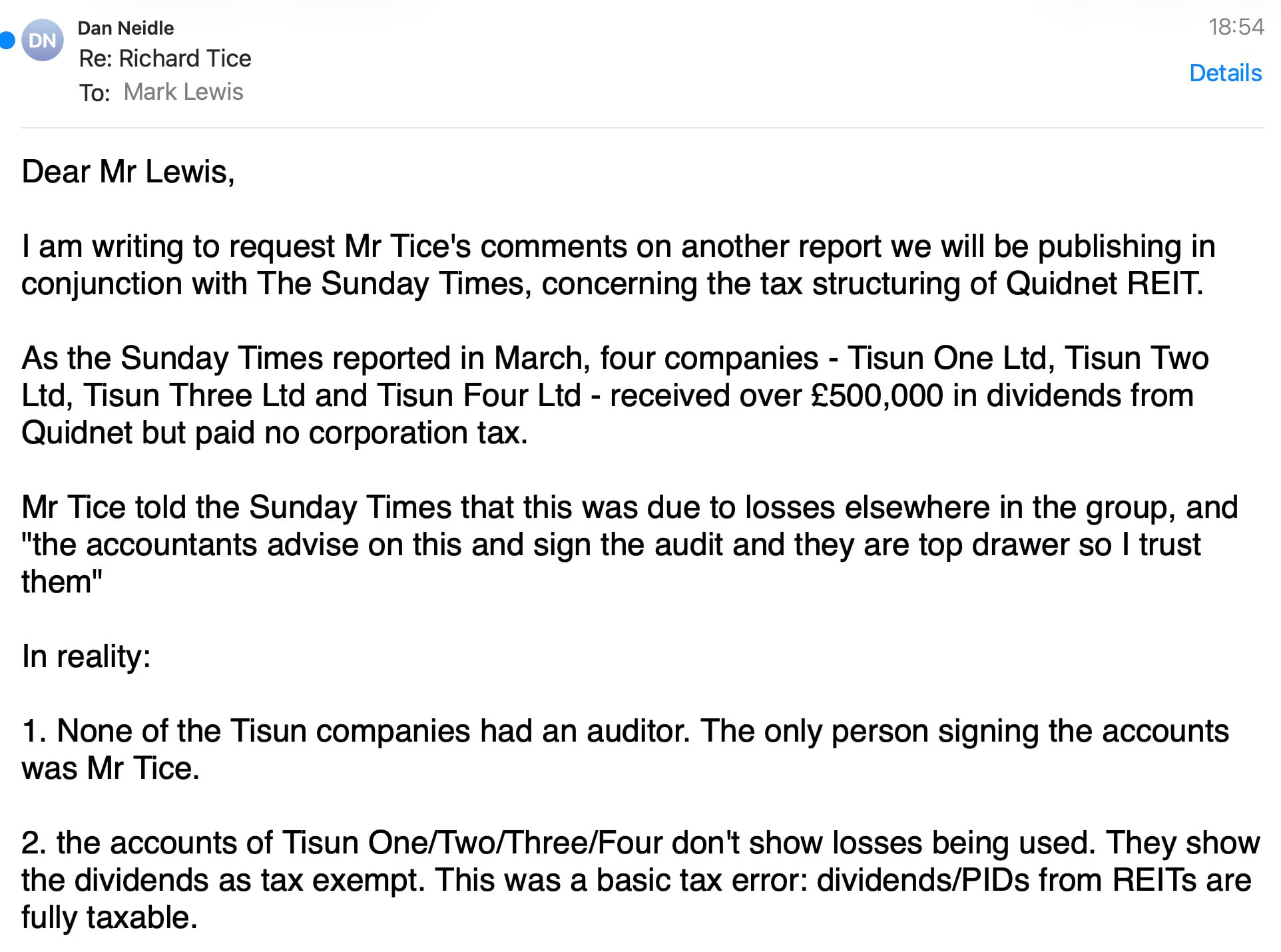

Richard Tice, the deputy leader of Reform UK, used his Quidnet property company’s REIT status to save tax. That meant Quidnet itself paid no corporation tax on its property business – but the quid pro quo was that its corporate shareholders had to pay tax on the dividends they received. They did not. Instead, Mr Tice signed accounts wrongly claiming that the dividends – £514,000 in total – were tax exempt. The result: they failed to pay £98,000 of corporation tax.

This is a different issue from our previous report, which found that Quidnet REIT failed to withhold about £120,000 of tax on distributions to Mr Tice and his offshore trust. But it arises from the same underlying mistake: claiming the tax benefits of a REIT but ignoring the tax liabilities.

- From Quidnet REIT to Tice companies (Label: £514k dividend)

- From Quidnet REIT to Tice companies (Label: £514k dividend)

Key points:

- Quidnet REIT paid about £514,000 of property income distributions to four companies: Tisun One, Tisun Two, Tisun Three and Tisun Four.

- Quidnet REIT paid no corporation tax on this income, because it was a REIT. The four Tisun companies were supposed to pay tax instead — but they didn’t.

- The payments were wrongly treated in the accounts as tax-exempt ordinary dividends. In fact they were taxable REIT property income distributions.

- The result was about £98,000 of unpaid corporation tax.

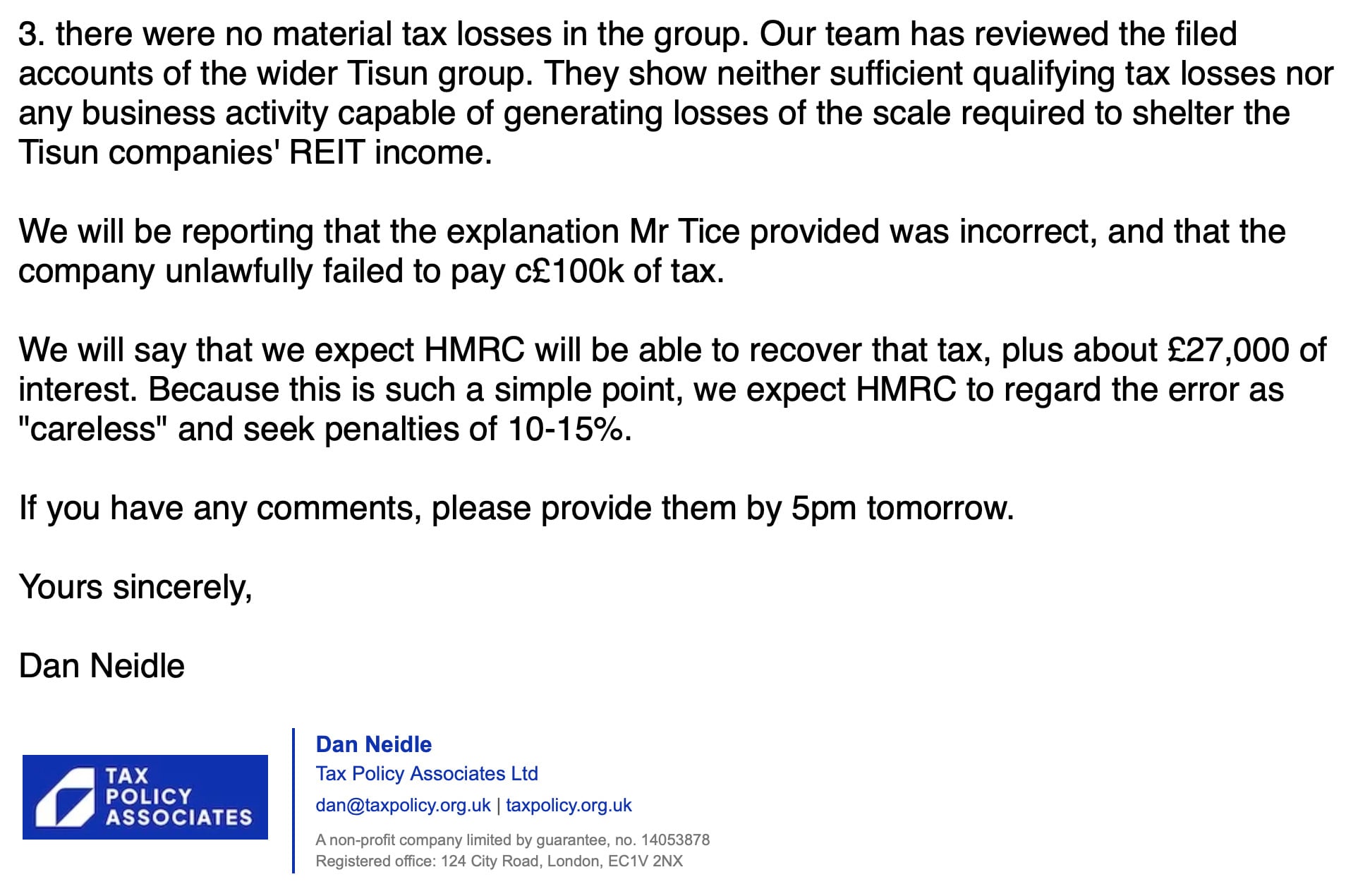

- Mr Tice has previously said the lack of tax was due to losses elsewhere in the group. The accounts contradict that, and our analysis finds there were insufficient losses in the group to eliminate the tax.

- HMRC should be able to assess the tax, plus roughly £27,000 of interest and penalties likely in the region of 10–15%.

These are basic errors. That raises a further question: what else went wrong? In particular, did Mr Tice’s offshore trust also fail to pay tax on the distributions it received from the REIT?

We worked on this story in conjunction with Gabriel Pogrund of The Sunday Times – his story is here.

Mr Tice did not respond to requests for comment from us or The Sunday Times.

In this report:

- The REIT structure

- Richard Tice's original explanation

- The accounts don't show loss utilisation

- Is it theoretically possible tax losses were used?

- Could the accounts just be wrong and tax really was paid?

- The consequences

- Richard Tice's response

- Methodology – determining the taxable profit

- The full reconciliation

- Methodology – group relief

- Methodology – interest calculation

- Disclosure

The REIT structure

From 10 September 2018 to 9 August 2021, Quidnet was a REIT: a form of tax-exempt investment fund that invests in real estate. The consequence is that the company becomes exempt from corporation tax on its property rental business, but its investors are (broadly speaking) taxed as if they held the real estate directly.1

Here’s Quidnet REIT and its shareholders:

Quidnet REIT direct shareholders as at 1 July 2021

- From Richard Tice (direct) to Quidnet REIT (Label: 13.00%)

- From RJS Tice Family Settlement to Quidnet REIT (Label: 16.88%)

- From RJS Tice Family SIPP to Quidnet REIT (Label: 34.98%)

- From Tisun One to Quidnet REIT (Label: 7.80%)

- From Tisun Two to Quidnet REIT (Label: 7.78%)

- From Tisun Three to Quidnet REIT (Label: 7.78%)

- From Tisun Four to Quidnet REIT (Label: 3.38%)

- From Huntress (CI) Nominees to Quidnet REIT (Label: 4.42%)

- From NJG Tribe SIPP to Quidnet REIT (Label: 2.99%)

- From Employees to Quidnet REIT (Label: 0.98%)

Quidnet REIT correctly paid no tax on its property income. But that shifted the burden elsewhere.

It had to withhold tax on dividends it paid out of that income to Richard Tice and his offshore trust – “property income distributions”. As we’ve previously reported, it didn’t do that. Quidnet mistakenly treated the dividends as ordinary dividends and failed to withhold about £120,000.

This report is about another, potentially more serious, error. Quidnet’s UK corporate shareholders had to pay tax on their dividends. They did not – they treated them as tax-exempt.2

There were four corporate shareholders:3 Tisun One Ltd, Tisun Two Ltd, Tisun Three Ltd and Tisun Four Ltd. The sole director of all four companies was Richard Tice.

Quidnet REIT made about £514,000 of payments to the four Tisun companies.4 None of them ever paid tax.

The consequences are straightforward: HMRC can recover the tax, with interest and penalties. We return to this below.

Richard Tice’s original explanation

The Sunday Times asked Mr Tice why none of the four Tisun companies ever paid any corporation tax. Mr Tice told The Sunday Times that this was because of “wider losses suffered by the group”:

These statements were incorrect:

- The accounts do not show losses being used.

- There were in fact no tax losses in the group.

- The front page of the accounts shows that the Tisun companies had no auditor – the only person who signed the accounts was Mr Tice:

The accounts don’t show loss utilisation

What the Tisun companies’ accounts actually show is an incorrect claim for a dividend exemption.

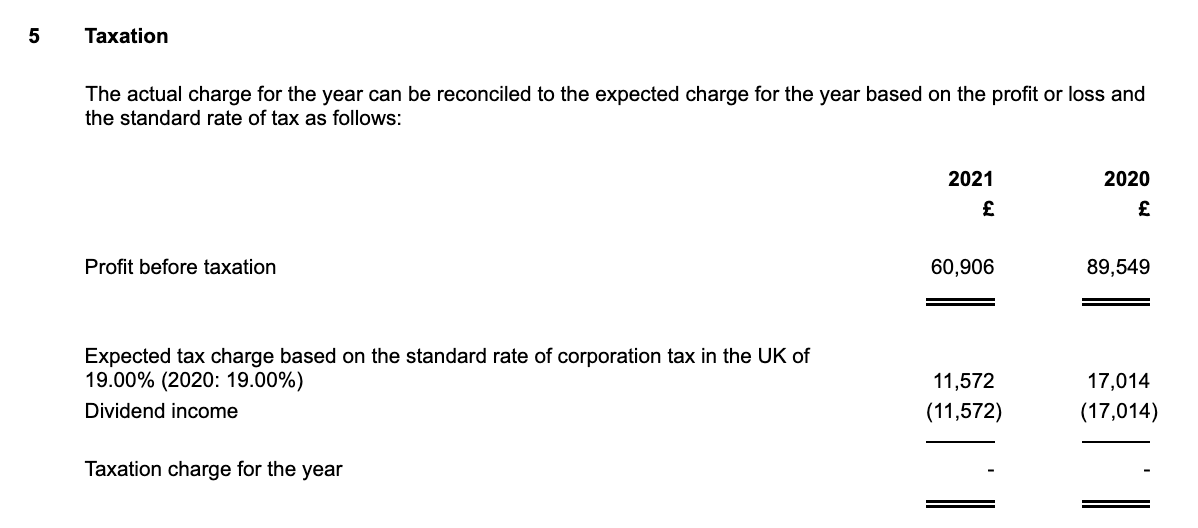

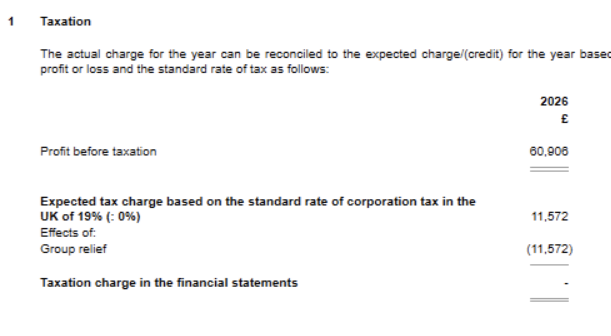

Here’s Tisun Three Limited’s tax reconciliation from its 2021 accounts (the tax reconciliation shows how you get from the profit in the accounts to the tax charge).

In this period, Tisun Three received £60,906 of property income distributions from the REIT. The accounts show the expected tax charge of £11,572 if you just apply the corporation tax rate of 19% to the £60,906 of income.

The tax reconciliation then explains why this tax doesn’t in fact arise. It shows the £11,572 of tax cancelled-out by a £11,572 negative entry labelled “dividend income”. The meaning is clear: the accounts are saying this was a dividend, and companies are normally exempt from corporation tax on dividends.

The problem is that this wasn’t a normal dividend at all. It was a “property income distribution” from a REIT – the REIT had been exempt on that profit, but corporate shareholders were not exempt. Tisun Three Ltd made the same mistake as Quidnet REIT did – it treated the payments from Quidnet as normal dividends, not as property income distributions.

The company therefore unlawfully failed to pay tax.

The result was that Tisun Three failed to pay tax on £60,906 of income in 2021, meaning lost corporation tax of £11,572 (at the 19% rate at the time).

This is repeated across almost all the Tisun companies accounts for all relevant years.5 You can download all the relevant accounts here.

The total untaxed income was £513,901, and therefore the lost tax was £97,641.6 Our methodology for this calculation is set out in full below.

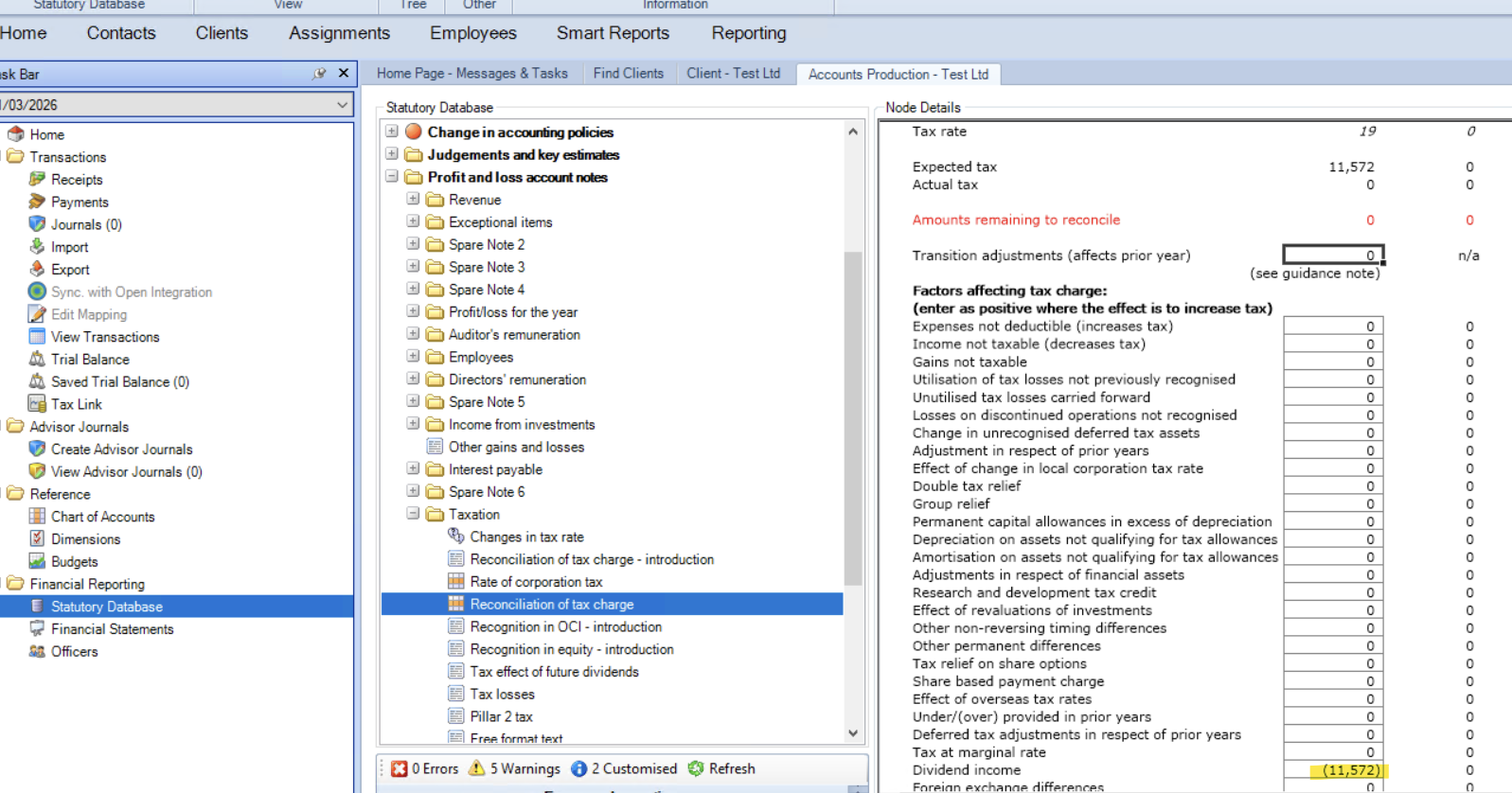

We should, however, consider the possibility that someone was being sloppy and typed “dividend income” when they really meant “dividend income is sheltered by losses”. If all we had was the printed accounts then we couldn’t exclude that possibility. We can, however, go beyond the printed accounts and read the underlying iXBRL code7 that Tisun Three Ltd’s accounting software uploaded to Companies House. The code for this line is:

This shows that the “(11,572)” figure in the tax reconciliation, negating the tax, was given the tag “TaxIncreaseDecreaseFromEffectDividendsFromCompanies”. This is a specific tag for the dividend exemption.8

If the company really had sheltered its income with losses, we would expect to see a group relief or loss-related reconciliation item (such as “TaxIncreaseDecreaseArisingFromGroupReliefTaxReconciliation”), not a dividends-from-companies item.

The iXBRL code also shows the accounts were submitted using CCH Accounts Production software. Here’s a screenshot showing what the accountant would have seen when entering the figures into that software, and what they would have entered to get the result that we see:

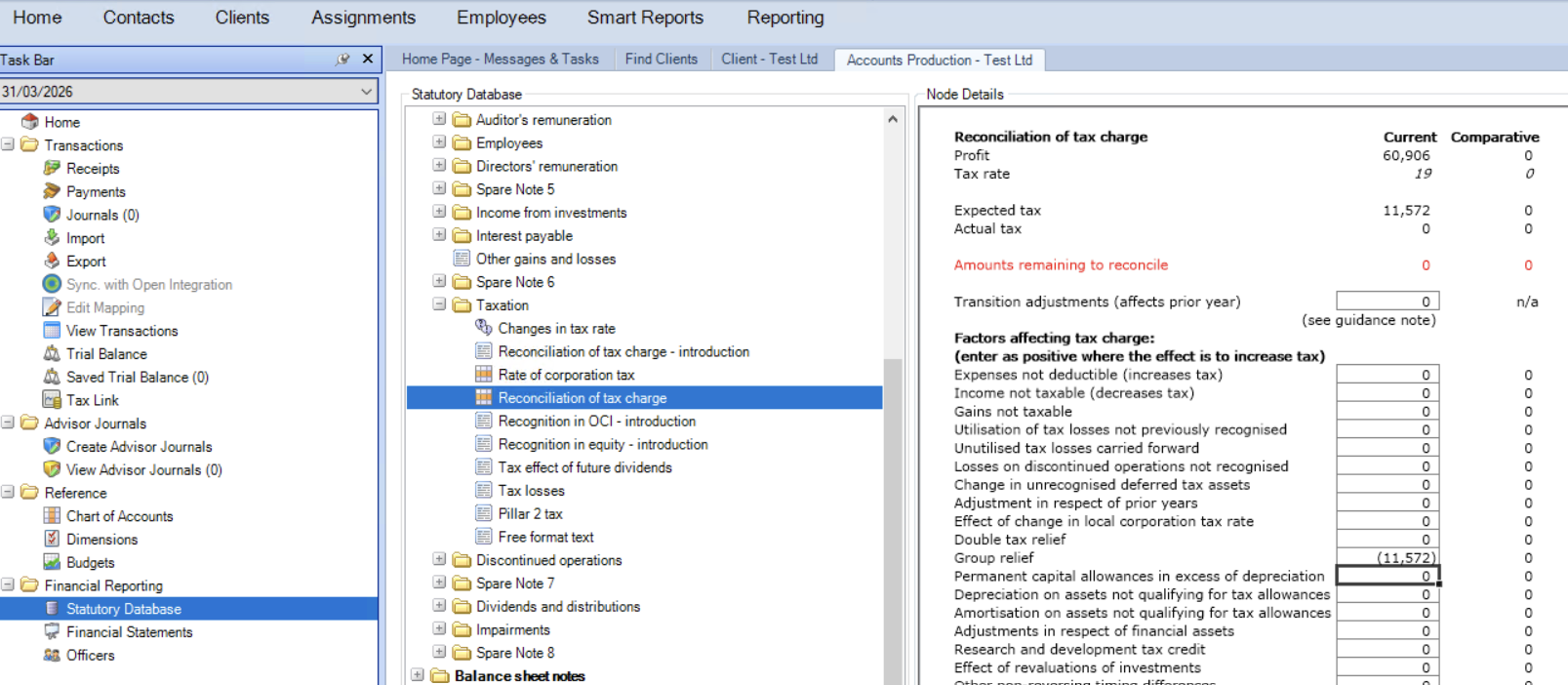

And here’s what they would have entered if they were actually claiming group relief:

With this result:9

The iXBRL code tells us that the tax reconciliation wasn’t merely poorly or sloppily worded – the accountant submitting the return actively selected the dividend exemption – when the dividend exemption could not in fact apply.

Is it theoretically possible tax losses were used?

It is possible in principle that Mr Tice was correct that group relief was claimed, and the accounts are simply wrong. For example, an accountant simply absent-mindedly used the dividend exemption box, when actually the Tisun companies were utilising losses from elsewhere in the group. The tax accountants we spoke to thought this would be unlikely. This is not a “fat finger” error, because it was repeated for three different companies across three years: 2020, 2021 and 2022.

There is, however, a more fundamental problem: our team undertook detailed due diligence of the wider group (including a review of 38 companies’ filings and 260 sets of accounts), and we found no material losses that could have been used to shelter the Tisun companies’ profits. That’s because, in short, the parent of the Tisun companies didn’t have assets or liabilities that could generate a material tax loss, and the way the group was structured means that losses of companies in the wider group were unavailable. Full details of this analysis are set out below.

So we believe we can exclude the possibility that the reason the Tisun companies paid no tax was the availability of losses elsewhere in the group.

Could the accounts just be wrong and tax really was paid?

We can exclude this for two reasons.

First, all four Tisun companies received dividends from Quidnet and then passed them straight up10 to their parent, Tisun Investments, without retaining anything to pay tax. The Tisun companies show no sign of any borrowing to fund any tax liabilities, and no creditor liability reflecting an upcoming tax bill. Their accounts show that each company’s sole asset was its investment in Quidnet REIT shares (funded by an inter-company loan).

Second, when the Sunday Times first asked Mr Tice about the lack of tax in the Tisun companies, he agreed they paid no tax, but said that was because of group relief.

The consequences

This is not tax avoidance. There was no loophole or grey area here. The rules on REIT property income distributions are clear: they are taxable in the hands of UK corporate recipients. This is understood by all advisers and (in our experience) most businesspeople owning and operating REITs.

Nor is this tax evasion – a criminal offence requiring dishonesty and intent. There is no evidence of either here.

The Tisun companies just paid the wrong amount of corporation tax. The practical consequence is that HMRC is likely to seek to recover that tax.

In most cases, HMRC would do this by issuing a “discovery assessment” — reopening a closed tax year where it discovers that tax has been underpaid. This is routine where an error only becomes apparent after the original return was filed.

Where a company has failed to take reasonable care — what the law calls a “careless” error — HMRC has six years from the end of the relevant accounting period to assess the additional tax. All of the periods in question here appear to fall comfortably within that window.11 We expect HMRC’s starting position would be that a failure to tax property income distributions is careless, and it is not obvious what explanation the company could provide that would overcome that.

In addition to the tax itself, penalties are likely. For careless inaccuracies, the statutory penalty range is up to 30% of the tax due. In practice, where the taxpayer cooperates and the error is disclosed, penalties are often lower — commonly around 10–15%.

Interest would also be payable on the late-paid tax: HMRC charges interest automatically on underpaid liabilities, calculated from the original due date, and in this case it would come to about £27,000 – the calculation is below.

There is then a wider question. If Quidnet failed to withhold tax because it didn’t understand the nature of REIT distributions, and the Tisun companies failed to pay tax on those distributions for the same reason… what other errors were made? In particular, did Mr Tice’s offshore trust pay any tax at all on its distributions? It certainly should have done – but the errors we have found make us wonder if in fact it did.

Richard Tice’s response

The Sunday Times wrote to Mr Tice on Thursday. We wrote on Friday:

We didn’t receive a response; neither did The Sunday Times.

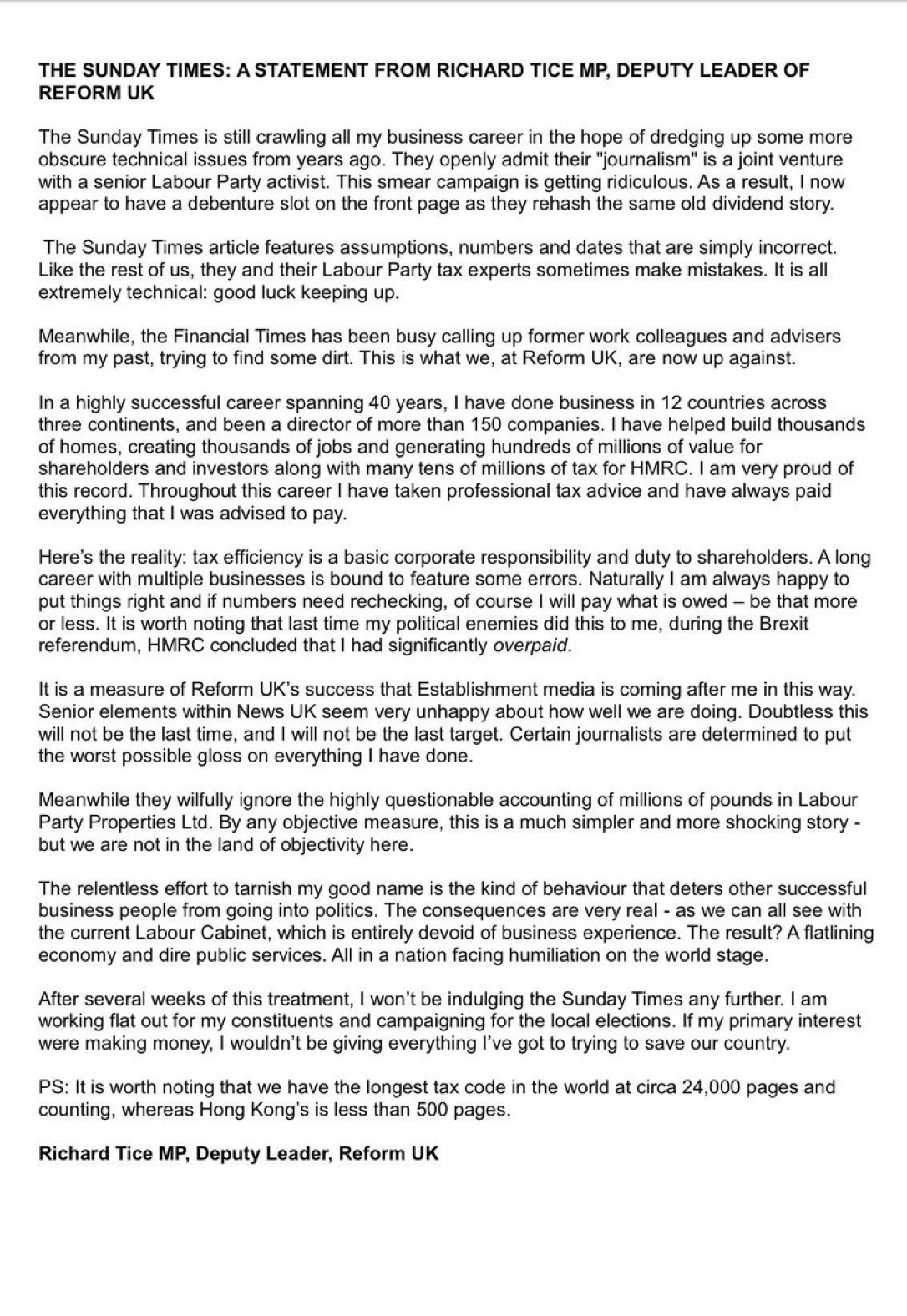

Shortly after publication of this report, Mr Tice published a statement. It does not deny any element of our reporting:

Methodology – determining the taxable profit

We calculate the £513,901 figure by:

- identifying the REIT distributions (PIDs) declared by Quidnet

- matching them to Tisun shareholdings

- reconciling against the filed accounts

The first step was to reconcile the dividend income shown in the Tisun accounts against the dividends we know Quidnet REIT declared, and the shareholdings recorded in Companies House filings.

Quidnet’s own accounts explicitly disclose the PID per share for each financial year. The table below sets out, for each year, the total PID per share, the individual dividends that make it up, and the treatment we have adopted:

| Financial year | Total PID per share | Individual dividends making up the total | Notes / treatment |

| FY2019 | 12.75p | 12.75p FY2019 final dividend, paid March 2020. | 100% PID. |

| FY2020 | 10.43p (weighted annual average) | 5.00p H1 interim (paid September 2020 as scrip) + 6.00p FY2020 final (paid April 2021). | 100% PID. The 10.43p figure ≈ total FY2020 dividends (£682,432) ÷ year-end shares (6,542,911). The 2020 dividends were paid as scrip — shares in Quidnet rather than cash — but the corporation tax treatment of scrip dividends for a REIT is the same as for a normal company, i.e. identical to cash dividends. |

| FY2021 | 6.99p (of which 5.50p H1 interim + 1.49p “REIT-period” slice of the final) | 5.50p H1 interim (paid August 2021); 5.30p FY2021 final declared 10 May 2022 for the period 1 July – 31 December 2021. | Quidnet ceased to be a REIT on 9 August 2021. The full 5.50p H1 interim was declared while Quidnet was still a REIT and so we treat it as 100% PID. Of the 5.30p final, only 1.49p qualifies as PID (covering the pre-9 August 2021 part of the post-H1 period); the remaining 3.81p is a post-REIT ordinary dividend and is not PID. |

| FY2022 onwards | 0.00p | — | No PIDs after the REIT period ended. |

We can cross-check these figures against the Tisun accounts. For Tisun One, the FY2019 final (£63,028) plus the H1 2020 interim (£26,665) totals £89,693 — the accounts show £89,680 (a trivial difference from scrip share rounding). This gives us high confidence that the PID calculations are correct.

There are, however, three anomalies that affect all the other accounts:

Anomaly 1: the dividends that didn’t exist

As we have reported, in 2020, all of the REIT distributions were paid in shares, not cash. According to Quidnet’s Companies House filings, those shares remained owned by the four Tisun companies. Yet the four sets of accounts show dividends being paid up to their parent company, Tisun Investments. There was no cash to fund those dividends, and no capital raising or increase in creditors to fund a cash dividend.

We don’t think this can be correct, but it’s not clear what happened. However, this does not change our calculations – the tax position is unaffected by whether the four Tisun companies in fact retained the shares or paid them as a dividend to Tisun Investments.

Anomaly 2: the FY2021 ~3.5% shortfall in Tisun One, Two and Three

For the year ended 31 December 2021, each of Tisun One, Two and Three booked dividend income of roughly £2,300 less than the per-dividend, per-share calculation implies. The shortfall is consistent in size (about 3.5%) and consistent in direction (accounts are lower than the calculated figure) across all three companies.

The per-dividend calculation for 2021 is simply the FY2020 final dividend (6.00p PID) plus the H1 2021 interim dividend (5.50p PID), each multiplied by the relevant Tisun shareholding at the record date:

| Company | Quidnet shares | FY2020 final 6.00p × shares | H1 2021 interim 5.50p × shares | Calculated 2021 total | Per filed accounts | Shortfall (£) | Shortfall (%) |

| Tisun One | 550,494 | £33,030 | £30,277 | £63,307 | £61,029 | £2,278 | 3.6% |

| Tisun Two | 549,383 | £32,963 | £30,216 | £63,179 | £60,906 | £2,273 | 3.6% |

| Tisun Three | 549,383 | £32,963 | £30,216 | £63,179 | £60,906 | £2,273 | 3.6% |

| Total | £98,956 | £90,709 | £189,665 | £182,841 | £6,824 | 3.6% |

The shareholdings are taken from the Quidnet confirmation statements on file at Companies House. The PID rates are the figures Quidnet discloses in its own 2020 and 2021 accounts: a 10.43p annual PID for FY2020 (broadly equal to the 5p H1 interim plus the 6p FY2020 final — we have treated it as 6p for the final on the basis of the stated per-dividend rates) and a 5.5p interim for H1 2021.

We cannot explain the ~3.6% shortfall. It is consistent in percentage terms across three separately-filed sets of accounts in one year; it could be some kind of intentional methodology but it seems more likely to be a calculation error.

In any event, for the purposes of the corporation tax calculation we will use the amounts Quidnet actually paid, per Quidnet’s audited accounts and the confirmation-statement shareholdings.

The effect is to increase our calculation of the Tisun companies’ taxable PID income by about £6,800 in aggregate, or about £1,300 of corporation tax at 19%.

Anomaly 3: Tisun Four’s dividend that didn’t exist

Tisun Four was incorporated on 11 September 2020 and subscribed for 238,233 Quidnet shares on 21 September 2020. Both dates are after the record date for Quidnet’s H1 2020 interim dividend, so ordinarily Tisun Four should not have received any part of the H1 2020 dividend, only the FY 2020 final dividend (paid in 2021) and then the H1 2021 interim dividend (paid later in 2021).

Tisun Four’s accounts for its first period (11 September 2020 to 31 December 2021) record total dividend income of £37,951. The comparative column in its 2022 accounts splits that 2021 income between a “Final paid” figure of £24,848 for 2020 and an “Interim paid” figure for 2021 of £13,103.

We can reconcile the “interim 2021” figure exactly:

| Line in Tisun Four accounts | Amount Booked in Tisun Four’s accounts | Reconciles to line in Quidnet’s accounts | Calculation based on Quidnet accounts and Tisun Four’s holding | Match? |

| Interim 2021 paid | £13,103 | H1 2021 interim @ 5.50p | 5.50p × 238,233 = £13,103 | Exact |

However we cannot reconcile the £24,848 “final 2020” figure against Tisun Four’s actual legal entitlement to dividends in 2020:

| Line in Tisun Four accounts | Amount Booked in Tisun Four’s accounts | Reconciles to line in Quidnet’s accounts | Calculation based on Quidnet accounts and Tisun Four’s holding | Match? |

| Final paid — the 6.00p paid when Tisun Four was shareholder | £24,848 | FY2020 final @ 6.00p | 6.00p × 238,233 = £14,294 | Does not match booked figure |

The £24,848 only reconciles against all Quidnet REIT’s 2020 dividends – which is wrong, because Tisun Four shouldn’t have been entitled to the 2020 interim dividend, as it wasn’t a shareholder on the record date.

| Line in Tisun Four accounts | Amount Booked in Tisun Four’s accounts | Reconciles to line in Quidnet’s accounts | Calculation based on Quidnet accounts and Tisun Four’s holding | Match? |

| Final paid (2021 comparative) — as booked | £24,848 | Full FY2020 annual PID @ 10.43p | 10.43p × 238,233 = £24,848 | Exact |

This cannot be correct, not least because Quidnet’s 2020 accounts (the statement of changes in equity in particular) only reconciles if the 2020 interim dividend was not paid to Tisun Four.

We will again resolve this by following the Quidnet audited accounts, not the Tisun Four accounts. That has the effect of reducing Tisun Four’s taxable PID income by £10,554, i.e. reducing the tax underpayment by £2,005.

Net effect on the corporation tax calculation

Anomalies 2 and 3 pull in opposite directions but the headline number is unchanged:

| Adjustment | PID income | CT at 19% |

| Tisun One/Two/Three FY2021 shortfall (added back to match Quidnet-paid PID) | +£6,824 | +£1,297 |

| Tisun Four H1 2020 excess (removed to match Quidnet) | (£10,554) | (£2,005) |

| Total adjustment vs. booked accounts | (£3,730) | (£708) |

The full reconciliation

Adjusting for the anomalies, and using the Quidnet audited accounts PID rates and the known shareholdings at each dividend record date, we can calculate the PIDs received by each Tisun company:

| Dividend | Tisun One | Tisun Two | Tisun Three | Tisun Four | Total |

| FY2019 final (12.75p PID) | £63,028 | £62,900 | £62,900 | £188,828 | |

| H1 2020 interim (5.00p PID) | £26,665 | £26,611 | £26,611 | £79,887 | |

| FY2020 final (6.00p PID) | £33,030 | £32,963 | £32,963 | £14,294 | £113,250 |

| H1 2021 interim (5.50p PID) | £30,277 | £30,216 | £30,216 | £13,103 | £103,812 |

| FY2021 final (1.49p PID) | £8,202 | £8,186 | £8,186 | £3,550 | £28,124 |

| Total PIDs | £161,202 | £160,876 | £160,876 | £30,947 | £513,901 |

The FY2019 final and (subject to anomaly 3) the H1 2020 interim dividends pre-date Tisun Four’s existence – it was incorporated in September 2020. The later dividends were received by all four companies.

This produces total taxable income of £513,901. The corporation tax rate at the time was 19%, and so the unpaid tax was £97,641.

Methodology – group relief

The Tisun group from 20 November 2020

At the time of the later REIT payments, the Tisun companies were in a small group. This diagram shows the group, and the other Quidnet REIT shareholders:

Tisun / Quidnet group structure as at 1 July 2021

- From Richard Tice to Tisun Holdco (Label: 77.1%)

- From Richard Tice to Tisun Holdco (Label: 22.9%)

- From Tisun Holdco to Tisun Investments (Label: 100%)

- From Tisun Investments to Tisun One (Label: 100%)

- From Tisun Investments to Tisun Two (Label: 100%)

- From Tisun Investments to Tisun Three (Label: 100%)

- From Tisun Investments to Tisun Four (Label: 100%)

- From Richard Tice (direct) to Quidnet REIT (Label: 13.00%)

- From RJS Tice Family Settlement to Quidnet REIT (Label: 16.88%)

- From RJS Tice Family SIPP to Quidnet REIT (Label: 34.98%)

- From Tisun One to Quidnet REIT (Label: 7.80%)

- From Tisun Two to Quidnet REIT (Label: 7.78%)

- From Tisun Three to Quidnet REIT (Label: 7.78%)

- From Tisun Four to Quidnet REIT (Label: 3.38%)

- From Huntress (CI) Nominees to Quidnet REIT (Label: 4.42%)

- From NJG Tribe SIPP to Quidnet REIT (Label: 2.99%)

- From Employees to Quidnet REIT (Label: 0.98%)

A company in a group can use “group relief” to utilise another group member’s tax trading losses, property business losses, and losses on certain financial and other types of assets, but not losses on capital assets.

There are, furthermore, stringent conditions for companies to be in a group relief group. There has to be a 75% common corporate shareholding (i.e. not via an individual owner). So the only possible companies that could have generated losses for the four Tisun companies are those in this diagram, and not other companies held separately by Mr Tice.12

Tisun Holdco never had any material assets or liabilities other than its shareholding in Tisun Investments.13 That leaves Tisun Investments Ltd as the only entity that could in principle have had losses that the four Tisun companies could have used. Tisun Investments’ accounts for 202014, 2021 and 2022, show that it did have sizeable accounting losses every year. However the nature of its assets and liabilities mean that we expect almost none of these losses would be recognised for tax purposes.

Tisun Investments Ltd’s assets were:

- Two flats in Kent, combined into a single dwelling, in a building where all the other flats are now owned by the Tice family. The value of the dwelling was around £600,000 and at the time in question it was unmortgaged.15 So, whether used by the family or rented out, the property is unlikely to have generated material tax losses, and certainly not the ~£170k/year needed to shelter the Tisun profits.16

- A motor vehicle on hire purchase – likely a personal car. The cost of this may be partially allowable for tax purposes, but the amounts are not material (probably £5-15k each year of capital allowances and running costs).

- Unlisted investment assets, never more than £120,000. We don’t have any information about what the investments are, but the limited value means that they won’t have justified material management expenses, and any loss on disposal would be a capital loss (which can’t be used to shelter trading profits or property income).

- Shareholdings in its subsidiaries – Tisun One, Two, Three and Four, and JMT Holdco. Management expenses incurred wholly and exclusively for the purposes of managing these assets would be tax deductible; but given the passive nature of the companies, it’s difficult to see how that could generate material deductible costs.

- Loans to its subsidiaries (Tisun One, Two, Three and Four), and its parent, (Tisun Holdco).17 Loans to connected parties generally generate no deductible debits for the lender (even if impaired or written off). The Tisun subsidiaries’ accounts suggest no interest is charged but, even if it was, the tax deductions for the payer would be matched by taxable income in Tisun Investments. These loans are therefore not a plausible source of net deductible tax losses.

- Loans to related parties, with a balance fluctuating between £0.8m and £1.1m. These include loans to Richard Tice personally, to Reform UK, and to other connected parties. The loans are all either interest-free or non-commercial. Non-commercial loans don’t generate deductible losses for the lender, and (again) neither do loans to connected parties.

Its liabilities were:

- 270,000 preference shares at 7% – treated as debt for accounting purposes but not for tax purposes, so no tax deduction available.

- £1,679,712 owed to JMT Corporation, an associated company that’s not part of the group relief group. The loan is interest-free18, so doesn’t generate any losses for Tisun Investments.

- Loans from related parties – again, these appear to be non-commercial funding arrangements. Any associated costs would be unlikely to be deductible, and there is no evidence of significant interest expense in the accounts.

We therefore conclude that Tisun Investments Ltd did not generate material losses that could be used to shelter profits elsewhere in the group. It looks like the company’s accountants agreed, as there’s no sign of a deferred tax asset, or any mention of losses or group relief.

It follows that the accounting did not merely misstate a group relief claim as a dividend exemption. There was no group relief in 2021 and 2022.

The Tisun group in 2020

Until 20 November 2020, Tisun Investments and its subsidiaries were part of a much larger group, headed by Sunley Family Holding Ltd.1920

Sunley / Tisun group structure as at 19 November 2020

- From Sunley Family Holding to Sunley Family Limited (Label: None)

- From Sunley Family Holding to Tisun Investments (Label: None)

- From Sunley Family Holding to JMT Corporation (Label: None)

- From Sunley Family Holding to West Eleven Investments (Label: None)

- From Sunley Family Holding to William Tice Family (Label: None)

- From Sunley Family Limited to Sunley Holdings (Label: None)

- From Sunley Holdings to Sunley Estates (Label: None)

- From Sunley Holdings to Executive Centre Brighton (Label: None)

- From Sunley Holdings to Environ (Kent) (Label: None)

- From Sunley Holdings to Bach Homes (Sunley) (Label: None)

- From Sunley Holdings to GMH (2004) (Label: None)

- From Sunley Holdings to SP (2004) (Label: None)

- From Sunley Holdings to Sunley FPR (Label: None)

- From Sunley Holdings to Fairfax Shelfco 321 (Label: None)

- From Sunley Family Limited to Prospero 2006 (Label: None)

- From Sunley Family Limited to Sunley Investments (Label: None)

- From Tisun Investments to Tisun One (Label: None)

- From Tisun Investments to Tisun Two (Label: None)

- From Tisun Investments to Tisun Three (Label: None)

- From Tisun Investments to Tisun Four (Label: None)

In the interests of clarity, the diagram omits the REIT and its other shareholders. It also omits a large number of inactive and/or dormant companies21, and entities (LLPs, settlements) which are not companies and so not relevant for group relief purposes.

During this period, Tisun Investments’ assets and liabilities were, so far as material, as set out above regarding the post-2020 period – so it had no losses to surrender to the Tisun companies. However the Sunley group had companies with much a wider and more extensive degree of activity than Tisun Investments, and some of the Sunley companies could have had large losses – potentially hundreds of thousands of pounds.22232425 So, at first sight, this could be an answer to how the Tisun companies’ 2020 profits were eliminated.

There is, however, a technical barrier that means in fact no losses the Sunley group could be used by the Tisun companies. Sunley Family Ltd had a “tracking share”26 structure. The economic rights to Tisun Investments Limited were not held by the wider Sunley group but were reserved to holders of Sunley Family Ltd’s “B ordinary shares”.27 Those B shares were held by Richard Tice – partly for himself, and partly as trustee for his Tice children. This “broke” the tax group – if the economic interest in a company is held by a third party then it’s no longer a member of its parent company’s tax group:

- The group relief legislation is in Part 5 CTA 2010. The basic rule is that two companies are in the same group if one is a 75% subsidiary of the other, or both are 75% subsidiaries of a third company.

- There are a further series of complex tests which mean that if the economic rights of the subsidiary are in fact with a third party, the subsidiary is not in its parent’s tax group. The statutory gateway for this is section 151 CTA 2010.28

- HMRC explain the policy rationale in CTM81005. The rules are designed to stop group relief where the apparent parent is not the true economic parent – otherwise it would be easy for economically unrelated companies to use each other’s losses. 29

It follows that Tisun Investments was not part of the Sunley group for tax purposes.30

The Sunley losses are therefore irrelevant – however large they were, they couldn’t have been used by the Tisun companies. The only potential source of losses for the four Tisun companies was Tisun Investments and, for the reasons set out above, it had no material tax losses.

Earlier periods

Tisun One, Two and Three were incorporated on 6 July 2018, and Tisun Four was incorporated on 11 September 2020. But Tisun Investments Ltd was not a newly-created shell when the Quidnet REIT structure was put in place: it had existed since 2006 and, as its filed accounts show, had a mixture of investment, property, loan and short-lived work-in-progress activity over the years.

However, any tax losses from these earlier activities could not have sheltered the £514,000 of Quidnet REIT property income distributions received by the Tisun companies. Until 1 April 2017, carried-forward losses in one company could never be surrendered as group relief to shelter the profits of another company at all – they stayed locked in the company that made them. From 1 April 2017, the new Part 5A CTA 2010 regime allows carried-forward losses to be surrendered as group relief, but only if they arose on or after 1 April 2017 and only where the surrendering and claimant companies were members of the same group when the loss arose.31 Pre-2017 Tisun Investments losses are therefore locked inside Tisun Investments.

For completeness, we reviewed every filed set of Tisun Investments accounts from 2007 to 2024.32 The picture is of an investment/holding company with some short-lived property and work-in-progress activity, paying tax in several years and with no material carried-forward losses.

Methodology – interest calculation

We calculated late-payment interest using HMRC’s published late-payment rates, applying simple daily interest to the corporation tax outstanding in each period. The first period starts on 1 October 2021, the first deadline for paying the tax. The amount outstanding then increases when later corporation tax liabilities fall due:

| Period | HMRC rate | Amount owed | Interest |

|---|---|---|---|

| 1 Oct 2021 to 7 Jan 2022 | 2.60% | £51,055.85 | £356.41 |

| 7 Jan 2022 to 21 Feb 2022 | 2.75% | £51,055.85 | £173.10 |

| 21 Feb 2022 to 5 Apr 2022 | 3.00% | £51,055.85 | £180.44 |

| 5 Apr 2022 to 24 May 2022 | 3.25% | £51,055.85 | £222.76 |

| 24 May 2022 to 11 Jun 2022 | 3.50% | £51,055.85 | £88.12 |

| 11 Jun 2022 to 5 Jul 2022 | 3.50% | £56,261.28 | £129.48 |

| 5 Jul 2022 to 23 Aug 2022 | 3.75% | £56,261.28 | £283.23 |

| 23 Aug 2022 to 1 Oct 2022 | 4.25% | £56,261.28 | £255.49 |

| 1 Oct 2022 to 11 Oct 2022 | 4.25% | £92,297.63 | £107.47 |

| 11 Oct 2022 to 22 Nov 2022 | 4.75% | £92,297.63 | £504.48 |

| 22 Nov 2022 to 6 Jan 2023 | 5.50% | £92,297.63 | £625.85 |

| 6 Jan 2023 to 21 Feb 2023 | 6.00% | £92,297.63 | £697.92 |

| 21 Feb 2023 to 13 Apr 2023 | 6.50% | £92,297.63 | £838.26 |

| 13 Apr 2023 to 31 May 2023 | 6.75% | £92,297.63 | £819.30 |

| 31 May 2023 to 11 Jul 2023 | 7.00% | £92,297.63 | £725.74 |

| 11 Jul 2023 to 22 Aug 2023 | 7.50% | £92,297.63 | £796.54 |

| 22 Aug 2023 to 1 Oct 2023 | 7.75% | £92,297.63 | £783.90 |

| 1 Oct 2023 to 20 Aug 2024 | 7.75% | £97,641.19 | £6,717.18 |

| 20 Aug 2024 to 26 Nov 2024 | 7.50% | £97,641.19 | £1,966.20 |

| 26 Nov 2024 to 25 Feb 2025 | 7.25% | £97,641.19 | £1,764.90 |

| 25 Feb 2025 to 6 Apr 2025 | 7.00% | £97,641.19 | £749.03 |

| 6 Apr 2025 to 28 May 2025 | 8.50% | £97,641.19 | £1,182.39 |

| 28 May 2025 to 27 Aug 2025 | 8.25% | £97,641.19 | £2,008.33 |

| 27 Aug 2025 to 9 Jan 2026 | 8.00% | £97,641.19 | £2,889.11 |

| 9 Jan 2026 to 15 Apr 2026 | 7.75% | £97,641.19 | £1,990.28 |

| £26,855.91 | |||

The calculation runs to 15 April 2026 and assumes no tax was paid before then.

Disclosure

Dan Neidle, the founder of Tax Policy Associates, is a member of the Labour Party. Tax Policy Associates has no political affiliation. Our previous reports suggesting politicians failed to pay the tax due investigated Angela Rayner, Keir Starmer, Ian Lavery and Nadhim Zahawi, as well as local Conservative, Labour and Liberal Democrat parties. We have also published reports rejecting accusations that Jeremy Hunt (twice) and Rishi Sunak avoided tax.

This issue was identified by one of our contributors, D. We developed this report in conjunction with Gabriel Pogrund of the Sunday Times, who discovered the initial tax issues with the Quidnet structure.

The REIT and accounting analysis for this and our original report was mostly from K, M1, and P1, with additional insights from D, R, P2 and M2. Thanks to J, B and M3 for practical advice on, and demonstrations of, the CCH accounting software used by the Tisun companies.

And finally thanks to all the volunteers who worked on the group relief due diligence, reviewing filings for 38 companies and 260 sets of company accounts.

Photo by Derek Bennett, CC BY 2.0, via Wikimedia Commons.

.jpg){kind=link}

The questions Richard Tice isn’t answering

Richard Tice’s property company failed to pay £120,000 in tax

Companies House flaw exposed five million directors and enabled company hijacking

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

The bizarre UK group selling US tax fraud to hundreds of Britons – and prosecuting its critics

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Footnotes

The logic is that funds don’t pay tax; their investors do – we see this across almost all forms of investment fund, although it’s achieved in a variety of different ways. ↩︎

When a UK company receives a normal dividend from another company, it doesn’t pay tax – there’s a corporation tax exemption for dividends. The reason is that the subsidiary would have paid tax on its profits, so it makes no sense to tax them again. However property income distributions from REITs are different. A REIT does not pay tax on its property income. So it stands to reason that a UK company receiving a property income distribution pays corporation tax on it – and that is indeed the result. ↩︎

Why have so many companies? At the time, the REIT rules penalised a REIT if any single corporate shareholder held 10% or more. By splitting a single ~27% holding across four companies, each holding under 10%, it was straightforward to avoid the prohibition. The 10% rule was regarded as rather pointless by both taxpayers and HMRC and changes in 2023 mean it now rarely applies. All of which means that we would regard the splitting of the ownership (of itself) as tax planning, not tax avoidance; we don’t believe HMRC would have any realistic prospect of challenging it. ↩︎

Because they were UK companies, there was no requirement for Quidnet REIT to withhold tax. ↩︎

We see the same exact approach in the Tisun One, Tisun Two and Tisun Three accounts from 2020 to 2022, and the Tisun Four accounts for 2022. Tisun Four has no tax reconciliation for 2020 and 2021 but its accounts for these two years are otherwise consistent with the other ten accounts. In 2022, the companies did receive some ordinary dividends which really were exempt, but also property income distributions which were not. Our reconciliation distinguishes the two cases. ↩︎

These figures fully take into account that some dividends were ordinary dividends which absolutely were exempt. ↩︎

When a UK company files accounts electronically, it often does not send Companies House a simple PDF. Instead, it sends an iXBRL file: a document that looks like ordinary accounts on screen, but with machine-readable tags embedded behind the text and numbers. The tags were standardised by the Financial Reporting Council – you can see and search them all here. ↩︎

Also note that the £60,906 income in the tax reconciliation statement is given the tag “DividendIncome”; not technically correct. ↩︎

The screenshots are from the current version of CCH Accounts Production; we understand from the accountants we spoke to that the screens were the same in 2020, 2021 and 2022. ↩︎

Subject to an oddity about scrip dividends, discussed further below. ↩︎

i.e. because the earliest accounting period ended 31 December 2020, meaning HMRC has until 31 December 2026. ↩︎

A significant entity – JMT Corporation Ltd – is excluded from the diagram and analysis below because, whilst it is held by Tisun Investments, it isn’t part of a 75% group with the Tisun companies and so can’t surrender losses to them. JMT Corporation was Richard Tice’s late mother’s former investment company. JMT Holdco was incorporated in March 2020, held by Richard Tice directly – it then acquired JMT Corporation. At some point between March and December 2021, Tice sold 55.4% of the shares in JMT Holdco to Tisun Investments; Tisun Investments therefore treats it as a subsidiary for accounting purposes (but it’s not part of a group relief group). By 2024, JMT Corporation’s sole material asset was a £1.66m intercompany loan to Tisun Investments. ↩︎

It was incorporated on 17 March 2020. From 2020 to 2023 it appears to have been a very thin holding company: its only visible asset was its 100% shareholding in Tisun Investments Limited, carried at £32,418, and its only visible liabilities were short-term group creditors and, in 2020-2021, accruals/deferred income. The filed accounts do not include a profit and loss account. From the balance sheet/reserve movements only, the apparent results are: 2020 loss £925; 2021 nil movement; 2022 positive movement/profit £925; 2023 nil movement. ↩︎

Note the 2020 accounts were massively restated the following year; the 2020 accounts themselves show a large profit. ↩︎

In late 2022, a further part of one of the flats was acquired, worth £126,000, and a £491,000 mortgage with Weatherbys was taken out over all three titles the following year 2023. ↩︎

The building is on a private estate. We have full details of the dwelling, have reviewed planning consents, and believe we have identified how the dwelling is used; we are, however, not publishing further details given the possible privacy implications for the Tice family. ↩︎

The identity of the borrowers is not explicitly disclosed but the £2,064,976 “owed by group undertakings” in Tisun Investments’ 2024 accounts exactly reconciles to the balances shown in the latest accounts of the four Tisun subsidiaries and Tisun Holdco. Tisun One shows £559,961 owed to group undertakings, Tisun Two £558,960, Tisun Three £558,960, Tisun Four £369,500 and Tisun Holdco £17,595, giving £2,064,976 in total. ↩︎

We know JMT Corporation was the lender because JMT Corporation’s 2022 accounts show a matching amount “owed by group undertakings”. We know it’s interest-free because we can use JMT Corporation’s balance sheet to reverse-engineer its profit and loss account. The accounts show the company’s total assets decreasing by £31,261 as it liquidated its entire £488,192 investment portfolio, drew down its cash and other debtors, and used these funds to increase the pre-existing loan to Tisun Investments. Concurrently, total liabilities decreased by £17,229 as the company paid down historical short-term creditors and deferred tax provisions. Offsetting the £31,261 drop in assets against the £17,229 reduction in liabilities results in a net asset decrease of £14,032, which matches the company’s reported loss for the year. We see the same in other years. We conclude that there cannot have been any interest received on the loan to Tisun Investments. ↩︎

Until October 2020, Tisun Investments sat “lower” in the group, under Sunley Family Limited group. In October 2020 it moved under Sunley Family Holding Ltd, and on 20 November 2020 it moved out to Tisun Holdco. We discuss the consequence of that below. We show the October to November 2020 picture for clarity. ↩︎

Sunley Family Holding Ltd was itself held partly by Shuttlecock Holdings Ltd and Sunciera Holdings Corporation – both offshore companies, the ownership of which is unknown and not disclosed at Companies House. ↩︎

Bernard & Mary Sunley Limited, BHE Property Developments Limited, Castleford Homes Limited, John B Sunley & Sons Limited, Sir John Jackson Limited, Sunley Group Limited, Sunley London Limited, Sunley Properties Limited, Sunley Securities Limited, Sunley Trading, Great Maytham Hall Management Limited, Swallowfield Park Management Limited, JMT Settlement Limited, and William Tice Settlement Limited ↩︎

In particular, Sunley Estates Limited was a substantial property company. Its 2020 accounts show investment property of £2.1m, group debtors of £12.2m, group creditors of £1.5m and net assets of £13.6m. Its profit and loss account grew from £8,862,526 in 2019 to £9,426,401 in 2020, telling us that the company’s total profits were £563,875 that year (the accounts disclose no dividends). However we need to reverse out two elements that are disregarded for tax purposes: a £1,171,448 positive revaluation of property assets, and a “deferred tax” provision of £222,575. That tells us the company may actually have made a loss of about £385,000. That is absolutely not a robust number – it’s possible that some or even all of this loss would disappear if we actually knew the underlying revenue and expense items. The loss would also be smaller or disappear if dividends were paid. Subsequent accounts (and the lack of any obvious utilisation against later profits here or elsewhere) suggest to us this may not actually have been a tax loss. Nevertheless, we conservatively assume that the tax loss we’ve inferred was real. ↩︎

West Eleven Investments looks much larger at first sight. Its net assets fell from £1,497,834 to £1,151,898, and its profit and loss reserve moved from a £2,176 deficit to a £348,112 deficit. That is a raw reserve fall of about £346,000. But the notes show a £399,546 tangible-asset revaluation loss and a £35,653 investment revaluation gain. Reverse those revaluations and the large apparent loss disappears entirely — the adjusted position is a small profit, not a loss. But, again, it doesn’t matter how many losses were generated – the overlapping period rules still apply. ↩︎

William Tice Family may have generated some small losses. Its net assets increased from £1,936,930 to £1,967,402, and its profit and loss reserve increased from £724,348 to £754,820. It therefore did not show an accounting loss overall. The accounts include a £69,540 investment revaluation gain and deferred tax increased from £94,389 to £121,235; stripping those out suggests, at most, a small underlying loss of about £12,000. ↩︎

On the (rare) occasions when these companies submitted full accounts, there was evidence of group relief. Sunley Holdings Limited’s accounts for 2017 and for 2019 show group relief surrendered and received. JMT Corporation Limited’s 2011 accounts show losses surrendered. However neither company filed full accounts in 2020 and so this doesn’t help us determine if losses were surrendered in 2020. ↩︎

This is sometimes done where for e.g. historic/tax/contractual reasons shares have to stay owned by one person/company, but it’s been agreed that actually all the benefit should go to someone else. In other words, it’s a way of executing a demerger without all the consequences of an actual demerger. ↩︎

The B shares were created on 13 October 2006, reclassifying 12,512 ordinary shares held by Richard Tice as B ordinary shares tracking all economic rights in Tisun Investments (defined to be “B Company Limited”). A 2010 resolution re-designated 3,713 D ordinary shares as B ordinary shares, ranking pari passu with the existing B ordinary shares. The structure was restated in new articles adopted in December 2014. Those articles again defined “B Company Limited” as Tisun Investments Ltd and preserved the same tracking rights over distributions and assets from that company. By the 2020 confirmation statement there were 16,225 B ordinary shares. The structure was then unwound in October 2020. A 16 October 2020 share-exchange resolution put Sunley Family Holding Limited above Sunley Family Limited. A 19 October 2020 dividend-in-specie resolution then declared a dividend on the B ordinary shares, satisfied by transferring the entire issued share capital of Tisun Investments Ltd. The result was that Tisun Investments was now in both the legal and the economic ownership of Mr Tice. ↩︎

The detailed equity-holder and profits/assets rules are in Chapter 6 of Part 5 CTA 2010, including section 158, section 165 and section 167. ↩︎

HMRC’s CTM81121 example illustrates the same point: ordinary share capital can give the appearance of a group, but if the profit rights show someone else is the true economic parent, the group-relief relationship fails. ↩︎

A point of detail: on 19 October 2020, Sunley Family Limited transferred the issued share capital of Tisun Investments to Sunley Family Holding Limited by dividend in specie; the B shares remained so Tisun Investments did not join Sunley Family Holding Ltd’s tax group. Then on 20 November 2020, Tisun Investments was acquired by Tisun Holdco. ↩︎

A separate anti-avoidance rule in CTA 2010 Part 14, Chapters 2C and 2D (ss.676CB, 676CE and 676CH) also blocks pre-entry carried-forward losses from being surrendered as group relief for five years after an accounting period in which there is a change of ownership of the surrendering company. ↩︎

The relevant documents are: 2007 accounts, 2008 accounts, 2009 accounts, 2010 accounts, 2011 accounts, 2012 accounts, 2013 accounts, 2014 accounts, 2015 accounts, 2016 accounts, 2017 accounts, 2018 accounts, 2019 accounts, 2020 accounts, 2021 accounts, 2022 accounts, 2023 accounts and 2024 accounts. ↩︎

Leave a Reply to Dan Neidle Cancel reply