the data is each tax as a % of overall tax revenues. Then the UK looks rather unexceptional, raising proportionately a bit less in personal tax than most of the world, but a bit more in property tax.

So many of the loudest voices in the tax debate are wrong. The UK is not horribly over-taxed. Wealth in the UK is not horribly under-taxed. We have a pretty typical tax system. We could tax a bit more, or tax a bit less, and there are certainly plenty of aspects of the system we could and should improve. But the case for revolutionary change often relies upon an inaccurate picture of how things are now.

These figures include all national, state, local taxes.

This is OECD data, and so (whilst I’m not certain) I don’t believe it will pick up the significant recent UK corrections. There may be similar data issues with other countries.

It’s OECD only, so no Singapore (not an OECD member because it’s not a democracy).

“Property/wealth” is a combination of capital gains tax, inheritance tax, stamp duty/land transfer taxes, council tax, and other recurrent and transaction taxes on property. This won’t quite be an apples-to-apples comparison, because property taxes in some countries pay for services which in other countries you pay for privately (e.g. garbage collection).

“NI/SS/payroll” includes employee and employer taxes (because the economic burden ultimately falls on employees). Also includes such things as the UK apprenticeship levy. Comparisons need to be done with care because some countries have greater private pension provision, and others achieve an economically similar result with income-linked state pensions.

Oil/gas taxation is included in “corporate tax”. You could argue it shouldn’t be; the inclusion is less a point of principle, and more because disentangling it from this dataset is hard.

Small countries like The Netherlands, Luxembourg and Ireland (some would say “tax havens”) somewhat distort the data. Their corporate tax looks high; their GDP (particularly in the case of Ireland) is artificially inflated, so the overall level of tax looks low.

Mexico, Colombia and Chile suffer from a large informal economy and so their personal tax revenues are relatively low, and they are disproportionately dependent on corporate tax and indirect taxes.

Plenty of other factors complicating simple comparisons between countries, e.g. US private healthcare provision being economically akin to taxation but not showing in this dataset.

A few countries haven’t provided recent data yet – Australia, I’m looking at you – and so are missing from the first charts. The animated chart replaces missing data with the previous year (to avoid it looking like the country has disappeared).

GDP data is frequently subject to revisions, both corrections and changes in methodology. The OECD has kindly confirmed that the data we use here reflects all these revisions, and so it is appropriate to e.g. compare the 2021 GDP figures with the 1990 GDP figures.

Following our report on Property118, landlords have been getting in contact and asking what they should be doing. Tax Policy Associates doesn’t, and can’t, provide tax advice – but it’s a fair question. Here’s a quick summary of how we see things:

A landlord whose business looked like this in 2015:

Now looks like rather different – after tax, he’s making a loss:

That’s a huge deal for buy-to-let landlords, and it’s understandable that many are desperate for a structure that fixes the problem. There is no such structure.

There are three choices, and only three choices.

Choice 1: incorporate

Instruct a proper tax adviser, incorporate a company, and move the business to that company. The mortgage interest will then be fully deductible against the company’s corporation tax.

There, however, are several important complications:

Your current mortgage lender is very unlikely to agree to carry your existing mortgage over to the new company. You’ll need a new mortgage, and it will almost certainly be more expensive (higher interest and higher fees). This may add up to more than the tax benefit of interest deductibility. Do the math very carefully.

There will almost certainly be stamp duty/SDLT at up to 15% on the transfer to the company (and another 2% if you’re a non-resident).

Some people claim that married couples can retrospectively claim to be a partnership, and escape SDLT on incorporation using the partnership rules. The recent SC Properties case makes clear this has very little likelihood of working, because of the complete lack of evidence of the married couple in question acting like partners in a business partnership :

“For these reasons we have concluded that the Partnership has no legal reality. It existed as a planning idea in the minds of the Appellants’ advisers and Mr Cooke, but had no substance beyond the forms which were completed in order for it to obtain the tax result suggested by the Appellant’s advisers.”

There may be capital gains tax when you transfer the properties to the company. CGT incorporation relief is potentially available, but you have to demonstrate you have a “business”, something that HMRC do not always accept. Be aware that “clever” structures (such as declaring trusts, creating loans, using LLPs etc) risk blowing up incorporation relief, and costing you much more tax than they save.

The company is taxed on its profit, with a deduction for its interest costs. You then have a second level of tax when the company returns that profit to you, as dividends, wages or (in some limited circumstances) as a capital gain. Again, you need to do the math carefully to make sure you fully take this into account.

Choice 2: don’t incorporate

Continue as you are, bearing the cost of the section 24 non-deductible interest.

Your could reduce your leverage, so you don’t make an after-tax loss (but of course you’ll then need to deploy more capital).

Choice 3: sell-up

It may be that neither of the first two options work – section 24 simply makes your rental business uneconomic. That seems to have been Osborne’s intention.

In which case, you may need to sell-up. It’s not an admission of failure – it’s an admission that investors have to adapt when circumstances change.

What is the fourth choice?

There isn’t one.

Trusts, LLPs, offshore arrangements… not only are they very likely to fail when challenged, but the consequence could be much much worse than if you’d done nothing at all. SDLT plus CGT could easily be a six figure sum. And complex structures can easily have complex, and expensive, additional tax consequences.

Whether you’re a multinational executing a £10bn M&A transaction, or a landlord considering incorporating a one-property business, the key tax question is always the same: “how much do I benefit if this goes right, and how much do I lose if this goes wrong?”.

Even if the Property118 structure probably worked (which it doesn’t!) the downside risk of it going wrong is much, much larger than the benefit.

Unsurprising, if HMRC have never been properly told what precisely the scheme is. Typically promoters are careful to only discuss limited aspects of their schemes with HMRC. Rarely, if ever, is the whole structure explained.

Responds to all technical queries with confident assertions that HMRC has accepted the structure.

Again, it’s doubtful full details were given to HMRC. But, if the scheme doesn’t work technically, then any HMRC clearance is worthless, and the fact they may have sneaked it past one sleepy inspector doesn’t stop HMRC re-investigating it at any time in the next 20 years.

“Our unique system”, “our proprietary strategy”, “our IP”, etc.

I used to advise the largest businesses in the world, doing deals of many £bn. If I’d told them I planned to use anything “unique” or “proprietary”, I’d have been out the door in seconds.

When it comes to tax, sensible people do what everyone else is doing. Be boring.

Any adviser proudly touting their “unique IP” is accidentally revealing a “hallmark” that means the structure may well be disclosable to HMRC as a tax avoidance scheme.

“We have a KC opinion”

Normal people shouldn’t be doing anything so complicated and uncertain that it requires a KC opinion (I’d certainly never put myself in that position).

The fact a KC opinion was obtained is an alarm bell that something high risk is going on. That’s particularly the case if the KC opinion was obtained by the adviser for the adviser. Then you can’t rely on the KC opinion – if everything goes wrong you can’t sue the KC. Worse still, the fact the adviser obtained the KC opinion may make it harder for you to sue the adviser (as they’ll blame the KC). So a KC opinion can actually make your position worse.

“We’ve glowing testimonials from dozens of clients”

This is how a salesman talks.

No discussion of risks and downsides

Any client – whether an individual or the largest corporation – should ask two important questions of a tax adviser. What’s the result if this goes according to plan? What’s the risk if it doesn’t? And how much will it cost me if it doesn’t?

Many of these structures have a relatively small benefit (tax relief on interest) but risk a massive up-front SDLT and CGT cost. Not worth the gamble even if the odds were 70% in your favour (which they won’t be).

Pressure to go ahead/sign a contract

That’s how a (bad) double glazing salesman behaves.

“We’re fully insured”

That’s great – for them.

Professional indemnity insurance protects an adviser against being successfully sued. It’s useful to a client because it gives you assurance that you will still have someone to sue if the adviser disappears/goes bust. But it doesn’t make it easier to sue them, and it certainly isn’t your insurance..

“Your normal advisers won’t be familiar with these obscure rules”

A common tactic to pull clients away from trusted existing advisers, and often said by people who don’t in fact have any tax qualifications.

Property118 is an unregulated adviser which works in a “joint venture” with a barristers chambers called Cotswold Barristers. They promote a tax avoidance scheme aimed at buy-to-let landlords. But nobody involved appears to have any tax qualifications and in our view the scheme fails spectacularly.

This report explains the scheme, and explains why in our view, and that of the mortgage lenders’ industry body, it is likely to default the landlord’s mortgage. We also set out a detailed analysis of the serious tax problems with the structure. We are going into more technical detail than usual given the widespread promotion of this scheme in the market. Anyone who has entered into these arrangements should seek independent advice.

UPDATE: 16 September. Property118 have responded to this report. Despite having two months’ notice of our findings, their response contains no response to any of the points we’ve made, just assertions that their structure is fully compliant, and that HMRC and lenders have never challenged it. As we note below, we doubt the structure has ever been properly disclosed to HMRC or lenders. Now HMRC and lenders is aware of the structure we expect challenges over the coming months and years.

UPDATE: 22 September. We’ve a further report on another aspect of Property118’s planning.

UPDATE: 5 October. See also our report on Less Tax for Landlords. A different scheme, but with some commonalities; in many senses an even worse scheme than Property118’s.

UPDATE: 24 October. Mark Smith of Cotswold Barristers published a response on the s162 point, but one which does not address the key problem with the structure. We’ve updated the text below.

UPDATE: 9 November. The analysis below is of the structure Property118 intended to implement. Our review of their actual documentation reveals several critical implementation failings which means the actual position of their clients is likely significantly different, and significantly worse. We analyse this here. This means that much of what follows below is likely academic.

UPDATE: July 2024: HMRC have issued a “stop notice” making it a criminal offence for Property118 to continue to promote the structure.

The sales pitch

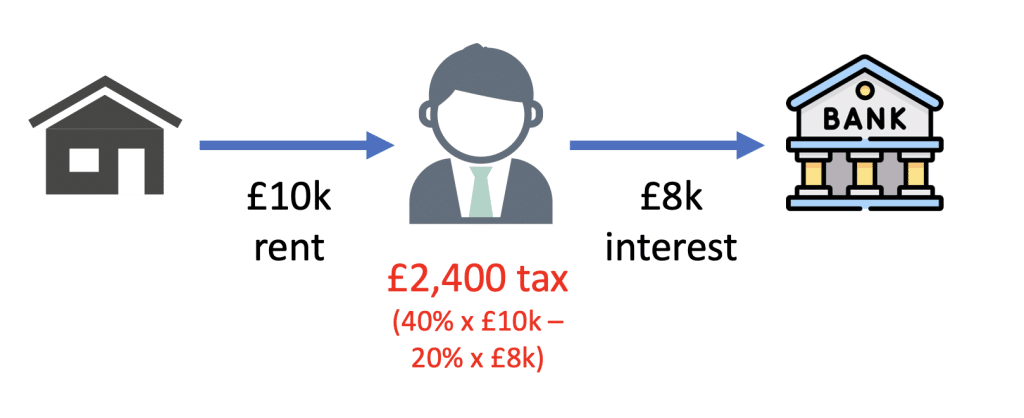

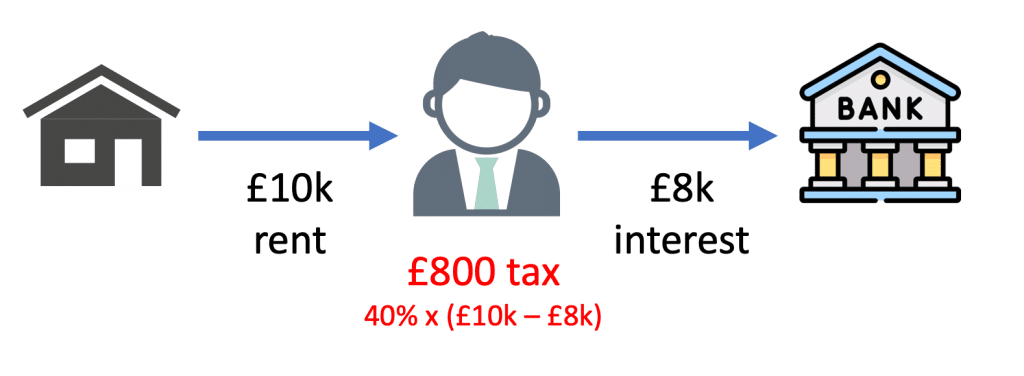

Most buy-to-let landlords hold their properties personally. So they pay income tax at 40% or 45% on the rental income. Until 2017, their mortgage interest was deductible, meaning a result something like this:

Many landlords view this as unfair, because the £2,400 tax is more than their £2,000 net income (although the purpose of the rules was expressly to discourage buy-to-let mortgages, so this rather punitive outcome is actually the point).

The obvious move is to hold the properties in a company. Corporation tax is less – below 25%, for a small company1 and companies get full tax relief for mortgage interest.2

But it’s not easy for a buy-to-let landlord to move their properties into a company. There can be capital gains tax and stamp duty land tax (SDLT) on the way in. And – most seriously – the mortgage lender won’t allow the existing individual mortgage to move to a company. You could get a new mortgage, but mortgages for companies are significantly more expensive than buy-to-let mortgages. 3

Advisers therefore frequently caution clients that the increased interest cost of moving properties to a company can easily exceed the tax saving. It’s often a mistake to be over-focused on tax savings.

The Property118 solution

Wouldn’t it be wonderful if you had all the tax benefits of moving to a company, but could keep your existing bargain-price mortgage?

Property118 say you can, with what they call the Substantial Incorporation Structure:

The landlord – let’s call him X – sets up a new company (which I’ll call the Company), and sells the properties to it, getting shares in return

But “completion” of the sale is deferred – X remains the registered owner of the properties. A trust is created, with the landlord as trustee, and the company as beneficiary.

This is invisible to the world – and to the mortgage lender. So X doesn’t ask the mortgage lender for consent, or even tell the mortgage lender about it.

Property118 claim that, because the transaction creates a trust, it’s not a breach of X’s mortgage.

They claim that “incorporation relief” applies so there’s no capital gains tax.

Often they say that X and their spouse were in a partnership, so SDLT partnership rules apply and there’s no SDLT to pay either.

X continues to make mortgage payments to the lender but, behind the scenes, the Company agrees to reimburse/indemnify X. The Company claims tax relief for those payments. So – claim Property118 – it’s just as good as if the Company had borrowed itself.

But it’s better – because they say this isn’t just a company – it’s a “Smart Company“. The idea is that the Company issues shares to X’s children which supposedly have no initial value, but will grow in value over time. So future increase in the value of the property portfolio will fall outside X’s inheritance tax estate.

The end result is that, by signing a piece of paper, X gets a dramatically better tax result with no downside:4

What actually happens – the short version

The structure doesn’t work.

The sale likely puts the mortgage into default. The mortgage terms usually require consent for the sale to the Company, and that wasn’t obtained.

We asked UK Finance, the trade association for mortgage lenders, and they said:

“Transferring ownership of a property into a trust without informing your lender and seeking their consent would most likely be a breach of a mortgage’s terms and conditions.”

The tax will also go badly wrong.

Property118 have forgotten that X is still there, still paying £8k to the bank, but now receiving £8k of new income in the form of the indemnity payments. Those indemnity payments are fully taxable, but the bank interest isn’t deductible for him (because X no longer has a property business; he has no basis to claim any tax relief).5

So the structure increases the overall tax bill by 50%.

It gets worse. There is potentially also a large up-front tax hit of a large amount of CGT and SDLT when the structure is established. That could amount to hundreds of thousands of pounds.

And then an ongoing requirement to file an annual tax on enveloped dwellings (ATED) return, which is easily missed – failure to file creates late-filing penalties of £1,600 per year.

In our opinion this structure is a disaster.

We’ve set out the legal analysis of these issues in detail below.6

Is this tax avoidance?

Yes.

The “Substantial Incorporation Structure” has no benefit to the landlord other than (supposedly) saving tax. It will therefore be regarded as tax avoidance by a number of statutory anti-avoidance rules, which will potentially negate the tax benefits (if there are any, which there probably aren’t).

This is by contrast with a normal incorporation, which absolutely does have other benefits for the landlord. In particular, it segregates legal liability: if the landlord is sued by the lender or by a tenant, then if the properties are held in a company, that liability will normally not attach to the landlord personally. A normal incorporation is not usually tax avoidance, even if it has tax benefits.

However, the substantial incorporation structure does not achieve legal segregation. As far as the lender, the tenants, and the world are concerned, the landlord remains personally the owner of the properties and therefore as a legal matter remains personally liable.7

Property118 and Cotswold Barristers

Property118 and Cotswold Barristers often charge fees of over £40,000 to relatively small landlords earning less than £100k/year. They’re set up to get referrals from other websites, paying £2,000 for a click that results in new business – meaning that they’re widely promoted by other firms (for example here).

For £40,000 you could expect to instruct a well-known accounting or law firm, staffed by qualified tax lawyers/accountants.

But neither Property118 nor Cotswold Barristers appear to have any members or employees with tax qualifications or experience. Property118 is entirely unregulated. I had a very confusing exchange of emails with Mark Alexander, head of Property118, in which he didn’t appear to have even heard of the two main tax qualifications: ATT and CTA.8

The head of Cotswold Barristers, Mark Smith9, is a generalist whose practice ranges from business law, to tax, to criminal defence work, to private prosecutions (including one where he was suspended by a month by the Bar Standards Board for acting negligently and “failing to act with reasonable competence“). His profiles in 2017 and 2020 don’t include tax in his areas of practice.

Barristers chambers usually list their members – the members being the whole point of the chambers. Cotswold Barristers is unusual in not doing this. It did at one point – and included as part of its team a fake barrister with a dubious past who was jailed for conning a dying woman out of her life savings. There is no suggestion that Cotswold Barristers was aware of his actions, but Cotswold Barristers does appear to have been responsible for listing him as part of its team.

The reference to “delegated authority” is strange. The claim that a non-barrister could be bound by Bar professional standards and be subject to the Bar Standards Board has perplexed all of the barristers we’ve spoken to.

We put this to Mark Smith of Cotswold Barristers. He said:

“Barristers must disclose, to the BSB and clients, any associations they have with people or entities in their provision of legal services. This is a code of conduct requirement. This was complied with at the outset of our relationship with Property 118 (P118). It has recently (Jan-Mar 2023) been re-examined by the BSB as part of a routine audit of Cotswold Barristers (CB) following an update of the BSB’s Transparency Rules. We had correspondence with the BSB about this, and they were and are satisfied our association is compliant. We did review the wording relating to ‘delegated authority’ at that point, as it was ambiguous. P118 has since amended this portion of their materials, so it makes it clear their consultants only work under delegation when the client has engaged with CB. Again, so long as it is made clear to the client, and the barrister is ultimately responsible, sub-contracting of work is permitted under the Code of Conduct.”

We don’t see an ambiguity: we think the claim that Property118 are bound by Bar professional standards, and subject to the BSB, is false. We asked Mr Smith to explain this claim, and he did not respond.

We’re writing to the Bar Standards Board to see if they can cast any light on these issues. We are also asking them to look into the wider question of why Cotswold Barristers are giving legal and tax advice that is obviously wrong.

Professional indemnity insurance

Property118 say that their barristers’ professional indemnity insurance means their clients are “shielded from financial risk”:

That’s not at all how professional indemnity insurance works. If the tax structure turns out to be the disaster we think it is, and the client wants to recover their loss, they have to successfully sue the barrister for negligence. That’s never a straightforward undertaking; not least because the barrister would presumably deny causation on the basis that you would have followed Property118’s advice even if Cotswold Barristers hadn’t been involved. And Property118 aren’t regulated, are unlikely to have any insurance, and probably aren’t good for the money (its owner lives in Malta).

The mortgage problem

Property118 say their structure is “fully compliant for mortgage purposes”:

However this appears to rely significantly on not telling lenders that their security has become the subject of a trust:

We asked UK Finance, the representative body for mortgage lenders, what they thought of the structure. They said:

“If someone wishes to transfer ownership of a buy to let property they should contact their lender to discuss whether this is permitted under the terms of any mortgage on the property. Transferring ownership of a property into a trust without informing your lender and seeking their consent would most likely be a breach of a mortgage’s terms and conditions.”

We believe UK Finance are clearly right on this. But even we didn’t agree, we’d suggest that it’s not a good idea to enter into a structure which your lender believes most likely breaches the terms of your mortgage.

Property118 and Cotswold Barristers seem to be in denial. They tell their clients:

The idea a lender can’t require repayment of a mortgage when it is in default is very strange. The 2016 Court of Appeal case they cite concerned whether a lender could require repayment of a mortgage when there was no default. We don’t understand how Property118 can make this claim when their own founder was the claimant in the case.

The problem with the trust

Property118 do seem aware there could be an issue with declaring a trust that shifts beneficial ownership to a company without telling the mortgage lender. They say:

There’s a similar theme on the Property118 website:

Is this an accurate reflection of most mortgage T&Cs?

One of our team undertook a very fast and incomplete review of major mortgage lender BTL T&Cs, carried out in about one hour.11

So the specific claim there are only two lenders with prohibitions is false.

But the larger problem is more basic. This is the key claim made by property118 (highlighted in blue):

The “Barrister-At-Law” will be Mark Smith of Cotswold Barristers. He takes the same approach: “as a matter of law, unless it says specifically in the terms and conditions [that] you can’t do it, then you can”.

This is not how English law security documentation works. The mortgage terms don’t need to have a specific prohibition on declaring a trust. All that’s required – and this is common – is to simply prohibit the sale or transfer of the property, and define “property” so it includes all interests, meaning the beneficial interests that would be transferred by a trust.

Other lenders have a general transfer of ownership prohibition which is drafted broadly enough to capture trusts and sales of beneficial interest. For example, TSB:

After undertaking this review, we spoke to a series of experienced real estate finance lawyers, who act for lenders and borrowers on everything from small domestic conveyancing transactions to the largest commercial real estate transactions. It was their unanimous view that, one way or another, a trust would be prohibited by most and possibly all mortgage T&Cs.

We put this point to Property118 and Cotswold Barristers, and specifically gave one of these mortgage terms as an example. They declined to explain their position as a legal matter, instead asserting that large conveyancing companies agreed with them, and that no bank had ever raised the point. That, again, does not answer the question. The large conveyancing firms are built to handle straightforward conveyancing at scale, not to answer technical queries on unusual trust arrangements. Mortgage lenders will not raise the point unless they become aware of it. Until now, we don’t believe they were. However, we briefed the mortgage lenders’ representative body, UK Finance, on the structure, and their view is now clear:

“Transferring ownership of a property into a trust without informing your lender and seeking their consent would most likely be a breach of a mortgage’s terms and conditions.”

It is therefore reasonably clear that entering into this arrangement without the consent of the lender likely defaults the mortgage.12

Legal and tax analysis – capital gain

X probably has a large latent capital gain in the properties. For example, if X’s acquisition cost of the portfolio was £4m, and X sold it now for current market value of £8m, X would have a £4m capital gain, and pay £1.12m CGT.

But Property118 claim their Substantial Incorporation Structure means that CGT incorporation relief applies.

That would have two very nice outcomes for X. First, there’s no CGT at all to pay on the transfer to the Company. Second, the capital gain is “rolled over” into the shares in the Company, so that any sale of the shares is subject to CGT broadly as if X had held them all along. The latent capital gain of the properties themselves is eliminated – the properties are “rebased” to current market value. So if the Company sold the properties for £8m, there would be zero tax to pay.

However, there is considerable doubt whether incorporation relief will apply.

The legislation requires that “the whole of the assets of the business” move to the Company. And that’s not happening13

The problem here is that legal title in the properties is being left behind. This is not some minor legal formality; legal title over real estate has reality and value to it. You can’t borrow without legal title. You can’t refinance. You can’t sell. In many “bare trust” cases this is a distinction without a difference, because the beneficiary can call for legal title at any time. Here they cannot, because the consent of the mortgage lender would be required. The Company’s inability to acquire legal title is a real constraint on its business – and that demonstrates that it did not in fact acquire the “whole assets of the business”.14

Another way of putting the same point is that there is no transfer of a “business as a going concern”, just an economic transfer under a trust. The “business” is operated by the person with the legal title, as it’s that person who has all the dealings with the tenant, bank, service providers, etc. This “business” isn’t moving at all.

So our view is that incorporation relief likely does not apply.15

(In many cases there will also be doubt as to whether X’s activity as a landlord is enough to constitute a “business”.16)

UPDATE: Mark Smith finally published a specific response to this point on 20 October 2023. He makes the obvious point that capital gains tax normally looks to beneficial ownership, not legal ownership, when considering whether a disposal has been made. But section 162 is not looking at whether a CGT disposal has been made – it uses the terms “whole assets of the business” and “transfers… a business as a going concern”. We read these as factual tests. And, factually, significant elements of the business remain with the landlord. Only the landlord can deal with the lender, the tenants, letting agents, and other contractual parties. The business of the company is very different – it’s just a passive investor. We made this point above; Mr Smith does not attempt to respond to it.

Mr Smith again makes the claim that HMRC have accepted the position. This would only be relevant if the true nature of the structure was disclosed to HMRC, and the s162 point above specifically drawn to HMRC’s attention. We doubt that is the case, but even if it was, it would only provide comfort to the taxpayers specifically covered by that correspondence. HMRC would not be bound for other Property118 clients.

There is therefore, as ever, no substitute for properly considering the legal position.

Legal analysis – SDLT

On the face of it, SDLT17 is due on the transfer of the properties by X to the Company, on the full market value at a marginal rate of up to 15%.18 That’s potentially a huge up-front cost. There’s a relief for partnerships incorporating, but not for individuals incorporating.

In many cases, SDLT would make the Substantial Incorporation Structure uneconomic, with a large up-front tax cost. Here’s the Property118/Cotswold Barristers solution:

It’s to claim that, where a husband and wife run a property rental business together, in fact they’ve always been a partnership, and partnership relief is available. They do this, even in cases where there was no partnership agreement, no partnership tax returns, and no extraneous evidence of any kind that a partnership existed. Technically that does not make it impossible that there was a partnership – it’s a question of fact. But the recent SC Properties case shows just how difficult is to establish a partnership in such circumstances – and the burden of proof is on the taxpayer. It is usual for a married couple to manage their financial affairs together, but that does not normally mean there is a partnership in the legal sense. Relations between spouses are very different from the business relations of partners in a partnership.19

If SDLT were payable (because the properties are not partnership property), then interest and penalties for late filing would be due. Although multiple dwellings relief would usually be available to reduce the SDLT charge, this relief is unavailable if it is not claimed in a return or an amendment to a return. And an SDLT return cannot be amended more than one year after the filing date for the transfer. If any of the properties were occupied by X or his relatives (or not held for a qualifying business purpose) the SDLT rate on that property would be 15%.20

In our view, it will only be in rare cases that this strategy succeeds, and SDLT relief applies – and HMRC guidance suggests that HMRC are likely to contest the point.21

Finally, although no annual tax on enveloped dwelling (ATED) would be payable to the extent that the properties are let out to third parties, ATED relief must be claimed. It is unclear to us if Property 118 advise their clients to file ATED returns (our sources have not seen such advice). Failure to file triggers late-filing penalties of up to £1,600 per return per year. For companies that used these arrangements over five years ago, it might come as quite a shock that they are liable to £8,000 of penalties even though no ATED is due.

Legal and tax analysis – taxation of the interest payments

Property118 and Cotswold Barristers say:

They make a slightly different claim in the video below: that the “legal owner continues to make mortgage payments (as nominee of the beneficiary) and claims the payments back from the beneficiary as out of pocket expenses, which are tax free”.

But that is not right at all. X, the legal owner, is not the “agent” or “nominee” of the Company under the loan – X remains the borrower under the loan in their own right. You cannot declare a trust over obligations. What is actually happening is that the Company is making indemnity payments to X, which pays the mortgage lender (and this is the case as a legal matter even if, as I suspect, there are never any cash payments from the Company to X). X therefore remains taxable.

When we look at the actual legal and tax analysis that follows from this, the entire structure falls apart.

Deductibility of interest paymentsfor the Company

Mark Smith says in this video that the payment is “deductible in accordance with normal corporation tax principles”. That’s not correct.

The corporation tax treatment of debt is governed by the loan relationship rules in Part 5 of Corporation Tax Act 2009. For these rules to apply, the Company must have a “loan relationship”, for which it has to be “standing in the position of debtor under a money debt” which must “arise from a transaction for the lending of money“. But the Company doesn’t have a money debt and never borrowed any money – it’s just making indemnity payments. There is only one loan, and that was from the mortgage lender to X – and it’s still there.22

So the Company doesn’t have a loan relationship and will not achieve a deduction under the loan relationship rules.23

It might achieve a deduction under the general rules for a company carrying on a UK property business. That requires the indemnity payments to be recognised in the accounts and for the indemnity payments to be regarded from a tax perspective as income of the property business and not as further consideration for the capital transaction of the original acquisition of the beneficial interest. We don’t think either is a straightforward point. 24

So it cannot be assumed that the Company will achieve a deduction for its indemnity payments. If it doesn’t, we are in a worst-case scenario for X which looks like this:

More than doubling X’s original £2,400 tax bill. Not a good result.

Even if the Company does achieve a deduction, the result is still worse than the original £2,400 of tax:

We put this point to Cotswold Barristers. They asserted that the payment was deductible but were unable to explain how or why.

Taxability of indemnity payments

We can immediately dismiss the explanation in the video – that X is receiving tax-free out-of-pocket expenses. That would be the case if the loan had been entered into by X as trustee for the Company. But it wasn’t – the loan was simply entered into by X and X alone, and the trust can’t change that). The payments X makes to the lender are not trust expenses – they’re X’s personal expenses. And no agreement X signs with the Company can change this – you can’t transfer an obligation, or create a trust over an obligation.

That’s a big problem. X no longer has a property business (because he is a mere trustee). So X has zero basis for claiming a deduction on the interest he pays the bank. But he is now receiving a stream of indemnity payments under a legal obligation. They will be taxable (perhaps as “annual payments“, perhaps as “miscellaneous income“). That creates a large tax charge for X – it’s the worst-case outcome we show above.

We see only one potential counter-argument: to say that the indemnity payments actually form part of the consideration for the original sale,25 and so are capital and not revenue items. If so, and the original sale was exempt from CGT, then there’s no additional tax to pay; but the consequence of this argument is that the Company absolutely won’t get a tax deduction for its indemnity payments (because they must be capital payments too). That results in this, which we think is the best-case outcome of the Substantial Incorporation Structure:

Note that the best-case outcome here (which we’d expect HMRC to resist) is still worse than the original £2,400 tax bill. You’d have been better off doing nothing.

Or, if the original sale was subject to CGT then probably26 each indemnity payment is subject to CGT at 28%, resulting in this bad-but-not-quite-worst-case outcome:

We put this point to Cotswold Barristers. They were unable to explain why the indemnity receipts weren’t taxable, but said that HMRC had never raised the point. We expect that is because the issue has never been properly disclosed to HMRC.

Back in 2019, Mark Smith gave a mystifying explanation in a now-deleted video:

“Finance costs accrue to the beneficiary, the company pays the expense of running the mortgage and it’s deductible on normal corporation tax principles. You don’t even have to change your direct debit or standing order payments, because you are allowed to receive the money for the mortgage repayments from the company as their agent without it being taxable in your hands, as long as at some point it flows through the company books, the company bank account, it’s only taxable by the company. You only receive the money as their agent, you make the payment as the company’s agent. And there’s a fallback position. Even if HMRC tried to tax you on it, you only pay tax at trustee rates, which basically washes out any impact of having to pay tax on it because you get the tax credit back again at 20% basic rate.”

This is gobbledygook. The individual is not the company’s agent when making mortgage payments – the individual entered into the mortgage as principal. The mortgage doesn’t form part of the trust – you can’t declare a trust over an obligation. The trust rate (and associated credit rules) apply to settlements, not bare/simple trusts – they cannot apply to this structure (and if the arrangement was a settlement there would be an array of other consequences, mostly adverse).

Legal and tax analysis – inheritance tax

Cotswold Barristers send clients materials presenting them with extraordinarily large (and unrealistic) inheritance tax calculations. We’ve seen one projecting that a client’s portfolio of under £10m would be worth £200m in ten years’ time, so with a potential inheritance tax bill of £80m. This is, at best, sharp practice and, at worst, misselling.

They say that the advantage of their Smart Company solution is that:

So you say the property portfolio is currently worth £10m, and issue shares which are worth the value of the portfolio minus £10m. Those shares are therefore worth £0 today (you claim), and you can give the shares to your children with no inheritance tax or capital gains consequences. But if the portfolio did become worth £200m in ten years’ time, the shares would be worth £190m. More magic.

The flaw in this is that the shares plainly aren’t actually worth £0 when created. It’s easy to test this: would they sell them to Tax Policy Associates for £1,000? That’s a fantastic deal for them, if the shares are really worth nothing. But obviously, nobody would take up that offer – because there’s a large expected capital appreciation embedded in the value of the shares. And that’s the tax conclusion too: the shares have a large current value equal to the discounted expected capital appreciation. We’re aware of two cases where shares of this kind have been litigated, and the contention that the shares were valueless failed (with, in one case, the Tribunal actually giving the shares a seven-figure value).

That means this structure probably has immediate inheritance tax and capital gains tax consequences (possibly also consequences under the “employment related securities” rules).

A further twist:

Cotswold Barristers and Property118 often advise putting these shares in a discretionary trust. We’ve seen them recommend “Creation of a Discretionary Trust controlled by you via a Letter of Wishes to shelter all future capital growth in the portfolio from Inheritance Tax”.

A “discretionary trust controlled by you” isn’t a trust – it’s a sham.

And another twist:

Part of the idea seems to be that shares are being created for children, so they can receive dividends and pay less tax than the parents (because of their allowances and lower tax rates). But there are specific rules that stop this.

DOTAS

Given that the main (and perhaps sole) purpose of Property118’s scheme is tax avoidance, it seems likely that their structures should be registered with HMRC under DOTAS – the rules requiring disclosure of tax avoidance schemes.

Cotswold Barristers told us that HMRC considered this point in 2021 and did not take it forward.

We would query if Cotswold Barristers made HMRC aware of the size of their fees. A “premium fee” (being a fee which is more than the time value of the work carried out) is one of the hallmarks which can trigger DOTAS.

Another DOTAS “hallmark” is where it is reasonable to expect a promoter would wish an element of the arrangements to be kept confidential from any other promoter. Property118 sent us correspondence refusing to explain elements of their structure, because it was “valuable intellectual property”. That may amount to an (accidental) admission that the confidentiality hallmark applies.

Failure to comply with DOTAS can result in fines of up to £1m.

More strange Property118 advice

The Property118 website has other examples of tax planning that raises alarm bells, because it has no reasonable prospect of success. We’ll mention just two examples:

Capital gains value shifting

The capital gains tax avoidance below ignores the existence of a specific anti-avoidance rule:

An entirely artificial step is used to reduce the capital value of the shares, and then immediately re-inflate it. There are very longstanding rules to counter such “value-shifting” transactions (as well as a plethora of other statutory rules, plus common law anti-avoidance principles).

The structure as presented in our view has no reasonable prospect of success.

UPDATE 22 September: after this report was published we found more details of this scheme, and it turns out to be rather different from the description above, and much worse. We’ve written a short analysis of this here.

SDLT avoidance

This page suggests that SDLT can be reduced when acquiring a “house in multiple occupation” (HMO), i.e. where many people have separate bedrooms but there is one front door and usually one living room. The idea is that “multiple dwellings relief” applies.

That is, however, wrong – MDR applies only where there are separate dwellings, and a bedroom is not a dwelling. That was fairly obvious when the page was written in 2020. It is more obvious now, as an Upper Tier Tribunal has ruled on the point.27

What if you’ve entered into a Property118 scheme?

We would strongly suggest you seek advice from an independent tax professional, in particular a tax lawyer or an accountant who is a member of a regulated tax body (e.g. ACCA, ATT, CIOT, ICAEW, ICAS or STEP). Given the potential for a mortgage default, we would also suggest you urgently seek advice from a solicitor experienced with trusts and mortgages/real estate finance (e.g. a member of STEP).

We would advise against approaching Property118 given the obvious potential for a conflict of interest.

Property118 and Cotswold Barristers’ response to this article

It is common practice to give the subject of a report or investigation 24 hours to respond. The response we received from Property118 was unusual in several respects. We set it out below in full.

The initial response was a request from the CEO of Cotswold Barristers to join a recorded Zoom call: “Why won’t you come on video and ask your questions? The public deserve to make their own assessment”.

Property118 then failed to respond to any of the technical questions we asked.

Cotswold Barristers responded, but leant very heavily on the claim that their approach has been accepted by HMRC and other accounting firms. We are sceptical that full disclosure was ever made to HMRC; if you approach HMRC for a clearance but don’t mention all the facts, or all the technical issues relevant to the clearance, then any clearance you get cannot be relied upon.28 And HMRC clearances can never be relied upon where there is tax avoidance.

The final response was a vague legal threat: “Your continued blackmail is noted and our response to any damages caused to our businesses by your future actions will be dealt with accordingly.”

In the interests of transparency, we set out the correspondence in full below. The thumbnails should expand when you click on them. Alternatively, the correspondence can be downloaded as a PDF here.

Our original query:

The initial response from Property118, including HMRC correspondence29, customer testimonials, a complaint about the timescale and a vague legal threat:

The clerk/CEO of Cotswolds Chambers responded by suggesting a recorded Zoom call, because that’s “what the public would expect in 2023”:

We then received a letter from Mark Smith. This responds to our queries about the unusual relationship between Property118 and Cotswolds Barristers by referring to a recent BSB audit (discussed further above). Mr Smith responds to our CGT incorporation relief criticism by misunderstanding the s28 deeming rule; otherwise there is little in the way of technical content. For the most part, the response is “no one else has complained“:

We asked for a specific response to the technical points we had made:

Smith asks for two weeks to respond to our email. When we say that’s not realistic, and these are points they should already know the answers to, Mark Alexander sends a somewhat intemperate response:

Then a more detailed response, with a long list of people he works with (names redacted out of fairness to the individuals):

And finally a vague legal threat and accusation of blackmail:

Many thanks to G and S for bringing this to our attention. Thanks to J, T, F and BM for their help with the mortgage aspects, as well as UK Finance. Thanks to E for trust law expertise, T for insurance law input, H, S and O for the barrister conduct issues, A and Sean Randall for the specialist SDLT input, and C for advice on the direct tax/indemnity point. Thanks to Pete Miller, who wrote on the incorporation relief point three months ago, and independently reached the same conclusion as us. Pete and Sean also kindly reviewed a draft of this report, and provided invaluable feedback. J kindly provided some technical corrections after the initial version of this report was published. And thanks to Ray McCann (former senior HMRC inspector and past President of the Chartered Institute of Taxation).

We rely upon the goodwill and expertise of a large number of tax professionals, only some of whom we can name. As ever, Tax Policy Associates takes sole responsibility for the contents of this report.

The rate is 19% for profits under £50,000, with a “catch-up rate” of 26.5% on profits up to £250,000, so that the overall effective rate smoothly transitions into the full rate of 25% ↩︎

Obviously you will want to get the money out at some point, but being able to defer and roll up low-taxed income is valuable in itself ↩︎

Because a landlord can walk away from a company in a way that they cannot walk away from a personal mortgage ↩︎

We have established this is their structure from published information on the Property118 and Cotswold Barristers websites (e.g. this brochure, and here, here, here, and here) as well as copies of their advice we received from our sources. ↩︎

This is perhaps the most likely of a number of possibilities, all discussed further below ↩︎

In the interests of concision, we don’t go into one somewhat difficult point: the effect of a sale when that sale is prohibited by another contract (the mortgage). The Don King v Warren case is general authority for the proposition that such a sale will still be effective in equity, and we expect that will be the case here. However the issues are not straightforward; and if we’re wrong, and the sale is not effective in equity, then essentially nothing has happened from a tax perspective, and it’s as if the transaction never happened. No tax benefit, but also none of the unfortunate results we go into below. ↩︎

the landlord may be able to recover from the company under the indemnity, but if the companies’ assets are insufficient, the landlord will remain on the hook. There are, therefore, no liability advantages from the substantial incorporation structure, compared to, if the landlord just held the properties personally. ↩︎

In an earlier (and unrelated) LinkedIn discussion, Mark Smith, head of Cotswold Barristers, hadn’t heard of the term “tax set” – i.e. he was unaware that there were specialist tax barristers’ chambers. ↩︎

Not to be confused with Mark Smith, the respected extradition barrister. ↩︎

This is from a document they sent to a client a few months ago ↩︎

Caveat: our team only had English expertise; the law is different in Scotland and Northern Ireland and therefore none of the analysis in this section applies to it; however given that Property118’s English lawyers get the English law position wrong, it would be optimistic to assume that they have the Scots and Northern Irish position right ↩︎

The original version of this report also discussed the potential for the trust to invalidate the buildings insurance of freehold property, which would be another mortgage default. Our was undertaken by insurance specialists but has been questioned by others with expertise in insurance law. This report is intended to reflect a consensus view of relevant experts, and therefore (given there is at least some doubt as to the position) we have removed that text. The general point about mortgage defaults (for both freehold and leasehold property) remains, and it is this point that UK Finance are referring to. ↩︎

An additional problem is that the liabilities of the business are not being transferred; rather they are being covered by an indemnity from the Company, and that means the consideration does not just consist of shares (which s162 requires). On the face of it, that prevents incorporation relief applying. There is an HMRC concession that HMRC do not take this point (ESC D32). That is very convenient (and necessary) for the Substantial Incorporation structure. But two important niggles: (1) there is no technical basis for ESC D32 and therefore, following the Wilkinson case, it’s unclear how HMRC can continue to apply it, and (2) a taxpayer engaged in tax avoidance cannot rely upon any HMRC concession or published practice (a point HMRC go out of their way to stress in their guidance). ↩︎

Similar issues may arise with other assets of the business which are staying put as a legal matter but (presumably) purportedly being assigned in equity: e.g. buildings insurance policies, tenancy agreements, letting agent agreements, the right to recovery of . The legal title that is being left behind is an asset, and not a valueless one. A business that only has equitable title to the core elements of its business is not the same as a normal business. A landlord is also subject to a large number of regulatory requirements around deposit protection, fire safety, etc – and these obligations will remain with the landlord as legal owner. ↩︎

Cotswold Barristers’ response was that there was a deemed CGT disposal of legal and beneficial title day one, and so the whole assets of the company were deemed to be transferred. We don’t think that’s defensible. Section 28 is a rule which sets the time of a disposal for CGT purposes. It is not some wider deeming rule which deems an asset to have been actually transferred on a different date. Incorporation relief refers to “transfer” (the legal/commercial concept) and not “disposal” (the CGT concept). This is therefore a misreading of section 28. The courts havealways held that deeming rules should be restricted to their statutory purpose.) UPDATE: Property118’s own KC ended up agreeing with us on this point ↩︎

or the equivalent devolved taxes if one or more of the properties is in Scotland or Wales ↩︎

That’s including the 3% surcharge for purchases of dwellings by companies. In some cases we would also need to add the 2% increased rate for non-resident transactions. ↩︎

Section 2(1) of the Partnership Act 1890 is clear that joint ownership is not enough, and sharing profits is not enough. It’s the relationship between the parties that is key. This is something that Smith and Property118 appear to overlook. ↩︎

Plus the 2% increased rates for non-resident transactions, if applicable). ↩︎

There may be other potential attacks on the “retrospective partnership” strategy using anti-avoidance legislation and principles ↩︎

The obvious way to test the loan relationship point is to ask whether the Company can be sued by the mortgage lender; the obvious answer is that it cannot. Note that whether there is a “loan relationship” or not is a legal test, not an accounting test – even if the accounts here show the Company as party to a loan, it won’t have a loan relationship ↩︎

One correspondent raised a plausible argument to the contrary: condition C in s330A CTA 2009 applies on the basis that there was a “transaction which [had] the effect of transferring to the company all or part of the risk or reward” of the mortgage (this is not an argument Property118 has made; there is no evidence they are aware of any of the provisions of the loan relationships rules). We are, however, doubtful that an indemnity has that effect – it is cashflows which are (economically) transferred, not risk/reward. An indemnity is economically and legally distinct from defeasance. Financing cost indemnities are often seen on commercial transactions, and the idea s330A applies to such arrangements would be novel. It is, furthermore, unclear if X would benefit even if s330A applied. It seems likely that the main purposes of the arrangement are to enable the Company to obtain a tax advantage; on that bass, s455C would apply to deny the deduction ↩︎

A better argument Property118 could make is that the company doesn’t need a deduction for the indemnity payment, because under the trust it’s only entitled to the net rent (after mortgage payments are made). That, however, is contrary to the nature of a bare trust – see e.g. the HMRC guidance here↩︎

Property118’s actual implementation is unclear. We have seen some documentation which states that the indemnity payments are consideration (which we expect is the intended outcome). However we have also seen a legal advice note from Mark Smith in which he says that the consideration is the issue of shares equal to the market value of the property (i.e. with no deduction for the debt) – we do not know if this was a on-off mistake, or reflects a general confusion as to the legal character of the transaction ↩︎

“Probably” because we think the uncertainty as to how long the mortgage will remain in place probably makes the stream of indemnity payments “unascertainable future consideration”, charged to CGT when each payment is made. But there’s a risk that, at least in some cases, it’s not unascertainable (for example, if the mortgage doesn’t have long to run). In that case, the stream of indemnity payments would have to be calculated and added to the original disposal consideration, with no discount applied – potentially a really bad result ↩︎

There is also a technical problem with the claim on this page, which Sean Randall (an experienced SDLT adviser and Chair of the Stamp Taxes Practitioners Group) explained here – with an unconvincing response from Property118. ↩︎

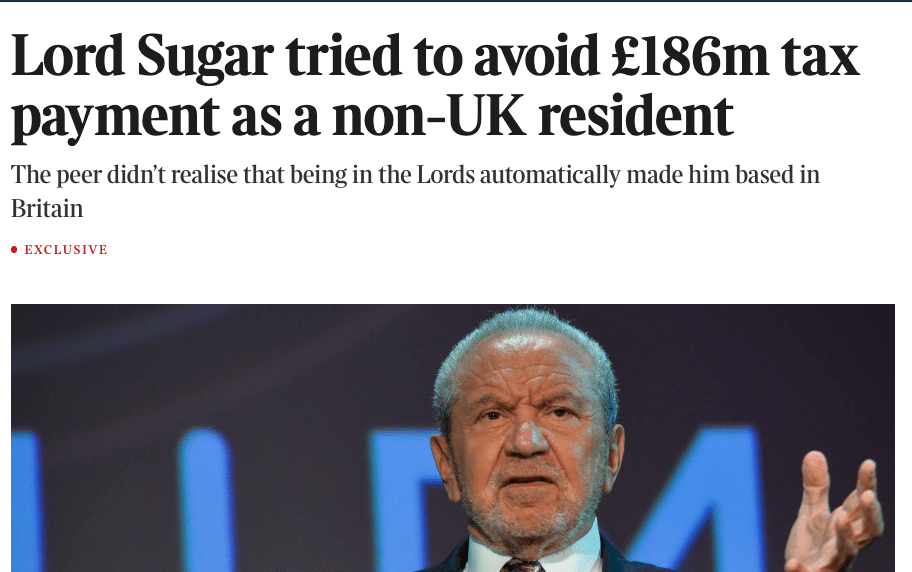

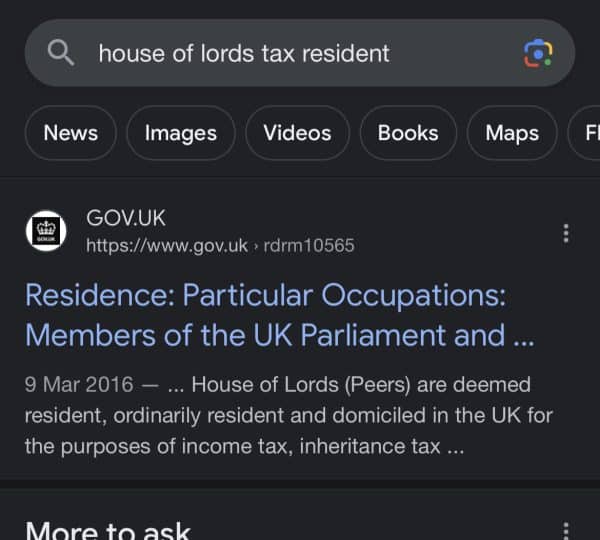

The Sunday Times has a remarkable story that Lord Sugar tried to avoid tax by leaving the UK for Australia. The idea was that he’d cease to be UK resident, and so would escape £186m of tax on some very large UK dividends.

Somehow neither Sugar, his team, or his advisers ever thought to do a simple Google search:

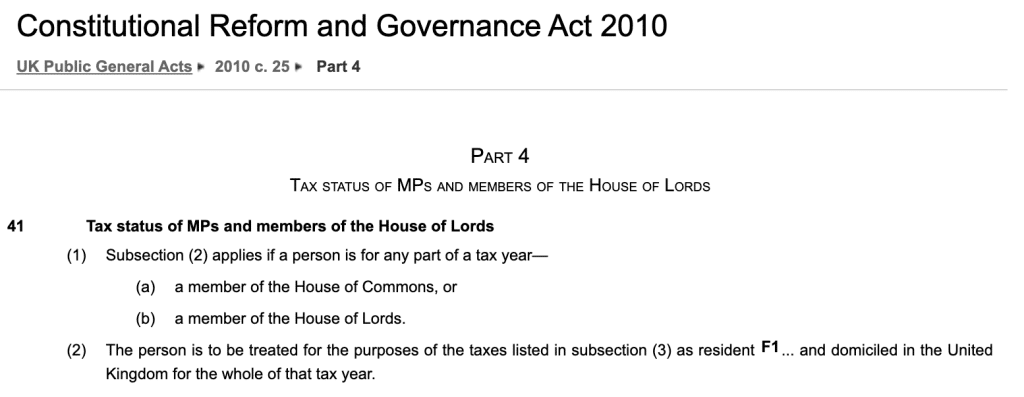

Which would have led them to this:

So the answer as to why Lord Sugar failed to become a tax exile is easy. The CRGA means that, as a member of the House of Lords, he would have been UK tax resident whether he lived in Basingstoke, Sydney or on the Moon.

It’s a fun story (not for Alan Sugar, and not for his advisers, who the Sunday Times says he’s now suing 1). But there’s a bigger question: why does the UK make it so easy to become a tax exile?

Looking at the Sunday Times “Rich List”, I’m struck by how few of those listed still live in the UK. Most of these people left the UK for a very specific reason. They built up a successful business, and were about to make a large amount of money from that business (perhaps by selling it; perhaps through a large dividend). They left the UK, sold the business (or received the dividend) and made a large tax-free gain/profit. They became a tax exile.

How tax exile works

There isn’t a loophole or trick – its just that, like almost all4 other countries, the UK only taxes people who live here – who are “UK tax resident”.5

A Frenchman in Paris won’t be subject to UK tax on dividends from UK companies. If he moves to the UK, he’ll become UK tax resident, and be subject to tax on that income6.

A Brit living in London is of course UK resident, and subject to UK tax on her UK dividends. But if she leaves the UK, she’ll no longer be taxed on those dividends.

This is sensible and uncontroversial. The UK has no business taxing people who don’t live here.

It becomes more controversial if that Brit has spent her life in the UK growing a business, and is (say) sitting on an offer from someone to buy the business for £50m. The UK has, by international standards, a pretty low rate of tax on capital gains – 20%. But if she leaves the UK and moves to a country that doesn’t tax capital gains then she’ll escape all tax on the £50m. That used to mean going to a tedious tax haven like Monaco, but there are an increasing list of non-tax havens that don’t tax recent immigrants on their foreign gains – e.g. Australia, Portugal7 and Israel.8

Could we stop tax exiles?

Absolutely. Many countries try to stop tax exiles, or limit the tax they avoid, with “exit taxes”.

Typically how this works is that, if you leave the country, the tax rules deem you to sell your assets now, and if there’s a gain then you pay tax immediately (not when you later come to sell). Sometimes you can defer the tax until a future point when you actually sell the assets or receive a dividend.9 And if your new home taxes your eventual sale, then your original country will normally credit that tax against your exit tax. Of course, it works out more complicated than this in practice because it’s tax, but the basic principle is both straightforward and commonly implemented in other countries. For example:

France has a 30% exit tax on unrealised capital gains, with a potentially permanent deferment if you’re moving elsewhere in the EU, or to a country with an appropriate tax treaty with France.

Germany has a 30% exit tax on unrealised capital gains. If you’re moving elsewhere in the EU you used to get a deferral; from the start of 2022 you instead have to pay in instalments over seven years.

Australia has an exit tax on capital gains tax – unrealised gains are taxed at your normal income tax rate for that year. There is a complicated option to defer.

The US has an exit tax for people leaving the US tax system by either renouncing their citizenship, or giving up a long-term green card. Unrealised gains in their assets, including their home, become subject to capital gains tax at the usual rate. No deferral.

Canada is of course much nicer than the US. Unrealised gains are taxed, but there’s a deferral option, and your home isn’t taxed at all.

Why didn’t the UK create an exit tax years ago? We didn’t have capital gains tax at all until 1965, and it was easy to avoid until the 90s. After that, we ran into a big problem with EU law, which greatly complicates exit taxes – in particular by requiring an unconditional interest-free deferral of exit tax until an actual disposal of the assets. That enables a massive loophole for taxpayers to leave a country, and then extract value through dividends, rather than a sale. Germany is attempting to ignore this, and I expect that will not end well.

So one new freedom the UK has post-Brexit is the ability to impose our own exit tax that has no leaks, and which the CJEU can’t stop. 10

(The UK has some exit taxes already. Companies migrating from the UK pay an exit tax. Stock options are subject to a mini-exit tax. Some trusts are subject to an exit tax. I’m sure there are a few more. But we currently have no general exit tax on individuals).

Should we stop tax exiles?

There are, inevitably, two opposing views:

One is that everyone is free to live where they wish, and if they move somewhere with lower tax, that’s up to them. No Government has a right to tax people for leaving. The knowledge that high-earning individuals can skip the jurisdiction, imposes a useful pressure on governments not to raise tax too high. It’s a useful form of tax competition.

The other view is that if you spend years in the UK building up your business, it’s only right that the UK should have the right to tax the gain you make on selling that business. More pragmatically, it seems counterproductive for the tax system to incentivise people to leave. This kind of “tax competition” is an undesirable infringement on countries’ right to raise taxes, particularly on the wealthy.

So what should we do?

I’m not sure. I’d want to see more evidence and analysis of the real-world impact of an exit tax. A poorly designed tax could put people off coming to the UK, or even accelerate departures (i.e. by causing entrepreneurs to flee to Monaco as soon as things start going well, rather than waiting until just before their big payday). And even just talking about an exit tax is dangerous, because it could prompt tax exiles to skedaddle immediately.11 Any exit tax would also need to be carefully designed to have no impact on people genuinely leaving the UK for other “normal” countries in which they’ll be fully taxed on their future gains – it should be targeted specifically at those who leave for tax havens (but targeting specific tax results, not specific countries).

In the interests of fairness, if we’re introducing new rules for capital gains when people leave the UK, we should also look again at the capital gain rules when you arrive in the UK. Right now if (for example), you build a business worth £100m from nothing, come to the UK and sell your business the next day, the UK will tax you on all £100m of gain. Even though little or none of that gain was made in the UK. That feels unfair; and there is anecdotal evidence that it deters some entrepreneurs from moving here. So we should have an entry adjustment – “rebasing” the asset to its market value at the date you arrive in the UK.

So there is a case to be made for changing the law in both directions, and establishing a principle that the UK taxes gains made when you were in the UK, and doesn’t tax gains made when you weren’t. But any change needs to be implemented cautiously and with great care.

Footnotes

Most professional negligence claims settle well before reaching a court, but on on the face of it this looks like a slam-dunk. However, we don’t know all the circumstances, what questions were asked, and whether advice was preliminary or definitive. The advisers may also be able to point to limitations of liability in their standard terms – accountants often limit liability to £1m (or thereabouts), even on very large transactions, and whether these limitations apply in a particular case is often a difficult question. Sugar would also have to show that, if he had been properly advised, he would have resigned his seat in the Lords, and then remained non-UK resident for five years – and demonstrating these kinds of counter-factual questions isn’t always easy ↩︎

The original version of this article included Toto Wolff, the motorsport executive. I don’t think he really belongs in it – he left the UK for tax security reasons, but given he wasn’t born here, and didn’t make his money here, he shouldn’t be on the list. ↩︎

Dixon’s Wikipedia article says he voluntarily pays tax in the UK. I doubt it. ↩︎

“almost all” meaning “everyone except the US”. There’s a reason the US is an outlier here. ↩︎

There used to be a huge loophole – you could leave the UK on 4 April 2020, become non-resident for the 2020/21 tax year and receive your massive gain tax-free, then fly back into Heathrow on 5 April 2022. That no longer works. There’s a special rule to tax “temporary non-residents”. If you leave the UK but become UK resident again within five years, any capital gains you made during the five years are immediately taxable. ↩︎

But not his unremitted French income/gains, because he will be a “non-dom“. ↩︎

Correction: Portugal would tax gains, but not dividends. So obvious ploy is to keep hold of the shares, but extract all the value via a dividend. Which amounts to the same thing, subject to a bit of messing around with distributable reserves ↩︎

And the UK is in a similar category in the reverse case – the UK non-dom rules means that a foreigner coming to the UK is not taxed on their foreign gains, unless they remit them to the UK. That is less generous than Australia, Portugal and Israel, where the gains are exempt even if brought into the country. ↩︎

Often you have to provide some form of guarantee so you can’t just promise you’ll pay in future, and then scarper ↩︎

Some tax nerds will worry that the UK’s many double tax treaties make this hard, because we often give up our right to tax non-residents on their capital gain. To which I say: easy, deem the tax to apply on the last day they were UK resident, so the treaty isn’t relevant. And then expressly override the treaty anyway, just to be safe. After all, treaties are supposed to be used to prevent double taxation, not to avoid taxation altogether. ↩︎

It follows that any exit tax would have to be announced suddenly and with great fanfare, and made retrospective to the date of the announcement. This would be controversial, but introducing a non-retrospective exit tax would be *massively damaging* – there would be a mass exodus of the super-wealthy ↩︎

Comment policy

This website has benefited from some amazingly insightful comments, some of which have materially advanced our work. Comments are open, but we are really looking for comments which advance the debate – e.g. by specific criticisms, additions, or comments on the article (particularly technical tax comments, or comments from people with practical experience in the area). I love reading emails thanking us for our work, but I will delete those when they’re comments – just so people can clearly see the more technical comments. I will also delete comments which are political in nature.

6pm update: St James’s Place sent me a statement saying “We are currently investigating this matter, including the nature of the planning outlined and how the marketing material was published on the website. While we work with clients to consider the tax efficiencies of their financial plans, SJP does not endorse the use of tax avoidance schemes.”

No response from Apollo, although their website has been “down for maintenance”since this afternoon.

Back in May, we reported on a widely promoted tax avoidance scheme for funding private school fees. The basic idea was to create a trust in favour of your children and put valuable assets in it (e.g. shares in a family company). The return on those shares would then be taxed at the children’s lower tax rate and benefit from the children’s tax allowances – potentially saving tens of thousands of pounds.

These schemes don’t work. There’s a specific tax rule that says that, if a parent puts assets, directly or indirectly, in the name of their children, then the assets are taxed as if still owned by the parents. HMRC subsequently confirmed this in a “Spotlight” update.

The firms we wrote about were all fairly minor players, which is what we’d expect.

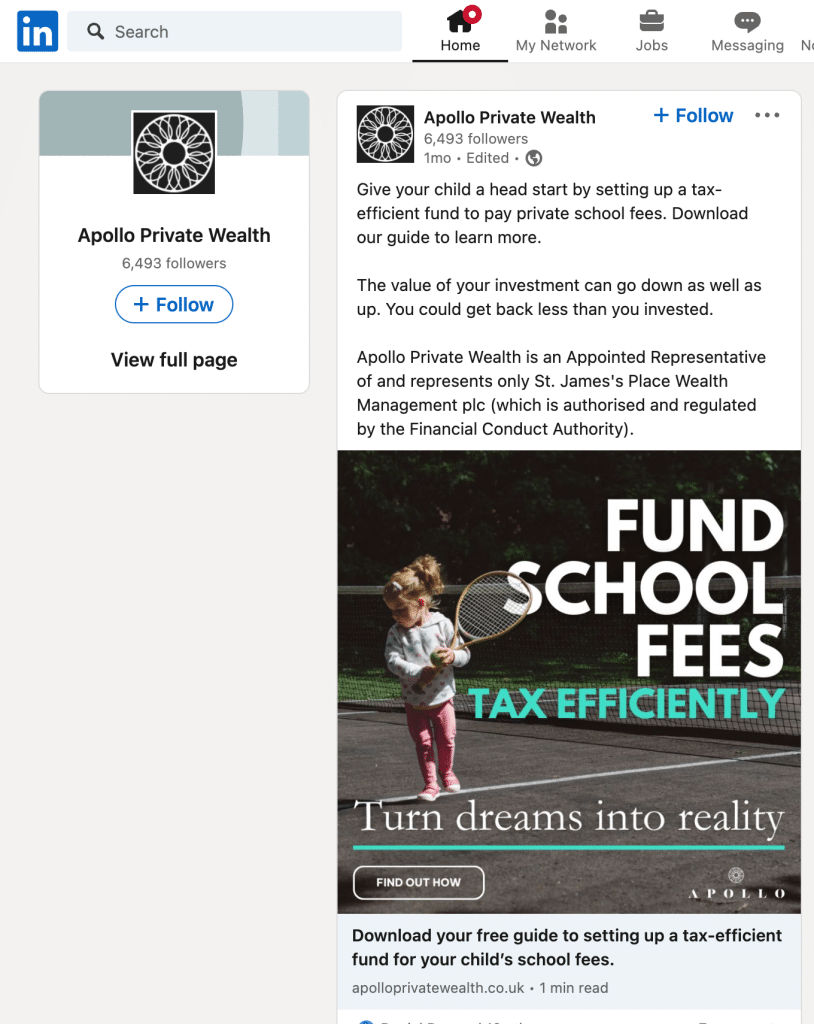

The schemes were, as you’d expect, promoted by small firms – surely no serious adviser would touch such nonsense. It turns out that the country’s largest private client firm, Apollo Private Wealth, absolutely is promoting this nonsense.

Apollo Private Wealth may be the country’s largest private wealth firm,1 and is a “senior partner practice” of St James’s Place, the FTSE listed wealth management business. These are significant businesses, with large numbers of high net worth clients.

The scheme

This LinkedIn post looks like it’s promoting something boring and sensible like an ISA.

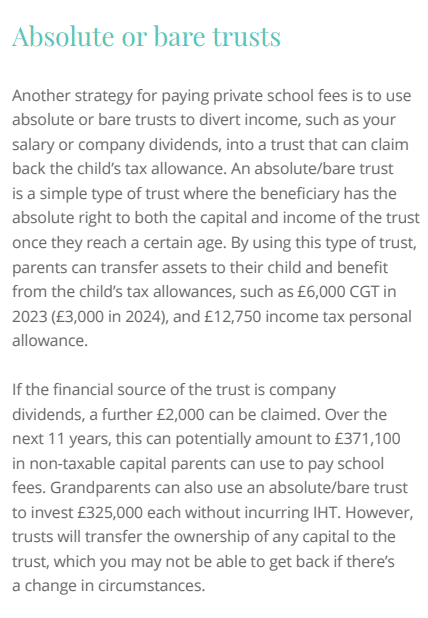

The link goes through to a pretty brochure (archived here) which does indeed mention ISAs, but also includes this proposal:

The meaning is clear: that parents can use a trust to “divert” their own assets/income to their children, and benefit from the children’s lower rate and higher allowances.

Tax law can be complicated, with unclear and highly contestable boundaries between good tax planning, failed tax planning, and tax avoidance.

In this case, it’s easy.

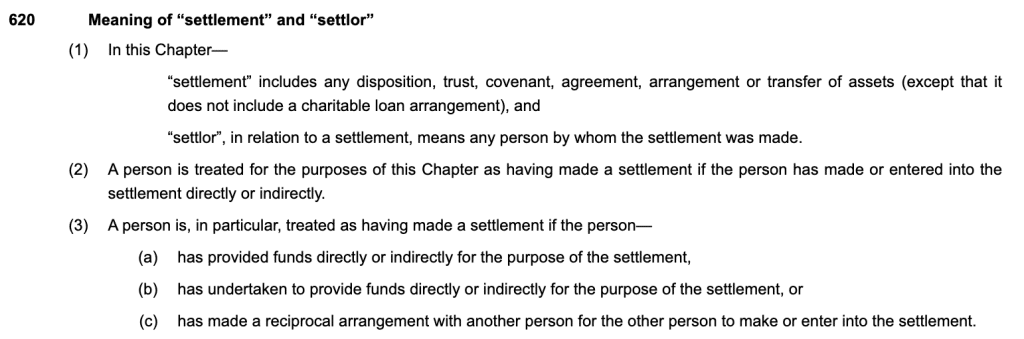

Here’s section 629 of the Income Tax (Trading and Other Income) Act 2005:

The terms “settlement” and “settlor” are defined exceedingly broadly:

Applying these rules to the Apollo proposal: the trust is a “settlement”, the parents are “settlors”, and income is paid under the settlement for the benefit of the settlor’s children. Section 629 then applies and the parent, not the child, is taxed on the income. Whatever layers and complexity are added won’t make a difference, given the breadth of the legislation.

Any client entering into the arrangement Apollo suggests would, once HMRC become aware, have to repay the tax, plus interest, plus (very likely) penalties for carelessness. Any tax adviser should know this – there’s no grey area or uncertainty here.

The questions for Apollo

It’s pretty worrying that a large advisory firm is promoting something that just can’t work, and after HMRC issued a Spotlight on the same subject. More worrying if they’ve actually advised anyone to do this. The obvious question is: if they get something this simple wrong, and are happy to put something this rubbish in a glossy brochure, what on earth are they recommending to clients behind closed doors?

I’ve asked Apollo and St James’s Place for comment.

Many thanks to Sam Brodsky for bringing this to our attention.

Footnotes

Apollo Private Wealth has no connection with Apollo Global Management, the asset management giant ↩︎

The “grandparent” variation they mention would work, if the assets start out truly owned by the grandparents and not the parents. But then you don’t need a trust – the grandparents could just pay the school fees directly. ↩︎

During the pandemic, Baroness Mone referred a company called PPE Medpro to the Department of Health and Social Care to supply PPE equipment. PPE Medpro was awarded £200m of contracts, in circumstances which are now the subject of litigation and a fraud investigation by the National Crime Agency.

BaronessMone at the time did not disclose any connection to PPE Medpro, and in 2020 her lawyers denied “any suggestion of an association”. However, new evidence suggests that PPE Medpro’s true ownership was hidden by a company controlled by her husband, Douglas Barrowman. If that was intentional, then criminal offences were committed.

Our full analysis is below, and the Sunday Times is carrying a report on our findings here.

The Department of Health and Social Care has commenced legal action to recover the £122m paid under the second of the two contracts. PPE Medpro is also the subject of an ongoing fraud investigation by the National Crime Agency, and Mone’s actions are the subject of an investigation by the House of Lords Commissioners for Standards’ Office1.

Mone has said she is in no way associated with PPE Medpro. Lots of press coverage has been highlysceptical of this.

Who really owns PPE Medpro?

At the time, PPE Medpro’s shares were owned by an Isle of Man resident, Anthony Page.

Sometimes the true owner of a company – the “person with significant control” (PSC) – can be different from the shareholder. For example, if one person owns shares in a company, but there is a formal or informal understanding that they always act on the instructions of another person, then both people should be listed as PSCs.

But the Companies House register showed Mr Page as the sole PSC:

At the same time, Anthony Page was the managing director of the Knox Group.

Another director of PPE Medpro was Voirrey Coole – who was the director of another Barrowman company.

This suggests three possibilities:

PPE Medpro was a private venture of Mr Page, and nothing to do with Mr Barrowman.

Mr Barrowman’s Knox Group was engaged to provide corporate services for an unknown third party, and Mr Page was the shareholder in his capacity as employee of the Knox Group.

Mr Barrowman was the true owner of PPE Medpro. The Guardian says it has a document listing PPE Medpro and LFI Diagnostics as “entities” of the Barrowman family office (but Tax Policy Associates has not seen that document, and so we cannot independently assess this claim).

How plausible are the three scenarios?

Scenario 1: Mr Page owned PPE Medpro in his own right

New evidence means that this scenario can now be ruled out.

The Sunday Times reported last week that Anthony Page was dismissed from the Knox Group for “gross misconduct”. If Mr Page owned PPE Medpro in his own right then his ownership of PPE Medpro would have been unconnected with his employment by the Knox Group. Page would have remained the PSC of PPE Medpro when the Knox Group fired him.

The obvious inference is that Mr Page held the PPE Medpro shares as part of his employment by the Knox Group and, when that employment ceased, he was required to transfer his ownership of those shares. He was not the true owner, and should not have been registered as the sole PSC.

Scenario 2: Mr Page and the Knox Group are acting for some unknown third party

There are, however, two problems with this explanation.

First, Mr Page and Ms Coole are not acting at all like typical corporate service providers.