During the pandemic, Douglas Barrowman’s company, PPE Medpro, sold £200 million of PPE to the Government. It made £65m profit, which went into trusts benefiting Barrowman and Mone’s families. Most of the PPE was later ruled to breach sterility standards but, rather than repay the money, Barrowman put PPE Medpro into administration.

New documents show HMRC is now claiming £39 million in tax, in addition to the £122m (plus interest) owed to the Government for the faulty PPE. We think we know why.

Barrowman companies have previously run aggressive tax avoidance schemes and, when they failed, entered administration so that no tax was paid. The evidence suggests he may have done the same again – using a scheme to avoid tax on the £65m, and an administration to ensure that any HMRC challenge is pointless.

However new rules mean that this may not be the end of the story. HMRC may be able to recover the £39m from Barrowman personally.

In this report:

Barrowman’s history of selling avoidance schemes

Barrowman styles himself as an entrepreneur. In reality, most of his money was made from selling highly aggressive tax avoidance schemes. When, inevitably,1 HMRC cracked down on the schemes, his clients were left with huge liabilities, many were financially ruined, and four died by suicide.

We believe there is evidence that some of these schemes involved deception: of HMRC, his own clients and his commercial counterparties, and we’ve called for this to be investigated as potential fraud.

As well as selling failed avoidance schemes, Barrowman’s companies have a history of disregarding their legal obligations. Two Barrowman companies unlawfully failed to disclose their tax avoidance schemes to HMRC. One of these companies then unlawfully failed to comply with an HMRC information request. And Barrowman continues to unlawfully hide his ownership of companies – he has admitted lying about concealing his ownership of PPE Medpro, but the company’s records still fail to record Barrowman as the beneficial owner.2

Barrowman’s history of avoiding tax himself

We know about at least one previous case where Barrowman made a profit from a transaction, avoided UK tax on that transaction, and then put the company into administration before HMRC could challenge the arrangements.

In July 2008, a Spanish company called B3 Cable Solutions made a €6.3m payment to a UK company⚠️, Axis Ventura Limited. That payment was intended to be tax-deductible, reducing B3 Cable Solution’s Spanish corporate tax bill by €1.6m (and the Spanish tax authorities challenged this.3) Axis Ventura Limited then proceeded to avoid UK tax on the €6.3m it received. It paid all the money to an employee benefit trust, which made loans to directors/employees and/or their dependents4. We expect neither the company nor the beneficiaries of the loans paid any tax5 on the loans.6

Barrowman’s history of walking away from the consequences

After extracting their cash from the company, without paying any tax, Axis Ventura Limited was put into administration.

In other words, Barrowman and his team walked away from Axis Ventura Limited – winding it up with no cash, in circumstances where it was in my view likely that HMRC would raise an enquiry and seek to recover tax, and it is (at the very least) plausible Barrowman and the others involved knew that they would. The directors nevertheless signed a declaration of solvency.

This is a classic way to eliminate all risk of tax avoidance. You run your tax avoidance scheme in a company without many assets, make sure you have documentation showing that you believed the avoidance worked, and then wind up the company afterwards, making any HMRC enquiry pointless. It’s sometimes called a “bottom of the harbour” scheme.7There are rules enabling HMRC to go after shareholders in some circumstances but those in existence in 2008 didn’t apply to PAYE. There were other rules potentially applicable; we assume they were not used.

In the event, HMRC assessed the company to owe £1.4m of tax, but it doesn’t look like they were ever able to recover this.8

As is typical of Barrowman9, he almost, but not quite10, denied any involvement in Axis Ventura Limited.11

This is not the only case where a Barrowman-linked company avoided tax and was then put into insolvency. AML Tax (UK) Limited, a company used to sell the doomed contractor tax avoidance schemes, owed £159k of tax and penalties: it made two tax appeals and, when it lost, went into insolvency, never paying a penny.

Is that what Barrowman did with PPE Medpro?

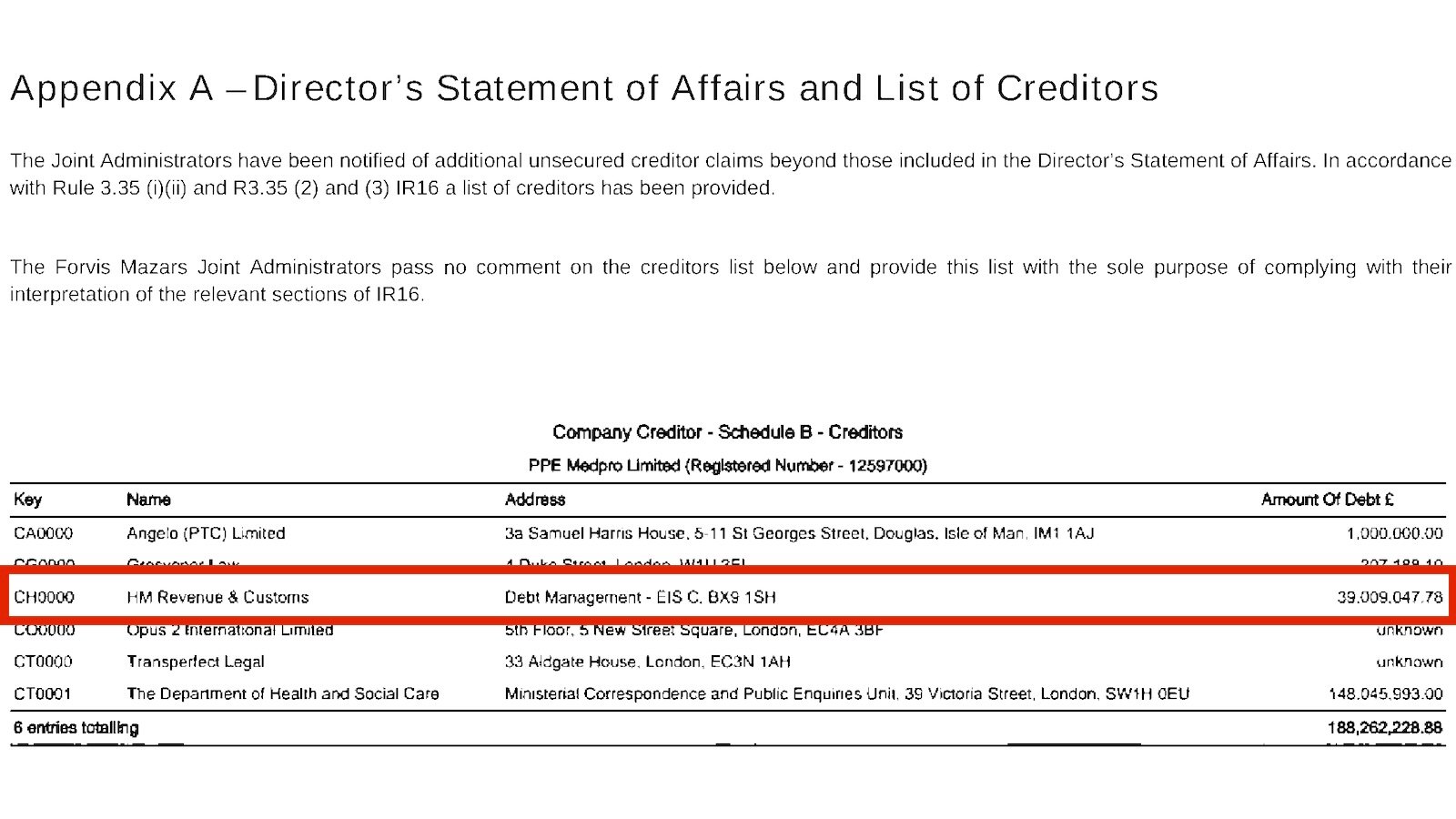

It’s been reported that PPE Medpro made a £65m profit, which ultimately ended up in trusts and companies controlled by Barrowman.

A normal company in PPE Medpro’s position would have paid corporation tax of around £12m (19% of £65m) and then paid a dividend of the remaining £53m to its shareholders.12

There’s no sign of that in PPE Medpro’s accounts, and it seems unlikely that is what happened. PPE Medpro’s administrators13 just published a report, which, says:

“A review of the Company’s bank statements reflects a small number of entities that have received the vast majority of funds from the Company’s bank account.

Information requests have been issued to third parties who appear to have relevant information and/ or documentation which will aid in this review. No further information can be provided at this time whilst investigations remain ongoing.”

That, plus Barrowman’s history, suggests to us that no dividend was paid, and instead payments were made to companies/trusts. That is one of the scenarios we discussed when we first looked at PPE Medpro’s accounts.

The administrators report says HMRC claims to be owed £39m.14 What could be the reasons for this?

£39m is a lot more than the £12m of corporation tax we’d expect PPE Medpro to pay. But what if PPE Medpro did something similar to Axis Ventura Limited, but on a larger scale?

We would speculate, based on the past actions of Barrowman entities, that the facts could have been something like this:

- Barrowman acted as a shadow director of PPE Medpro Ltd – someone who isn’t officially a director, but acts as one, and is therefore regarded as a director by the Companies Act.15

- PPE Medpro extracted its profits as a £65m payment to an entity. This was, in essence, a means of providing a reward to Barrowman.

- That entity then made an on-payment to a trust or other entity chosen by Barrowman.

- PPE Medpro claimed the £65m payment was deductible, meaning it had no corporation tax liability, and no other entity or person paid tax on the amount.

That would be a typical Barrowman avoidance scheme. There would probably be other elements, intended to defeat the relevant anti-avoidance rules; but the history of the last 25 years is that such schemes inevitably fail in the courts.

The consequence for PPE Medpro of the scheme failing would be:

- PAYE income tax at 45% = £29m

- Employee national insurance: at 2% = £1m

- Employer national insurance at 13.8% = £9m

That totals £39m. It’s quite the coincidence that’s the same number HMRC is claiming.

Likely it’s not as simple as this – the actual profit may be smaller, and we’d expect HMRC to charge interest. But this for now is our best guess as to what the £39m represents.

It’s important to say that this is informed speculation. We do not know that this is what happened. It is possible that Barrowman paid the corporation tax in full. We haven’t asked Barrowman’s lawyers for comment because he has a history of instructing his lawyers to lie to the media.

Will Barrowman get away with it again?

It’s not 2008. It’s harder for people to strip assets from companies using tax avoidance schemes and then walk away.

Under the “joint and several liability notice” rules, introduced in 2020, shadow directors and others can be jointly and severally liable if a company avoids or evades tax and then becomes insolvent.16

We would expect HMRC is considering whether and how to apply these rules to PPE Medpro.

Many thanks to K for accounting input, C for insolvency law advice, and M for his remuneration tax expertise.

Footnotes

The Government had previously warned that remuneration avoidance schemes would be subject to retrospective liability. This is what happened. Barrowman’s companies failed to pass this critical warning to their clients; in any event the schemes were technically hopeless (and retrospective legislation was employed because the sheer number of schemes meant that individually challenging them was impracticable). Our view is that it’s fair to blame HMRC for not cracking down on the schemes at an early stage, but ultimate responsibility for mis-selling technically hopeless avoidance schemes rests with Barrowman and other promoters. We’ve more on the history here. ↩︎

This is a recurring theme. AML Tax (UK) Ltd, the tax that breached the DOTAS and information notice rules, never recorded Barrowman as its beneficial owner. The court appointed liquidator thought that he was the true beneficial owner. ↩︎

They prosecuted Barrowman and others for tax fraud; Barrowman and the others were cleared; we don’t know the outcome from a Spanish civil tax perspective, but the Spanish tax advisers we spoke to have said that the reported remarks of the judges imply that a deduction was not in fact available. ↩︎

We know about the EBT from the 2008 accounts, which include a curious reference to a £61,000 investment “previously held on the balance sheet [which] was not owned by the company” – we don’t know what that could mean. ↩︎

That said, it’s not clear how the company obtained a deduction given Schedule 22 FA 2003 and Part 12 CTA – possibly there was some additional structuring here that’s not visible in the accounts of the liquidator’s report. Given the history of Barrowman’s companies, it’s unlikely they just forgot about the point – there would have been some “structuring” intended to defeat these rules, albeit the kind of “structuring” that hasn’t succeeded in any UK court decision for many years. We don’t believe it’s legitimate to plan your taxes on a basis that the courts have repeatedly rejected. ↩︎

This was in our view clearly tax avoidance. The intention of Parliament was that people pay tax on their remuneration. Recasting that remuneration in the form of a “loan” (scare quotes because few if any of these loans were intended to be repaid) subverts that intention. Nevertheless, a surprising number of people at the time thought that the EBT/loan structure “worked”, including a series of tax tribunals, and it took a decision of the Inner House of the Court of Session (broadly the Scottish equivalent of the Court of Appeal) and then the Supreme Court to reach the sensible and obvious conclusion that payments to EBTs were “earnings” and should have been subject to PAYE. We wrote about some of the history of these schemes here, but it’s important to note that those tribunals, which found in favour of the schemes did so on the basis of an understanding that the loans were intended to be repaid. That understanding was in most cases based on deceit from scheme promoters and users – the planning only makes sense in most cases if the loan is not intended to be repaid, and in almost no cases were loans actually repaid. ↩︎

Although strictly that term relates to a practice in Australia where there was no tax avoidance – just asset-stripping a company and leaving it to go bust with unpaid tax. We don’t normally recommend Wikipedia articles, but this is a good one. ↩︎

The liquidation converted into an insolvent liquidation in 2015. HMRC kept the insolvency going for years, even though the company had no assets – the only reason we can think of for HMRC to take such a step would be because they were looking into whether they could recover some of the £1.4m from Barrowman and other current/former shareholders and directors. The insolvency finally concluded in July 2021, with the company wound up, still owing £1.4m to HMRC. ↩︎

This all follows the established pattern: a company associated with Barrowman does something questionable, and he denies being a shareholder or director. In at least two cases (PPE Medpro and Vantage Options Limited) we know those denials were lies. In those cases the apparent shareholder was actually a trustee of a trust which was (in practice if not in legal theory) controlled by Barrowman. ↩︎

Here’s what he doesn’t deny: being the ultimate beneficial owner and the person who ultimately controls the company. We asked his lawyers last year if they would comment; they declined. ↩︎

Until 28 March 2008, Barrowman was a director and shareholder of Axis. The other director was (and remains) Timothy Eve, deputy chairman of Barrowman’s Knox business. After Barrowman stepped down, Michael Walton and Mark Price Williams became directors, and Paul Ruocco became the shareholder. Williams and Ruocco are frequent Barrowman associates. Walton was the original owner of Tri-Wire, a company acquired by B3 Cable. From April 2016, the “person with significant control” of Axis should have been registered. But nobody was listed as the PSC, not even Paul Ruocco, who held all the shares. That kind of non-compliance is typical for Barrowman-linked companies.

So whilst we can’t know for sure who was really controlling Axis Ventura Limited, the individuals involved, the non-denial, Barrowman’s past behaviour, and the existence of the prosecution, all suggest that Barrowman was controlling or at least influencing the company even after he ceased to be a shareholder. ↩︎

PPE Medpro was never owned by Barrowman, or another Barrowman company. Its sole shareholder has always been a Barrowman employee. Barrowman has admitted that he’s the ultimate beneficial owner of PPE Medpro, but PPE Medpro’s Companies House entry claims that these employees are the sole beneficial owners. That seems likely to be untrue, and indeed a criminal offence. We expect in reality the named Barrowman employees have owned PPE Medpro as trustees of a trust. ↩︎

There were originally joint administrators, Mazars and Clarke Bell. Clarke Bell recently resigned; we don’t know why. ↩︎

The report also identifies that the directors say HMRC owes them £948k. This could be VAT. PPE Medpro wasn’t required to account for VAT on its sales of PPE because, at the time, PPE was zero-rated. If PPE Medpro incurred VATable costs (e.g. legal fees) then ordinarily it could have been able to recover the costs. ↩︎

And also – critically – by remuneration tax anti-avoidance rules, which treat shadow directors in the same way as directors. ↩︎

It’s also possible that PPE Medpro’s administrators will be able to recover tax from Barrowman or other persons to whom payments were made. Some insolvency practitioners have been successful in recovering tax from directors after HMRC pursued failed avoidance schemes. Whilst the administrators of PPE Medpro were appointed by a Barrowman entity, they owe duties to creditors generally, and if they don’t act in accordance with those duties then a court can require them to act fairly, or even remove them. ↩︎

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Tax barristers and fraud: how the Bar responded to our allegations

Rogue barristers are enabling a billion pound tax fraud – and the Bar won’t act

Samuel Leeds: the “property guru” and his bogus tax loopholes

Leave a Reply