Douglas Barrowman and Michelle Mone appear to own a house in Belgravia through two BVI companies and a trust. They should all show Barrowman and/or Mone as the beneficial owner. They don’t. That’s a breach of company law – and potentially a criminal offence.

UPDATE 22 December 2023: The Times has reported that Barrowman sold the Belgravia house earlier this year for £19m. That doesn’t explain or excuse the failure to correctly report the ownership of the company holding it. The sale doesn’t show up in the land registry. Possibly the sale was recent, the filings were delayed, or the land registry has been slow – it’s also possible that this was not a straightforward sale, but some kind of aggressive arrangement to avoid tax. Barrowman has form for this.

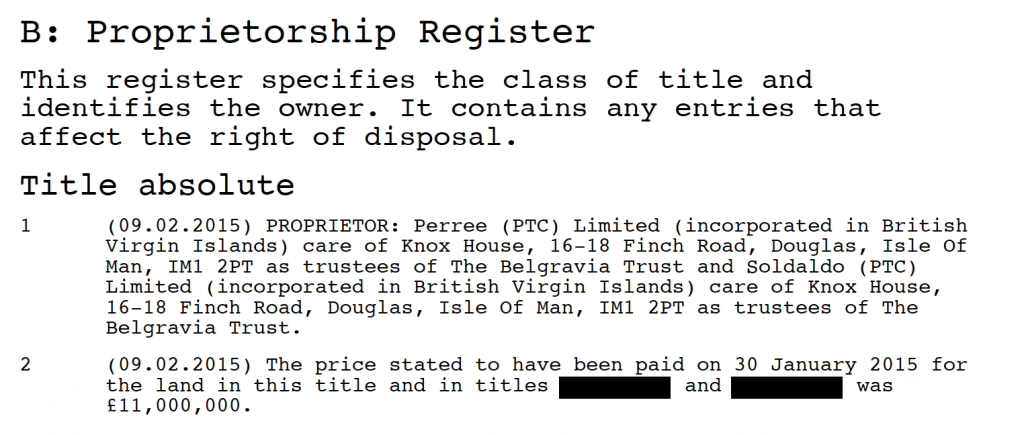

Last year, the Times and then The Daily Mirror reported that Douglas Barrowman and Michelle Mone own (and sometimes live in) a £20m house in Belgravia which is owned by two British Virgin Islands companies called Perree (PTC) Limited and Soldaldo (PTC) Limited.

Here’s the Land Registry entry for their house:

The UK was perhaps the first country in the world requiring foreign companies owning real estate to register their beneficial ownership.1 The deadline for registration of existing ownerships was 31 January 2023. Naturally Barrowman/Mone didn’t do this.

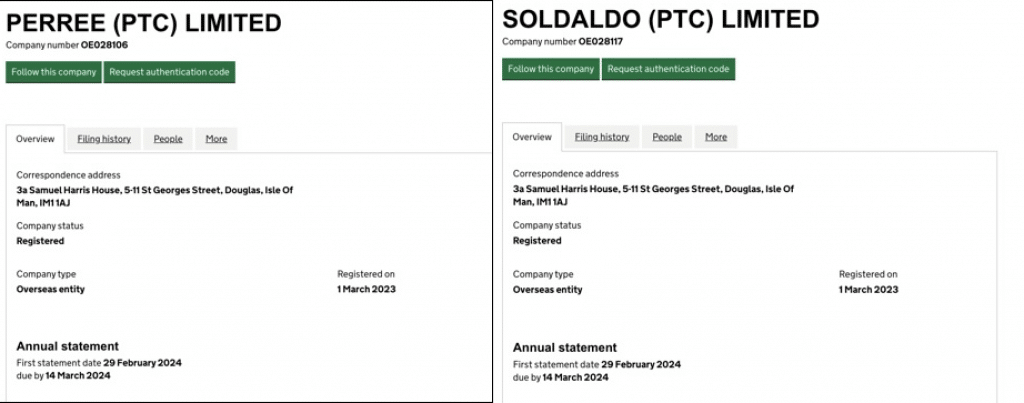

The rules have some “teeth” – a foreign company that fails to register can’t buy or sell the real estate. Hence, perhaps because Mone/Barrowman are now selling the house, they registered Perree (PTC) Limited with Companies House on 1 March 2023, and Soldaldo (PTC) Limited on the same date:

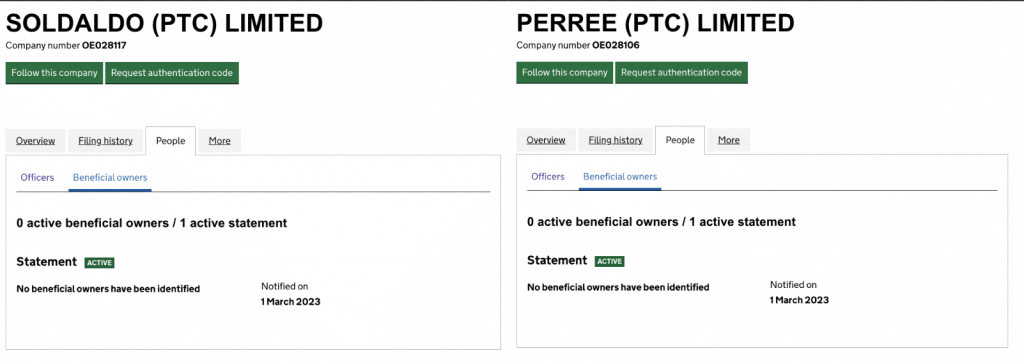

The main purpose of the rules is requiring foreign companies to identify their beneficial owner. Here are the entries for the two companies:

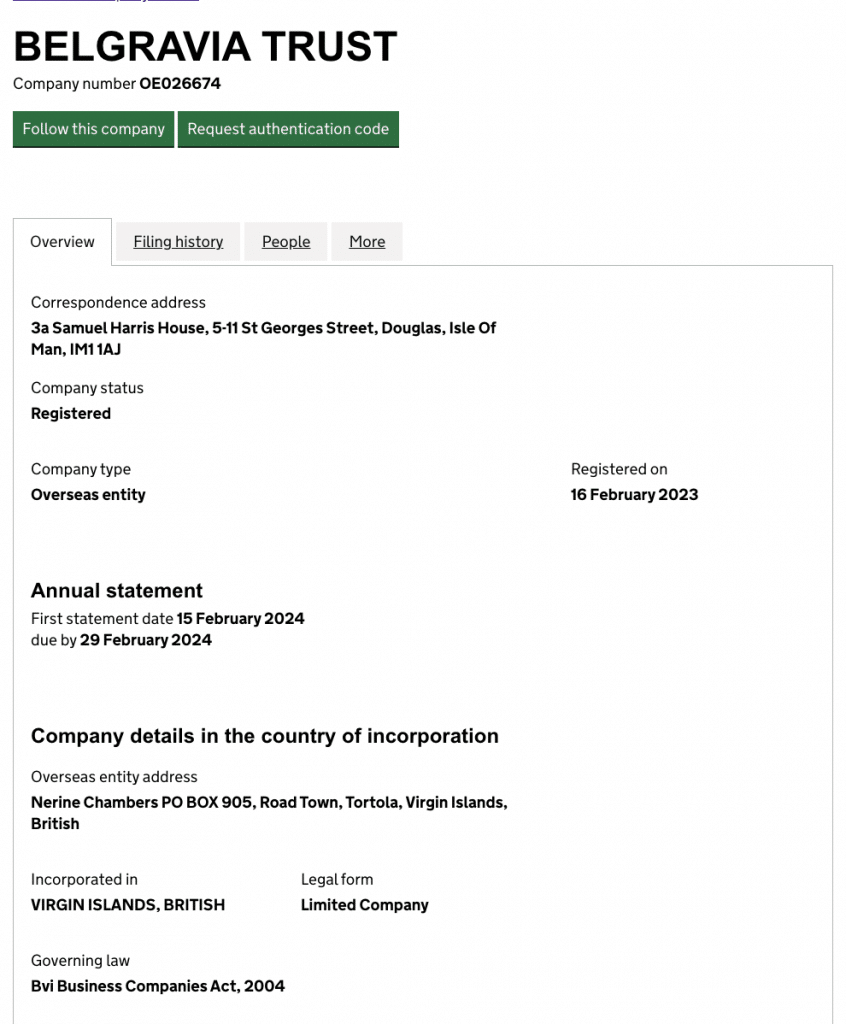

The Companies are said to hold the property as trustees of the Belgravia Trust. The trust is also on the register of overseas entities, bizarrely stated to be a “limited company” (which is almost certainly impossible):2

The Belgravia Trust lists as its beneficial owners its trustees, Soldado (PTC) Limited and Perree (PTC) Limited. Which isn’t right, because beneficial owners for this purpose have to be individuals (with an exception for companies subject to their own disclosure requirements, which BVI companies definitely are not).

Who is the actual beneficial owner?

Section 12 of the Economic Crime (Transparency and Enforcement) Act 2022 requires that a company take reasonable steps to identify its beneficial owners.

The definition of “beneficial owner” is in Schedule 2 of the Economic Crime (Transparency and Enforcement) Act 2022. It includes straightforward cases, e.g. anyone holding more than 25% of the shares in a company, but also this general rule:

We don’t know who ultimately controls the Belgravia Trust, Perree (PTC) Limited and Soldaldo (PTC) Limited, but here’s what we do know about the three entities:

- They own a house used (according to the Mirror) personally by Michelle Mone and Douglas Barrowman

- They each give as their service address the headquarters of Barrowman’s Knox Group in the Isle of Man.

- They each list as their “managing officers” Anthony Edward Page and Claire Voirrey Coole. Page was the managing director of the Knox Group; he subsequently had some kind of falling-out with Barrowman. Coole is a director of PPE Medpro and another Barrowman company. 3

So it seems likely, from the known facts, that Barrowman exercises “significant influence or control” over the trust and the companies. If so, then Barrowman should be listed as the beneficial owner.4

It is possible in principle that the directors tried and failed to identify the beneficial owner – it was a complete mystery they were unable to resolve, despite taking appropriate steps.5 That seems very unlikely given that the Knox Group are in the business of company formation. Page and Coole didn’t become directors by accident.

The consequences

Section 4 of the Act requires the beneficial ownership information to be included in the application for registration. Plainly that didn’t happen.

Under section 32, it’s an offence for anyone, without reasonable excuse, to deliver (or cause to be delivered) a false or deceptive filing under the Act – on conviction they can be liable for an unlimited fine. The offence is “aggravated” if a person knows it was false or deceptive – there is then also the possibility of up to two years’ imprisonment.

In this case, if Barrowman was the beneficial owner, the registration documents were false/deceptive in not listing him. Surely the directors knew they were false.

That suggests that Page and Coole may have committed the aggravated offence. If Barrowman was aware, he may also be liable.6

If this was a small widget company then we could be forgiving about a technical breach of the law. People make mistakes, and those unfamiliar with the law can easily misunderstand what it means. But the Knox Group is in the business of providing corporate and fiduciary services⚠️ – setting up and managing companies. Knowing how these rules work is literally their job.

Why do Barrowman and his companies ignore the law?

In the BBC interview with Barrowman and Mone, Laura Kuenssberg asked specifically why Barrowman wasn’t visible on PPE Medpro’s Companies House filings (our original report on PPE Medpro is here). Barrowman first suggested this was a complicated technical question. Then he admitted being the ultimate beneficial owner;7 finally he seemed to blame his staff. Most of this was cut from the TV edit, but the BBC made the full audio available here – the relevant section starts at 41:53.

Perhaps the real explanation comes a bit later – “I don’t want anyone in the press to know of any business activity or anything I get engaged in”.

He goes on to suggest that concealing the true ownership of companies is very standard:

“What happens in family offices is that the senior people in our family office tend to hold all the appointments for any businesses or companies I own, which is very common across family office structures around the world.”

Unfortunately for Mr Barrowman, there is no exemption from transparency laws for people wanting privacy. And Barrowman’s suggestion that most private offices operate this way is false. Sure, the ultimate owner is often not a director or direct shareholder of a company – but they are always listed as the beneficial owner – that’s what the law requires.

Two examples demonstrate how this works in practice:

Richard Branson has a private office. He’s not a director or shareholder of Virgin Holdings Limited. I’m sure the ownership arrangements are highly complex (and Mr Branson has never been shy about his desire to minimise tax). But, quite properly, Mr Branson is listed as the beneficial owner.

James Dyson has a family office. He’s no longer a director of Weybourne Group Limited, which holds his UK businesses. Again, I’m sure his ownership arrangements are highly complex – Mr Dyson is much wealthier than Mr Barrowman, with interests around the world. Yet Weybourne, quite properly, lists Mr Dyson as the beneficial owner:

The only reason Douglas Barrowman’s company filings are different from Messrs Dyson and Branson is that Mr Barrowman chooses to ignore the law. He has form for this.

What about the agent?

The Act doesn’t just trust companies to file correct beneficial ownership information. Regulations made under the Act require that an agent (regulated under money laundering rules) must verify beneficial ownership and submit details to Companies House within 14 days of registration, using this form.

In this case, that clearly went wrong.

You can see the agent details for Perree (PTC) Limited in the company’s filings – it was FCLS Group Limited. The same for Soldaldo (PTC) Limited and the Belgravia Trust. This isn’t a case where Mr Barrowman’s people misled the agent into thinking some accountant was the true beneficial owner. The registration lists no beneficial owner at all. And surely nobody misled FCLS into thinking a trust was a company – that’s a complete non-sequitur.

What was FCLS Group Limited thinking? Or have they created an automated process that doesn’t involve any thinking?

Next steps

I’ve written to the Knox Group and FCLS seeking comment, and will update this article with anything I receive.

The question is whether Mr Barrowman and his team will face any criminal sanctions for what appears to be their widespread practice of treating inconvenient laws as optional.

Thanks to K and P for an invaluable discussion, and to W for hugely helpful technical input after we published our initial report. And thanks to M for the tip.

Photo – obviously not of Barrowman/Mone’s actual house – by Amanda Slater, licensed under Attribution-ShareAlike (CC BY-SA 2.0)

Footnotes

This follows a recommendation of the Financial Action Tax Force. You can access the complete list of foreign companies owning UK real estate here – you have to register, and agree to a licence, but it’s free and straightforward. ↩︎

Trusts aren’t required to be registered. Either the Belgravia Trust has a truly bizarre nature/structure, or this is a mistake of some kind. ↩︎

Note that the company is only disclosing its managing officers because it decided it had no beneficial owners. This is the “fallback” under the rules. What should have happened was Barrowman disclosed as beneficial owner and no managing officers disclosed. ↩︎

Shares in the two companies are likely “orphaned” – held through private purpose trusts (with an “enforcer“) or foundations so that they have no actual individual as their beneficial owner. However Barrowman would almost certainly only agree to such a structure if he could control it as a practical matter, albeit perhaps not as a strict legal matter. That kind of “nod and wink” control can sometimes fool tax rules, but it doesn’t fool the beneficial ownership rules here. In such a case, Barrowman would have “significant influence” over the companies. All the more so when, as here, his own employees are the directors. ↩︎

e.g. issuing “information notices” to their shareholder. ↩︎

Either on the basis he “caused” the false filing to be delivered, given the apparent group-wide policy of hiding his ownership, or alternatively on the basis he is a shadow director. ↩︎

This may be a rare case where someone admits to a criminal offence in a TV interview. ↩︎

Douglas Barrowman and Michelle Mone may have avoided tax on their £65m PPE profits

![32 [F1 General false statement offence] [F1 False statements: basic offence]

[F' (1) It is an offence for a person, without reasonable excuse, to—

(a) deliver or cause to be delivered to the registrar for the purposes of this Part any document that is misleading,

false or deceptive in a material particular, or

(b) make to the registrar, for the purposes of this Part, any statement that is misleading, false or deceptive in a

material particular.](https://taxpolicy.org.uk/wp-content/uploads/2023/12/Screenshot-2023-12-28-at-11.41.07-640x118.png)

Douglas Barrowman: 25 more companies with unlawfully hidden ownership

Michelle Mone failed to declare her interest in an offshore trust

Zahawi, Barrowman and Mone: why libel law rewards liars, and how we could change it.

Who secretly owns Britain? The hidden offshore owners of £460bn of UK property

Leave a Reply to Tom Millar Cancel reply