The Royal Household has, for the first time, disclosed how much voluntary “tax” the King pays: £12.9m for 2024/25, £11.7m for 2023/24, and a little over £5.4m for the six months of 2022/23 in which he was King.1 The documents also continue the practice of disclosing the Prince of Wales’ tax: £7.76m for 2024/25, £8.34m for 2023/24, and approximately £4m for the six months of 2022/23 in which he was Prince of Wales.

This looks like transparency. It isn’t. We get three numbers for the King and three numbers for the Prince. We don’t get the calculations, the income figures, the deductions, the expenses, the treatment of private investments, or any explanation of how “official” and “personal” expenditure are separated. We knew it wasn’t real tax; it’s not real transparency either.

Still, the numbers are not entirely useless. They let us do one thing the Royal Household has not done: put a conservative lower bound on the King’s private income and gains. And they point to a more basic problem with the Prince of Wales: why is he paying voluntary “tax” at all, rather than normal statutory tax like everybody else?

I should say up-front that my view on these issues is coloured by two opinions that others may not share:

- I think the monarchy is preposterous and unjustifiable, and we should definitely keep it. Partly because the monarchy ties us to our history; mostly because the alternatives are worse.

- I don’t like the fake transparency that we get from some public figures about their taxes. Every year the Prime Minister and Leader of the Opposition trumpet that they are publishing their tax returns, but they are not. They publish a bowdlerised summary which omits anything of real worth. The King’s “transparency” seems even worse.

The documents are all now online: the Royal Household’s Royal Finances paper and Sovereign Grant annual report, and the Duchy of Cornwall’s integrated annual report.

Also relevant: the Duchy of Lancaster’s 2024/25 annual report and accounts, published last summer, and the one-page Sovereign Grant summary.

How do the King and Prince of Wales pay tax?

The answer for the King is simple: he doesn’t.

Income tax, capital gains tax and inheritance tax are all imposed by statutes that don’t bind the Crown, so the Sovereign isn’t within the charge.2

The King pays voluntary “tax” anyway. This odd arrangement dates to 1992 – the Queen’s “annus horribilis” – when there was a medium-sized kerfuffle around the cost of rebuilding Windsor Castle. After much internal debate within the Government, the then-Prime Minister announced that the Queen and the then-Prince of Wales would begin paying income tax and capital gains tax on a voluntary basis. The terms were set out in a Memorandum of Understanding with the Treasury.3 The Memorandum of Understanding was rewritten for the new reign in 2023, with Charles paying tax on the same basis as his mother.

But this voluntary “tax” is not much like real tax.

Most of the King’s private income comes from the Duchy of Lancaster – which publishes accounts. But he also has private investments which are not disclosed at all. The King pays income tax on his private income only to the extent it isn’t used for official purposes, and capital gains tax on his private assets – but never on the Duchy of Lancaster’s capital.

The Prince of Wales pays income tax (but not capital gains tax) on the Duchy of Cornwall’s surplus, again after official expenses, plus income tax/capital gains tax on his personal assets.

Nothing that passes from one monarch to the next bears a penny of inheritance tax.4

Both Duchies – and the Sovereign Grant – publish audited accounts each year (and have done for some time). There are some interesting numbers in these documents. The Duchy of Lancaster reported a surplus of £24.4m for 2024/25; the Duchy of Cornwall a distributable surplus of £21.55m for 2025/26.5

How much private income does the King have?

We can come up with a lower bound estimate by reversing out the figures that we know.

The King and some of his family are supported by the Sovereign Grant. In 2024/25 that amounted to £86.3m.6 This is to cover official expenses and is not subject to the voluntary “tax”. So this doesn’t help us.

We know from the Duchy of Lancaster’s 2024/25 accounts that the Duchy made a £24.4m surplus. This is taxable7 after the deduction of official expenses of the King, and any official expenses of other members of the royal family which he covers. To say that the Royal Family’s boundary between “official” and “personal” is unclear would be an understatement.

The King has other private income and gains from his own investments. The Royal Household’s Royal Finances paper confirms the King has a “personal investment portfolio”, managed on a discretionary basis, plus private estates. The size of these investments, and the income they generate, are not disclosed.

However we can, with some confidence, put a conservative lower bound of £4.2m on the King’s income and gains from his personal investment portfolio. Here’s my reasoning:

- Let’s assume that the King claims no deductions for his expenses (or those of other members of his family).

- The £24.4m from the Duchy of Lancaster then results in a maximum of £11.0m of tax (if taxed at the 45% rate).8

- There is therefore a £1.9m “gap” between the tax on the Duchy of Lancaster income and the £12.9m of tax he paid.

- The £1.9m “gap” represents a minimum of £4.2m of income (if taxed at the highest rate, 45%).

The lower bound is helpful because it involves no speculation. Once we start speculating, the figure can only get higher. For example:

- Let’s say the King claims a relatively modest £2m of expenses: that means we are “missing” at least £2m of income, so his total private investment income/gains will be at least £6.2m.910

- Then continue to guess/hypothesise that the King has £2m of expenses, but assume his private income is comprised of £3m of capital gains and (for the rest) dividend income. Then his total income/gains must be £8.4m.11

Other than calculating that £4.2m lower bound, we can say precisely nothing about the King’s private income. We can say nothing about the King’s expenses.

Why doesn’t the Prince of Wales pay tax like a normal person?

It’s clear why the King and Duchy of Lancaster don’t pay income tax, capital gains tax or (in the case of the Duchy) corporation tax. They are both part of the Crown, and the Crown doesn’t pay these taxes.

For the same reason, the Duchy of Cornwall doesn’t pay these taxes – it’s said to be a Crown body. It’s far from clear that’s correct – but let’s accept it for now.

The obvious question: why doesn’t the Prince of Wales pay normal income tax or capital gains tax?12 He certainly isn’t part of the Crown – but nevertheless is considered exempt from tax on his considerable Duchy of Cornwall income, and pays “tax” on it on the same voluntary basis as the King.

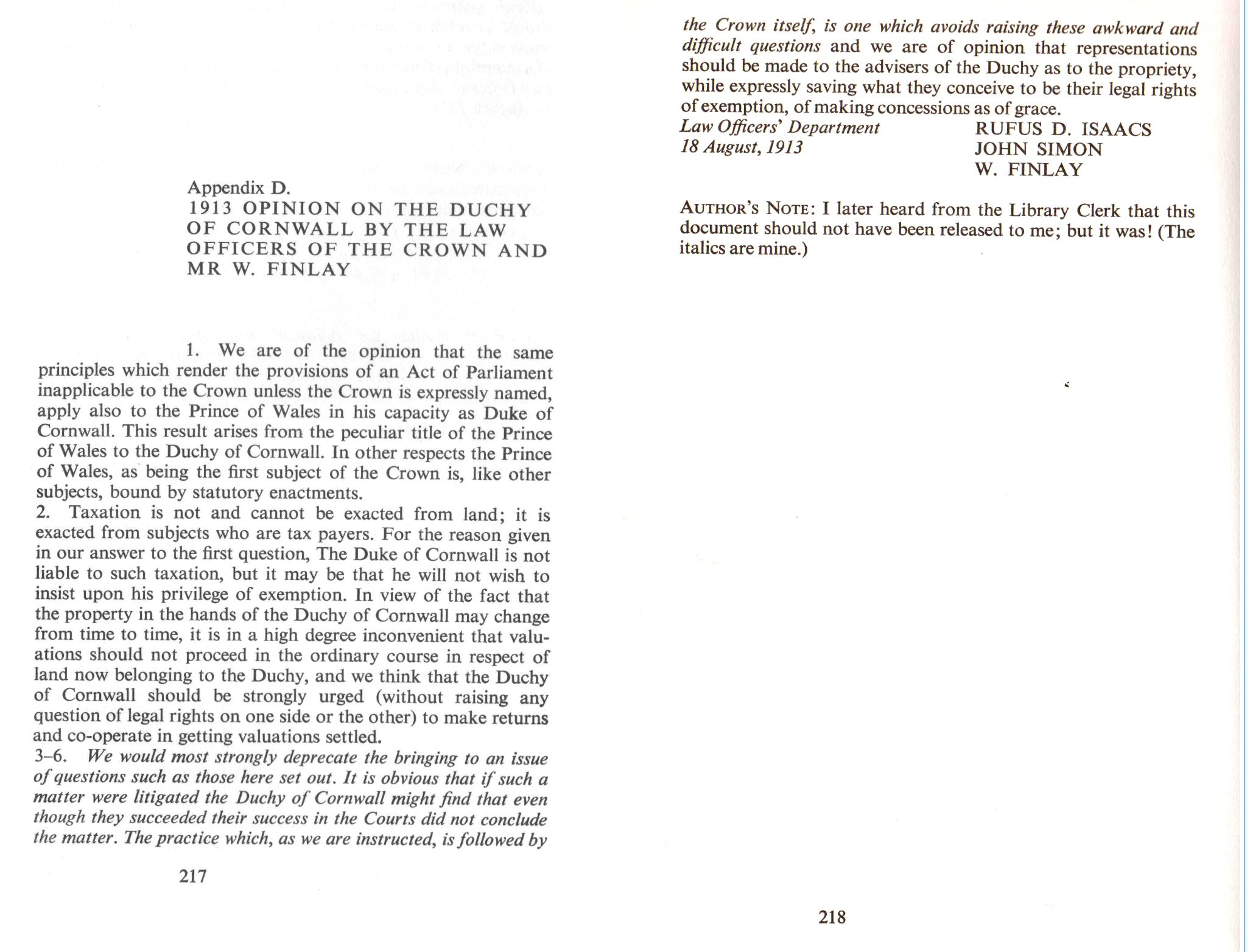

The rationale turns out to be a 1913 opinion issued by law officers. It is a very thin document:

Perhaps this passed muster in an age of greater deference, but to modern eyes it’s not an opinion at all – just an assertion with no reasoning. There are lots of bodies that are exempt from tax for various reasons. Income from those bodies is always taxable absent specific statutory provision. Why should the Prince of Wales’ income from the Duchy of Cornwall depart from this principle?

The opinion doesn’t seem to have convinced many people at the time. George V had asserted Crown immunity for the Sovereign in 1910, but the Duchy of Cornwall kept paying income tax until 1921, when it stopped and instead made a voluntary £20,000 contribution to the Exchequer. There’s an excellent history of this in an article by John Kirkhope in the Plymouth Law and Criminal Justice Review.

The opinion seemed even less convincing when the House of Commons debated the Duchy of Cornwall in 1982.

My opinion, and that of the other tax lawyers I spoke to, was that the Prince of Wales should be paying tax on his income from the Duchy of Cornwall. Not fake “Memorandum of Understanding” tax, but real, normal, statutory tax.

The two answers

My tentative answers to the two questions at the top are therefore:

- The current voluntary tax framework is pointless. A whole bunch of money is just going round in a circle at a considerable expense, and it would be a lot easier for everyone involved if we simply reduced the sovereign grant and scrapped the voluntary tax concept. If we must keep it, then let’s have a bit more transparency.

- The Prince of Wales’ tax exemption on his Duchy of Cornwall income seems hard to justify. My usual principle that people should pay tax on the basis of law. When that doesn’t happen, then that should be challenged, or the law should change.

What this shows

The new disclosure gives us the appearance of transparency, but almost none of the substance. We know that the King paid £12.9m of voluntary “tax” in 2024/25. We don’t know the income, gains, expenses or deductions behind that number. We don’t know how much of the Duchy of Lancaster surplus was treated as used for official purposes. We don’t know how much private investment income he has. The best we can do is reverse-engineer a conservative lower bound.

But fundamentally, it is legally and constitutionally correct that the King does not pay tax like the rest of us.

The Prince of Wales’ position is more troubling. The Prince of Wales is not the Sovereign. He receives a very large income from the Duchy of Cornwall, and the legal basis for treating that income as outside normal statutory tax appears very thin indeed

That’s deeply unsatisfactory. Either the Prince of Wales is legally taxable on his Duchy income, in which case HMRC should tax him. Or Parliament thinks he should not be taxable, in which case Parliament should say so. What should not happen is that a major constitutional tax exemption continues indefinitely on the basis of convention, deference and a Memorandum of Understanding – none of which are the law. And we should all, prince or pauper, be taxed under the law.

Image of a redacted tax return by Tax Policy Associates Ltd (and – of course – is symbolic and not the King’s tax return).

Many thanks to T and B for their analysis of the Duchy of Lancaster accounts and the implications.

Property118’s tribunal win – it doesn’t help their clients; it looks vulnerable to appeal

A modest proposal for a new tax

New data suggests Scotland’s 48p tax rate may be losing money

John Healey should cut National Insurance, not raise the personal allowance

What would a land value tax actually do?

What if Andy Burnham lowered the mansion tax threshold to £1.5m?

Footnotes

The documents don’t give that £5.4m figure. They give the £12.9m and £11.7m figures, and say the total for the three years is over £30m. ↩︎

The current Memorandum (below) says so at paragraph 1.2: the Sovereign “is not legally liable to pay income tax, capital gains tax or inheritance tax because the relevant enactments do not apply to the Crown”. The Duchies of Lancaster and Cornwall are Crown bodies and share that immunity. ↩︎

The original Memorandum was dated 5 February 1993 and took effect from 6 April 1993; it was amended in 1996, 2009 and 2013. I can’t locate a copy of the 1993 document. ↩︎

Income tax is charged on Privy Purse income “to the extent that the income is not used for official purposes” (2023 Memorandum, Appendix A). No CGT arises on the Duchies – supposedly because their capital can’t be paid out to the King or Prince (but that’s an unconvincing justification when the cash generated from capital disposals can be paid out). The inheritance tax exemption for assets passing from one sovereign to the next is justified on the footing that private estates such as Sandringham and Balmoral have “official as well as private use”. ↩︎

Neither Duchy pays corporation tax, income tax or CGT – both are Crown bodies. Each surplus is what ultimately flows up to the King and the Prince respectively, and is the starting point for the voluntary “tax” calculation. ↩︎

The Grant is “disregarded” for income tax (2023 Memorandum, para 2.9): tax-free coming in, and the official costs it funds aren’t deductible against anything else. It rose to £132.1m in 2025/26, mostly to finish renovating Buckingham Palace. ↩︎

Because the memorandum provides that tax is paid on an accruals basis, not a cash payment basis ↩︎

45% is the additional rate of income tax. The Duchy surplus is overwhelmingly rental and property income, taxed at 45% – not the 39.35% dividend rate, despite the Duchy labelling its distribution a “dividend”. ↩︎

Because the expenses reduce his tax, so there must be additional income/gains to bring it up to the £12.9m figure. ↩︎

It also follows that, if some of the Duchy of Lancaster income is taxed at a lower rate, then the income/gains from his private investments must be higher (again, to bring the tax up to £12.9m). ↩︎

i.e. because then £24.4m of Duchy of Lancaster income (minus £2m of expenses) taxed at 45% plus £3m of capital gain @24% plus £5.4m of dividend income @39.35% equals £12.9m, the declared total tax amount. ↩︎

The Duchy of Cornwall’s own accounts state that “The Duchy of Cornwall is not subject to income tax”, and that on a voluntary basis the Prince “pays income tax at the prevailing rates in respect of the net revenue surplus”. ↩︎

Leave a Reply