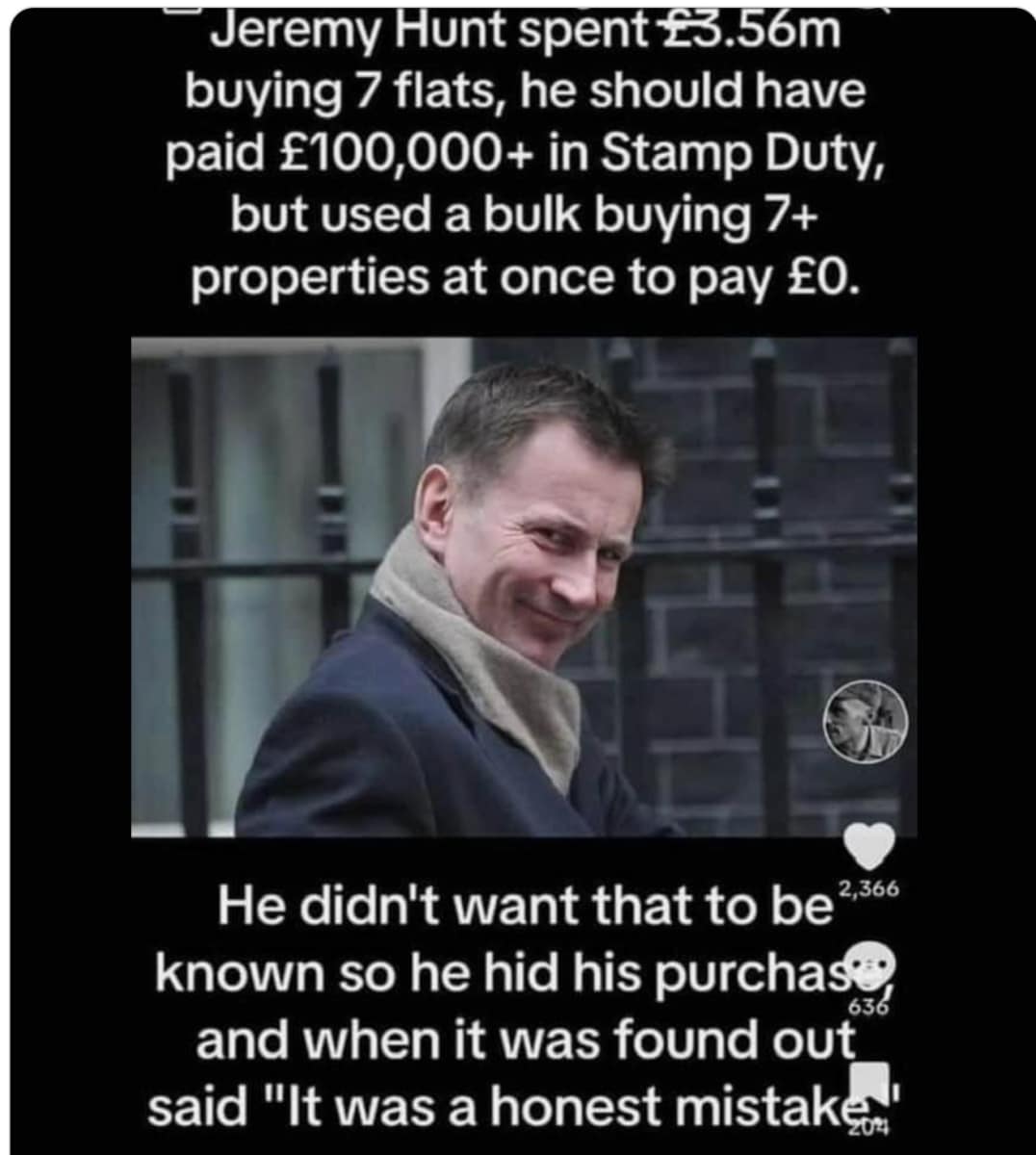

Some people on social media are convinced that Jeremy Hunt avoided tax when he bought seven flats through a company in 2018. We’ve analysed the transaction and believe it’s clear that he didn’t.

Here are the claims (click to expand):1

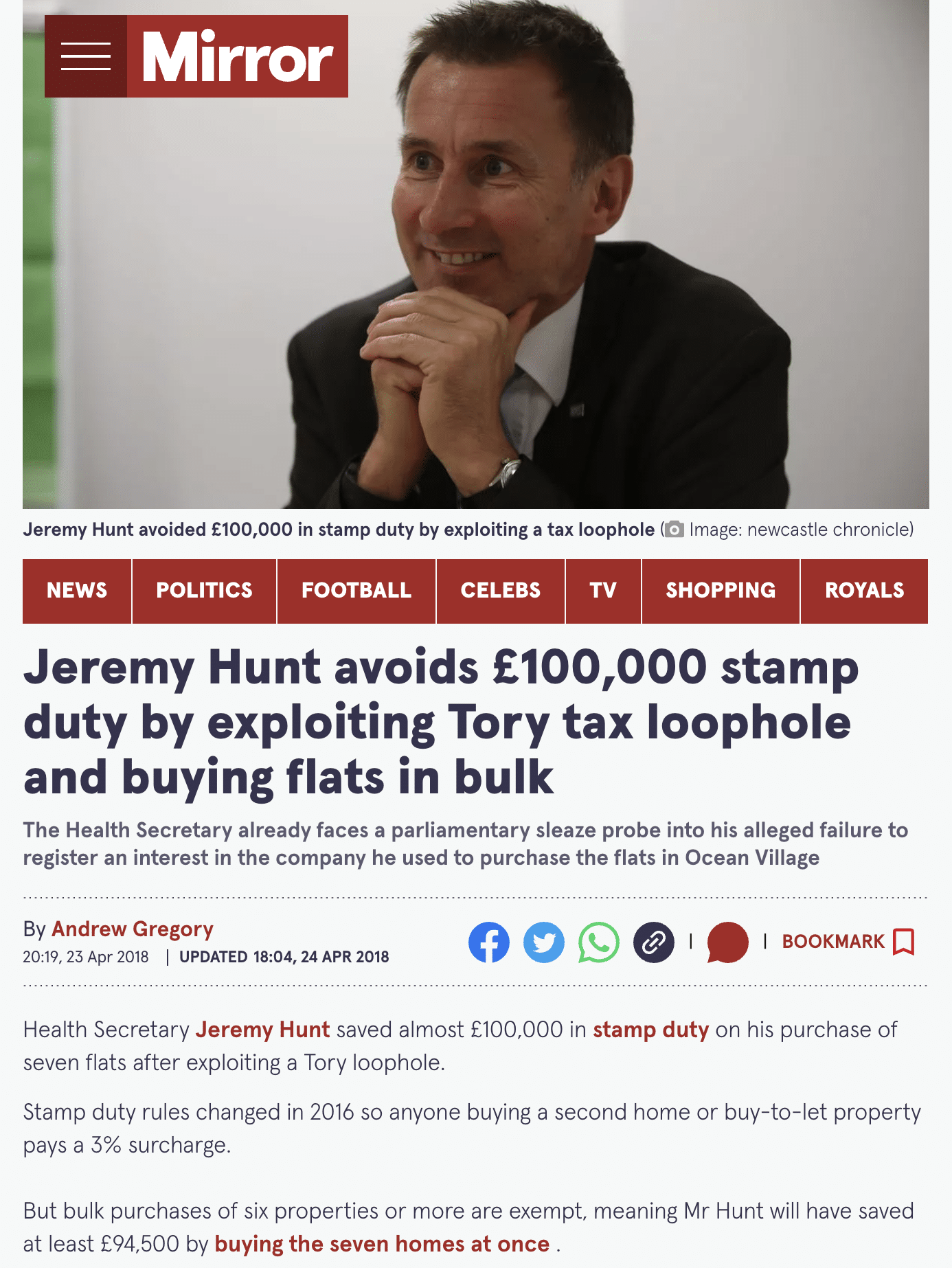

Probably originating from this piece in the Mirror in 2018, itself based on this Telegraph report:

The basic accusation is that Jeremy Hunt “exploited a Tory loophole“ when he bought, through his company, seven flats in Ocean Village in Southampton.

These are different from the false claims that Hunt avoided tax when he sold his education business – we wrote about these back in 2022.

Hunt’s transaction

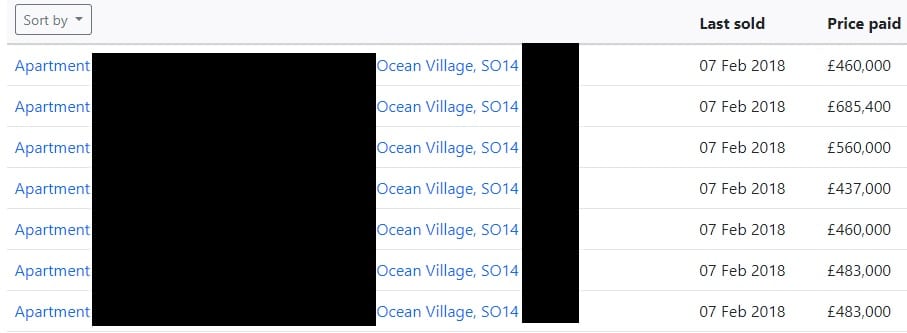

In 7 February 2018 Hunt’s company, Mare Pond Properties Limited, acquired seven apartments. We can see the price paid data on the land registry or from various other online sources:

i.e. a total price of £3,568,400.

How much stamp duty land tax (SDLT) was payable on that?

The actual SDLT result

SDLT rates are very different for residential and commercial property.

Residential property is taxed at escalating rates from (in 2018) 0% to 12%, with an additional 3% if you were acquiring a second (or further) residential property.2 Commercial property, on the other hand, is taxed at much lower rates, which only reach 5%.

So was this a residential or commercial purchase?

One might expect the answer to be obvious: it’s residential, because these were flats that people would live in – and therefore there’s SDLT of around £450k.

But here the obvious answer is wrong, because of section 116(7) Finance Act 2003:

This is the 6+ rule. If you buy six or more dwellings, then it’s treated as a purchase of non-residential property. So you get lower rates, and no 3% additional tax. The rule was included in the original SDLT legislation back in 2003.

And those were the facts here. Hunt’s company was buying seven dwellings from the same seller on the same day in a single transaction.

This means that, instead of £450k, the SDLT due would be £167,920. We can be reasonably sure this is what happened, because it’s consistent with the fixed assets reported in Mare Pond Properties Ltd’s accounts.3

The Mirror and the social media posters therefore all understate the benefit to Hunt of the 6+ rule. He didn’t save £100,0004 – he saved almost £300,000.5

But the critical point is that this wasn’t a choice – s116(7) applies automatically. Hunt didn’t “claim” the 6+ rule – the way the rule works made this inevitable. It wasn’t actually possible for Hunt to pay £450k SDLT.

The alternative SDLT result

Whilst it’s not possible to opt out of s116(7), Hunt’s company could have obtained a different SDLT result if it had claimed “multiple dwellings relief” (MDR).6

MDR means that, when you buy multiple properties at once, instead of applying SDLT to the overall purchase price, you can opt to pay the average SDLT for each property.7 That will usually result in less tax, because the average property will be in a lower band than if the full purchase price was taxed.

An example:

- Say you are buying one £2m property (as a second home) plus one £20k property.

- On the face of it (using 2018 rates, including the 3% surcharge), SDLT on the overall £2,020,000 transaction is £217k.

- But if you claim MDR then you instead work out SDLT on the average property price of £1,010,000. That would be £75k.

- MDR gives a result of 2 x £75k, i.e. £150k

- MDR has saved you £67k.

This might be a straightforward transaction, but it could also be avoidance, where the £20k property is an artifice created to reduce the stamp duty. Here are some examples HMRC has seen:

Because of HMRC’s concern there was widespread abuse, MDR was abolished earlier this year.

What if Jeremy Hunt had claimed MDR?

We can calculate the result like this:

- The average price paid for his seven properties: £510k

- SDLT on a £510k property would have been £31k

- MDR therefore gives a result of 7 x £31k = £215k.

So if Hunt had claimed MDR, his company would have paid £48k more tax.

Why in this case does MDR give a worse result? Because the 6+ rule converts residential properties to non-residential, and that’s more valuable than the MDR effect of applying lower bands.

Did Jeremy Hunt avoid tax?

We would say clearly not.

He bought seven flats and paid the SDLT on that transaction. He didn’t make any kind of claim or election.8 The fact he benefited from the 6+ rule is a natural consequence of how the tax system works. It’s not just the legal outcome, it’s the fair outcome – whether or not you think the 6+ rule is itself fair.9

Now if he’d bought five flats plus one teensy-tiny property just to get within the 6+ rule, then it would be fair to say he avoided tax. But he didn’t.

The fact Jeremy Hunt could have paid more tax by claiming MDR is hardly relevant. There are often things one can do voluntarily to trigger more tax; the failure to do that isn’t tax avoidance.10

There is no single definition of tax avoidance, but we’ve written an FAQ explaining the conventional view is that tax avoidance is using “loopholes” or other features of the tax system to save tax (“obtain a tax advantage”) in a way that wasn’t intended by Parliament. The 6+ rule was absolutely intended by Parliament.

Some people will disagree with that. But we can’t see any coherent definition of “tax avoidance” that includes Jeremy Hunt. He literally did nothing.

Many thanks to S, who researched and wrote almost all of this article (but the views expressed are the views of Tax Policy Associates).

Daily Mirror front page © Reach Plc, and reproduced here for purposes of review/criticism.

Footnotes

We very often look at claims that businesses or politicians avoid tax. Sometimes this follows queries from journalists; sometimes tips from professionals or the public. The great majority of the time we conclude there is no avoidance. Where the accusation hasn’t been publicised, we don’t generally publish our conclusion that there is no avoidance. Where the accusation is published or, as here, gaining traction on social media, we generally do. ↩︎

When a company acquires, in some cases there can be a 15% flat rate but not, as here, when it is acquiring to lease out the properties. ↩︎

The accounts show “fixed assets” of £3,751,666 for 2018. Accounting rules require assets to booked in their historic costs – meaning that this figure will reflect the purchase price, stamp duty and other costs. £3,751,666 = £3,568,400 + £167,920 + £15,346. Suggesting that we have the correct figure for stamp duty, and Hunt’s other costs (legal etc) were £15k, which is in the right ballpark. ↩︎

The £100k is the figure from escaping the additional 3% SDLT, but the 6+ rule also saves the higher residential rates. ↩︎

i.e. compared to the standard SDLT result, with no 6+ rule and no MDR. ↩︎

A tweet I posted last week suggested Hunt had used MDR. That was incorrect. ↩︎

Subject to a minimum SDLT amount of 1% of the overall purchase price – that’s relevant if the average falls below the threshold at which SDLT starts to apply. ↩︎

As an aside, he also didn’t properly declare his interest in the flats in his Parliamentary disclosure, or to Companies House. ↩︎

The likely intended purpose of the 6+ rule, in conjunction with the 3% surcharge, was to continue the Osborne policy of encouraging large-scale professional/institutional landlords, and discouraging small-scale/”accidental” landlords. However there certainly is an argument that the 6+ rule is an unjustifiable relief for landlords. ↩︎

Indeed if he had claimed MDR we would have been suspicious that there was something untoward happening; going out of one’s way to pay more tax is a red flag. ↩︎

Tenancy reform: the accidental stamp duty headache for 150,000+ tenants

Why Angela Rayner is likely to pay £8,000 in stamp duty penalties

The Angela Rayner tax proposals – how much sense do they make?

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Leave a Reply to Dan Cancel reply