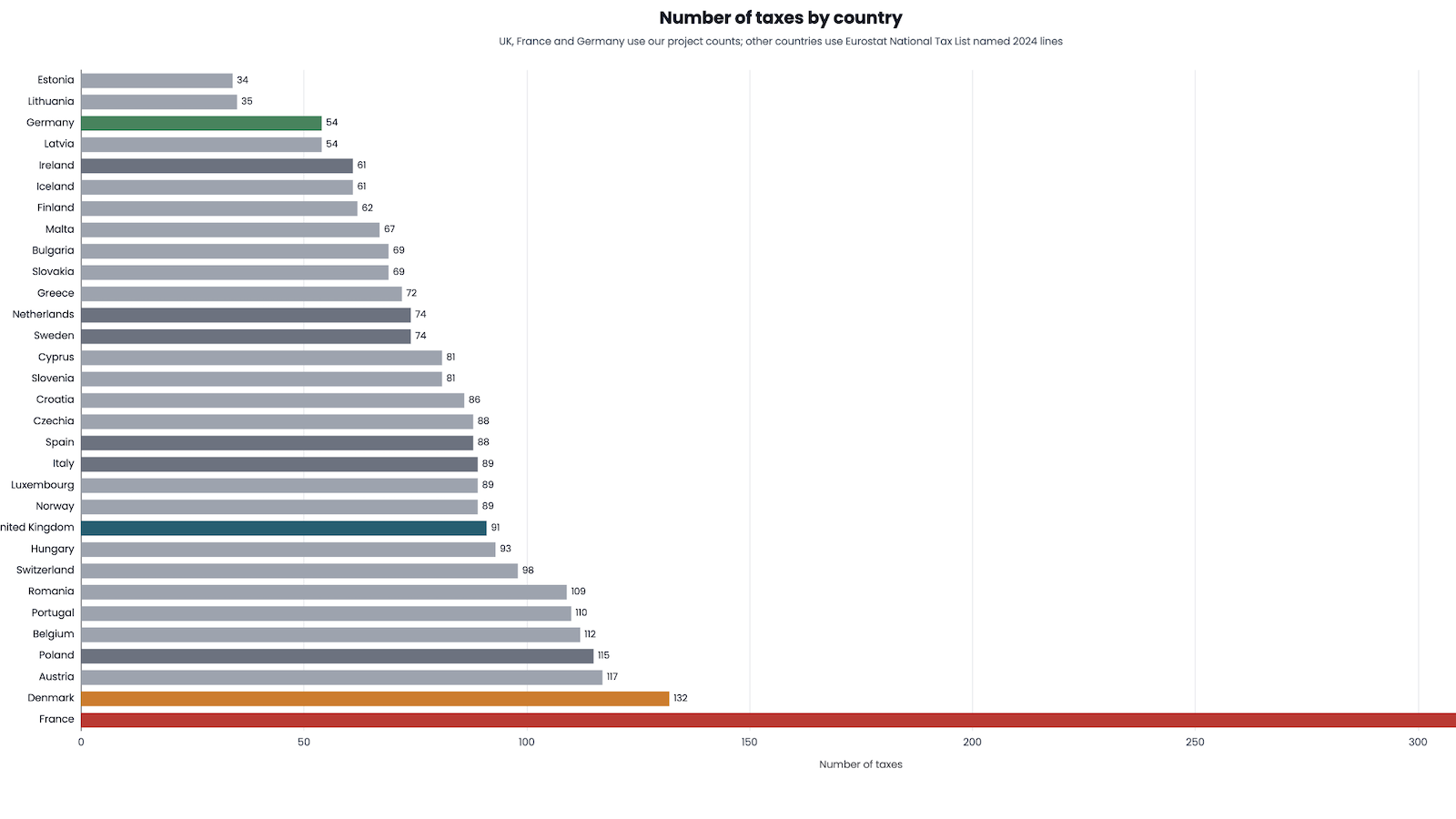

The UK has 90 different taxes – more than at any time since 1834. France, on the other hand, has 348. But Germany, which has overall levels of tax closer to France than the UK, has only 60.

Why is that? And are there lessons for the UK?

This is the third in a series. We first looked at all the UK’s 90 taxes, then at the historic trends that led to that point.

The charts are interactive: click on a segment or category to drill down. The control underneath switches between euros, percentage of GDP, and percentage of total tax.

France

Here’s the French tax system as it was in 2024:

France raises a lot of tax: €1,321bn, equal to 45.3% of GDP, compared to 37% in the UK.1

It does so with a huge number of taxes.

According to the Cour des comptes (Court of Audit) there are 243 “low-yield taxes”. 148 of those are included in the chart2, although you generally have to zoom into a category or subcategory to make them out. There’s another 95 “low-yield taxes” where we couldn’t find any sources identifying the yield. That doesn’t (necessarily) mean they raise nothing but, absent any data, we’ve had to exclude them from the chart.

More visible on the chart are the long tail of small, often highly specific taxes: training levies, chamber taxes, insurance levies, sector charges, nuclear taxes, water levies, gambling levies, local land-agency taxes, and many more.3 Many are relics of history or political compromises; together they create a tax bureaucracy much more burdensome than we face in the UK.4

The UK has seen a dramatic increase in the number of taxes since 1991; but it would still take us 200 years to equal the number of French taxes.5

Germany

Germany is different. It is not a low-tax country: in 2024 it raised €1,817bn, equal to 42.2% of GDP. But the structure is much simpler than France’s – only 60 taxes:

The big German taxes are familiar: social contributions, income tax, VAT, corporation tax, trade tax, insurance tax, energy tax, tobacco duty, inheritance tax and property taxes. The chart has a few German oddities, such as coffee duty, dog tax, the broadcasting contribution, and the solidarity surcharge. But there is nothing like the French long tail.

So Germany is interesting. It raises an enormous amount of tax without needing hundreds of separately reported taxes. Complexity is not an unavoidable consequence of a high tax burden.

Part of the explanation is that Germany had not one but two separate sets of reforms.

The German Federal Ministry of Finance traces⚠️ many central features of the modern system back to the 1919-20 Reich financial reform6: uniform taxation at federal level, income-tax reform, and a restructuring of fiscal relations between the federal and Länder governments.

The post-war Basic Law then constitutionalised a shared-tax federation. Article 105 centralises much tax legislation, and Article 106 allocates revenues: income tax, corporation tax and VAT are joint taxes shared between levels of government, while municipalities receive trade tax, property tax and shares of income tax and VAT.7

Tax systems across Europe

France and Germany are the extremes. If we run an approximate international comparison8, we see that the UK sits between them:

There is no obvious relationship910 between the number of taxes and the overall tax take:11

(France is initially hidden from the chart, because its anomalously high number of taxes “compresses” the other countries – the button at the bottom re-includes it.)

So it’s reasonably clear that a high-tax state does not require hundreds of taxes. Germany raises more tax than the UK, as a share of GDP, with far fewer separately reported taxes – and so do many others.

Does it matter?

We think it does. We usually focus on complexity within individual taxes12, but “number of taxes” is also a sign of complexity.13 When you’re a company looking to do business, each tax means a new adviser, a new set of advice, and a new list of things you can and can’t do.14

The Tax Foundation ranks France dead last in its table of international tax competitiveness. The UK is near the bottom – below many countries with higher overall level of tax. This accords with our experience that complexity can be more of a problem for business than the actual level of tax.

The UK is moving in the wrong direction. Our historical tax-count work suggests the UK now has more taxes than at any time since 1834. In the twentieth century the state became much larger, but did so through a relatively small number of broad taxes.15

The recent pattern is different: more environmental taxes, devolved taxes, behavioural taxes and small segmented charges16, often without a corresponding increase in the overall tax burden.

We don’t need to worry about turning into France – at least not for 200 years. But we should worry why we’re not more like Germany. And we could start by abolishing unnecessary and duplicative taxes.17

Methodology

The tax counts in this article should not be regarded as definitive, and we are less confident than we were for the UK count. Our approach was as follows:

France

The French chart starts with the European Commission/Eurostat National Tax Lists workbook for France, 2024, which gives national-accounts tax and compulsory-social-contribution rows in million euros.18 The control total is €1,321.460bn: €1,326.081bn gross, less €4.621bn of D995 taxes and social contributions assessed but unlikely to be collected. Dividing that by INSEE 2024 current-price GDP of €2,920bn gives 45.3% of GDP.

We then added the Cour des comptes low-yield-tax inventory, because Eurostat often groups small French taxes into aggregates.19 To avoid double-counting, every separately shown low-yield tax is netted out of the relevant positive Eurostat aggregate. That is why the detailed chart still reconciles exactly to the Eurostat control total.

Negative rows are not shown as chart leaves; they only reduce the relevant positive amount.20 Rows with no usable individual amount remain outside the sunburst: there are 95 such current French low-yield taxes. They are included in the country-count comparison, but not in the revenue chart. So the French count is 348 taxes: 253 positive-yield chart leaves plus 95 no-yield current rows.

The classification is ours. It follows the UK chart where possible: employment, goods/services, business, land, wealth, environmental, and other. The purpose is to show what is being taxed, not the collecting body or legal form. Analogous categories use the same colours as in the UK chart.

Main French sources: Eurostat National Tax Lists; Cour des comptes, Les taxes à faible rendement; PLF 2025, Évaluations des voies et moyens – tome 1; and INSEE annual-average CPI releases for 2020, 2021, 2022, 2023 and 2024.

Germany

The German chart starts with the same Eurostat National Tax Lists workbook, using the Germany sheet for 2024.21 The Eurostat rows used for the chart sum to €1,816.514bn. Dividing that by Destatis 2024 current-price GDP of €4,305.3bn gives 42.2% of GDP.

We aggregate repeated Eurostat sector splits of the same economic tax, and use the German Federal Ministry of Finance 2024 cash receipts table only where it gives useful statutory detail inside a broader Eurostat control row.22 The solidarity surcharge is shown separately at €12.634bn and netted out of the related income-tax, capital-income-tax and corporation-tax rows.

The classification and colours are the same as for the UK and France. Negative BMF cash rows for wealth tax and investment grants are excluded from the chart rather than displayed as negative wedges.23 The resulting German chart has 60 positive leaves and reconciles exactly to the Eurostat control total.24

Main German sources: Eurostat National Tax Lists; Bundesministerium der Finanzen, 2024 cash tax receipts by tax type; and Destatis current-price GDP.

The code that generated the charts is available on our GitHub, together with the underlying data.

Many thanks to T and O; particular thanks to V for generously sharing some of her work on French taxes. Original idea of looking at the French taxes came from Patrick Fitzgerald.

Chart created using Apache ECharts, by the Apache Software Foundation and contributors (Apache-2.0).

Why does Britain have more taxes than at any time since 1834?

90 UK taxes. On one chart.

What would a land value tax actually do?

What if Andy Burnham lowered the mansion tax threshold to £1.5m?

Has Britain run out of “other people” to tax?

Tax will go up but public services will get worse. This is why.

Footnotes

The UK figure of around 37% of GDP is the standard OECD comparator: see OECD, Tax revenue (% of GDP), and HMRC/OBR’s National Accounts taxes overview. The headline UK ratio moves around between OECD, ONS and OBR depending on whether imputed social contributions and EU own resources are included. ↩︎

126 with a 2024 Cour amount, 21 where we uprated a 2019 Cour amount to 2024, and one where an exact 2024 amount appears in the PLF 2025 taxes-affectées data. ↩︎

The Conseil des prélèvements obligatoires has separately criticised the proliferation of earmarked taxes (fiscalité affectée): see La fiscalité affectée : constats, enjeux et réformes, which describes it as opaque, fragmenting parliamentary control of the budget, and a key driver of tax-count inflation. ↩︎

The Inspection générale des finances reached the same conclusion a decade earlier in its 2014 report on Les taxes à faible rendement, identifying 192 low-yield taxes and recommending mass abolition; very few were in fact abolished, which is why the Cour des comptes revisited the topic in 2025. ↩︎

The UK had 45 taxes in 1991 and has 90 now. So a growth rate of 1.3 taxes per year, and we reach 348 taxes in around 200 years. ↩︎

The 1919-20 reforms are usually called the Erzbergersche Reform after finance minister Matthias Erzberger. For a modern overview see the BMF’s own centenary monthly-report essay, the Wirtschaftsdienst piece Geburtsstunde des modernen Steuerstaats, and the DIW Wochenbericht 100 Jahre deutsches Steuersystem. They merged the separate Länder tax administrations into a single Reichsfinanzverwaltung and introduced a national income tax. ↩︎

Basic Law for the Federal Republic of Germany, Articles 105 and 106. For how the shared-tax mechanism works in practice, see the Bundesbank’s regular commentary in its Monthly Reports, and the BMF’s overview of the föderale Finanzbeziehungen. The practical effect is that Länder and municipalities mostly receive shares of the big federal taxes rather than running their own parallel tax codes. It’s an interesting comparison with the UK, where devolution has been accompanied by the creation of new parallel taxes. ↩︎

For the UK, France and Germany, this chart uses our own tax-map counts: 90 for the UK, 348 for France, and 60 for Germany. For France, that includes the 95 current low-yield taxes outside the revenue chart because no usable individual amount was located. For the other countries, we used the European Commission/Eurostat National Tax Lists, counting positive 2024 named tax rows and deduplicating repeated rows with the same name and amount. This may undercount minor taxes in countries we have not mapped in detail. So there is a real risk that France, UK and Germany all actually have relatively fewer taxes than this simple chart suggests – that’s why we say this chart is “approximate”. ↩︎

Please note our warning above regarding the approximate nature of the international figures. Leaving that aside for a moment, we ran simple OLS regressions on the scatter dataset. If we include France, there is a weak positive relationship between number of taxes and tax as a % of GDP, but it is not significant at the conventional 5% level (p-value: 0.074). If we exclude France (as an obvious outlier), the estimated relationship remains positive but becomes weaker and clearly statistically insignificant (p = 0.144). ↩︎

There is, however, a highly statistically significant correlation between the number of taxes a country has and the number of types of cheese (p=0.0000000375). The reason why is fairly clear from this chart:

If we exclude Italy and France, the correlation disappears (p=0.183). The source for this was a simple query of wikidata, and therefore accuracy is not necessarily guaranteed. ↩︎

The x-axis uses OECD Global Revenue Statistics, measure tax revenue as a percentage of GDP, sector S13, total tax revenue, latest available year. Note it’s different from other figures given for tax as a % of GDP, and inconsistent with the data we used for our historic UK chart; that’s inevitable if we want to compare like-with-like. We used OECD data for 2024 for all countries except Romania, where the latest OECD value is 2023. OECD Global Revenue Statistics has no Cyprus value; to keep every country from the previous chart on this chart, Cyprus uses the 2024 Eurostat gov_10a_taxag value for taxes and compulsory social contributions after D995 deductions, excluding imputed social contributions. OECD’s tax/GDP definition is not identical to the Eurostat national-accounts control totals used for the France and Germany sunbursts. ↩︎

See How to reform corporation tax, which argues that base design matters as much as rates, and that reform can be revenue-neutral while still improving growth incentives. ↩︎

Tax complexity has many dimensions, and number-of-taxes is only one. For a broader treatment see the IFS Mirrlees Review (especially the tax simplification chapter in Dimensions of Tax Design), and the Office of Tax Simplification’s Tax Complexity Index for the UK. ↩︎

The compliance cost is real; it’s often said to disproportionately fall on small businesses, but in our experience also impacts large business decision-making (and has been responsible for some significant decisions to locate operations, startups, and headquarters elsewhere). See the National Audit Office’s The administrative cost of the tax system (2025), the Public Accounts Committee’s follow-up report on the cost of the tax system, HMRC’s Administrative Burdens Advisory Board Tell ABAB 2024-25 report, and the FSB’s Taking a Toll. ↩︎

This is the standard “broad base, low rate” prescription that runs through both the Mirrlees Review (Tax by Design) and the OECD’s Tax Policy Reform and Economic Growth. The historical UK pattern – income tax, NICs, VAT and corporation tax as the bulk of the take – broadly followed it. The recent drift has been the other way. ↩︎

Recent additions and announced additions include the Soft Drinks Industry Levy (2018), the Plastic Packaging Tax (2022), Digital Services Tax (2020), Residential Property Developer Tax (2022), Energy Profits Levy and Electricity Generator Levy (2022), the Economic Crime (Anti-Money Laundering) Levy (2022) and Scottish/Welsh devolved taxes including LBTT, LTT, Scottish Landfill Tax, Welsh Landfill Disposals Tax, the Scottish Aggregates Tax (2026) and the proposed Welsh visitor levy. ↩︎

The OTS, before it was abolished, made the same point repeatedly: see e.g. OTS simplification recommendations: summary at March 2015, and the Simplifying everyday tax for smaller businesses review. Many of its recommendations to remove or merge small taxes were not implemented. ↩︎

We used the France sheet in the National Tax Lists workbook updated on 22 April 2026, linked from Eurostat’s tax revenue statistics page. The workbook covers general government plus EU institutions, so local taxes are in scope. ↩︎

We included current Cour rows only: taxes marked as in force between 2019 and 2024, or created between 2019 and 2024. The Cour annex supplies 2024 amounts for 126 rows, worth €5.978bn. For 21 more rows we uprated positive 2019 amounts to 2024 using INSEE annual-average CPI inflation for 2020-24, producing €887m of estimated detail. For one further row, the tobacco retailers’ licence duty, we used the PLF 2025 taxes-affectées table’s exact 2024 execution amount of €360m. We did not allocate multi-tax PLF aggregates across individual Cour rows. ↩︎

A sunburst area chart cannot sensibly show negative wedges. This applies both to Eurostat D995 rows and to low-yield-tax overlap adjustments. ↩︎

The workbook covers general government plus EU institutions, so local taxes such as trade tax, property tax, dog tax and other municipal taxes are in scope, as are compulsory social contributions. ↩︎

For example, the chart combines Eurostat’s domestic VAT, import VAT and VAT under-compensation rows into one VAT leaf, and combines business and household motor vehicle tax rows. BMF cash data are used only for selected splits, including capital-income withholding taxes, alcohol duties, very small import/federal taxes, and the solidarity surcharge. The BMF table is not used as the overall chart total because it excludes ordinary municipal taxes and social contributions. ↩︎

The excluded BMF rows are Vermögensteuer at -€11,178, and two Investitionszulage rows at -€428,560 and -€345,390. The Eurostat Germany rows used for the chart contained no negative rows. ↩︎

Eurostat’s National Tax Lists group small German Bagatellsteuern into aggregate rows rather than naming each separately, so a naive Eurostat-only count understates Germany compared to the UK and France methodologies (which enumerate every statutory tax). We therefore split the Eurostat Grundsteuer A/B row into the two distinct statutory property taxes, and reallocate parts of the Eurostat catch-all übrige Gemeindesteuern row to five named local taxes that have separate legal bases: Übernachtungsteuer / Bettensteuer (city overnight-stay tax, estimated €200m), Zweitwohnungsteuer (second-home tax, estimated €150m), Verpackungsteuer (Tübingen-model packaging tax, estimated €1m and upheld by the Bundesverfassungsgericht in 2024), Pferdesteuer (horse tax, estimated under €1m) and Schankerlaubnissteuer (licence-to-serve-alcohol tax, estimated under €1m). The amounts for the five reallocated taxes are TPA estimates from public city- and Land-level reports because Eurostat does not publish them separately; in each case the parent übrige Gemeindesteuern row is reduced by the same amount so the chart still reconciles. See the BMF’s Steuern von A bis Z (2025) and the Haushaltssteuerung lexicon of Gemeindesteuern. Each of these is counted only once even though they are levied by different rates across thousands of municipalities, because German statutory law treats each as a single tax type under the relevant Kommunalabgabengesetz. ↩︎

Leave a Reply