Simon Goldberg1 and his UK-based organisation, Empower the People, are running an elaborate scheme to defraud the US Government. The group files fake US tax returns to trick the IRS into refunding their members’ everyday UK consumer spending – a practice the US tax authorities have repeatedly warned is fraudulent.

When YouTuber Salim Fadhley publicised the fraud, Goldberg reported Fadhley to the UK police for harassment, instructed a law firm to send a “cease and desist” letter, and ultimately commenced a private criminal prosecution against him in Chelmsford Magistrates’ Court.

Empower the People operates a wider pseudo-legal grift. They run bogus “mortgage-elimination” schemes – which the Financial Conduct Authority warns are scams and potentially criminal to provide. None of this is done for free – they charge £1,300 for the US tax scam, plus 13% of the return – but Empower the People fails to charge UK VAT on its services, or pay corporation tax on its profits.

We believe there should be a criminal investigation into Goldberg and his group, and that the CPS should immediately take over Goldberg’s private prosecution, and discontinue it if it is not in the public interest.2 HMRC and the FCA should also investigate what appear to be widespread breaches of tax and regulatory law.

In this report:

- The claim – the IRS will refund all your spending

- The reality

- How the fraud works

- How much tax is being defrauded?

- Who are Empower the People?

- The private prosecution

- The evidence for the 1099-OID fraud

- Have Goldberg and his team committed fraud?

- What else does Empower the People do?

- Failure to pay UK tax

- Failure to safeguard its members personal information

The claim – the IRS will refund all your spending

Simon Goldberg says he’s found the ultimate loophole: a way to legitimately claim back almost every penny you have ever spent on everyday bills, credit cards, and mortgages, using the 1099-OID US tax form:3

The core claim is so absurd it is hard to understand how anyone believes it: whenever you pay a bill in the UK, your bank secretly creates a matching credit. Goldberg tells his followers they can claim this hidden credit as a cash refund directly from the US tax authority – the IRS. And so you can claim a cheque from the IRS covering almost all your day-to-day spending.

Goldberg says his organisation, Empower the People, will handle this entire process:

- Tally up your spending: Members calculate their total spending across all bank accounts and credit cards for a given calendar year. Almost everything counts: utility bills, rent, mortgage payments, petrol, and even buying gold. Only cash withdrawals are excluded.

- Hand over your passport: Members send their physical passports to Empower the People so they can apply for a US Individual Taxpayer Identification Number (ITIN).

- Sign blank forms: Empower the People passes the financial figures to a secret “expert” (who calls himself “Paul Muad’ib” after the sci-fi character). Because the expert’s method is his “intellectual property”, members receive signature pages for two US tax forms(with nothing completed on the forms). They sign them in blue ink and send them back to Empower the People – pledging under penalty of perjury to the contents of a completed tax return they are never allowed to see.

- Send the forms to the IRS: Empower the People couriers the forms to the IRS in carefully timed batches so it doesn’t look “bloody obvious what’s going on”.

- Wait for the cheque: Goldberg promises that, if successful, the IRS will send the member a physical cheque in US dollars. He says that the IRS retains about 20% of the refund, and Empower the People takes a fee, leaving the member with a cash windfall of roughly 65% of everything they spent that year.

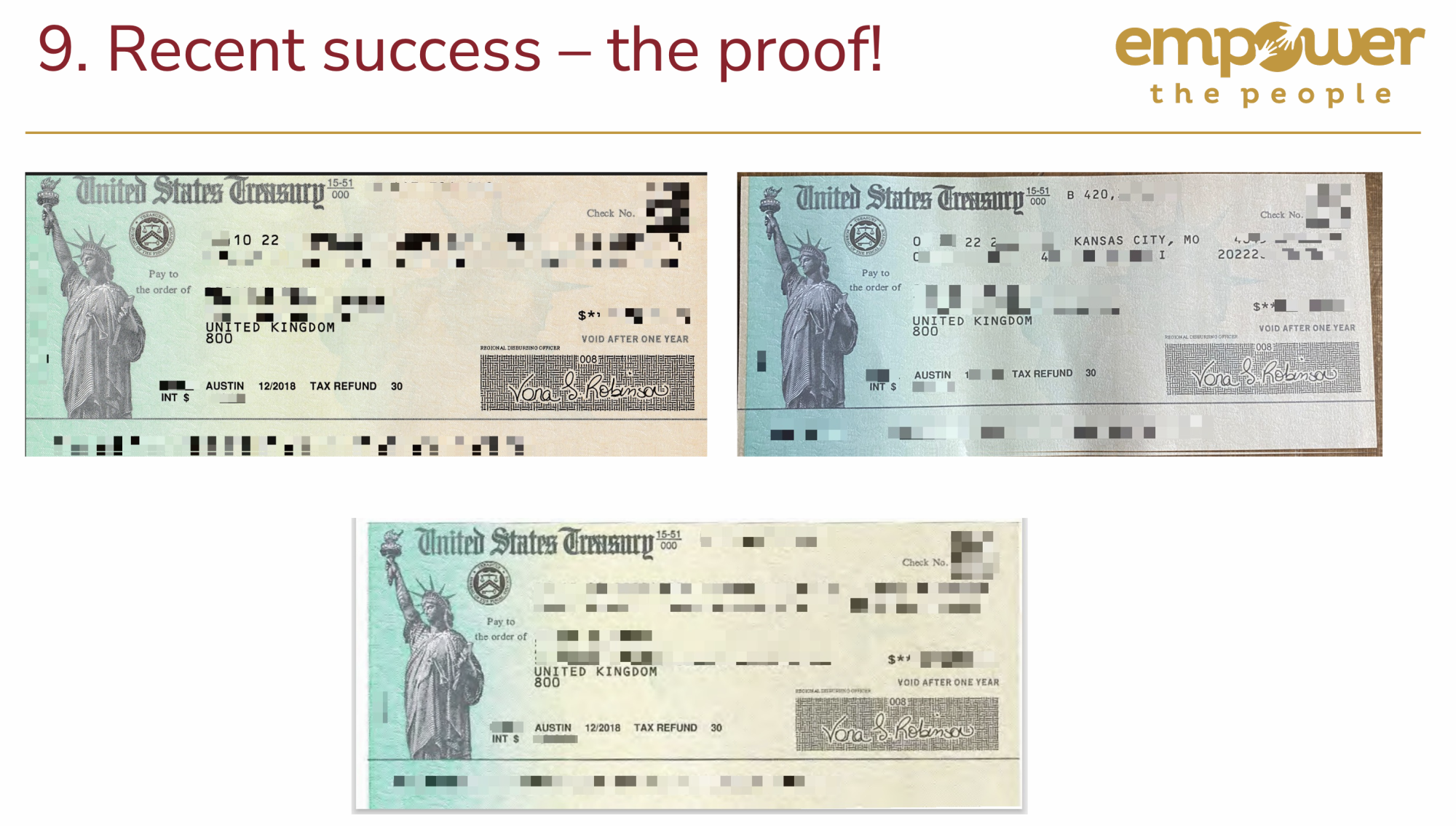

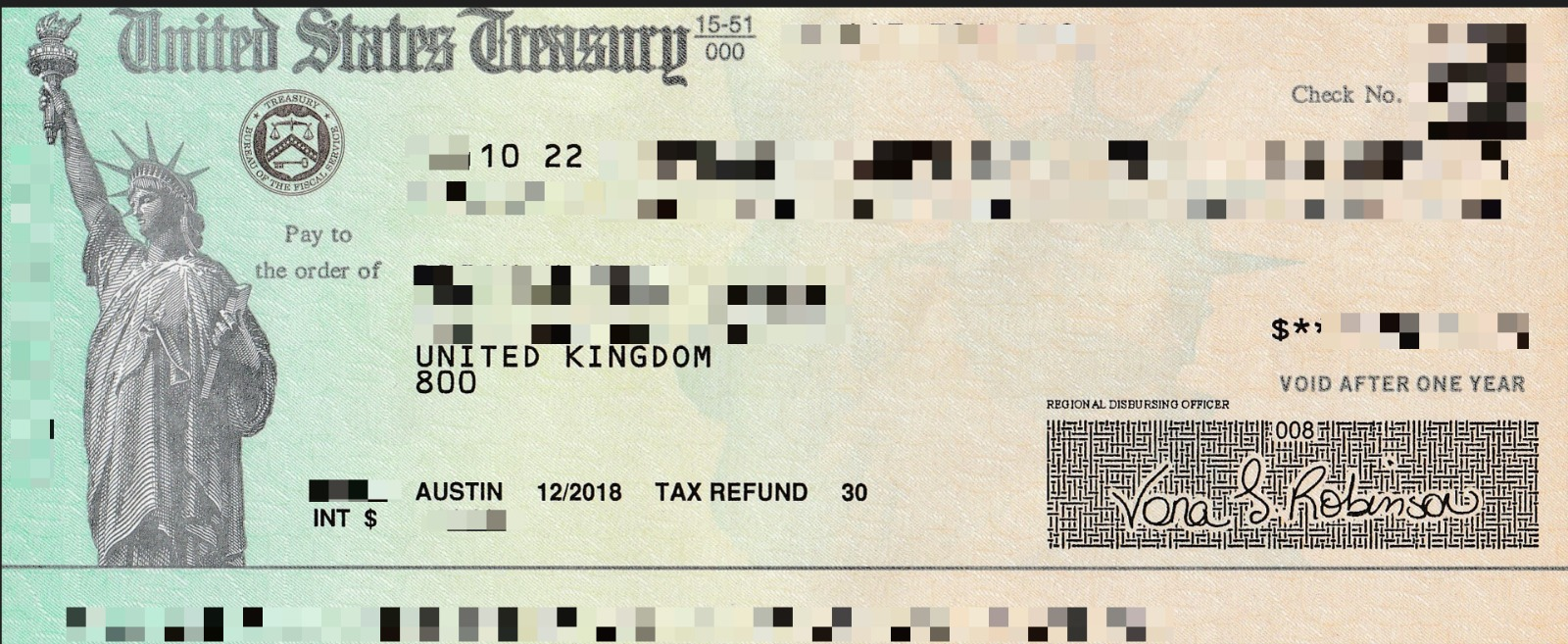

- The cheques arrive: there is a success rate of about 50% – and Empower The People provide this proof that cheques are actually received from the IRS:4

Naturally there is a fee – an upfront “donation” of £1,300 per year claimed, plus a 13% “back-end fee”:

Members are then encouraged to “recycle” this fabricated wealth by spending it to pay off their mortgages – which they can then tally up and claim back again the following year, creating a “snowball” of debt-free cash:5

The reality

None of the claims are real. It should go without saying, but the IRS doesn’t knowingly give US tax refunds for UK consumer spending.

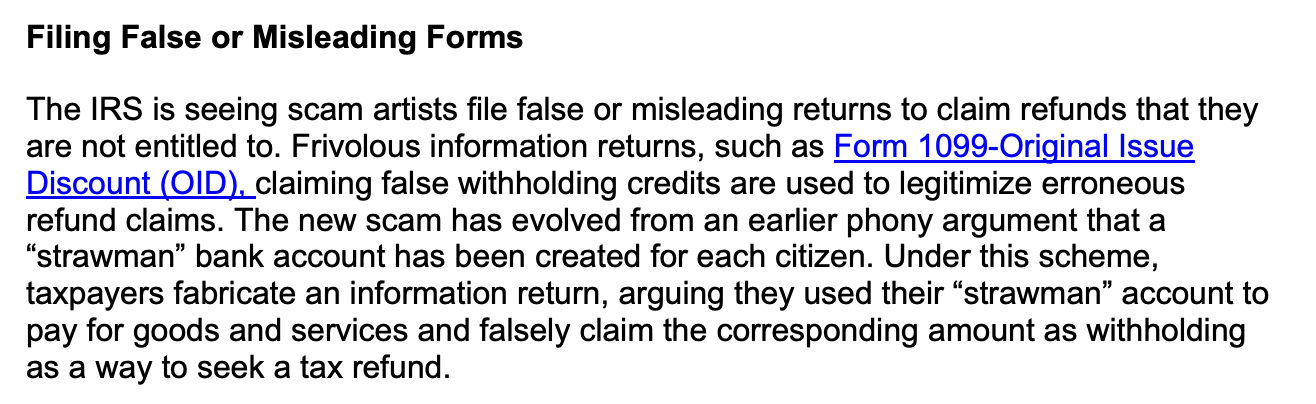

There have been many schemes like Goldberg’s, which use the 1099-OID form to trick the IRS into posting refund cheques. The IRS publishes an annual “dirty dozen” list of tax scams, and the 2009 list explicitly called out a 1099-OID fraud that perfectly describes Goldberg’s methodology:

These schemes are so persistent that the IRS continues to issue warnings about them, most recently including them in its 2025 list.

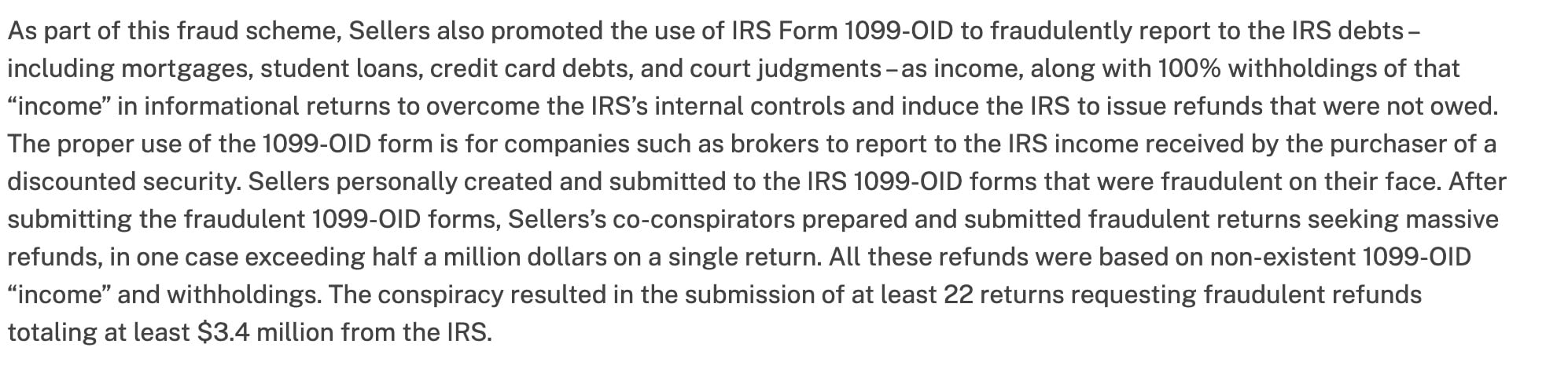

The US authorities do not just issue warnings; they aggressively prosecute 1099-OID promoters. In May 2024, a promoter was sentenced to five years in jail for running a scheme remarkably similar to Empower the People’s:

This is not an isolated case. There have been many other prosecutions for substantially identical schemes.

While most of the frauds prosecuted to date involved US citizens, international borders do not offer immunity. The IRS has successfully extradited 1099-OID fraudsters from Trinidad and Tobago and from Canada to face trial:6

In his webinars, Goldberg refers extensively to the “expert” who completes the forms – the anonymous man who calls himself “Paul Muad’ib”. We do not know who he is. It is possible he does not exist and is an invention of Goldberg. It is also possible he is a real person, with “expertise” in US tax fraud. The one thing we are certain of is that he is operating completely outside the bounds of legitimate US tax practice. If he holds a valid IRS credential, Federal regulations strictly prohibit him from charging a percentage-based fee.7 Whether credentialed or not, he is operating illegally as a ‘ghost preparer‘—charging for tax preparation but unlawfully hiding his identity from the IRS by failing to sign the returns he generates.8

How the fraud works

Goldberg provides a threadbare justification for UK residents using 1099-OID forms to claim US tax refunds: payment of bills creates a “security” and that, because “your time is priceless”, your bills have been discounted:

He says:

Because whenever you pay a bill, what you’re actually doing is creating another debt, as it were, or in many cases, new cash, a new security.

…

The fact of the matter is that your time is priceless. So whether you’re accepting a thousand pounds an hour, 200 pounds an hour or five pounds an hour, you have discounted your value, your time from infinity down to that figure. It’s been discounted. And then you issued bills and you were the original issuer of those bills.

Why does Goldberg say this? And why is one particular US tax form, the 1099-OID, so important?

A 1099-OID form is used to report “original issue discount” (OID) – taxable income generated under US Federal tax law when debt securities are issued at a discount from their maturity value. The company that issued the securities gives its investors a 1099-OID, and they include it in their US tax return. In some unusual circumstances, the issuer of the debt security will withhold US tax at 30% from the discount amount. The taxpayer can reclaim this in their US tax return – and in some cases this can result in the IRS issuing a cheque to a person. This footnote has a more complete example of how a 1099-OID normally works.9

A real 1099-OID refund scenario looks like this:

- From Company issues $10,000 bond to investor for $9,500 cash to A year later, company redeems bond, paying investor $10,000 (Label: None)

- From A year later, company redeems bond, paying investor $10,000 to Company withholds $150 tax from this (i.e. 30% of the $500 OID) and pays to IRS (Label: None)

- From Company withholds $150 tax from this (i.e. 30% of the $500 OID) and pays to IRS to Company gives investor 1099-OID showing $500 OID and $150 withheld (Label: None)

- From Company gives investor 1099-OID showing $500 OID and $150 withheld to Investor files tax return with 1099-OID and claims credit/refund of the $150 (Label: None)

None of this has anything to do with personal bank or credit card transactions. And nothing Goldberg says bears any relation to what is on an actual 1099-OID form, and his nonsense about our time being discounted bears no relation to the actual US tax definition of “original issue discount” in 26 U.S.C. § 1273(a)(1) (as explained in IRS guidance). Most importantly: at no point does Goldberg explain how a withholding tax refund can possibly be due, when his clients never suffered any US withholding tax in the first place.

Any feature of a tax system which can result in a cash payment by a tax authority is vulnerable to fraud10 – and that’s the problem with 1099-OIDs.

The essence of the fraud is simple: fabricate a 1099-OID to show withholding tax that you never suffered, and use it to claim a refund:

- From UK consumer spends $10,000 to ‘Expert’ fabricates 1099-OID showing $10,000 of OID and $10,000 of tax withheld. No tax was actually withheld (Label: None)

- From ‘Expert’ fabricates 1099-OID showing $10,000 of OID and $10,000 of tax withheld. No tax was actually withheld to EtP files tax forms showing $10,000 of income and overpaid tax of $8,000 (Label: None)

- From EtP files tax forms showing $10,000 of income and overpaid tax of $8,000 to IRS retains 20% of the $10,000 as tax and refunds the remaining $8,000 (Label: None)

In principle, the IRS should always be able to spot this, because they should be able to see that they never received the withholding tax.11 In practice the timing of returns and refunds mean that the IRS often pays out refunds before it has reconciled refund claims with the filings it has received. The reconciliation also seems imperfect, probably because of the very large volumes and antiquated systems – so some 1099-OID frauds continue for a while before being discovered.

How much tax is being defrauded?

Empower the People’s 1099-OID scheme seems to have started in 2022. This cheque, from the webinar slide deck, shows it was issued in October 2022 and relates to tax year 2018.12

At its 2023 Annual General Meeting (AGM), the organisation boasted to members that it had processed 80 claims that year.

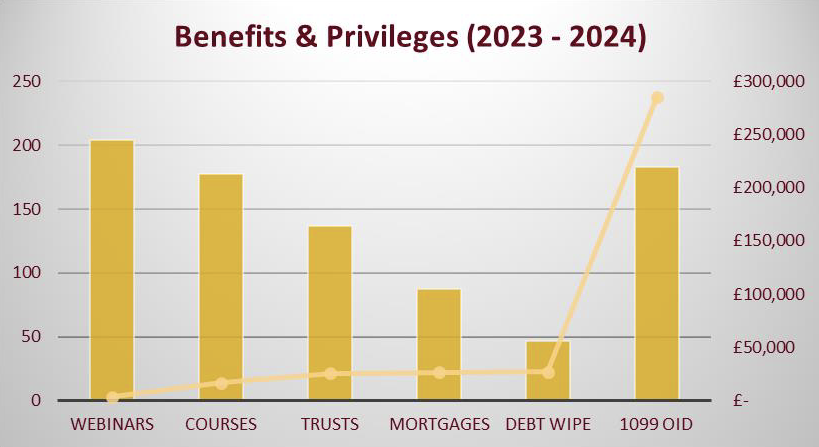

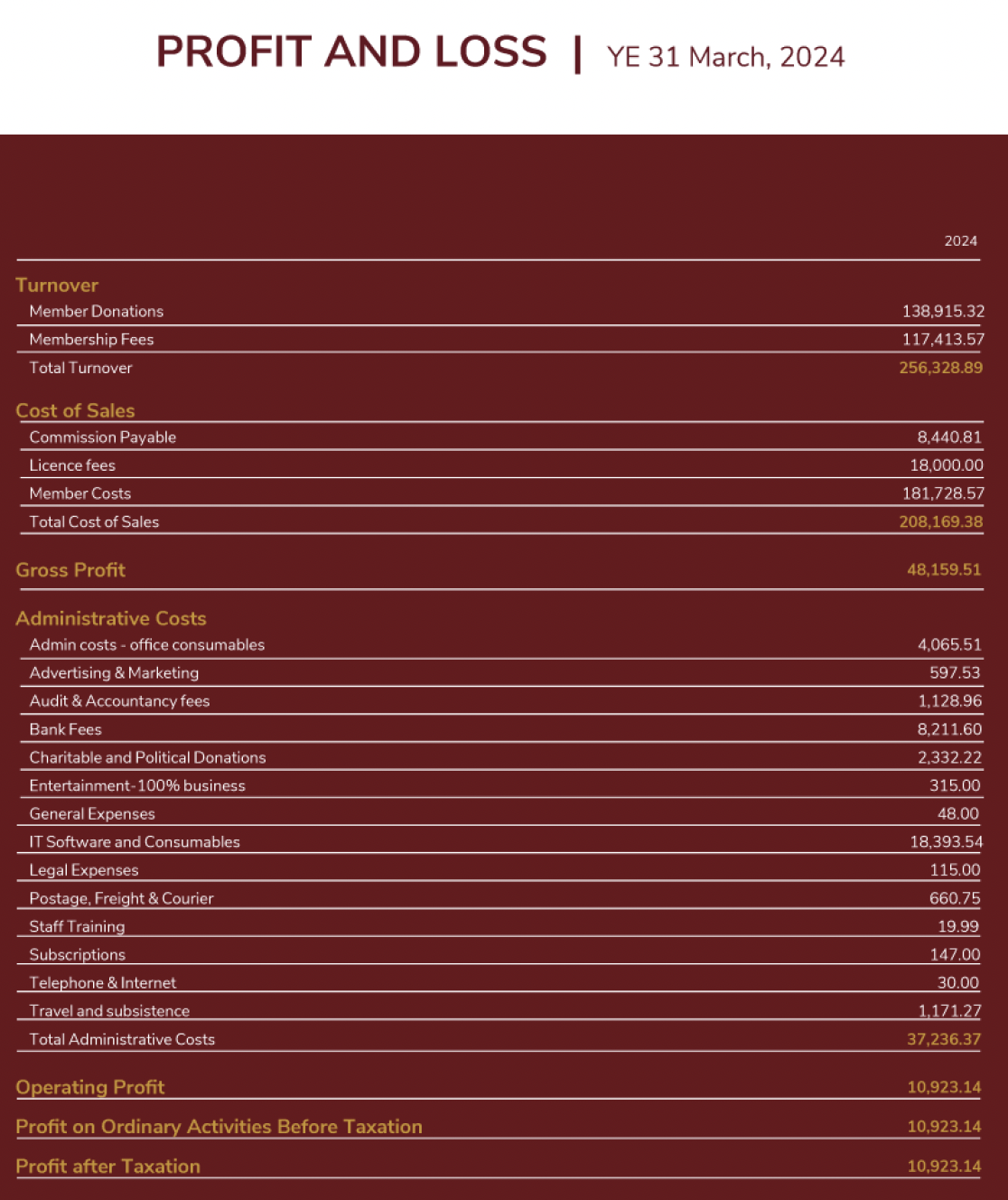

While the 2024 AGM presentation omitted the exact number of claims, it did reveal the group’s revenue from the scheme:

Based on their fee structure, this revenue implies they successfully defrauded the IRS of around $1m during the 2023-24 period.13

This number is actually surprisingly low if we check it against other claims by Empower the People. If people really were claiming refund cheques for house purchases14, the annual number would be significantly higher than $1m. Similarly, if Simone Marshall (co-founder of Empower the People) was correct when she said in this 2024 interview15 that they’d received a $536,000 cheque the previous week, then annual refunds would greatly exceed $1m.

We can’t explain that discrepency.16

Who are Empower the People?

Empower the People’s public website and videos are strangely vague about what exactly they do:

They sometimes claim to be charitable, but they are not registered with the Charity Commission. That can be a criminal offence.

There is a linked organisation, “You and Your Cash“. The relationship between Empower the People and You and Your Cash is not clear to us; in the interests of clarity we will refer only to Empower the People throughout this report. Both are unincorporated associations.17 There are a number of related companies which all appear to be dormant.

The reality is that Simon Goldberg (who sometimes calls himself “The Spaniard”) and Empower the People are part of what they call the “truth movement”, and most outside observers call the “sovereign citizen” movement.18 Sovereign citizens claim to believe19 that the legal and financial system is a conspiracy, and that by using the right documents or forms of words, a person can exempt themselves from laws, eliminate debt and create money out of nothing (often by claiming tax refunds for tax that wasn’t paid).

These “pseudolaw⚠️” theories originated in the US but are now increasingly common here. These claims have no legal foundation, and as far as we’re aware, they’ve failed every time they’ve reached a court in the UK, the US, Canada or Australia (the countries where sovereign citizens are most prevalent). There is a magisterial analysis of sovereign citizen legal positions in the Canadian judgment Meads v Meads.20 We have reported on one of the most financially successful sovereign citizens, Iain Clifford Stamp.

Goldberg is unusual for a sovereign citizen in that the true nature of his beliefs, and the services he sells to members/clients, is not readily apparent. He went as far as denying to us that he was a sovereign citizen. But in this video, no longer online, he is much more candid:

Goldberg says:

- He’s a “sovereign movement” (at 33:21)

- Everyone has a “straw man” – the sovereign citizen belief that everyone is attached to a corporate legal entity (at 25:41 and 53:07)

- Governments guarantee everyone’s debt (at 29:25)

- Judges are bankers (at 27:26) – because “they sit on the bench, which is an archaic word for “bank”

- Birth certificates are a “financial bond” (at 43:58)

- The Cestui Que Vie Act 170721 means that everyone is the beneficiary of a hidden trust (at 52:23).

We also obtained a copy of this presentation which sets out similar views:

Goldberg told us the presentation does not reflect his views and was used in a session to “debunk pseudo‑legal theories circulating online.”. But it is completely consistent with the views Goldberg himself expounds in the video above. The 1099-OID reclaim scheme webinars are full of sovereign citizen tropes, including that that everyday banking operates under “the law of the sea” (admiralty law).

As with many fringe political movements, the sovereign citizen movement is fragmented, with different groups often feuding with each other. Goldberg and Stamp have a particular animus, and both have published numerous articles and videos saying the other is fraudulent.22

The private prosecution

Salim Fadhley presents a YouTube channel exposing conspiracy theories.

In Spring 2025, Fadhley published a series of videos criticising Goldberg. Here the first of the videos23 – Fadhley refers to “The Spaniard”, which is the name Goldberg often uses online:

if you have time, we would recommend watching this video and judging the tone and content for yourself before reading the rest of this section of our report.

Goldberg subsequently reported Fadhley to the police for harassment, and then commenced a private criminal prosecution against Fadhley and two other individuals. Goldberg himself is the private prosecutor, instructing a reputable barrister – Gary Summers of 9BR Chambers – to act for him. Goldberg crowdsourced donations to pay the legal fees.

Chelmsford Magistrates’ Court granted the summonses on 25 September 2025, and the barrister’s chambers published a press release. This goes much further than merely announcing the fact of the summonses, and states as fact that there was a “campaign of online harassment” and that the defendants “engaged in a pattern of defamatory, abusive, and racially charged communications across multiple platforms”. It adds that:

Despite opportunities for constructive engagement, the three individuals chose instead to continue to weaponize social media, targeting EtP’s trustees, members, and partners with falsehoods and inflammatory content which were not expressions of free speech but calculated efforts to harass, intimidate, defame, and destabilise.

We infer that this was drafted by Goldberg and/or Empower the People, not the barrister.

The prosecution is currently adjourned pending determination by the Crown Prosecution Service of whether to take it over. The next hearing is listed for 20 April 2026.

Given the contempt of court rules, we will not express any view on the harassment allegations. It is, however, our view that – on the basis of the evidence presented in this report – it is not in the public interest for Goldberg to be a private prosecutor. We will, therefore, be asking the CPS to take over the prosecution, and discontinue it if it is not in the public interest.

(We understand that Goldberg is also crowdsourcing a private prosecution of Iain Stamp. Whatever our views of Stamp, in our view it cannot be in the public interest for Goldberg to prosecute him.)

Before commencing the prosecution, Goldberg instructed a law firm, Artington Legal, to send this “cease and desist” letter to Fadhley:

In our view this was an improper letter for a solicitor to send to an unrepresented individual:

- Meritless threats: It states that Fadhley faces potential prosecution for breaches of GDPR by “obtaining or disclosing personal data without consent”. Obtaining personal data is not, in itself, a breach of GDPR. Furthermore, there is no suggestion in the letter that Fadhley actually disclosed personal data at all. This threat of prosecution for GDPR breaches appears meritless and contrary to the SRA guidance on SLAPPs.

- Ignoring journalistic exemptions: The letter entirely disregards the significant exceptions to GDPR that apply when processing is for journalistic purposes and the publisher reasonably believes it is in the public interest. The ICO expressly recognises that journalism is not limited to traditional media and applies to independent YouTubers.

- Unparticularised claims: The letter makes broad, completely unparticularised allegations of defamation, which is again contrary to the SRA’s warning notices on abusive litigation and SLAPPs. The letter doesn’t even attempt to say what statements are being complained of, much less why they are defamatory.

- Misrepresenting civil procedure: The letter concludes: “Failure to respond or comply will be treated as a refusal to remedy your breaches, and our client will take the necessary steps to protect their rights and interests without further notice to you”. This statement is untrue. A solicitor knows that their client cannot simply commence civil court action “without further notice”. The Civil Procedure Rules require pre-action letters to be sent in a specific format, which this letter does not follow.

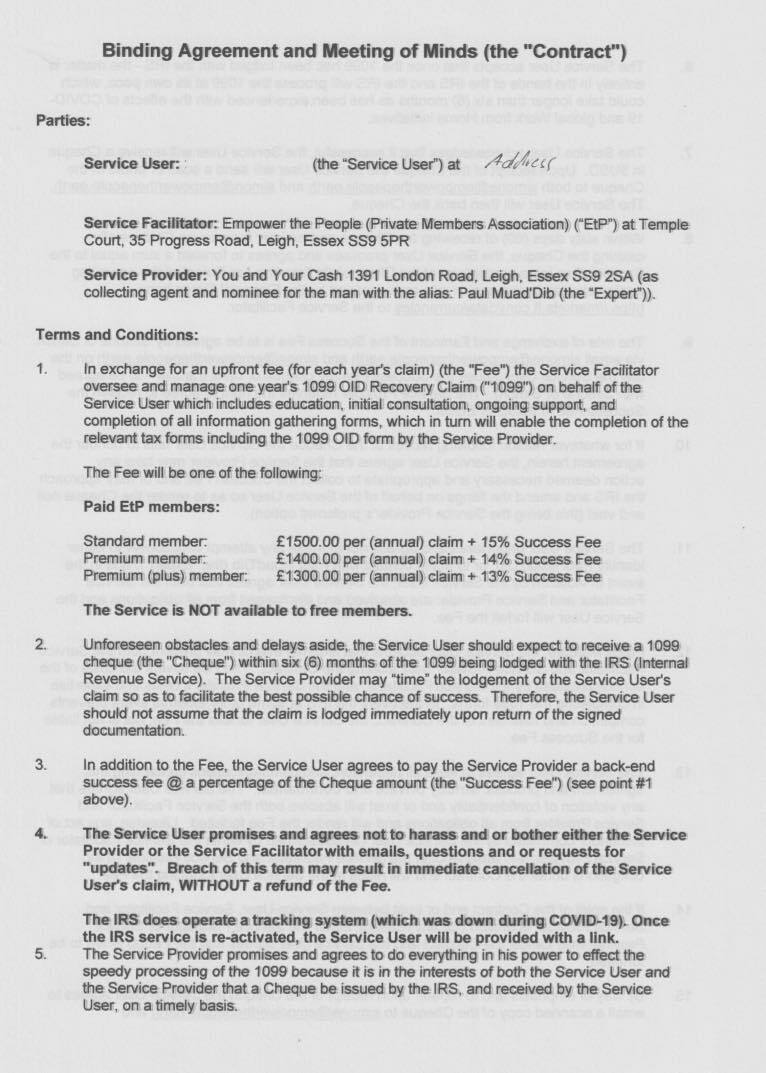

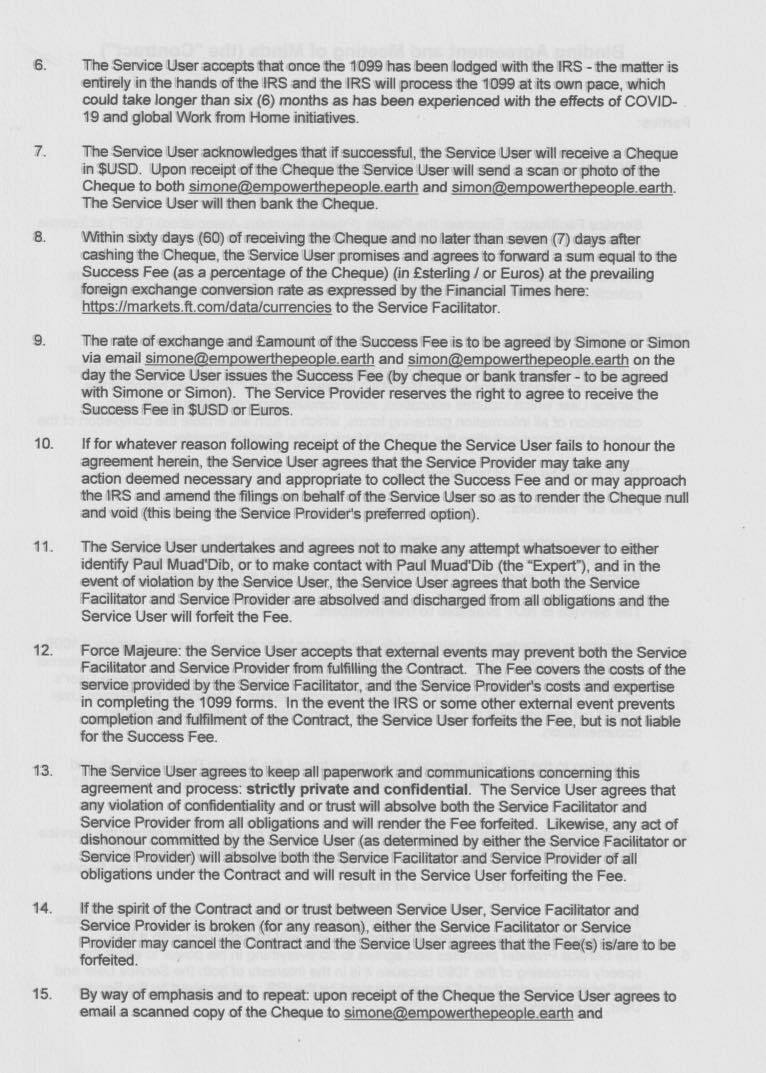

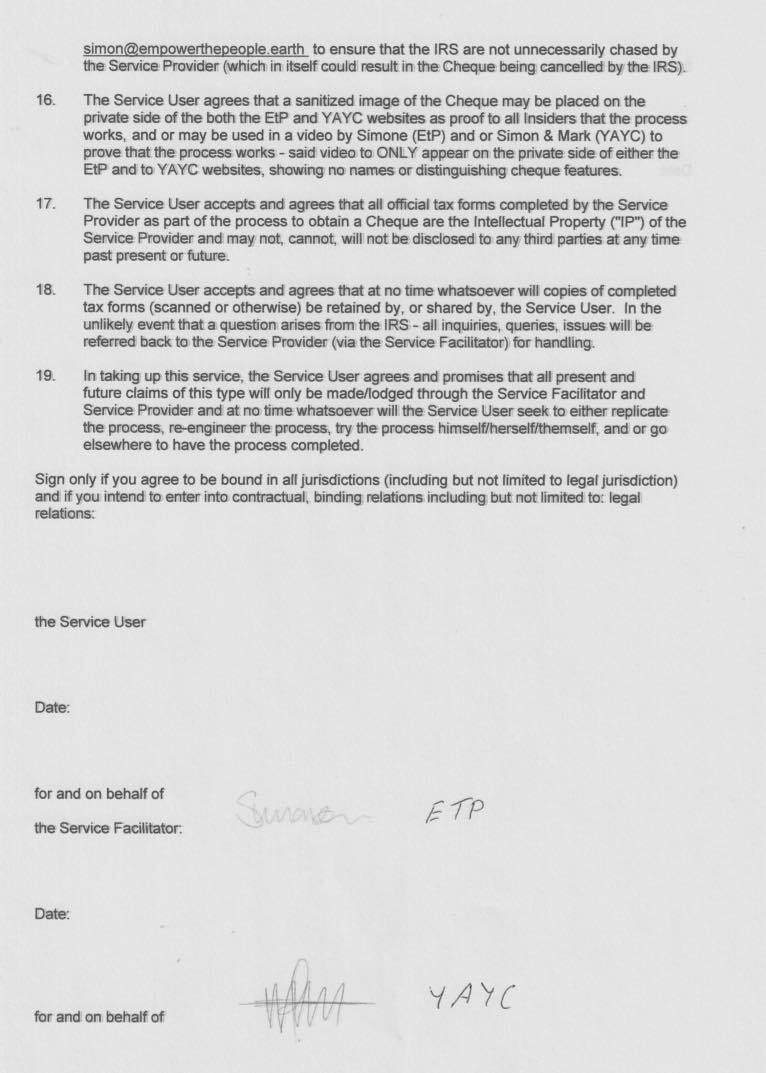

The evidence for the 1099-OID fraud

This report is based on extensive documentation and video evidence provided by multiple independent sources.

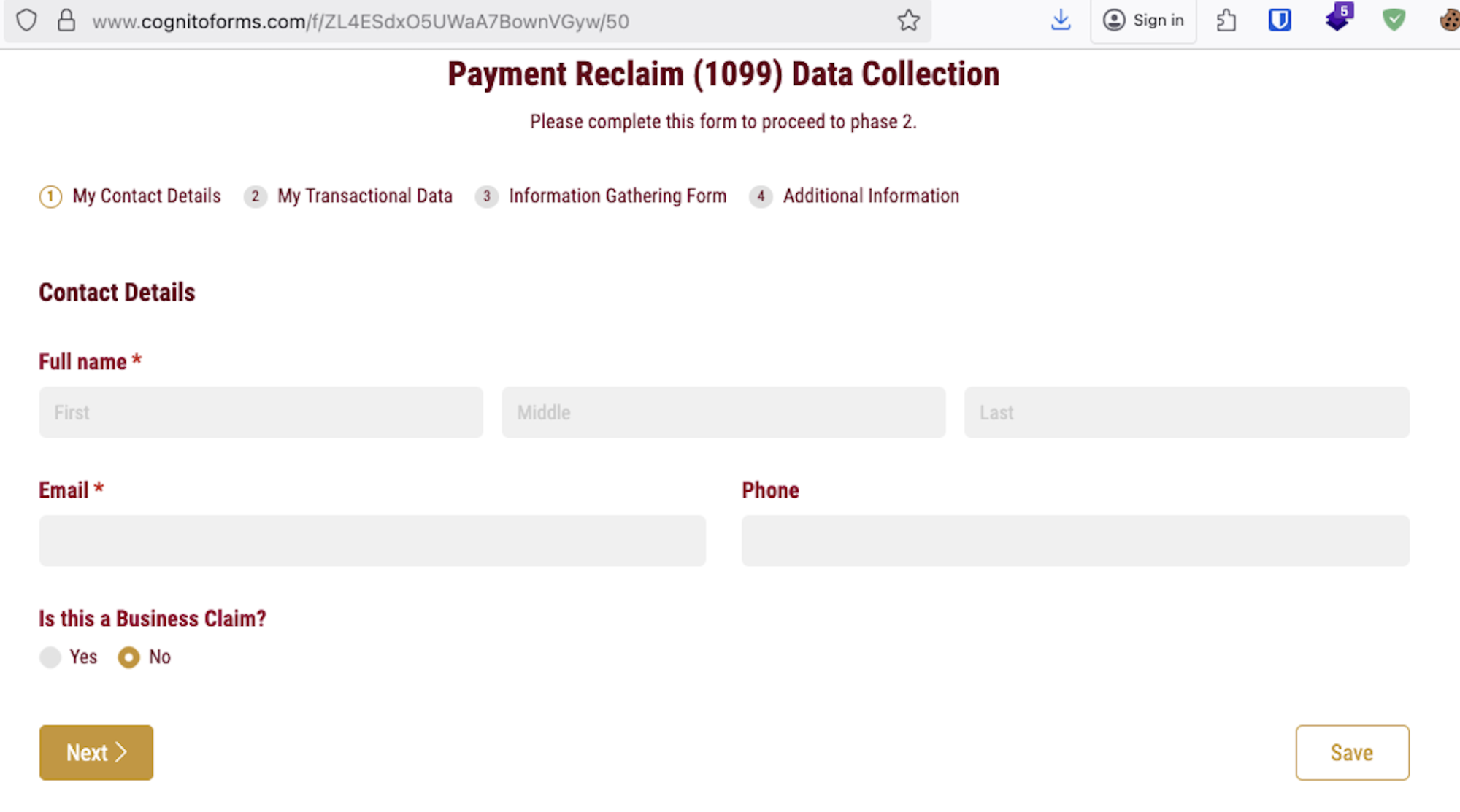

The mechanics of the entire reclaim process are set out in detail in Empower the People’s “Standard Operating Procedure” document (which we obtained from two separate sources):

Clients participating in the scheme sign up online:

And are then required to sign this contract:

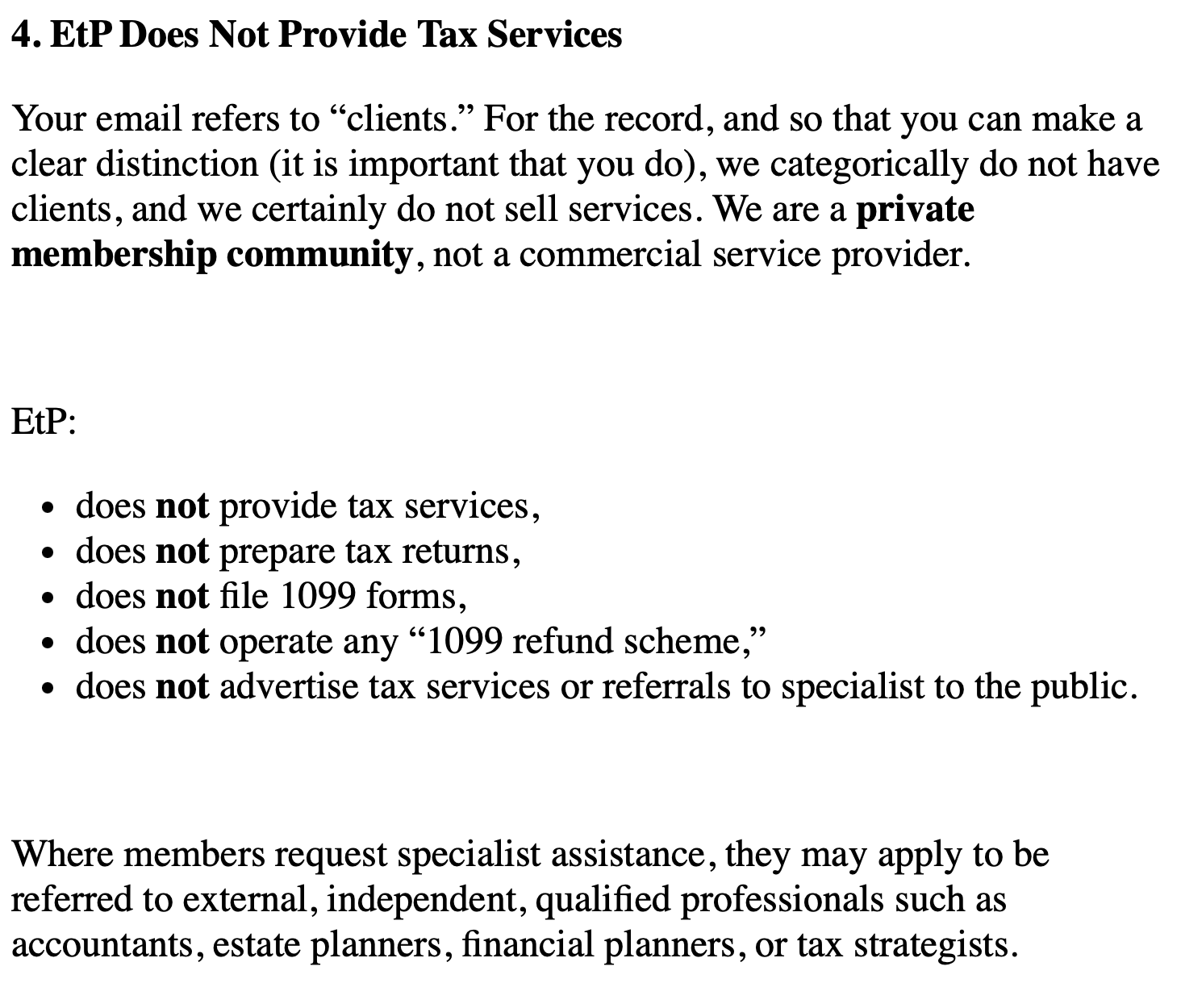

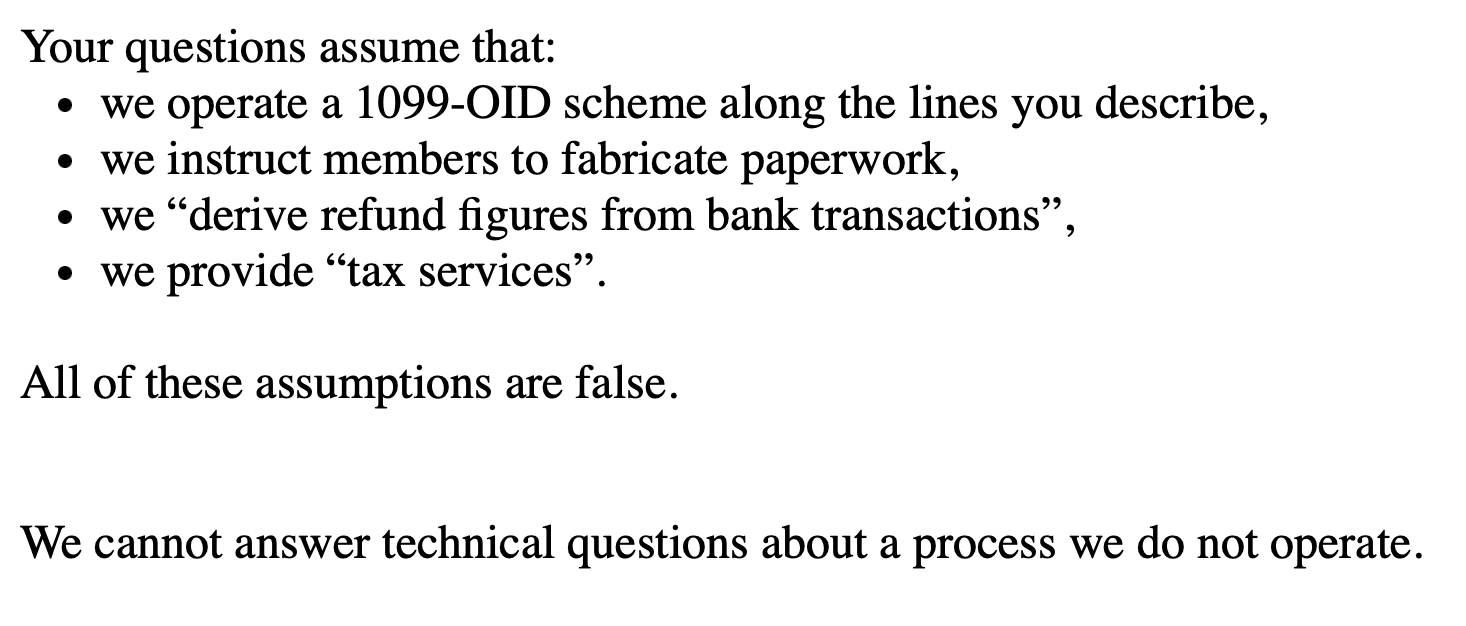

We are always meticulous before publishing allegations of fraud, and we presented our documentary evidence to Goldberg well in advance of publication. His response was not just to deny committing fraud – he outright denied that Empower the People provided any 1099-OID services at all:

And:

He even went so far as to claim the “Standard Operating Procedures” manual was fabricated as some kind of decoy:

All of this is a lie.

Here is a promotional flyer for an Empower the People webinar in August 2022, explicitly advertising a 1099-OID scheme:

And here is a complete recording of that webinar, in which Goldberg details exactly how his organisation runs its 1099-OID operation:24

We also obtained a recording of another, shorter, webinar, we believe from Spring 2023, covering much of the same ground:25

The video snippets interspersed throughout this report are drawn directly from these two recordings. Both webinars use this Powerpoint slide deck – the author in the metadata is “Simone Marshall”, co-founder of Empower the People.26

We can go back a little and see how the operation was set up. Here is Goldberg, at a members’ meeting in 2022, explaining that they’ve hired someone to operationalise the fraud by hiring “Ambia”, who they describe as a “1099 expert” because she has “undergone the 1099 process with Simon [Goldberg], and is very confident in the process and how to do it. She will be taking on that process when we roll that product… that benefit out, which is very imminent”:

And we can jump forward to see some of the claims made more recently. Here’s an excerpt from an interview with Simone Marshall (co-founder of Empower the People) in 2024.27. She discusses how Empower the People’s “1099 service” is much more effective than the service provided by their rival, Ian Stamp/Matrix Freedom:

“The only person in the UK that is successfully doing this is Spaniard [i.e. Goldberg]. He’s been doing it for three years now. Last week we had a cheque for $536,000, alright? So it works. Simon wouldn’t do stuff if it doesn’t work or if it’s going to hurt somebody. It’s all about reputation.”

(We are sceptical of the claim she received a cheque for $536,000. That seems much larger than the other indications of the scale of the operation.)

There is little reference to the 1099-OID scheme on the public internet, but there are traces – for example on the “You and Your cash” affiliate page28 it says:

1099 OID Essentials is not included, but 1099 OID Claims are – see the 1099 Session on Jedii Interactive for more details.

We wrote to Goldberg that he had lied to us in his initial written response. We have not received a reply.

Have Goldberg and his team committed fraud?

We believe this report demonstrates there is sufficient evidence for a criminal investigation of Empower the People and, if supported by that investigation, a prosecution.

The IRS aggressively prosecutes promoters of 1099-OID schemes for tax fraud, and sometimes prosecutes scheme participators (and anyone who signs a US tax form they haven’t read is in a very precarious legal position). So it seems reasonably clear that Goldberg and his colleagues are at risk of a US federal prosecution.

However, given that the participants, promoters, and evidence are overwhelmingly based in the UK, this may be a case where a UK prosecution of the promoters is more appropriate.29

Here is how the Crown Prosecution Service summarises the offence of fraud by false representation:30

The Empower the People scheme involves a series of blatant false representations: that the client’s ordinary consumer spending was “original issue discount”; that a large amount of tax was withheld when in fact none was; and that a tax refund was due when the IRS explicitly states it is not.

The scheme intends to make a gain for Empower the People’s clients (through the refunds) and for Empower the People itself (through the upfront and back-end fees it charges). It is therefore defrauding both the IRS and Empower the People’s own clients.31

The crucial legal question is whether those involved were “dishonest.” Under English law, this means asking whether their conduct was dishonest by the standards of ordinary decent people (regardless of whether the individuals themselves believed at the time that they were being dishonest).32

The leading textbook of criminal law and practice, Archbold, states:

“In most cases the jury will need no further direction than the short two-limb test in Barton “(a) what was the defendant’s actual state of knowledge or belief as to the facts and (b) was his conduct dishonest by the standards of ordinary decent people?”

In our view it is highly likely that Goldberg and his team knew full well that the IRS views 1099-OID schemes as illegitimate. We base this on the following five points:

1. Basic research reveals the fraud

As noted above, the IRS has included 1099-schemes in its “dirty dozen” list of tax scams, starting in 2009 and continuing to the most recent list in 2025. A simple Google search for “1099-OID scheme” reveals many websites explaining the fraud, including a Wikipedia page and a report of a successful IRS prosecution of a scheme looking almost identical to Goldberg’s scheme. It strains credulity to believe that Goldberg and his team did not see any of this, particularly after Salim Fadhley publicly accused him of fraud.

2. A massive rejection rate

Goldberg says their “success rate” is 45 to 50%33. No legitimate adviser sees half their tax forms rejected. This alone should have put him on notice that the IRS did not accept his legal positions.

Furthermore, Goldberg admits they have had filings formally rejected as “frivolous”.34. He gives the impression this is a minor administrative hurdle, but a basic Google search would have revealed that it is serious for a filing to be rejected as frivolous. Indeed that same Google search would have revealed an IRS notice which specifically describes Goldberg’s own scheme as frivolous, and would have revealed recent prosecutions for essentially the same scheme.

To explain away this high failure rate, Goldberg invented a story blaming rogue IRS staff for throwing applications in the bin to reduce their workload:35

OK, but someone in their bloody wisdom decided that, well, I’ve got all this backlog of paperwork where people have been working from home or they’ve been off sick or they’ve decided to jack it in. And in fact, a lot of people that were in the US that were from other countries were sent home. So a load of cheap workers left, which left the IRS short on staff, created a backlog. And so what did someone do? What’s the easiest way to get rid of a paper backlog, do you reckon? Well, let me tell you what some bright spark decided to do was bin all the paperwork over at the IRS. I know it sounds ridiculous, I know it sounds hard to believe, but a member of staff actually trashed a whole load of paperwork in order to get rid of it. I guess that’s one way of clearing a backlog but anyhow they were then found out. There was an audit conducted on the IRS – I think it was by the Fed – and they discovered that this had happened and it all blew up and was reported in the Washington Post.

3. Empower the People deliberately stagger their form submissions to prevent detection

Goldberg explicitly states that Empower the People does not submit all client forms at once. They stagger them so that the authorities do not notice what they are doing:

“It goes by courier to the IRS to make sure it doesn’t get lost in the bloody post, all right. Now from the moment it’s been couriered – because we have to time this, we don’t send them reams of stuff and hundreds of cases all at once because then it’s bloody obvious what’s going on. We don’t want it to be obvious what’s going on. We want these things to slip in with what the elite are doing, and what the nobles are doing, and what the bankers are doing.”

And:36

“So the IRS are on the lookout for people that are processing these claims because we’re not supposed to, we’re not part of that elite group. We’re not part of their club. So they don’t necessarily know everyone that’s not part of the club, right? So they’re on the lookout.”

This strongly implies a consciousness of guilt – an understanding that the IRS would reject the refunds if they understood what was going on.

4. Empower the People ensure their clients never see the tax forms submitted in their name

The clients don’t ever see what’s written on the tax forms that bear their signature:37

“Then we’re going to need certainly digital files, so scans of the passport to be sent over through [their admin assistant], through us to the expert38 so that the expert can create the forms for you and complete the forms for you

And you will be provided with the signature pages only because the actual mechanism that has been formulated by the expert – it is his intellectual property.”

People are signing US tax forms, under penalty of perjury, without knowing what they contain. The IRS says “never sign a blank tax form“, but that is exactly what Empower the People requires. British citizens are signing US federal tax forms, under penalty of perjury, without knowing what they contain.

We’ve never heard a tax adviser claim that the way they complete simple tax forms is valuable intellectual property. We expect the reality is more sinister: if the clients saw the completed 1040-NR and 1099-OID forms, they might immediately see that they were committing perjury. They would see a form falsely claiming that a UK bank39 withheld thousands of dollars in US federal income tax, which is obviously untrue (and Goldberg at no point even mentions withholding tax to his clients). By only providing the signature pages, the “expert” ensures the client remains entirely ignorant of the specific lies being submitted to the US government in their name.

5. Internal fears of IRS scrutiny

A source provided us with an internal chat log between Empower the People staff during their 2025 AGM, in which EtP’s “paralegal” said:

“Unfortunately, arseholes like Stamp and now that Salim guy have most probably raised the bar of scrutiny at the IRS.”

Conclusion

Even if Goldberg and his colleagues began as true believers in sovereign citizen theories, a jury could well conclude that, as time went on, they must have realised that their core claims were untrue. If so, we expect most ordinary decent people would say that their behaviour was dishonest. Ultimately that is something a jury would have to decide.

What else does Empower the People do?

While the 1099-OID scheme targets the US government, Empower the People also runs a sprawling pseudo-legal operation targeting UK institutions, local authorities, and consumers. Here’s their description of upcoming projects at a 2022 meeting:

“1099 reclaims” is the US tax fraud discussed in this report (and which Goldberg denied to us that he operates). The others are various sovereign citizen-style pseudo-legal services which Empower the People sell to their members (for a fee).

Most of their claims are now hidden behind members-only logins, but some are still available, for example:

” If you know what you’re doing, and if you understand why it works, and your true relationship to the SYSTEM and in particular the CORPORATE STATE, then “yes”, you can clear debts using nothing more than a signature! “

The explanation for why this works is incoherent:

A source provided us with a complete set of the documents which Empower the People use to provide these services. This includes standard-form templates as well as drafted client letters. We will not be publishing all the documents,40 but a few examples show how the operation is both dangerous and absurd.

This is Empower the People’s “acceptance for value” template. It purports to discharge debts by “accepting” a bill as a money order and appointing the creditor as “fiduciary trustee” to set off the account. This is a standard sovereign citizen approach, and it is legally meaningless.

This is a template document intended to nullify a Transport for London penalty. It relies on an incomprehensible claim that the then-Secretary of State for Transport, Grant Shapps, was appointed by Empower the People under a power of attorney (similar documents are discussed here):

Much of Empower the People’s activity involves charging adherents for pseudo-legal documents that supposedly will eliminate mortgage debt. In this arena, they’re competing with Iain Stamp. Like Stamp’s operation, the documents are an incoherent mixture of legal misunderstandings and conspiracy theories, none of which are recognised by English law.

A slight variation in the Empower the People documents is that the correspondence is directed to the Land Registry rather than to the client’s bank. Here’s an example:

When that correspondence is (inevitably and correctly) ignored by the Land Registry, Empower the People send further rounds of correspondence, and eventually (after ten letters) send a final letter claiming that the failure to respond gives rise to a massive financial penalty. In this example they claimed the Chief Executive of the Land Registry had, by ignoring their correspondence, assented to pay a penalty of £39m:41

This is nonsense. It is a fundamental principle of English law that you cannot create a contract where another party’s silence is deemed acceptance. We are unaware of any court in England, or indeed in the English speaking world, accepting arguments like this.42

These activities present a severe risk to consumers, who may be fooled into paying steep fees for documents that have zero legal effect. Worse, by following this “advice,” clients may end up defaulting on their mortgages and losing their homes.

The Financial Conduct Authority published a notice in 2022 warning consumers from dealing with people like Empower the People. The FCA said that they believed these services constituted “claims management services” requiring regulatory authorisation. The FCA’s prosecution of Goldberg’s rival, Iain Stamp, states the FCA also believes these activities breach the prohibition on unauthorised debt counselling⚠️, mortgage advice⚠️ and financial promotions⚠️. The regulatory experts we spoke to agree with this assessment.

These regulatory breaches may amount to a criminal offence.

The FCA told us:

“We can’t comment on individuals.

We have warned consumers about false claims that they can avoid having to pay their mortgage, taxes or other debt.

We would urge any consumers who are struggling to speak to their lender and ask for support.”

Failure to pay UK tax

As well as facilitating US tax fraud for its members, Empower the People appears to be systematically failing to pay its own UK taxes.

Here is Empower the People’s accounts for 2024, published at their AGM:

As an unincorporated association carrying on a trade, Empower the People is subject to corporation tax – but the accounts from this and previous years suggest no corporation tax has ever been paid.43

The payments members make to join the 1099-OID scheme are described as “donations” but obviously are not – they are fixed payments for a specific service.44 That, and the fact the group’s revenue is above the £90,000 registration threshold, means the payments are subject to VAT.45 Empower the People should be registered for VAT, and accounting to HMRC for VAT on the fees it receives for the services it provides. We believe it does not.

We asked Simon Goldberg why Empower the People appeared to pay no VAT or corporation tax. He did not respond.

It may be relevant that, in this video from 2013, Goldberg claims that tax is voluntary:

Goldberg’s justification is that tax legislation applies to “person” but, “according to the Acts of Parliament and the Interpretation Act, the definition of the word ‘person’ is an artificial entity, corporate soul or legal fiction”. It’s an obviously false claim, rebutted by one look at the legislation, but US sovereign citizens have been making similar arguments, and failing in court, for decades.46

Where did Goldberg get these ideas?

Simone Mitchell, co-founder of Empower the People was recently interviewed on a podcast. She told the host that Goldberg “studied under Winston Shrout”.47 And Goldberg himself said at a meeting that “having woken up, [he] went to some Winston Shrout seminars”:

Winston Shrout is one of the most well-known sovereign citizens in the US48 – and a tax fraud promoter. Shrout was convicted of tax fraud in 2017, sentenced to ten years in prison, went on the run in March 2019, and was caught and jailed in November 2019.

Failure to safeguard its members personal information

Empower the People is taking advantage of vulnerable and naive people by selling them schemes that are in some cases just ineffective, and in some cases criminal. There’s an additional problem: a complete failure to safeguard their data.

Neither Empower the People nor You and Your Cash are registered with the Information Commissioner. Failure to register and pay the ICO fee is a breach of UK GDPR.

The breach is more than technical. The day after we published this article we were contacted by several people who had noticed that Empower the People stored client/members’ documents on their website without any security.49 Anyone could go to a standard WordPress API endpoint🔒 and see a complete list of all the files on the website, including pseudo-legal documents drafted for their members (for example claiming millions of pounds from the Land Registry).

We discussed this with information security specialists who told us that this kind of vulnerability is routinely discovered by automated scanning tools that continuously crawl the internet looking for these kinds of misconfiguration. Criminal groups routinely use automated scanning tools to locate websites with exactly this type of misconfiguration and harvest exposed documents for identity theft, fraud, or resale. The specialists we spoke to said that vulnerabilities of this type are commonly discovered within days or weeks by automated scanners, and that it was therefore plausible that the documents had already been indexed or downloaded by third parties.

We reported the vulnerability to Empower the People the next day, 27 February. We didn’t receive a response, but soon after, they blocked direct access to the documents. However they failed to block access to the complete list of documents, including the names of many of their clients/members. We wrote to Empower the People again on 3 March reporting this; access to that list has now been secured. We didn’t receive a response, although it seems Empower the People has asked its members to write to us complaining about the data breach. Those complaints would be better directed at Empower the People.50

Before we knew about the vulnerability, we received a large number of Empower the People’s internal documents (perhaps obtained through this vulnerability, perhaps otherwise). We’re passing them all to the authorities but will not retain copies of any personal information.

Salim Fadhley video © Salim Fadhley and licensed under a Creative Commons licence.

Other images and videos © Empower the People and their other respective owners, and used here for the purposes of criticism and in the public interest.

Many thanks to B for initial research, K, P and C for their US tax expertise; P, C and M for additional research; C2 for UK regulatory insight; N for advice on the mutual trading exception; and Michael Gomulka and A for English criminal law advice. Thanks to J for invaluable comments on a late draft, and to Dr S for picking up errors on timestamps.

Tax barristers and fraud: how the Bar responded to our allegations

Rogue barristers are enabling a billion pound tax fraud – and the Bar won’t act

![DECLARATION of SOVEREIGNTY & DEED

of DISCRETIONARY REVOCABLE CONDITIONAL

TRUST and WITHDRAWAL of CONSENT to

MANDATORY TAXATION

I, [Name]

Currently of [address]

on this [Day] of [Month] [Year]

being of sound mind, DECLARE AND SAY as follows:

1. I, a sovereign man / woman resident in the United Kingdom consent to pay all taxes in

favour of Parliament, the Government of Britain and Northern Ireland, public authorities

and/or institutions, HMRC, the DVLA, local Council, corporate bodies and/or businesses,

and/or individuals acting as agents of HM Government (hereinafter jointly and severally

known as the “Primary Beneficiary”), in consideration of various taxes, fees, fines,

rents, duties, levies, demands or charges made upon me under various Finance Acts, laws

and/or regulations enacted, passed or issued by the Primary Beneficiary, and as trustee

will hold said payment(s) in whole or in part on discretionary, conditional, revocable

trust for the Primary Beneficiary until the last day of the financial year.](https://taxpolicy.org.uk/wp-content/uploads/2024/03/Screenshot-2024-03-15-at-17.50.27-640x545.png)

“No tax for genocide” – an anti-tax cult, and its false claim you can legally stop paying tax

The questions Richard Tice isn’t answering

Richard Tice’s property company failed to pay £120,000 in tax

Companies House flaw exposed five million directors and enabled company hijacking

Footnotes

An obvious point: Simon Goldberg is a fairly common name, and a search on the internet for Simon Goldberg finds people who are nothing to do with the Goldberg that is the subject of this article. ↩︎

This case illustrates a known problem with private prosecutions; the lack of any assurance that the private prosecutor is acting in the public interest. The Government closed a consultation on the subject last year, and it’s widely expected that the law will change in the next two years to introduce a mandatory code of practice, separate investigative and prosecutorial functions, a requirement for private prosecutors to meet the Director of Public Prosecutions’ (DPP) public interest test, and to introduce an accreditation system and regular inspections for private prosecutors. ↩︎

This and other video excerpts in this report are compiled from the webinars in the evidence section below. Here we have edited together different sections so as to clearly show what is proposed in one video, and added subtitles. The edit is consistent with the overall message, as is clear if you watch the whole of the webinars. ↩︎

We have not been able to verify if the images are genuine, but we expect that they are. Recent US prosecutions of people running these schemes (discussed below) show that the schemes can be extremely successful, at least in the short/medium term. And it would make little sense for EtP to continue to operate the scheme for four years if nobody ever received a cheque. So EtP’s claimed success rate of 50% may or may not be accurate, but we expect that their clients have received a material number of cheques (and the figures discussed below support that). ↩︎

This clip illustrates what a peculiar organisation Empower the People is: it starts with nonsensical claims into creating a “snowball” of free cash from IRS using an obvious fraud, then segues into detailed and rather sensible advice as to how to pay down your mortgage. ↩︎

Although it is possible that in the Goldberg case, a defendant could successfully argue that it is more appropriate to prosecute in the UK, given that is where the witnesses and evidence are. The offences that were extradited had more connection to the US, including the use of US bank accounts. ↩︎

See §10.27 of Circular 230. ↩︎

When a person prepares a tax return for someone else they are supposed to obtain a “preparer tax identification number“, add it to the return and sign the return, which is then signed by the taxpayer. Empower the People’s “expert” doesn’t do this. He is a “ghost preparer” – invisible to the IRS (there’s another excellent article on that subject here). ↩︎

A company issues securities with a face value of $10,000 to an investor. The securities are issued at a discount, so the investor pays $9,500. A year later, the securities redeem for $10,000. The company provides the investor with a 1099-OID form showing the company’s name and the $500 of “original issue discount” income (in box 1). The investor then includes this income in their US tax return.

If the investor is a UK resident then, in very rare cases, the company would be required to withhold US tax at 30% on the “original issue discount” of $500. So it withholds $150 and pays the investor $350. It gives the investor a 1099-OID form specifying the company’s name and (in box 4) the $150 of tax the company withheld.

It must be stressed that this is a highly unusual scenario. We spoke to three experienced US tax counsel, and none had ever seen “original issue discount” withholding applied to UK retail investors – box 4 is usually empty. That’s because in practice the withholding tax exemption for “portfolio interest” would almost always apply. The cases where that exemption wouldn’t apply – e.g. securities held by banks, bearer securities, securities where the interest is contingent on profits – are unlikely to be relevant to debt securities held by normal UK investors.

But in this unusual case, it would make sense for the UK retail investor to complete a US tax return and obtain a refund of the $150 of tax withheld. They obtain a US tax number from the US and complete a US tax return, using form 1040-NR, and file it together with the 1099-OID given to them by the issuer. The investor isn’t subject to US tax on the original issue discount income (because they’re not resident in the US) but they get a credit for the $150 on the 1099-OID. If the investor had no US taxable income at all, they’d receive a cash cheque for $150. ↩︎

Some recent examples: the cum-ex scandal, VAT carousel fraud and R&D tax credit fraud ↩︎

The withholding tax is in most reported fraud cases equal to the “discount” – that should ring alarm bells given the actual withholding tax rate is 30%, not 100%. And a further bell should ring because, when the issuer of a debt security gives a 1099-OID to an investor, they file an identical copy to the IRS – a modern tax system really should only issue refunds once withholding tax payments and 1099-OID forms have been received, and basic initial checks have been satisfied. ↩︎

It’s common in these frauds to file for retrospective reclaims. ↩︎

If we assume they processed 80 claims in 2024, then the total initial fees were 80 x £1,300 = £104k. The chart shows about £230k of income – if the additional £126k represents the 13% back-end fee then that implies around £1m of refunds were obtained, i.e. $1.3m. Of course it’s possible that there were more claims in 2024 than 2023, which would mean more of the £230k comes from the initial fee and less from the 13%, implying a lower level of refunds. We don’t know if that’s the case, so believe it’s fair to say “around $1m”. ↩︎

See 00:30:41 of the first webinar. ↩︎

There are, perhaps, three possibilities. First, our estimate could simply be wrong – the fees may not work our in the way we infer from Empower the People documents – and the refunds larger than our estimate above. Second, our estimate could be correct, and Goldberg/Marshall are exaggerating – the refunds are much less successful, or much smaller, than they suggest. Third, the refunds are much larger but the money is not all being booked in Empower the People’s accounts, for whatever reason. ↩︎

You and Your Cash claims to be a “private trust”, but probably isn’t. ↩︎

In 2010, the FBI said it regarded sovereign citizens as domestic terrorists – for the very good reason that people who claim laws don’t apply to them tend to attack public authorities, courts and police officers. Since then, it’s become common for people promoting sovereign citizen ideology to vehemently deny that they’re sovereign citizens. We should be clear that we don’t regard this group as terrorists, or indeed as physically dangerous in any way. The combination of sovereign citizen ideology and US gun rights means that the position in the US is much more dangerous than that in the UK. Here, whilst there have been cases of sovereign citizen violence, they have been much more limited. ↩︎

We say “claim to believe” because sovereign citizen “gurus” often make large amounts of money by selling sovereign citizen schemes, and it’s often not clear if they really believe what they say, or it’s just a scam. ↩︎

Yisroel Greenberg has written about UK adherents to these theories, from the perspective of a local government lawyer. The criminal barrister who tweets as @CrimeGirl has compiled a useful summary of UK caselaw. The Ministry of Justice recently sent an impressively complete FOIA response to someone asking about these theories. ↩︎

An archaic statute which is probably no longer in force, but at the time provided a practical solution for the families people lost at sea by deeming them to be dead after seven years. It appears at some point someone in the US confused the name of this Act with “cestui que trust” – an archaic term for beneficiary. This became a common sovereign citizen belief, and is used by fraudsters in the UK to sell fake car insurance. The Ministry of Justice has received dozens of Freedom of Information Act applications from people convinced “cestui que vie” trusts are real, and now refer people to the detailed response noted above. ↩︎

We would caution against relying on anything that either person (or their organisation) says. For example this article, which accuses Goldberg of US tax fraud, appears to be AI written and references to documents/sources that are not provided and may not exist. This article does not use anyone connected with Stamp as a source, and our article on Stamp does not use anyone connected with Goldberg as a source. ↩︎

Fadhley mentioned Goldberg in an earlier video, but only in passing. ↩︎

AI-generated transcript here, or here with time markings. We should add that we are not completely certain this is the exact webinar promoted by the flyer above – the time of year appears to match, but there could be an additional webinar around the same time which we have not yet obtained. ↩︎

AI-generated transcript here, or here with time markings. This video, unlike the previous one, shows images of participants during the Q&A at the end. We have blanked out the participants except for Goldberg, out of fairness to people who may in some cases be victims of a fraud. Note that the audio is very out of sync by about 45 seconds – we haven’t corrected this because we didn’t want to modify the file (beyond the redaction). ↩︎

Noting of course that metadata can easily be added, removed and altered by anyone at any time; it’s not evidence that the document is genuine (the preponderance of other evidence makes that clear beyond reasonable doubt) but is an indication that she prepared the slides. ↩︎

Full video here: excerpt taken from 00:43:16 ↩︎

We are linking to our archive of the page, because we anticipate it will be amended shortly. It was live on 26 February 2026. ↩︎

We expect the police/CPS would not prosecute the scheme participants. A case could be made that they are involved in a conspiracy to defraud and/or fraud by false representation, but establishing dishonesty for the retail participants would be much more difficult than for the promoters. ↩︎

There are other possible offences, for example conspiracy to defraud. ↩︎

The clients might not feel defrauded if they end up making money, but (based on Goldberg’s own figures) roughly half pay fees and never receive a refund; furthermore, those receiving a refund may eventually be required by the IRS to repay it with penalties. ↩︎

The subjective element of the test for dishonesty (see Ghosh (1982)) was removed by Ivey [2017] for civil cases, and that decision was confirmed to apply to criminal cases in Barton [2020]. The fact that a defendant might plead he or she was acting in line with what others were doing, and therefore did not believe it to be dishonest, is no longer relevant if the jury finds they knew what they were doing and it was objectively dishonest. ↩︎

See 00:28:09 of the second video. ↩︎

See the second video, 01:06:57 to 01:07:53, and 01:11:51 to 01:12:08 ↩︎

The Washington Post reference may be a complete misreading of this event – the IRS destroyed 30 million paper-filed information returns (1099s and W-2s filed by third-party companies, not personal tax returns) because their antiquated software was being taken offline for the 2021 tax season. It wouldn’t have impacted Goldberg’s 1099-OID claims. ↩︎

This is from the second webinar, cropping out the other participants (thus the low resolution). Note that the audio is very out of sync. ↩︎

This is at 53:23 of the first video ↩︎

That’s the anonymous person who calls himself “Paul Muad’ib” after the sci-fi character. ↩︎

Another possibility is that the form is completed in line with the sovereign citizen conspiracy theory that everyone has an “all caps name” which is a company, and their “all caps name” is stated as the issuer. That seems less likely; we’d hope the IRS’s systems would pick up if JANE SMITH LIMITED was a stated issuer on a 1099-OID. ↩︎

We are withholding the bulk of the documents because of the obvious concern that they could be adapted for use by other sovereign citizen groups, and we have no desire to add to the burden on the public authorities, courts, and businesses who have to deal with this nonsense. If any researchers or authorities would like a copy of the documents, please get in touch. ↩︎

In principle this kind of correspondence could amount to a criminal offence, such as fraud by false representation or blackmail. In practice it tends to just be binned. ↩︎

Although others have certainly tried to play games by pretending that someone can be forced to agree to pay penalties by magical contractual wording. ↩︎

In our view EtP is clearly carrying on a trade of providing services. The fact the services may be illegal does not prevent it from being taxable (and see also here). The “donations” are in our opinion taxable income, either because they are in reality payments for services, or under the rule in Falkirk Ice Rink. Many of the expenses won’t be deductible, particularly any which amount to the commission of an offence. The “mutual trading” exception is unlikely to apply because some members are being charged large fees to participate in the 1099-OID scheme, but (broadly speaking) they don’t get any enhanced rights to the association’s surplus. The very commercial nature of the fees charged for the services also feels unlike a normal mutual trading situation. ↩︎

The leading case on this point involves a Dutchman called Mr Tolsma, who played a barrel organ on a street corner and invited passers by to leave donations. The Dutch tax authorities claimed he had to account for VAT on these payments, because he was making a supply (or barrel organ music) to those passing by. The court disagreed; the passers-by heard the music whether or not they made a donation. There was no “necessary link” between the musical service and the payments to which it gave rise. There is a “necessary link” between Empower the People’s 1099-OID services and the “donations” they charge. ↩︎

Most illegal services are subject to VAT. ↩︎

Often relying, as Goldberg does in this video, on looking up words in an old US legal dictionary, and thinking that has force of law, and indeed overrides statute law. ↩︎

And in Cambodia – see the peculiar end of this very story, courtesy of Jack Adamović Davies. ↩︎

Their website is run on WordPress, a standard platform for hosting websites, with a “plugin” that enabled pages for members to be secured. However the plugin did not secure the members’ documents, which anybody could access, and the API was not locked down. ↩︎

The exposure may constitute a breach of the UK GDPR. Personal data must be processed “in a manner that ensures appropriate security”, including protection against unauthorised access (Article 5(1)(f) and Article 32 UK GDPR). Leaving members’ documents accessible through a public API for an extended period strongly suggests that appropriate technical and organisational measures were not in place. In addition, organisations that become aware of a personal-data breach must notify the Information Commissioner’s Office within 72 hours if the breach is likely to pose a risk to individuals (Article 33). Where the risk is high – for example because personal documents have been exposed – the affected individuals must also be informed (Article 34). Failure to implement adequate security measures or to notify the ICO of a notifiable breach can lead to regulatory investigation, enforcement action, and potentially substantial financial penalties. ↩︎

Leave a Reply to Dan Neidle Cancel reply