MP Estate Planning1 is an unregulated advisory firm using an extensive social media campaign to sell expensive “asset protection trusts” to elderly homeowners, often of relatively modest means.

The pitch is simple: put your home into a trust and you can avoid inheritance tax, care home fees, divorce claims and creditors. Our investigation, drawing on the expertise of over a dozen specialist lawyers and tax advisers, found that the claims are false – and may leave families facing large tax bills and, ultimately, cause a complex and expensive probate process.

We were disappointed but not surprised to find trusts being missold – that’s been going on for years. What we found was much worse – a firm that operates on the edge of legality, and may step over the line. A series of misrepresentations as to what it is and what it does, and advice to clients that goes beyond “merely wrong” into shocking negligence. And when we asked MP Estate Planning for comment, they failed to provide any response to our technical criticisms, and provided answers to other points that we consider to have been intentionally misleading.

The length of this report reflects the seriousness of what our investigation found.

The problems with MP Estate Planning

It all starts with a lack of expertise. The firm’s founder, Mike Pugh, says he is an “estate planning lawyer”. He isn’t. The firm’s website says it employs “experienced lawyers”. That is also untrue. We believe nobody at MP Estate Planning has any legal, tax or accounting qualifications.

The lack of expertise doesn’t stop the firm marketing its business very aggressively. It has over 400 videos on social media pushing an alarmist message: “if you own anything, it can be taken from you”. Pugh says their mission is “quite literally to save the middle class from being completely wiped out in the UK”. The solution is simple: “every home in a trust” – and they’re pushing this proposition to elderly people with assets of as little as £150,000:

The firm’s videos and website make a variety of striking claims:

- You put your house and other assets in trust. They’re then outside your estate for inheritance tax purposes.

- There are no adverse tax consequences of this.

- The trust will reduce probate costs.

- Your house won’t be assessed in determining whether you have to contribute towards care home fees (should they be needed).

- You can financially support your children after you die, but if they divorce then their spouse will have no claim on their assets.

- Assets in the trust are safe from your creditors, and can’t be touched if you go bankrupt.

All these claims are false. The Society of Will Writers has published guidance telling its members not to make these kinds of claims. The Association of Lifetime Lawyers has published a report demonstrating the damage caused by unregulated providers making claims like this.

Our investigation uncovered multiple serious problems with MP Estate Planning’s claims and business practices.

- Lifetime trusts are poor tax planning for most people. They often result in more inheritance tax because the spouse exemption and residence nil rate bands aren’t available to trusts.

- The MP Estate Planning structures we reviewed have no material tax benefit and likely trigger a series of unnecessary tax bills.

- One experienced adviser told us that the tax claims made by MP Estate Planning were so egregiously bad that they looked like fraud (although most of our team believe the firm is just unqualified and reckless).2

- They publish hundreds of videos which include multiple legal errors, often referring to US law concepts that have no equivalent in the UK. Their website is full of false claims and appears to be largely AI generated.

- The firm claims the backing of an eminent KC, James Kessler, who told us he’s never given it, and in fact told MP Estate Planning to stop using his name.

- MP Estate Planning claim their “head of legal”, and Mike Pugh’s mentor, is Dr Paul Hutchinson, who “trained with Kessler for 20 years”. In fact MP Estate Planning have never had a “head of legal”, or indeed any legally qualified staff at all. Dr Hutchinson told us he has never met Mr Kessler, and has never had any dealings with MP Estate Planning.

- It appears that the firm is drafting property trusts for its clients, despite not employing qualified lawyers. If so, that’s potentially a criminal offence. And we’ve seen trust deeds that include very basic but highly significant errors.

- Mike Pugh’s previous firm, Maplebrook Wills Ltd, went bust owing £1.7m to HMRC – an extraordinarily large amount for a small will-writing business. Mike Pugh’s actions are currently being investigated by the company’s liquidator.

We therefore believe MP Estate Planning is misselling trusts to people who probably do not need them and who are unprepared for the legal and tax complexities these structures create. Bad inheritance tax planning usually remains hidden until the taxpayer dies, decades after the planning was put in place. It is the taxpayer’s grieving children who are then left to pick up the pieces.

A prominent Scottish law firm failed in 2021 after selling unsuitable “family protection trusts”. Its pitch was similar to MP Estate Planning – but at least it was regulated, and so its clients had the prospect of recovering their loss. MP Estate Planning is completely unregulated, and anyone let down by its trusts will have no recourse at all.

We will be referring the firm to the Solicitors Regulation Authority for carrying on reserved legal activities without authorisation. We hope that HMRC investigates the firm for failing to disclose tax avoidance schemes.

In this report:

- The problems with MP Estate Planning

- The red flags

- The pitch and the reality

- What is a trust?

- The pitch

- 1. "Presto magic" to avoid the 6% anniversary charge

- 2. Avoiding GROB with a school uniform

- 3. Using a 1999 licence loophole that doesn't exist

- 4. Gifts that ignore an anti-avoidance rule

- High risk landlord tax planning

- Saving probate costs

- Divorce protection

- Bankruptcy protection

- Care home costs

- The trust defaults the mortgage

- Incompetent advice

- The scale of the problem

- The response from MP Estate Planning and Mike Pugh

The red flags

Before we present the products sold by MP Estate Planning, and the reasons why they don’t work, there are numerous red flags that in our opinion indicate this is not a business to be trusted.

Deceptive claims about their expertise

Mike Pugh says he’s a “tax lawyer” and an “estate planning lawyer”:

He isn’t🔒. Mike Pugh worked as a Will writer after emigrating from Canada to the UK. He set up MP Estate Planning in 2023, but has no UK legal, tax or accounting qualifications. It’s an offence to hold yourself out as a solicitor or barrister, but the term “lawyer” is not legally protected – we nevertheless regard it as highly misleading for someone with no legal qualifications to claim to be a lawyer.

The MP Estate Planning website said they are a firm of “experienced lawyers” – this is untrue. We can’t identify anyone at MP Estate Planning who has any legal, tax or accounting qualifications. Neither any of the staff nor the firm itself is regulated. When we asked MP Estate Planning about this we didn’t get a response; they just changed the website.

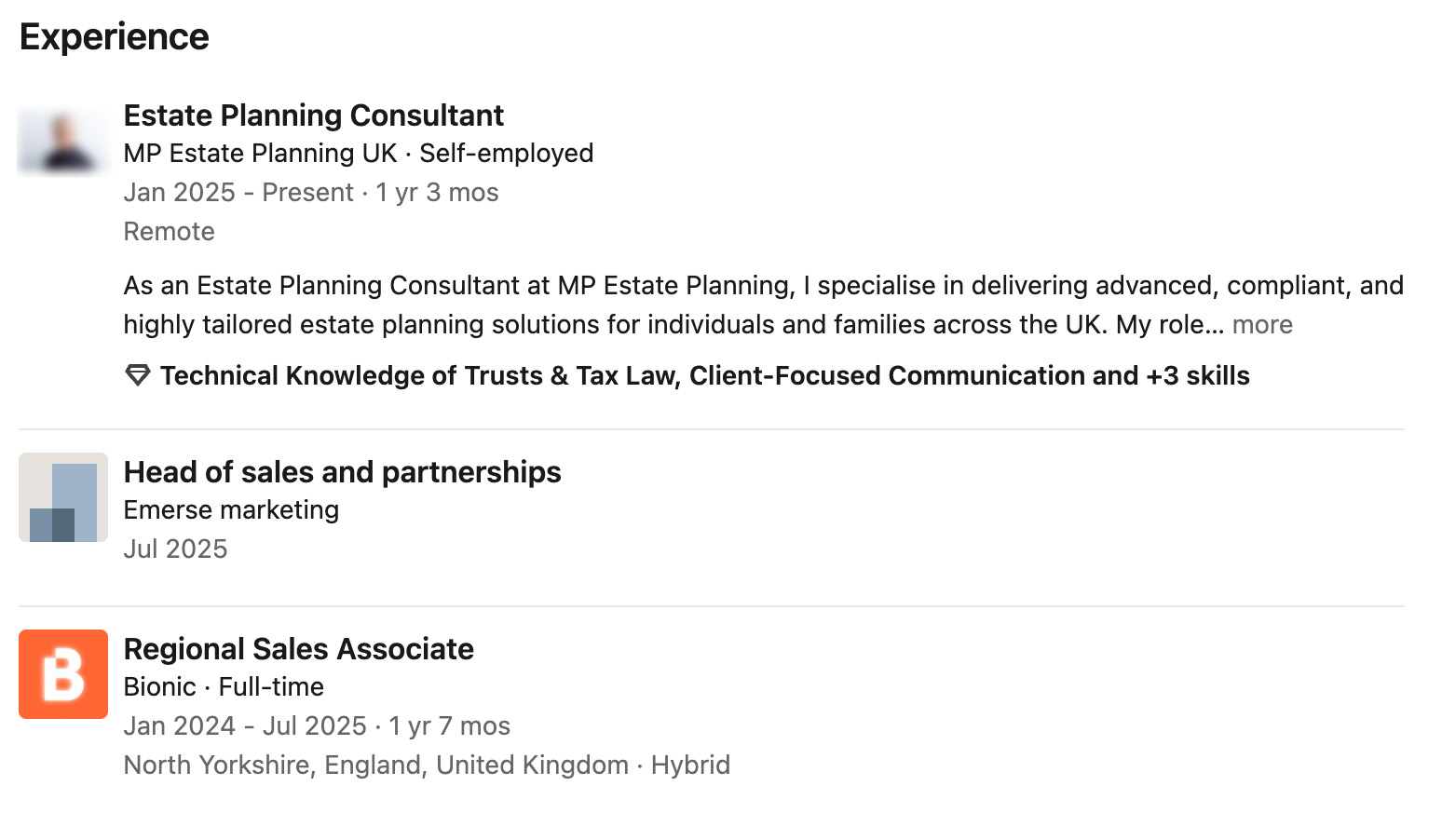

Here’s the, fairly typical, CV of one of their representatives: he worked in sales until nine months ago, and now claims to be an “estate planning consultant” who can “specialise in delivering advanced, compliant and highly tailored estate planning solutions”:

In reality he’s still working in sales, just with a different job title.

We can see how MP Estate Planning hires and trains its salespeople from a recent recruitment advertisement:

It takes three to five years to train to be a chartered accountant and two years to train to be a chartered tax adviser. MP Estate Planning tell their salespeople they can earn £20,000 per month after three weeks’ training. That would be less concerning if all they did was sales; but they tell potential clients they’re “consultants”, and we’ve seen multiple cases where the salespeople claim to be qualified to give advice.

Nobody else involved appears to have any relevant qualifications. Dan Irwin, MP Estate Planning’s “head of property” was previously a director of Safe Hands Plans Ltd, a pre-paid funeral plan business which collapsed in 2022, with 46,000 people losing most of their money. Two individuals who ran the business are currently being prosecuted for fraud. There is no suggestion Mr Irwin was involved in the fraud, and we don’t know if the fraud was underway when Mr Irwin ceased to be a director in April 2018.3

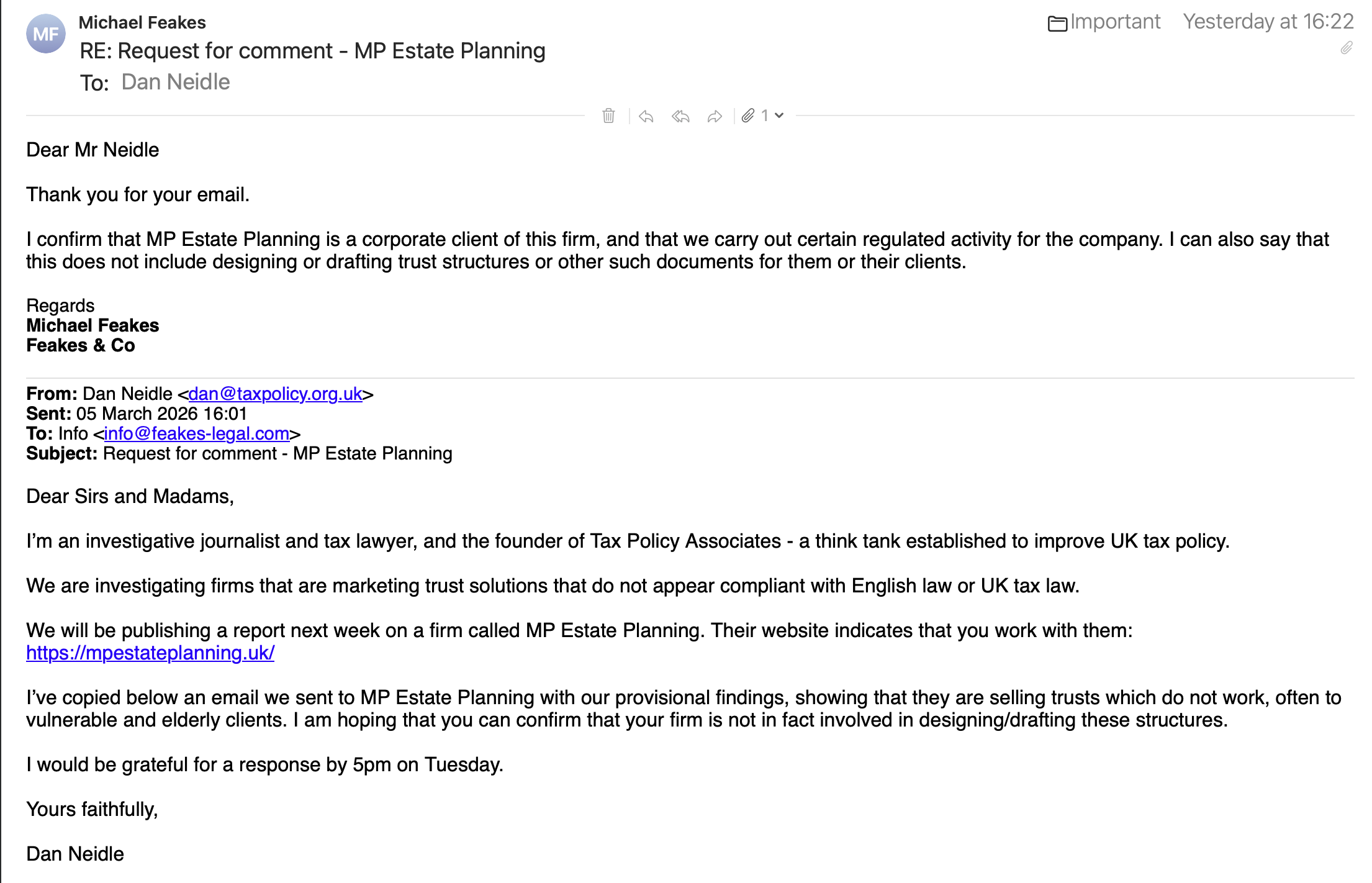

The website says they work with a solicitors firm called Feakes & Co – but the firm told us that, whilst they provide some “corporate advice” to MP Estate Planning, their role “does not include designing or drafting trust structures or other such documents for them or their clients”.

{kind=link}

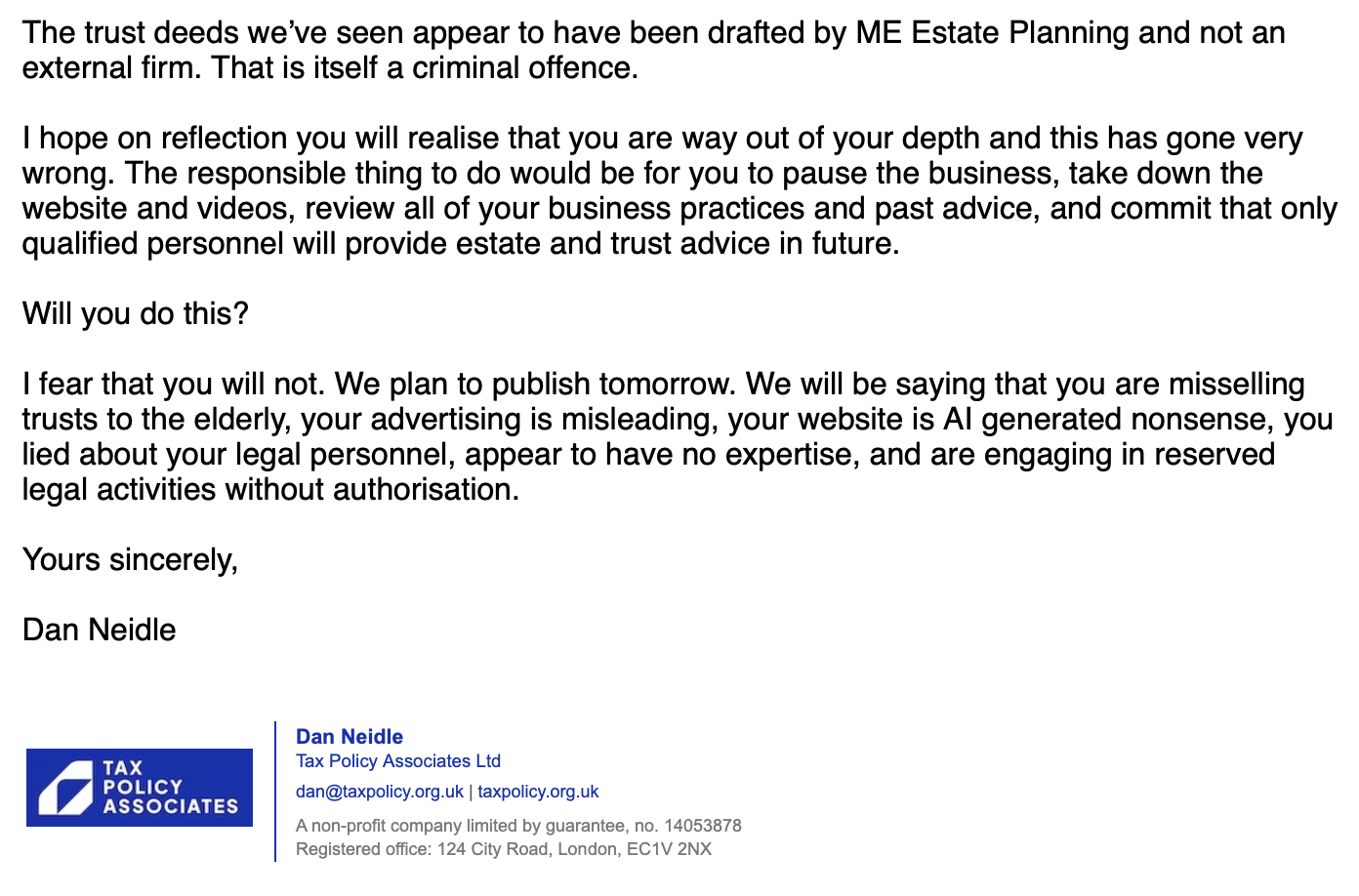

MP Estate Planning told us that “Where a client’s circumstances require specialist or regulated advice, we refer or signpost to appropriately qualified external professionals”. However, there’s no sign that the trust deeds we reviewed were drafted by an external firm – the only firm mentioned on them is Feakes & Co, apparently because they undertake trust registrations.

Here’s another example of how MP Estate Planning recruits sales personnel:

Our view is that a highly incentivised sales team operating with no tax/legal qualified staff is extremely dangerous.

Deceptive claims about their legal team

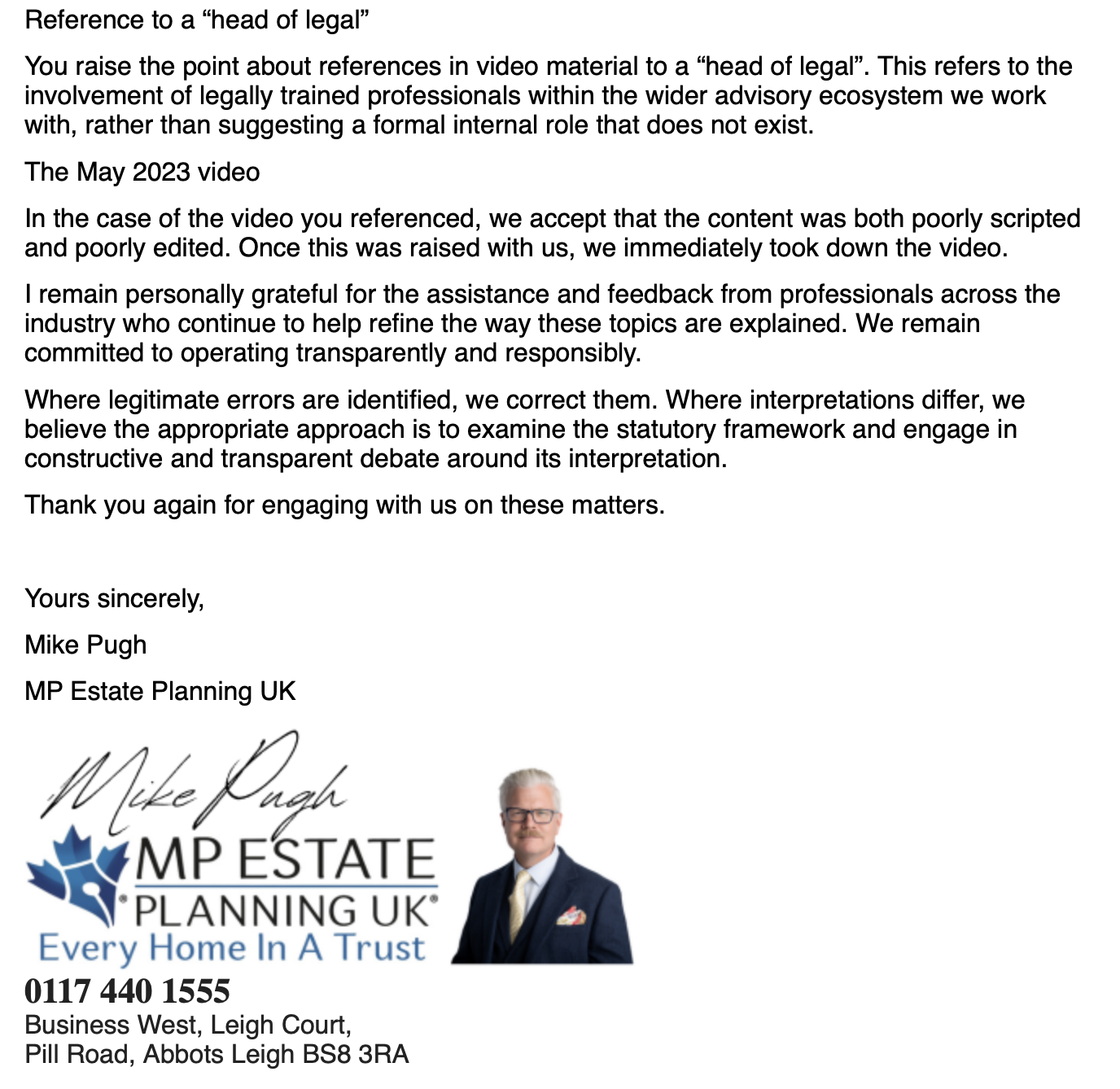

Mike Pugh describes his “head of legal” in numerous videos. There isn’t one. MP Estate Planning has never had a lawyer on its team:

We asked Pugh about this. He responded:

“You raise the point about references in video material to a “head of legal”. This refers to the involvement of legally trained professionals within the wider advisory ecosystem we work with, rather than suggesting a formal internal role that does not exist.”

That is a very unconvincing explanation of what we would characterise as a lie.

Mike Pugh often claims an association with James Kessler KC, often rated as one of the country’s leading private client advisers, and Dr Paul Hutchinson, a respected Will writer (with a PhD in Law), who appears to be the man he’s saying is his (non-existent) “head of legal”:

First video: “We use the Kessler 15th edition, James Kessler KC. I’ve actually had emails with him allowing me to use the precedents. He’s a lovely man. He’s the number one guy for taxes and trusts worldwide, period. I’ll just throw a shout out to my mentor, Dr. Paul Hutchinson, who I’ve worked closely with for 10 years. Paul trained under Kessler for 20 years. So we’re pretty comfortable with our technical capabilities.”

Second video: “At MP Estate Planning UK, our head of legal is a doctor of law specialising in taxes and trusts.”

Mr Kessler is the lead author of a well known practitioners’ textbook on Wills and trusts, which includes trust and Will precedents. He has never met Dr Hutchinson, much less trained him for 20 years. The claim that MP Estate Planning had some kind of special permission to use the precedents is false – and that plus other uses of his name🔒 sufficiently alarmed Mr Kessler that he includes a warning on his website:

MP Estate Planning (UK)

This company have been marketing themselves as Kessler Will UK and as providing “Kessler Wills”. This has been done without James’ permission.

James has no association with this company. He does not endorse this company or any of their so-called “Kessler Wills”. He does not vouch for any product offered by this company.

On 10 November 2025 the company has, through its directors, entered into formal undertakings including not to use or refer to the name Kessler and/or to use or refer to “Kessler Wills”.

If anyone is aware of them using the name Kessler or the phrase “Kessler Will”, or holding themselves out as being associated or endorsed by James, please let us know at the email address on this website

In all cases, James strongly recommends you take advice only from solicitors or accountants who are qualified and regulated.

Dr Hutchinson told us he used to provide in-house training for Pugh’s previous firm Maplebrook Wills. He lent the firm some money, and became a shareholder to try to recover it – but then Maplebrook Wills went bust and he was never repaid. He says he’s had nothing to do with Mr Pugh since:

I wish to have no association with Mr Pugh or his company and do not consider myself his mentor… for the record I have never met Mr Kessler let alone “trained under him”. I have his texts as reference material, but that is it.”

We can’t find any evidence that MP Estate Planning has a “head of legal”, but it certainly isn’t Dr Hutchinson.

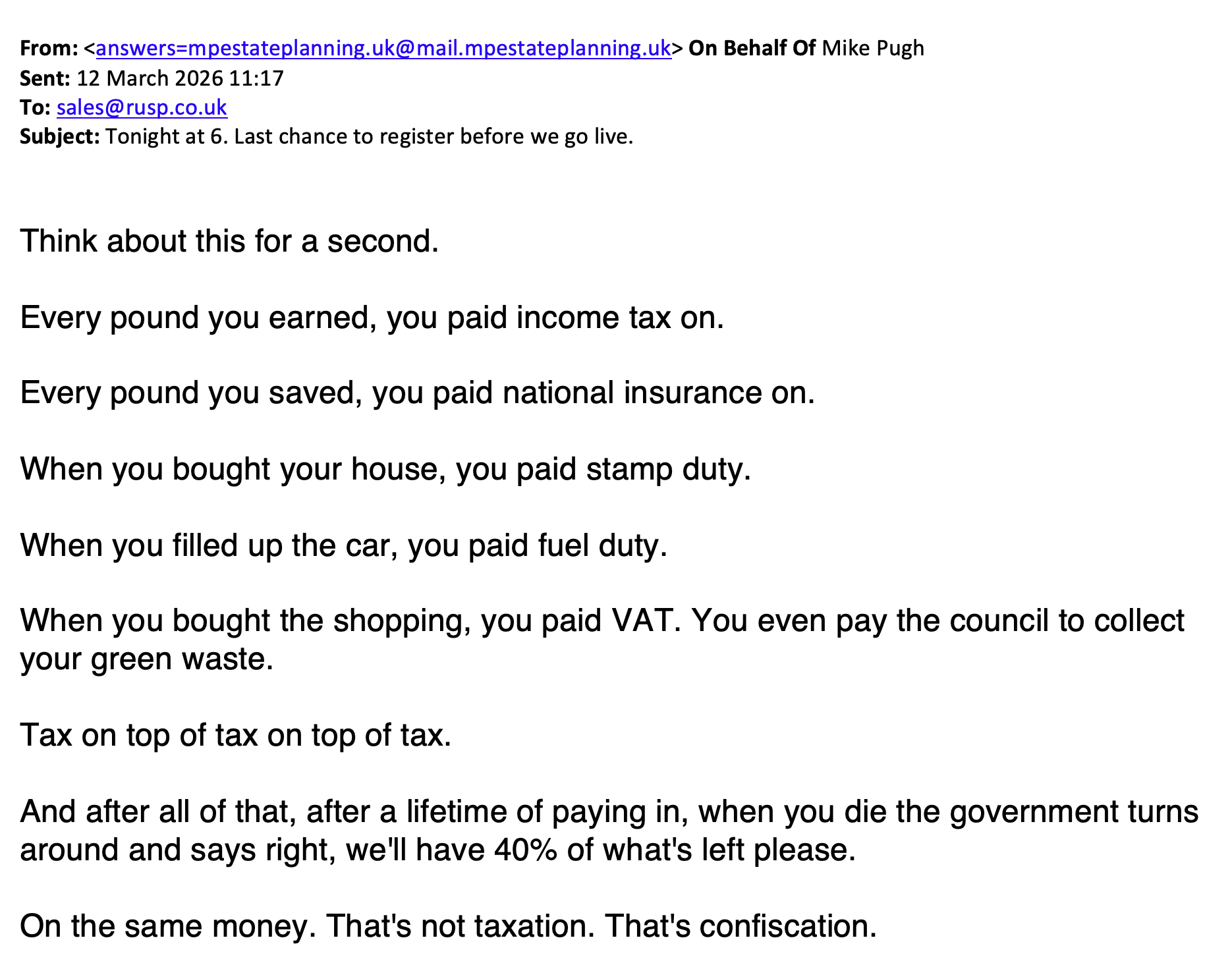

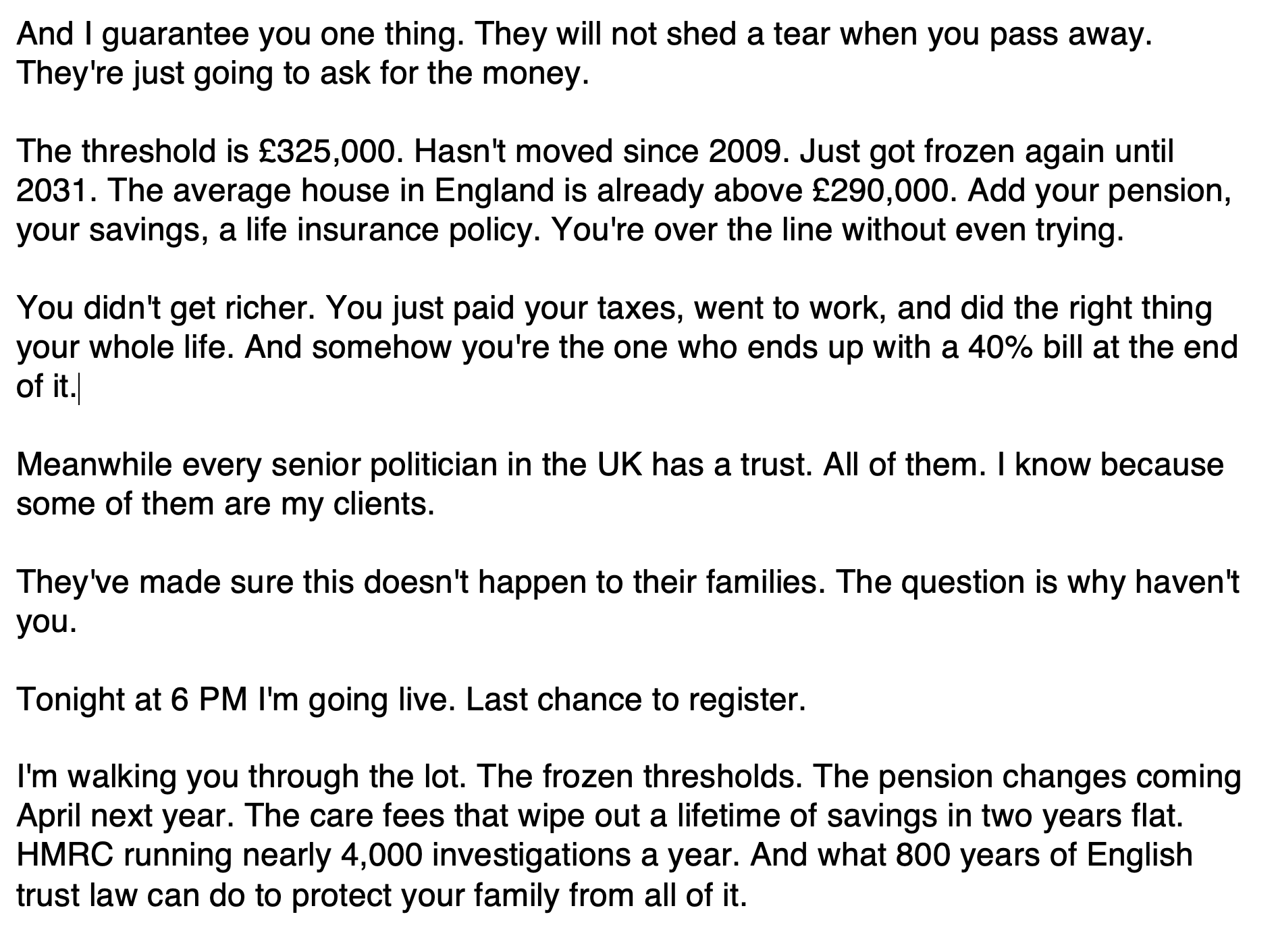

MP Estate Planning continued pushing out marketing containing falsehoods even when they knew this report was about to be released. This was sent to their mailing list the day before we published:

Every senior politician does not have a trust. Trusts are poor tax planning for most people. So it is therefore unsurprising that the List of Ministers’ Interests and the Register of Members’ Interests show only a small number of politicians declaring family trusts. We cannot know for sure, but we are very sceptical that MP Estate Planning has any senior politician as a client.

These claims – particularly the “head of legal” and “trained under Kessler for 20 years” were more than slips of the tongue, or the typical exaggeration of a salesman. They were concrete claims, made repeatedly. Mr Pugh surely knew the claims were was false. It is not far-fetched to suggest that a criminal offence may have been committed here.4

A deceptive website

The MP Estate Planning website has several elements we regard as deceptive.

First, the claimed associations and awards are untrue and misleading.

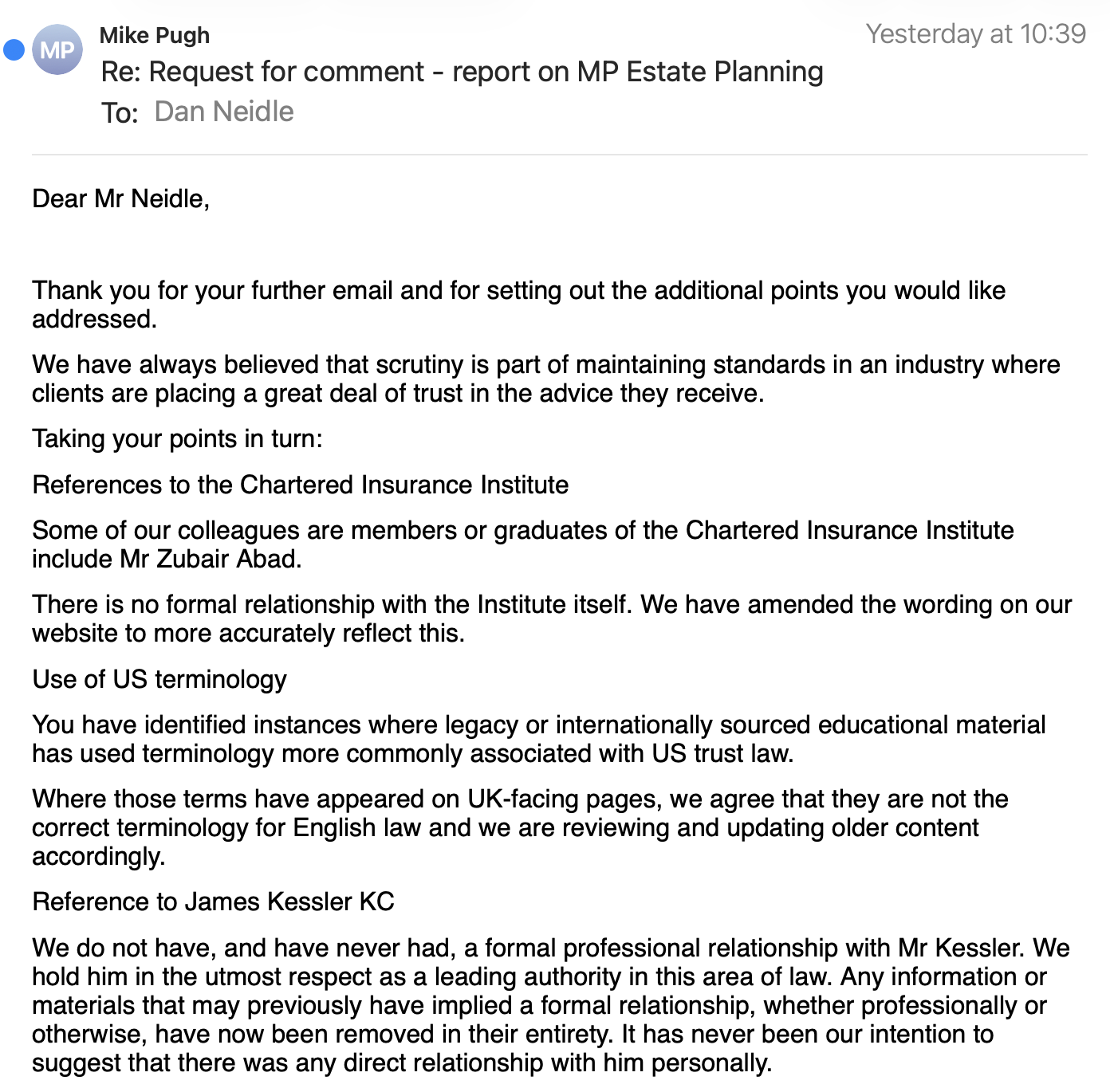

We spoke to the Chartered Insurance Institute. They’ve never heard of Mike Pugh or MP Estate Planning, and neither are members of (or have any association) with the Chartered Insurance Institute.

Pugh told us:

Some of our colleagues are members or graduates of the Chartered Insurance Institute include Mr Zubair Abad.

There is no formal relationship with the Institute itself. We have amended the wording on our website to more accurately reflect this.

Zubair Abad does not appear to be a member of the CII. It is possible he has CII qualifications. The wording on the website now says MP Estate Planning is “Aligned with or members of” the CII and other organisations. That still seems to us to be misleading.

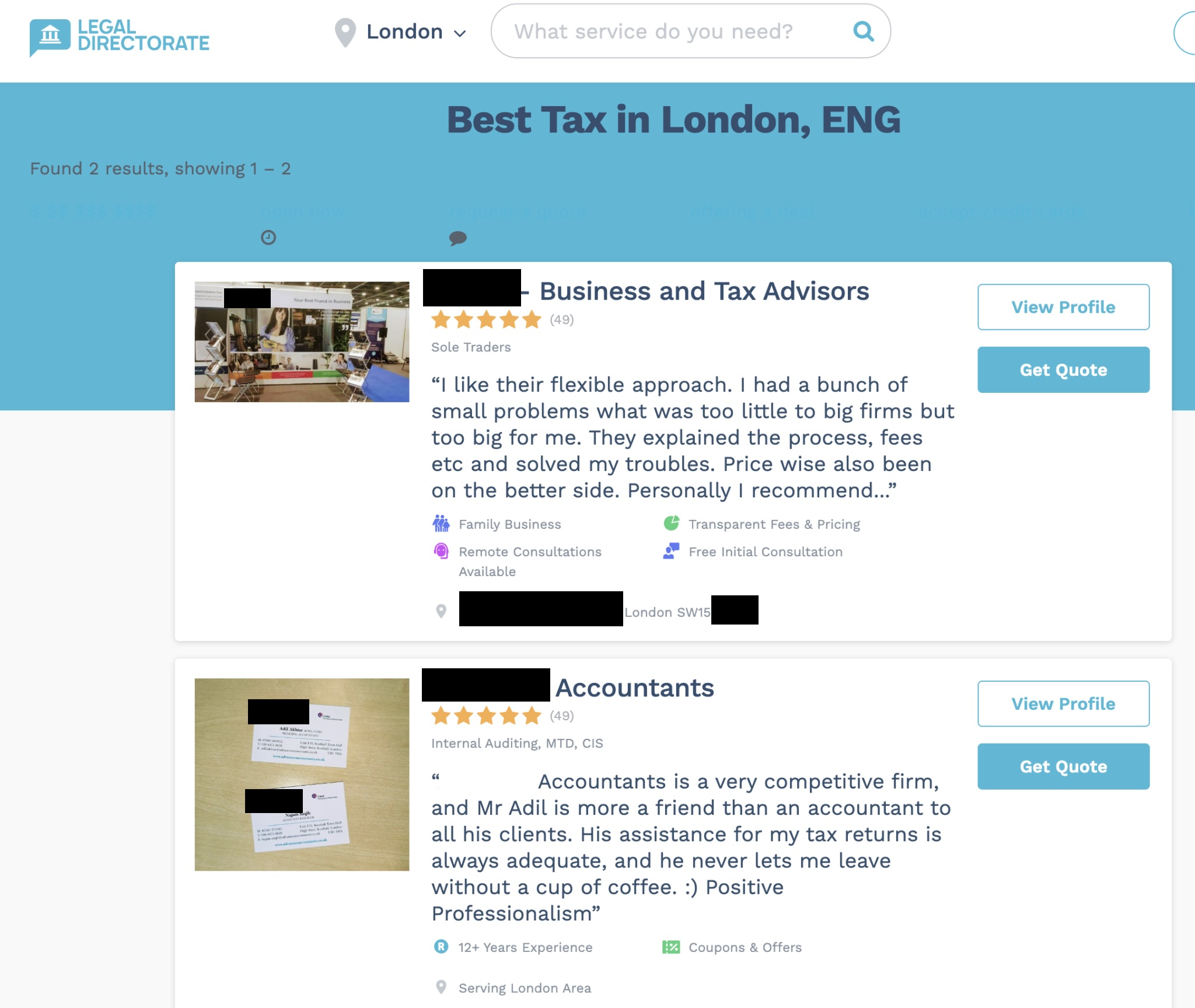

Second, the claimed award from “Legal Directorate” was phony. Legal Directorate is a “pay for play” directory which uses AI to generate fake reviews and fake awards, with listings of “best firms” that (with respect to the firms listed) are not credible:

At some point someone paid for an entry/award for Mike Pugh’s old firm, Maplebrook Wills. When he set up MP Estate Planning Ltd, it “inherited” the fake award, but Legal Directorate never changed the url – it’s still “https://legaldirectorate.co.uk/company/maplebrook-wills-441174401555-weston-super-mare/“, with reviews that are likely fake/AI generated.5

Since we asked about this, the “Legal Directorate” badge disappeared from the MP Estate Planning website.

Poor understanding of English law and UK tax

The MP Estate Planning videos and websites show a very limited understanding of UK tax and the English6 law of trusts. Here’s Mike Pugh last month:

“Never transfer your assets into your kids’ names, especially real estate. Here’s why.

Let’s say you bought a home many years ago for £300,000, and now it’s worth £900,000.

If you transfer or dispose of the property, you could trigger a capital gains charge, and your children might be responsible for paying a charge on the £600,000 of gain.

There are workarounds. For example, if your children move in and live with you, then you may be able to transfer the property to them without triggering the capital gains tax, as long as you continue to qualify for the main residence relief or private residence relief.

An easier solution than living together is to set up a trust and put your house into the trust and name your adult children as trustees and beneficiaries.

If you want to protect your home and see it safely get to your kids, click on the link in the description to watch my free master class on how to put assets into trust in the UK.”

This is nonsense from start to finish. If it’s your home, then the main residence exemption usually applies – so there’s no capital gains tax if you give the property to your kids. If it wasn’t your main residence then there would be CGT, but on you and not your kids. Having the children live with you wouldn’t change the result in any way.

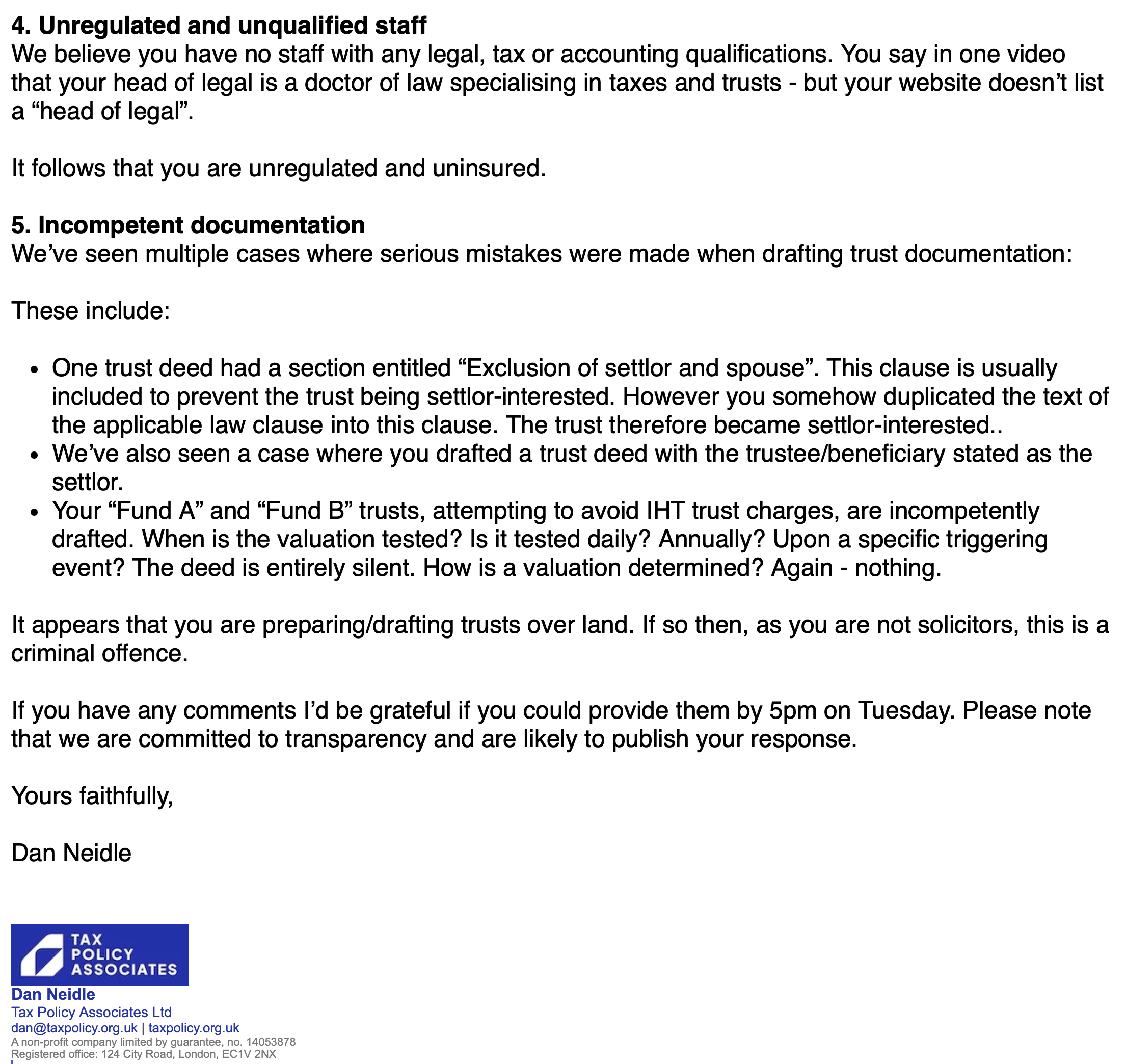

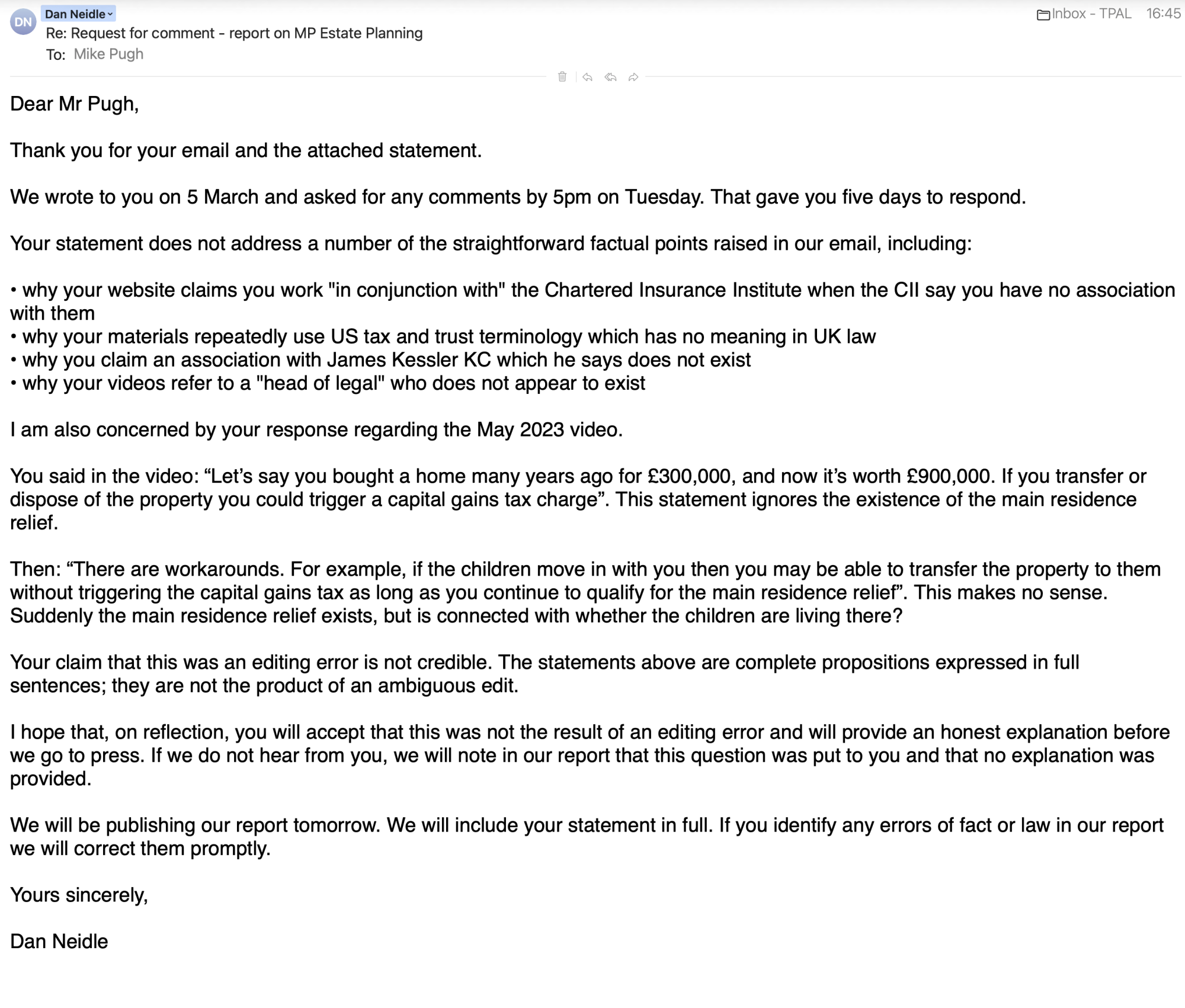

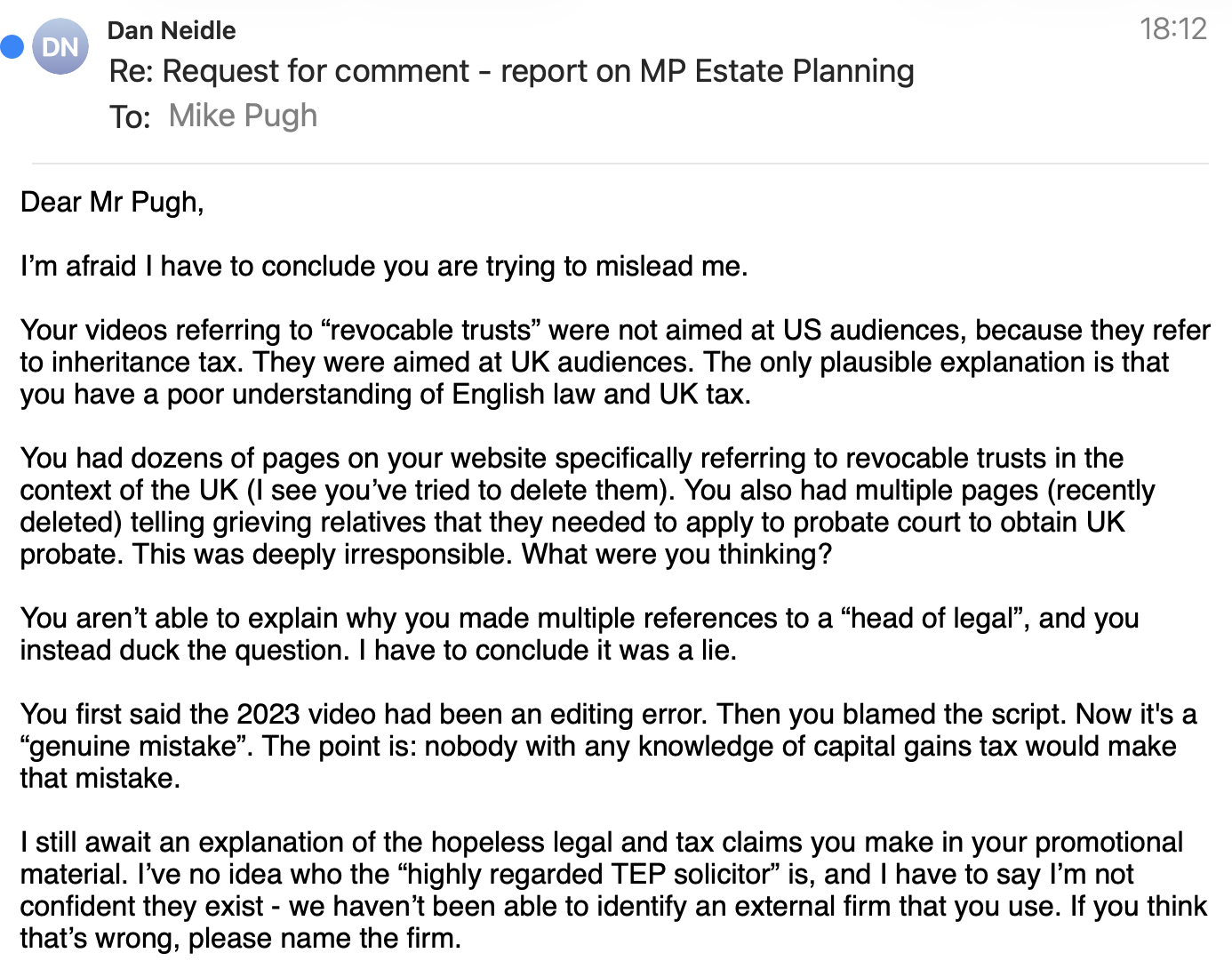

When we wrote to MP Estate Planning for comment in advance of publication (see below), their explanation for this video was that “the editing of the short-form clip conveyed the point poorly and could lead to confusion”. This is not credible. The statements above are complete propositions expressed in full sentences; they are not the product of an ambiguous or misleading edit. We put this to Mr Pugh; we didn’t receive a response.

It is hard to see any explanation for this video other than that Mr Pugh had no understanding of basic UK tax principles.

A series of errors

There are other basic errors and false claims in the many videos published by MP Estate Planning.

A video on cryptocurrency claims “certain reforms by the Labour Party may lead to increased tax guidelines on digital assets. This could impact how they are taxed during transfers and inheritances” – but there are no planned or announced changes to the UK tax treatment of cryptocurrency.

Another video says that if you declare a bare trust then the assets are still considered part of your estate and your estate pays tax on the income. That’s false: the beneficiary of a bare trust is usually considered the owner, and pays tax on the income.

And in another video, Mike Pugh says there’s stamp duty if parents gift their home to their children – there isn’t.7

There are lots of small errors like this that we regard as “tells” – signs that Pugh and his colleagues don’t understand their subject. Then there are some very large errors – the firm seems to believe that English law is similar to US law, when it very much is not.

Confusion between UK tax and US tax

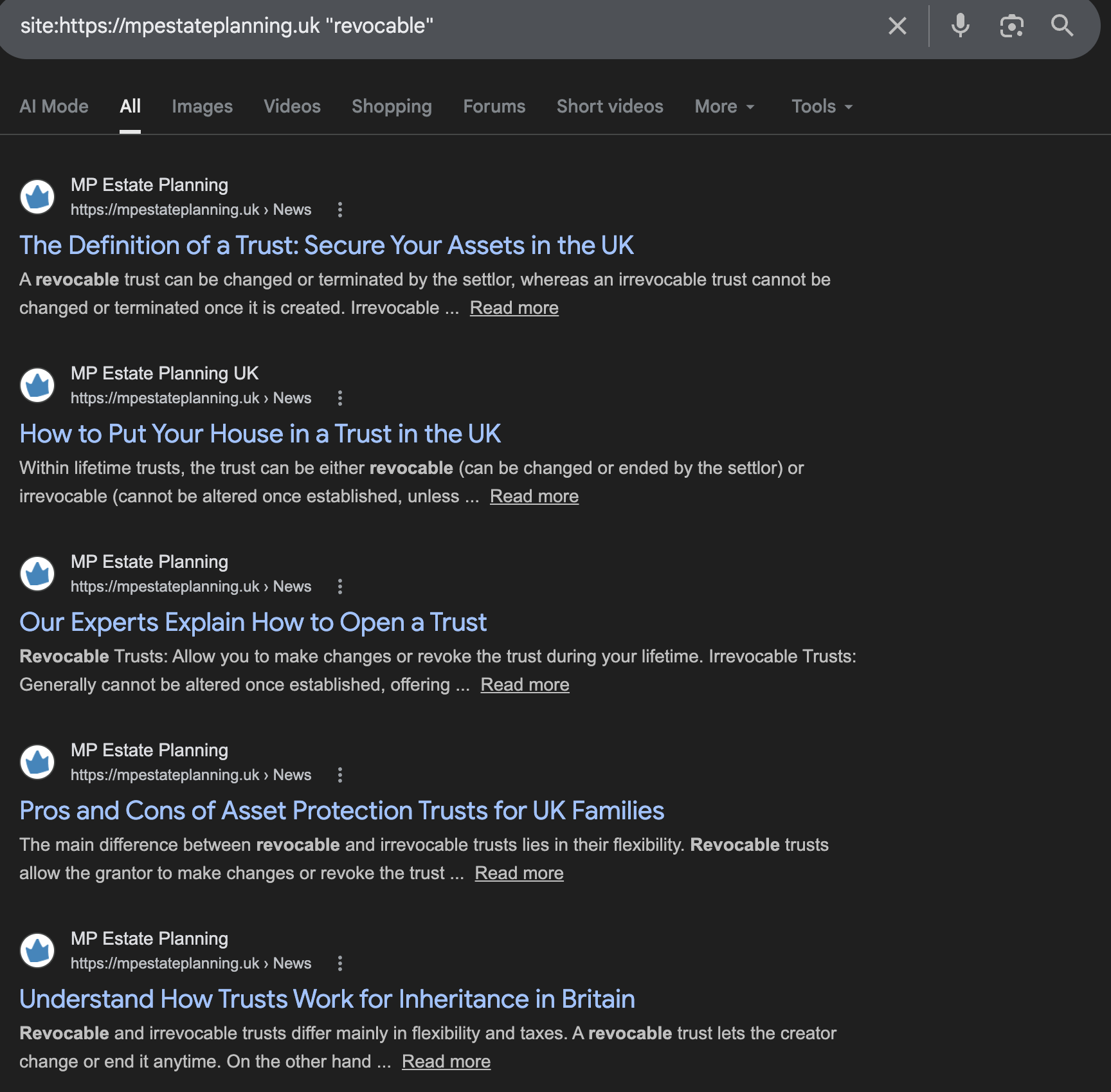

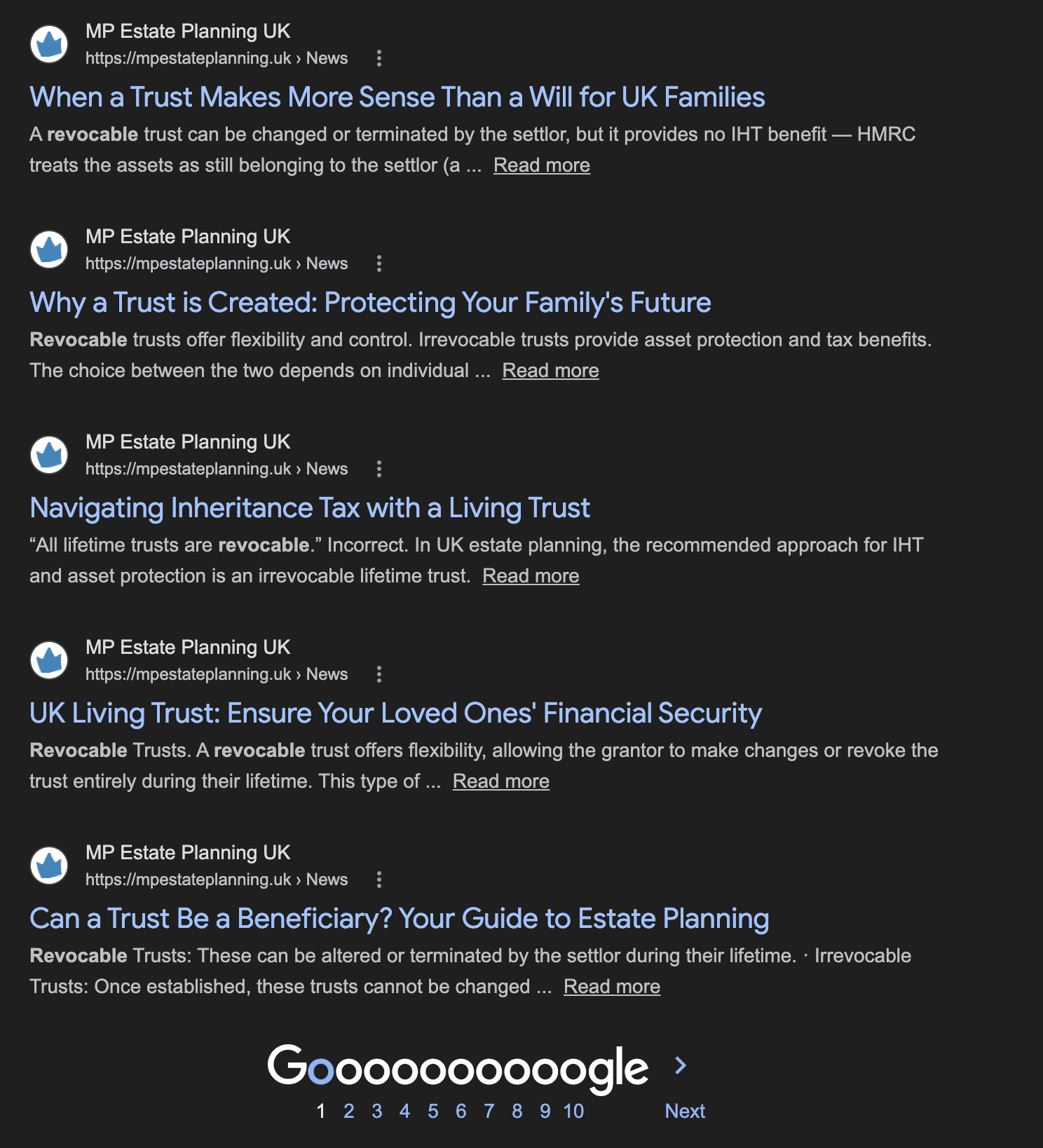

Mike Pugh frequently talks about “revocable trusts” and “irrevocable trusts”. These are US tax terms, which no competent UK adviser would use:

This isn’t a one-off. Multiple videos on MP Estate Planning’s YouTube channel, and dozens of pages on their website, discuss revocable and irrevocable trusts. In this video, Pugh claims that revocable trusts avoid probate and are “commonly used in estate planning”. They do not and they are not. Indeed American citizens who move to the UK are usually advised to terminate revocable trusts, because of the uncertainty as to how the UK system characterises them:

In this video, Pugh says that “revocable and irrevocable is more to do with tax status” and that you can “close” an irrevocable trust with an “advancement of the trust period”. None of this has any meaning in English law.

And this, from “frequently asked questions” on the MP Estate Planning website, suggests the firm is actually setting up “revocable trusts” for their clients:

We asked MP Estate Planning about this. Mike Pugh told us:

“You have identified instances where legacy or internationally sourced educational material has used terminology more commonly associated with US trust law.

Where those terms have appeared on UK-facing pages, we agree that they are not the correct terminology for English law and we are reviewing and updating older content accordingly.”

This appears to be untrue. This wasn’t “legacy or internationally sourced material”. It was Mike Pugh speaking in their own videos, for a UK audience, mixing up UK and US concepts in the same video.

A website full of “AI slop”

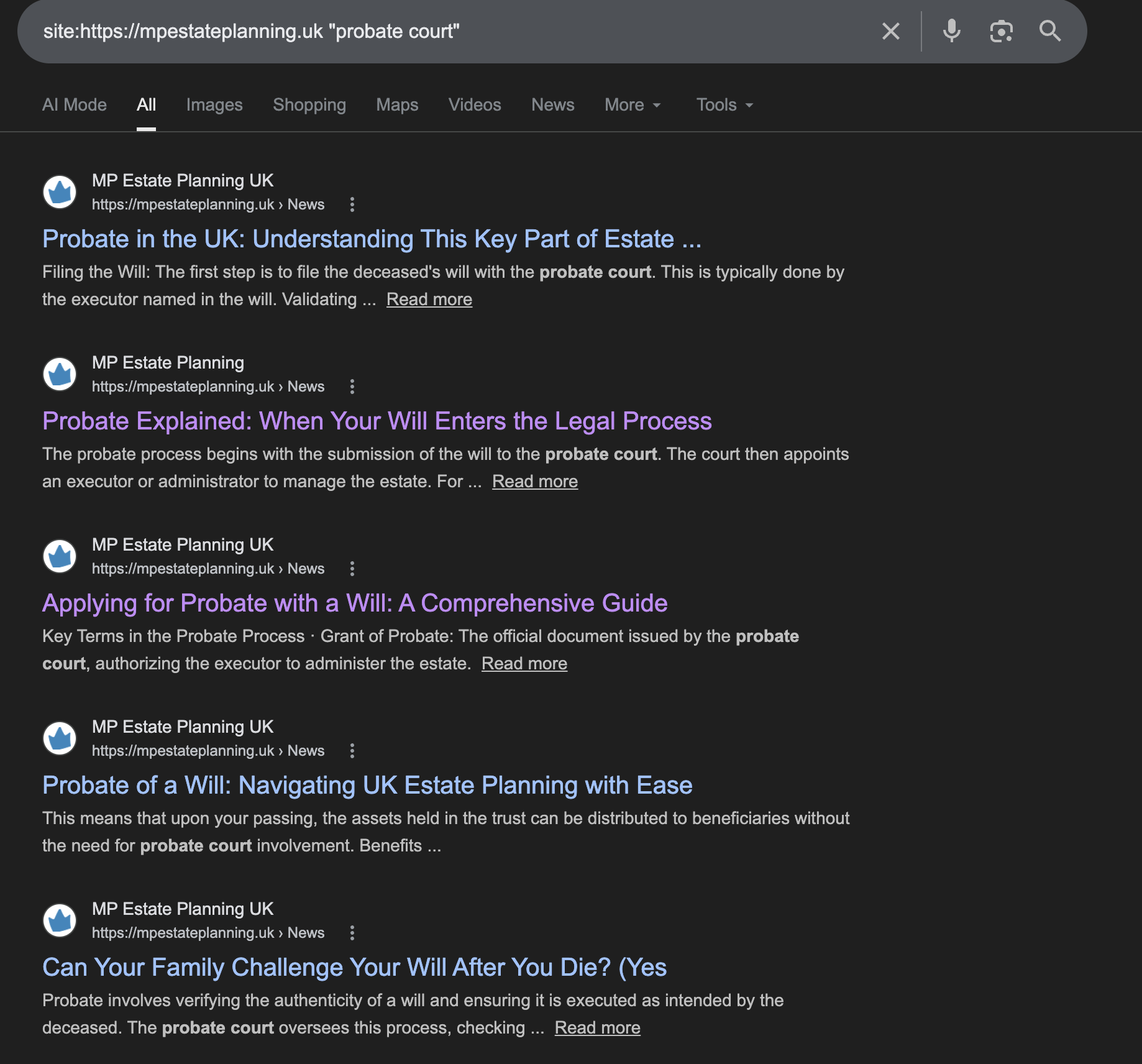

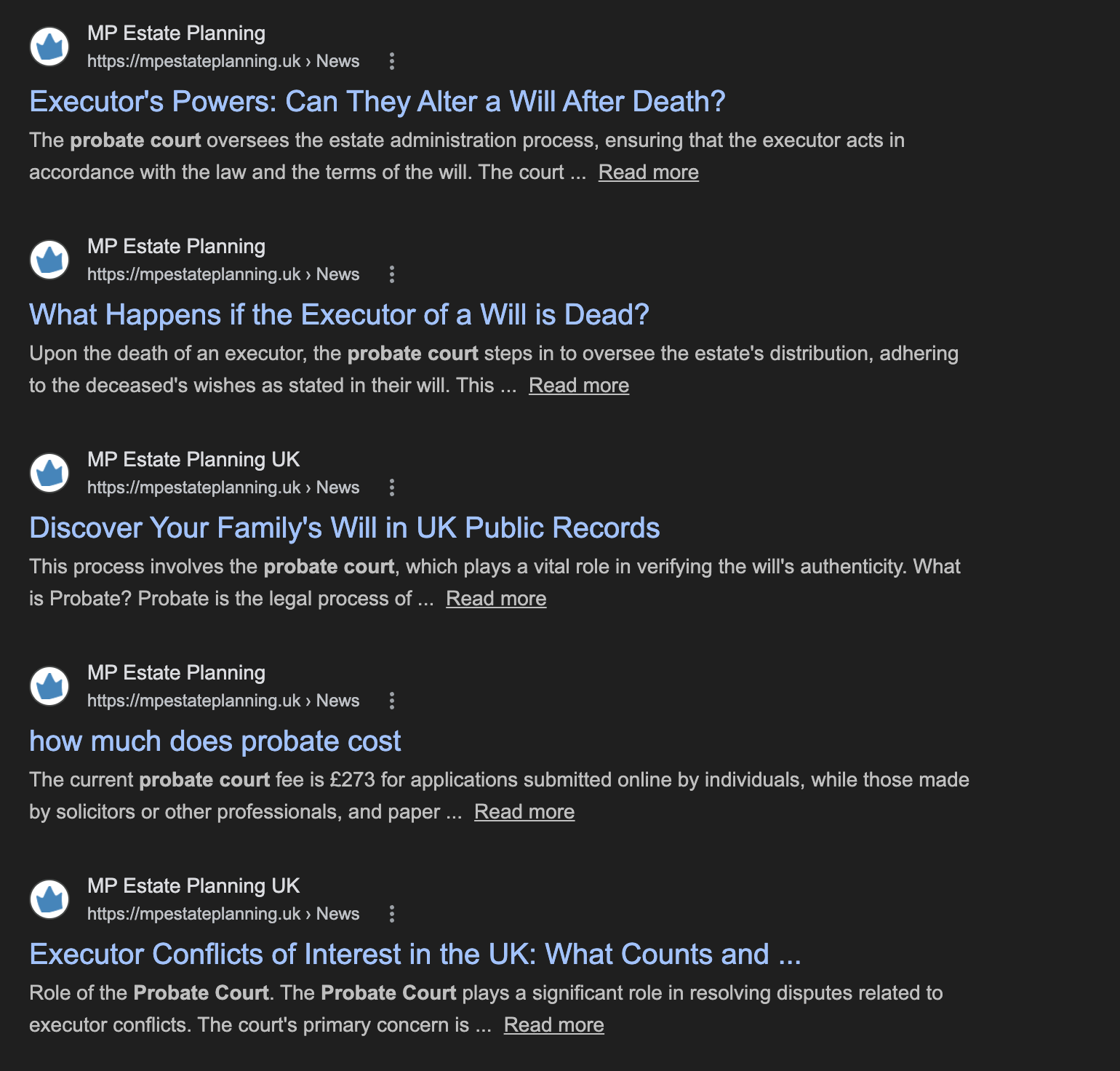

The MP Estate Planning website has hundreds of pages containing false claims about English law and UK tax:

- This page says the first step of probate is to submit the Will to a probate court. There is no “probate court” in the UK – you apply for probate using a form or online. Courts only become involved in contested cases. A dozen pages on the MP Estate Planning website used to refer to probate court, in the context of UK probate. Since we wrote to MP Estate Planning, these have been changed.

- A page on “asset protection trusts” says that life interest trusts and interest in possession trusts don’t trigger immediate inheritance tax charges – that is incorrect.

- This page on “settlor interested trusts” is extremely lengthy, and long on generic waffle (“settlor interested trusts occupy a distinct position, offering flexibility and control.”) but its list of tax issues omits the key point that a settlor interested trust is usually something that tax planning tries to avoid because the trust settlor remains taxable on trust income, and it’s a gift with reservation.

- This page on “how to put your house in a trust in the UK” discussed using a “revocable trust” – but that’s a US concept that has no equivalent in English law or UK tax law. Multiple pages discuss “revocable trusts”. Since we wrote to MP Estate Planning, they’ve been rewritten.

- This page about “inheritance tax allowances for married couples” talks about the IRS $15m gift tax exemption. This page on “How much can you gift each year without paying inheritance tax” said “[t]he annual gift exemption allows you to gift up to $18,000 per recipient per year”. There is of course no gift tax in the UK. But the MP Estate Planning website has dozens of pages warning about gift tax.

- Similarly, multiple pages discuss the concept of an “attorney-in-fact”. It’s not a concept in English law.

- This page about deeds of variation goes on for pages, talks about “gift tax” and repeats meaningless phrases like “several notable cases in UK law highlight the importance of Deed of Variation regulations” (there are no such regulations).

- A page on “Preventing Nursing Home Takeover” said “Options for funding care and government support, like Medicaid, might be available”. Medicaid is a US programme that can cover medical costs for people on low income. It is, obviously, not available to anyone in the UK. The new page is fixed.

- There are then many pages full of misinformation, many with little to do with tax or trusts. A page about dementia, for example, incorrectly describes the laws around incapacity, and includes an entirely invented quote attributed to the Alzheimer’s Society.

- This page says that if a UK resident gifts assets to a spouse living abroad, they may need to report the gift to HMRC. There is no such rule.

- Then more mundane errors: a page entitled “How to legally avoid inheritance tax: 2026 edition” says business property relief and agricultural property relief provide 100% relief – that was no longer correct after the 2024 Budget.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

There are over a thousand articles on various aspects of tax and trusts, and over three million words – and it’s full of errors. You can see a complete list here and here – note how the edit times are often only a minute apart (and you can also see, at the top of the second files, all the edits made after we approached MP Estate Planning in March 2026).

The obvious explanation: the website is mostly AI-generated – it’s what’s often called “AI slop“.

We expect the website was created in this way to maximise MP Estate Planning’s Google hits for people researching tax and trusts. It is, however, deeply irresponsible, because it’s providing people with false information.8

If an accounting or law firm behaved in this way then we expect there would be serious regulatory sanctions. MP Estate Planning, however, is entirely unregulated.

A mysterious business failure

MP Estate Planning is not Mike Pugh’s first Will writing venture. Before that, he incorporated a company called Maplebrook Wills Ltd in 2017. It provided similar services to MP Estate Planning, as well as selling a “franchise opportunity” to use its software, brand and templates in your own business.

Maplebrook Wills never appears to have had the success of MP Estate Planning. The business filed “micro-entity” accounts for 2019, 2020, and 2021. Its final filed accounts in 2021 showed total net assets of just £85,841. It then failed to file accounts for 2022, Pugh resigned as director (replaced by someone who appears to be his wife), and the company entered liquidation.

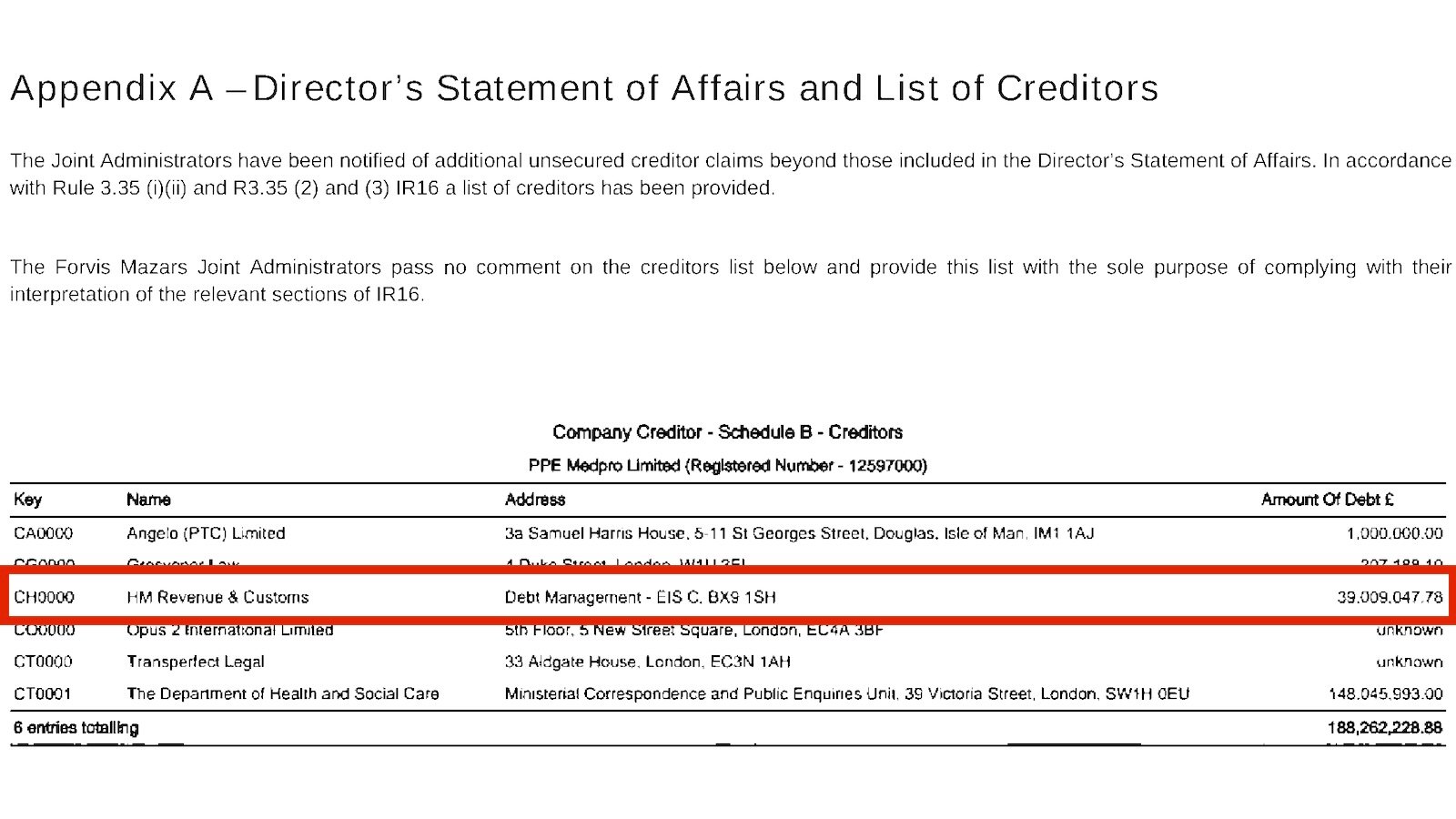

The liquidators’ initial 2023 statement of affairs made this look like a fairly ordinary small-company collapse: about £169,000 was owed to creditors, including about £78,000 to HMRC. But the later documents suggest there may be much more to the story.

Most strikingly, the liquidators’ 2025 report says that HMRC had now submitted a claim for £1,735,520. That is an astonishing figure for a small company. The report treats that claim as unsecured, not preferential. If so, that means it is not for VAT, or PAYE income tax or national insurance (which rank as secondary preferential debts in an insolvency). The £1.7m must, therefore, be something else – most likely corporation tax and/or very large HMRC penalties.

We don’t understand how so small a company could run up a £1.7m tax liability; to owe that much in standard corporation tax alone, a business would need to generate roughly £9 million in profit (and the accounts suggest this business’s profits were less than a tenth of that figure). Whatever the explanation, something appears to have gone badly wrong. And, at the same time, the preferential debts went up to £176,807.

The impression that something went very wrong is supported by the liquidator’s report that the director and bookkeeper have failed to cooperate with investigations into the company’s final trading period:

As previously reported, my statutory investigations into the company’s affairs remained ongoing. Creditors are aware that these investigations concern the movement of the company’s assets and liabilities since the last set of formal accounts was prepared, as well as transactions undertaken during the company’s final trading period.

Throughout the reporting period, I have continued to make extensive efforts to determine whether the transactions identified during the company’s final trading period were made in the ordinary course of business. I have also continued enquiries into the movement of assets and liabilities during the same period to ensure that such movements can be accurately accounted for.

Despite repeated requests issued to the director and the company’s bookkeeper, I have not received sufficient information to progress these enquiries.

Accordingly, following the period under review, I have formally instructed my Solicitors, Freeths LLP, to assist in obtaining the information required to advance my statutory investigations. Freeths LLP are currently reviewing the material available and will advise me on the appropriate next steps in due course.

I will provide creditors with a further update in my next report.

That is unusual language for what was supposedly a straightforward small-business failure. The liquidators are investigating transactions in the final trading period, movements in assets and liabilities after the last filed accounts, and have had to instruct solicitors because they say they have not received enough information from the director and the bookkeeper. That does not tell us what happened. But it does suggest the liquidators believe there are serious unanswered questions about the company’s affairs.

We can only speculate about the detail. One notable fact is that the Maplebrook franchise business appears to have been transferred to a new company, Maplebrook EDGE Network Ltd, incorporated before Maplebrook Wills Ltd went into insolvent liquidation. It is possible the liquidators are examining whether assets were moved out of the company for less than full value. But that is just a possibility.

This due diligence report from business intelligence firm Tech City Labs contains further information on MP Estate Planning, Maplebrook Wills, and other connected companies and individuals.9

Currently we have no explanation why a small company with roughly £90,000 of initial non-tax unsecured creditors should suddenly owe £1.7m to HMRC.

We asked Mike Pugh; he didn’t respond.

Accounts that make no sense

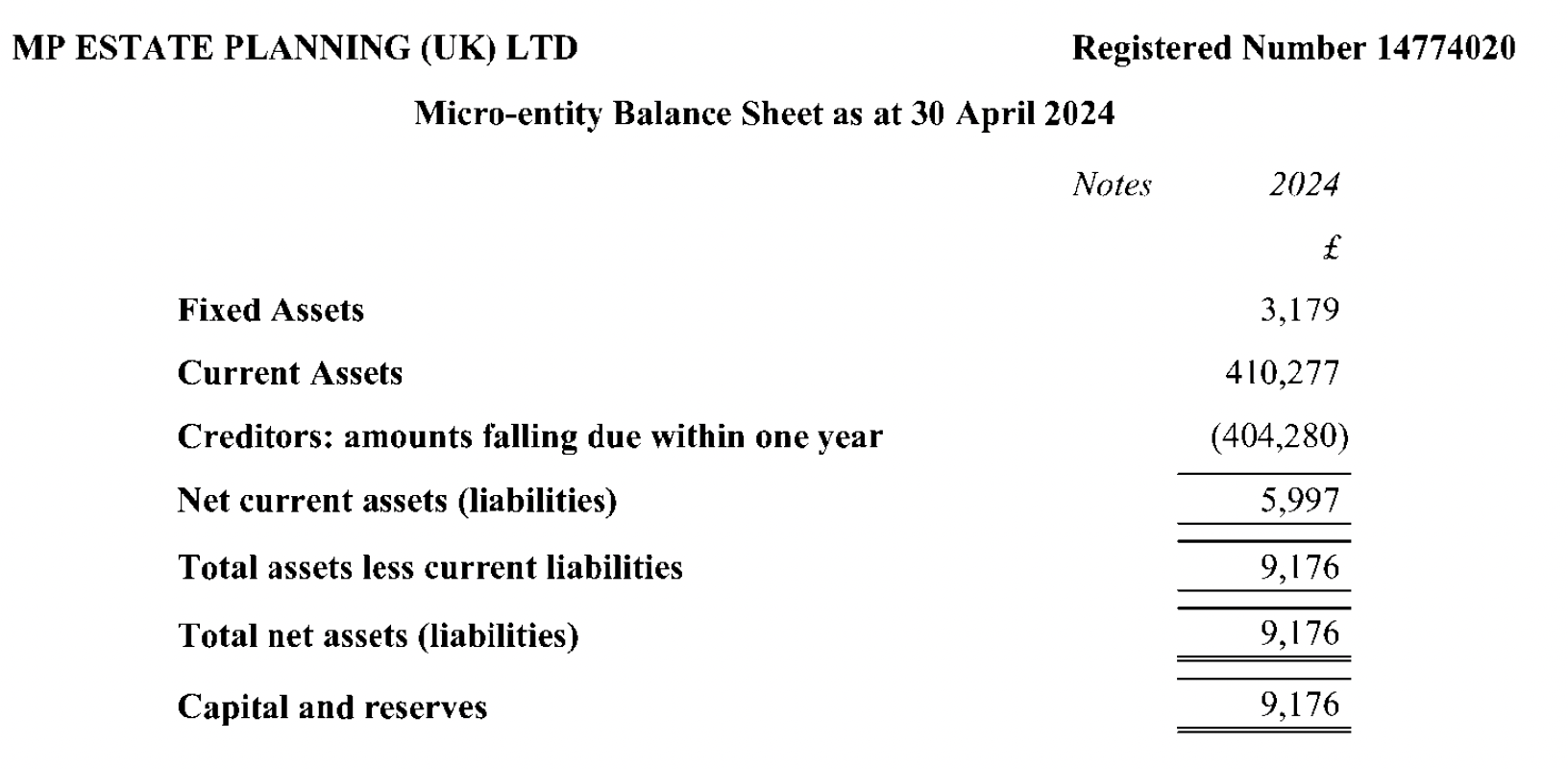

Here’s MP Estate Planning’s balance sheet for its first full year of trading, 2024:

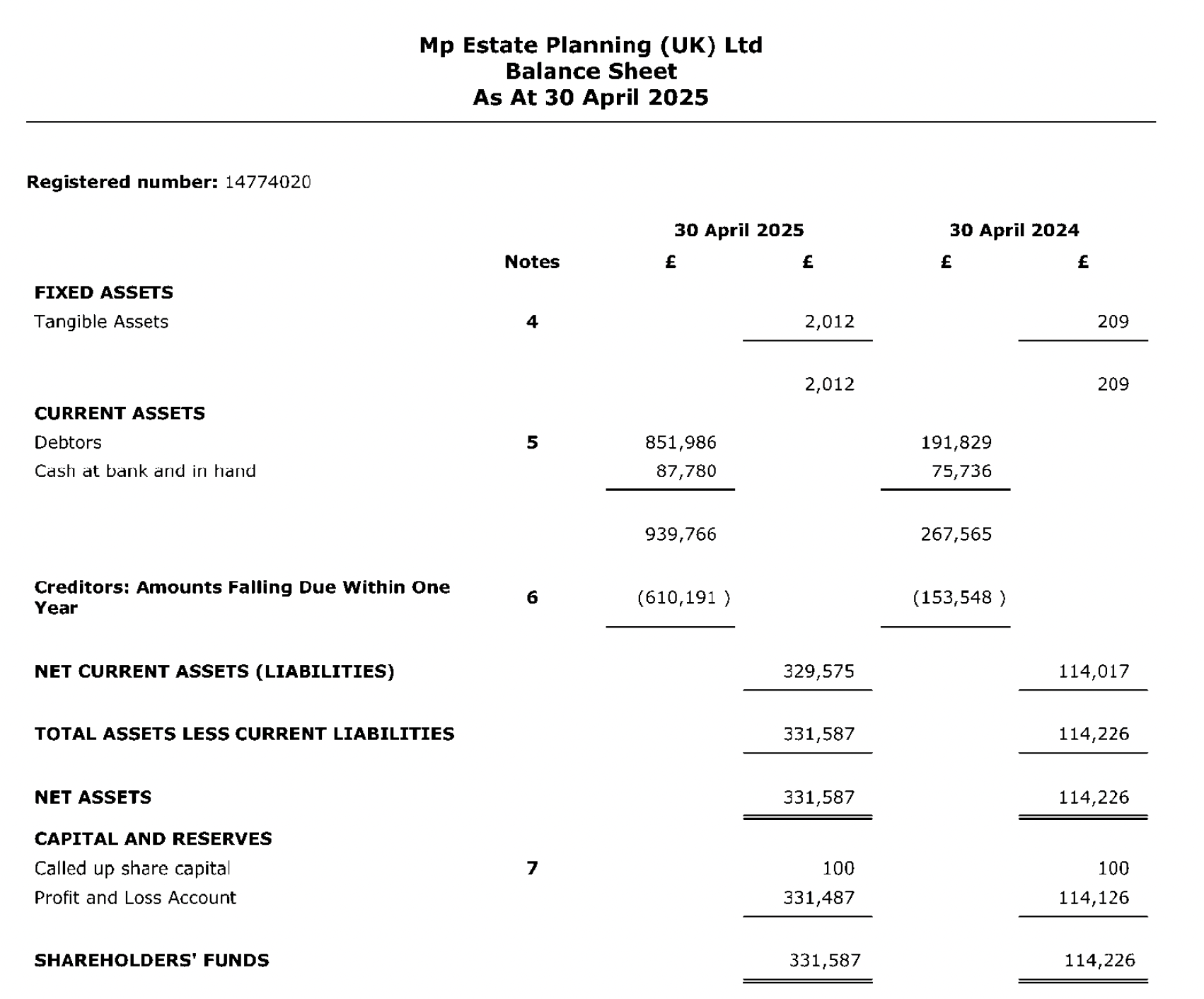

And here’s the balance sheet for 2025:

The 2024 figures here bear no relation to the figures in the 2024 accounts:

- Fixed Assets: The original 2024 accounts show £3,179. The 2024 comparative column in the 2025 accounts shows £209.

- Current Assets: The original 2024 accounts report £410,277. The 2024 comparative in the 2025 accounts reports £267,565.

- Creditors (due within one year): The original 2024 accounts list £404,280. The 2024 comparative in the 2025 accounts lists £153,548.

- Total Net Assets/Equity: The original 2024 accounts state the company had £9,176 in net assets. The 2025 accounts state the 2024 net assets were £114,226.

This isn’t a rounding issue, formatting issue, or taxonomy issue. These are just fundamentally different numbers. The accounts weren’t restated, there’s no prior year adjustment, and no note explaining the reason for the changes.

We have no explanation for this.

The 2024 accounts were filed using the Companies House online service (probably by Mike Pugh or someone at MP Estate Planning). The 2025 accounts were filed using professional accountancy software by “LC Accounting”. We believe it’s this small firm in Somerset – we wrote to them asking for comment, but didn’t hear back.

The pitch and the reality

What is a trust?

MP Estate Planning, and many other unregulated firms, sell trusts as a magic box that makes your assets disappear from the taxman and your creditors. The reality is that trusts are much less mysterious, and much less able to achieve these objectives.

A trust is a legal arrangement for holding assets. The key idea is that legal ownership (whose name is on the title) can be separated from beneficial ownership (who is entitled to benefit).

Every trust has:

- Trustees: the people (or a company) who hold the assets legally and make decisions. Trustees must act in the best interests of the beneficiaries and follow the trust deed. They can be personally liable if they get it wrong.

- Beneficiaries: the people who can benefit from the trust (for example, by receiving income or capital, or by living in a property).

- A settlor: the person who creates the trust and usually provides the assets.

- A trust deed: the document setting out who the trustees and beneficiaries are, and what powers and rules apply.

Trusts are used for many legitimate reasons (for example, to manage assets for children, to provide for a vulnerable person, or to control how family wealth is distributed). But they come with real-world consequences: trustees have duties, paperwork and often ongoing administration.10

- From Settlor to Trustees (Label: Transfers assets)

- From Trustees to Trust Assets (Label: Legal Ownership)

- From Trustees to Beneficiaries (Label: Beneficial Ownership)

Newspaper headlines often give the impression that trusts avoid tax. However, for most normal people, trusts are not good tax planning vehicles. Precisely because of their historic association with tax avoidance, successive Parliaments have built an extensive set of rules around them:

- A gift into trust is a “chargeable lifetime transfer” – inheritance tax at 20%11 of the value of the property put into trust (after the £325k nil rate band).

- The trust is then liable to an “anniversary charge” of up to 6% on its value (above £325k) every ten years.12

- If you “give away” an asset but keep the benefit (for example, you keep living in your home rent-free), tax law will often treat you as still owning it, whatever labels are used in the documents.

- You can be hit with a capital gains tax charge when you put assets into trust.

- The trust itself is subject to capital gains tax and income tax, and its distributions to beneficiaries are also taxed.13

This is a very simplified summary of what is a very complex and frequently-changing set of rules.

The pitch

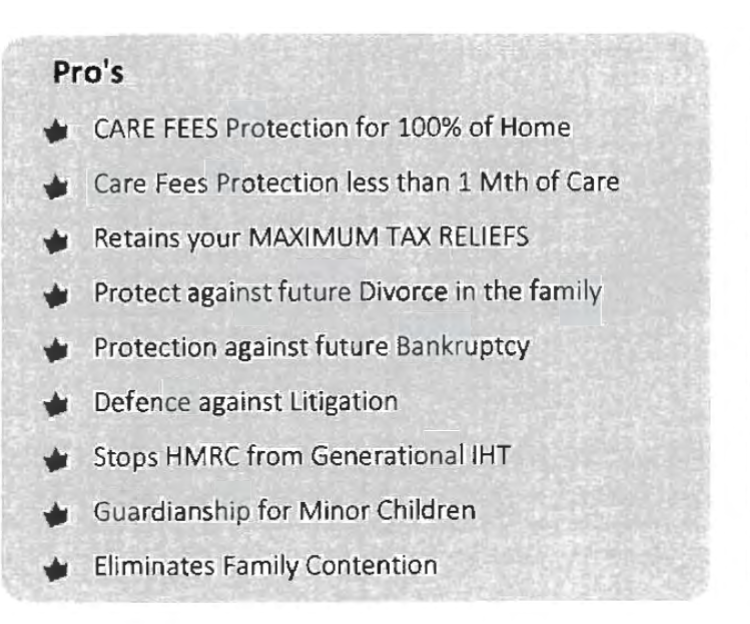

MP Estate Planning UK Ltd was founded by Mike Pugh, a Canadian who came to the UK in 2017. He claims to have a solution to “ALL THE MODERN THREATS”. Meaning: inheritance tax, care home fees, divorce and creditors:

Here’s a complete client proposal from MP Estate Planning:

There are four separate tax claims here:

- You can put assets in trust but avoid the 20% entry charge and 6% anniversary charge.

- You can give assets to your children but still live in your house, and avoid the “gift with reservation of benefit” (GROB) rules.

- Another loophole lets you give your house to your children, and still live in it, thanks to a 1999 case.

- And you can give your rental properties to your children, but get them to “gift” the rent back to you, so you still live off the income.

Our starting point is that lifetime trusts are poor tax planning for most people. They often result in more inheritance tax because the spouse exemption and residence nil rate bands aren’t available to trusts.

The MP Estate Planning structures we reviewed are, however, worse than that: they have no tax benefit and likely trigger a series of unnecessary tax bills.

In this video, Mike Pugh describes advising an elderly widow to put a £650,000 property in trust. That’s terrible advice – as he says, there is no inheritance tax benefit – but what he doesn’t say is that there will be up-front inheritance tax on the creation of the trust of £65,000.14 Putting the property in trust also results in the permanent loss of the residence nil rate band, which would have been worth up to £110,000 for her.15 And any future capital gain will be taxed in the trust – it wouldn’t have been if she’d retained ownership. This is a tax disaster – for which Pugh says he charged her £5,340.

One experienced adviser told us that the tax claims made by MP Estate Planning were so egregiously bad that they looked like fraud.16

The following sections look at each of these claims. We put our criticisms to MP Estate Planning and they told us they’d respond – they didn’t.

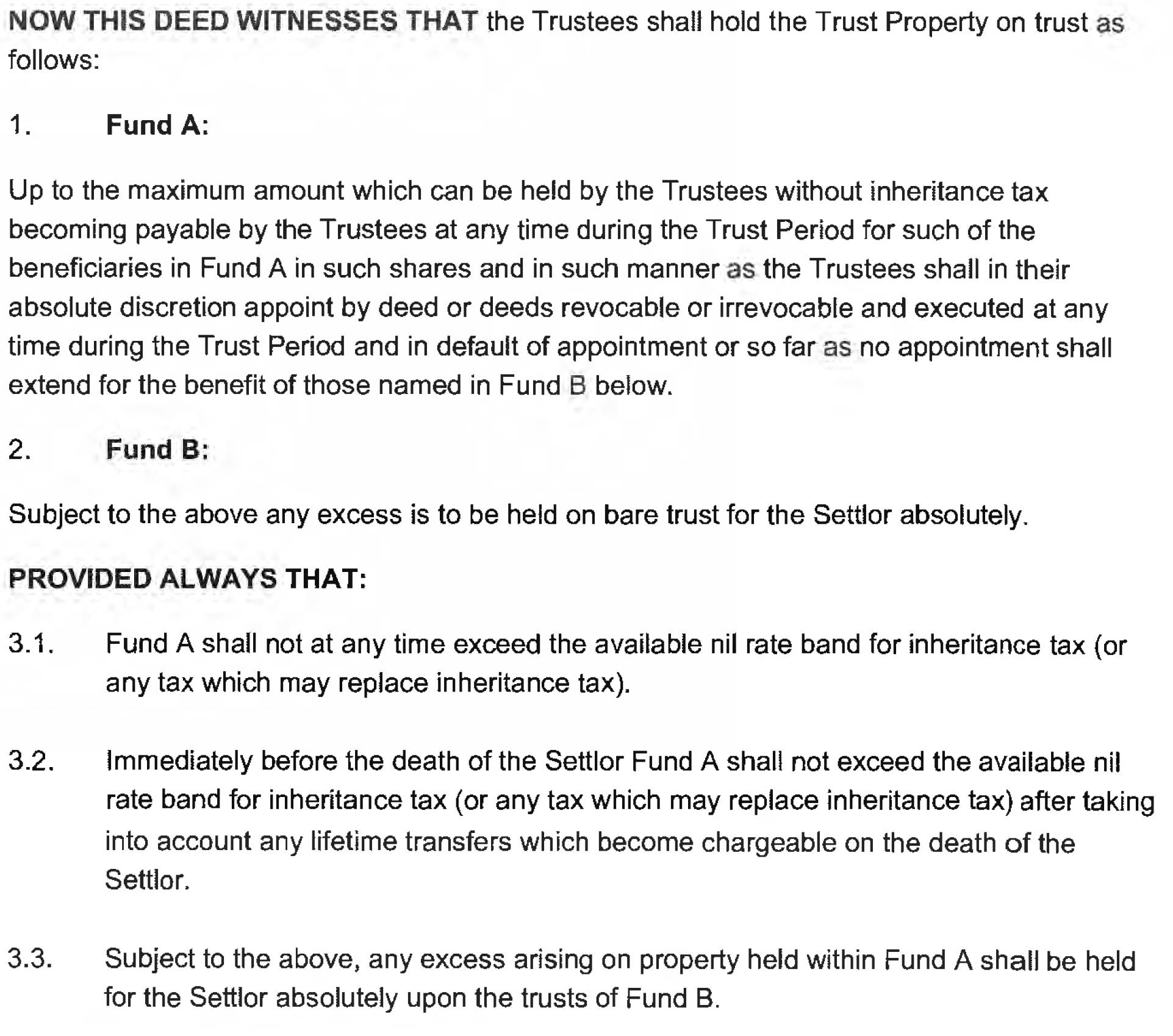

1. “Presto magic” to avoid the 6% anniversary charge

The inheritance tax changes in the 2024 Budget created a huge demand for inheritance tax planning. That’s caused an influx of unregulated firms offering inheritance tax solutions that are “too good to be true”.

MP Estate Planning’s pitch of “every home in a trust” has the immediate problem of the 20% entry charge and 6% anniversary charge every ten years, each on value over £325,000.

But Mike Pugh has a solution: trustees can simply shift the excess over £325k out of the trust and, “presto magic” there’s no tax to pay:

We’ve seen how they implement this:

This does not work:

- An obvious point: all the claimed advantages of the trust: inheritance tax avoidance, protection against divorce and care home fees, are now limited to the first £325k of value. That’s pretty pointless, given that the first £325k of value is exempt from inheritance tax anyway.17 We expect most of MP Estate Planning’s clients have houses that are either worth more than that, or will likely be worth more than that in the foreseeable future.

- It’s unclear how this is supposed to work as a practical matter; it’s even possible the trust is void for lack of certainty.18

- The fact the settlor can receive back value from the trust means that it’s classified as a “settlor interested trust”, and so there’s an up-front capital gains tax charge on the disposal of the property to the trust (unless main residence relief applies). Hold-over relief is unavailable.19 Any income from the trust (for example rental income) is taxable in the hands of the parent/settlor.

- When and if the value of the trust property exceeds £325k then the way the trust is drafted means there is a reallocation from Fund A to Fund B, and a transfer of beneficial ownership to the parent/settlor. That’s probably a capital gains tax disposal at market value. So any rise in value over £325k, even just as property prices rise over time, may trigger a 24% CGT charge (although how this would work in practice is not clear).20

- One of the main purposes of the trust is to avoid the 6% anniversary inheritance tax charge. This is achieved by the Fund A and Fund B mechanism, which we regard as contrived and abnormal. MP Estate Planning promote this structure. It follows that MP Estate Planning had an obligation under the Disclosure Of Tax Avoidance Schemes rules to disclose the structure to HMRC. We understand that they did not.

- This trust could well mean that the parents lose the main residence capital gains tax exemption (because they no longer own the house). That’s a serious tax downside which MP Estate Planning never mentions.

We discussed this structure with a leading tax KC – he said he thought the trust was “a poorly drafted mess and would cause more problems than it solved”.

2. Avoiding GROB with a school uniform

The most obvious inheritance tax planning is to give your house and other valuable assets to your children – provided you live for seven more years, the assets are outside your estate.

You are perfectly entitled to do this if you are really making a gift. But if the gift is just on paper, and you continue to benefit from the property, then your “gift” is ignored for inheritance tax purpose thanks to the “gift with reservation of benefit” rules. The classic example is: I give my house to my children, but I continue to live in it. It’s a “gift with reservation of benefit” and disregarded.

MP Estate Planning say there’s an easy solution:

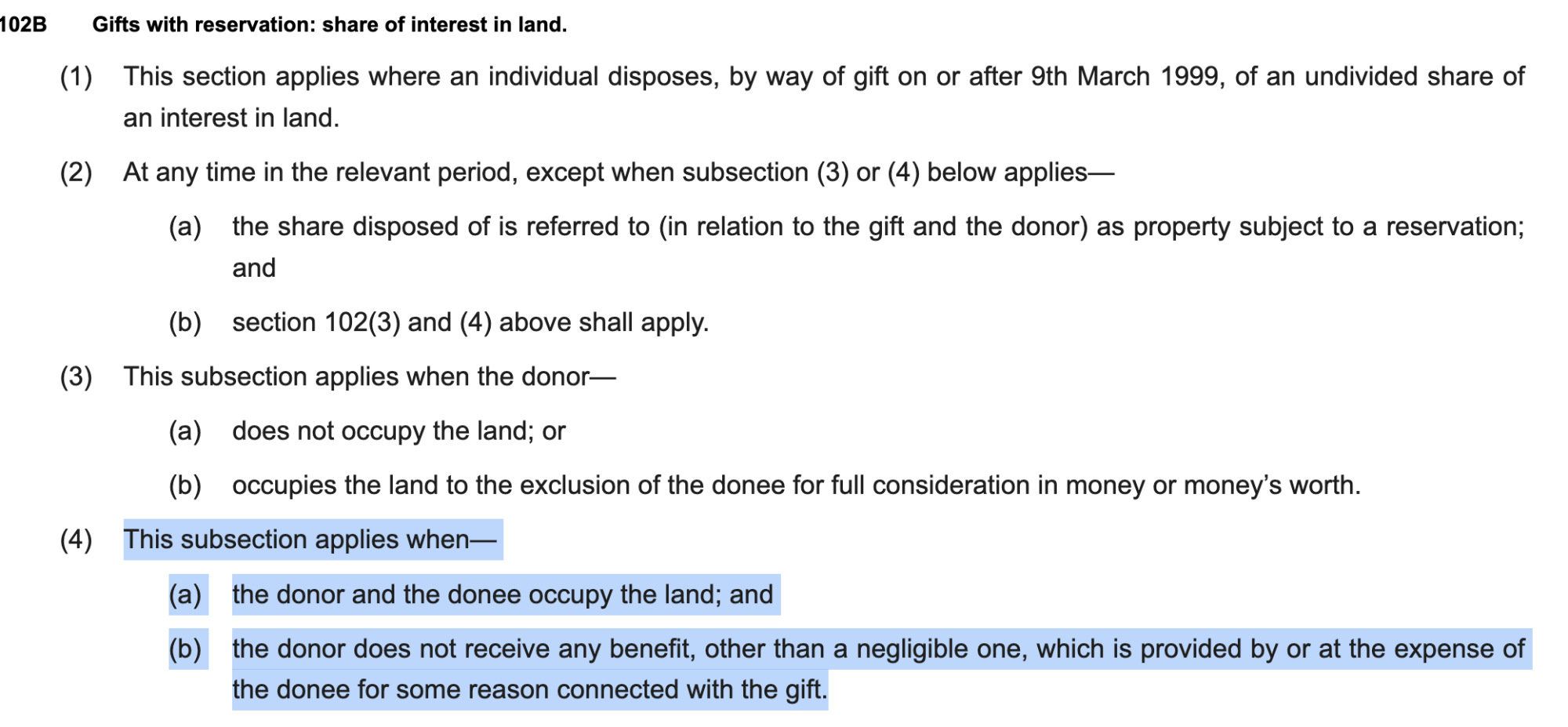

Mike Pugh is referring to the rule in section 102B(4)(a) Finance Act 1986 – it was introduced specifically for the situation where an adult child lives with a parent to look after them:

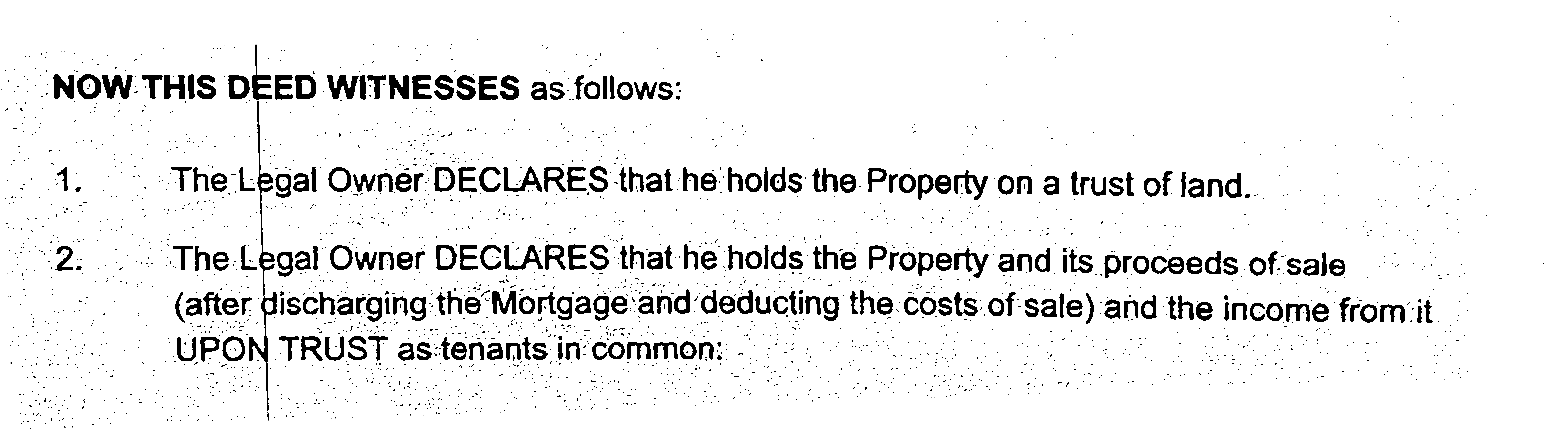

The key elements are that there is a gift of an undivided interest in land (e.g. “parent gives half the property to the child”), the donor and donee occupy the land and the donor doesn’t receive a benefit from the gift.

The first thing MP Estate Planning get wrong is that they don’t know what an undivided interest in land is. Here’s their attempt to create one:

One person cannot hold as “tenants in common”. It’s a hopeless failure to get within section 102B.

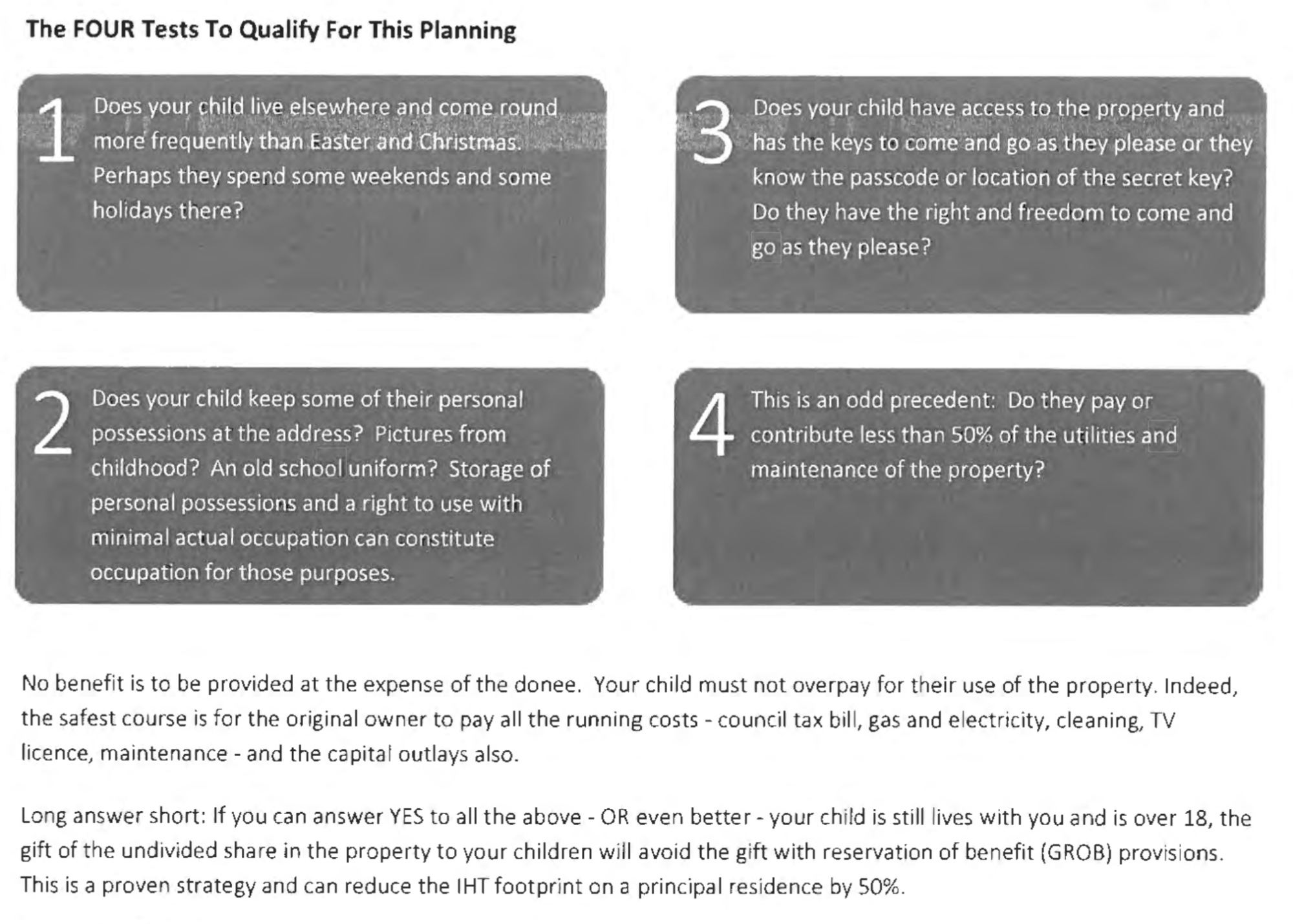

Even when they get that right, MP Estate Planning have a bizarre idea of what the word “occupy” means:

In other words, they think that a child will “occupy” the land for this purpose if they visit their parents occasionally, keep belongings in the house (such as a school uniform), and have access to the property and a key. That is contrary to the normal human meaning of “occupy”. Some advisers interpret the section as permitting children to live elsewhere primarily, provided they visit most weekends and holidays.212223 However MP Estate Planning’s view that you “occupy” a property if you visit it a few times a year goes far beyond anything our team has seen.

We therefore view this planning as well outside mainstream tax planning; we believe HMRC would challenge it if they became aware of it, and we don’t think the taxpayer would have any material prospect of success.24

MP Estate Planning suggest the planning is more effective if the child receives the gift and then lives with the parents. That is obviously correct – indeed the planning works if the child lives with the parents (and in our view that would continue to be the case if, for example, the children were at university but retained a bedroom at their parents’ house, and stayed there for some weekends and most holidays). However the problem is that children tend to leave, and at that point the reservation of benefit rules will apply.

We believe one of two things are happening. Either MP Estate Planning has misread “occupy” in s102B(4)(a) as “able or entitled to occupy” (the test in a preceding section), and don’t realise that section 102B(4)(a) requires actual occupation. Or this is an attempt to fool HMRC with a school uniform.

One experienced adviser described it to us as “utter nonsense”. Another, a tax KC with trusts tax expertise, said “it doesn’t look like they’ve read the legislation”.

There is a further even more obvious problem. We’ve seen a case where MP Estate Planning advised that the “occupy” strategy worked to prevent a gift with reservation of benefit where property was put in trust. It cannot. Section 102B(4)(a) requires that the “donee” occupy the property. When property is declared on trust then the “donee” is the trust, and a trust can’t occupy anything. This point is usually well⚠️ understood by advisers.25

3. Using a 1999 licence loophole that doesn’t exist

MP Estate Planning claim to have found another loophole, and one which has existed since 1999:

Mike Pugh is very vague here, but we’ve seen documents where Estate Planning claim that you can put your home into a trust, exclude yourself as a beneficiary, but still carry on living there under a “trustee licence”. They say this means there is no “gift with reservation of benefit”.

We saw an email to a prospective client in which an MP Estate Planning employee said:

“The design allows the settlor to retain occupation under a trustee licence, not a beneficial right — ensuring no ‘gift with reservation’…

No rent or benefit is reserved.”

This is a hopeless argument. The gift with reservation rules look at whether you have given away the property whilst still “enjoying” it. The legal form used – lease, licence, or anything else – is entirely irrelevant.

There is a straightforward, well‑known way to make a gift of a home effective while you keep living there: you pay the new owner a full market rent for the rest of your life. The legislation expressly allows for this.26 MP Estate Planning’s pitch is the opposite: they say there is a “trustee licence” and “no rent”. If that is what happens in real life, it is hard to see how the arrangement can be anything other than a reservation of benefit.

The 1999 case they refer to is Ingram v IRC (1999). The case is nothing to do with licences vs leases (there is a nice explanation of Ingram here), but in any event Ingram was effectively overriden by legislation in 1999.27

Quite aside from not working, the structure has the significant downside of losing the parents’ main residence capital gains tax exemption.

There may again be an obligation for MP Estate Planning to disclose the scheme to HMRC under DOTAS; we understand that they have not done so.

A tax KC we spoke to described MP Estate Planning’s approach as “baffling”, saying “I have no idea what they think this can achieve”.

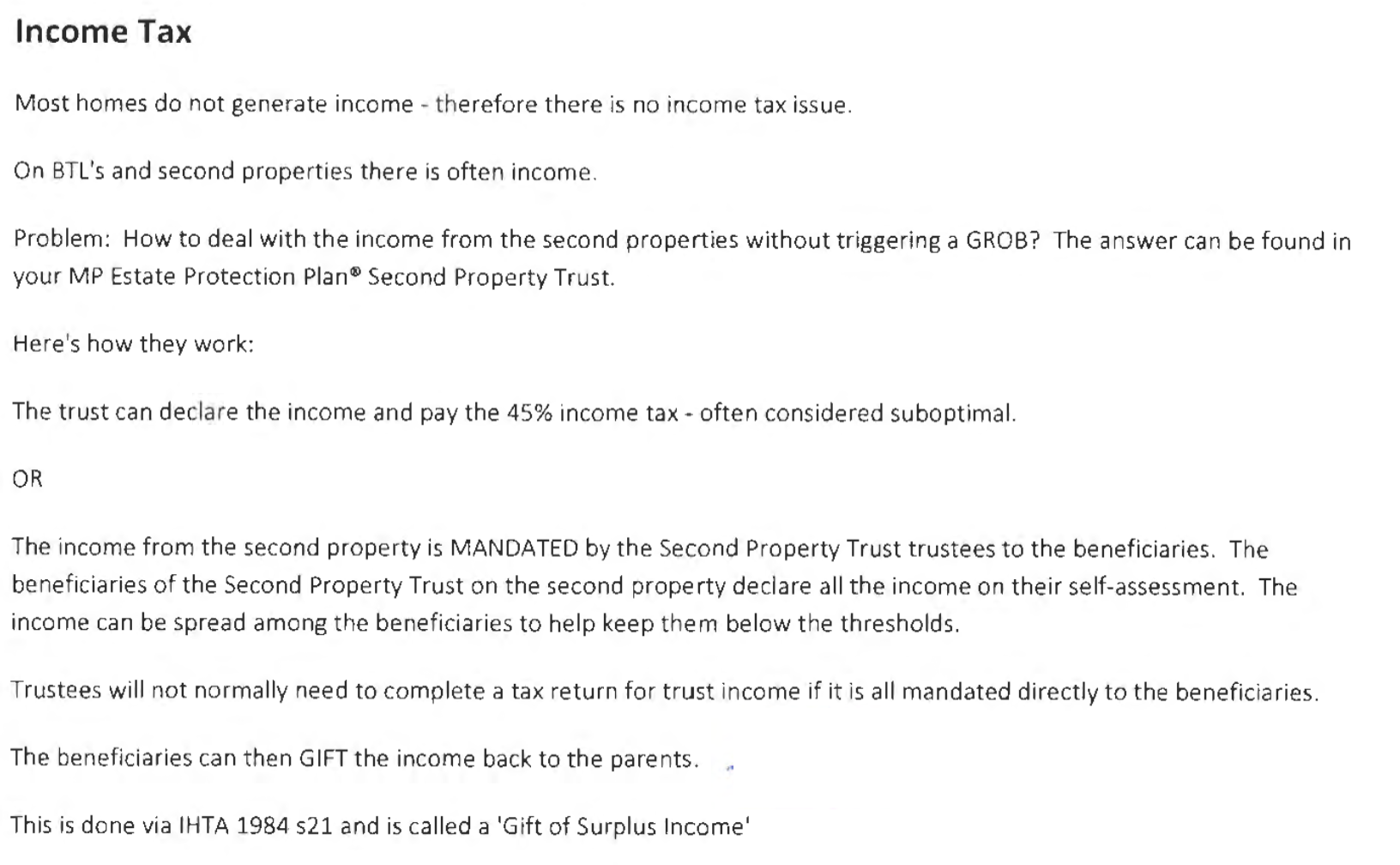

4. Gifts that ignore an anti-avoidance rule

In principle it’s easy to avoid inheritance tax: just give your assets to your children. But there’s an obvious problem: most retired people who have assets live off the proceeds of the assets.

MP Estate Planning say you can have your cake and eat it: put rental properties into a trust, but still receive the rent from the properties:

The idea is simple: the trust mandates the rental income to the beneficiaries (the children) and they pay tax on it, and then give the money back to their parents.

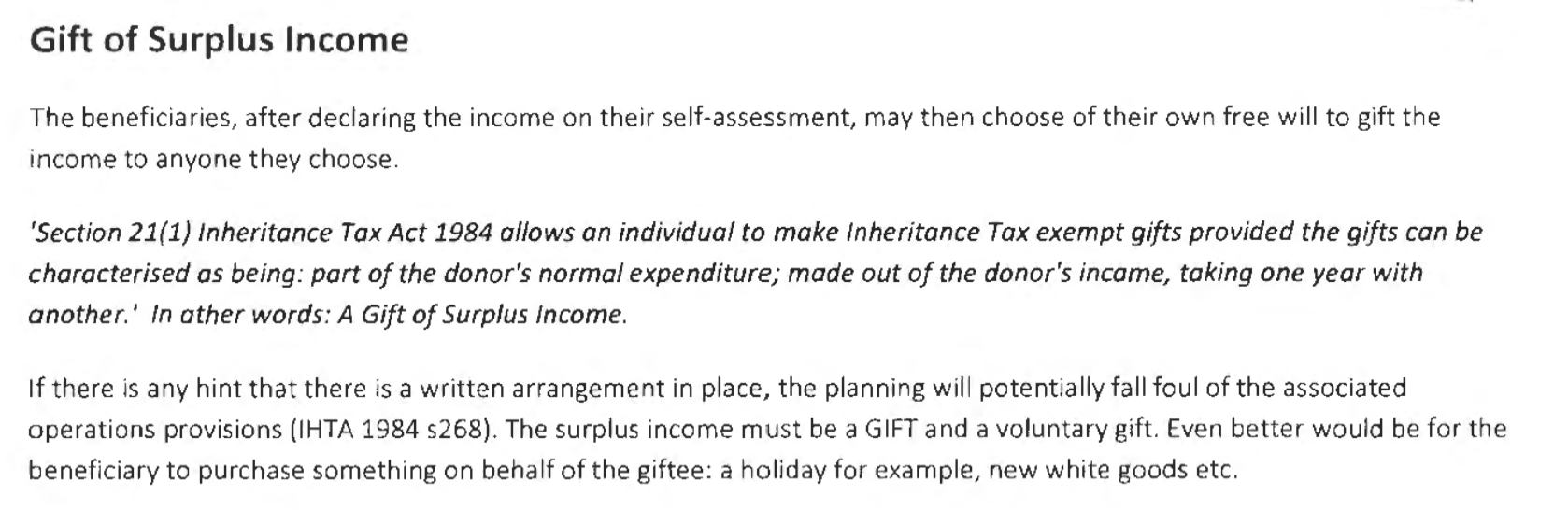

And MP Estate Planning say that, as long as there’s no written agreement, it’s fine:

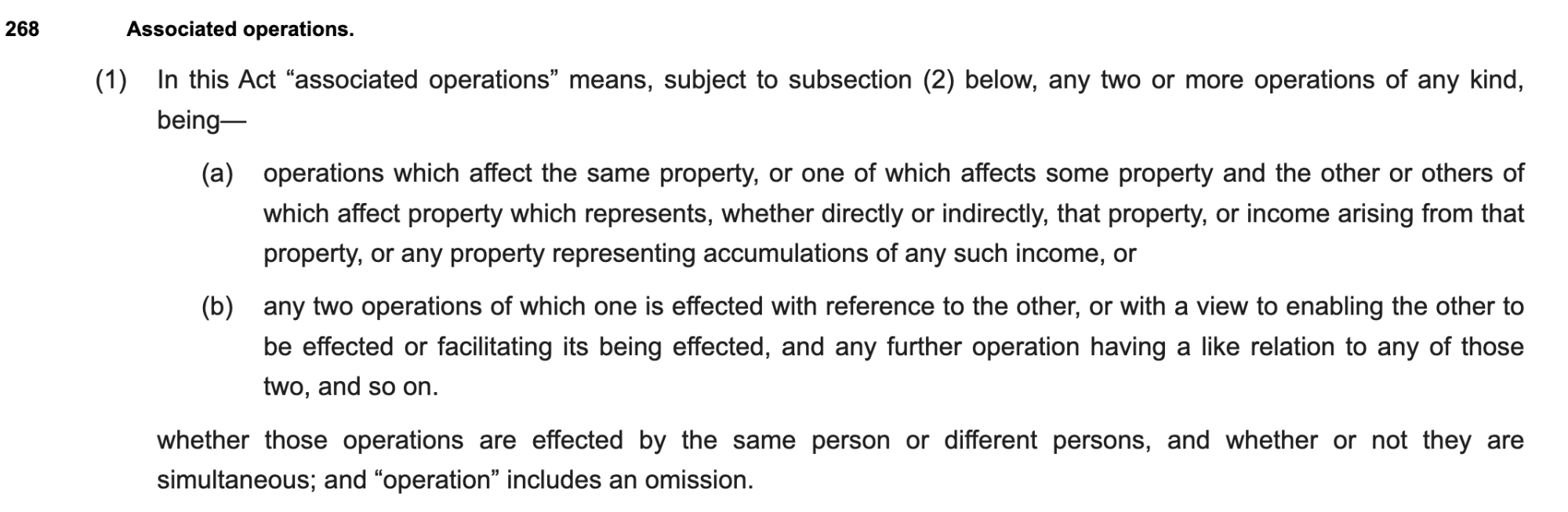

“If there is any hint that there is a written arrangement in place, the planning will potentially fall foul of the associated operations provisions (IHTA 1984 s268).”

This is very wrong.

The “associated operations” rules allow HMRC to treat a series of connected transactions and steps as a single arrangement when determining whether a transfer of value (like the gift of rental properties) has taken place.

Here’s the definition:

There is no requirement in the legislation, caselaw or HMRC guidance that the “operations” in question are in writing (and HMRC give an example in their guidance where successive gifts are subject to the rules).

In HMRC v Parry, the Supreme Court held that, applying Macpherson, the associated operations rules may apply if steps form part of and contribute to a scheme intended to confer a gratuitous benefit. Whether such a scheme exists is a question of fact, and may be established by evidence showing how the steps were intended to operate together; it does not require a formal written arrangement.

In this case there is clearly a scheme: the gift of the properties and the return of the income are clearly intended to operate together. This, after all, is what MP Estate Planning are selling. We therefore think it’s reasonably clear the “associated operations” rules will apply, so that for inheritance tax purposes the gift and the return of income would be analysed together as a single scheme.

The effect is that the arrangement must be analysed as a single scheme, so that (for inheritance tax purposes) the parents continue to benefit from the rental income. The ‘gift with reservation of benefit’ rules will, therefore, immediately bite. The consequence is that the full capital value of the properties will be treated as still belonging to the parents’ estate when they die, and heavily taxed. The structure therefore fails in a rather messy, entirely pointless, and highly expensive manner.28

High risk landlord tax planning

MP Estate Planning seems to be trying to move into general tax planning for landlords, and are adopting some planning that we would characterise as extremely high risk.

A slide from an MP Estate Planning podcast is suggesting that a landlord holding properties directly could form a partnership for a year, then incorporate the partnership, and have no capital gains tax or stamp duty:

![lf you have a property portfolio with 4 or more

properties, did you know it’s possible to:

© Reduce the 40% Inheritance Tax rate to *

# Reduce the 24% Capita) Gains Tax rate to

# Reduce Stamp Duty to 1

(UR approach

1, Paromita 1 Yam]

2 lncarparation

3 teu thereafter)

4. Share Plann

ha

Ngee FOR SALE](https://taxpolicy.org.uk/wp-content/uploads/2026/03/slide_sdlt_partnership.jpg)

The idea appears to be that the landlord first transfers their properties into a newly-created partnership – so, for example, if they own property with their spouse, the married couple are the partners in the partnership. They run that partnership briefly, and then transfer the partnership business to a company. The promoters claim that this avoids capital gains tax, stamp duty land tax and inheritance tax.

This planning is extremely high risk.

In principle a partnership can in some circumstances incorporate its real estate business without stamp duty land tax – but if there is a scheme of transactions to establish the partnership and then incorporate then the section 75A anti-avoidance rule means that SDLT will likely apply. If someone is obtaining the advice in this slide from MP Estates then it will be reasonably clear there was a prior arrangement. Waiting one year, or five years, makes no difference.2930

The capital gains tax planning could in principle succeed – there is potentially incorporation relief on the transfer of a business to a company. However it is a technical and difficult relief which normally requires the landlord to be carrying on a genuine property business, not merely holding investment properties, and can be hard to apply where the property is mortgaged. HMRC are scrutinising incorporation relief claims at the moment, and the law is about to change to require incorporation relief claims to be filed with HMRC.

We would suggest landlords carefully consider whether the tax and other benefits of incorporating justify the risk of high capital gains tax and stamp duty land tax charges. A competent tax adviser will always explain the level of risk and the worst case downside. When an adviser doesn’t do this, in our view it raises a large red flag.

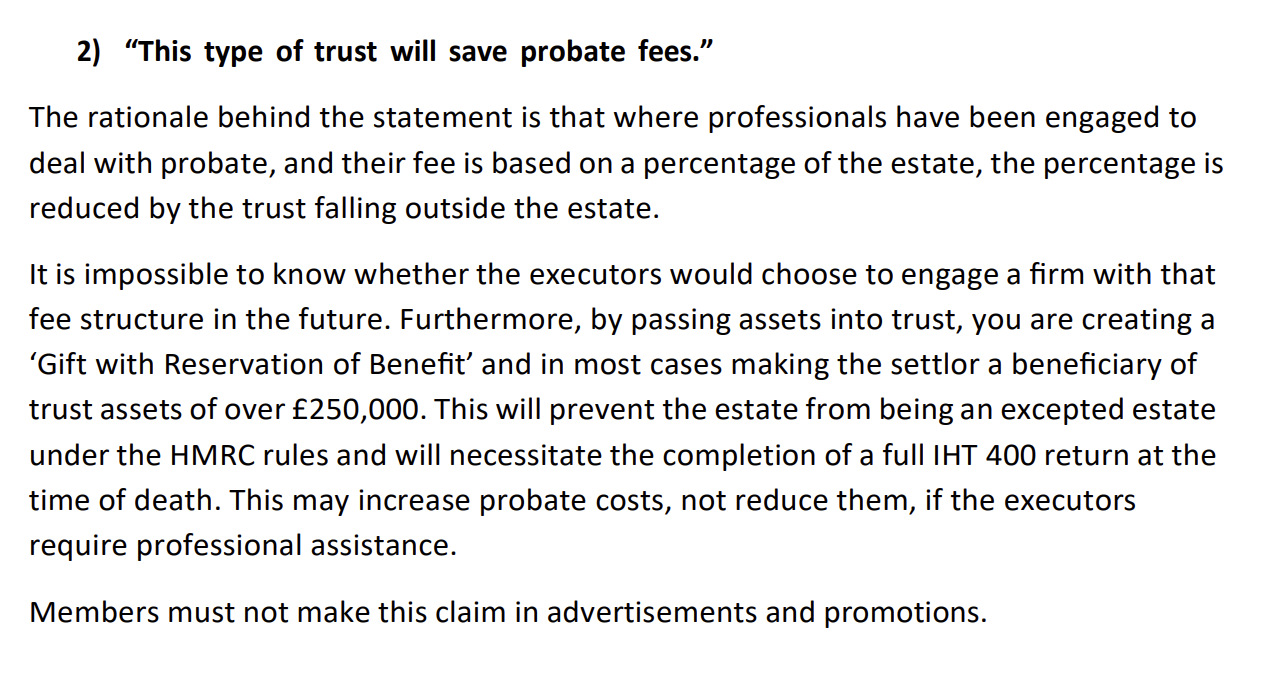

Saving probate costs

Elderly people are often worried about the future costs of probate. Mike Pugh says they should be, and his trusts can solve the problem:

“By putting your largest asset into a trust, you can help to reduce future probate costs, as probate’s often geared on the size and complexity of the estate.

If your house doesn’t form part of the estate, it doesn’t form part of the price analysis.”

In our view the opposite is the case: the complexity caused by MP Estate Planning’s trusts will greatly add to the cost of probate. That would be the case even if the trusts were correctly structured and drafted – but they are not. We are aware of one case where the heirs of an MP Estate Planning client had to engage a KC at great cost to resolve the difficulties MP Estate Planning had caused.

The Society of Will Writers tells its members not to make this claim:

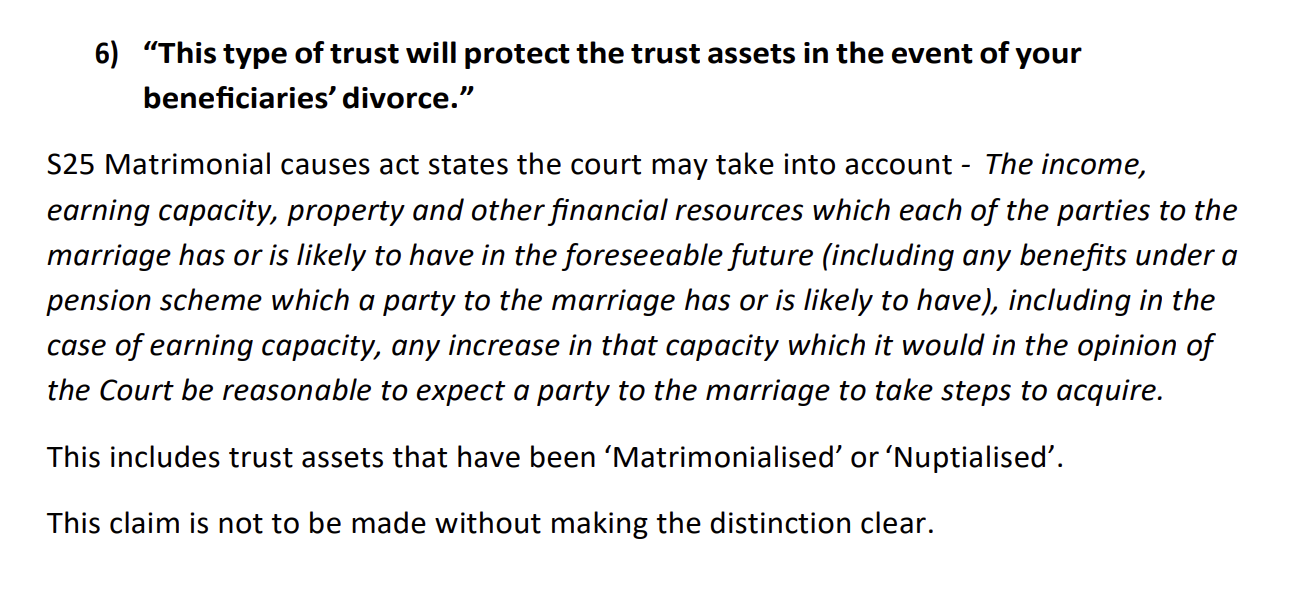

Divorce protection

MP Estate Planning heavily markets their trusts as a way that can financially support your children after you die, but if your children divorce then their spouse will have no claim on their assets:

“The divorce rate in the UK is 42%. What if your child gets a divorce? Your child’s future Mr. or Mrs. Wrong could walk out with half your life savings if your assets are not in a trust. Don’t leave money to children. Leave it to a trust. A trust will never get a divorce. A trust is the only thing we have that will make money stick to blood”.

We spoke to barristers and solicitors specialising in chancery law, family law, and nuptial agreements, and they all expected the trust would fail to achieve this.

- Divorcing spouses have been successful in arguing that an ex-spouse’s ability to benefit from a trust is a matrimonial asset (even where it’s a discretionary trust) and should be part of the divorce settlement. Courts can and do make orders reallocating trust assets.

- The decided cases have involved trusts where the trustees were genuinely independent, and beneficiaries could therefore argue that they weren’t necessarily going to have access to the trust assets. In the MP Estate Planning trusts we reviewed, the beneficiaries are also the trustees – the trusts are therefore highly vulnerable to attack in divorce proceedings. They’re simply part of the “property and other financial resources⚠️“31 of the child, and part of the “matrimonial pot” in the same way as any other asset. The arrangement achieves nothing.32

- The courts often don’t need to award trust assets to a spouse – they can simply adjust the allocation of other assets to reflect the expected value of a trust interest (although this “judicial encouragement” doctrine has limits).

The Society of Will Writers tells its members not to make this claim:

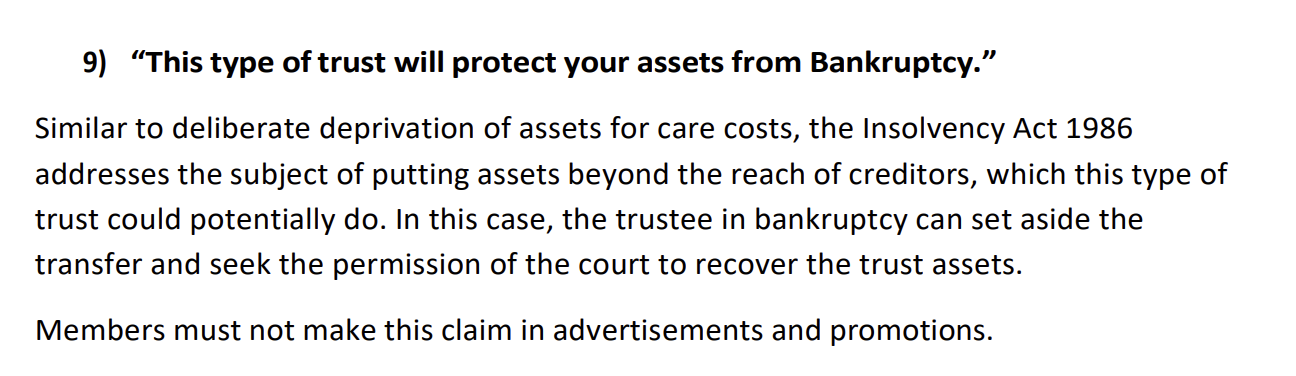

Bankruptcy protection

Mike Pugh warns elderly clients that if they’re sued, they could become homeless:

He promises that trusts will protect your estate from insolvency (as well as divorce and care home fees; more on that below):

“

So what happens if you do not set up a trust?Well, if you own anything, it can be taken from you.

If you don’t own it, it can’t be taken from you. And that’s what a trust does.

A trust removes you as the sole legal owner of an item. Therefore, you can’t lose it in a future divorce or to care fees or to taxes or litigation or bankruptcy.”

Similarly, their October 2025 proposal lists “Protection against future Bankruptcy” as one of the primary benefits of the “MP Estate Protection Plan”.

This is all variant of the “deed in the drawer” structure that’s been used for centuries. As one judge summarised it:

“The phenomenon of the “deed in the drawer” is one that is now frequently encountered. X appears to be the owner of a property, and people lend to him or otherwise deal with him on the footing that he owns it. But if X becomes bankrupt or the subject of enforcement proceedings a deed is produced which shows that in truth he holds the property upon trust for somebody else. In some cases these deeds are simply not authentic. In other cases they are authentic, but simply not noted in any public register.”

This is misleading. First, for almost all the elderly people MP Estate Planning are targeting, bankruptcy is not something they realistically should be worrying about (the bankruptcy of their children is a more reasonable concern; but that’s not the claim made in the above video).

Presenting bankruptcy as a “modern threat” is scaremongering. But if someone does go bankrupt, it is absolutely not the case that they “can’t lose” property if it’s in a trust:

- Gifts into a trust will be set aside if made within two years of your bankruptcy, or five years if you were insolvent at the time.

- A gift made at any time can be set aside if a court is satisfied that the gift was made for (amongst other things) the purpose33 of putting assets beyond the reach of a person who is making, or may at some time make, a claim against him. 34

- Given the explicit marketing claims made by MP Estate Planning, it would be difficult to argue that protecting assets from creditors was not a primary purpose of setting up the trust.

The Society of Will Writers tells its members not to make this claim:

Care home costs

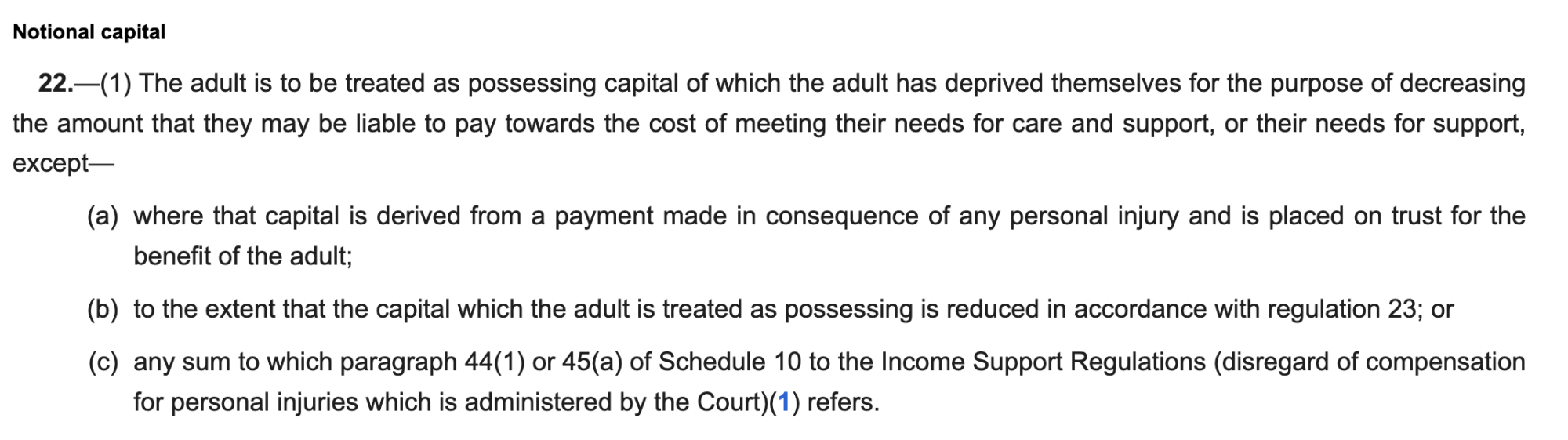

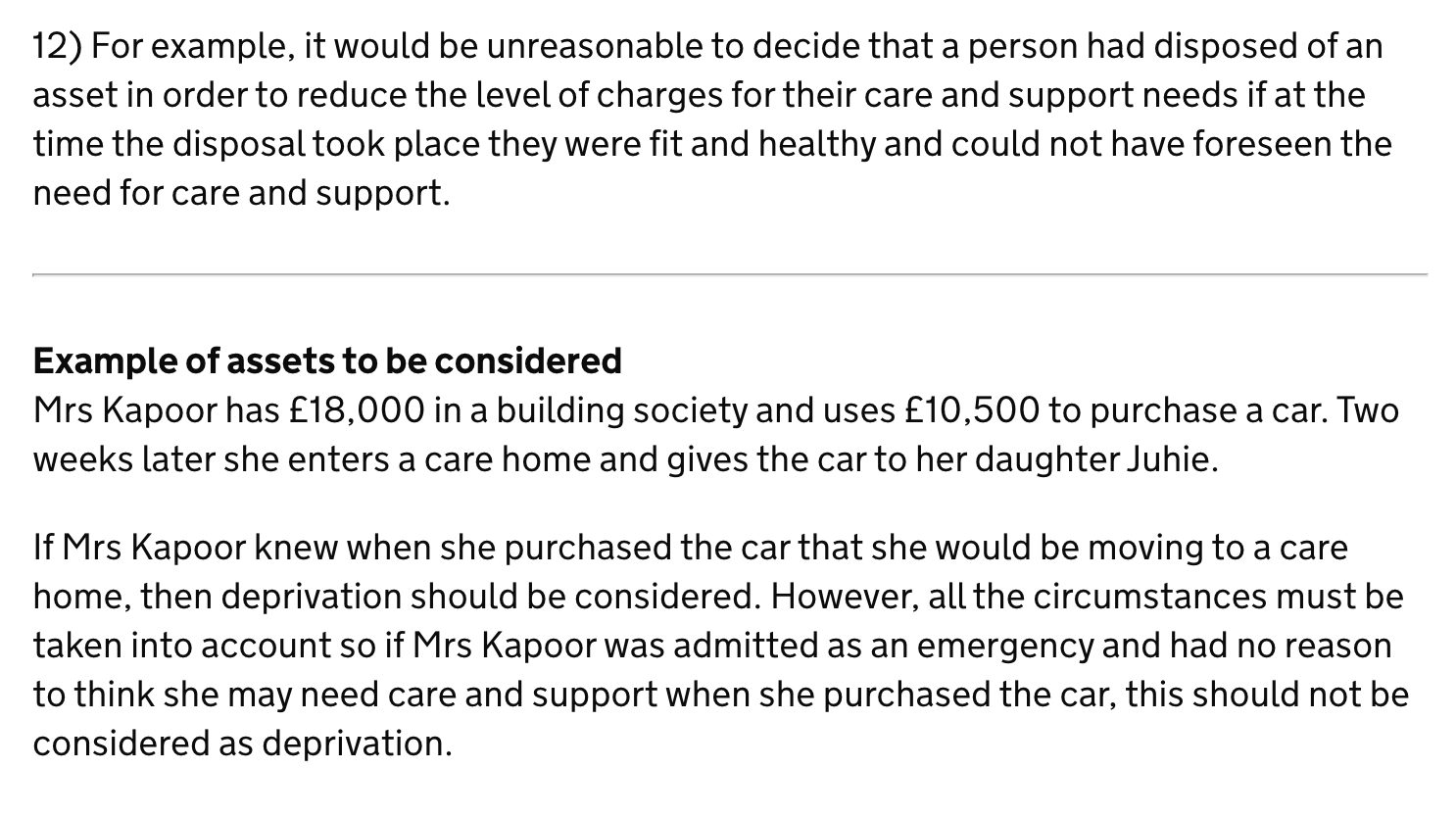

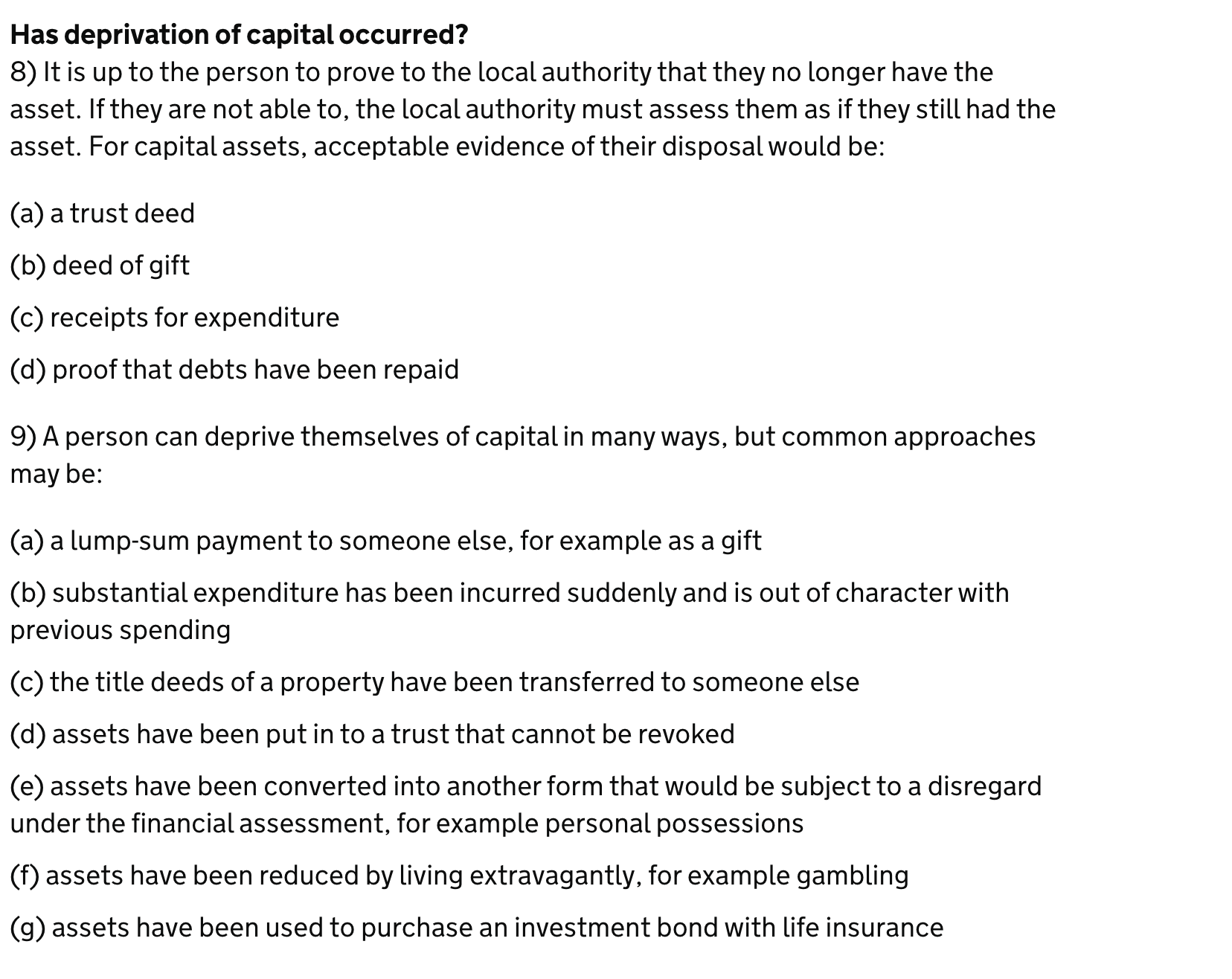

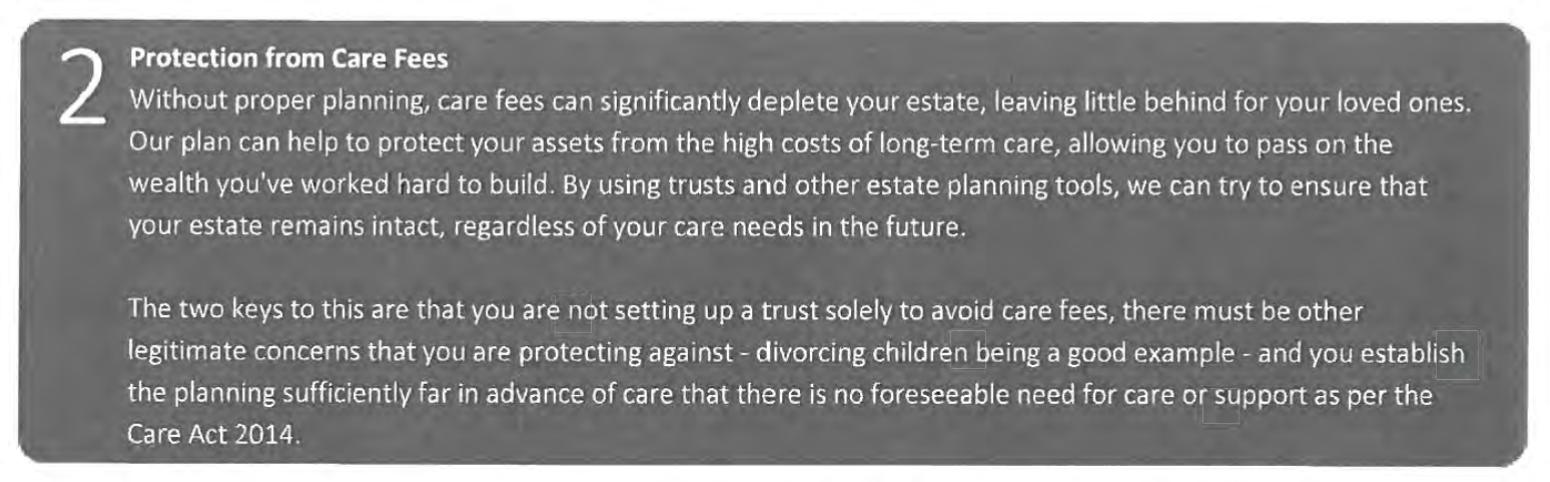

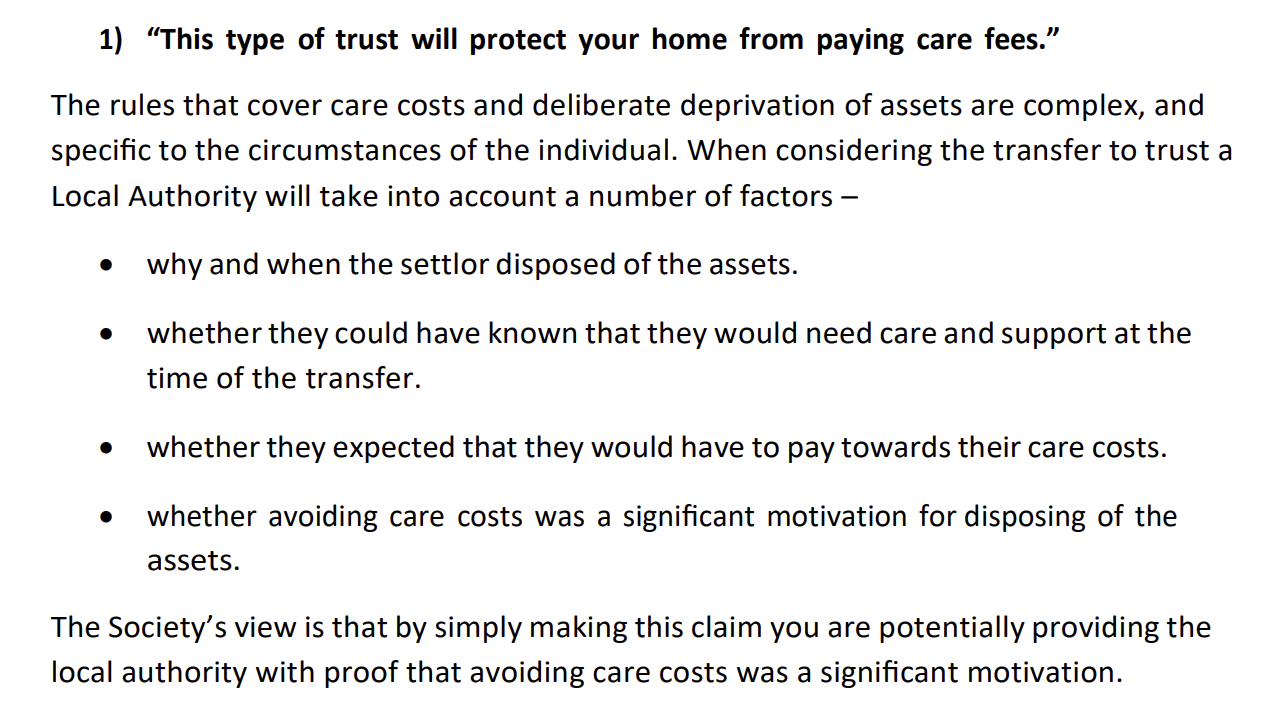

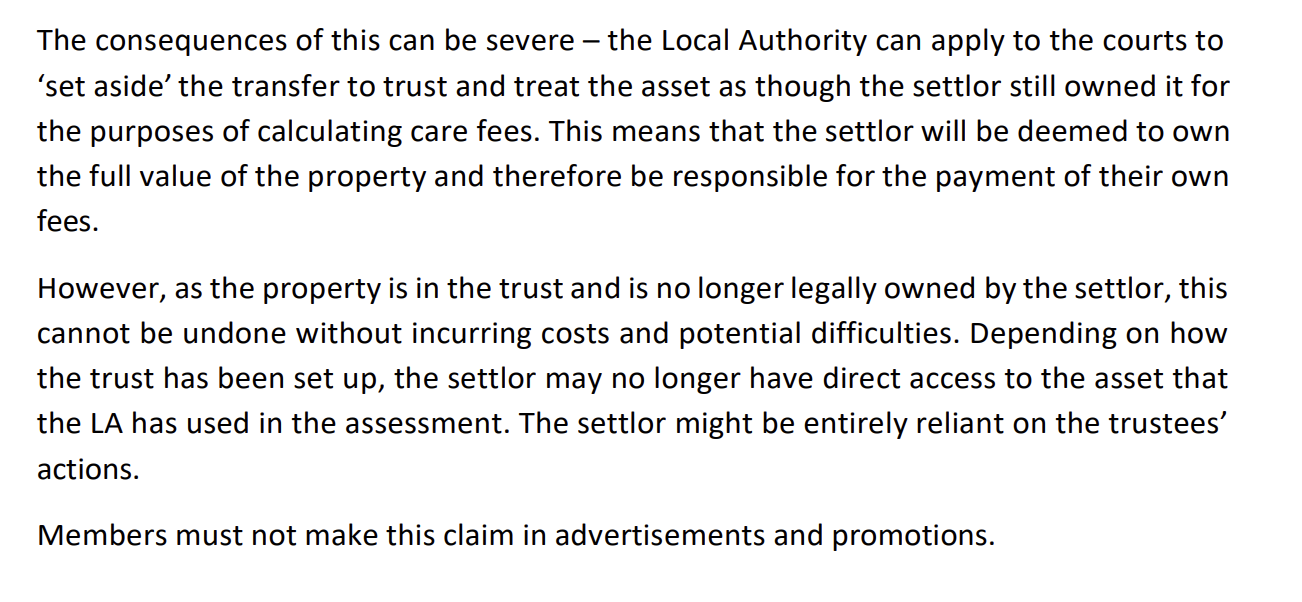

The rising cost of social care is a significant financial challenge for local authorities, and now accounts for 40% of all local authority spending. To try to control this, almost all local authorities only cover the cost of social care for people with assets of less than £23,250. It has been politically challenging to find a better solution. In the meantime, firms like MP Estate Planning market trusts as a solution to avoid having to pay for social care. The idea is to reduce your assets to below £23,250, or at least make sure your house never forms part of those assets.

There are rules in the Care Act which disregard any steps people take to avoid these rules by depriving themselves of assets. MP Estate Planning appears to have not read these rules.

In this video, Mike Pugh says people who’ve been diagnosed with a serious illness should put their property into trust, and that will stop local authorities assessing them to make a contribution if they later require long term care.

He for some reason starts talking about the Insolvency Act (which is irrelevant):

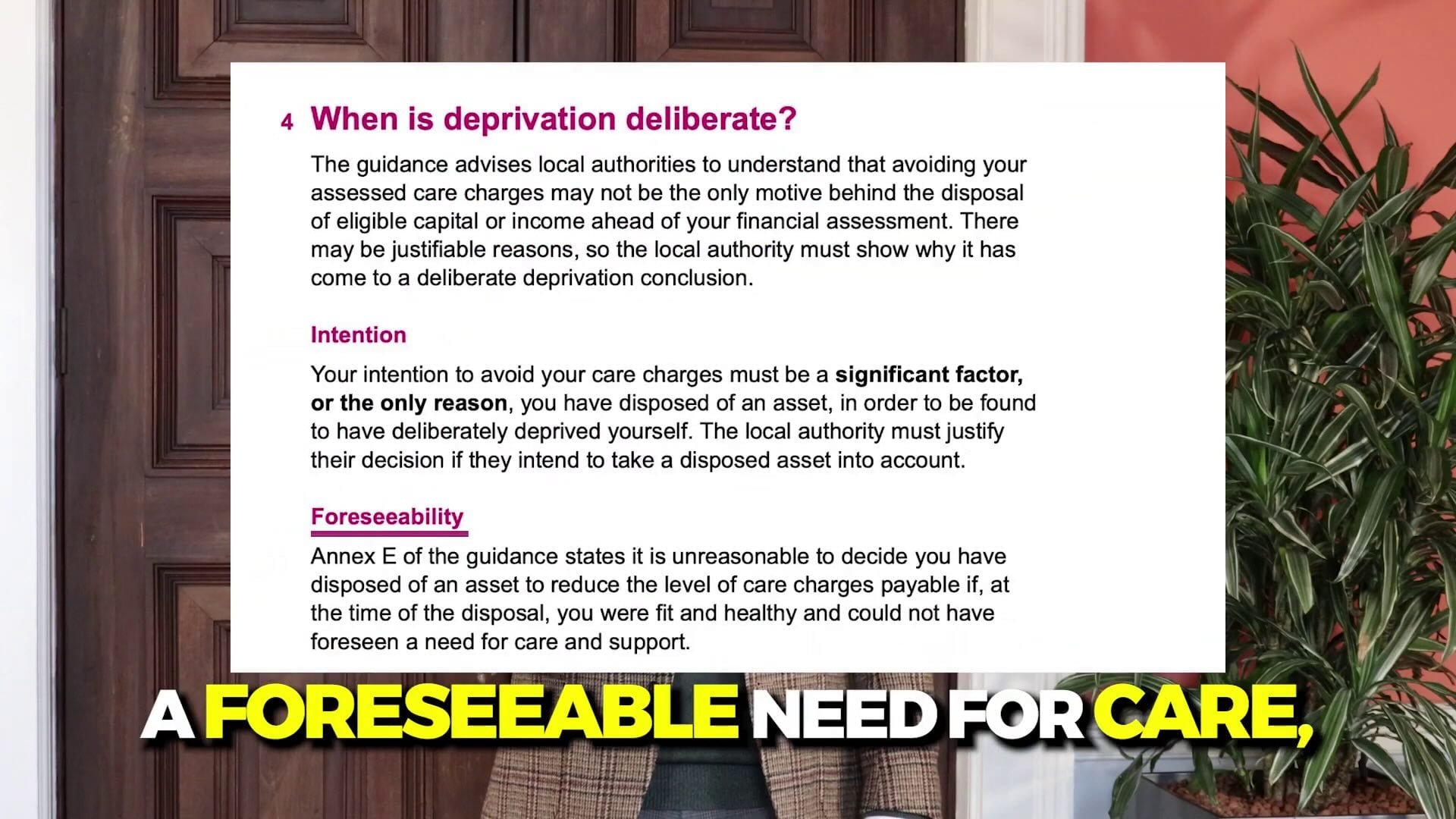

“So let’s remember that the CARE Act states that only if there’s a foreseeable need for care would you be crossing any lines…

…

Let’s clear up the misunderstandings around deliberate deprivation.

The deliberate deprivation stems from the Insolvency Act. It is criminal to try to hide assets from creditors. That’s a criminal offense.35 And so if you’re going to go bankrupt under the Insolvency Act, you’re not allowed to place assets into a trust.

Here, what we’re talking about, however, is a potential future care element. That means there are no creditors today. You don’t owe any money for care, you’re not in care, and there’s no foreseeable need for care. So that means you are welcome to place your property in the trust now.

The statute has a simple purpose test:

The statutory test is not “foreseeable”. That word is taken from the statutory guidance:

This is just making the point that foreseeability is relevant when determining what the “purpose” of a transaction was. We don’t believe the guidance anticipates a trust structure being sold specifically to avoid paying care charges. The courts in practice determine “purpose” from surrounding circumstances.36 In the view of Care Act specialists we spoke to, it would be reasonable for a local authority to decide that someone who’d bought the MP Estate Planning structure37 had “deprived themselves for the purpose of decreasing the amount that they may be liable to pay towards the cost of meeting their needs for care and support”.38 Local authorities could obtain disclosure of MP Estate Planning’s advice in order to establish this. 39

They’d be aided in this by the statutory guidance, which gives putting assets into trust as a specific example of “deprivation of assets”:

Some local authorities have expressly identified “lifetime trusts” (like those created by MP Estate Planning) as examples of asset deprivation. 40 It’s notable that the people selling these trusts are almost always unqualified and unregulated, whilst actual qualified solicitors warn against them.

It is therefore quite wrong for MP Estate Planning to confidently suggest it’s all about “foreseeability”, and ignore both the wording of the statute and the references to trusts in guidance:

In other videos, Pugh claims that putting property into trust is effective to avoid care fees if the trust is created more than two years in advance. There is no legal basis for this.

This is a particularly egregious error because the video above flashes onto the screen a clip from guidance from Age UK, which makes clear that it’s fundamentally the intention behind a disposal which is relevant:

The Society of Will Writers tells its members not to make this claim:

The trust defaults the mortgage

MP Estate Planning claim that you can put a property into trust without telling your mortgage lender. This is false. Most standard residential mortgages contain strict covenants prohibiting the borrower from transferring interests in the property (including beneficial ownership) without the lender’s express written consent.

As UK Finance told us when we investigated another trust structure in 2023:

“Transferring ownership of a property into a trust without informing your lender and seeking their consent would most likely be a breach of a mortgage’s terms and conditions.”

MP Estate Planning go further, and claim you can mortgage a property that’s already in a trust:

“The property can be taken out of the trust, mortgaged, and then put back into the trust”

This is very poor advice.

Taking the property out of trust doesn’t fix the fundamental problem that most mortgage terms prohibit transferring ownership of the property.

But it’s worse than that. There are now potentially two capital gains tax events (the trust disposing of the property to the parents, and the parents disposing of it back into the trust). If the value of the trust is over £325,000 then pulling the house out triggers an IHT exit charge. Then, when they put the house back into the trust after getting the mortgage, it triggers a new 20% IHT entry charge (on the value over £325,000). Their “simple” workaround could easily cost the client hundreds of thousands of pounds in tax every time they want to fix their mortgage rate.

Here’s a nonsensical explanation we saw from MP Estate Planning:

The “equitable value” is not a legal concept. The mortgage amount and the market value are almost always different. The lender is not the “legal owner” of the property. A real estate law specialist we spoke to concluded that whoever wrote this has no understanding of mortgages.

Incompetent advice

We have seen a series of badly drafted documents and incompetent responses from MP Estate Planning personnel:

We saw one trust where a mother was declaring a trust with her daughter as a trustee and discretionary beneficiary. The trust document listed the daughter as the settlor. When challenged on this, the adviser at MP Estate Planning didn’t appear to understand the difference between a settlor and a trustee.

An MP Estate Planning adviser did not understand that the fact value could pass back to the settlor made it a settlor-interested trust. He responded that “Any tax related matter should be dealt with by an accountant”: but no accountant was involved when they established the trust.

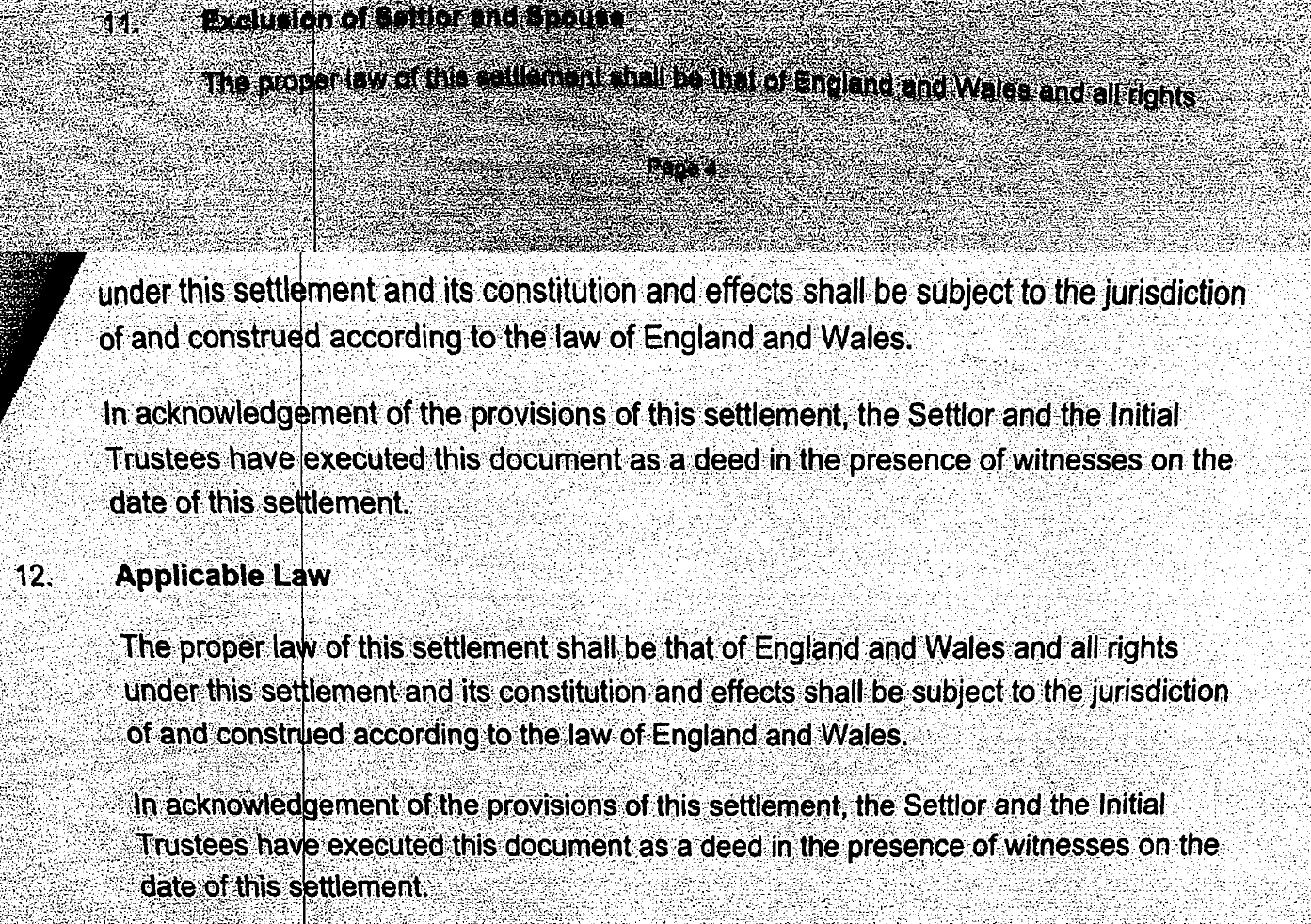

We also saw one trust deed with one of the worst drafting errors we’ve seen:

Under the “Exclusion of Settlor and Spouse” there should be a clause preventing the settlor and their spouse ever benefiting from the trust. This is necessary to prevent the settlor interested trust rules applying, causing (amongst other effects) an up-front capital gains charge. But instead someone accidentally duplicated the text of the next clause (“Applicable Law”) into “Exclusion of Settlor and Spouse”. That’s a serious error, because it means the trust likely will be a settlor interested trust.41

And, as noted above, we saw another deed where MP Estate Planning tried to create ownership as tenants in common, and failed (because they didn’t realise that requires two or more people):

It’s believed by our team that this kind of error is most likely caused by people with no legal qualifications drafting complex legal documents. Drafting trusts over land is a “reserved activity” that can only be conducted by solicitors and certain other qualified professionals – if unqualified staff are indeed drafting these documents then that’s a criminal offence.

The scale of the problem

A recent recruitment video claims that, in the first six months of 2025/26, MP Estate Planning made £1.66m in fees, with huge growth year-on-year. That implies they’ll bill at least £3m in fees this year.

![What lop Closers Want Ilo See -

Growth

A company scaling fast with verified momentum.

A market opening wider every year.

An income opportunity that compounds as we expand.

A business model where elite performers rise quickly.

This is what momentum looks like and we're still early.

Profit and Loss

MEE atare Panny ett

Dew tre wae orate WI Agee Meh

a 3] 1660 100 46 Vet 77 62 478 162 8

strong

Documented Revenue

Growth (2024 — 2026 YTD)

2023/2024: £479k

2024/2025: £1.46M (+300%)

2026 YTD: £1.66M+

(+500%)

Passed Last Year

with 6 months to go!

We NP ESTATE

*Q PLANNING UK

Reaititvwthicchie WwW

Every Home In A Trust](https://taxpolicy.org.uk/wp-content/uploads/2026/03/figures_from_recruitment_video.png)

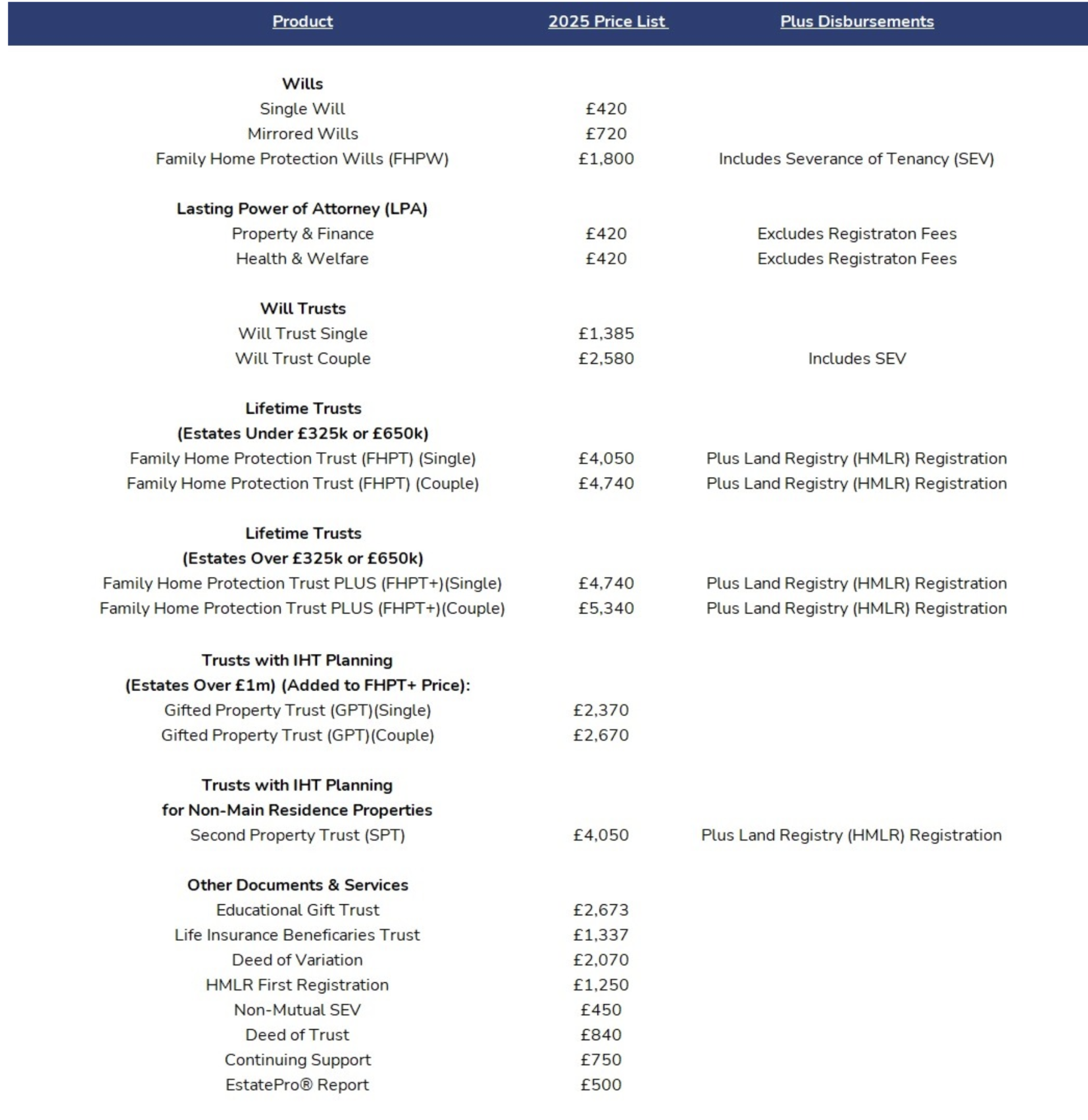

MP Estate Planning are unusual in publishing their pricing on their website:

However, most of their clients are buying multiple products, and so these prices quickly add up – we understand overall fees in the tens of thousands are common (and indeed that would be necessary for a team of this size to make £3m in revenue). Mike Pugh says:

“I do know that my competitors that offer the sophisticated high end stuff, they tend and – I’m talking Magic Circle and inside the M25 – they tend to charge either two percent of asset value or 10 percent of tax savings.

If you’re saving five million pounds, they could charge up to half a million… and I’m nowhere near the M25 – I’m in Bristol and we do not charge big city prices.

So we’re in the tens of not the hundreds of thousands.”

The claim that firms charge 2% of asset value or 10% of tax savings is, in the experience of our team, not correct. Legal/tax fees of £500,000 would be for very large estates, not people worth “mere” millions.

The response from MP Estate Planning and Mike Pugh

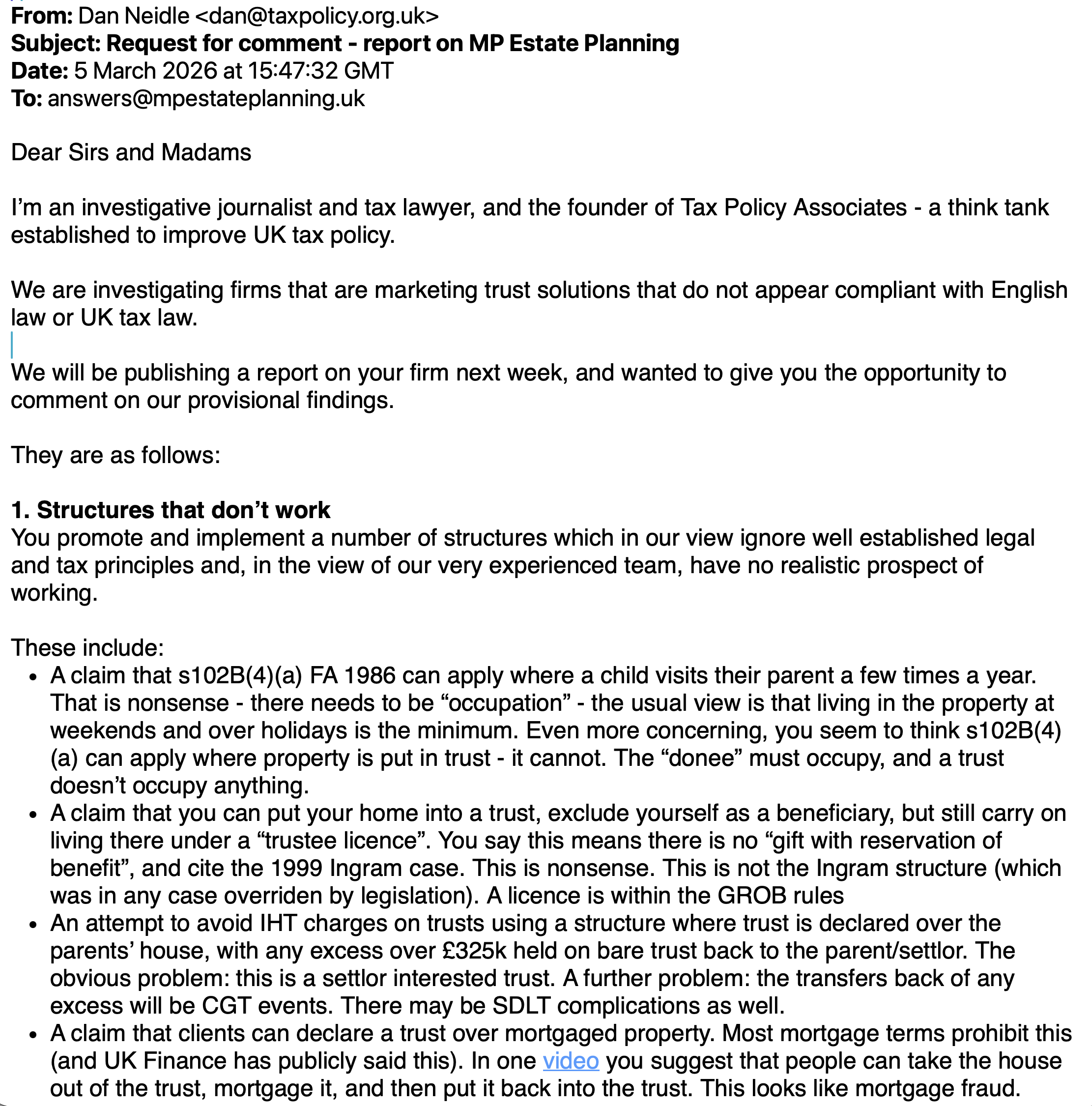

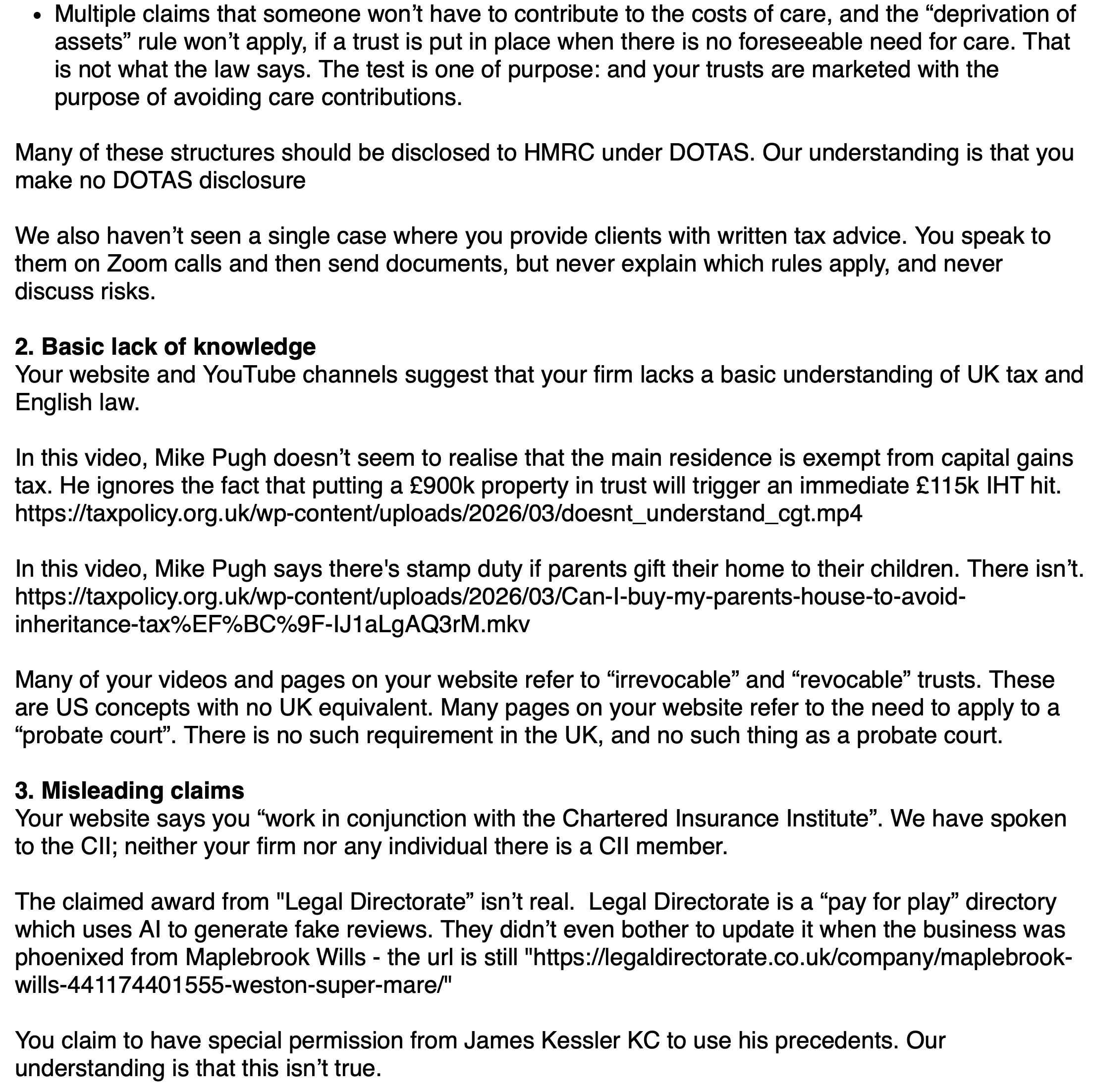

We asked MP Estate Planning to respond to the most significant points in this report:

Here’s our original email asking for comment:

And then, after MP Estate Planning acknowledged receipt:

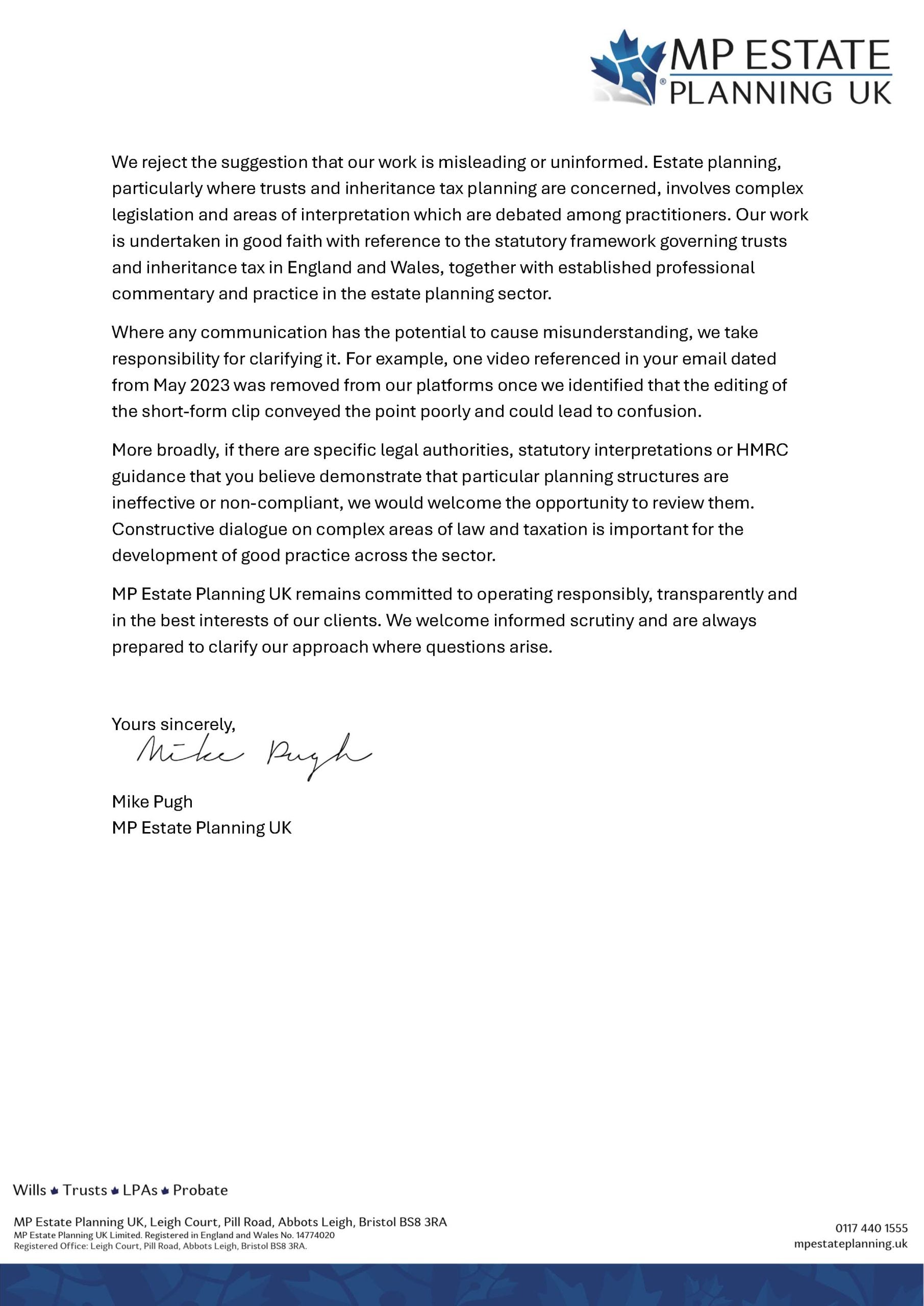

Here’s their response. It reads like a press release, and doesn’t answer a single substantive point (other than the unconvincing “editing” explanation for their May 2023 video, as noted above).

This is our response to that letter:

We received a further reply – this time with responses to the “non-existent head of legal” and “use of US terminology” points that we regard as deliberately misleading:

We gave then Mike Pugh a final chance to respond substantively:

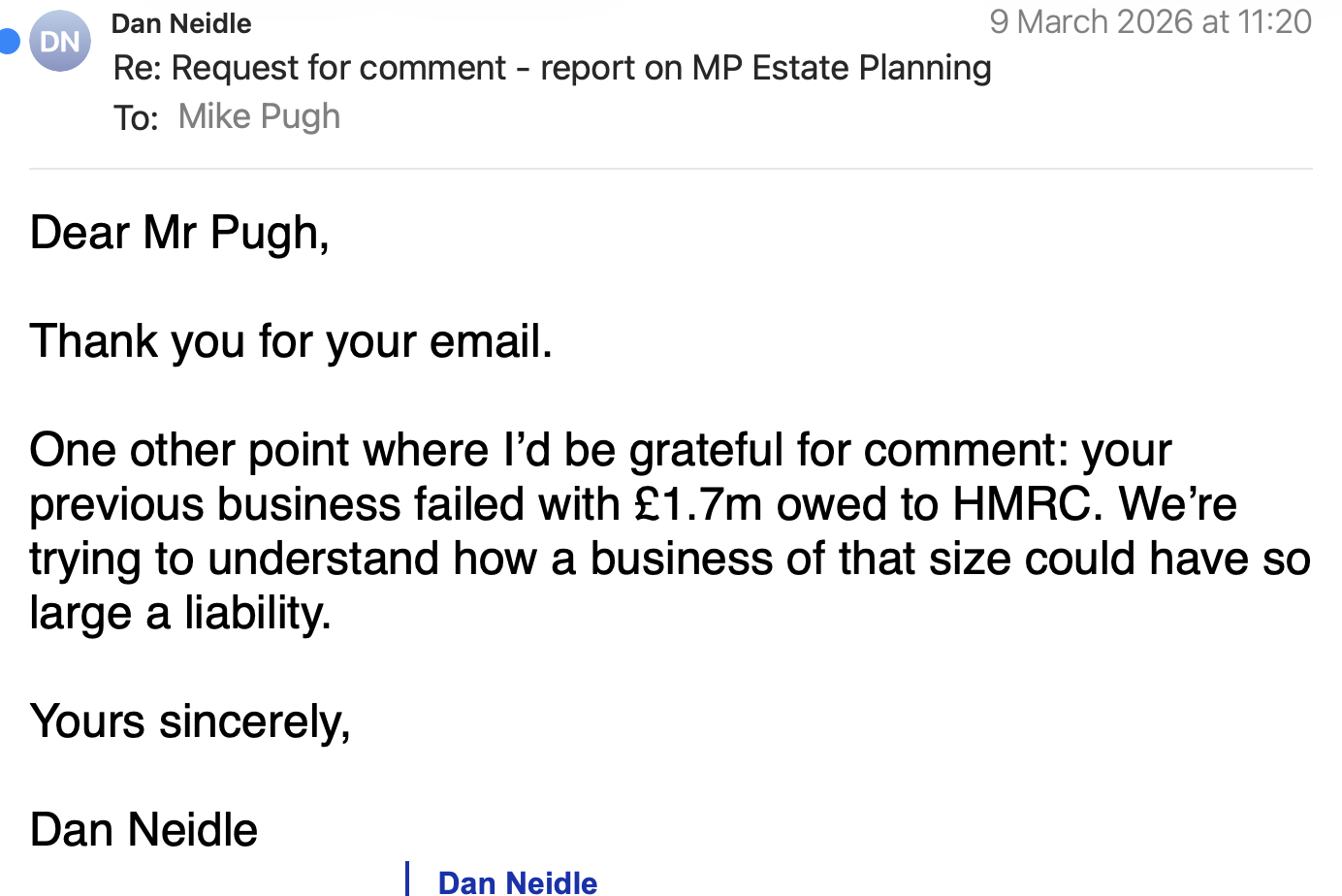

Pugh told us we’d receive a response to our technical questions: we never did. Nor did we receive an explanation as to why his previous small business went bust owing HMRC £1.7m.

Text and images © MP Estate Planning (UK) Ltd republished here for purposes of criticism and review, and in the public interest.

Many thanks to B, S1, K and I for telling us about their experiences with MP Estate Planning (UK) Ltd.

This was a particularly complex investigation which we couldn’t have undertaken without a large team of lawyers and tax specialists, all acting pro bono. This article was written thanks to:

- Inheritance tax: SH for her invaluable initial analysis, then further work from P and M and additional review from J2 and SH (again).

- Other direct tax: D and Rowan Morrow-McDade (who found the 2023 video with the nonsensical claims about main residence relief)

- Stamp duty land tax: J1 and Rowan, again.

- Real retate finance: P

- Care Act: V and Y.

- Family law: T – and thanks also to N for picking up an error post-publication.

- Insolvency law: A and I with additional review from C.

- Corporate structure and business history: M.

- Additional research and data: business intelligence provider Tech City Labs.

Plus numerous other practitioners who read through late drafts.

We usually can’t name our contributors, partly because it could be professionally awkward for their current employer, and partly because of concerns about retaliatory legal action.

Footnotes

Full name MP Estate Planning (UK) Ltd. It shouldn’t be confused with MP Estates, a reputable estate agent. ↩︎

For MP Estate Planning personnel to actually commit fraud would require them to know that they were making false claims and to be acting dishonestly; we don’t know if either is the case. It is plausible they are just reckless. ↩︎

We are reasonably sure it is the same individual. The Daniel James Irwin who was a director of Safe Hands had a date of birth May 1990. Daniel James Irwin, date of birth June 1990, is also a director of a previous Maplebrook trust entity. He has two LinkedIn accounts, neither of which are updated, and neither of which show his time at Safe Hands. ↩︎

It is reasonably clear that an untrue representation was made by Mr Pugh with the intention of making a gain, and that he knew it was untrue. The crucial legal question to determine whether an offence was committed is whether Mr Pugh was “dishonest”. Under English law, this means asking whether his conduct was dishonest by the standards of ordinary decent people (regardless of whether the individuals themselves believed at the time that they were being dishonest). The subjective element of the test for dishonesty (see Ghosh (1982)) was removed by Ivey [2017] for civil cases, and that decision was confirmed to apply to criminal cases in Barton [2020]. The fact that a defendant might plead he or she was acting in line with what others were doing, and therefore did not believe it to be dishonest, is no longer relevant if the jury finds they knew what they were doing and it was objectively dishonest. The leading textbook of criminal law and practice, Archbold, states: “In most cases the jury will need no further direction than the short two-limb test in Barton “(a) what was the defendant’s actual state of knowledge or belief as to the facts and (b) was his conduct dishonest by the standards of ordinary decent people?”. ↩︎

We don’t think any real person would write “Best will writing service and lasting power of attorney in Bristol, UK” or “MP Estate Planning offers great services and customer care when it comes to estate planning, lasting power of attorney and will planning in Bristol”. ↩︎

We refer to English law because our usual team does not have expertise in Scottish law or the law of Northern Ireland; but we are reasonably confident that Pugh’s comments are equally inapplicable to Scottish and Northern Irish law. ↩︎

There would be stamp duty if the children took over the mortgage – but MP Estate Planning appears to leave the mortgage where it is. ↩︎

The website also has about 800 “doorway pages” – pages identical apart from the location, for example “estate planning in Stevenage” – you can see the complete list here. This is a well-known strategy to capture Google searches which is widely seen as abusive and misleading (“Based on our 18 years of experience providing inheritance tax advice in London…” or “Do You Need 24 Hour Emergency Estate Planning Services in Litton?“). The figures in the main text for the number of articles and words exclude these “doorway pages”. ↩︎

Tech City Labs kindly provided us with the report pro bono and has authorised us to publish it here. ↩︎

The trusts discussed here are discretionary trusts and settlements – the kinds of trust MP Estate Planning sells. The most common kind of trust is a “bare trust” or nominee arrangement – those arise all the time by operation of law in many ordinary personal and business contexts, and don’t normally have tax consequences. ↩︎

The lifetime rate of IHT is 20% but in practice, and especially where the trustees only hold assets not cash, the effective rate is normally “grossed up” to 25% as it’s the donor rather than the trustees that pay the tax. ↩︎

Plus an exit charge on any part-ten year period when/if the trust comes to an end. ↩︎

With complex rules that often, but not always, avoid double taxation. ↩︎

20% of £650,000 minus the £325,000 nil rate band. ↩︎

The RNB is £175,000 for her plus £100,000 from her late husband, who died in 1984. ↩︎

As we say in the introduction, for MP Estate Planning personnel to actually commit fraud would require them to know that they were making false claims and to be acting dishonestly; we don’t know if either is the case. ↩︎

After seven years another £325k nil rate band becomes available, but for the first seven years this structure is all downside. ↩︎

When is the valuation tested? Is it tested daily? Annually? Upon a specific triggering event? The deed is entirely silent. How is a valuation determined? Again – nothing. And how does “Fund B” Work? It’s not clear it can be a “bare trust” because under Saunders v Vautier, the beneficiary (the Settlor) would be entitled to call for the trust property – but here that can’t happen because the trustees are holding for both the bare trust and the discretionary trust. However the intention is clear enough that the trust lawyers we spoke to thought that the trust would likely be given effect, notwithstanding the very unclear mechanics. ↩︎

Ordinarily, transferring assets into a relevant property trust allows for capital gains tax to be held over under section 260 of the Taxation of Chargeable Gains Act 1992. However, section 169F specifically denies this relief for settlor-interested trusts. ↩︎

A gift to a trust is not usually subject to stamp duty land tax, because there is no consideration. However this is not a gift – the parent/settlor is getting something back – the right to receive all value over £325k. We’ve considered whether that gives rise to an SDLT charge, either on day one or subsequently – our conclusion is that it probably doesn’t (but it’s a complex question and we haven’t undertaken a full analysis). ↩︎

Patrick Soares says he believes the section applies if a child “treats [the property] has his home, is physically present there most weekends and for some holidays, has an earmarked bedroom and study, keeps some of his possessions there and has the keys to come and go as he pleases, and he is not just a guest or temporary visitor”. Emma Chamberlain takes a slightly more cautious view, saying that there must be substantive occupation even if not as a main home. These seem defensible readings to us – “occupy” clearly means actual physical presence but it doesn’t necessarily mean full time occupation. There is some risk in the Soares/Chamberlain approach, and we can’t exclude HMRC challenging such an arrangement on the basis that, for two people to “occupy” a property, their presence must be of similar (but not identical) intensity (which seems to have been the intention of the Government that enacted the rule). Other advisers take a more cautious view. ↩︎

There is no caselaw on this point. There are, however, non-tax authorities on the meaning of “occupy”; they illustrate the (obvious) point that it requires an actual presence, not just the potential for a presence. In this case we feel the purpose of the taxing statute (as elucidated by the Dawn Primarolo statement) puts the point beyond reasonable doubt. ↩︎

The Soares and Chamberlain articles have been widely read, and their approach has been adapted by some firms into a much less rigorous approach that we suspect Soares and Chamberlain would disagree with. For example, Countrywide says “The test is likely to be satisfied where, for instance, there is a gift of a share of the main residence to a child who visits the property on a regular basis, is able to come and go as they please, have their own key and leaves their possessions at the property. There does of course need to be more than mere storage of items at the property and so an occupier having their own bedroom and being able to come and go as they please would certainly make the test easier to satisfy”. This may be over-reading HMRC guidance on occupation in the context of the pre-owned assets rules – HMRC has an obvious incentive to give the term a wide meaning here, but HMRC guidance is not legislation and in practice cannot be relied upon by taxpayers. ↩︎

There are other more sophisticated structures involving s102B, and it has been suggested the GAAR could apply to them (see page 20 of this expanded version of the Patrick Soares article), but we don’t think the GAAR would be necessary to the MP Estate Planning structure. ↩︎

Even if MP Estate Planning’s “loopholes” did work to avoid the gift with reservation rules (they don’t), there is a separate anti-avoidance regime that can still impose an ongoing tax charge: the pre-owned assets tax (POAT). POAT was introduced to counter arrangements where someone successfully removes an asset (typically a home) from their estate for inheritance tax purposes, but continues to enjoy it. It is a standalone income tax charge on the benefit of continued occupation/use of an asset you previously owned or funded. The rules are complex but, given MP Estate Planning’s trusts fail to avoid the gift with reservation rules, we won’t go into them further. ↩︎

Sch 20 para 6(1)(a) says the donor’s continued “actual occupation of the land … shall be disregarded if it is for full consideration in money or money’s worth”. This is the statutory basis for the “pay market rent” approach. ↩︎

Ingram involved a “lease carve‑out” scheme: the homeowner created and kept a proprietary lease (so they had a real property right to stay), and only then gave away the freehold. Later legislation severely restricted that approach. Subsequent attempts to find similar work-arounds have failed. ↩︎

We think it probably isn’t disclosable under DOTAS because it is in sense “too simple”: there’s nothing contrived about it. It is however possible that the “premium fee” hallmark applies as a factual matter. ↩︎

Although less than three years may trigger a charge under the unrelated provision in paragraph 17A Schedule 15 Finance Act 2003. ↩︎

There seems to be a common view amongst some unregulated advisers that it’s safe to form a partnership, wait three years, and then incorporate. There is no such limitation on section 75A in the legislation or any HMRC guidance – the sole question is whether partnership and incorporation are, together, “scheme transactions”. Where a partnership is established as a step towards incorporation, then in our view there probably would be “scheme transactions”. That is particularly the case when there is no rationale other than tax to establish the partnership (and it’s hard to see what other rationale there could be). ↩︎

The courts have found trusts to be “other financial resources” in numerous cases of “real” trusts where the settlor influences the trustees, but does not have complete control. The test in Charman v. Charman [2006] 1 WLR 1053 is “whether, if the husband were to request [the trustee]to advance the whole (or part) of the capital of the trust to him, the trustee would be likely to do so”. ↩︎

Note we previously referred to section 37 of the Matrimonial Causes Act – that’s not relevant here where a parent is the settlor. Many thanks to N for pointing this out, and our apologies for getting this wrong. ↩︎

Such an improper purpose will exist even if there are other purposes, such as tax avoidance. ↩︎

The Lemos judgment provides a useful example of how the courts apply section 423 in practice. ↩︎

In addition to incorrectly citing the Insolvency Act, Pugh also incorrectly claims this is a “criminal offense”. In the UK, transferring assets to put them beyond the reach of creditors is typically a civil matter leading to the transaction being set aside under section 423 of the Insolvency Act 1986. While there are some specific bankruptcy offences if a person is already bankrupt, merely putting assets into a trust to avoid future creditors is legally ineffective, but not generally a criminal offence in itself. ↩︎

See also the Local Government and Social Care Ombudsman’s approach to deprivation of capital cases. ↩︎

As is often the case with tax planning, this means that MP Estate Planning’s own marketing undermines the effectiveness of their product. Someone who obtains advice from MP Estate Planning and then creates a trust could well be in a worse position than someone who creates a trust themselves, or using some other adviser who doesn’t use care home fees as a selling point. ↩︎