The Housing select committee has said stamp duty does economic damage and should be reformed. The Telegraph says the stamp duty increase last year “backfired”: transactions slumped, and receipts fell with them. I wish that was right, because there would then be an easy argument to reverse the increase, and even abolish the tax. But it isn’t. There was a short-term increase in transactions, and whilst there will be a long-term fall, the overall effect is a significant increase in revenue.

The depressing truth is that stamp duty1 isn’t even close to the top of the Laffer curve2, so each increase damages growth, jobs and happiness, but still raises additional tax. And so successive Governments have become addicted to what is possibly the UK’s worst tax.

In this report:

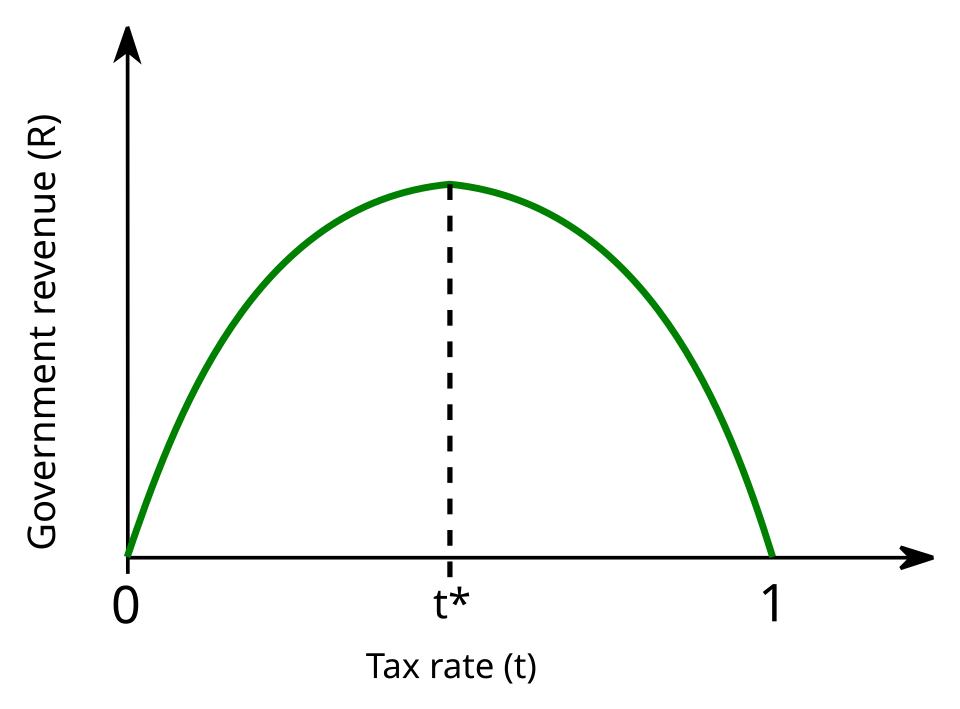

The Laffer curve

Here’s the usual representation of the Laffer curve:3

As the tax rate increases, people do less of the thing that’s taxed. As the tax rate approaches the dotted line, diminishing returns set in. At the point it hits the dotted line, tax revenue has been maximised – any further increase in rate reduces revenues.

It’s very plausible the UK tax rates in the 1970s hit the top of the Laffer curve (although less because they put people off working, and more because it was so easy to avoid the tax).

The Telegraph’s story suggested that stamp duty had sailed over the top of the Laffer curve, with a fall in transactions and tax receipts.

The stamp duty “raid”

In April 2025, the temporary stamp duty thresholds introduced by Liz Truss expired.4 This added £2,500 of tax for most standard buyers above £250,000 but a much bigger effect5 for first-time buyers:

The practical impact is clearer if we view the SDLT as a percentage of house price:

What should we expect to happen?

The principle is obvious: stamp duty is a tax on moving house. Raise it, and you see fewer house moves.

We can do better than intuition and put a number on the effect. Politicians have incessantly fiddled with stamp duty in a way that’s been bad policy in almost every sense, but has had the upside of letting us measure the real-world impact of stamp duty changes.

HMRC has calculated, and the Office for Budget Responsibility (OBR) uses, SDLT “semi-elasticities” – the percentage change in transactions from a 1 percentage point rise in the effective SDLT rate at a given price.6

We can use this to “predict” the impact on house-moving transactions of the April 2025 stamp duty increase. (I say “predict” because this has already happened, but I’m going to try and be careful not to cheat, and just apply the theory rather than peeking at the actual outcomes.)

Applying the semi-elasticities to the April 2025 stamp duty increase suggests a simple standard-buyer transaction drag of about 3.2%,7 and a bigger effect for some first-time buyers.8

Here’s what this theory predicts. The chart shows actual England and Northern Ireland residential transactions to February 2025, then uses the simple 3.2% standard-buyer price-mix estimate and historic “spike” effects to project forward:9

Taking into account the “spike” and subsequent drop, the model predicts an overall decline (2.1%) in the number of transactions. What does that imply for receipts?10

A significant overall increase in revenue.

In the twelve months before the forestalling period, February 2024 to January 2025, HMRC SDLT cash receipts were £13.1bn. Our projection for the twelve months from February 2025 to January 2026, including the pre-deadline spike, is £14.3bn – i.e. about £1.2bn of additional revenue.

That’s consistent with HMRC’s own ready reckoner, which shows that raising the lower SDLT bands still raises money after behavioural response11 – it is only the very high rates (the 12% top band, the additional-property surcharge and the non-resident surcharge) that appear close to or past the revenue-maximising point.12

It’s also what the OBR expected. When the temporary higher SDLT thresholds were introduced in 2022, the OBR-certified costing assumed that ending them on 31 March 2025 would raise revenue: £850m in 2025-26, £1.44bn in 2026-27 and £1.635bn in 2027-28.13

So our model and the OBR costing all point the same way: fewer transactions, but higher receipts. Theory suggests we were not past the top of the Laffer curve.

All the code for the modelling in this section (and generating the charts in this article) is available on our GitHub.

What actually happened

Now let’s open our eyes and look at the actual data for what happened (the red line):

Instead of our projected drop of 20,000 transactions, we see an overall increase of 85,000 compared to the previous year.

Why? There’s an absolutely huge “spike”. We assumed the transactions in the “spike” would be accelerated transactions from the next few months, and so expected an additional drop-off in transactions after the stamp duty increase kicks in (i.e. in addition to the expected effects of the increase itself). There is a drop-off, but it’s much less than expected.

Receipts are therefore considerably more than our model suggested: £2.4bn of additional revenue rather than £1.2bn. They were also above the OBR’s pre-year forecast. HMRC cash SDLT receipts for 2025-26 were £15.159bn, £507m above the OBR’s October 2024 forecast for total SDLT.14

Why are there so many more transactions?

One possibility is that the negative effect of the stamp duty change was masked by positive macro factors – the fall in mortgage rates, increase in mortgage approvals or just a general market rebound. However if these effects were significant then we’d see an increase in prices for houses where the stamp duty change had little or no effect. We found no obvious sign of this in the least-exposed price bands.

That leaves two dull technical possibilities:

- The theory and semi-elasticities don’t apply to this kind of stamp duty change. People are less responsive to stamp duty than expected.

- There is an error in our modelling (certainly possible; although we tried two completely different methods and got the same answer).

And then one interesting real possibility:

- The prospect of increased stamp duty didn’t just accelerate purchases by a few months (a well-understood and expected effect) but pulled forward purchases from further into the future, or enticed people into buying when otherwise the decision was marginal.

We don’t know. But this was a one-off effect. Once the spike and its immediate payback have washed through, the underlying behavioural drag is likely to be smaller than the first-year numbers suggest. Re-running the same simple standard-buyer model with OBR’s steady-state elasticities gives a long-run transaction drag of around 2.7%; the more detailed cohort model gives a similar 2.6%.15 On English transactions running at around a million a year, that is roughly 25,000 to 30,000 households who would otherwise have moved but will not.16

In narrow tax terms, this looks like a success because stamp duty receipts are about 10% higher, even after the long term decline in transactions.17 Rachel Reeves did not hit the top of the Laffer curve, and the tax increase clearly raised more revenue.

Why did the Telegraph say transactions fell? Because they compared the first quarter of 2025 (with that huge spike) with the first quarter of 2026 (the “new normal”) and saw fewer transactions. You can’t ignore the spike – it’s part of the behavioural response to the tax increase. The correct approach is to compare the pre-announcement/pre-forestalling baseline with the full twelve-month period affected by the change, including the pre-deadline spike and the subsequent payback.

Transactions did not slump overall, and receipts did not fall. There will be a long-term fall in transactions, but the increased rate will more than compensate. In narrow fiscal terms the tax rise worked.

But there was, of course, a price.

The price of a stamp duty increase

The data suggests that, thanks to the increase, after that first year spike there will be about 30,000 fewer residential property transactions every year. The Budget made life appreciably worse for those 30,000 households. They wanted to move house, and would have moved house, but now won’t.18 Few tax increases are so modest in fiscal terms, while having so large an impact on people’s lives.

There will also be a knock-on effect on the housing market, the labour market, and the economy:

- Stamp duty stops the housing market working efficiently: it discourages mutually beneficial moves and stops properties being held by the people who value them most.19 That means fewer downsizing chains; older households stuck in homes too big for them, and younger families squeezed into homes too small. Around 40% of English households are under-occupied while around 3% are overcrowded.20 Some of that mismatch persists because the tax cost of moving is too high.

- Stamp duty and similar taxes reduce labour mobility; they deter long-distance, job-induced moves.21

- The economic effect is much more modest. A loss of 30,000 transactions implies somewhere around £300m of gross moving-related spending lost.22 The effect is real, but small in macro terms.

These are the reasons why we should be finding ways to abolish stamp duty, not increase it.

It would be nice if there was a free lunch here: that stamp duty is now so high that cutting it would raise revenue. But that is not what the evidence shows. The Telegraph’s comparison was misleading; the increase did raise revenue. That does not make it good policy. Stamp duty still stops people moving, worsens the allocation of housing, and damages the labour market.

The problem is not that stamp duty increases “backfire”. It is worse than that: they work fiscally, while doing real economic and human damage.

Many thanks to P and T for help with the modelling. All the calculations, code and source notes are on our GitHub.

The front page is © Telegraph Media Group, and is reproduced here for purposes of criticism and review.

Tenancy reform: the accidental stamp duty headache for 150,000+ tenants

Why Angela Rayner is likely to pay £8,000 in stamp duty penalties

The Angela Rayner tax proposals – how much sense do they make?

The tax longlist – 35 ways Rachel Reeves could raise £22bn

How to reform property tax

![t 1] E SHARING BEST PRACTICE

proper y .S FOR UK LANDLORDS & PRS

The Ultimate Guide to

LANDLORD TAX PLANNING

and transitioning between ownership structures](https://taxpolicy.org.uk/wp-content/uploads/2024/07/Untitled.jpg)

Property118 – more hopelessly wrong tax advice for landlords

Footnotes

The tax in question is stamp duty land tax, the modern tax on land in England. “Stamp duty” is a separate, much older, tax on documents. However we will, in the interests of clarity, refer to the tax as “stamp duty” in this article – our apologies to tax advisers. ↩︎

That’s true generally, and for the great majority of people, but there’s an important exception: second house purchases and/or non-resident purchases of high value properties, where the rate is plausibly at or over the top. That is intentional – more on this below. ↩︎

Laffer curve illustration, Bastianowa CC BY-SA 2.5 ↩︎

The standard nil-rate band fell from £250,000 to £125,000, the first-time-buyer nil-rate band fell from £425,000 to £300,000, and the first-time buyer relief cap fell from £625,000 to £500,000. See the GOV.UK residential rates and HMRC’s temporary threshold measure. ↩︎

The first-time buyer effect is concentrated around the old £425k and £625k relief boundaries: a £425k first-time buyer went from zero SDLT to £6,250; a £625k first-timer buyer lost relief entirely and saw SDLT jump from £10,000 to £21,250. ↩︎

See the OBR residential SDLT elasticities note. The current numbers were estimated following HMRC analysis of the 2014 slab-to-slice reform. Throughout this article we use OBR’s year-1 transaction semi-elasticities: -7.0 below £250k, -5.0 from £250k to £1m, and -6.0 above £1m. One important caveat: HMRC’s underlying analysis “regressed the change in transactions against the change in effective tax rate in comparable 28-day periods before and after the policy change” (OBR note, paragraph 1.2). The December 2014 reform was announced and took effect on the same day, so this short window contains no forestalling, but it also tells us less about how transactions evolve over a longer horizon than we are projecting here. OBR also publishes “steady state” elasticities which are slightly smaller (-6.0, -4.5 and -6.0); we use the year-1 numbers because we are projecting twelve months from the change, but the long-run drag is likely to be a little smaller than the headline figures here suggest. ↩︎

This is a transaction-weighted price-mix estimate, not a buyer-type average. We took English Price Paid transactions in the pre-change period from January 2024 to March 2025, treated each as a standard buyer, calculated the old and new SDLT, converted the tax increase into a percentage-point rise in the effective SDLT rate, and applied OBR’s year-1 transaction semi-elasticity at that price. The resulting transaction-weighted mean is -3.155%, rounded to 3.2%. Standard-buyer examples: -5.0% at £250k, -4.2% at £300k, -2.5% at £500k, -1.7% at £750k, -1.3% at £1m. ↩︎

Many lower-price first-time buyer transactions saw no SDLT change, so the first-time buyer effect doesn’t change the overall impact very much. But around the relief boundaries the effect is much larger: 0% up to £300k, about -7.4% at £425k, -6.3% at £500k, and -9.0% at £625k, where relief was lost altogether, and that creates a significant regional disparity. ↩︎

The projection applies the 3.2% transaction drag to the post-deadline monthly baseline after modelling forestalling. To model forestalling, we use the September 2021 SDLT deadline as the analogue. We estimate the September 2021 England and Northern Ireland spike as the excess over the average of September 2020 and September 2022. That gives 58,405 accelerated transactions. We add these to March 2025, then deduct the same number from April to December using a geometric decay, so more are deducted from April and May than from later months.

We also built a more detailed cohort model, estimating the split between standard buyers, first-time buyers and additional-property/HRAD buyers. That produced a similar national result: about a 2.8% average Apr-Dec drag. But Price Paid Data does not identify buyer type, so the model has to infer the buyer mix from external data and calibration targets. That makes it useful as a sensitivity check, but not obviously better as the headline model: it adds modelling judgement and potential over-fitting risk without materially changing the national result. The chart therefore uses the simpler and more transparent 3.2% standard-buyer price-mix estimate. ↩︎

For the receipts projection, we start with HMRC monthly SDLT cash receipts and the transaction projection above. We then adjust post-change receipts using monthly 2024 Price Paid Data to estimate the ratio between old-threshold and new-threshold SDLT for that month’s transaction mix. This remains a theory-only projection, not HMRC administrative liability data. ↩︎

HMRC’s ready reckoner estimates that raising the residential 2% marginal rate by 1pp would raise £420m in 2026-27, and raising the 5% rate by 1pp would raise £685m. By contrast, raising the 12% rate by 1pp loses £25m, and raising the higher-rates-for-additional-dwellings surcharge by 1pp loses £45m. That is consistent with the high rates being near or past the Laffer peak, but the lower bands being some distance from it. The April 2025 threshold change pulls more transactions into the 2% and 5% bands – exactly where HMRC’s own numbers say revenue still rises. ↩︎

It appears to be intentional that the non-residence surcharge is past the revenue-maximising point, because the idea was to discourage non-residents from acquiring and make property more affordable for UK residents. It is unclear to us what the macro effect of the additional property surcharge and 12% top band is, particularly when they are combined. It’s reasonably clear that they’ve had a highly negative effect on the high-end property market. Query what impact that has on the rest of the property market and the economy generally. Also query what the policy intention of these measures really was. ↩︎

See HMRC, Stamp Duty Land Tax: temporary increase to thresholds. The table says the figures were certified by the OBR. This is a policy-costing estimate, not directly comparable with our twelve-month cash-receipts projection, but it is the right starting point: the official forecast was that ending the temporary thresholds would raise revenue after behavioural response. ↩︎

The OBR’s October 2024 EFO forecast total SDLT receipts of £14.652bn for 2025-26. Actual HMRC cash SDLT receipts were £15.159bn. Later OBR forecasts moved as more information became available: actual receipts were £1.038bn above the March 2025 forecast, £255m above the November 2025 forecast, and £248m below the March 2026 forecast, which was published once most of the year was already known. This is a useful forecast comparator, not a perfect no-change counterfactual. ↩︎

Year-1 elasticities of -7.0, -5.0 and -6.0 give a 3.2% average drag (and 2.8% in the cohort model). The same calculation using OBR’s steady-state elasticities of -6.0, -4.5 and -6.0 gives a 2.7% to 2.6% range. We use the steady-state numbers as the long-run benchmark because OBR itself uses them for ongoing fiscal-drag modelling. ↩︎

Annualising the panel-based estimate gives a narrower figure of around 15,000 in the most-exposed districts. The 25,000 to 30,000 range applies the long-run drag to all English residential transactions. ↩︎

That’s on the same model, stripping out the timing spike and looking at a steady twelve-month period. ↩︎

It feels like this is a point that does not need evidence, but see ISER research using the British Household Panel Survey, Does moving improve housing satisfaction? The effect is heterogeneous – not every move is welcome, and some moves are stressful – but blocking desired moves reduces wellbeing. ↩︎

This is the long-standing IFS/Mirrlees view of transaction taxes: see The Mirrlees Review, chapter 16, and Paul Johnson, Stamp duty is an economic nonsense (IFS, 2017). ↩︎

See the English Housing Survey 2024-25 headline findings. Under-occupation and overcrowding are technically defined and the numbers are no more than indicative of real-world issues, but the gap shows the scale of mismatch in the stock. ↩︎

Foundational studies from the Netherlands and Australia consistently link increased transaction costs to reduced economic mobility. A 2017 study by Hilber and Lyytikäinen had surprisingly concluded that SDLT primarily stifled short-distance housing moves rather than long-distance labour mobility. Then a 2021 study by Eerola, Lyytikäinen, and others found that previous quasi-experimental research designs – like the boundary cut-off method used in the 2017 UK study – were prone to attenuation bias. By failing to account for “spillovers” (trading across control and treatment groups), the older methodology underestimated the negative effects of the transfer tax on overall mobility by roughly 20%. It confirms that transfer taxes do significantly deter long-distance, job-induced moves. Note also that the 2017 study covered a period when stamp duty rates were substantially lower than today’s, with the tax on an average home three times greater today. ↩︎

i.e. assuming £10k of moving-related spending per prevented transaction, but some spending will be displaced elsewhere. ↩︎

{kind=link}

Leave a Reply