![THE HON. MRS JUSTICE COLLINS RICE DBE CB

Approved Judgment

Kamal v Tax Policy Associates

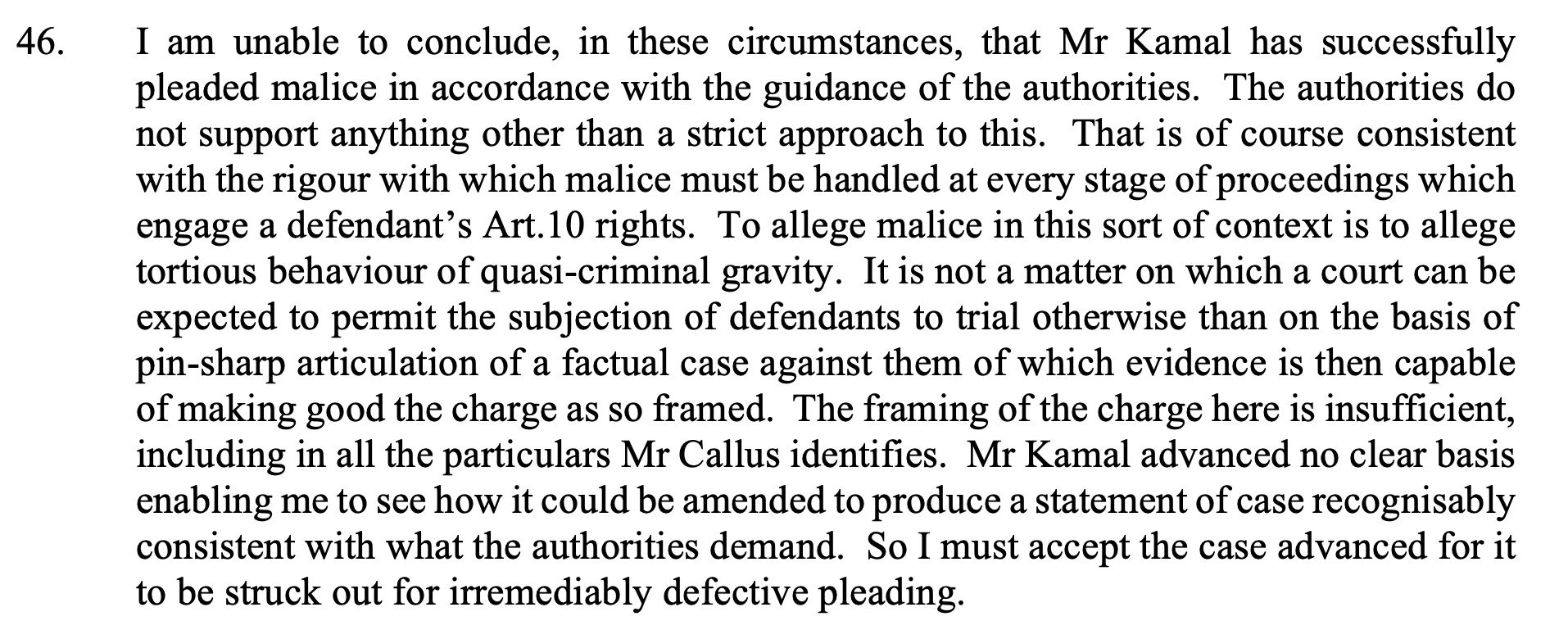

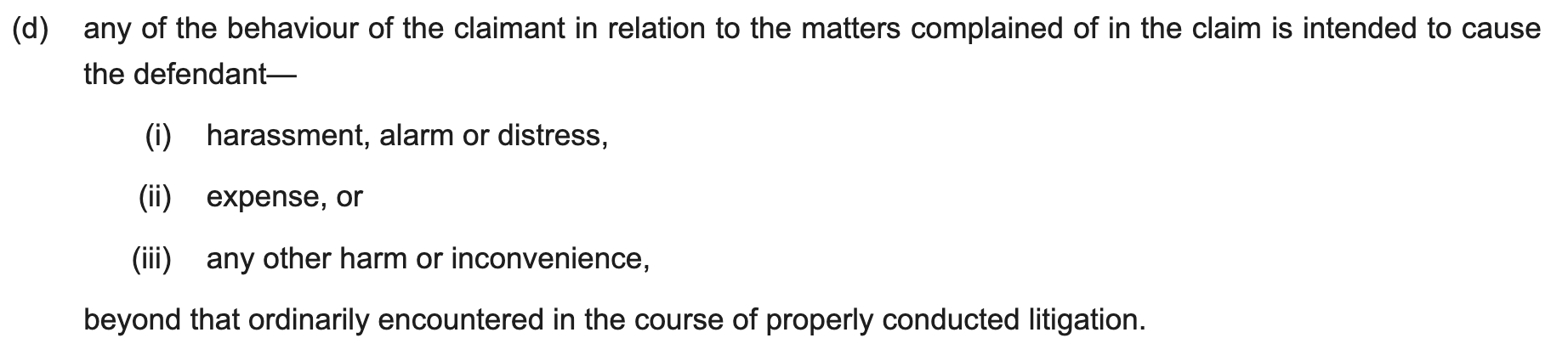

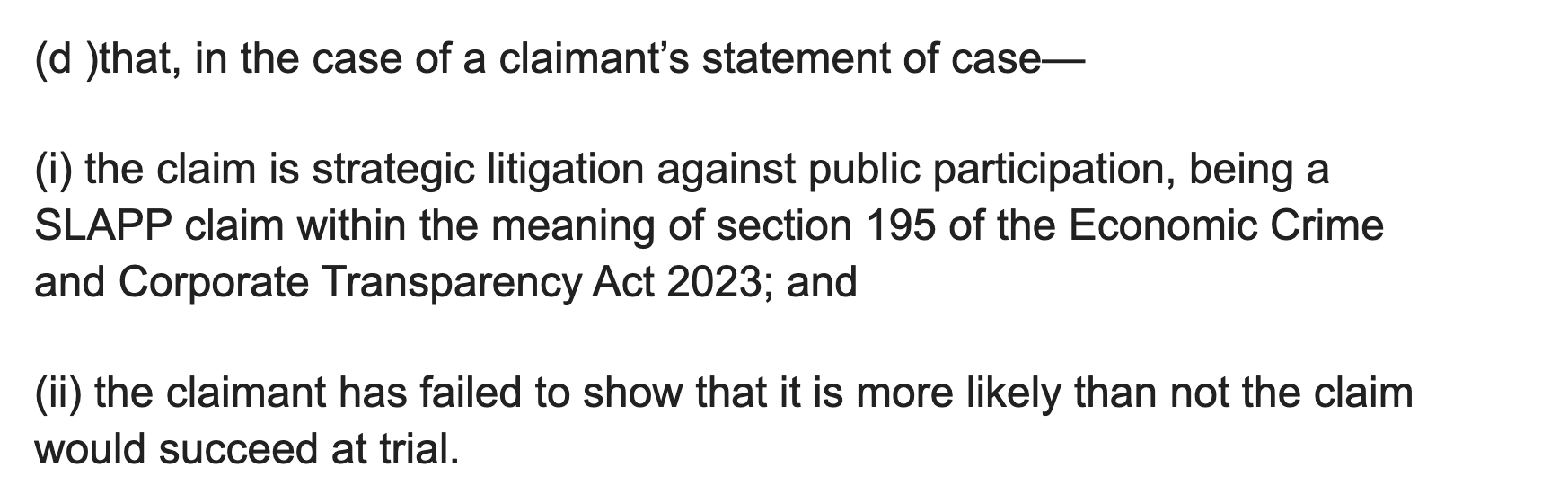

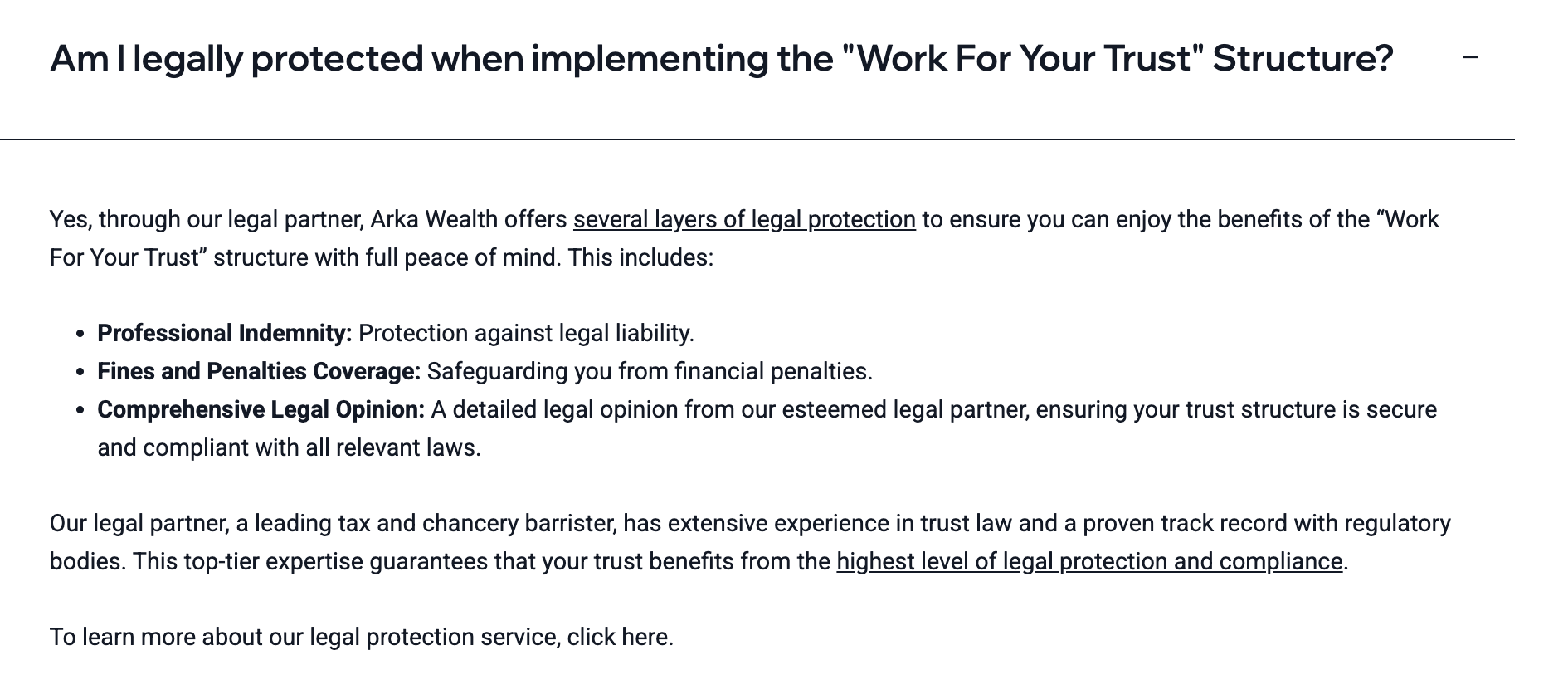

31. In the circumstances, the pleading that it was ‘false and misleading’ to suggest that a

judicial finding of breach of duty had been made against him is incapable of forming a

part of the just disposal of Mr Kamal’s libel claim. The attempt to do so is an abuse of

the court’s processes. I grant the Defendant’s application to strike out [5(b)] of Mr

Kamal’s particulars of claim.](https://taxpolicy.org.uk/wp-content/uploads/2026/03/padded_judgment.jpg)

In February 2025, we published a report about a firm called Arka Wealth.1 They’d published hundreds of TikTok videos promoting a scheme that claimed to eliminate all corporate tax, income tax, capital gains tax and inheritance tax – not just in the UK but across Europe. An unbelievable claim, and all the tax advisers I spoke to – in the UK and across Europe – said the scheme was technically without merit. Many thought it could amount to fraud. But the really surprising part was that the firm was backed by a tax barrister, Setu Kamal, who said in a YouTube video he provided an opinion to all of Arka Wealth’s clients.

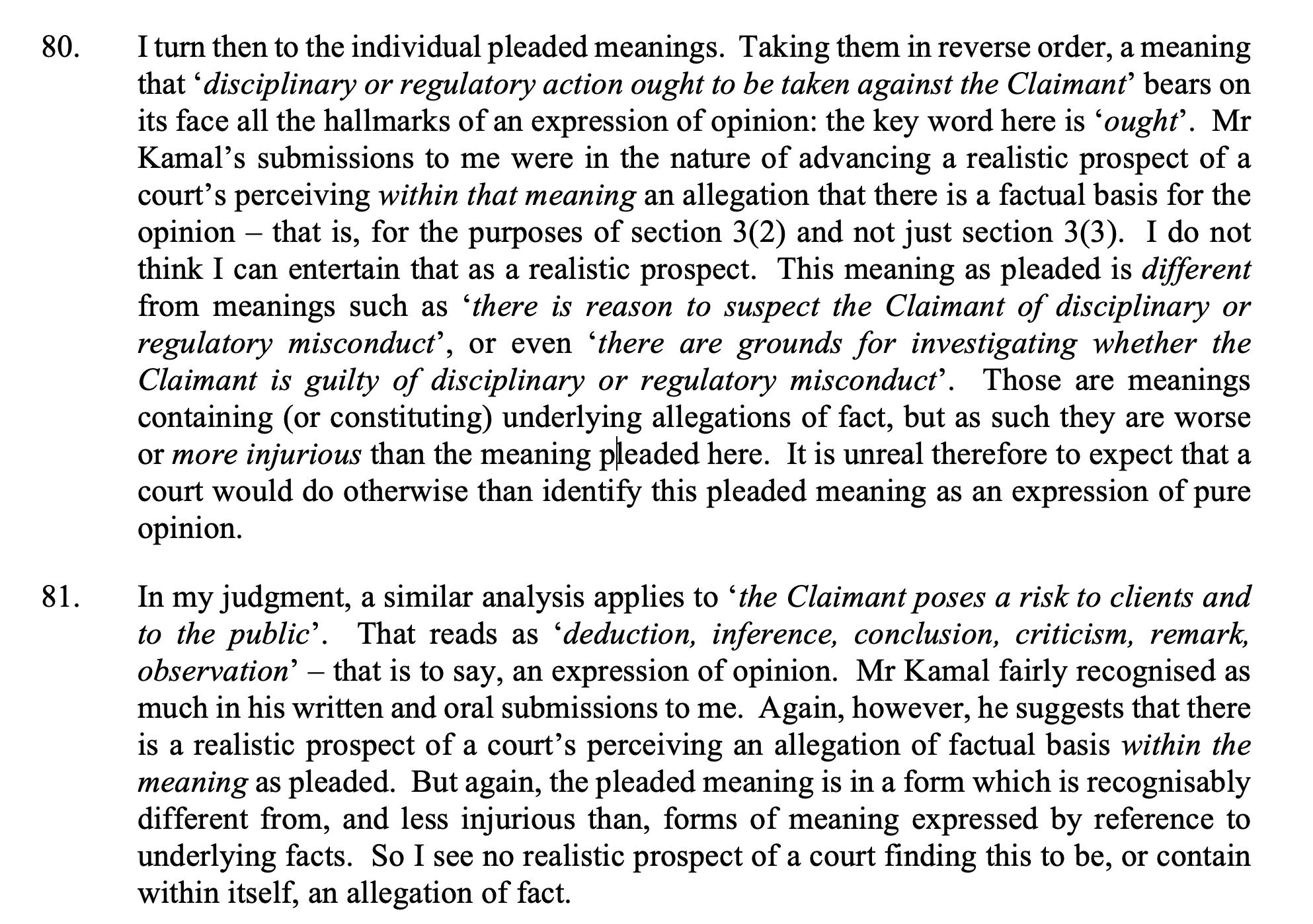

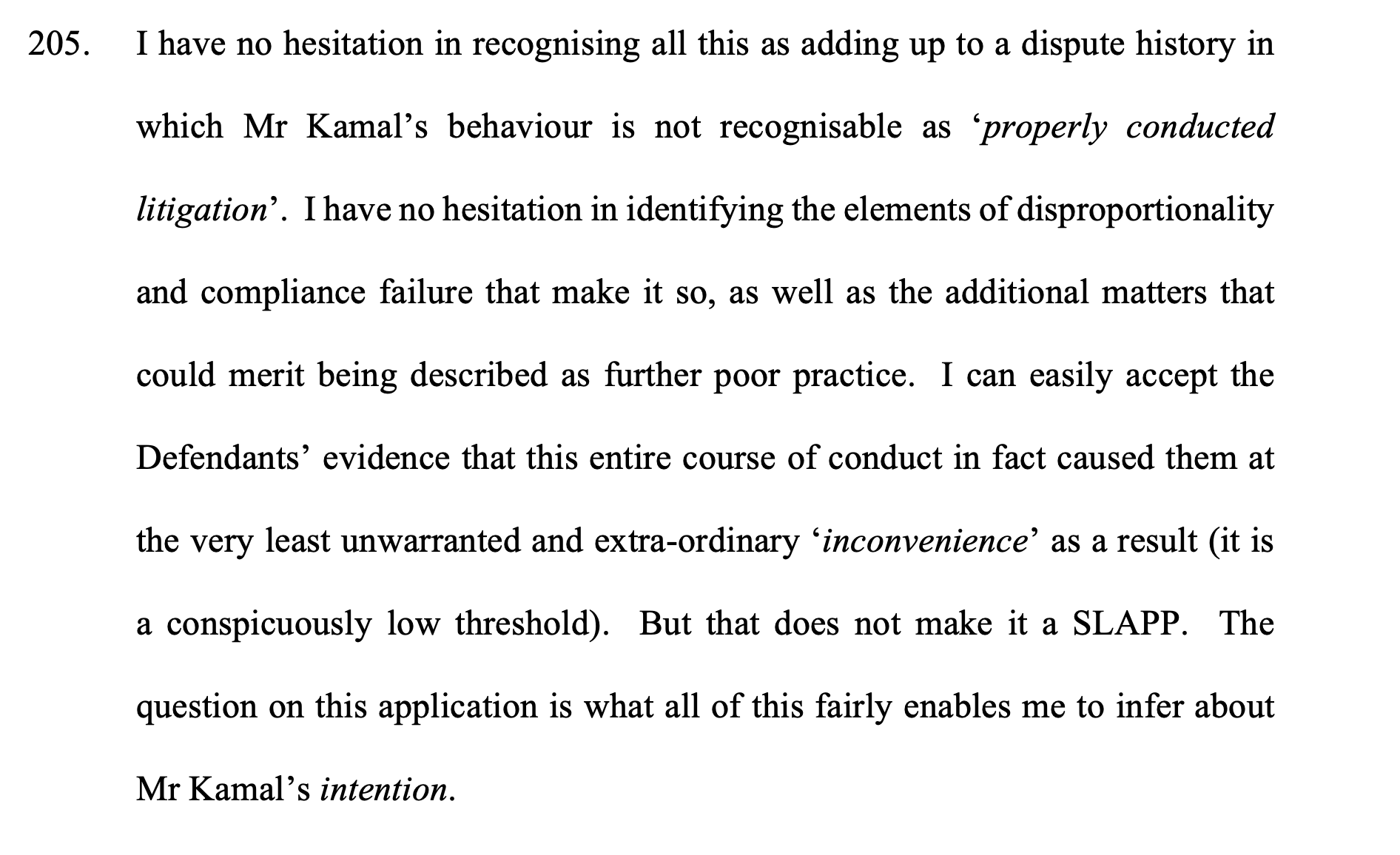

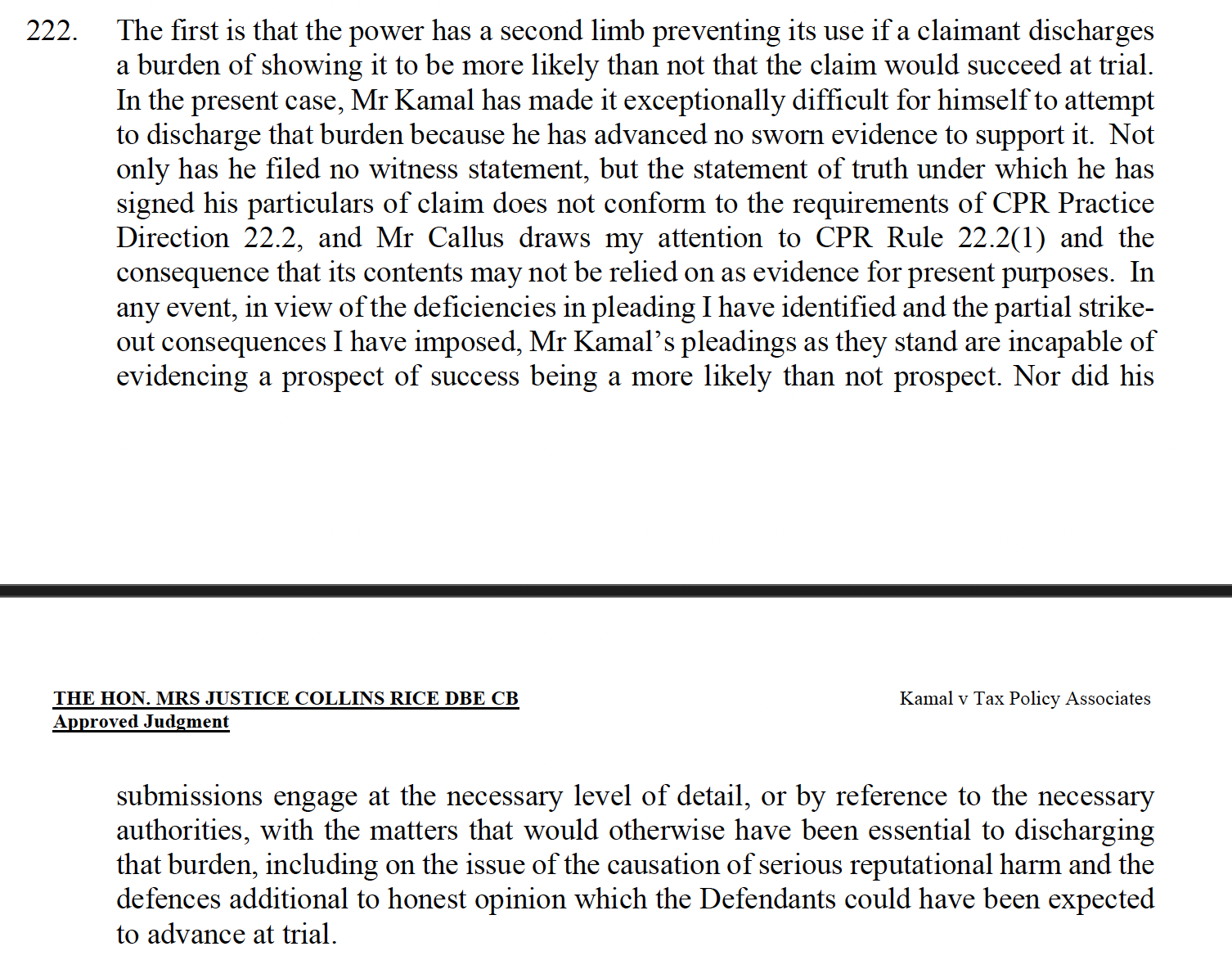

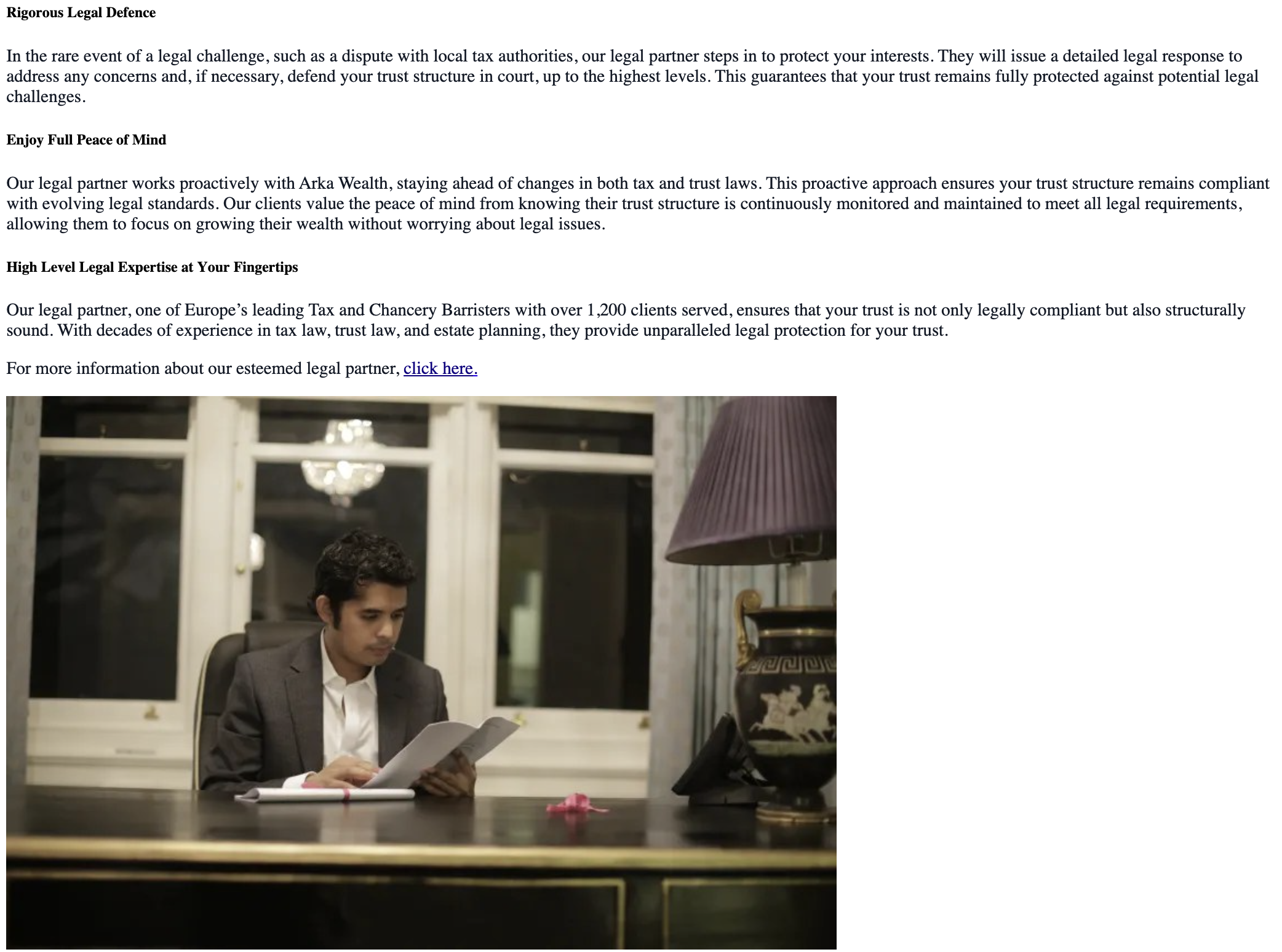

Kamal declined to comment on our article, either before publication or immediately afterwards. Months later, he threatened defamation proceedings unless we removed the article, although he was never very specific about what, precisely, his complaint was. He then sent me an email demanding that I pay him 80% of the amount his clients claimed he’d lost in fees, and that I publicly state my “sincere belief” that he is “the leading barrister in the field of taxation in the country”:

![In light of the reputational harm caused, which easily passes the threshold of “serious harm” under Lachaux v

Independent Print Ltd [2019] UKSC 27, | require the following steps to be taken within 7 days:

1. Publication of a clear and public confirmation of your sincere belief that | am the leading barrister in the

field of taxation in the country, as previously stated, and a sincere apology for your misleading and disparaging

remarks;

2. Retraction or substantial amendment of the headline and body of the article so as to remove the defamatory

implications it currently conveys;

3. Publication in full of my letter to the Information Commissioner, together with acknowledgment of the

outcome of the BSB investigation;

4. Written confirmation that you shall apply higher editorial standards in the future, and that no further false or

misleading references to any persons will be made in your publications;

5. Undertaking to make the following payment: you shall undertake to pay 80% of any amounts which my

regular or historic clients represent to you, in writing, as amounts they would have paid to me under an

engagement with me, but did not do so because of your publications.

Should you fail to take these steps, | will proceed without further notice to pursue all remedies available to me,

including injunctive relief, damages, and costs.](https://taxpolicy.org.uk/wp-content/uploads/2026/03/image-32-2000x994.png)

There was then a strange episode in August when Kamal tried to obtain an interim injunction against me and Tax Policy Associates but, in a serious breach of court procedure, failed to give us notice of his injunction application. Fortunately the Court rejected the application out of hand. I wrote about that here.

Soon after that, Kamal commenced an £8m defamation claim – again against me and Tax Policy Associates.

We had two responses. The first was traditional: we applied to the court to strike out the parts of the claim that were technically hopeless, and sought summary judgment on the rest. The second was novel: we were the first defendants to rely on the new anti-SLAPP rules in the Economic Crime and Corporate Transparency Act 2023. I wrote about that here, including Kamal’s court papers and our strike-out application.

The Court issued its judgment today. We won on all grounds. Part of the claim was struck out, and we obtained summary judgment on the rest. The court also held that the case was a SLAPP – had any part of the claim survived the earlier rulings, it would have been struck out on that basis alone.

The judgment is here (or, if you prefer, in Word format here):

Thanks to my brilliant legal team: Matthew Gill and Charlotte Teasdale at the Good Law Project, and to our counsel, Greg Callus and Hannah Gilliland from 5RB. And thanks to the team who initially wrote the report, and everyone who supported us since – particularly Nik Williams, Index on Censorship and the UK Anti-SLAPP Coalition.

In this report:

Libel law chills free speech

First, this demonstrates the two big truths about English libel law.

- Substantive libel law is fairly sensible, and a journalist who writes something that is true and/or opinion should expect to prevail in court.2

- The procedural aspects of a libel claim chill free speech.

Kamal’s claim was hopeless, elements of it were downright abusive (and intentionally so), and his conduct of the claim was incompetent. In other circumstances it would be met with ridicule – but the sum he claimed was so large that I had to take it seriously. It took six months, costs of about £146k, and an 85-page judgment, for me to have the claim dismissed.

For someone without my legal training or financial resources, it would be irrational to have fought Kamal. The rational thing to do would have been to give in, and delete the report. That’s why most libel threats succeed, and we never hear about them: a lawyer’s letter is sent, and the blogger or journalist quietly backs off. That’s a catastrophe for freedom of speech.

But it’s worse than that – it would have been irrational for a national newspaper to carry the story, because it was too niche to justify the editorial time and cost that a libel lawsuit carries. I have nothing but respect for the newspapers that do fight huge libel claims – but they have to pick their fights, and that means small but important stories get missed.

This is the chilling effect of libel law. No other area of litigation has libel law’s potential to damage public life. Libel law enabled Jimmy Savile, Robert Maxwell, Cyril Smith, and many other monsters (note that I’m too cowardly to mention the still-living examples). Rules that are rational in commercial litigation become actively dangerous when they can be weaponised to silence critics of wrongdoing. And so it’s right that we should treat libel law, and other laws3 that SLAPPers are abusing, differently from other litigation.

That means dramatically changing the cost equation for defendants. The SLAPP strike-out goes a little in that direction, but even in my case – just about the most favourable imaginable – the cost equation was still brutal. More radical reform is required:

- Make it much harder to bring claims. Right now, you can bring a libel claim without any evidence that a journalist said something false. The journalist has to prove truth (or opinion, or another defence). We should put the onus on claimants: require claimants to prove falsity, and that the publication wasn’t an opinion and wasn’t in the public interest.

- Go further: introduce an American-style requirement to prove malice when the claimant is a public figure.

- Give defendants assurance that, if they win, their costs will be covered. Make indemnity costs the default position.

- Introduce sanctions against claimants who knowingly or recklessly make untrue statements in the course of pursuing a libel claim (whether they ultimately win or lose the claim).

- Or go even further: take defamation out of the court and into informal “alternative dispute resolution” – faster, cheaper, and with no prize for the winner except a declaration that the article was false.

The Tax Bar enables abusive tax schemes

We published a report recently concluding that a small number of barristers were enabling abusive tax avoidance schemes which very possibly could be viewed as fraud, because nobody involved could seriously think the schemes had any prospect of success, and all the companies involved were liquidated as soon as HMRC started investigating.

We now have further evidence of this.

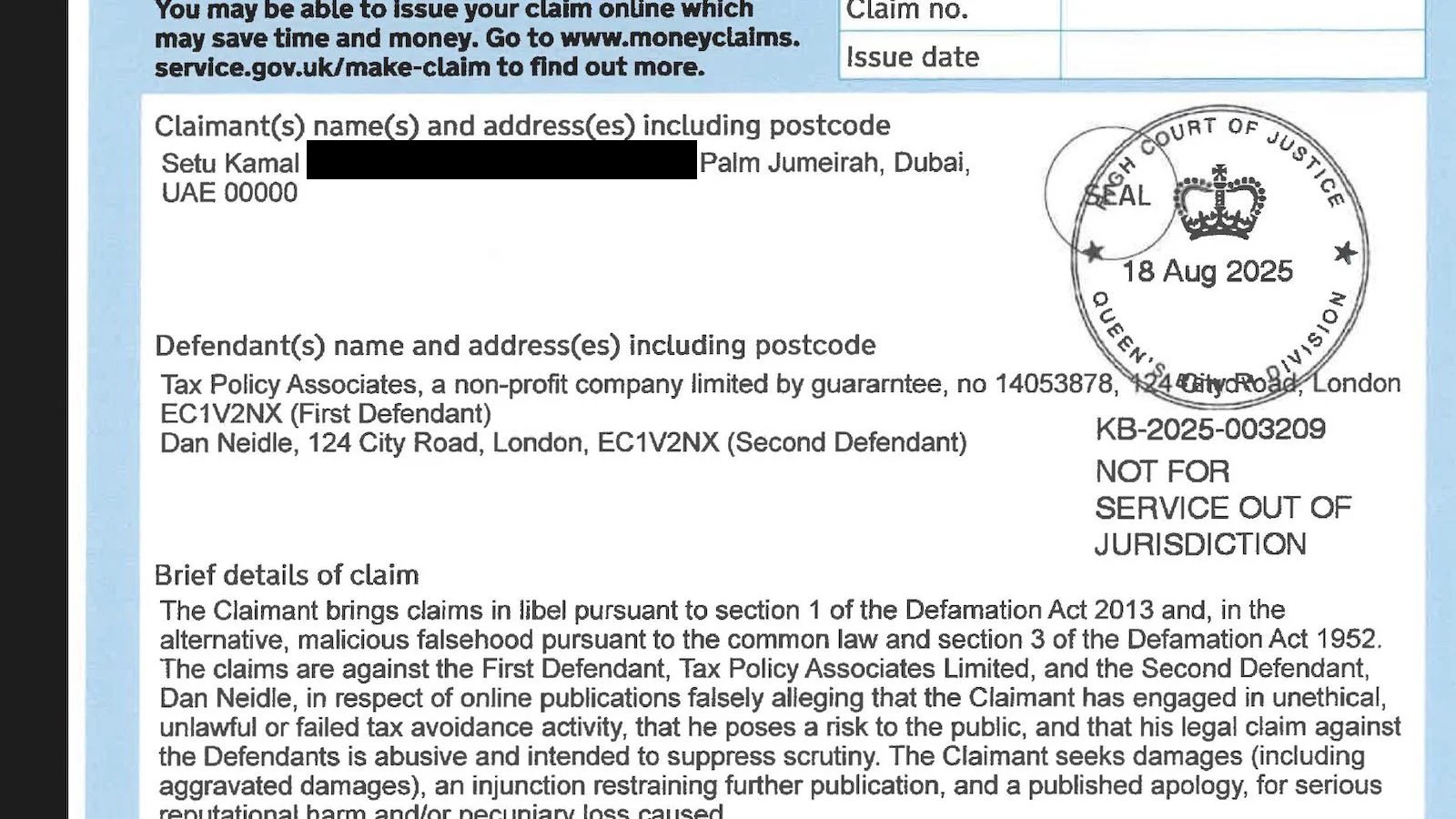

Kamal was claiming £8m in damages because he said he’d had a contract that was worth £8m, which he’d lost as a result of our article. My lawyers, Matt and Charlotte, realised something I’d missed – we were now entitled to ask for a copy of the contract. We received it just a few days before trial.

As the contract was referred to in court, I can now publish it in full:

The document has several extraordinary features:

- Kamal had designed a tax avoidance scheme which supposedly enabled a company, Umbrella Link Limited⚠️4, to hire individuals (and on-supply them to recruitment companies) but avoid accounting for income tax/PAYE on their wages.

- It’s stated that Kamal’s analysis confirms the scheme won’t have to be disclosed to HMRC. The document is also very careful to ensure it remains confidential. That strongly suggests that in fact it had to be disclosed to HMRC. Prima facie, this was an improper arrangement.5

- Umbrella Link targeted contractors, often on modest earnings – particularly social workers. We expect most had no idea they were participating in a tax avoidance scheme. These schemes are fundamentally unethical.

- The company paid Kamal £50,000 up-front for the scheme, plus 0.6% of the turnover of the company, and 0.4% for turnover over £8m. The nature of the scheme meant that Kamal was effectively receiving a percentage of the tax avoided.

- The contract was signed on 11 November 2024. Our article on Arka Wealth was published 26 February 2025. But two weeks before that, HMRC had publicly listed the company as operating a tax avoidance scheme and told the company it had unlawfully failed to disclose the scheme to HMRC. The company was doomed from that point.

- On 25 July 2025, HMRC issued a tax avoidance “scheme reference number” to Umbrella Link (with the five month delay probably thanks to delaying tactics from Umbrella Link).

- These companies never defend their tax positions – their (mysterious) ultimate owners just let them fold. So at some point, HMRC presented the company with a tax bill, the company ignored it, and HMRC applied for a winding up petition on 27 October 2025. A winding-up order was made on 10 December 2025.

The narrow point is that Kamal was never going to make £8m from this company. It only had a few months of operation. His claim was abusive, intended to intimidate me. As Mrs Justice Collins Rice said:

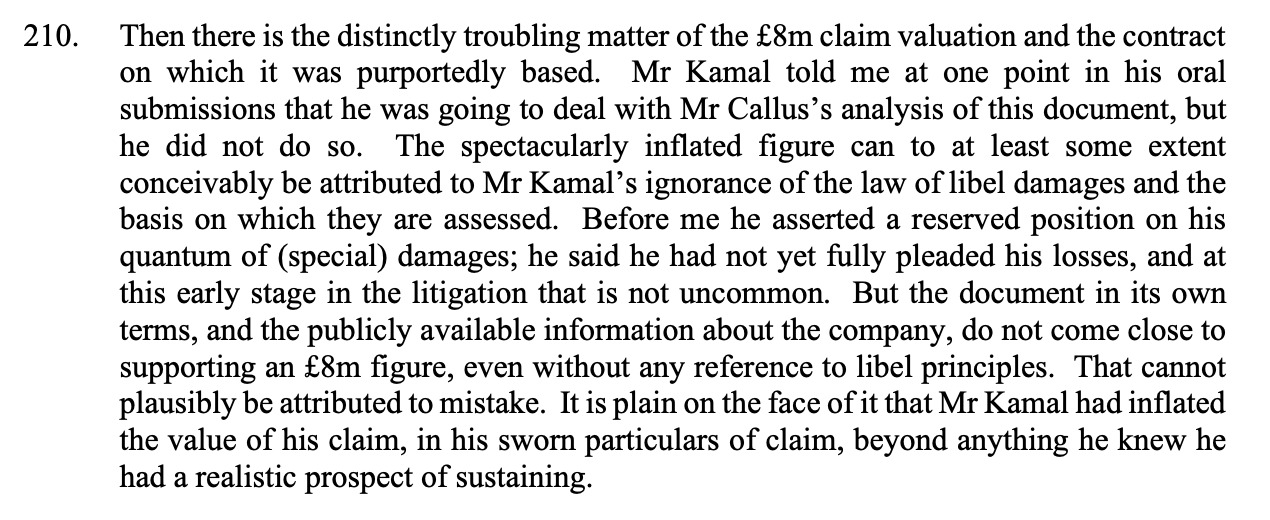

Then there is the distinctly troubling matter of the £8m claim valuation and the contract on which it was purportedly based. Mr Kamal told me at one point in his oral submissions that he was going to deal with Mr Callus’s analysis of this document, but he did not do so. The spectacularly inflated figure can to at least some extent conceivably be attributed to Mr Kamal’s ignorance of the law of libel damages and the basis on which they are assessed. Before me he asserted a reserved position on his quantum of (special) damages; he said he had not yet fully pleaded his losses, and at this early stage in the litigation that is not uncommon. But the document in its own terms, and the publicly available information about the company, do not come close to supporting an £8m figure, even without any reference to libel principles. That cannot plausibly be attributed to mistake. It is plain on the face of it that Mr Kamal had inflated the value of his claim, in his sworn particulars of claim, beyond anything he knew he had a realistic prospect of sustaining.

…

I am not prepared either to accept that the deployment of the £8m contract valuation in the context of this litigation was behaviour more likely than not attributable to simple inexpertise, particularly when considered together with the other unjustifiable and unsustainable ‘compelled speech’ remedies demanded. It may be that the Defendants viewed this behaviour with a degree of scepticism because of its very extravagance, and the expertise and advice available to them might well have encouraged that scepticism. But it is plain enough on the face of the documentary evidence that Mr Kamal intended his demands to be taken most seriously and to have a serious impact, and it appears that, to at least some extent, that was borne out in practice.

This may have consequences for Kamal, but there’s a much more important point. Tax barristers (and Kamal is not alone) are entering into contracts which are pure conflicts of interest. There is no “independence” or “integrity” to an opinion that a tax scheme works, when the barrister is paid per pound that goes into the scheme. I find it hard to believe that such contracts are permitted by the Bar Standards Board – if they are, it’s a disgrace, and if they’re not, action should be taken.

Why Kamal lost

Here’s a very brief summary of each of the points:

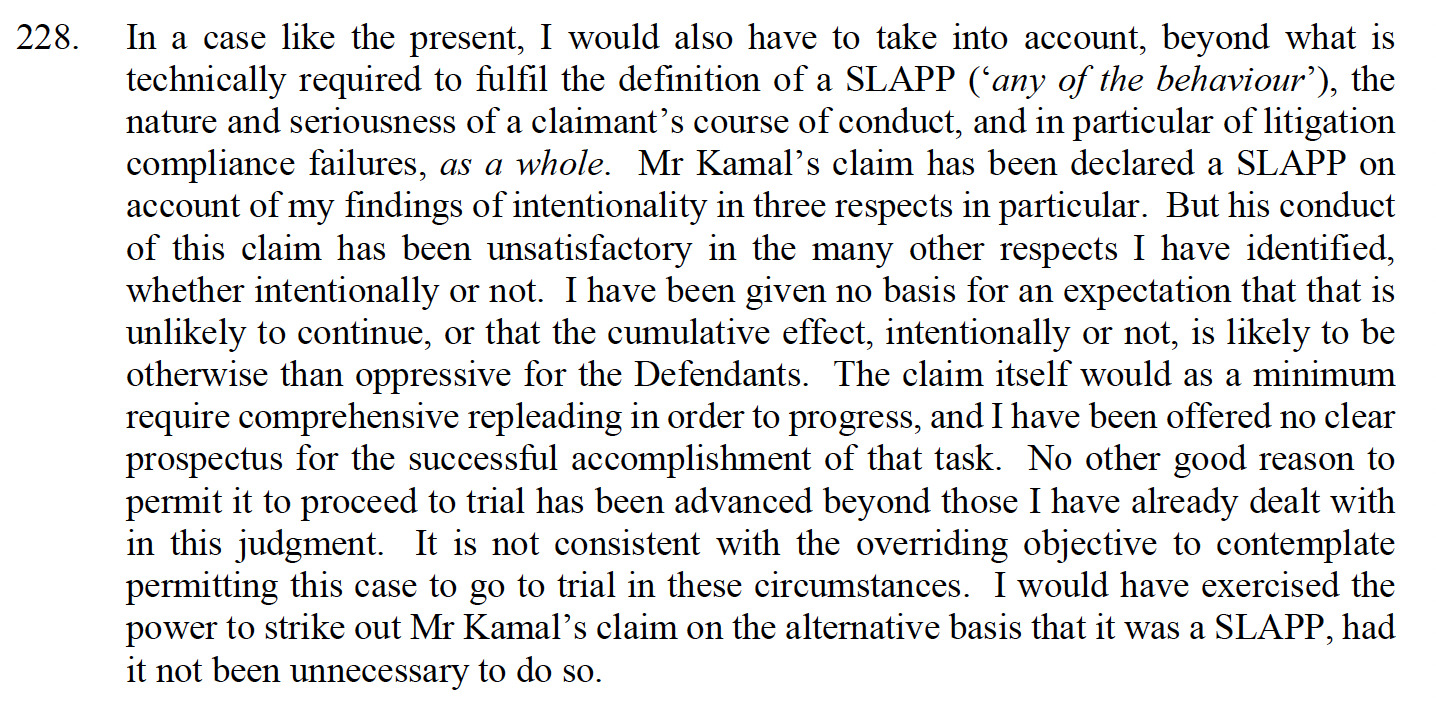

1. Kamal tried to sue on a Google search result. You can’t.

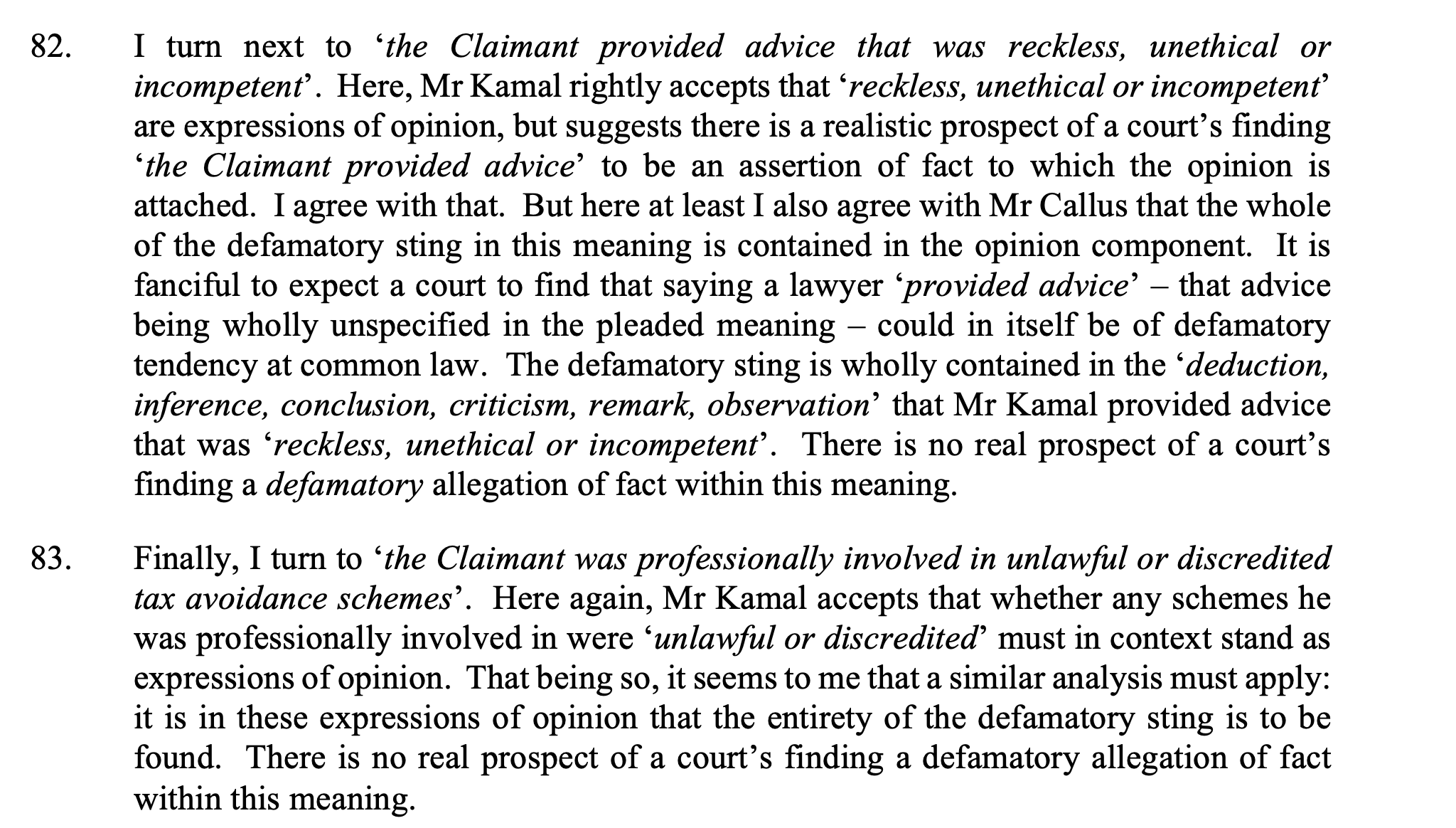

He complained that search engines displayed the following description of the article: “Failed tax avoidance from Arka Wealth and Setu Kamal” which he said was defamatory.6 But the rule in the Charleston case is that you can’t sue for defamation based on a headline in isolation – only on the complete publication. So Mrs Justice Collins Rice said the pleading was “bad in law” and “certain to fail”:

![18.

However I agree with Mr Callus that I am bound as a matter of law to apply the rule in

Charleston to Mr Kamal’s pleadings. The last two sentences of [4] of his particulars

of claim, whatever he intended by them, read as plainly and irremediably inconsistent

with the rule. I do not consider they can survive a strike-out application. They are bad

inlaw. As such, they disclose no reasonable grounds for bringing a libel claim in those

terms and are certain to fail.](https://taxpolicy.org.uk/wp-content/uploads/2026/03/image-34.png)

2. Kamal alleged I was dishonest, with zero evidential basis

He pleaded “malicious falsehood” – meaning that I wrote the article dishonestly or with an indifference to truth. But he had no basis for this, even if every fact in his pleading was accepted. So Mrs Justice Collins Rice struck this out. It was “irremediably defective”.

3. Kamal said it was “false and misleading” for me to accurately report a High Court decision

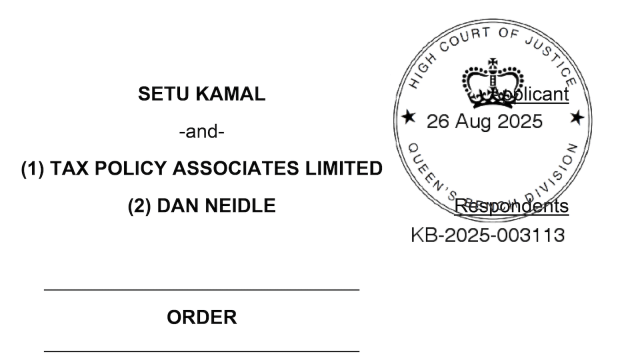

At this point Kamal approaches dishonesty. He said it was “false and misleading” for us to write that a court had found that he’d breached his duty of candour to the court. That was bizarre, because a court had found exactly that. Mrs Justice Collins Rice granted the strike-out and said Kamal’s pleading was an abuse of court processes:

![31.

In the circumstances, the pleading that it was ‘false and misleading’ to suggest that a

judicial finding of breach of duty had been made against him is incapable of forming a

part of the just disposal of Mr Kamal’s libel claim. The attempt to do so is an abuse of

the court’s processes. I grant the Defendant’s application to strike out [5(b)] of Mr

Kamal’s particulars of claim.](https://taxpolicy.org.uk/wp-content/uploads/2026/03/image-36.png)

4. Kamal’s attempt to compel me to apologise had no legal basis

He asked the court to order me to apologise. But courts can’t compel speech. So Mrs Justice Collins Rice struck this out too – it was “bad in law, and certain to fail”:

![34.

35.

Mr Kamal did not engage with the substance of this objection before me. Mr Callus is

undoubtedly right as to the law. To order an apology would be a form of compelled

speech which clearly engages the Article 10 ECHR rights of defendants. There would

have to be an identifiable basis in law for a court to be able to do it. There is none. A

court has no such power.

I grant the Defendants’ application to strike out [14] of Mr Kamal’s particulars of claim

(and the equivalent parts of the claim form). It is bad in law and certain to fail.](https://taxpolicy.org.uk/wp-content/uploads/2026/03/Screenshot-2026-03-12-at-07.58.06.png)

5. The rest of the article was just honest opinion

We then applied for summary judgment on the rest of the libel claim, on the basis that it was honest opinion. It’s unusual to obtain summary judgment on an opinion point, but in this case Kamal’s pleaded meanings for the article were “disciplinary or regulatory action ought to be taken against” Kamal, he “poses a risk to clients and the public”, he provided advice that was “reckless, unethical or incompetent” and was “professionally involved in unlawful or discredited tax avoidance schemes”. Each of these was clearly an expression of opinion, so we obtained summary judgment:

![84.

85.

I have thought particularly hard about this last point because, in his written and oral

submissions to me, Mr Kamal laid great emphasis on his principal objection to the

Article being its association of him with the Arka Wealth scheme it critiques. He says

he did not devise or advise on that scheme, and the Article suggests he did. I can see

that Mr Kamal might have pleaded (I do not necessarily say as to any particular

outcome) not only the generalised meaning he in fact pleaded at [6(a)] but also a factual

allegation setting out that (as he complains) he invented, promoted or advised on a

specific scheme and an associated expression of opinion that that particular scheme was

unlawful or discredited. That would be a worse meaning than he has in fact pleaded,

so there can be no real prospect a court would find such a meaning.

Mr Kamal might have pleaded single natural and ordinary meaning in a number of

respects which are worse than he has in fact pleaded (professionally-advised libel

claimants tend to plead meanings which are as high as they consider plausible short of

extravagance, precisely because they know they set a ceiling on a court’s

determination). A court is meaningfully limited in law by a claimant’s pleaded

meaning. Mr Kamal has made choices about the claim he is asking the Defendants to

address and the court to consider. His pleading of meaning in his particulars of claim

is not technically deficient as such — it does not require remedial amendment in order

to set out a case it would be fair to ask a defendant to defend. But it does delineate the

claim he himself has chosen to advance. I can consider the claim he has pleaded. I

cannot on a summary judgment application consider speculatively different claims he

might have pleaded but did not.](https://taxpolicy.org.uk/wp-content/uploads/2026/03/media-XXXXXXXX.QPtl5QAsB4.jpg)

![87.

88.

The first is the point of principle that, their Art.10 rights being engaged, courts ought

not to strive officiously to impute factual allegations to defendants where, informed by

the context of a publication read as a whole and by the ceiling imposed by a claimant’s

own pleading, it is straightforward to recognise that an ordinary reasonable readership

would have no difficulty in understanding they were receiving defendants’ opinions. A

court ‘should be alert to the importance of giving free rein to comment and wary of

interpreting a statement as factual in nature, especially where as here it is made in the

context of political issues’ (Yeo v Times Newspapers Ltd [2015] 1 WLR 971 at [97] per

Warby J (as he then was)). The subject matter of the present Article is not (party-

)political in the narrow sense, but it does avowedly enter the sphere of public policy

debate and law reform. In any event, the scheme of the statutory defences in the

Defamation Act 2013 is itself a recognition of the respect due to free speech in the form

of expression of opinion, the protection of which should not be ‘whittled away by

artificially treating comments as if they were statements of fact’.

The second reason lies in the structure of section 3 of the Act itself. The issue of basis

of opinion is something different from the prior question of fact/opinion, and courts

necessarily have to be careful not to elide the two. It is to the issue of basis of opinion

(section 3(3)) that I turn next.](https://taxpolicy.org.uk/wp-content/uploads/2026/03/Screenshot-2026-03-12-at-08.00.55.png)

Kamal spent much of his time arguing we’d defamed him by saying he devised or advised on the particular Arka Wealth scheme in question. But this wasn’t part of Kamal’s pleaded claim – and it never could have been, because we didn’t say that. We set out evidence from Arka Wealth and Kamal himself linking him to the scheme. More on that below.

The claim was a SLAPP

At that point, I had won. But we also applied to strike out the claim under the – new and untested – anti-SLAPP rules in the Economic Crime and Corporate Transparency Act 2023.

This required us to establish, first, that there was a SLAPP within the definition in section 195 of the Act.

That first requires satisfying the conditions in subsections (1)(a) to (c):

We could do this without much difficulty because:

- Kamal’s actions had the effect of “restraining [my] exercise of the right to freedom of speech”. Defamation actions will almost always have this effect.

- The “information” disclosed by the exercise of my freedom of speech had to be “to do with economic crime”. There was some discussion about the meaning of “information” but to my (non-libel lawyer) mind this is a straightforward point – the “information” is simply the stuff that we said.

- The Arka Wealth scheme was plausibly tax fraud in several countries, potentially including the UK – and those were “economic crimes” within the definition.

- I had to have “reason to suspect that an economic crime may have occurred and [believe]that the disclosure of the information would facilitate an investigation into whether such a crime has (or had) occurred”. I said I did, and Kamal didn’t challenge that.

- The disclosure had to be “for a purpose related to the public interest in combating economic crime”. We had said there should be an investigation; that was sufficient.

We then had to show that the condition in subsection (1)(d) was satisfied:

“Inconvenience” in particular is a very low bar, but I’d also suffered some alarm/distress at the size of the claim, and certainly significant expense. And Mrs Justice Collins Rice had no difficulty concluding that numerous elements were beyond that ordinarily encountered in litigation:

And then the difficult element: was all this intentional?

Some of it was simple incompetence, but Mrs Justice Collins Rice concluded that key elements on balance were intentional – in fact she comes close to saying that Kamal had been dishonest:

At that point, Civil Procedure Rule 3.4(2)(d) is engaged, giving the judge the discretion to strike out a case if:

We had established the first part. The onus for the second is on the Claimant – and (for reasons which are unclear) Kamal had failed to provide any sworn evidence to the court. So Mrs Justice Collins Rice had no hesitation in disposing of the point:

That just left the question of whether the Court should exercise its discretion to strike out the case. Mrs Justice Collins Rice concluded that, in light of Kamal’s behaviour, she would:

Kamal’s response

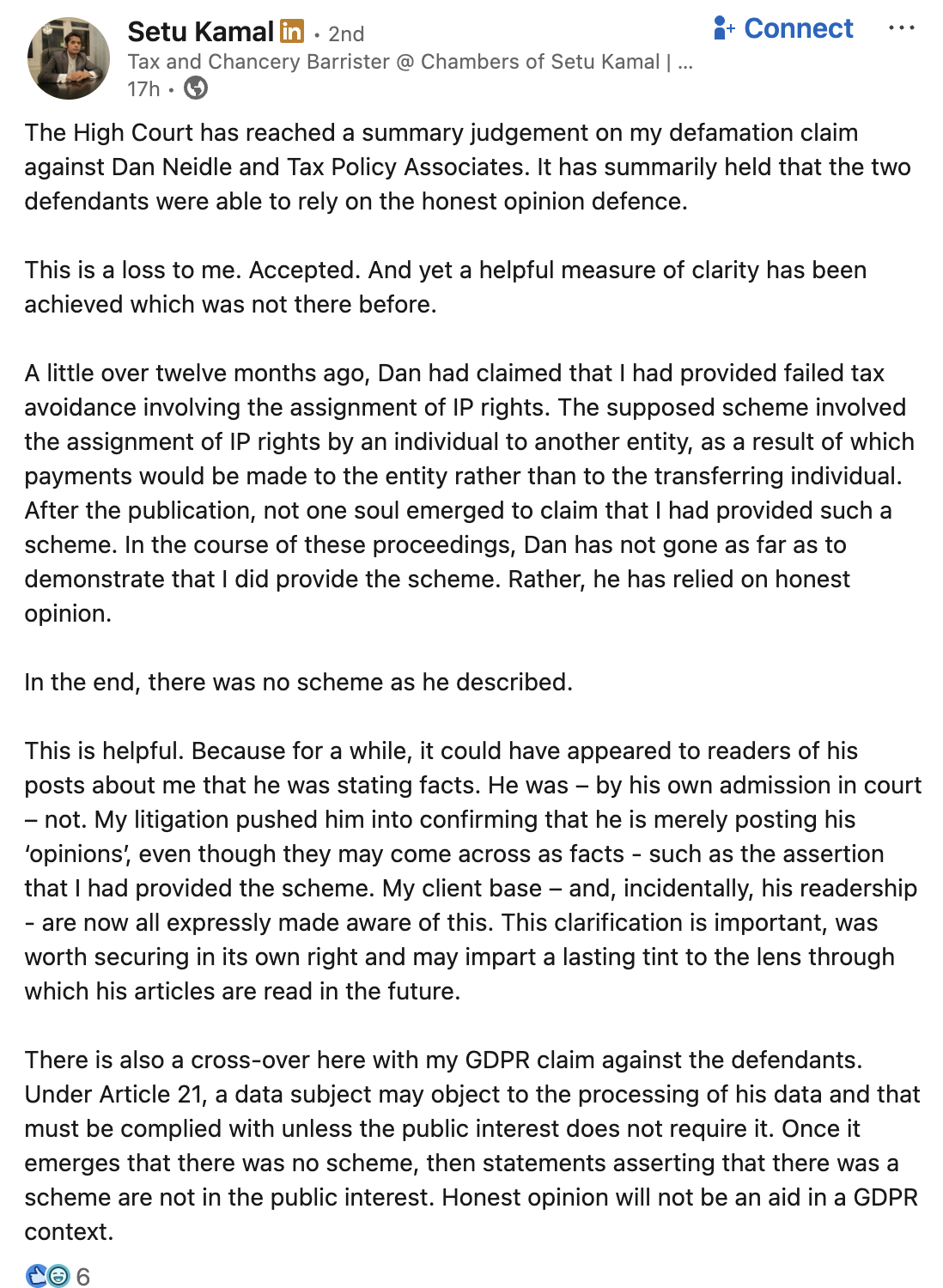

Here’s Kamal’s response to the judgment on LinkedIn:

This is delusional. It bears no relation to the actual reasons why he lost.

But what of Kamal’s complaint that he didn’t provide an opinion on the scheme?

That point was never litigated, because Kamal never pleaded it. But he couldn’t have done – because we never said that he did provide an opinion. Our report was very carefully worded and says no more than we could prove from available facts at the time.

Those facts were:

The Arka Wealth website said Kamal was their “legal partner” and provided a “comprehensive legal opinion” for everyone buying the scheme:

Kamal appeared in a video for Arka Wealth confirming that every Arka Wealth client receives a legal opinion from him:

The people alleging that Kamal provided opinions on the scheme were Setu Kamal and Arka Wealth.

Mr Kamal should sue himself.

Footnotes

The website went offline in July 2025 and it appears the company ceased trading around that time. ↩︎

This wasn’t always the case, particularly prior to the 2013 Defamation Act. ↩︎

Particularly the law of confidence, GDPR and privacy torts. ↩︎

The company was claimed to be ultimately owned by an individual resident in Mauritius, and later by an individual resident in Kazakhstan. It is likely these Companies House filings were false, unlawfully hiding the true beneficial owner. ↩︎

Promoters sometimes contest the application of the disclosure rules in front of tribunals – they have lost on almost every single occasion (the one exception was where the arrangement was disclosable, but the “promoter” targeted by HMRC wasn’t actually the promoter). ↩︎

Kamal’s actual pleadings were much more confused than this. He said he was complaining about the “slug” – the bit of the URL after the domain. But the slug was “tiktok-tax-avoidance-from-arka-wealth-why-the-government-and-the-bar-should-act” – Kamal should have referred to the website metadata that is picked up by search engines. That’s why Collins Rice J says “whatever he intended by them”. But even if he had pleaded the point competently, the rule in Charleston meant it was hopeless. ↩︎

I’m being sued for £8m for a report on tax avoidance

An incompetent attempt to silence me by tax barrister Setu Kamal

Carter-Ruck enabled the $4bn OneCoin fraud. Was it a crime?

Carter-Ruck: the libel firm trying to cover up that they’d acted for the $4bn OneCoin fraud

The Zahawi libel story isn’t over – his lawyer is appealing

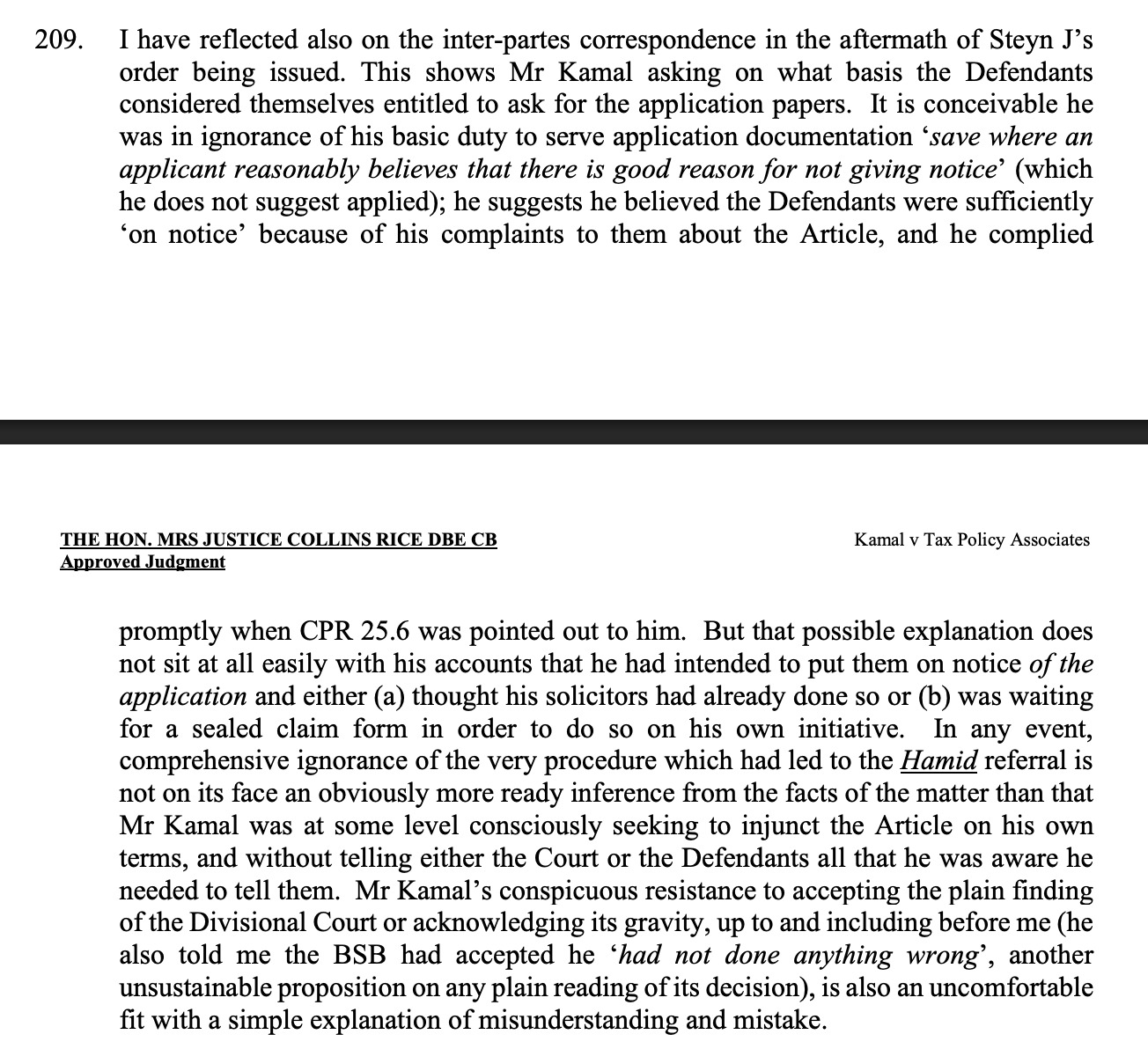

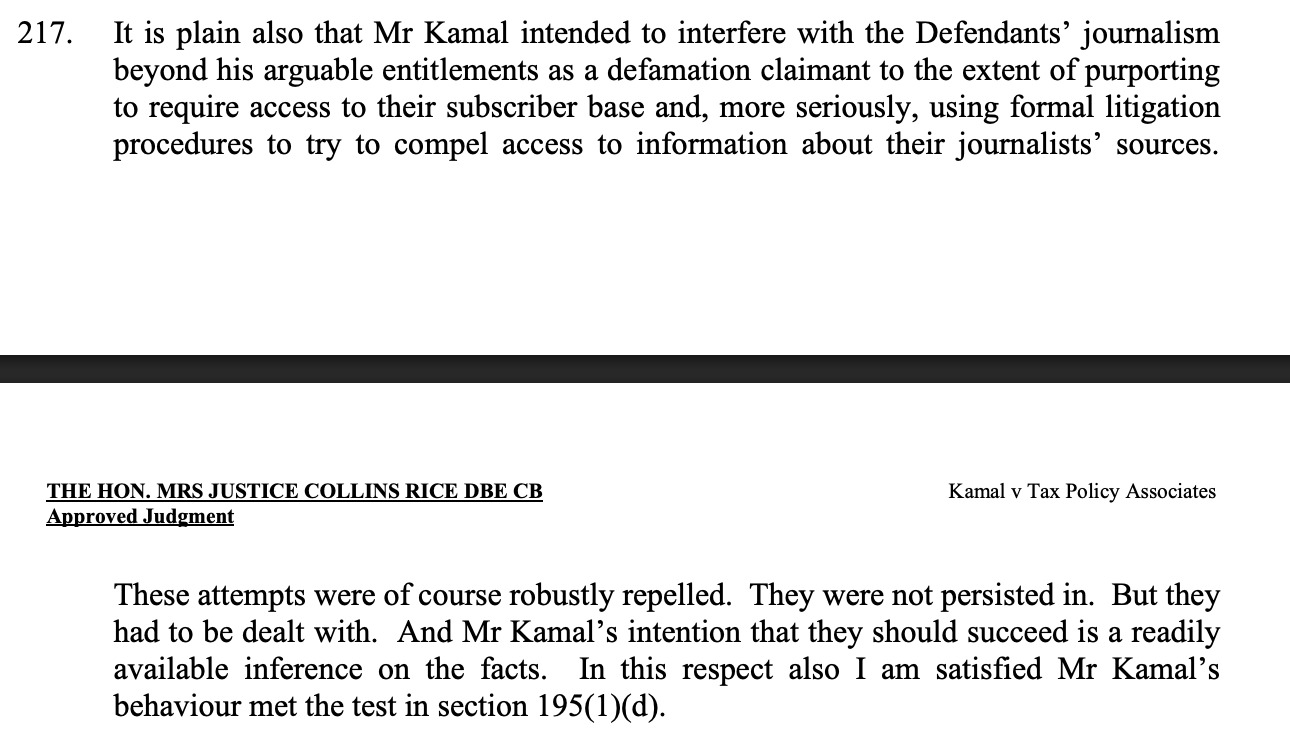

Leave a Reply