If you’re a US citizen then you pay US tax wherever in the world you live. Americans can’t escape the US tax system simply by moving abroad; they have to give up their citizenship. The Liberal Democrats and others have suggested the UK should adopt something similar: a “passport tax” on British citizens living overseas. But there would be very significant downsides, and in all likelihood, a passport tax would raise little or no revenue whilst complicating life for normal taxpayers on modest incomes.

How the UK system currently works – residence

The UK taxes individuals based on their residence. If you live in the UK for 90 days in one tax year then you are “resident” in the UK, and subject to UK tax on all of your income and gains for that year (more than 90 days if you have limited “ties” to the UK; less if you have lots of ties).12

The problem with this from some people’s perspective is that it becomes remarkably easy to stop being subject to UK tax. Simply quit the UK. Plenty of wealthy people skip the UK to move to tax havens, often just before making large capital gains.3

Whether you call this “tax avoidance” and/or think it’s immoral is a personal question on which different people will have different views. But – as long as they are really spending sufficient time abroad every year, and don’t come back within five years4, then leaving the UK is absolutely a proper, legal and 100% effective way to escape UK tax5

Some people also think it’s unfair that a British citizen living abroad pays no UK tax but can receive the benefit of British consular assistance. That is a reasonable point, but the flip side is that a foreign citizen living in the UK pays full UK tax but never receives the benefit of British consular assistance. So, it may be irrational that there is no link between consular assistance and tax, but at least this is a consistent irrationality.

The alternative – citizenship

There is an alternative: taxing, not on the basis of residence, but on the basis of citizenship. Only two countries in the world do this:6

One exception is Eritrea: it levies a flat 2% “diaspora tax” on citizens abroad. This is widely regarded as a coercive and illegal attempt to keep a totalitarian dictatorship afloat. It is not a normal tax.

The other case – and the one people normally think about when they talk about citizenship taxation – is the United States.

US citizens (and green card holders) are fully subject to US tax on their worldwide income and gains, no matter where they live. So you cannot escape US tax by moving to Panama. You can escape US tax by surrendering your citizenship – but, for wealthier individuals and higher-earners, that comes at the price of a very harsh exit tax which, broadly speaking, treats you as immediately disposing of all of your assets and subjects you to tax on those assets. This essentially eliminates all the immediate benefit of escaping US taxation.7

There is no other developed country that taxes on this basis.

On the face of it, if you want to stop billionaires from leaving the UK and escaping UK tax, this is the approach you’d want to adopt. However, there are significant practical and technical difficulties.

(You may, alternatively, regard such an approach as immoral, and think that no country has the right to tax people who want to leave – but I’m going to park such political questions and look at the practicalities)

The practical difficulty

The immediate practical difficulty created by citizenship taxation is that you end up paying tax in two places. A Brit living in France would pay UK tax (because they are a British citizen) plus French tax (because they are resident in France).

On the face of it, this shouldn’t be a problem, because the UK has double tax treaties with France and most other countries. Double taxation treaties are agreed between countries to ensure that their resident individuals and companies pay tax only once if they are potentially subject to tax in both countries. They are an important part of international law, without which travel, trade and investment would be greatly complicated.

These treaties in principle stop you from being taxed twice on the same income. And certainly in a simple case, for example if you are a US citizen living in the UK and have £100 of income, then the US and UK won’t both apply their full rate of tax to that income. The problems, however, go beyond simple double taxation.

We can get a sense of the issues by looking at the difficulties currently faced by US citizens (subject to US worldwide taxation) who live in and are resident in the UK (and therefore subject to UK worldwide taxation):

- The US has the “foreign earned income exclusion” for the first $132,900 of earned income for citizens living abroad (that’s the figure for the 2026 tax year).8 Even if this covers all of your income, you still have to file a US tax return.

- If your income goes above $132,900, or you have income other than earnings, then you have to file two complete tax returns – and pay tax – in two countries. Those tax returns have different rules for e.g. what is deductible and what isn’t. The upshot is that you are almost guaranteed to pay more tax than your peers in either the US or the UK – you essentially get the worst result from each system for every income/expense that you have. And you’ll need to prepare two tax returns which interrelate.

- Things are further complicated by the UK’s unique 6 April tax year, which means the US and UK tax returns aren’t just prepared on a different basis, but also cover different dates.9

- There are separate complications around the interaction between US Social Security rules and UK Social Security rules. This is – most of the time – not an issue for US citizens living in the UK because there is a Totalization Agreement which means a self-employed person resident in the UK pays UK Class 4 National Insurance and, on producing a certificate of coverage, is exempt from the US self-employment tax. However there are many countries where there is no such agreement, and US citizens living there face a complex and expensive interaction between two sets of social security rules – for example India, Singapore, the United Arab Emirates, and Israel.

- Capital gains present potential unfairness, because the US taxes you on your US dollar gains. For example: say you buy a house in the UK for £300k and sell it a few years later for the same price. No UK capital gain. But if Sterling appreciated over that period, so that the dollar purchase price was $380k but the dollar sale price was $450k, then you have a $70k US capital gain, but no cash proceeds to fund it. And the UK will do the same to your US assets.

- If you make a capital gain then the different filing and payment timetables mean that you’ll sometimes have to pay the full US tax, then the full UK tax, then claim a refund of the US tax.10

- This complexity impacts couples. If a couple have a joint account, and one is a US citizen and the other is not, then the joint account becomes subject to US tax. Married couples can normally not worry about the tax treatments of their family finances – but where one of the couple is a US citizen then even simple arrangements like joint accounts become very complicated.

- Many people in the UK have an ISA, where you can put cash or shares into an account and the return is exempt from tax. But it’s not exempt from US tax. So a US citizen living in the UK cannot use an ISA (or, to be more accurate, if they use an ISA they get no benefit from it). Some US advisers think it’s worse than that, and an ISA has a particularly awful US tax treatment: that’s a whole other class of problems that arises when one country’s tax system has to characterise the tax effect of another country’s legal and tax system.11

- You always get the worst of both worlds. For example, the US and UK take the opposite approach to the taxation of your house. The UK gives you no tax relief on your mortgage payments, but exempts you from capital gain on the value of the house. The US gives you tax relief on mortgage payments, but then taxes the capital gain. Both are somewhat balanced results. A US citizen living in the UK gets the worst of both worlds. They get no tax relief on the mortgage for their UK tax, but have to pay US capital gains when they sell. That’s an unbalanced result.

- It becomes very difficult to buy investment funds. The UK has rules that in practice mean no UK resident can buy an investment fund unless it is either established in the UK, or foreign but an “approved offshore reporting fund”. The US has rules that in practice mean it is very disadvantageous for a US citizen to invest into a non-US fund (the PFIC rules).12 A US citizen living in the UK is subject to both sets of rules, and therefore, realistically, can only invest in funds that are approved by both the US and UK authorities. There are very few funds like this.

- There’s an obvious incentive for US citizens abroad to simply not declare or pay their US taxes. That’s a criminal offence, but historically it was very hard for the IRS to spot. A whole international reporting regime – FATCA – was introduced to stop this. But that imposes a significant admin burden on non-US financial institutions with US citizen clients and, as a result, some banks don’t allow US citizens to open accounts.13

- There are many more issues. Tax on gambling/lottery winnings. The impact on minors. “Accidental Americans”.14 Retirement account taxation.15 Inheritance/estate tax interaction.16 Complexity when couples divorce. You don’t need to be wealthy, or to have complex personal finances, to have a horrible time navigating the US and UK tax systems at the same time.

- All this means that Americans with modest assets living in the UK will frequently spend much more in tax accounting fees than in actual cash US tax. Filing tax returns in two countries is complicated. You certainly can’t pay a few hundred pounds for a high street accountant to complete your US and UK tax returns – you’ll need more specialised and expensive advisers, and should expect several thousand pounds’ costs at a minimum. I know an American living in the UK who had no income one year (in either country) but a $5k capital gain – filing US taxes for that year cost them $3k.

These are unfair outcomes for normal people, particularly people who can’t afford lots of tax advice. Billionaires can cope with it; doctors and IT workers find it much harder:17

So if the UK adopted citizenship-based taxation then you might regard that as a “win” for taxing the very wealthy. But it would hurt many ordinary people who choose to live abroad.

The technical difficulty

Say we decided that we didn’t care about these issues, and we wanted the UK to impose citizenship taxation anyway. The surprising answer is that we couldn’t, because our double taxation treaties would prevent it.

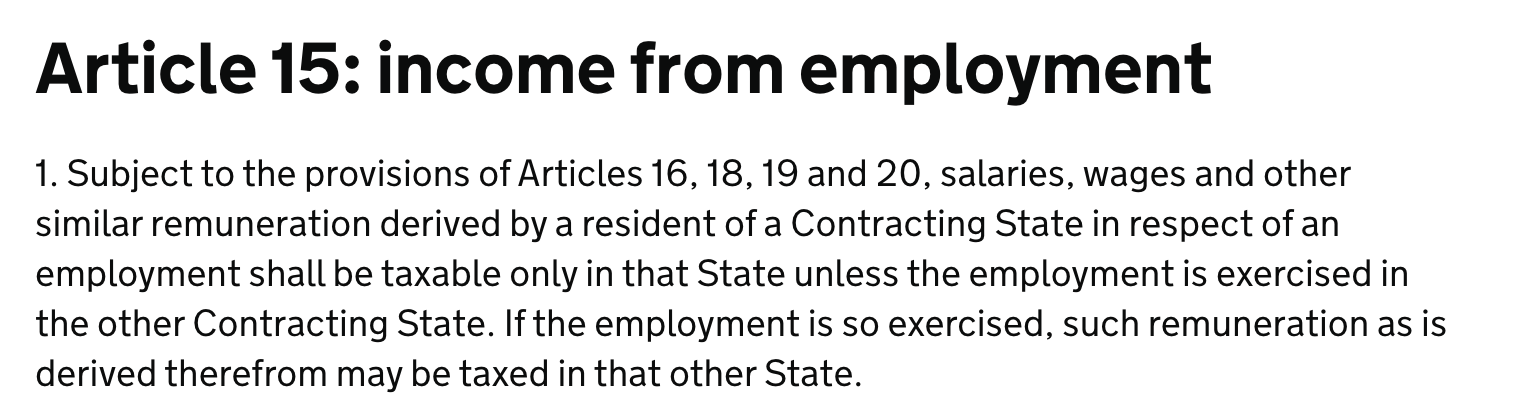

A key element of these treaties is that if someone is resident in a country, then only that country gets to tax their income. For example, the UK/France double tax treaty says:

This means that a French citizen who is resident in the UK and working in the UK is only subject to UK tax. France cannot tax them. Similarly, a British citizen living in France is only subject to French tax.

The consequence of this is that, if the UK was to introduce citizenship-based taxation, then that would not apply to British citizens living and working in France. And the UK has similar treaties with many other countries, including popular expat destinations like Singapore and Dubai. The UK therefore cannot introduce citizenship-based taxation within the framework of our existing treaty obligations.

This isn’t a problem for the United States because the United States always negotiates a “saving clause” in all of its treaties. Here, for example, is the saving clause in the US/UK double tax treaty:

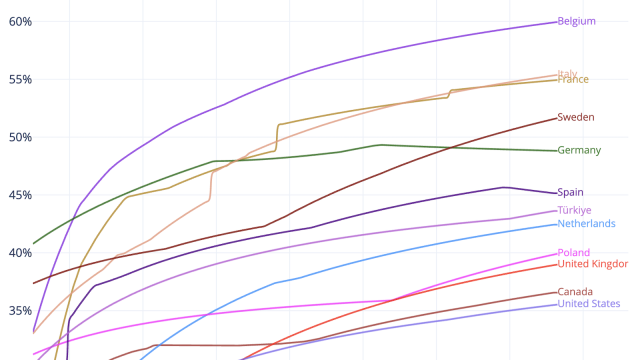

The UK, of course, hasn’t done this because it didn’t need to. In principle, the UK could start negotiating amendments for all of its treaties to add a saving clause – but the UK has around 130 treaties:18

Even amending just the most significant treaties would be a massive undertaking, taking years – and many countries would not agree to such a change, or (even if the Government agreed) its legislature would not ratify an amended treaty.

Part of the difficulty achieving treaty amendments would be political self-interest. Why would another country agree to this amendment when it would reduce its ability to attract UK expats?

It’s also hard to overestimate the procedural/constitutional difficulty. It’s very simple for the British government to enter into and then ratify a tax treaty. It can simply lay the treaty before Parliament. In most other countries, the procedure is more complex, often involving lengthy legislative procedures, and in some cases, like the US, a supermajority.19 In recent times, getting any treaties ratified by the US Senate has proved extremely difficult:2021

So ironically, the US, the exemplar of citizenship-based taxation, could well be a significant obstacle to the UK adopting citizenship-based taxation.

The UK could simply ignore its treaties and tax its expats regardless of what the treaty says (sometimes called a “treaty override“). The nature of international law means that there is no court that would stop the UK breaking its treaties, but such an act is unlikely to be viewed positively by other countries, who may then start breaking their own treaty commitments with the UK.22 The UK would also find it hard and, in many cases, impossible, to enforce its taxes extra-territorially if it has imposed them in breach of international law.23

Or the UK could abandon its treaties – but the adverse impact on British individuals and businesses would be significant.

The boring technical answer is therefore that the UK cannot, in practice, impose US-style citizenship-based taxation without renegotiating or overriding its treaty network, neither of which is practical. It could only apply cleanly to people living in countries which attract tax exiles, but with which the UK has no relevant tax treaty – Monaco, for example.

What if we only target tax havens?

What if we accept this limitation, and introduce citizenship-based taxation narrowly focussed on people who move to tax havens like Monaco?

This might be a workable solution if the only tax havens were Monaco and other easily-identifiable city-states and small islands. However, in reality, there are many “normal” countries that behave exactly like tax havens for Brits who move there. Singapore, Israel, Portugal, even Italy, don’t tax, or barely tax, the income of a wealthy Brit who moves there – but the UK has double taxation treaties with each one.24

So, whilst we could technically limit a new rule to Monaco, the Cayman Islands and other tax havens where we don’t have tax treaties, tax exiles would just emigrate to different countries. The change would achieve little or nothing. We’d create a lot of additional tax machinery for a small net yield.

So how much tax could the UK raise from citizenship-based taxation?

New tax revenue would be very limited.

The seriously wealthy would either renounce their citizenship before the rules came in or, more likely, move to a country with an appropriate double taxation treaty where they would be unaffected by the change.

That would leave some people in countries (like Brazil) without UK double taxation treaties who would pay additional tax and face additional administrative cost. They would not be the very wealthy – just expats and “accidental Brits”. So this would generate some limited revenue, but at a personal and financial cost for those individuals that I would regard as unfair.

On the other hand, the UK would need to build machinery to monitor and collect tax from its expatriates, and that would be a significant undertaking.

Then, more significantly, we would face wider consequences from taking a step most people would regard as pointless and unfair. Fewer people would arrive here, and fewer people would take up citizenship (particularly professionals, who’d be worried about the life-long financial consequences).

It is very plausible that all of this means that the overall result would be little new revenue, lots of cost, and a net loss in revenue.

So why does the US keep citizenship taxation?

If citizenship-based taxation is this unfair, this complex, and this unusual, the obvious question is why the US persists with it – and why it’s the only developed country that does? The answer is a combination of history, inertia, power and self-interest. None of those four things applies to the UK.

First, the US taxes its citizens abroad because it always has. Citizenship-based taxation isn’t a clever piece of modern design – it’s a relic of the Civil War, when Congress first taxed Americans living abroad on their worldwide income. The Supreme Court blessed the principle a century ago and has never revisited it.25 The inertia of the US legislature means that dislodging a rule that old is extraordinarily hard.26

Second, the US has more to lose than anyone from letting people leave. It is home to more of the world’s ultra-wealthy than any other country – by a wide margin, and still comfortably ahead of China:27

Those people would have every incentive to shed US tax if they could simply move abroad – and citizenship-based taxation, backed by the exit tax, is what stops them doing so cheaply. And renouncing US citizenship carries real practical and reputational costs.

Third – the mirror image of the UK’s problem – the US already has the machinery in place. Every US tax treaty already contains the “saving clause” that preserves its right to tax its own citizens. The US built its entire treaty network around citizenship-based taxation decades ago, so it never has to renegotiate anything. The UK, as we’ve seen, would have to reopen some 120 treaties to achieve the same thing. The US enjoys the benefit of a head start it locked in generations ago.

Fourth, and most simply: the US can get away with it. The depth of its capital markets, the reserve-currency status of the dollar, and the sheer gravitational pull of its economy mean the US attracts talent and capital despite its tax system. A deeply uncompetitive feature like citizenship-based taxation therefore imposes no visible cost – the entrepreneurs and investors keep coming anyway.28 A mid-sized open economy has no such margin for error. If the UK or France adopted citizenship-based taxation, the effect on their ability to attract new arrivals – the entrepreneurs, founders and investors every advanced economy competes for – would be immediate and obvious. What is a hidden cost for the US would be a highly visible own-goal for us. And what is a steady-state for the US, with a relatively small number of renunciations per year, would be a very large effect before any new rules came in:29

The obvious point: none of these are principled arguments for citizenship-based taxation. They are accidents of history, inertia, size and power – explanations for why the US is stuck with a bad policy, not reasons for anyone else to copy it.

The wrong question

The costs and downsides of citizenship-based taxation are considerable, and have been known for a hundred years – even if they are universally ignored by those calling for the UK to adopt such a system.

I tend to think that, when it comes to taxing the wealthy, citizenship-based taxation is a distraction. In the end, it’s not citizenship-based taxation that makes it very difficult for very wealthy Americans to escape US tax – it’s the US exit tax. If the UK adopted an exit tax, then citizenship-based taxation would be unnecessary. If, on the other hand, the UK adopted citizenship-based taxation without an exit tax, we wouldn’t stop the very wealthy escaping tax.

I regard the exit tax arguments as nuanced, and I am not convinced there is a clear answer. There are really two ways to look at this:

- The first is that we should continue to permit people to emigrate and immediately escape all UK tax. Some believe this on the principled grounds that everyone has a right to vote with their feet; others on the pragmatic grounds that people may be less likely to come here, and entrepreneurs less likely to stay, if we hit them with a large tax bill when they leave.30

- The other is to say that in some cases, where a person has accrued lots of untaxed capital gain during their time in the UK, the UK should have a right to tax it if they leave. In other words, we should have an exit tax.

I wrote more about exit tax complexities here.

But whatever view we take on exit taxes, I regard citizenship-based taxation as unfair and unjust. There are many features of the US tax system the UK should not copy. This is one of them.

Photo by James Giddins🔒.

Footnotes

It’s a bit more complicated than that, but these days the rules are fairly clear and sensible. KPMG have published a very nice flowchart. ↩︎

Unless you are the modern equivalent of a “non-dom”, which is a whole other story ↩︎

It’s occasionally claimed that people don’t move in response to higher tax rates. Most of this is based on studies of people moving from relatively highly taxed US States to relatively low-taxed states. It’s not applicable to the very wealthy moving to tax havens, which is hard to study statistically (too few people) but very easy to assess empirically (there’s no other reason a Brit would choose to live in Monaco) ↩︎

Under the UK’s temporary non-residence rules: if you leave, realise gains or certain income while non-resident, and then return within roughly five years, some of that income and gain can be dragged back into UK tax in the year of your return. The rules are designed to stop people taking a short “tax holiday” abroad to crystallise a gain and then coming home – something that was possible, and even straightforward, before 2013. ↩︎

There are exceptions. Everyone in the world, no matter where they’re resident, is subject to UK income tax, UK capital gains tax, and stamp duty land tax (or its devolved equivalents), on holdings/acquisitions of UK land. And everyone is subject to UK inheritance tax on their UK situs assets. A complication specific to people leaving the UK is that whilst you will cease to be UK tax resident more or less immediately, you will continue to be subject to UK inheritance tax on your worldwide assets for some time. ↩︎

Country boundaries: the public-domain Natural Earth world dataset. ↩︎

The exit tax only applies to “covered expatriates” — broadly, those with a net worth of $2m or more, or an average US income-tax bill over the previous five years above an inflation-adjusted threshold ($206,000 for 2025), or who cannot certify five years of US tax compliance. For those people, section 877A treats all their worldwide assets as sold the day before they expatriate, but the resulting gain is reduced by an exclusion of $890,000 (2025 figure, uprated annually). So a wealthy individual faces a real cost, but many ordinary citizens can renounce at little cost – the separate State Department renunciation fee was reduced from $2,350 to $450 in April 2026. ↩︎

The exclusion is uprated for inflation each year: for 2025 it was $130,000, claimed on IRS Form 2555. Crucially it only covers earned income — wages and self-employment profits — and does nothing for investment income, dividends, rent or capital gains. There is also a separate foreign housing exclusion. An alternative to the exclusion is the foreign tax credit (Form 1116), and in a high-tax country like the UK most expatriates are better off claiming the credit than the exclusion. The fact this footnote discusses three separate exclusions is an indication of how complex things can get, even in a simple case. ↩︎

The 6 April start date is a historical accident. Until 1752 the English tax year began on Lady Day, 25 March (and the reasons for that are fascinating and merit their own article). When Britain switched from the Julian to the Gregorian calendar in 1752, eleven days were dropped, and to avoid the Treasury losing eleven days of revenue the year-end was pushed forward – first to 5 April, then (after a further Julian leap-year adjustment in 1800) to the modern 6 April start. HMRC has periodically looked at moving it to 31 March or 31 December, but never done so – the transitional costs for HMRC and taxpayers would be substantial, and the benefits are much harder to pin down. ↩︎

This is a cash-flow and mechanics problem more than true double taxation. Relief for the other country’s tax is given as a credit, but a credit can generally only be claimed once the foreign tax is actually paid or accrued, and the US and UK tax years and payment dates do not line up (see the 6 April point above). So the taxpayer can be out of pocket for a year or more while a refund is processed, and can even face interest or penalties in one country for tax that is ultimately relieved in the other. ↩︎

Some advisers argue an ISA can be treated as a foreign trust, triggering the punitive Forms 3520 and 3520-A. At best a US citizen’s ISA is a UK-tax-free wrapper that the US taxes normally; at worst it is an actively harmful structure. The same problem affects the Lifetime ISA and Junior ISAs held for US-citizen children. ↩︎

The Passive Foreign Investment Company regime (sections 1291–1298) is deliberately punitive: absent a timely election, gains and “excess distributions” from a non-US fund are taxed at the highest marginal rate with an interest charge for each year of deferral, and the annual reporting on Form 8621 is onerous. Almost every ordinary UK unit trust, OEIC or investment trust is a PFIC. The practical result is that a US citizen in the UK is squeezed between the UK’s offshore reporting-fund rules and the PFIC rules, leaving a very small overlap of funds that are efficient under both systems. ↩︎

Under FATCA, foreign banks must identify and report US-citizen account holders (in the UK, via an intergovernmental agreement with HMRC) or face a 30% withholding tax on their US income. Faced with that compliance burden, some banks and investment platforms simply “de-risk” by refusing US-citizen customers. Separately, US citizens must themselves report non-US accounts over $10,000 on an annual FBAR (FinCEN Form 114), with severe penalties for non-filing — a duty that catches people who owe no US tax at all. ↩︎

An “accidental American” is someone who is a US citizen — usually by being born on US soil, or to a US-citizen parent — but who has little or no connection to the US. They are nonetheless subject to full US worldwide taxation and reporting. The best-known UK example is Boris Johnson, born in New York, who faced a US capital gains tax bill (reported at around $44,000) on the sale of his London home – which was exempt from UK tax as his main residence – initially refused to pay, calling it “outrageous”, then paid, and eventually renounced his US citizenship in 2016. ↩︎

Retirement saving is where tax systems are most nationally specific, so cross-border citizens face particular complexity. The US/UK treaty contains specific pension articles that prevent the worst outcomes, but only up to a point: employer contributions that are tax-free in one country can be taxable income in the other, the UK’s tax-free pension lump sum is not always recognised by the US, and self-invested pensions can fall foul of the US rules on foreign trusts and PFICs. ↩︎

The US taxes the worldwide estates of its citizens on death, and it interacts badly with UK inheritance tax: the two have different rates, thresholds and, critically, different spouse reliefs. A transfer between spouses is normally tax-free in the UK, but the US estate tax only gives an unlimited marital deduction where the surviving spouse is a US citizen — so mixed-nationality couples can be taxed on death in ways a same-nationality couple never would be. The UK/US estate and gift tax treaty exists precisely because these systems collide so badly. This issue is of more limited importance now than it was in the past because of the very high threshold at which US estate tax starts to apply – $15m. ↩︎

The table summarises the rules discussed above and is necessarily simplified. Mortgage interest: the US allows a deduction for a main residence (IRS Publication 936); the UK gives homeowners no relief. Main home: the UK exempts it from capital gains tax under private residence relief, whereas the US taxes gains above a $250,000 / $500,000 exclusion — and computes the gain in US dollars, so currency movements can create a “gain” with no economic profit. ISAs are UK-tax-free but not recognised by the US (and may be caught by the PFIC or foreign-trust rules). Ordinary funds must be both a UK reporting fund and outside the US PFIC regime — very few qualify. Pensions get partial protection under the US/UK treaty but can still trigger foreign-trust reporting. ↩︎

The map shades every country with which the UK has an income-tax double-taxation treaty in force. The year shown when you hover is the year the current treaty (or its most recent protocol) was given effect in UK law by an Order in Council – the UK’s own act of ratification, and a close proxy for the treaty’s entry into force. Compiled from the “Double Taxation Relief” Orders in Council on legislation.gov.uk (1949–2025); precise entry-into-force dates are on the per-country gov.uk tax-treaties pages. Where a treaty is inherited by successor states it is shown for each — for example the Czech Republic and Slovakia under the 1990 UK–Czechoslovakia convention (in force 20 December 1991), and Serbia, Montenegro and Bosnia and Herzegovina under the 1981 UK–Yugoslavia convention. A handful of jurisdictions with UK treaties are not shaded — Gibraltar, Guernsey, San Marino, the British Virgin Islands, Kosovo, Hong Kong and Taiwan – because the base map does not draw them as separate territories; in any event most are small enough that they would be barely visible at this scale. Country boundaries: the public-domain Natural Earth world dataset. ↩︎

In Switzerland and Liechtenstein there is even the possibility of a referendum being required to ratify a tax treaty. ↩︎

Both traces count income-tax treaties plus their protocols/amendments by year. United Kingdom: every Order in Council giving domestic effect to a treaty or protocol, from legislation.gov.uk (the “Double Taxation Relief” Orders), by the year the Order was made — the UK’s act of ratification. United States: the general effective date of each treaty/protocol from IRS Table 3. The two are measured slightly differently — the UK by its implementing Order, the US by effective date – but both approximate the year of ratification. The UK’s spikes in 1968 (26) and 1980 (19) are largely mass re-makes of existing agreements, many with Commonwealth territories, rather than brand-new treaties. UK data begins in 1949 (legislation.gov.uk does not carry earlier Orders); estate-and-gift and shipping/air-transport agreements, and purely domestic relief regulations, are excluded from both series. ↩︎

The near-total gap from 2011 to 2018 reflects a near-decade-long hold by a single senator, Rand Paul, broken only by the batch of protocols the Senate approved in 2019 (in force 2019–2020). The one 2024 entry is Chile, which was signed back in 2010. Estate-and-gift-tax instruments are excluded, as are treaties signed but never ratified (e.g. Hungary and Poland). Because Table 3 lists only treaties in force, superseded earlier treaties are not shown, so the chart slightly understates activity in the 1950s–1970s. This history means that some treaties remain held up and unratified (and not just tax treaties), but the bigger effect is that US administrations simply don’t sign many new treaties or protocols because they know that ratification is so difficult. The current US tax treaty backlog appears to be small but very old. The two bilateral income tax treaties actually sitting in the Senate are the Hungary treaty, signed in 2010, and the Poland treaty, signed in 2013. There is also a pending protocol to the multilateral Convention on Mutual Administrative Assistance in Tax Matters. Separately, the US has signed but not yet brought into force a new treaty with Croatia, now accompanied by a 2026 protocol; PwC says the protocol was intended to resolve Senate concerns over the double-tax-relief article. The 2015 Vietnam treaty is also signed but not in force, and Bloomberg Tax reports that Treasury is now looking to update it. ↩︎

In many countries, treaty overrides are not constitutionally possible. In the UK they are not only possible, but trivial – because, under our dualist system, Parliament can legislate contrary to a treaty and the domestic courts will apply the later statute. The doctrine of Parliamentary sovereignty means that nothing restrains Parliament from overriding a treaty. But doing so would breach the UK’s obligations under the treaty and under the Vienna Convention on the Law of Treaties (a state cannot invoke its own internal law to justify non-performance). These issues are minimal, and perhaps non-existent, for many current treaty overrides, because they are anti-avoidance rules, which it can be argued are clarifying the operation of a treaty rather than really overriding it. A savings clause is a very different matter. ↩︎

As an aside, tax treaties provide an entertaining reversal of common political positions. We see people on the Left – often horrified by breaches of international law – being extremely blasé about breaches of tax treaties, and people on the right – often blasé about international law – regarding tax treaties as sacrosanct. I won’t take a position on this other than to note the practical consequences of breaching tax treaties. ↩︎

it’s fair to say that the regimes in Portugal and Italy are much more fragile than a “proper” tax haven. Portugal closed its non-habitual resident regime to new applicants at the end of 2024 (replacing it with the narrower IFICI incentive), and Italy’s flat charge on foreign income for new residents has risen from €100,000 to €200,000, and to €300,000 for those arriving from 2026. These countries are not immune from the same revenue pressures that the UK currently faces, and so the direction of travel is towards increased tax on expats. But they still tax an incoming wealthy Brit far more lightly than the UK would. ↩︎

The US taxed the worldwide income of citizens living abroad from the Revenue Act of 1862 onwards; the 1864 Act taxed Americans resident abroad at a higher flat rate than those at home – reportedly, in part, to discourage the wealthy from sitting out the war in comfort overseas. The constitutionality of taxing a citizen on foreign-source income while permanently resident abroad was upheld by the Supreme Court in Cook v. Tait, 265 U.S. 47 (1924), on the theory that citizenship itself confers a benefit the government may charge for. For a modern critique of that reasoning, see Ruth Mason, “Citizenship Taxation”, 89 S. Cal. L. Rev. 169 (2016), and Tsilly Dagan and Ruth Mason, “Reconsidering Citizenship Taxation” (2025). ↩︎

Changing US tax law needs the House, the Senate and the President all pulling in the same direction – something that happens rarely, and usually only when a president is willing to spend serious political capital, as with the 2017 tax reforms. Nobody is willing to burn that capital to make life easier for expatriates, who are scattered thinly across every state and congressional district and vote as no one’s constituency. So proposals to switch to residence-based taxation keep being introduced, and keep going nowhere. The most recent serious attempt is Rep. Darin LaHood’s Residence-Based Taxation for Americans Abroad Act (H.R. 10468), introduced in December 2024. It lapsed when the 118th Congress ended in January 2025 and, as of 2026, is being reworked for reintroduction, held up in part by the need for a Joint Committee on Taxation revenue score – even though ending double taxation of Americans abroad reportedly has the President’s support. Advocacy groups such as American Citizens Abroad have been pressing the point for decades. The State Department estimate is that around nine million Americans live overseas – a large number of people, but not an organised electorate. ↩︎

The 2025 Forbes billionaires list counts 902 billionaires in the United States, against 450 in mainland China (516 including Hong Kong) and 205 in India. On any measure the US is the single largest concentration of mobile private wealth on earth. ↩︎

This is not to say the cost is zero. The academic literature is clear that citizenship taxation does disadvantage the US in competing for globally mobile talent – see Michael S. Kirsch, “Taxing Citizens in a Global Economy”, 82 N.Y.U. L. Rev. 443 (2007), and Mason, “Citizenship Taxation” (2016), who argues the policy handicaps the US in the competition for skilled migrants. The point is that the US is large and attractive enough to absorb that cost without it showing. Or if we want to be more cynical, the invisible nature of the cost means that there is no impetus for change. ↩︎

Source: the US Treasury’s “Quarterly Publication of Individuals Who Have Chosen To Expatriate” in the Federal Register, aggregated to annual totals (compiled by, among others, Wikipedia and the tax lawyer Andrew Mitchel). These are “published expatriates” — mostly citizens who formally renounced, plus certain long-term green-card holders who gave up US residence; the lists are widely thought to under-count. The dashed line marks the 2010 enactment of FATCA, which took effect from 2014; the 2020 figure of 6,705 is the highest on record, and (we expect) driven by pandemic-era relocations. ↩︎

The US doesn’t have an obvious problem with that, but this arguably goes back to the uniqueness of the US. ↩︎

Are UK workers over-taxed? The answer in four infographics

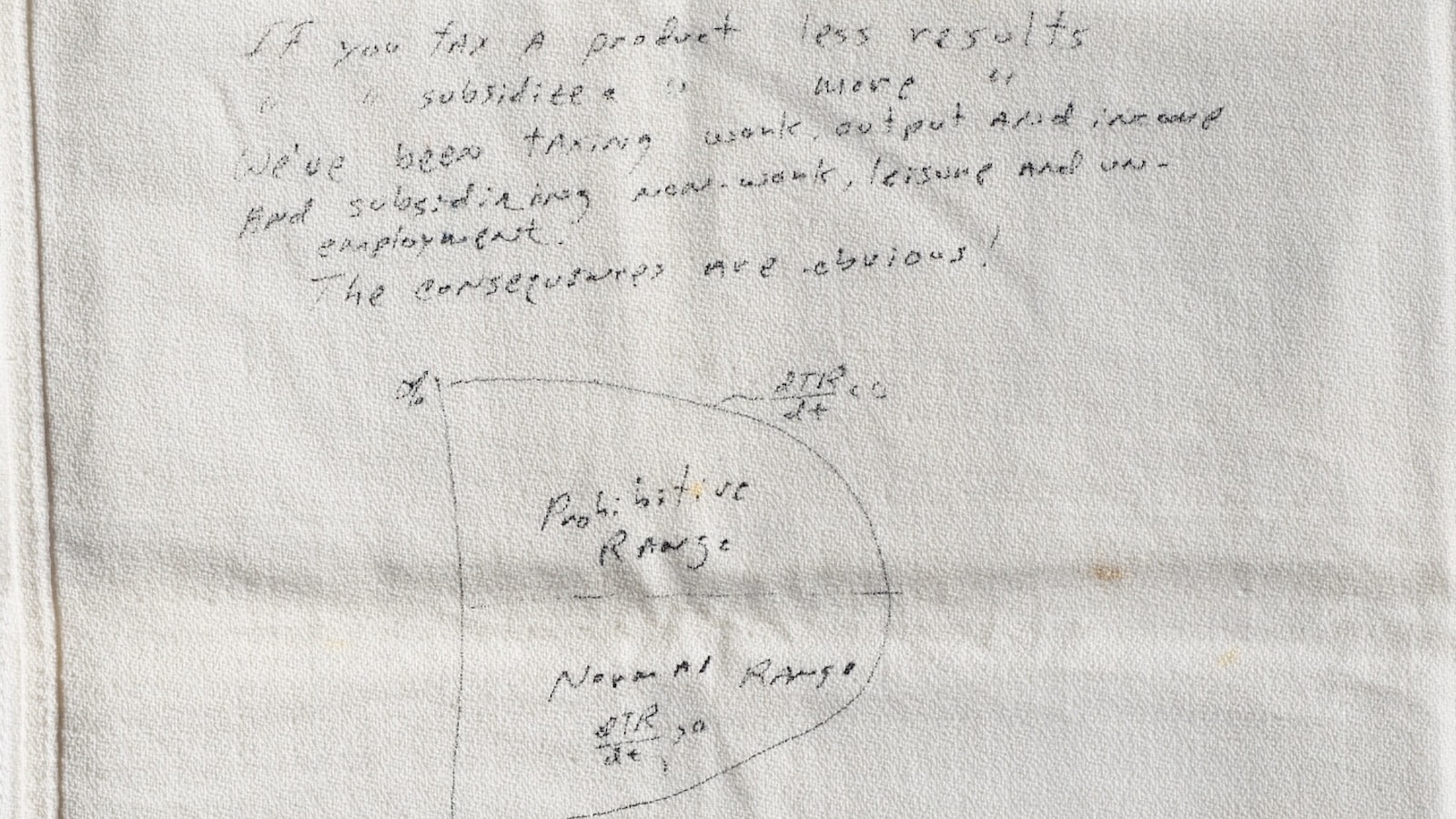

Untaxing – The Laffer curve, and the napkin that changed the world

Tax cuts and tax rises: do tax cuts pay for themselves?

The tax longlist – 35 ways Rachel Reeves could raise £22bn

Half the British public doesn’t understand income tax – new data

Leave a Reply