A business called Liberty Rock is marketing a bizarre tax “solution”: supposedly paying your tax by sending HMRC a “magic cheque” which claims to be a bill of exchange. HMRC has issued a “tax fraud” warning about these schemes. We agree: this looks like fraud. We are publishing full details of the Liberty Rock scheme, and naming those involved.

18 June 2026: update – HMRC has published another warning. Also note that, despite the very serious accusations in this article, we never heard from Liberty Rock or their lawyers.

The scheme

The idea is simple:

- The client pays Liberty Rock a fee equal to 25% of its tax bill (plus VAT). Thirty per cent of the fee is payable up-front.

- Liberty Rock then sends HMRC a piece of paper labelled a “bill of exchange”, instead of money, and the client is told the tax has been “settled”.

- The bill of exchange is supposedly drawn on a trust fund created when the client, or its director, was born and their birth registered.

- HMRC will not accept the bill of exchange as payment. But Liberty Rock’s scheme treats HMRC’s receipt of the document as if it were acceptance, and claims the tax is no longer owed.

- One of Liberty Rock’s directors then swears an affidavit before a notary, stating on oath that HMRC has accepted the bill of exchange in settlement of the account, and that the account is “settled in fact”.

- The notarised affidavit is then waved at HMRC enforcement officers and, if the company is wound up, at the court — supposedly as evidence that the tax has been paid.

The reality

HMRC describe these schemes as tax fraud, and say they will not accept even valid bills of exchange as payment for tax liabilities. We would go further: the bills of exchange schemes we have seen depend on invalid bills of exchange. They have to. The whole idea is to make an HMRC liability magically disappear – and that means pretending to create money out of nothing.

That is why Liberty Rock’s materials invoke the conspiracy theory that everyone has a personal trust account created when they are born. The idea emerged from far-right anti-government movements in the United States in the early 1980s, and became part of what is now often called the “sovereign citizen” movement. It is a bizarre theory for any business to market — let alone one presenting itself as a financial services company.

A real “bill of exchange” is a document with three parties: the drawer, who writes and signs the bill, the drawee, who is told to pay; and the payee, who gets paid. A cheque is the most common example.1 But there’s nothing magic about a bill of exchange – it’s not legal tender, and neither HMRC nor anybody else is required to accept one (which anyone who’s tried to pay with a cheque recently will have discovered).

The idea that bills of exchange have special properties was popularised in the United States in the 1990s and 2000s by sovereign-citizen promoters such as Roger Elvick, a serial fraudster, and Winston Shrout.2 The US Treasury says: “The theory behind their use is bogus and incomprehensible”. HM Treasury issued a similar warning in 2019. The same “money for nothing” ideas were dissected in the landmark Canadian case of Meads v Meads.3

Tax barrister Andy Wood was, we think, the first to write about the scheme’s recent use in the UK (he describes the schemes as “magic beans”). The scheme started life a couple of years ago as supposed SDLT “planning” – buy a property, file the return, and “pay” the SDLT with a bill of exchange drawn on your “birth trust”. The bigger and newer danger is that it has migrated into the umbrella-company sector – companies that employ hundreds or thousands of contractors, and on-supply them to recruitment companies and thence to public services and businesses. Umbrella companies have been used for numerous fraudulent schemes to avoid PAYE and other taxes, and unscrupulous operators see bills of exchange as another “solution”.4 These umbrella schemes always have a limited life before HMRC shuts them down – the bills of exchange scheme appears to be being used to confuse and delay HMRC, and prolong the life of the umbrella schemes.

We believe the Liberty Rock scheme has reached the courts on at least three occasions – and each time it has failed:

- Last year, in DG Resources Ltd v HMRC [2025] EWHC 2208 (Ch), a company engaged Liberty Rock, which wrote to HMRC saying that “payments were made in the form of cheques sent to HM Revenue and Customs, clearing within three days of receipt”. This was false. The Court ruled that HMRC had not in fact been paid.5

- There was a recent attempt to use the scheme by Halifax Rugby League Football Club Limited – that also failed, with the court holding that HMRC was entitled to decide which forms of payment it accepted, and the documents sent to HMRC were not valid bills of exchange. The judgment does not mention Liberty Rock, but we understand it was their scheme. The club subsequently went bust.

- And Direct Back Office Ltd, the company which used the affidavit below, was wound up in March 2026. The winding-up order doesn’t mention the affidavit or the bill of exchange – perhaps the company didn’t bother running the argument.

We don’t know what the facts were in the three cases above, and what involvement the companies and their directors had. We weren’t able to contact the three companies to ask.

It’s possible the companies didn’t understand anything and believed that the scheme was valid. We are, however, sceptical that anyone with any legal or business experience would think that.

The documents

It’s hard to believe anyone would run a scheme like this – that’s probably why Liberty Rock try to keep it very quiet. There’s no mention of it on their website, and when they hand materials to potential clients, they’re marked “STRICTLY PRIVATE AND CONFIDENTIAL – FOR AUTHORISED RECIPIENTS ONLY”.

We have, however, received Liberty Rock documentation from multiple independent sources. The documentation we’ve seen includes:

This “process and practice guide”, stating the fee right at the top:

And here’s a background briefing, containing the claim that the registration of your birth creates a “birth trust” holding valuable assets which you can access with a bill of exchange.

This is one of the documents implementing the scheme to pay a £3m tax bill. It’s a notarised affidavit, signed by Andrew Jackman, a director of Liberty Rock, for a company called Direct Back Office Ltd:

Liberty Rock

Liberty Rock’s public website makes extensive claims about expertise in tax, accountancy, asset protection, finance, investment, offshore structuring and litigation support, but does not identify any individual advisers, directors, professional qualifications, regulatory permissions, or named responsible persons. That absence is surprising given the nature of the services advertised.

The company is owned and run by Scott-Havard Williams and Andrew Donald Jackman. According to its accounts, it had £863,542 of cash in the bank at 31 January 2025; we understand the business has generated significantly more cash since then. There are a large number of similarly named companies.

Mr Williams is currently the subject of director disqualification proceedings. He was born Scott Havard Williams and changed his name by deed poll to “Scott-havard Williams” (sovereign citizens are often obsessed with capitalisation).

Mr Jackman may be connected to sovereign citizen fraudster Iain Clifford Stamp.6

Liberty Rock didn’t respond to two requests for comment by email, and their telephone lines were never answered.

The notary

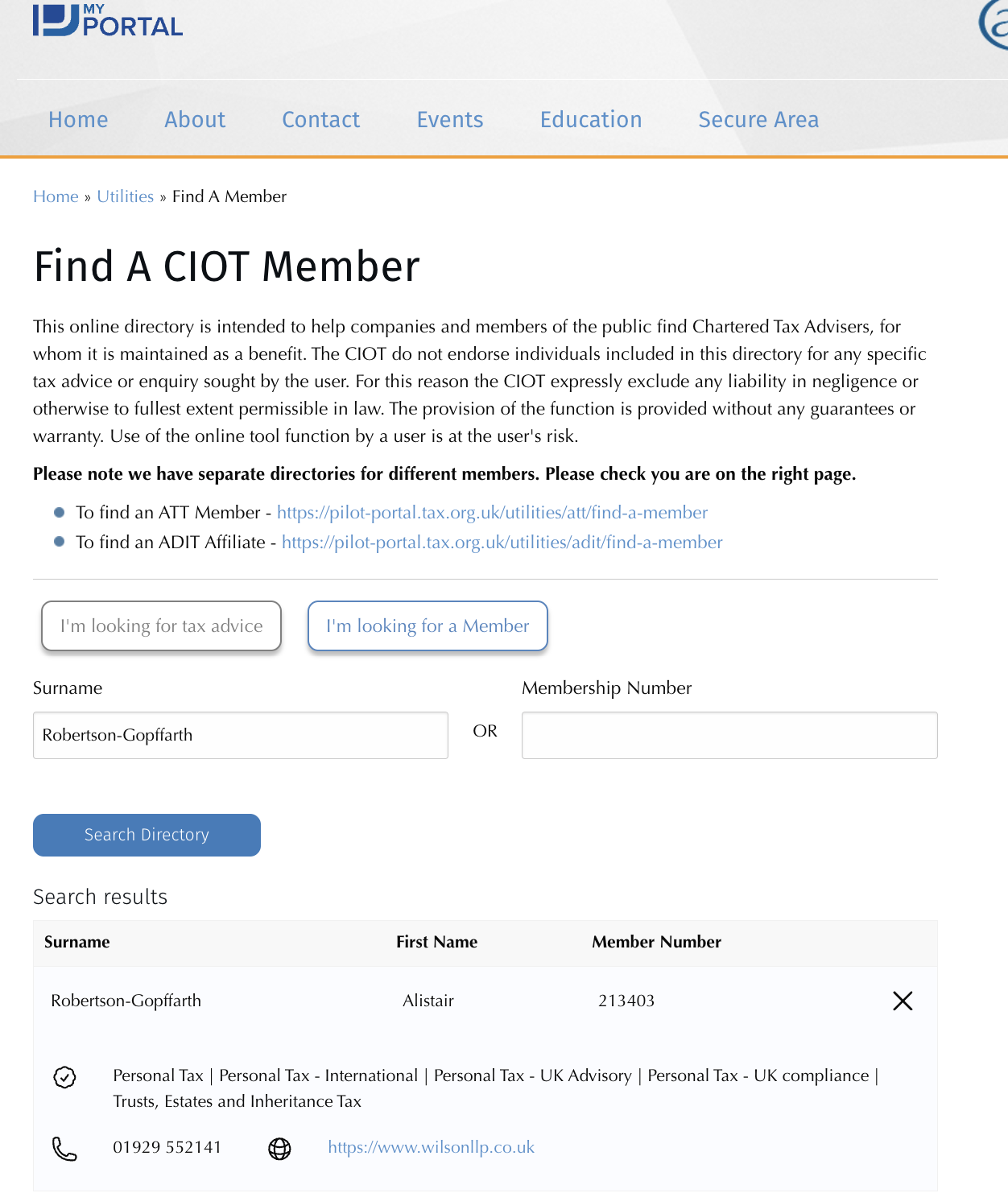

The whole Liberty Rock scheme is built on the notary’s seal. The notarised affidavit is what the client waves at HMRC field officers at the court at the eventual winding-up hearing. A notary public who notarises a statement that “HMRC accepted a bill of exchange in the sum of £3,000,000” lends the scheme the only piece of legal credibility it has.7

A notary public is a specialist lawyer, distinct from a solicitor, appointed and regulated by the Faculty Office of the Archbishop of Canterbury. There are only around 800 of them in England and Wales. Their job is to attest the authenticity of legal documents – typically for use abroad, where the notary’s seal is treated as conclusive proof that the document is what it says it is, was signed by the person named, and was sworn in proper form.8 Notaries are not rubber-stamping machines. A notary is required to make sufficient enquiries to be satisfied that no fraud is involved.9

All the affidavits we have seen were notarised by Alexander Alistair John Robertson-Gopffarth of ARG Notary, Holt, Dorset. Mr Robertson-Gopffarth told us that he did not prepare the affidavits, did not verify the claims within them, but says he verified the identity and status of the declarant in the standard manner, and denies fraud or misconduct. We don’t believe he made sufficient enquiries – the documents contained obvious signs of impropriety:

- The phraseology at the start of the affidavit (“I, a man by the name of Andrew Donald Jackman“) and at the end (“verify on my full and unlimited commercial liability“) should have raised an immediate red flag. It’s not how English law legal documents are written. It suggests something peculiar is going on, and is redolent of sovereign citizen frauds.

- Then the obvious point: nobody settles a multi-million pound HMRC liability by sending HMRC a “bill of exchange”.

- The suggestion that the Chief Executive Officer of HMRC had personally “accepted” such documents in settlement of tax debts was extraordinary and implausible.

- The statement that a mere Royal Mail proof of delivery “verified” acceptance by HMRC was also plainly wrong, as is the idea that this meant an account was “settled in fact”.

- As well as being a notary, Mr Robertston-Gopffarth is a solicitor and a chartered tax adviser. We understand he has notarised numerous similar affidavits. He failed to identify an obvious pattern.

{kind=link}

We have made a complaint of notarial misconduct to the Registrar of the Faculty Office.

Our full correspondence with Mr Robertson-Gopffarth is here.

Shortly after we first published this article, the Faculty Office published an alert warning notaries about the bills of exchange schemes, and saying that “Notaries encountering such matters should carefully consider whether the proposed act is proper in the circumstances and whether independent legal advice should be recommended to the client”.10

What should the consequences be?

We believe there is sufficient evidence for a criminal investigation of the individuals behind Liberty Rock, as well as their clients and others who have used the scheme. We make no specific claim as to who these individuals are, other than that Mr Jackman appears to have signed the affidavit.

In particular:

- The claims by Liberty Rock are false and we do not believe an honest person with any knowledge of the legal and financial system could think otherwise.

- The Liberty Rock letter quoted in the DG Resources case as saying that the “cheques” cleared within three days of receipt. That claim was false.

- Any claim that sending HMRC a worthless “bill of exchange” has settled a liability is a false representation.

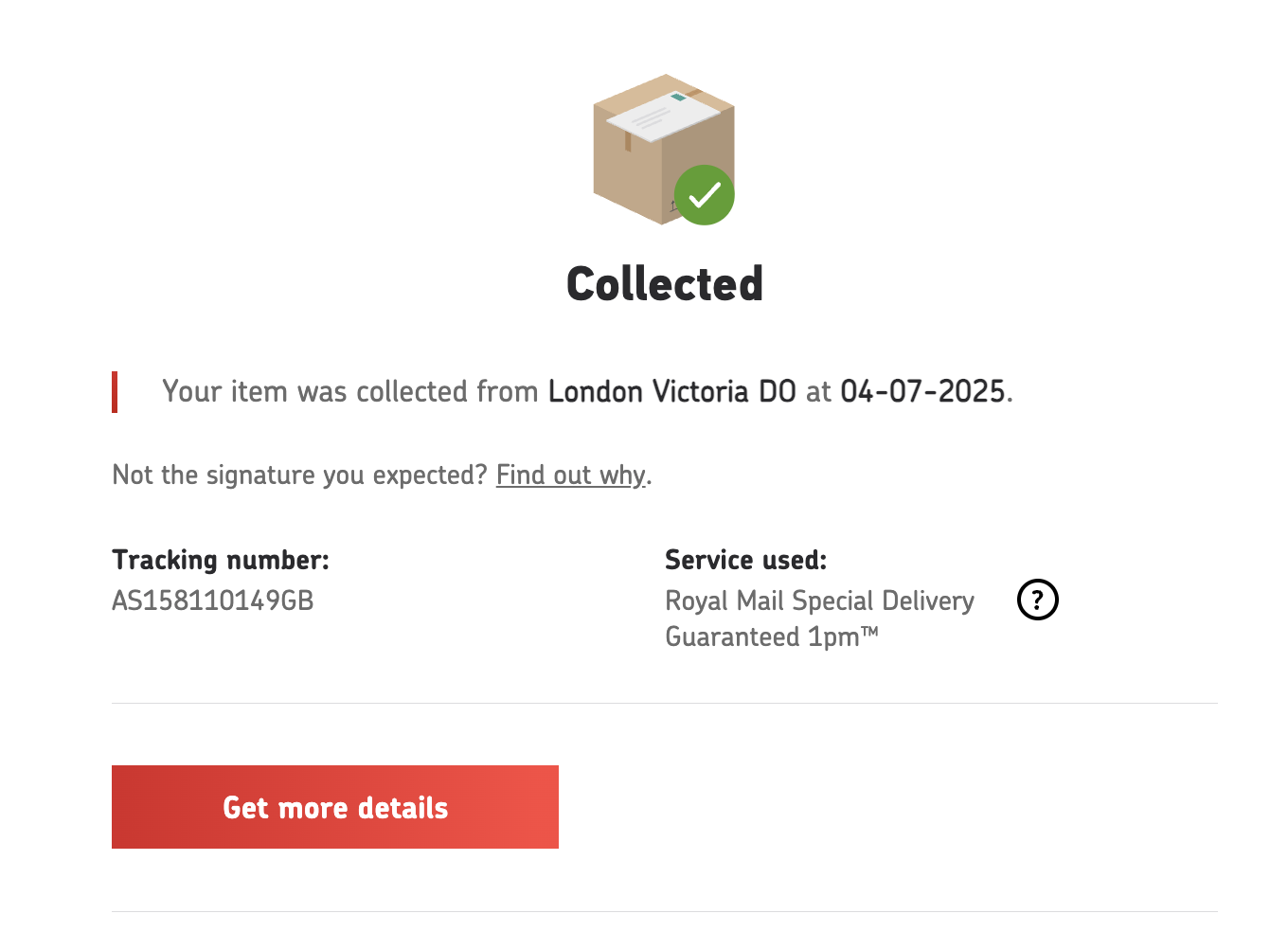

- The affidavit (sworn by Mr Jackman) says HMRC’s acceptance was “verified by a Royal Mail proof of delivery”. But the Royal Mail record does no such thing. It merely says the item was “collected” from London Victoria Delivery Office on 4 July 2025. It does not show delivery to HMRC, a signature, acceptance by HMRC, acceptance by HMRC’s Chief Executive, or settlement of any tax debt. In any case, the idea that the Chief Executive of HMRC sits around accepting cheques is risible.

{kind=link}

The most likely offences would be cheating the public revenue (which potentially carries life imprisonment), or fraud by false representation (the usual prosecution route where someone attempts to pay with a false cheque).11

For fraud by false representation, the question would be whether those involved dishonestly represented that the bill of exchange settled, or would settle, the tax liability, knowing that representation was or might be untrue or misleading, and intending thereby to make a gain or cause HMRC a loss or risk of loss. For cheating the public revenue, the question would be whether there was dishonest conduct intended to prejudice, or risk prejudicing, HMRC’s revenue.

We expect this would come down to whether the person in question was “dishonest”.

Under English law, determining whether a person was “dishonest” means asking whether their conduct was dishonest by the standards of ordinary decent people (regardless of whether the individuals themselves believed at the time that they were being dishonest).12

The leading textbook of criminal law and practice, Archbold, states:

“In most cases the jury will need no further direction than the short two-limb test in Barton “(a) what was the defendant’s actual state of knowledge or belief as to the facts and (b) was his conduct dishonest by the standards of ordinary decent people?”

Those involved may say that they genuinely believed the schemes worked. Whether that is true, and whether a jury would believe such an explanation, is a question of fact. However the outlandish nature of the scheme means that the criminal barristers we spoke to thought this would be an eminently prosecutable case.

HMRC’s response

We asked HMRC for comment. They told us:

“We are taking action against promoters of these schemes and welcome any information about those promoting them. We also urge anyone already using this payment arrangement to contact us as soon as possible.”

Many thanks to Andy Wood for his excellent Taxation Magazine article on which we have drawn heavily, and to Kareena Prescott for her article.

Thanks to all our sources in the recruitment industry – who must remain anonymous – for information on Liberty Rock and providing us with the underlying documents.

Documents © their authors and reproduced here in the public interest and for purposes of criticism and reporting on crime. The “Strictly Private and Confidential” marking on the Liberty Rock client document is of no legal effect: there is no confidentiality in iniquity.

The British fugitive, his $600m US tax fraud, and its 3,000 victims

Matrix Freedom – the scam conspiracy theory that makes £500k a month from the vulnerable

Inside a fake tax refund factory

The bizarre UK group selling US tax fraud to hundreds of Britons – and prosecuting its critics

Finance Monthly fabricated an interview with me

Herran Finance – another fake bank at Companies House

Footnotes

Historically bills of exchange were very important to facilitate international trade. The exporter draws a bill on the foreign importer, sells the bill to a discount house for cash, and the discount house collects from the importer at maturity. ↩︎

Shrout was convicted of fraud in 2018. He inspired Simon Goldberg, the subject of our “Empower the People” investigation. ↩︎

See the discussion of “money for nothing” schemes from paragraph 531 onwards, and the specific discussion of bills of exchange around paragraph 545. ↩︎

One of the directors, Scott-Harvard Williams, is also a director of an umbrella company, UK Pay Ltd. That company was recently the subject of an HMRC winding-up petition, with a hearing on 13 May 2026. ↩︎

DG Resources subsequently won a procedural appeal on service grounds ([2026] EWHC 201 (Ch)) but the substantive finding that no payment was made was unchallenged. ↩︎

This and other websites making the claim are created by critics of Stamp, some of whom are themselves sovereign citizens and/or criminals. So we would certainly not accept this as compelling evidence of a connection. We have, however, also received anecdotal reports of a link. ↩︎

This has been a particular problem in Canada – the Law Society of Alberta has published specific guidance. ↩︎

The notarial profession is statutorily regulated under the Public Notaries Act 1801, the Courts and Legal Services Act 1990, and the Legal Services Act 2007, with the Master of the Faculties as approved regulator. Notaries are bound by an approved Code of Practice and Practice Rules, the Notaries (Conduct and Discipline) Rules, and the Notaries (Prevention of Money Laundering) Rules 2008, and must make an annual Statement of Professional Independence. ↩︎

The Court of Faculties can suspend or strike off notaries for misconduct, impose practice conditions or further training, or order compensation. ↩︎

Thanks to the anonymous commentator below for drawing our attention to this. ↩︎

There are other possible offences, for example conspiracy to defraud. ↩︎

The subjective element of the test for dishonesty (see Ghosh (1982)) was removed by Ivey [2017] for civil cases, and that decision was confirmed to apply to criminal cases in Barton [2020]. The fact that a defendant might plead he or she was acting in line with what others were doing, and therefore did not believe it to be dishonest, is no longer relevant if the jury finds they knew what they were doing and it was objectively dishonest. ↩︎

Leave a Reply