I’m writing a short series of posts on the Tory candidates and tax. Today: the Sunaks. A recap of what we know, what we don’t, and the two big outstanding questions.

The following has been overtaken by Sunak’s recent denial to Andrew Marr that he’s used tax haven trusts. My assumption is that this denial is correct, and the Independent report was wrong. I’m keeping the rest of this post up because I think the point is of general interest. Right now there is no reason to believe the Sunaks are using an offshore trust to avoid tax.

The following is speculation based upon information on the public domain, my experience as a tax lawyer for many years, and conversations with other tax experts. I could be wrong – and if the Sunaks confirm that their tax position is actually completely straightforward, I’ll happily post a correction and delete my Twitter thread.

What we know about the Sunaks

After some initial resistance, the Sunaks eventually admitted that Akshata Murty is a non-dom, and that she had historically claimed the “remittance basis”. Which means she wasn’t taxed on her considerable overseas income – primarily several $million a year from Infosys, the Indian IT company started by her father.

After a considerable kerfuffle, Mrs Murty eventually agreed to stop claiming the remittance basis. Does that mean the Sunaks now pay UK income tax on the $m in Infosys dividends? Not necessarily.

The key piece of the puzzle: The Independent reported back in April that both Akshata Murty and Rishi Sunak were beneficiaries of offshore trusts in the British Virgin Islands and the Cayman Islands. This was never denied – the Sunaks refused to comment.

What we know about wealthy non-doms

Non-doms aren’t taxed on their foreign income and gains (my previous post explains this in more detail). That’s very generous of the UK, and very lovely for them. But, like all good things, it comes to an end. Either the non-dom becomes so attached to the UK that they can no longer credibly claim to be a non-dom. Or, after fifteen years, they become “deemed domiciled” in the UK by operation of law.

But what if you really, really, don’t want to lose the lovely ability to rack up foreign income and gains tax-free? Easy: set up an offshore trust before you lose your non-dom status. The trust then effectively preserves the tax-free nature of the assets in the trust forever1. This kind of arrangement is called an “excluded property trust” and is absolutely standard planning for wealthy non-doms – and you can see just how standard it is if you Google “excluded property trust”.

So it would be extremely unsurprising if Mrs Murty set up an excluded property trust.

What we don’t know – but can speculate

Let’s speculate that one of the trusts disclosed by the Independent is an excluded property trust holding Mrs Sunak’s Infosys shares. This could be completely wrong – in which case the Sunaks should say so, and I’ll correct this post.

But if that’s right, when Mrs Murty said she would now be taxed on her overseas income, she was being exceedingly cute. The reality would be that the dividend income is received by their offshore trust, and so isn’t Mrs Murty’s income at all. The Sunaks would then be avoiding several £m of UK tax on the dividends, and – if the trust sells the shares in the future – there’s no capital gains tax on the sale.

Whether or not Mrs Sunak is claiming the remittance basis would then be a red herring. Her non-dom status enabled her to set up the trust and put the shares in it (in a way a normal UK resident couldn’t). But the trust income/gains remain untaxed2.

Why we shouldn’t forget inheritance tax

Most of the press coverage around the Sunaks and tax focussed on income tax – and if the above speculation is right, the Sunaks are avoiding several £m of income tax each year on the Infosys dividends. But inheritance tax is much much more important – with holdings of close to a billion dollars, the Sunaks’ estate would face inheritance tax of several hundred million pounds if the Sunaks held their assets directly. An excluded property trust would avoid that tax.

The key questions

There are really just two:

What is the purpose of the offshore trusts and what do they hold?

Does Mrs Murty hold the Infosys shares and other foreign assets directly, so she’s now fully taxed on their income? Or are they in trusts, structured so as to escape UK tax?

Is this tax avoidance, and does that matter?

Whether something is or is not tax avoidance is a subjective question. But my view is: being a non-dom and claiming the remittance basis is not tax avoidance – it’s how the rules are supposed to work (stupid as that may be). It does, however, feel inappropriate for the family of a Minister.

But using offshore trusts to artificially extend the benefits of non-dom status is in my view clearly tax avoidance. And for a Chancellor or Prime Minister, it creates an impossible conflict of interest – it’s the job of Government to close tax loopholes, not secretly benefit from them

David Cameron was criticised for inheriting £30,000 from his father that had been in an offshore unit trust. I thought that was unfair – a unit trust is not very avoidance, and you can hardly blame Cameron for what he inherited. In any case, Cameron later confirmed he and his family did not benefit from offshore trusts.

By contrast, Sunak is asking to be Prime Minister whilst refusing to comment on whether he is a secret beneficiary of an offshore trust which conceivably avoids £100m of tax. He should clarify the position.

Inevitable caveats

I am speculating based upon information on the public domain. If the Sunaks confirm they don’t have valuable assets in an offshore trust, and are actually paying income tax on the Infosys shares and other foreign income, I’ll correct this post and delete my Twitter thread.

Footnotes

. Of course it’s a load more complicated than this, but I think that’s the essential truth ↩︎

Payments by the trust to the Sunaks in the UK would be taxable (although loans can be used to get around that). ↩︎

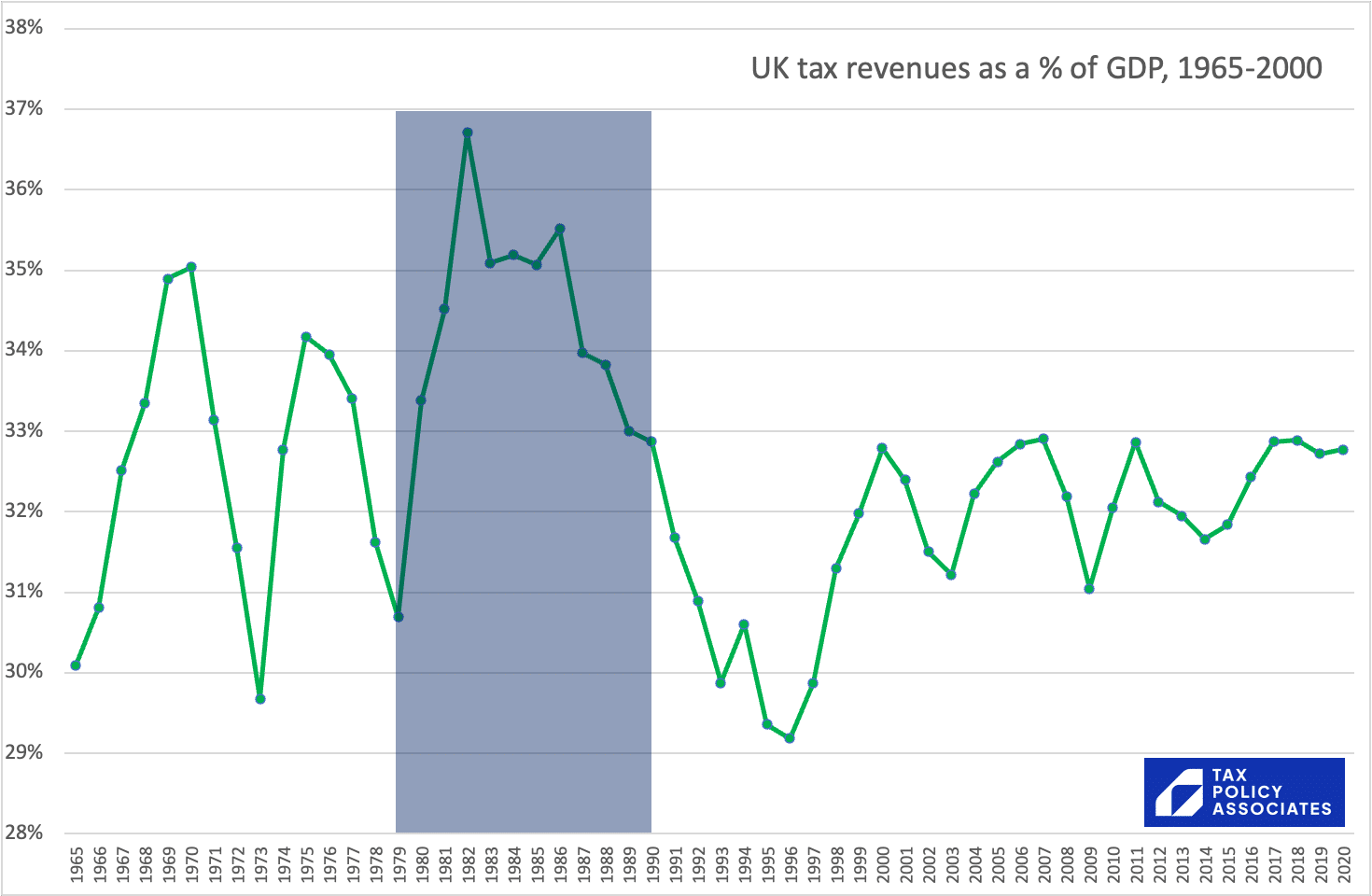

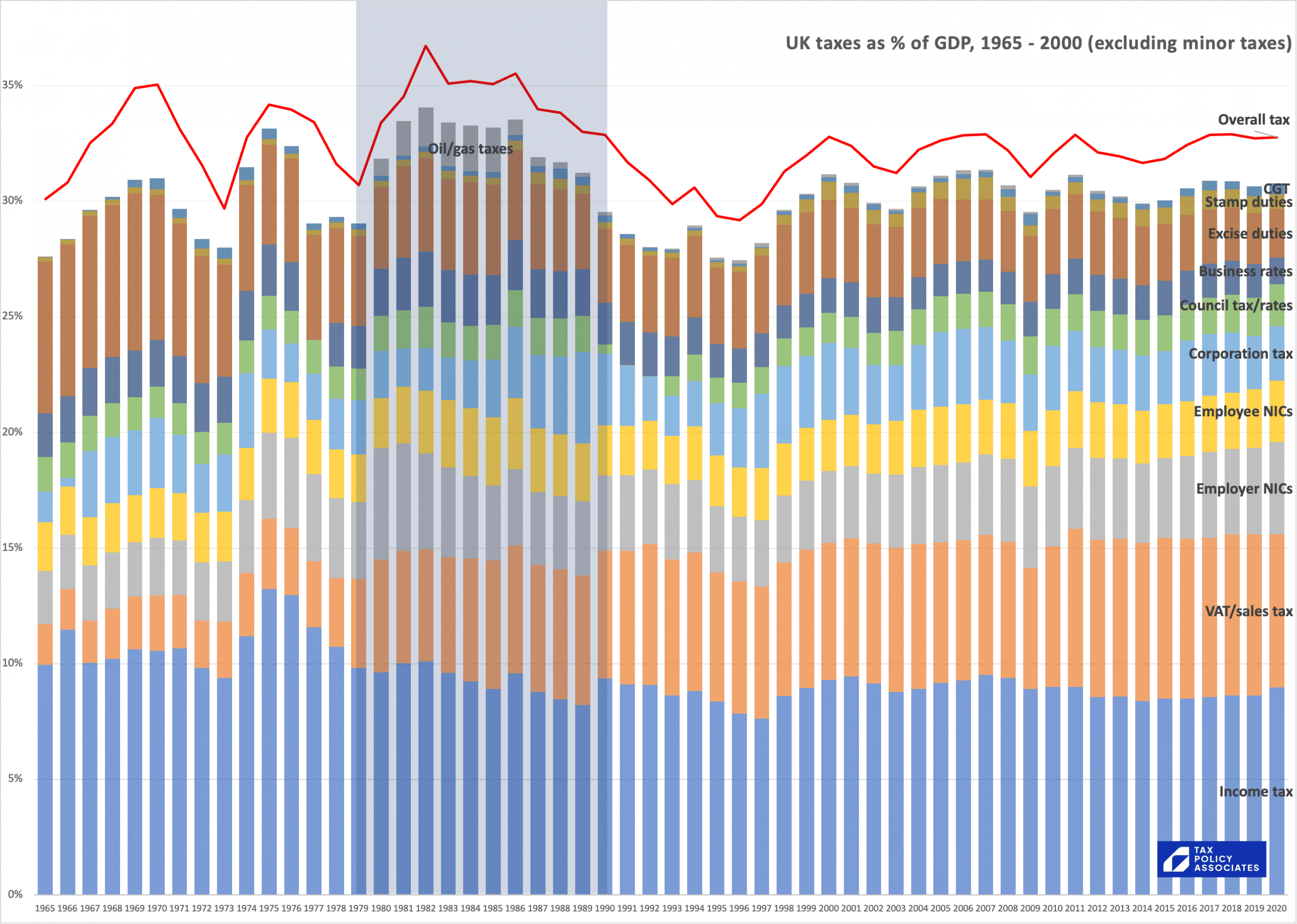

Mrs Thatcher is still heralded as a tax-cutter by many. But what actually happened to UK tax revenues, as a proportion of GDP, over her premiership?

They went up a lot, then down a fair bit, but not as much as they went up. Was this the result of specific policy decisions to raise tax? Or something else?

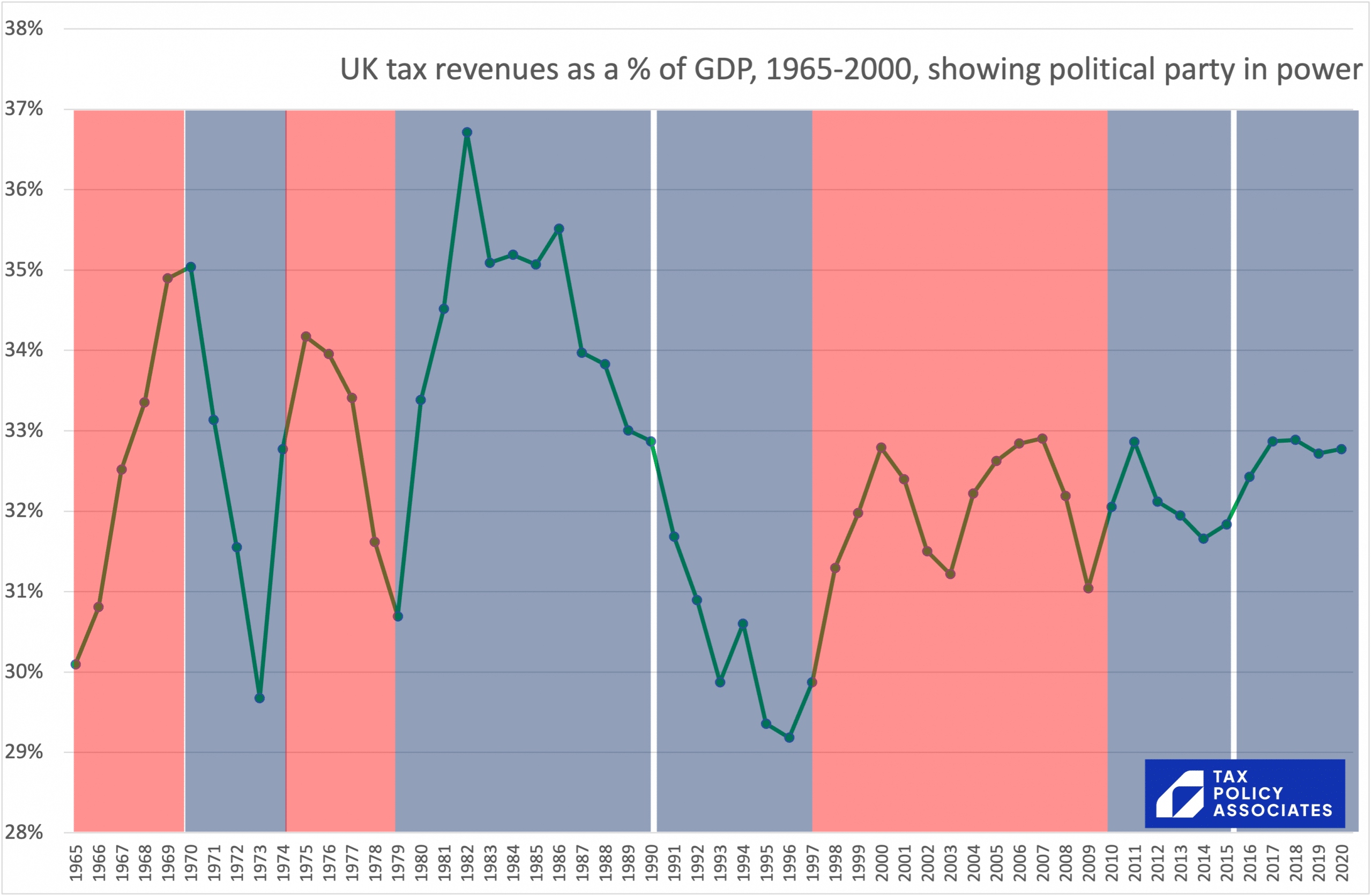

But first – can we make any general statement about the relationship between tax vs GDP and the political party in power? Not really:

One nice symmetry: the overall Thatcher increase in tax from 1979-1990 is almost exactly the same amount as the overall Blair/Brown increase in tax from 1997 to 2010.

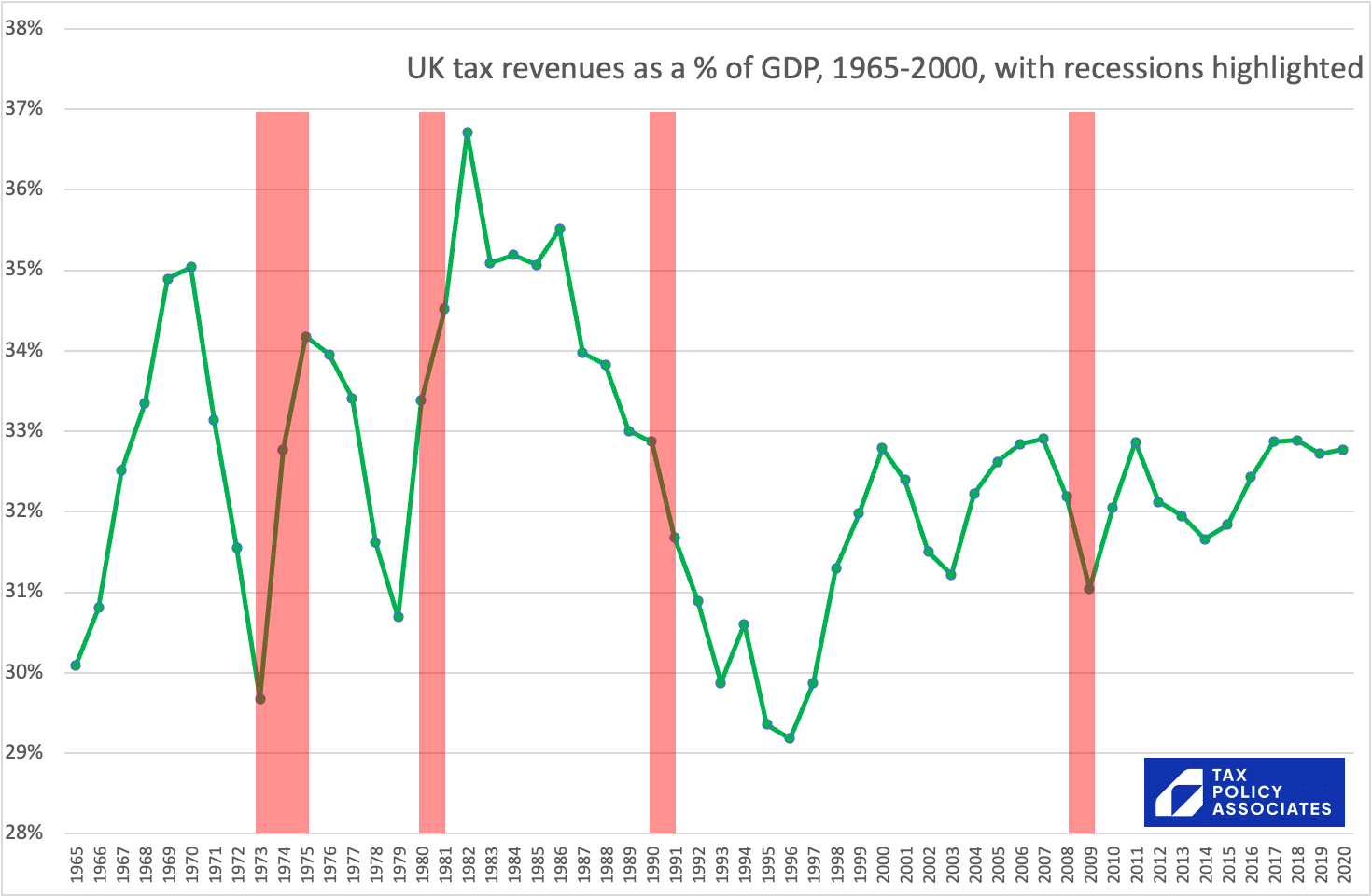

So is politics irrelevant? Are the wild swings in fact just driven by recessions, with GDP contracting and so tax/GDP increasing?

That looks like an inadequate explanation, only (arguably) fitting the data for the 1973-75 recession.

What if we look at the actual changes in individual taxes?

Now we have it: three drivers for the big tax increase over 1979-82: VAT rising from 10% to 15%, the North Sea oil boom, and the increase in employer NICs. Income tax was certainly cut, although not very dramatically, and that was more than overcome by the increase in VAT.

Seems fair to say that the Thatcher tax increase was an intentional policy-driven rise in tax, not a mere incident of GDP contraction.

All data from the wonderful OECD tax database, with similar taxes consolidated together to produce a reasonable like-for-like comparison across 1965-2020. Full spreadsheet here.

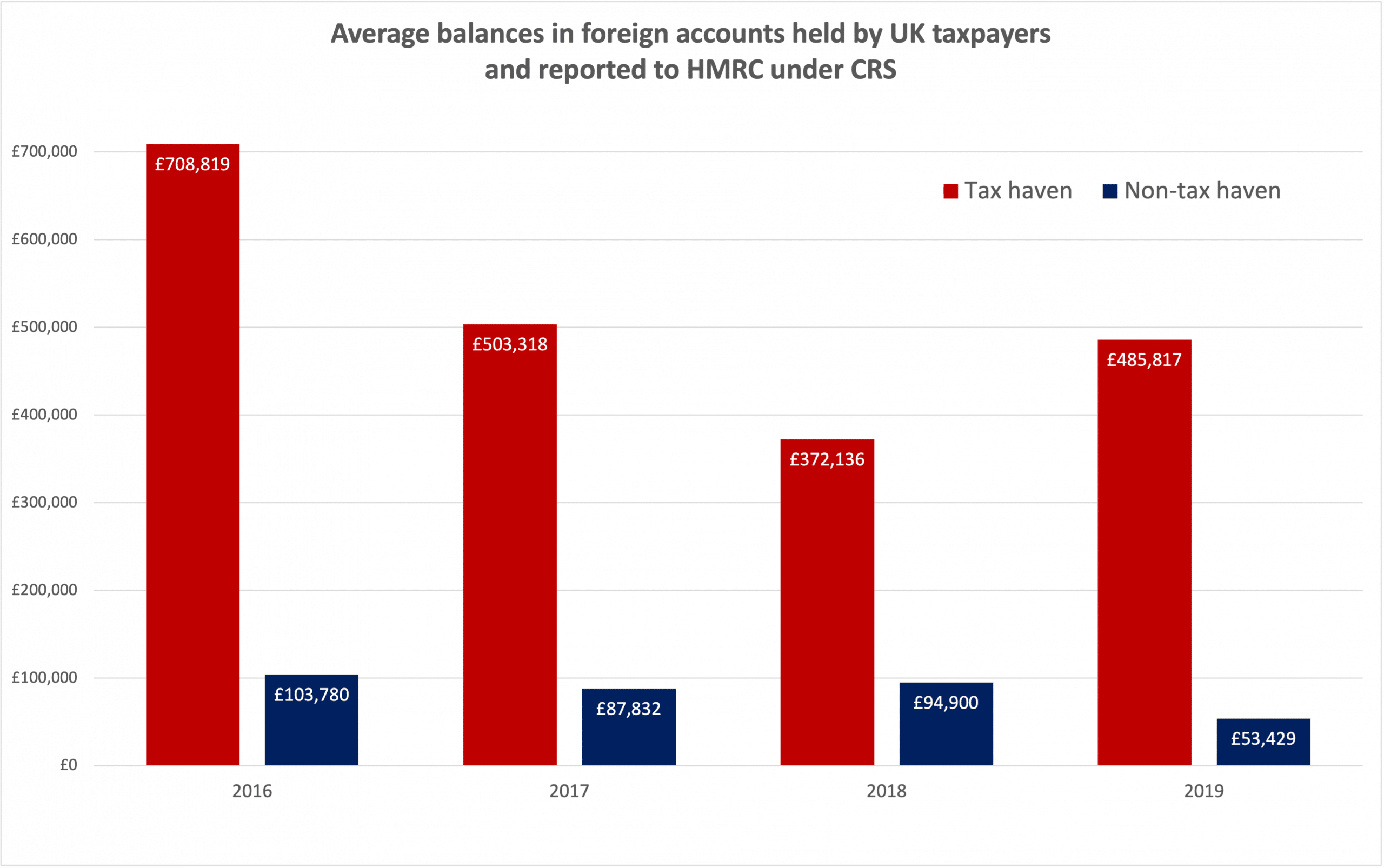

FOIA requests made by Tax Policy Associates reveal that £570bn is held in tax haven bank accounts by UK taxpayers, but HMRC has made no attempt to estimate how much of this is undeclared in UK tax returns, and therefore reflects tax lost to criminal tax evasion.

The background

Since 2018, almost all UK residents with overseas bank accounts have had their name, tax ID, and the balance and income on those accounts automatically reported to HMRC every year. That’s part of a revolutionary global project – the OECD Automatic Exchange of Information/Common Reporting Standard (CRS), under which €10 trillion of accounts were reported worldwide in 2019.

This should be a bonanza for HMRC. We’re all (except non-doms) supposed to declare income from foreign accounts in our tax returns, with up to 300% penalties if we don’t. So if someone has foreign account income reported under CRS which wasn’t included in their tax return, and they’re not a non-dom, HMRC should be able to immediately identify potential tax evasion.

The amounts are very large – in 2019 UK taxpayers had over £850bn in foreign accounts, of which £570bn was in tax havens – see chart above (and my definition of “tax haven” below). And the average account size in tax havens is considerably larger than the average in the rest of the world1:

Why is it important to have an estimate of the proportion of the £570bn that reflects tax evasion?

Because the scale of the estimate has enormous public policy implications.

If 30% of the accounts are undeclared (as some have previously suggested), then it’s a massive scandal and immediate action of the most serious kind will need to be taken. I’d say the same if the figure were 3%.

If, on the other hand, it’s 0.1% then all we should expect is efficient and effective HMRC enforcement.

The options

When HMRC started receiving this data back in 2016, it had several options:

The traditional approach. Build a computer system to cross-check the CRS data with everyone’s tax return, to see who has an offshore account on which they’ve received income that wasn’t declared on a tax return. Version 1.0 doesn’t need to be very expensive or complex – just pull out matching tax IDs (national insurance numbers or UTRs) from the two sets of data, where CRS data indicates large tax haven accounts but nothing is declared in the “offshore income” section of the tax return. See what comes out. Build up the complexity and sophistication from there.

The quick option. Set a bunch of junior tax inspectors to work manually pulling out a random sample of say 1,000 high-value individual CRS accounts in tax havens, locate those individuals’ tax returns, and look for anything suspicious. Then apply statistical tools to the result so you can estimate the overall level of non-compliance (albeit with significant uncertainty). Use that to inform whether you build a big system to automate this, and how you do it. Or maybe you find it’s slim pickings, and so just continue random manual checks for the largest accounts.

The nerd option. Anonymise all the CRS data, hashing names, addresses, and tax IDs. Do the same with the overseas income section from tax returns. Hand both datasets over to a bunch of smart academics and data scientists, so they can do all the hard cross-checking for you. For free.

The Thatcherite option. Do the anonymising thing again. But ditch the nerds – instead, offer private sector companies the chance to crunch the data and identify tax evaders, in return for payment of 10% of tax evasion recoveries. The nerds could apply too.

The implausible option. Don’t do any cross checking, automated or manual, large scale or small scale. Make no effort to match up CRS data with tax returns.

Right now it’s unclear quite what HMRC have done – they’re refusing to say. They’ve told the FT’s excellent Emma Ageyemang that they “systematically” check the CRS data, but won’t reveal more. We can speculate they’re looking only for huge anomalies (e.g. millions in CRS accounts but nothing in a self-assessment return) but not cross-checking everything (or they would surely say so).

That speculation is consistent with the letters we know HMRC have sent to people with foreign accounts disclosed under CRS, reminding them of their responsibility to declare foreign income. HMRC has made clear these letters are sent on the sole basis of the CRS data, and without cross-checking with actual tax returns.

What is clear is that HMRC have made no attempt to estimate the scale of the offshore tax evasion problem, or even determine if it is a problem. The FOIA response says:

Why?

We’ve had several justifications from HMRC.

First, in the FoIA response:

“A number of the accounts reported through the Common Reporting Standard (CRS) are not actually chargeable to UK tax, nor is every account of a suitable value to impact on a persons’ UK tax position”

These, and many other factors, are why the CRS data has to be used with care. They are not reasons to discard the statistical value of the data altogether. You’d expect any kind of audit or cross-check to exclude non-taxable accounts and low-value accounts. (Although the obvious reason why some accounts of UK residents are not taxable is that they are held by non-doms, and given HMRC normally receives no data at all on non-doms’ foreign assets, you’d think this itself would be very useful data.)

Second, when speaking to the FT, HMRC said:

Not all of the worlds’ jurisdictions are signed up to CRS and we could not say with certainty whether each account was ‘properly disclosed’. We would not publish a figure where we did not have certainty that is accurate.

Here HMRC seem to be taking the odd position that no estimate can be made unless it is certain to be accurate. That is not what the word “estimate” means, and statistical methods have been developed to deal with errors for at least two hundred years.

HMRC is certainly familiar with producing estimates which are highly uncertain – they do so very competently in their annual tax gap report. This contains estimates for tax evasion and avoidance which have very large uncertainties – HMRC describes them as the “best estimates based on the information available”. And that’s fine. What’s not at all fine, and in fact inexplicable, is using uncertainty as a reason for making no estimate at all.

Furthermore, the stated reasons for uncertainty do not seem very hard to overcome. Whilst there are some jurisdictions not signed up to CRS/FATCA, they are generally ones where rational tax evaders would not risk keeping funds. They’d make any estimate a baseline/lower bound, but that would not diminish its usefulness.

“Properly disclosed” is also not terribly challenging to overcome. For example: focus on CRS accounts where the income/gains is larger than the annual exemption, and where there is a straightforward national insurance number/UTR match with the tax return of a taxpayer who is not a non-dom. Again that would result in a lower bound estimate, but still a useful one.

So HMRC’s explanation for the lack of any estimate doesn’t make sense.

Can we use other sources to estimate how much of the £570bn reflects tax evasion?

I don’t think we can – which is why HMRC’s failure to product estimates is so unfortunate.

I am very sceptical of some of the claims that have been made that over 30% of offshore accounts are undeclared. Tax authorities have now had the CRS data for five years or more, those that aren’t asleep at the wheel have been cross-checking against tax returns, and there have been a handful of prosecutions rather than thousands. And the existence of CRS means that pre-2016 estimates are of limited value.

It’s also important to remember that there can be many entirely legitimate reasons for having a financial account in a tax haven:

Private equity funds, hedge funds and other types of non-retail funds are very commonly established in tax havens (most often Jersey, Bermuda, Guernsey and the Cayman Islands). As with most investment funds, the investors expect to pay tax on their return from the fund, but don’t expect the fund to also pay tax – that would be double taxation. You could achieve this in e.g. the UK with a great deal of work, but is much, much easier in a tax haven. So this isn’t tax avoidance – it’s tax lawyer avoidance. I expect a substantial part of the £570bn reflects fund holdings, and that almost all of this is properly declared to HMRC.

Corporate joint ventures often use tax haven companies for the same reason – preventing double taxation is just easier/cheaper.

Many companies will have legitimate business in some of the tax havens, e.g. shipping companies in Panama, lots of companies in Hong Kong and Brazil.

Non-doms who are trying to avoid taxable remittances will often do so with a tax haven account. I don’t like the non-dom regime, but given we have that regime, they’re making a legitimate choice.

Some of the tax havens have sizeable ex-pat populations in the UK, who have excellent reasons for retaining their home bank accounts.

But historically tax haven accounts were certainly used by the wealthy to hide assets away from tax authorities. Chances are some people are still doing this, whether because they are too disorganised to appreciate the risk of CRS, have some legal impediment which prevents them reacting to the risk (e.g. missing documentation), or are gambling that HMRC won’t spot them.

So I would be equally sceptical of any claim that there is no evasion hidden in the £570bn.

Are most of the offshore accounts held by non-doms?

Plainly not. The FOIAs show over a million tax haven accounts held by UK taxpayers in 2019. In that same year, there were fewer than 100,000 non-domiciled taxpayers claiming the remittance basis (i.e. for whom offshore accounts have a permitted tax benefit).

What should happen now?

In the interests of transparency, HMRC should publicly commit to:

Annually publishing aggregated CRS statistics, such as number of accounts, and the mean and median balances. It shouldn’t take FOIAs to extract this information.

An initial analysis of the CRS data, with – as a first step – the aim of estimating the proportion of accounts that haven’t been declared in tax returns. Any such estimate will be highly approximate, and number to numerous uncertainties. The HMRC tax gap report ably deals with much more difficult uncertainties (“unknown unknowns”); this is straightforward by comparison (“known unknowns”).

Publishing the result of that analysis (minus any details that could assist tax evaders).

Sharing the two key datasets: CRS data and the self-assessment foreign income returns – with academics, with suitable measures in place to protect taxpayer confidentiality.

Equivalent measures for FATCA.

To assist the ongoing public debate about the non-dom regime, publish the total balance of foreign accounts disclosed under CRS which are held by non-doms, the number of those non-doms, and the median account balance.

HMRC obviously should not reveal precisely how it uses CRS data, but it should be open about the results. How much additional tax has been collected from investigations sparked by CRS? How many penalties and prosecutions have there been?

This transparency is important for three reasons: keeping HMRC accountable; deterring tax evasion; and bolstering public faith and confidence in the tax system.

Full details

Everything is in three FoIA responses. The first reveals that the total amount held by UK taxpayers in foreign accounts is £850bn, the second says that £570bn of this is in tax havens, and the third admits that no effort has been made to estimate the proportion of CRS accounts which are undeclared to HMRC.

HMRC prefers not to use the term “tax haven”, so I defined the term using a particular technical definition which covers the following countries: Andorra, Antigua and Barbuda, Aruba, Barbados, Belize, Brazil, Colombia, Cook Islands, Costa Rica, Curacao, Faroe Islands, Gibraltar, Greenland, Grenada, Guernsey, Hong Kong, Isle of Man, Jersey, Korea, Lebanon, Lichtenstein, Macao (China), Mauritius, Monaco, Montserrat, Niue, Panama, Samoa, San Marino, Saudi Arabia, Seychelles, St Kitts and Nevis, St Lucia, St Vincent and the Grenadines, Vanuatu.

That’s not a perfect list of tax havens (I’d exclude Brazil and include Switzerland and possibly Singapore), but it’s a good approximation.

The data covers all financial accounts (cash bank accounts, security custody accounts, interests in investment funds) held by UK resident individuals and corporates that are not financial institutions.

This is CRS data only, and so doesn’t include accounts in the US, as the US reports under a different set of rules (FATCA) and HMRC wasn’t willing to disclose anything about the FATCA data it had received. So the actual total for non-tax haven accounts is likely much higher than the figures above.

Footnotes

A tax professional with a huge amount of experience in this area made the excellent point that we need to be careful to distinguish actual account holders vs UK controlling persons of companies (“Passive NFEs”) are accountholders. Otherwise we can be double or multiple counting – i.e. because one company can have multiple controlling persons, and some of those (trustees) won’t be taxed on the account. My FOIA should have extracted the accountholders only, but absent full disclosure by HMRC it is possible they have mistakenly given me UK controlling person data as well ↩︎

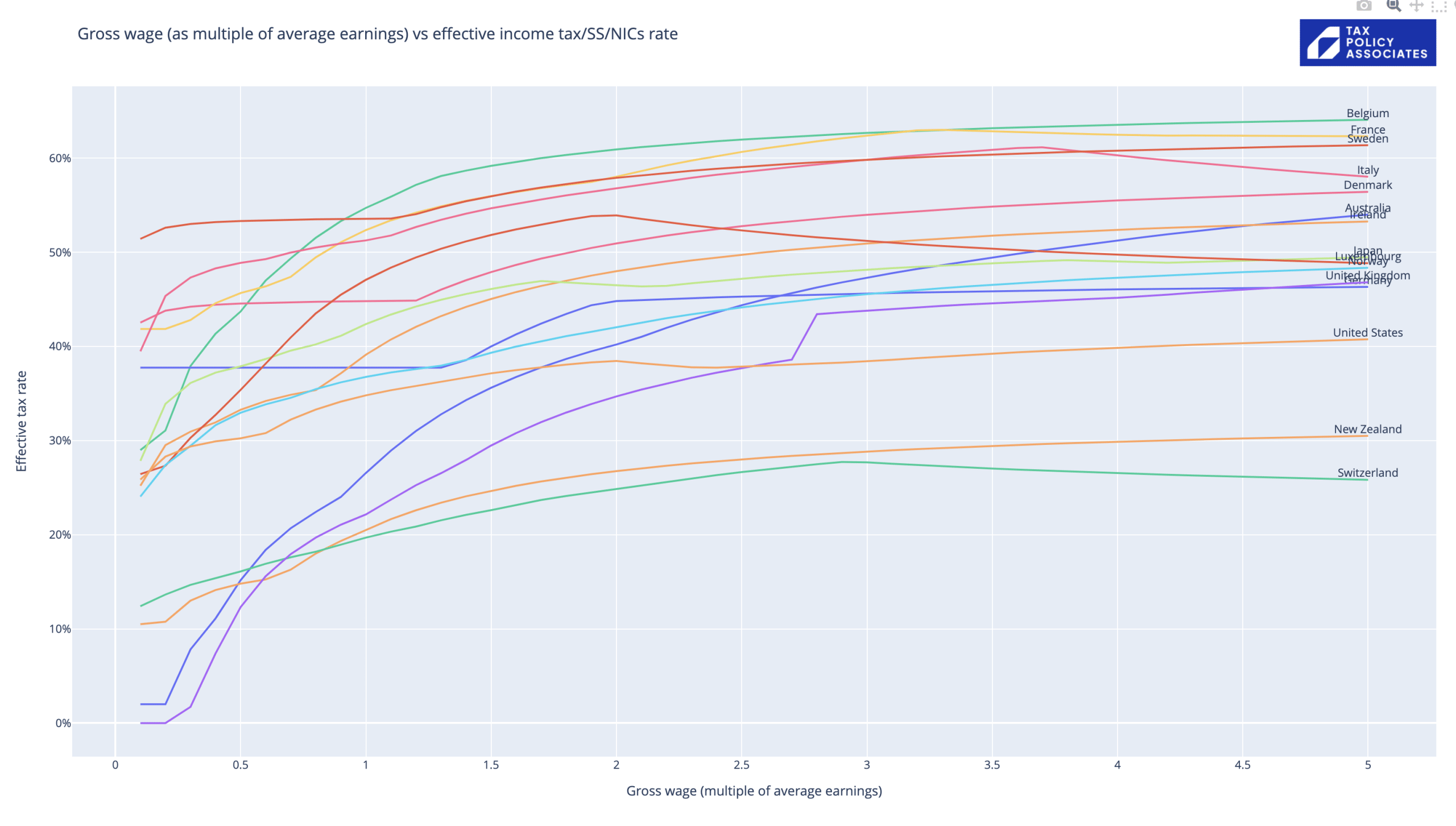

In the UK there’s income tax, and national insurance – both shown on our wage slip. But also employer’s national insurance – which the employer pays, and isn’t visible on our wage slip, but evidencesuggests is mostly borne by workers (i.e. because the employer has an amount they’re willing/able to pay as wages, and employer NICs come out of that).

Take all that together, and of the average UK wage of £37k, the total tax (sometimes called the “tax wedge”) is 22%. This is the “effective tax rate”, not to be confused with the “marginal tax rate”, for which see here.

How does the rate change as incomes increase? The chart at the top of this post looks at income vs tax wedge, measuring income as a multiple of the average wage (thanks to a little bit of python). Caveats below.

Obvious points: looks like a nicely progressive upwards curve until we hit £100k, at which point the personal allowance starts to be withdrawn and the curve kinks upwards way too steeply. Then eventually the curve trends towards the eventual marginal rate of 47% (45% income tax plus 2% national insurance).

How does this compare with other countries? Thanks to the wonderful OECD tax database and that bit of python, we can say it looks like this: (caveats caveats caveats below).

Click on chart for interactive version that lets you add/remove countries

Obvious conclusion: until you get to quite high incomes (almost twice average) the UK taxes income less than any comparable country, with only a few small countries/tax havens taxing less. I haven’t cherry-picked the comparisons here – if you click on the chart you can play around, clicking on different countries to hide/reveal them.

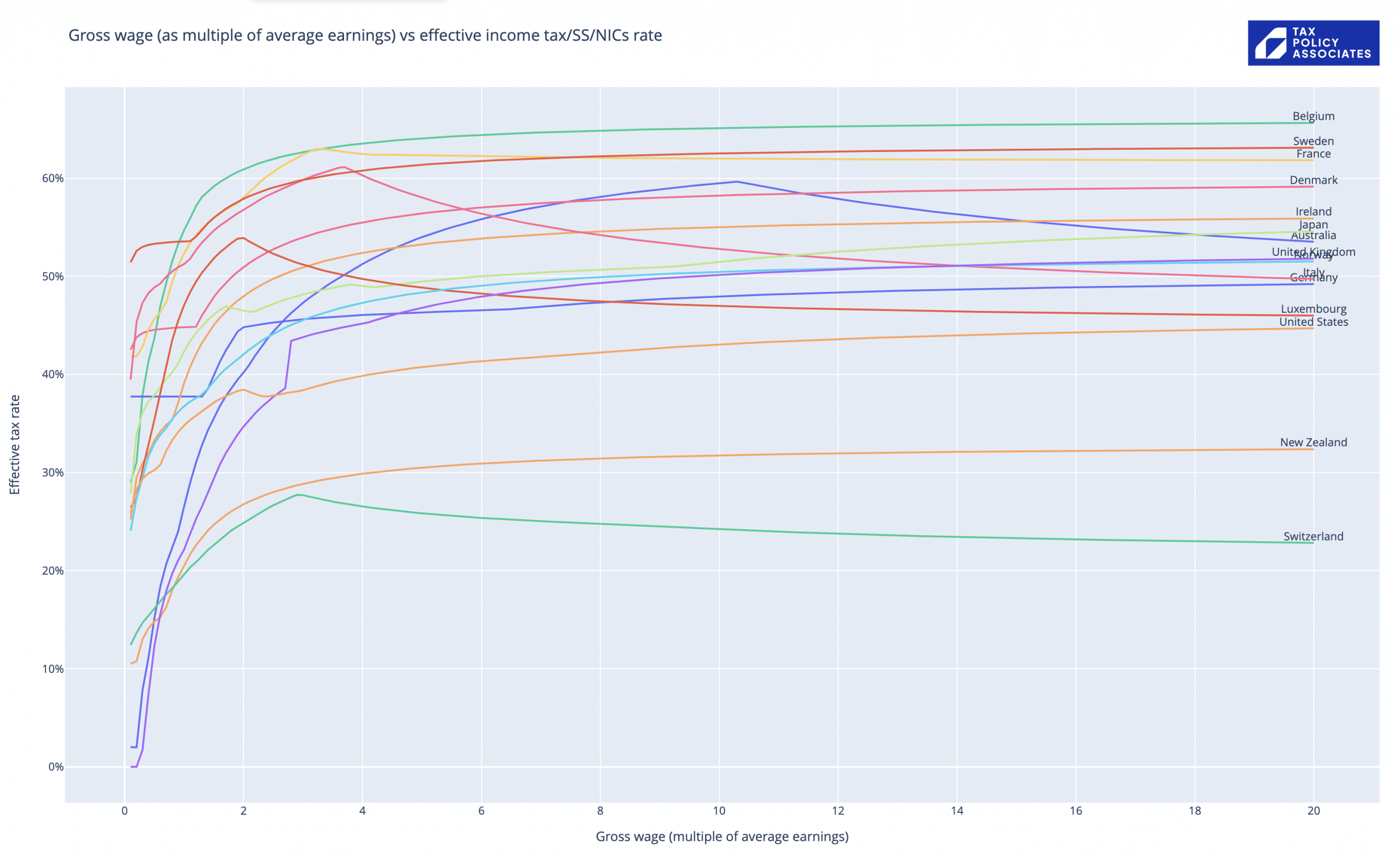

What about high earners? That’s clearer if we re-run the code to go up to 20x average incomes (which in the UK equates to about the top 1% of earners):

Click on chart for interactive version that lets you add/remove countries

The UK (purple line again) tracks lower than most of Europe, but (surprisingly) shows a higher effective rate of tax on high incomes than Germany or Spain. Way less than Belgium, France, Sweden.

There are political conclusions from both charts I will blog about another time.

Now the extensive, but probably incomplete, list of caveats:

All data is for 2020, the latest available from the OECD. UK national insurance has of course gone up since.

The code and underlying spreadsheet are “quick and dirty” and there are almost certainly mistakes and omissions. Please don’t use this for anything serious without checking carefully, ideally going to local experts to verify the data and assumptions. With a bit of work this could be a robust and useful project; it’s not there now.

The underlying data comes from the OECD tax database, and the average earnings figures from the OECD labour/wages database. Adapted in places (e.g. the Belgian local income tax figures reflect the revenue position for the Belgian local authority and not the position for taxpayers). I added the withdrawal of the UK personal allowance, because it is so significant; there may be similar issues in other countries which I have missed. All errors are mine.

The data takes into account employer and employee social security/national insurance, and national and state/local income taxes (at the national average). No other taxes.

The data completely ignores the benefits system. That has two big consequences. First, it means the apparently high effective rates on low incomes in many countries are misleading, because we’re missing the other half of the picture. Second, where benefits are means tested, there is often a high marginal rate at the point they’re withdrawn.

The data excludes mandatory pension contributions.

The data ignores deductions/reliefs (with the exception of universal allowances/credits). That doesn’t matter much for countries like the UK, where reliefs for employees are very limited; but it makes the US data unreliable given the very generous deductions/reliefs permitted in the US.

Where countries have different rates for different family types, the rates/allowances used are for wage income of a single person without dependants. This will somewhat affect the effective rate for someone on a lower income, but will have little effect on higher incomes.

The code assumes that local taxes use the national tax base (after personal allowance/credits) and national insurance/social security exclude all personal allowances/credits. That won’t always be right, and will cause errors for (in particular) lower incomes.

The fact VAT isn’t included has the overall effect of flattering every country except the US (i.e. because they’re the only major economy with no VAT).

Private medical insurance isn’t included. That has the overall effect of flattering the US figures (because we’re not comparing like with like). Possibly this and the VAT effect cancel out. Or possibly they don’t. Someone could do the math!

Property taxes aren’t included. That’s significant for countries like the UK where local authorities are funded by property taxes not local income taxes. So the chart is somewhat flattering the UK (particularly at middle incomes where there is no council tax relief, but the council tax bill could be 10% or more of a household’s total tax bill).

You are the beloved daughter of the dictator of Freedonia. You have oodles of cash, investments, real estate etc etc, all of which you earned through your legitimate occupation as a podiatrist. You aren’t taxed in Freedonia (because local tax inspectors generally take the view that taxing the dictator’s daughter is not compatible with their continued good health).

As we approach 2023, you’re thinking about moving to London. Yes, Daddy says it’s a decadent imperialist hell-hole, but the schools are awfully good, the Bottega Veneta salon top notch, and the chance of being executed for treason pleasingly low.

You engage a top team of private client tax advisers and give them a short set of instructions: you are arriving in the UK on 6 April 2023 and won’t be returning home any time soon. You want to spend lots of money in the UK, pay zero tax in the UK, and declare none of your assets to HMRC.

You expect this will be very hard indeed, and so are most surprised to find that the solution fits on a postcard.

This is what it says:

You should continue to own a large and gaudy estate in Freedonia, and write an Important Note documenting the fact that you intend to spend a few years in London and then return home. This is a huge fib; but absent HMRC employing a team of psychics, they have no chance of disproving it. Ta da: you’re a non-dom.

Next, open a bank account in Honduras (which maintains strict bank secrecy and doesn’t share account information with other countries).

Before 6 April 2023, make sure you put a modest amount of money into the account, enough to fund your lifestyle for a few years – say $1bn.

The new bank account has one unusual feature – any interest earned on the account is paid into your normal account (on some other tropical island).

You then move to London on 6 April 2023. Make sure all your expenses are paid from the Honduras account. Never use any other account for UK spending.

$1bn isn’t what it used to be. What if you start to run out of money in the Honduras account? You ask someone to make you a gift, straight into that account. Where does the gift come from? Who cares! (HMRC might, but they probably won’t even find out about it.)

Mission accomplished. You can now spend lots of money in the UK, but you’ll pay zero UK tax. Your tax return will show none of your foreign income or assets.

How can this be? Poor Dania had a horribly complex tax treatment when she remitted a modest amount of money to the UK from Germany. Why don’t you have an even worse time?

Because non-doms are only taxed when they remit funds/assets to the UK. This is often abbreviated to “bringing funds into the UK” but that’s wrong – bringing stuff into the UK is only a remittance if it derives from foreign income and gains after the point someone becomes UK tax resident. The Honduras bank account is, in the jargon, a “clean” account – because everything in it derives from before the time you became UK tax resident. Gifts are also “clean”, even if made after you become UK tax resident. So you can bring in what you like and there’s no remittance, and you pay no UK tax.

And as a bonus, you don’t declare any of your foreign income and assets on your UK tax form.

You’d declare any taxable remittances – but you don’t make any.

And you’d declare any UK income and gains – but you don’t have any.

Literally all HMRC know about you is that you’re a non-dom. HMRC can’t tell you – with your $1bn of liquid assets – apart from poor Dania.

All good things come to an end, and after seven years you will have to start paying the £30,000 charge to continue to use the remittance basis, and after twelve years, £60,000. A pretty sweet deal. After fifteen years you should lose the remittance basis entirely… but there are ways round that (I’ll discuss in a future post).

So:

The non-dom regime is of little or no use to normal people, in part because of its complexity, and in part because it turns off the allowances that shield middle class people from tax on modest investment income and gains.

The non-dom regime is a simply fantastic amount of use to the very wealthy, who with a little effort can live in the UK without paying any tax. If you have a huge amount of offshore cash, it isn’t even very complicated.

What should we do about this? That’s my next post.

Tiresome caveat: none of this is legal advice. Anyone stupid enough to plan their tax affairs on this basis deserves everything they get. Any oligarchs reading this and looking for tax advice should go to this well respected independent adviser.

This was written before the Conservative Government announced the replacement of the non-dom regime.

One response to the non-dom kerfuffle is to say: let’s just burn it all down, and replace it with nothing. Tax everyone the same. This is a powerful argument, but the messiness of international tax makes it hard for me to resist the conclusion we should have some form of special, nicer, UK tax regime for recently arrived immigrants.

Here’s an example.

Take Dania, the recent arrival from Germany* in our last example, but let’s make some changes.

First, say we’ve abolished the non-dom regime, and so she’s taxed like every other UK resident.

Second, instead of having €50,000 of savings in a Luxembourg investment fund, let’s say instead her savings are instead in an extremely sensible and boring German investment fund. Again €50,000, of which €10,000 is gain.

And Dania also has a house in Lederhose she bought for €500,000 in 2014 – now worth €490,000,

After moving to the UK, Dania sells her German house and her investments to fund the purchase of a flat in London.

What happens next?

Dania probably expects the sale of her investment fund to be taxed as a capital gain, and so entirely sheltered by the annual allowance – so no tax to pay. But the UK has a complex set of anti-avoidance rules for foreign funds which only permit capital gains treatment for “approved offshore reporting funds“. Most domestic German funds don’t have this status. That means that Dania’s sale is subject to income tax and she has €4,000 of tax to pay.

Dania probably expects a capital loss on the sale of her Lederhose house. Sadly UK capital gains tax works in Sterling. The Sterling value of the house when she bought it was about £400k; the current value is £420k – so she has a CGT gain, and tax to pay, even though in reality she has a loss.

Of course if Dania has no German/foreign property at all then she’s not going to run into any of these problems; but the more she has, and the more complex her affairs, the messier things will get… and the more likely the potentially horrid UK tax treatment will put her off moving to the UK.

So there’s a good argument – from both a fairness perspective and a utilitarian one that we should have a some kind of gentler, nicer, tax regime for newly arrived immigrants. One that avoids catapulting them straight into a complicated and potentially unfair tax result, and which gives them time to think things through (and potentially move their assets into types that have a more favourable UK tax treatment). The non-dom regime is absolutely not that – it does a terrible job at this for normal people, as we saw in my first example. On the other hand, it does an altogether spectacular job for the very wealthy – as we’ll see in my next example.

Here’s a thought: how about replacing the non-dom rules with something that helps those we want to help, without giving a massive handout to oligarchs?

* If I wanted to bang the point home even more, I’d have made Dania an American citizen, subject to US taxation on her worldwide assets even when UK tax resident. But (1) it’s just a horrid, horrid mess, and I don’t have the heart to go into it, and (2) it’s the fault of America for having such a uniquely unjust system..,. not reasonable to expect the UK to twist our tax system out of shape to accommodate it.

I’ll start with something simple and try to build up. Let’s start with a normal non-dom – the kind of person most people agree we want to attract to the UK.

Example 1: Dania vs Dan- the basic case

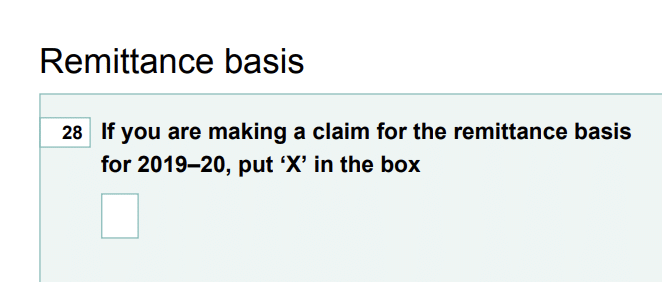

Dania is our non-dom. She was born in Germany, but moved to the UK to get experience in her profession, but sees her long term future back in Germany. So she is UK resident but German domiciled. That wasn’t a choice – it’s an automatic consequence, and it doesn’t change her income tax position one bit. Dania then ticks this box on her tax return :

That absolutely was a choice, and changes her tax position significantly.

Dania has a job in the UK and savings in the UK and is fully taxed on both. Because she’s claiming the remittance basis, Dania gets no personal allowance .

By comparison, Dan was born in the UK, has always lived in the UK. So he is UK tax resident, and also clearly UK domiciled. He has a job in the UK and savings in the UK. He is fully taxed on both (after using his personal allowance of £12,570).

Both Dan and Dania hold shares in the same Luxembourg investment fund. Dan is fully taxed on that – income tax on dividends, and capital gains tax if he sells (with an allowance of £12,300). But because Dania is a non-dom, the UK doesn’t tax her dividends and gains on the shares, provided she doesn’t bring (“remit”) the funds into the UK. She can pay the funds into her German bank account, use them to pay for holidays etc outside the UK. But bring it in, and it’s a taxable remittance.

Here’s the important thing: no other country will tax Dania’s dividends and gains on the shares. She’s not resident in Germany, so Germany won’t tax her. Nor is she resident in Luxembourg. Some countries impose withholding tax on dividends, but dividends on Luxembourg investment funds aren’t subject to withholding tax.

Note lots of people claim that the remittance rule just avoids double taxation. That’s somewhere between wrong and an over-simplification – and in this case, it’s dead wrong. The non-dom rules mean that Dania pays no tax, anywhere, on her Luxembourg investment fund.

So Dan is better off than Dania on their employment income – to the tune of about £5,000 cash (assuming they’re both 40% taxpayers). Dania is better off on her investment fund dividends and gains, which aren’t taxed at all. But actually the generous dividend allowance and CGT personal allowance means Dan won’t be taxed either, unless his portfolio becomes substantial.

Dania may be starting to think she got this one wrong.

Example 2: Dan and Dania buy a house – unrealistic example

Dan and Dania coincidentally both decide to buy a house, funding the deposit with their savings from not buying avocado toast, and by selling their substantial investment funds.

Now the unrealistic bit to make things easy: Dania bought her shares in the investment fund right before she became UK tax resident, paying €50,000. Six months later, after she’s become UK tax resident, the shares are worth €56,000 – in part because they’ve gone up in value by €5,000, and in part she received €1,000 of dividends which she reinvested.

At that point she sells the shares, and (another unrealistic bit) she has the €56,000 proceeds wired straight to her account in the UK. This is a taxable remittance, and Dania has to pay income tax on the €1,000 of dividend income – but because she’s a non-dom she doesn’t get the lower dividend rate or the dividend allowance*, so €400 of tax. Plus capital gains tax at 20% on the €5,000 of gains (with no allowance). So total tax of €1,400.

If Dan’s investment fund performed the same, he also has a gain of €5,000. But Dan will pay no tax at all, because the gain is entirely sheltered by his personal allowance.

Dania is probably shouting at her tax adviser at this point.

Example 3: Dan and Dania buy a house – realistic example

Everything is the same as in Example 2, but Dania didn’t buy the shares in the investment fund right before she became UK tax resident – she’s had them for years. The value when she became UK tax resident was still €50,000, and the value when she sold €56,000.

Now Dania has to work out all the historic gain on the shares (not just the gain during the period she was in the UK), and the taxable income on the shares (the income earned during the time she was UK tax resident). So a potentially tricky calculation, and – as there is more gain – more tax to pay.

Let’s make things more realistic still. Say Dania didn’t wire the sale proceeds straight to her UK bank, because her German broker couldn’t do that. The proceeds were paid into her German current account, which had €5,000 in at the time, and then paid straight out to her UK current account.

Because the funds mixed with other funds in Dania’s German current account, we now enter the twilight world of the mixed fund rules. Dania has to look at the €5k previously in her current account and ask: how much was was derived from income earned whilst she was UK resident?; how much was derived from capital gain whilst she was UK resident?; how much is capital (i.e. neither)? Then a priority rule is applied which basically gives Dania the worst possible tax result she could get from any combination of the funds in the account.

At this point Dania has probably paid considerably more tax than if she hadn’t claimed the remittance basis, probably lost another £5k in adviser fees, and very possibly lost the will to live.

This is why, in the real world, Dania really shouldn’t claim the remittance basis. It probably only makes sense for a “normal” person if they’re a good bit wealthier than Dania, so the remittance basis benefit eclipses the CGT allowance (probably meaning assets of well into six figures) and they positively, definitely, won’t remit a significant portion of those assets into the UK and they’re happy lobbing a few £k at a tax adviser on a regular basis.

The real world

Back in the real world, most non-doms are like Dania – it makes no sense for them to claim the remittance basis, and therefore they don’t.

How do we know this? 9.5 million people living in the UK were born abroad, so there are probably millions of non-doms. But only about 50,000 claim the remittance basis.

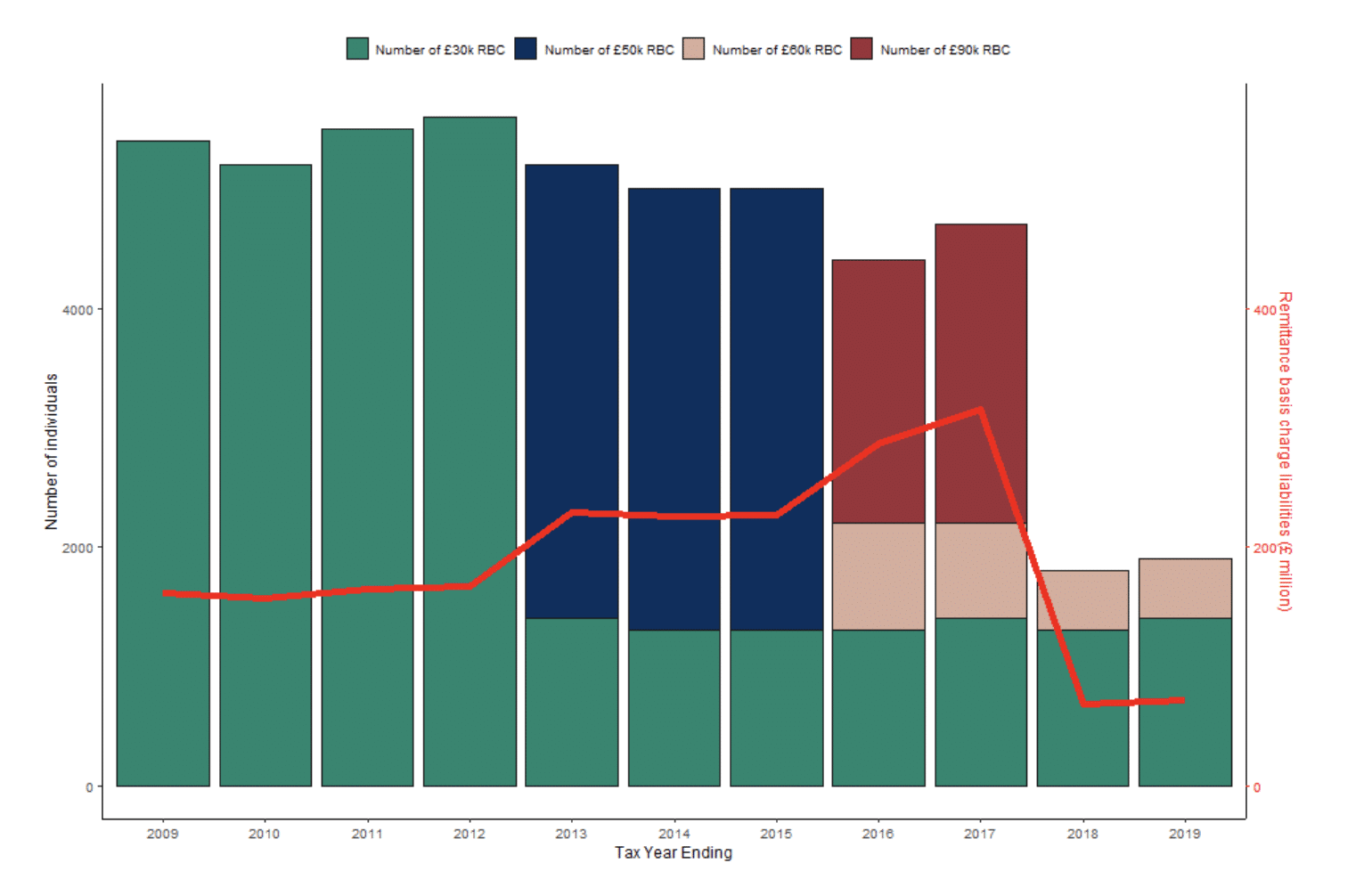

And for most of those, the benefit is pretty limited. How do we know that? Because of this chart from the ONS:

After 7 years of being a non-dom, you have to pay £30,000 a year to claim the remittance basis. After 12 years, £60,000. After 15 years, you used to be able to pay £90,000, but now you’re simply deemed UK domiciled.

Fewer than 2,000 people pay the £30,000. Telling us that there are only a few thousand people for whom the remittance basis is worth more than £30,000.

My next post looks at why we need any kind of non-dom regime. After that, I’ll look more closely at those few thousand people, and how the non-dom rules work for them. If your guess is “very well indeed” then you’re not wrong.

*many thanks to Nimesh Shah of Blick Rosenberg for correcting the initial version of this blog. I’d assumed the remittance of a dividend is taxed at the dividend rate, and benefits from the dividend allowance. Dead wrong. Unchecked assumptions are dangerous things.

Lots of people asking about the blog comment policy. I don’t have one. I was going to disable comments, and suggest people instead respond on Twitter, but some people thought comments could be useful for longer-form responses (and allegedly some people aren’t on Twitter). So I’ve enabled them for now, moderated for boring legal reasons, and will see how it goes. If the comments section becomes a ghost town I’ll remove it.

I decided, about a year ago, to retire from partnership with Clifford Chance LLP. It’s a job that I loved, and I’ve nothing but good things to say about Clifford Chance and my colleagues in London and around the world. It’s a genuinely meritocratic place, and an amazing way for people from all sorts of backgrounds, often (like mine) pretty ordinary, to reach a level of professional success that a generation ago was only available to a very few.

So I was and remain thankful for all the opportunities Clifford Chance gave me, but after almost 25 years I felt it was time to move on. My family deserves to see more of me, and I’m privileged enough to be able to make that decision. But I also felt I had a chance to use my accumulated expertise and contacts to make a difference, and achieve better tax policy in the UK and abroad. That’s what Tax Policy Associates Ltd is about. As the name suggests, it’s about tax policy, and about working in association with a bunch of different people: policymakers, academics, journalists, and others.

What’s my agenda? To improve public debate around tax policy, and improve tax policy. The two are linked. Change can’t be achieved from a purely tax-technical direction; it also can’t be achieved by gotcha stories about famous companies and celebrities avoiding tax (even when they are). It sounds trite to say we need both – but we need both.

What are my biases?

Many and varied.

I describe myself as a “tax realist”, with a firm bias towards evolution rather than revolution, and what is achievable and workable. Any tax proposal that doesn’t take account of past experience here and abroad, and which doesn’t consider likely taxpayer responses, should be DOA.

My political views have never been very well hidden – I believe the UK should have a larger and more generous welfare state, and a greater degree of redistribution, and tax should rise to pay for it. But that should be achieved with as few taxes as possible, and they should be simple and have as few exemptions as possible. Wide base, low rate.

Plenty of room for disagreement on the size of the state, and what tax rates should be – but no reason people across the spectrum can’t agree on what the taxes should be, and how they should work.

So that’s who I am, why I’m here, and what Tax Policy Associates Ltd aims to achieve. To help create better tax policy, in association with policymakers, academics, journalists – and anyone else interested in tax and improving our tax systems.