The deputy leader of Reform UK, Richard Tice, owns a property company – Quidnet REIT Limited. From 2020 to 2022 it paid around £600,000 of dividends to Mr Tice and his offshore trust. Quidnet was required by law to withhold approximately £120,000 of tax from those dividends and pay it to HMRC. But we believe it’s clear from the company’s accounts and public filings that Quidnet did not pay this tax.

Mr Tice has refused to answer the question directly, instead saying that he paid income tax on the dividends. That’s not an answer: the company was legally required to pay tax; the law doesn’t permit REITs to opt to defer their tax obligations.

The issue was first identified by Gabriel Pogrund of The Sunday Times – his report is here. Since the paper went to press we have conducted further analysis of the two last dividends, and so the figures in this report are higher than those reported in The Sunday Times.

Quidnet REIT

Quidnet REIT Limited is a property company controlled by Richard Tice, the deputy leader of Reform UK.

From 10 August 2018 to 9 August 2021. Quidnet was a REIT: an investment fund that invests in real estate. A company wishing to become a REIT has to apply to HMRC; the consequence is that the company then becomes exempt from corporation tax on its property rental business, but its investors are (broadly speaking) taxed as if they held the real estate directly. The logic is that a REIT is an investment fund, and the usual principle is that funds don’t pay tax; their investors do.

However, Mr Tice’s REIT was unusual: throughout its life, it was almost entirely owned by him and entities connected to him.

REITs are usually required to be widely held by different investors – they’re supposed to be genuine investment funds, not tax planning vehicles. The rules provide for a three year grace period in which REITs can become compliant but, as The Sunday Times previously reported, Quidnet REIT Ltd never attracted more than a small number of outside investors. Quidnet therefore ceased to be a REIT on 9 August 2021.

It’s unclear if real efforts were made to find outside investors – if they were not then we would regard this as aggressive tax avoidance which probably does not work technically.1 However this article is not about tax avoidance. It’s about what appears to be a simple failure by Richard Tice’s company to pay the tax that was due.

The tax Quidnet failed to pay

As a UK REIT, Quidnet was required to distribute at least 90% of its tax-exempt property rental profits to shareholders as “Property Income Distributions” (PIDs). This is essentially the quid pro quo for the REIT tax exemption – you have to pay profits to your shareholders, and the expectation is that (unless they’re exempt) they’ll be taxed on those profits.

But HMRC isn’t content to just wait for the shareholders to pay tax. That could be over a year from the date the profits were made. There’s also a risk that the investors would simply fail to pay tax on the dividends they receive. So, just as an employer is required to withhold PAYE tax when paying wages to its employees, a REIT is required to withhold basic rate income tax (20%) from its dividends, and pay it to HMRC. Dividends paid to UK pension funds (such as SIPPs) and UK companies are exempt from this withholding requirement. The Assura plc REIT has published a helpful summary of the rules.

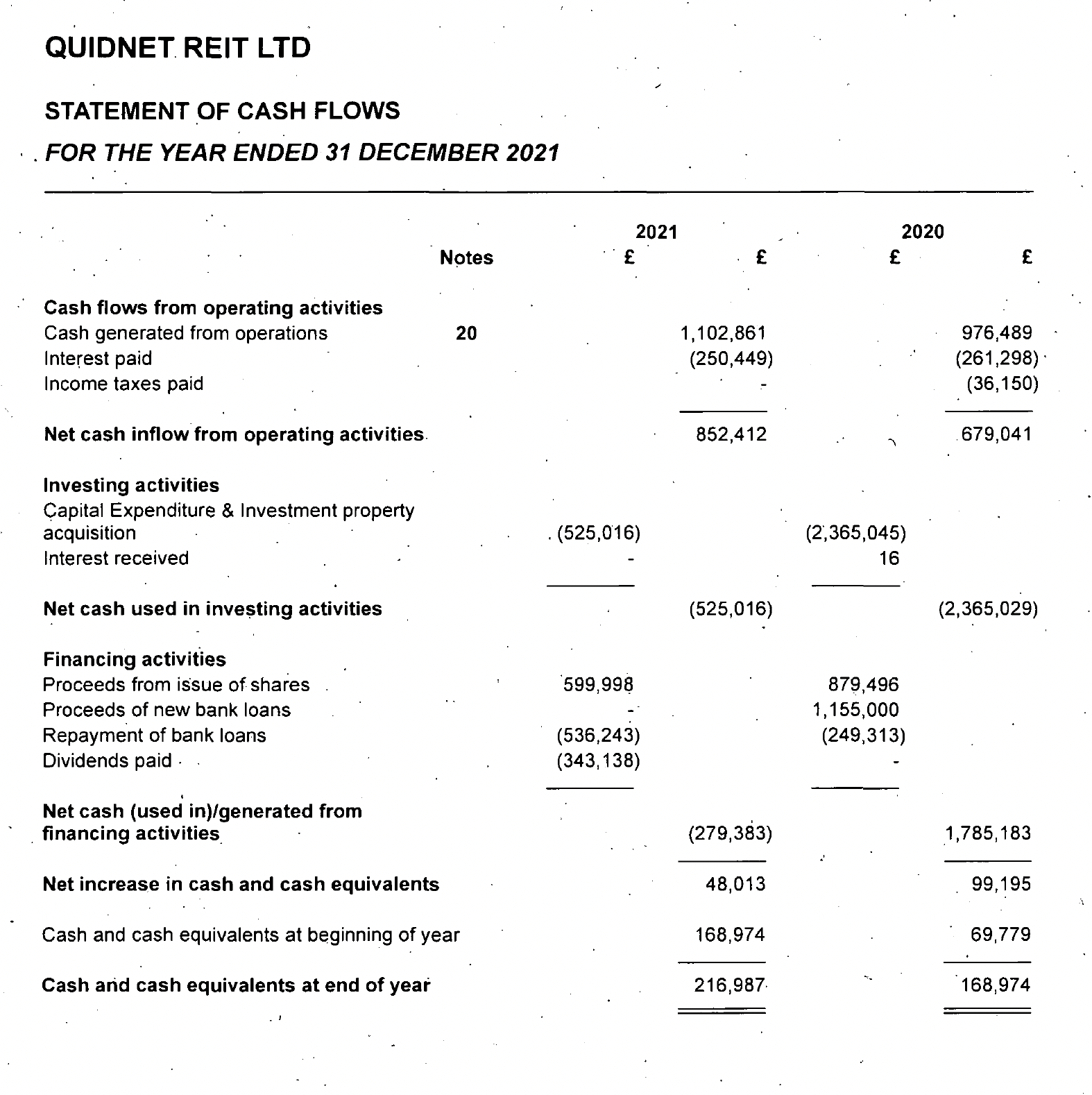

Quidnet paid around £600,000 in REIT dividends2 to Mr Tice and his offshore trust3 – the RJS Tice Family Settlement.

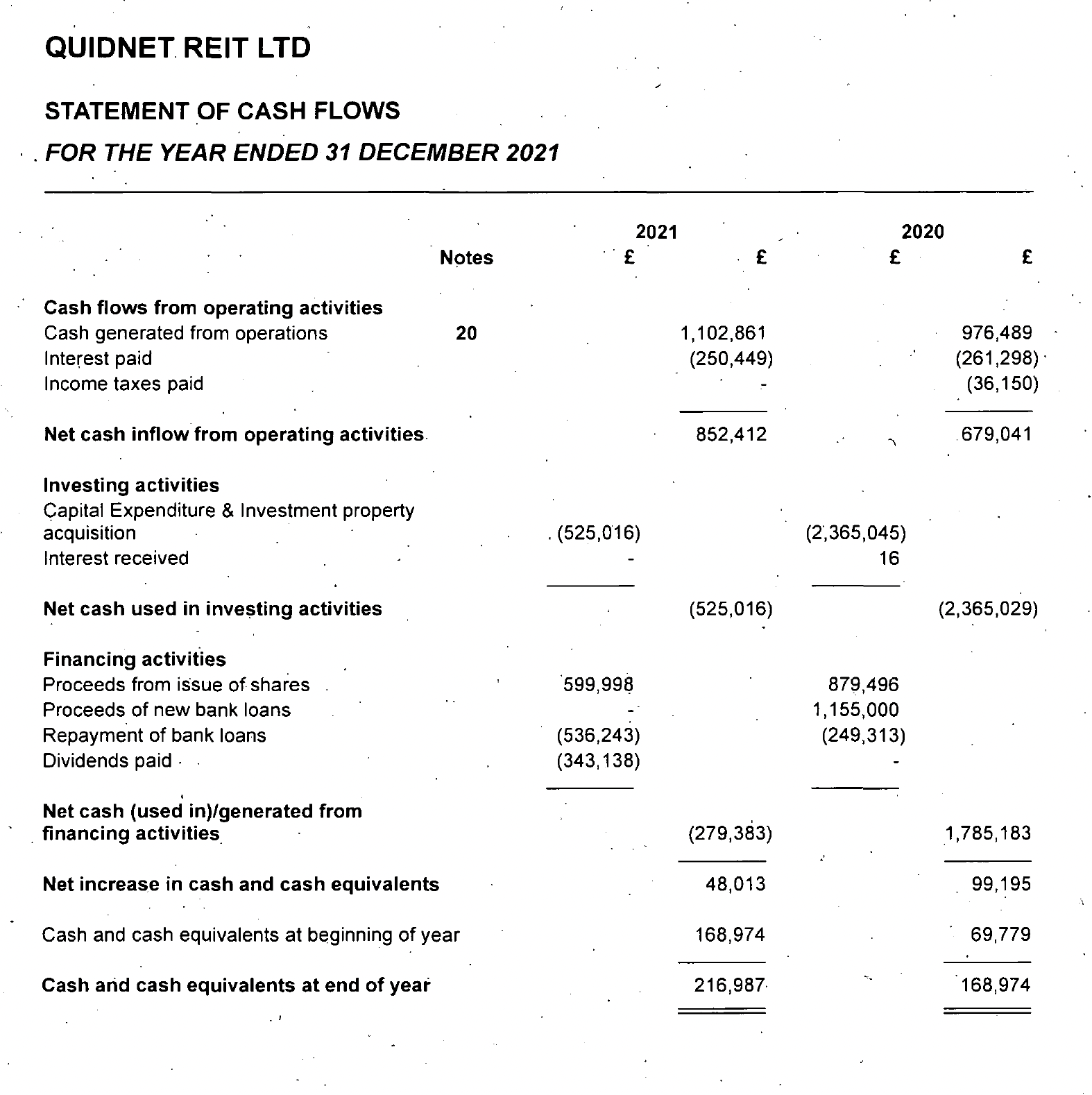

Quidnet should have withheld around £120,000 of income tax from these dividends, and paid it to HMRC. There is, however, no sign of this in the company’s cash flow statement – the tax should have been there (either under tax or dividends), and it isn’t:4

The “methodology” section below goes through a detailed analysis of how, even aside from the accounting treatment, we can be confident that the company failed to withhold around £120,000 of tax.

The obligation for a REIT to withhold tax is well understood and (absent very unusual circumstances) we expect HMRC would say that the failure to withhold tax was careless. On that basis, HMRC would have six years to make an assessment and collect the tax5 plus interest and penalties.6

Richard Tice’s response

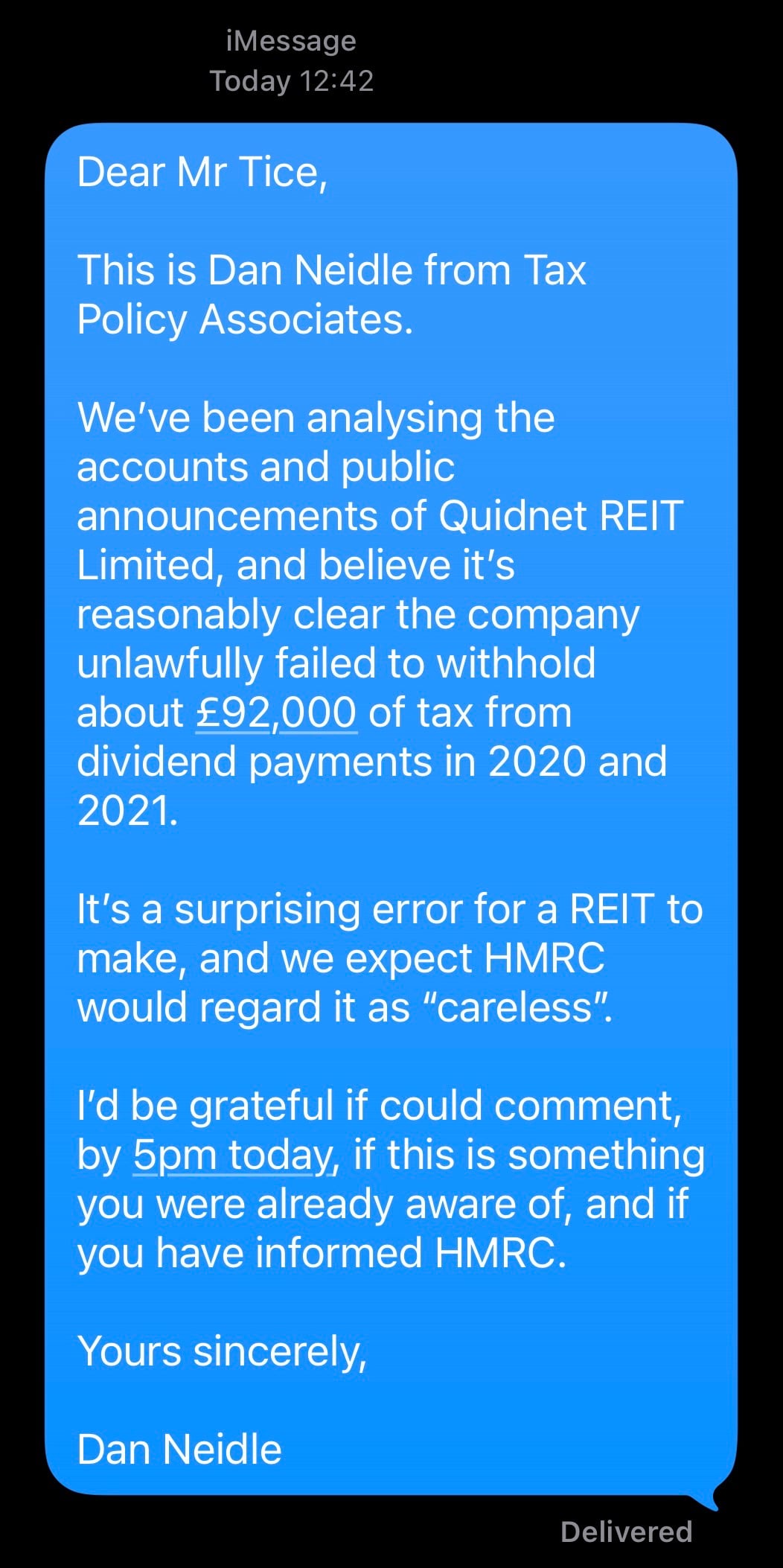

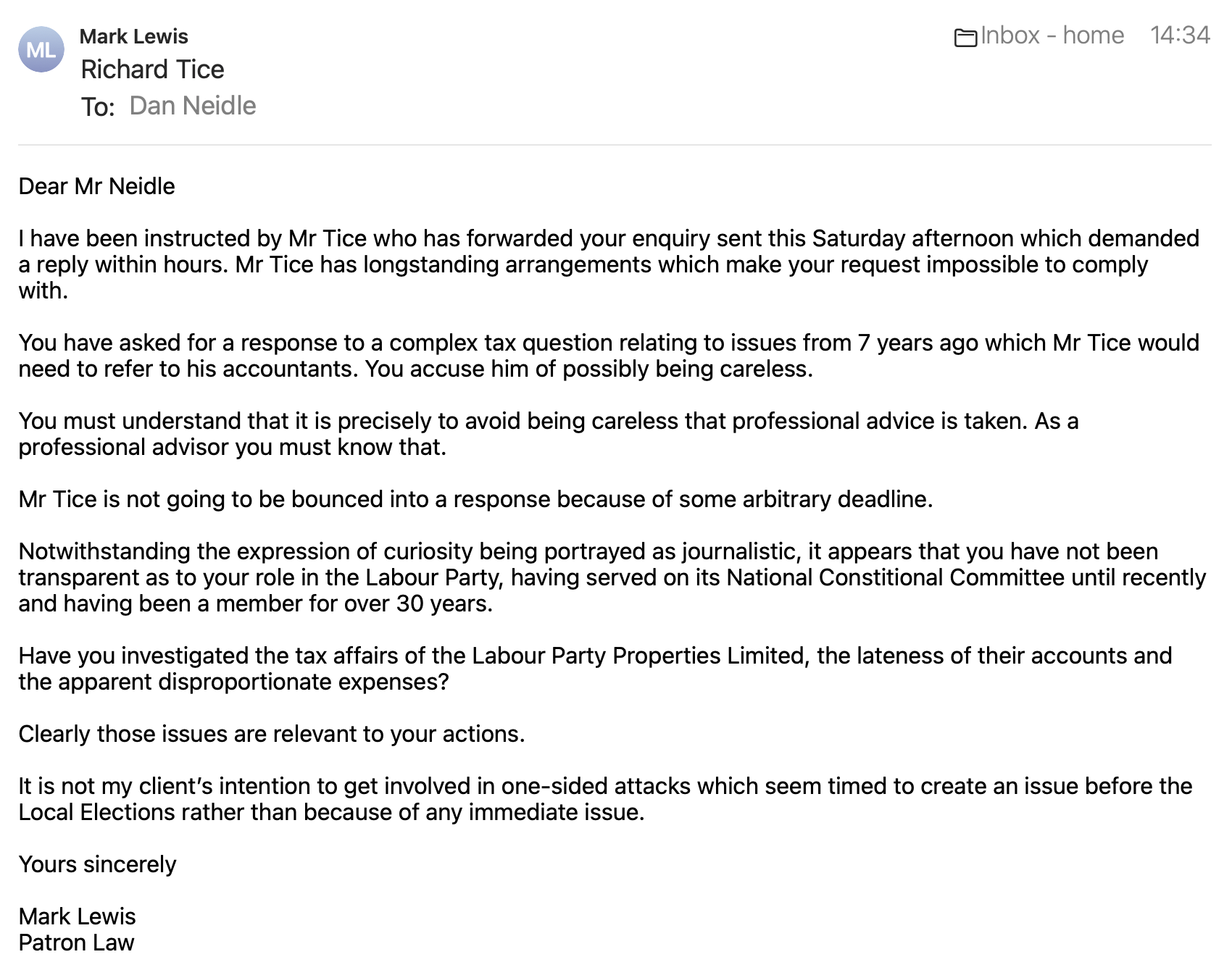

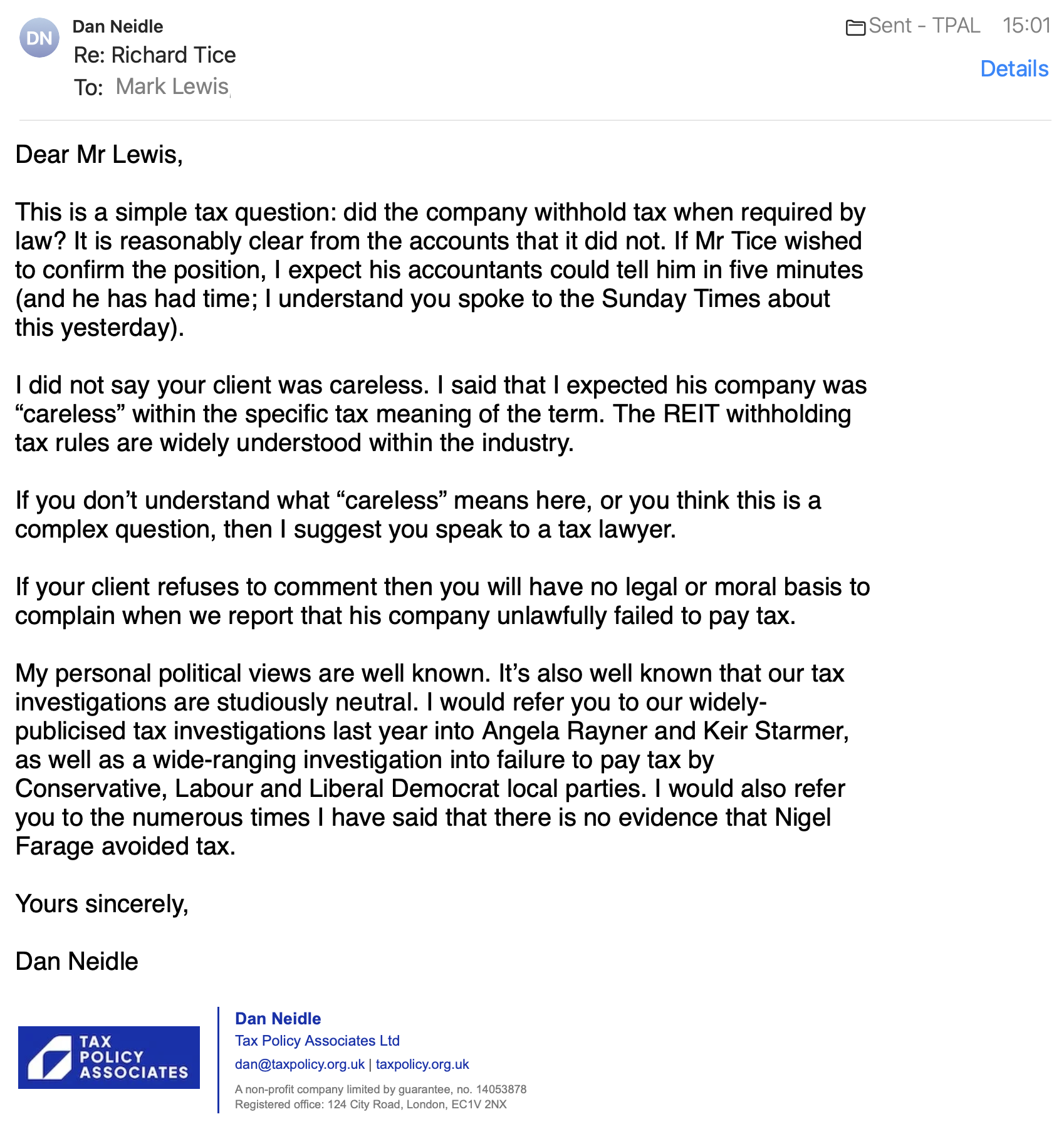

We wrote to Mr Tice seeking comment for this story. We received a response which failed to engage with the substance of the matter. Here’s our initial request, the response from Mr Tice’s lawyer, and our reply.

Mr Tice was more forthcoming to The Sunday Times:

Tice, the Boston & Skegness MP, implied the failure amounted to a “technicality” and appeared to suggest it did not matter as he ultimately paid income tax on the dividends he received. He said: “I have paid all tax at the highest rate on all dividends received. HMRC has been paid in full.”

And then, shortly after we published this report, on X:

![Richard Tice MP * @ § © TiceRichard: th xX

Desperate still to smear me & Reform, Sunday

Times has again spent weeks pouring over my

company accounts with Labour-supporting tax

accountant

All that effort has revealed overall HMRC received

the correct amount of tax due

Journo now effectively complaining | paid too much

tax rather than company pay some tax on my

behalf! All due to complex tax technicality around

dividends to certain shareholder classes in REITs

But S Times refuses to investigate serious

accounting irregularities & possible multi million

pound electoral law breaches by Labour Party

Properties Ltd, that | exposed

Meanwhile, I'll get on with representing the people

of Boston &Skegness & campaigning to kick out

this dreadful government

O 72 thes OK ih] 20K N](https://taxpolicy.org.uk/wp-content/uploads/2026/04/IMG_4082.jpg)

Mr Tice’s certainty that the correct overall amount of tax was paid is inconsistent with his solicitor’s complaint that Mr Tice hasn’t had time to refer the point to his accountants. And Mr Tice also doesn’t mention the Jersey trust – it’s unclear if the trust paid UK tax at all.

But the more important point is that, regardless of what tax was paid by Mr Tice and his trust, REITs and their investors have no choice how and when tax is paid. The law requires that a REIT withhold tax from its dividends immediately. It would be much more convenient for its shareholders if they could skip the withholding and wait to pay all the tax until they file their own tax return, up to 21 months later. The law, however, does not permit this. The law is also straightforward and, in our experience, well understood in the REIT industry.

It’s important to add that this was not tax evasion – a criminal offence – because there’s no reason to believe Quidnet’s directors or employees acted dishonestly – in our view that would be far-fetched. It was also not tax avoidance – an attempt to exploit a loophole. It was much more simple than that: Quidnet mistakenly failed to pay the tax required by law, and is now required to pay it.

Methodology

Many of the dividends in question were either paid by issuing new shares, or satisfied by issuing new shares. New shares are tracked in company records, and this gives us a second independent confirmation that there was a failure to withhold tax as required by law (in addition to the cashflow statement in the accounts).

The shareholdings

At the start of the period in question (July 2019), Quidnet had seven shareholders. Dividends paid to UK companies and pension funds are exempt from REIT withholding, leaving two shareholders subject to withholding tax on Quidnet’s dividends:

- Richard Tice personally — 824,100 shares (15.36% of the total)

- His Jersey trust — 1,033,598 shares (19.26% of the total)

Together they held 34.62% of the company’s 5,366,193 ordinary shares.7

The dividends

There were three types of dividends paid by Quidnet, and the 20% withholding tax rule applies to them all in a slightly different way:

Simple cash dividends

Tax is simply deducted at 20%. So, for example, if a dividend of £100 is declared to an individual REIT shareholder, then £20 should be withheld by the REIT and remitted to HMRC, and £80 paid to the shareholder:

- From REIT declares £100 cash dividend to HMRC (Label: £20 tax withheld)

- From REIT declares £100 cash dividend to Investor (Label: £80 dividend)

This example from Industrial REIT Ltd shows how this is usually managed in practice.8

Scrip dividends

Instead of paying a dividend in cash, a company can pay a “scrip” dividend by issuing new shares to the shareholders.

A scrip dividend is subject to withholding in the same way as a cash dividend. So, for example, if a dividend of £100 is declared to an individual shareholder, and satisfied by issuing 100 shares worth £1 each, then the REIT should withhold 20 shares, issue 80 shares to the shareholder and pay £20 to HMRC.9

- From REIT pays scrip dividend of 100 £1 shares to HMRC (Label: £20 tax withheld)

- From REIT pays scrip dividend of 100 £1 shares to Investor (Label: 80 £1 shares issued)

For an example of how this is usually done in practice, see the bottom of page 3 of this document from LondonMetric Property Plc, and the worked example on the following page.

Dividend reinvestment plan

A company can declare a normal cash dividend but then satisfy it by issuing shares to investors, sometimes at the investors’ option (in which case it is often called a “dividend reinvestment plan” or DRIP). The end result looks the same as a scrip dividend, but legally it’s just a cash dividend followed by a share subscription. So, for example:

- From REIT declares £100 cash dividend to HMRC (Label: £20 tax withheld)

- From REIT declares £100 cash dividend to Investor (Label: Investor opts to receive 80 £1 shares instead of cash)

There’s an example here of how this is usually done – “the net dividend after tax is effectively reinvested by acquiring additional shares in the Company” (our emphasis).

The following paragraphs look in detail at the dividends paid out of REIT profits, and therefore subject to the withholding rules.

Dividend 1: FY2019 final (March 2020)

On 16 March 2020, the board declared a dividend of £684,055 for the year ended 31 December 2019. On the same day, it resolved to issue 423,040 new shares at £1.617 per share.10

The value of the shares issued — 423,040 × £1.617 = £684,055.68 – matches the gross dividend.11 This wasn’t a scrip dividend, but a cash dividend – satisfied in shares, with zero cash paid out.

If Quidnet had properly withheld 20% tax, it should have issued approximately 29,300 fewer shares and remitted around £47,364 to HMRC.12 Instead, shares were issued for the full gross value of the dividend – that provides independent confirmation (in addition to the accounts) that there was a failure to pay the correct tax.13

We can conclude that no tax was withheld from the £237,000 of dividends paid to Mr Tice and his trust, and £47,400 of tax was underpaid.

Dividend 2: H1 2020 interim (September 2020)

On 25 August 2020, Quidnet declared an interim dividend of 5p per ordinary share, to be paid on 21 September 2020 “by issuing shares at the new NAV per share of 155.1 pence”.

The announcement stated that “Shareholders are to receive 1 share for every 31.02 ordinary shares held”. A TISE announcement on 18 September 2020 confirmed that 186,627 shares settled the scrip dividend.14

This was a true scrip dividend. The conversion ratio is uniform for all shareholders — every holder gets 1 new share per 31.02 held, regardless of their tax status. If 20% had been withheld from non-exempt shareholders, the effective dividend would be 4p (not 5p) per share, and at an NAV of 155.1p this gives a ratio of 4/155.1 = one share for every 38.78 shares held.

Richard Tice received 28,661 shares worth about £44k. The trust received 35,947 shares worth about £56k. Both should have been subject to 20% withholding tax, but there’s no sign of that in the figures.15

We conclude that no tax was withheld from the c£100,000 of scrip dividends paid to Mr Tice and his trust, and around £20,000 of tax was underpaid.

Dividend 3: FY2020 final (April 2021)

On 17 March 2021, Quidnet declared a final dividend of 6p per ordinary share for the year ended 31 December 2020, with shareholders having the option16 to apply the dividend to subscribe for ordinary shares.

By cross-referencing the share register17, we can determine that Richard Tice personally took this dividend in cash, receiving £55,000 cash, and the trust took the dividend in shares, receiving 40,145 shares worth £64,000.1819

Once again, the full gross dividend was distributed with no apparent deduction for withholding tax.20 The trust received about £64,000 shares from which £13,000 should have been withheld and Mr Tice received about £55,000 cash from which £11,000 should have been withheld. And again, there’s no sign of any tax being withheld in the company’s cash flow statement for 2021.

{kind=link}

We conclude that no tax was withheld from the c£119,000 of dividends paid to Mr Tice and his trust, and so about £24,000 of tax was underpaid.

Dividend 4: H1 FY 2021 (August 2021)

On 17 August 2021, Quidnet announced its interim results for the six months to 30 June 2021, and declared a further cash dividend of 5.5p per share, payable on 23 August 2021. Quidnet ceased to be a REIT on 9 August 2021. However this dividend was paid out of profits made when Quidnet was a REIT, and so we expect was fully subject to the REIT withholding tax rules.

To satisfy some of this dividend, filings show the company issued 132,212 new shares in late August at the newly reported net asset value of £1.613 per share.

Because we have the exact share counts from the July 2021 confirmation statement, we can calculate precisely what was owed and how it was paid. The trust held 1,191,173 shares, entitling it to a gross dividend of £65,515 (1,191,173 × 5.5p). If we divide the trust’s £65,515 gross dividend by the £1.613 share price, it equates to an allocation of 40,611 shares. Confirmation statements show the trust’s shareholding increasing by precisely that amount.21 This confirms the trust elected to take its entire 5.5p dividend as scrip, and that the shares were issued for the full gross amount, with no shares withheld for tax.

At that time, Richard Tice held 917,728 shares, entitling him to a gross dividend of £50,475 (917,728 × 5.5p). His shareholding remained unchanged after this; confirming he took his £50,475 dividend entirely in cash. Just as with the previous dividends, there is no evidence the company operated the required 20% tax deduction on this cash payment.

We conclude that no tax was withheld from the c£116,000 of dividends paid to Mr Tice and his trust, and so about £23,000 of tax was underpaid.

Dividend 5: FY 2021 final (10 May 2022)

On 10 May 2022, Quidnet announced a final cash dividend of 5.3p per ordinary share. This covered the period from 1 July 2021 to 31 December 2021. Quidnet was only a REIT for a small amount of that time. In principle the rules require withholding to be applied to such amount of that dividend as attributable to profits made during the REIT period. We have no way to determine that, so will instead estimate the amount using a simple pro-rata calculation, i.e on the basis that Quidnet was only a REIT for 40/184ths of H2 2021.

On that basis, we estimate that the REIT rules applied to approximately £10,00022 of dividends paid to Mr Tice (received in cash) and £14,00023 of dividends paid to the trust. That’s a total of £24,000 – but there’s no sign of any income tax deducted in the accounts.24 It follows that £4,800 was underpaid.

Total tax at stake

Looking at the overall position:

| Dividend Period | Type | Approx dividend paid to Tice and Trust | Approx unpaid income tax |

| FY2019 Final | Cash (Settled in Shares) | £237,000 | £47,400 |

| H1 2020 Interim | Scrip | £100,000 | £20,000 |

| FY2020 Final | Cash / Scrip Mix | £119,000 | £24,000 |

| H1 FY2021 | Cash / Scrip Mix | £116,000 | £23,000 |

| FY2021 Final | Cash (Pro-rated) | £24,000 | £4,800 |

| TOTAL | £596,000 | £119,200 |

HMRC would be able to collect the £119,200 by a simple assessment.

Disclosure

Dan Neidle, the founder of Tax Policy Associates, is a member of the Labour Party. Tax Policy Associates has no political affiliation. Our previous reports suggesting politicians failed to pay the tax due investigated Angela Rayner, Keir Starmer, Ian Lavery and Nadhim Zahawi.

Many thanks to Gabriel Pogrund of the Sunday Times, who discovered this story, and to K and M for the REIT and accounting analysis that underpins this report.

Photo of Richard Tice by Laurie Noble, licensed under CC BY 3.0

{kind=link}

Footnotes

Either because of the specific anti-avoidance rule in the REIT legislation or because of the general anti-abuse rule (GAAR). This announcement suggests that there may have been an attempt to technically meet the requirements, notwithstanding that the shareholders were all connected to Mr Tice, rather than an actual attempt to find genuine outside investors ↩︎

The accounts show that almost all the profits were property rental profits – see the “expected tax charge” line in the tax reconciliation. The accounts use the term explicitly. ↩︎

Apparently this was subsequently brought onshore; we’re not aware of the details. ↩︎

The cash flow statement does show £36,150 of “Income taxes paid” but that’s too small to be the tax that should have been withheld; we expect it was another item (the most common cause of REITs having a tax liability is failure to distribute 90% of their property rental profits, but there are several other ways tax can arise). Withholding tax could also be included in the “dividends paid” line, but the figures here are the same as the cash dividends (and so zero in 2020); there is no sign here either of any tax. ↩︎

If that results in double taxation, then it is possible (but far from certain) that HMRC would in practice not collect the tax (as that would result in economic double taxation); we expect that HMRC would still apply penalties. ↩︎

The original version of this report said that the usual penalties regime applied, meaning probably 15%. However that is likely incorrect; there is no specific tax-geared or daily penalty that applies to a failure to withhold tax. The position is probably that if Quidnet filed an incorrect CT61 then penalties are limited to £300 per return, or £3,000 per return if it was careless. So plausibly £15,000 overall. If, on the other hand, Quidnet did not file CT61s art all then the penalty is probably limited to £300 per return, so £1,500 overall. Daily penalties only start to run after notification from HMRC. This is a curious result and at some point it would make sense to bring withholding tax penalties in line with the usual penalty rules. ↩︎

The remaining shareholders were RJS Tice Family SIPP (36.04%), and NJG Tribe SIPP (1.75%) and three UK companies: Tisun One Ltd (9.21%), Tisun Two Ltd (9.19%), Tisun Three Ltd (9.19%). ↩︎

The shareholder then gets a credit for the tax withheld, so overall the right amount of tax is paid, and the withholding tax is really just an advance payment. ↩︎

The authority for this is s973(3A) ITA 2007, which says applies the usual rule that the cash value of a scrip dividend is treated as its “amount” for tax purposes. So when we apply the withholding rules, instead of withholding some shares and giving them to HMRC, the requirement is to hold a cash amount. That is by contradistinction with the “funding bond” rules, which (in a different context to a REIT) can require securities to be withheld and handed over to HMRC. ↩︎

These and other corporate announcements can be found on the Channel Islands stock exchange (The International Stock Exchange) website. ↩︎

The small difference is rounding. ↩︎

If 20% had been withheld from the non-exempt shareholders (Tice 15.36% + trust 19.26% = 34.62% of the total), only ~393,700 shares should have been issued instead of 423,040. The difference of ~29,300 shares at £1.617 = ~£47,400. ↩︎

We can go further by reconciling share figures from the confirmation statements filed with Companies House, i.e. starting with share ownership figures in the July 2019 confirmation statement and adding in the shares that would have been received if tax had not been withheld; that equals the holdings we see in later confirmation statements. This confirms that Mr Tice and the trust received the gross number of shares – more on that below in the footnote to the second dividend. ↩︎

A further 567,051 shares were issued as new equity to fund a property acquisition. ↩︎

Perhaps the announcement was just sloppily worded and in fact tax was withheld and Mr Tice and the trust received 80% of the stated numbers? We can eliminate that possibility by looking at the change in Mr Tice’s shareholding from the July 2019 confirmation (when he held 824,100 shares) to the July 2021 confirmation (when he held 917,728 shares). That’s a difference of 93,628: exactly equal to the 64,967 shares he received for dividend 1 plus the 28,661 shares he received for dividend 2. So it’s clear that the shares were issued without any withholding. ↩︎

The announcement says that the option to subscribe was offered to shareholders who were directors or employees of the company; we believe this was loose wording and that Mr Tice’s trust also had this opportunity. Our reconciliation of share subscriptions shows that the trust did in fact subscribe for the shares. ↩︎

Because his July 2021 shareholding of 917,728 is exactly explained by his original 824,100 shares plus the two 2020 pro-rata scrip allotments (64,967 + 28,661 = 917,728). He therefore received no new shares from this dividend. ↩︎

The RJS Tice Family Settlement’s holding increased by approximately 40,145 shares between the end of the H1 2020 interim dividend and the July 2021 confirmation statement — precisely matching scrip at the £1.602 issue price; i.e. no shares/tax were withheld. ↩︎

There is a small amount “missing” here. The trust had compounded its holdings to roughly 1,151,028 shares by this point, so a 6p per share dividend means it was actually entitled to a gross dividend of around £69,060. This implies the trust either took the remaining ~£4,760 in cash or there is a source of error we are missing. That’s not clear – so we will conservatively assume there was no cash dividend. ↩︎

The scrip shares (140,304 × £1.602 = £224,767) plus the cash (£168,246) total £393,013 — almost the same as the gross dividend of 6p × 6,542,911 shares = £392,575. ↩︎

It looks like Quidnet failed to file correct confirmation statements for 2022 and 2023, as they show no changes in shareholdings, but the July 2024 confirmation statement shows the trust holding 1,231,784 shares – i.e. a difference of 40,611 shares. ↩︎

Mr Tice’s holdings at this point were 917,728 shares. So 917,728 x 5.3p x 40/184 = £10,574. ↩︎

The trust’s holding at this point was 1,231,784 shares. So 1,231,784 x 5.3p x 40/184 = £14,192. ↩︎

The cashflow statement on page 14 of the 2022 accounts shows £69,095 of tax paid in 2022. That is almost exactly the same as the £69,098 of corporation tax shown on page 19. We conclude that no tax was deducted from dividends in 2022. ↩︎

Companies House flaw exposed five million directors and enabled company hijacking

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

The bizarre UK group selling US tax fraud to hundreds of Britons – and prosecuting its critics

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Samuel Leeds: the “property guru” and his bogus tax loopholes

Leave a Reply to Tom Cancel reply