Richard Tice isn’t denying that Quidnet REIT, his property company, failed to pay around £120,000 of tax when it paid dividends to Mr Tice and his offshore trust. He says it doesn’t matter, because he paid tax in full. That’s wrong: Quidnet’s failure to withhold REIT tax was unlawful, and the £120,000 remains due.

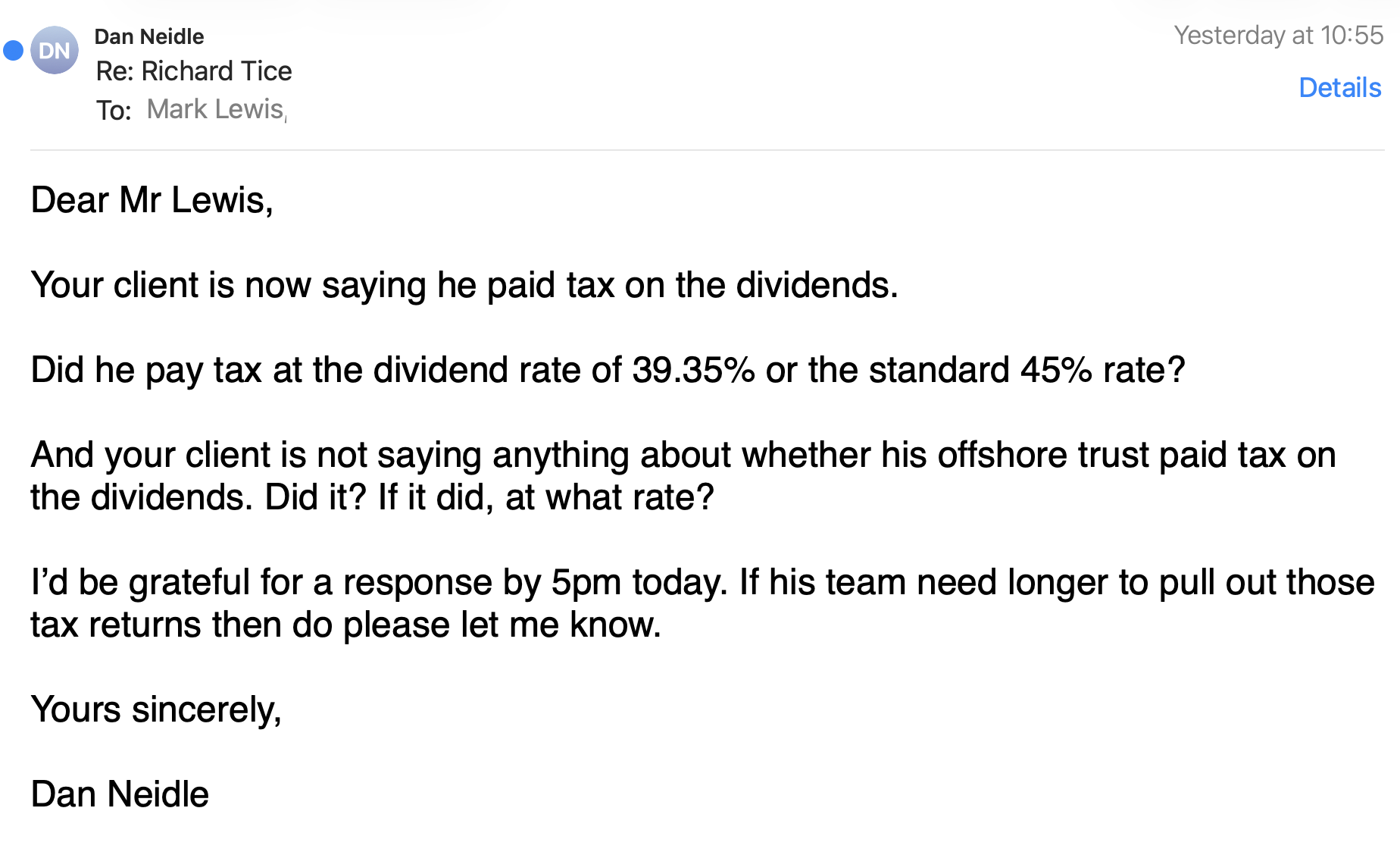

But perhaps more importantly, Mr Tice is failing to answer two critical questions. Did his offshore trust pay any tax on the dividends? And did he and his trust pay tax at the correct rate?

Our original report on the £120,000 tax issue is here. The point was first identified by Gabriel Pogrund of The Sunday Times; we assisted with the story. The Sunday Times’ report is here.

What we know went wrong with Quidnet’s tax

From 2018 to 2021, Quidnet was a REIT – a real estate investment trust.

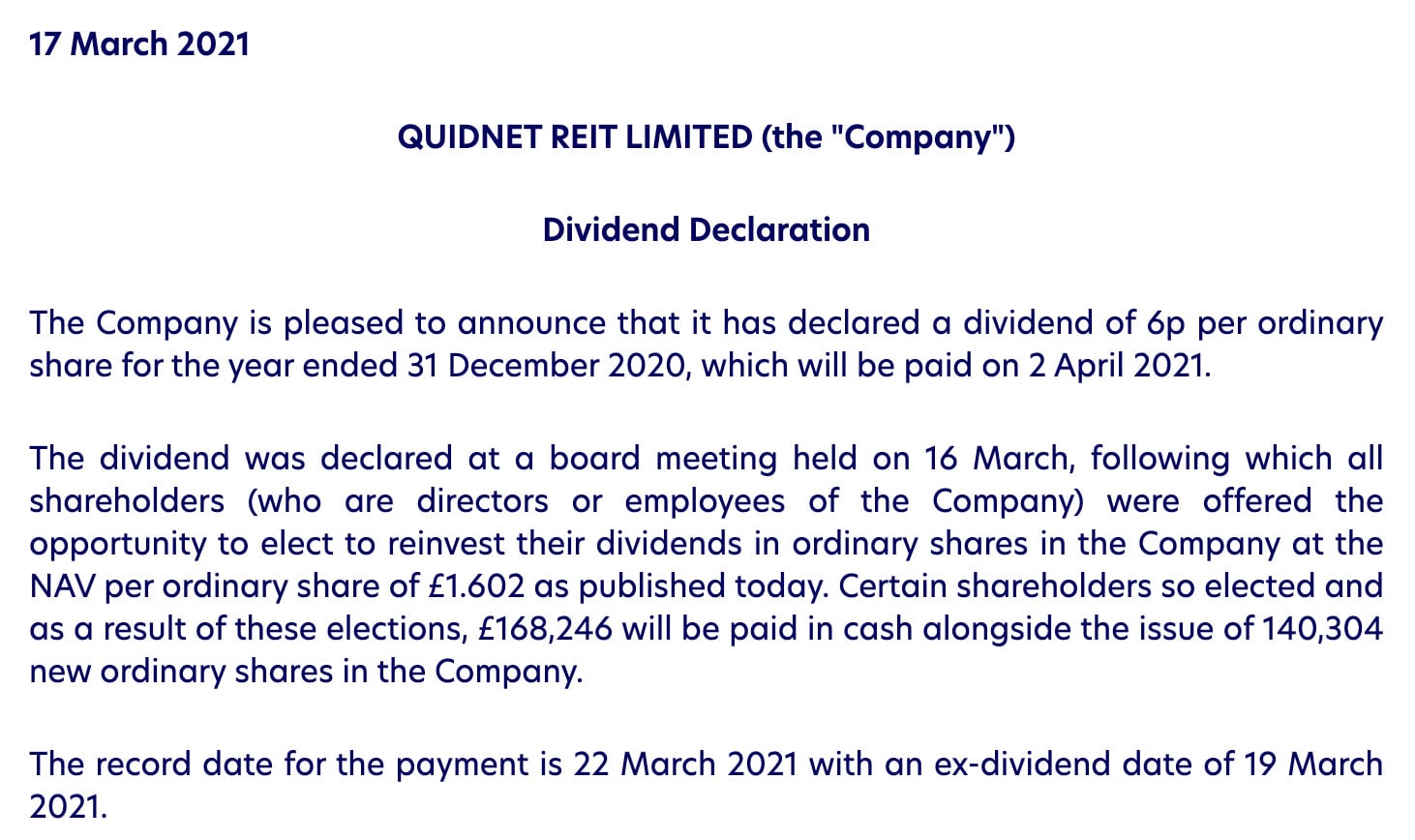

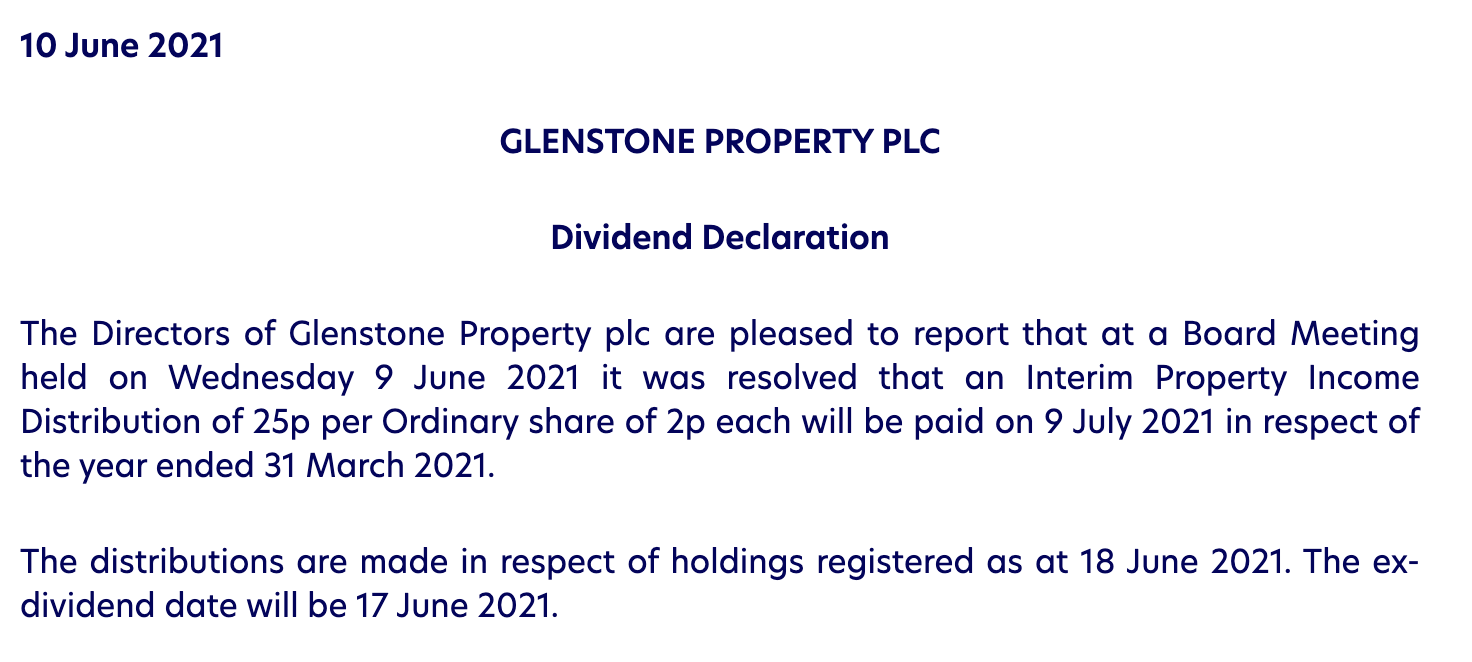

Here’s a dividend declaration from Quidnet, alongside a declaration from another REIT, Glenstone.

There’s a telling difference. Glenstone says it’s declaring a “Property Income Distribution”. Quidnet says that it’s declaring a “dividend”.

REITs are exempt from tax on the income and gains from their UK property business. The quid pro quo is that, when they pay their profits to shareholders, it’s not a normal dividend – it’s a “property income distribution”.

A normal dividend – as would be paid by e.g. Tesco plc – has no withholding tax. A UK individual or trust shareholder pays tax at the top rate of 39.35% when they file their tax return in January of the following tax year.

A property income distribution – as is usually1 paid by REITs – has 20% withholding tax immediately. A UK individual or trust shareholder pays tax at the top rate of 45%, in the January of the following tax year with a credit for the tax withheld – so really a 25% top-up.

Glenstone fully understands this. It looks like Quidnet and its advisers didn’t understand this, and treated all their dividends as normal dividends. So Quidnet paid about £270k to Mr Tice and £330k to his offshore trust, without any withholding tax.

What we don’t know about Mr Tice and his offshore trust

This was a surprising error for a REIT and its advisers to make – it’s a very basic and fundamental REIT point. We don’t know how the error was made, but there are broadly two ways it could have played out:

1. The REIT got it wrong. Everyone else got it right.

In this scenario, the REIT got it wrong, and thought it was paying normal dividends – so didn’t withhold. But the shareholders got it right, and realised it was a property income distribution.

So Mr Tice and his trust both paid tax at 45% – the correct treatment.

Mr Tice can say that this was a mere technical failure and HMRC wasn’t out of pocket. It is, however, more than that: Mr Tice obtained an unlawful tax benefit – the 20% was paid up to 21 months later than it should have been. And Mr Tice’s payment didn’t fix the company’s failure to withhold tax – the tax remains due.

2. Everyone got it wrong

In this scenario, everyone2 acted consistently, and thought Quidnet was paying a normal dividend.

The REIT didn’t withhold. Mr Tice paid tax at 39.35%. The offshore trust either paid tax at 39.35%, or didn’t pay tax at all.3

In this scenario, HMRC is most definitely out of pocket, and Mr Tice and/or the trust owe tax, plus interest and probably penalties.

Which scenario are we in?

Richard Tice isn’t saying.

In his own statements and Reform UK’s statements they’re clear that Mr Tice paid tax, but they’re not saying anything about the rate he paid, and not mentioning the trust at all.

We asked Mr Tice’s lawyer these questions yesterday, but didn’t receive a response:

These are very easy questions to answer: one look at the tax returns will show whether the dividends were correctly reported as “other income” or, incorrectly, as “dividend income”.

We will update this article if Mr Tice responds.

Many thanks to Gabriel Pogrund of the Sunday Times, who discovered this story, and to K and M for the REIT and accounting analysis that underpins this and our original report.

Photo of Richard Tice by Laurie Noble, licensed under CC BY 3.0

{kind=link}

Footnotes

Not always. REITs are required to invest mainly in property and to pay out 90% of the profits from their property rental business to shareholders as “property income distributions”. If they have other income, this can be a normal dividend. Our review of Quidnet’s accounts suggests that all or almost all of its dividends were property income distributions; the accounts use the term explicitly. ↩︎

We are assuming that Mr Tice’s advisers also act for the offshore trust, and so that they would have filed consistent returns. If that’s wrong then there are of course more potential outcomes. ↩︎

Why? Because offshore trust structures are usually intended to avoid normal UK taxes. That can be a legitimate result in some cases, and not in others – but tax will always be due on a property income distribution. That’s because it’s treated like a payment of rental income and always taxable, no matter who in the world receives it (unless they are exempt, e.g. a pension fund or under a double taxation treaty which doesn’t reserve to the UK the right to tax UK land – the offshore trust would be in neither category). There is a nice technical summary of how trusts are normally taxed on dividends in a comment on our original report. ↩︎

Richard Tice’s property company failed to pay £120,000 in tax

Companies House flaw exposed five million directors and enabled company hijacking

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

The bizarre UK group selling US tax fraud to hundreds of Britons – and prosecuting its critics

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Leave a Reply to Dr Robert Dyer Cancel reply