It wasn’t mentioned in the Chancellor’s speech, but the Spring Statement papers contain a major suite of anti-tax avoidance proposals, probably the toughest ever introduced. If enacted this will, in effect, criminalise the tax avoidance industry. We welcome it.

There is a mini-industry of creating tax avoidance schemes which have no prospect of success. We don’t believe a single one has succeeded in court in the last twenty years. That hasn’t stopped promoters from collecting millions in fees. The long series of new laws introduced to stop them have been ignored.

The Government is getting serious – for the first time there is a proposal to criminalise the promoters’ activity. If the Government follows through, and HMRC uses these new powers, we could all be billions of pounds better off.

I was less than flattering about the Autumn Budget, particularly the national insurance increase, farming inheritance tax change, and general failure to include any tax reform measures. However the new anti-avoidance proposals are excellent, and should be welcomed by everyone who wishes to see the tax avoidance industry ended.

I’ve summarised the proposals below, with my initial thoughts. We’ll respond to the consultation when we’ve been through the proposals in more detail. If you have additional thoughts, do please get in touch.

Criminalising doomed schemes

HMRC has a power to issue a “stop notice” to the promoter of a tax scheme, making further promotion of that tax scheme a criminal offence.1 The problem is that HMRC will issue a stop notice to one entity, and the promoter will simply move its business to another.2

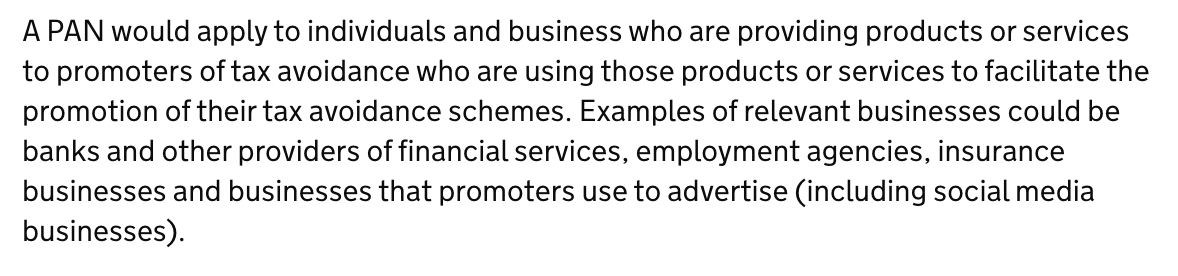

The Government is proposing a “universal stop notice“. This would empower HMRC to issue a notice specifying a scheme; no person could then promote or enable that or any similar scheme. Anyone who did would commit a criminal offence, as would any person controlling or influencing them.

The proposals go further. The Government would be able to issue a “promoter action notice” to third parties who facilitate the scheme:

This is important; promoters have, for some time, been using offshore entities to make it harder for HMRC to take action against them. However any business targeting UK clients is inevitably going to rely on banks, social media etc in the UK – so it makes sense to enable HMRC to target.

I would, however, be a little concerned about overreach (and I sense the Government is too). I would personally suggest making these powers apply only where either the individual promoter or their entity is outside the UK. This should be a fallback option, not the first line of attack.

Criminalising breaches of DOTAS

One of HMRC’s most important weapons against tax avoidance is DOTAS – the rules requiring promoters of tax avoidance schemes to disclose the schemes to HMRC. That has two consequences:

- HMRC gets early warning of schemes, and can close them down.

- Anyone looking to use the scheme receives warning that it is classed as an avoidance scheme (because they have to put a DOTAS reference number on their tax return).

DOTAS is therefore a serious threat to promoters’ business, and promoters deal with this by simply ignoring it (often based upon frivolous legal arguments, typically followed by promoters simply letting their firms fail).

I believe that, of the many tax avoidance schemes we’ve reported on, not one was disclosed under DOTAS. They all should have been.

We have therefore called for failure to comply with DOTAS to become a criminal offence for the individuals responsible, with strong protections to prevent innocent mistakes being penalised. So I’m delighted to see that is what the consultation paper proposes (with a “reasonable excuse” defence, so that innocent people aren’t caught).

There isn’t much detail in the document (that’s typical at this stage). But we will be responding to the consultation proposing that the criminal offence apply to the company’s directors and shadow directors.

We will also ask for a clear statement that the criminal offence will never be used against normal advisers or commercial parties who made an innocent mistake. One way to differentiate the bad actors from normal advisers would be to make the criminal offence only apply where a scheme is mass-marketed, or there is a premium fee (i.e. reflecting more than an adviser’s usual hourly rate). Other approaches could be considered.

Expanding DOTAS

The Government is proposing a new DOTAS hallmark to more clearly target disguised remuneration schemes.

These schemes are rampant – often pushing people on modest or low earnings into complex avoidance schemes (which aren’t properly explained and are sometimes hidden). The result: loss of tax for HMRC, and often large liabilities for the (often unwitting) scheme users.

It’s our view that all the disguised remuneration schemes are already covered by DOTAS, but perhaps the intention is to make it easier to deploy the new criminal offence against them?

Increasing DOTAS penalties

Another problem with DOTAS: the penalties are too low.

The standard penalties are currently £600 per day, or up to £1m. This is determined not by HMRC but by a tax tribunal. That delays the day of reckoning for promoters; by the time the tribunal hears the case, the fees have often been made, and cash extracted from the promoter’s business.

The consultation proposes allowing HMRC to charge a penalty, with a right of appeal to a tribunal. That is a sensible step to speed things up.

But there are other problems: even £1m is an insufficient deterrent when a promoter can make millions of pounds of fees in a few months. And promoters typically don’t stick around to pay penalties. So we would suggest:

- The penalty should be geared to the fees received by the promoter (say 200% of fees) or, where a promoter does not adequately disclose the fees received, such amount as is just and reasonable under the circumstances.

- A promoter’s directors/owners should always be joint and severally liable for the penalties. Right now it’s too easy for them to walk away from their company.3

New information powers

HMRC has extensive powers to require information from taxpayers using “information notices”. Normal taxpayers take information notices extremely seriously. Tax avoidance scheme promoters typically ignore them, and HMRC often struggles to impose penalties, not least because of the opaque ownership structures used by the promoters.

So the consultation proposes the creation of new information powers, backed up by criminal offences.

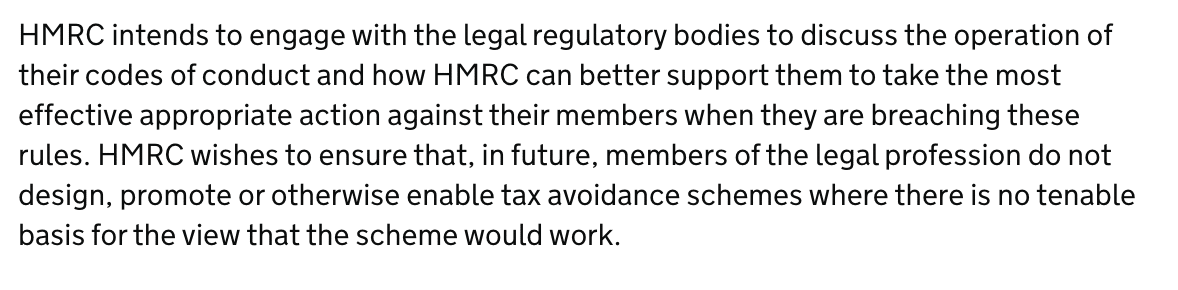

Targeting legal professionals

Many tax avoidance schemes are facilitated by a small number of legal professionals (almost exclusively barristers). We have published a series of examples.

The barristers provide opinions that the schemes are lawful, and DOTAS disclosure is not required. The courts almost always conclude the opposite. But the role of the barrister was not really to provide correct advice; it was to facilitate the scheme. The promoters can then claim “we have a KC opinion”. When the opinion turns out to be wrong4, the end-users of the scheme cannot sue the KC, because they weren’t the client – the promoter was. And the promoter has done just fine.5

The opinion serves two purposes. It greatly helps marketing the scheme. And it gives the promoters a defence against penalties or criminal prosecution – after all, they received legal advice. The advice itself will almost always be privileged – HMRC cannot see it.

This is, in our view, corrupt. Jolyon Maugham KC wrote about the problem eleven years ago; nothing has been done. Ideally the Bar Standards Board would act.

The consultation contains a series of somewhat tentative proposals. Likely the most impactful are:

- Enabling HMRC to publish the names of lawyers who design tax avoidance schemes.

- Waiving legal privilege where a tax avoidance scheme is marketed as being supported by a legal opinion.

It seems HMRC and the Government also share our view that the professional regulators need to be more effective:

What else is required?

The most important element is simply resources. If these new rules are enacted and just added to HMRC’s toolbox, they will be rarely used.

HMRC should create a specialist team whose only role is pursuing civil and criminal penalties against tax avoidance scheme promoters. It would sometimes accept referrals from others within HMRC, and sometimes act on its own initiative. It would be staffed by a mixture of tax specialists, investigators and white-collar crime lawyers.6

There are additional minor and costless measures HMRC should adopt.

- Currently, when tax avoidance schemes and their promoters are publicly named by HMRC for promoting a DOTAS scheme, this is only for twelve months. After that, their name is taken off the list (although at least one excellent website preserves the listing forever). The one year expiry date should be ended. UPDATE: thanks to the people who let me know this isn’t the whole story. Those named because of DOTAS are indeed only listed for twelve months. However Finance Act 2022 gave HMRC a new power to publish the names of promoters which isn’t dependent on DOTAS. There is no expiry date on these names – and in practice HMRC now always names under the Finance Act 2022 power.

- Particularly egregious schemes are often considered by the General Anti-Abuse Rule Advisory Panel. The GAAR panel publishes its opinions; but the taxpayers and firms involved are not named. They should be, either in all cases or in the cases where the GAAR panel finds against the taxpayer (which it has thusfar in every single case).

- HMRC could be empowered to publish the names of people it prosecutes, and the charges against them. Right now this is only announced in some cases (the precise policy isn’t clear).

Footnotes

“Stop notices” were a new power granted to HMRC in 2021, with the rules now in section 236A Finance Act 2014. The effect of a stop notice is that the recipient of the stop notice mustn’t promote the specified arrangements, or anything similar to them. The stop notice also requires the recipient to provide HMRC with detailed information on its clients, and to pass details of the stop notice to those clients. ↩︎

In theory the existing rules should deal with that. The effect of a stop notice also applies to (amongst others) anyone who controls, or has significant influence, over the recipient of the stop notice. And if the recipient transfers its business to another person, then the stop notice applies to them too. All of this is in theory: in practice the entities tend to be offshore and highly opaque, and it is difficult or impossible for HMRC to prove the relationship between them. ↩︎

i.e. expanding HMRC’s existing powers by removing conditions B and D – HMRC should simply be able to pursue directors/participators as soon as a DOTAS penalty is issued. ↩︎

Either because frivolous legal positions were taken or indefensible assumptions of fact were made ↩︎

Interestingly this doesn’t seem to be the case for Setu Kamal’s opinions for the Arka Wealth scheme – he seems to really give opinions to end users. The scheme may be laughable, but at least the users get some legal recourse (although possibly Mr Kamal has little practical exposure given he’s based outside the UK). ↩︎

To be clear, this is not a job-creation scheme for me – I’m retired from full time work and, even if I wasn’t, I don’t have the right skillset for such a job. ↩︎

12 responses to “Radical anti-avoidance measures hidden in the Spring Statement”

A combination of grandstanding politicians, a supine parliament and a hopelessly bureaucratic Revenue Authority have led to the most complex tax code in the world with then inevitably opportunities for the tax avoidance industry to exploit. So rather than stuff like this (and that on tax agents) put some serious effort into code simplification.

This all makes good headlines for the Government, but at least with avoidance HMRC have some idea of what is going on, while the big elements in the tax gap are in pure evasion where the effort of HMRC should be concentrated

I find it astonishing that someone could use a defence of “I received legal advice” without having to disclose that advice.

Surely courts shouldn’t accept someone’s word for something, it feels like a murderer saying “I was somewhere else” and the court taking their word for it and letting them off!

Dan. I am far from convinced by your proposal to absolve “normal advisers or commercial parties who made an innocent mistake”. Anyone promoting a tax avoidance scheme should understand there are penalties, possibly criminal, if the scheme stands no or negligible chance of success. A solicitor or accountant doing this will incur professional responsibility. If a non-professional doing so is not held to a comparable responsibility, they will invoke fictitious “innocent mistake” defences.

the boundaries of some of the DOTAS hallmarks are unclear. Many or even most commercial transactions have tax-driven elements – quite properly. It is not always 100% clear they fall outside DOTAS, even though they are (sensibly viewed) not tax schemes at all.

So we need to be careful that an innocent mistake in a commercial transaction isn’t accidentally transformed into a criminal offence.

There are a few ways to do this.

I agree your suggestion of a dedicated team within HMRC to enable these matters to be property pursued and ensure the promoters are held accountable and have fees at risk of confiscation.

There is a balance as you mention of not overly penalising the hapless or naive taxpayers and/or their regular tax advisers that might be persuaded of the supposed merits of a scheme… a technical yet innocent error …rather than considered scheme promotion and intent

Good summary, Dan, and thanks for all your work highlighting the ongoing problem of a small group of promoters.

There is a lot that I agree with here – in particular a deemed waiver of LPP where the barrister’s opinion is touted around as part of the marketing. (I suggested this, via a CIOT submission, some time ago).

I have three concerns, though:

1. The “A” in DOTAS is not “Avoidance”, it is – at least when you get into the detailed rules “Advantage”. That is so widely defined that even delaying paying £1 of tax by 1 day in a perfectly vanilla and legal way is a tax “Advantage”. The only thing that stops every piece of tax advice being DOTASable are the hallmarks. But HMRC can change those at Will. At present the hallmarks are reasonable and balanced. But if criminal sanctions are introduced, this puts a huge weight on HMRC – who will effectively have the power to criminalise something at will by issuing a hallmark. With a strict liability offence and only “reasonable excuse” as an untested defence this feels very draconian. So if a criminal sanction is introduced, it should be for a more limited subset of DOTAS disclosures. I quite like the test (later in the paper) of “no tenable basis” as an additional safeguard.

2. LPP. The paper – as usual – omits the crucial detail that LPP belongs to the client not to the lawyer. I have no truck with the barristers you have highlighted previously and then hidden behind LPP. But we need to be very careful that lawyers aren’t caught between a rock (LPP preventing them from disclosing) and a hard-place (the client tactically waiving LPP just at the wrong moment, thereby criminalising the actions of their lawyer). This needs more thought.

3. All of these proposals seem reasonable enough…if one assumes that HMRC are behaving constitutionally and democratically. But any increase in HMRC’s powers like this (particularly where criminal sanctions are in point) need to be judged against a hypothetical Magnitsky test.

Sergei Magnitsky, you will know but others may not, was a Russian tax adviser who uncovered corruption in the Russian Tax authorities. When he revealed this, the Tax authorities used draconian powers against him; criminalised him; prosecuted him; imprisoned him; and then beat him to death in prison.

Fortunately the UK is a long way from that still…but only because of constant vigilance around the powers of the police, HMRC and other government agencies.

Every proposal to criminalise the behaviour of lawyers and other advisers needs to be tested against a hypothetical…what if a few rogue HMRC inspectors take against you?

I am not convinced that the safeguards here entirely work in every hypothetical situation…particularly the two I’ve highlighted above…and that should concern everyone who believed in the rule of law.

Make sure you check under your bed and in the cupboard before you go to sleep tonight. There could be monsters.

Hi Dan,

you should take no small credit for your determined reporting of these scam schemes. I would hope that acknowledgement (formal or informal) finds its way to your door!

Seems like a step in the right direction, provided the authorities actually use any new powers and allocate the resources to ensuring anyone who makes money promoting tax avoidance schemes is caught, and punished.

This is excellent news. To a lay person it is simply astounding that such a tax avoidance industry exists to the extent that it does. Governments have continually pandered to vested interests to leave lay investors financially exposed and without practical recourse, while the ‘professionals’ go scott-free.

However, as good as all this sounds, and as you point out, if HMRC do not have sufficient resources, then these will simply become a set of unused tools to sit alongside all the other rarely used tools in HMRC’s toolbox.

I do so hope that this isn’t what happens!!

It’s about time too this was done.

What does worry me though is how effective can HMRC police the system, with the resources they have, how management works etc.

HMRC and ultimately the government need to ensure the right people with conviction, who are motivated and well rewarded (and I mean well) to do the job properly

Part of the problem with HMRC is the remuneration structure, this really does not support this.

I have found having HMRC letting me go, (and yes I was one of the good guys!) that I could earn 100% more in the private sector jut using my knowledge, (and no I don’t undermine HMRC only ensure they operate as they should!)

How HMRC is set up with the regional offices in big cities, does not help, as the private sector can easily cherry pick the best staff to the private sector.

Now this is third hand, but came from a very reliable source when I was at HMRC (and from seeing how HMRC regional offices work, I can corroborate this) – Private firms were advising candidates to get a job with HMRC do two years and then go back to them.

I do hope it works, (and yes I am sorry to say this), however with a lot of promises made by the government where HMRC are involved in the past the actual results never met the expectations!

Hello Dan, The condocs re interesting reading and I’ve not reflected on them enough to comment properly. It would be good to get to the stage where the promoters worry that they will be arrested when they arrive at Heathrow.

In relation to: “The GAAR panel publishes its opinions; but the firms involved are not named”. I think it is HMRC that publishes the anonimised opinions rather than the GAAR panel. It also looks like HMRC only publish some of them: “We will only publish an opinion here if we can anonymise it to protect taxpayer confidentiality”. However, HMRC does not give any description at all as to the unpublished ones and so there is no information as to what the topic is. I think that should change.

I do not think taxpayers should be named (and you are not suggesting they should be). What the GAAR panel does is very different to a court that makes findings of fact.

I have no problems naming advisers where the GAAR panel’s opinion is that the scheme is not reasonable.

I also agree with the removal of names on HMRC’s naughtly list after 12 months. That just seems silly.