Chancery Law & Tax is “one of the UK’s leading providers of Legal Services”. It appears to have no employees or directors with any legal or tax qualifications. It’s owned by a man called Tony Gimple.

Mr Gimple’s previous firm, Less Tax for Landlords (aka the One Consultancy Group) promoted a landlord tax avoidance scheme. Mr Gimple sold the scheme very successfully for years – but it was an incompetent disaster, was shut down by HMRC, and has left hundreds of landlords in a dire financial position.

Mr Gimple has learned nothing. Chancery Law & Tax is going down the same path – advising landlords but getting the basics badly wrong. If the new proposed regulation for advisers doesn’t put him out of business, it isn’t working.

Less Tax for Landlords

Mr Gimple was one of the founders of Less Tax for Landlords (LT4L), before leaving the firm in 2020. Our reporting on Less Tax for Landlords is here.

LT4L advised landlords to move their properties into an “hybrid partnership” LLP. Mr Gimple said this somehow enabled an inheritance tax exemption (it didn’t) and that LLP income was “trading income” (it isn’t). These were elementary mistakes that a trainee accountant would spot.

When a landlord politely asked how the structure could possibly work, Mr Gimple’s only response was an aggressive dismissal.

Worse still, Mr Gimple assured potential clients that:

This was false – professional indemnity insurance does not work this way. And, sure enough, HMRC did not agree with the way the scheme was structured, and says it should have been disclosed as a tax avoidance scheme. No landlord has received a penny from LT4L’s insurers.

Mr Gimple now says he never understood the structure, and trusted LT4L’s accountant, Chris Bailey, to get the tax right. But listen to one of his interviews – he’s talking at length, with great confidence:1Original interview here.

Or this presentation:

Almost everything he says in the interview and the presentation is dangerous nonsense.

Someone with so little understanding of UK tax should never have been selling a tax scheme, and certainly shouldn’t be running a tax firm now. But he is.

Chancery Law & Tax

Mr Gimple’s new firm has just published a guide to incorporating a property business.

It contains a very serious error.

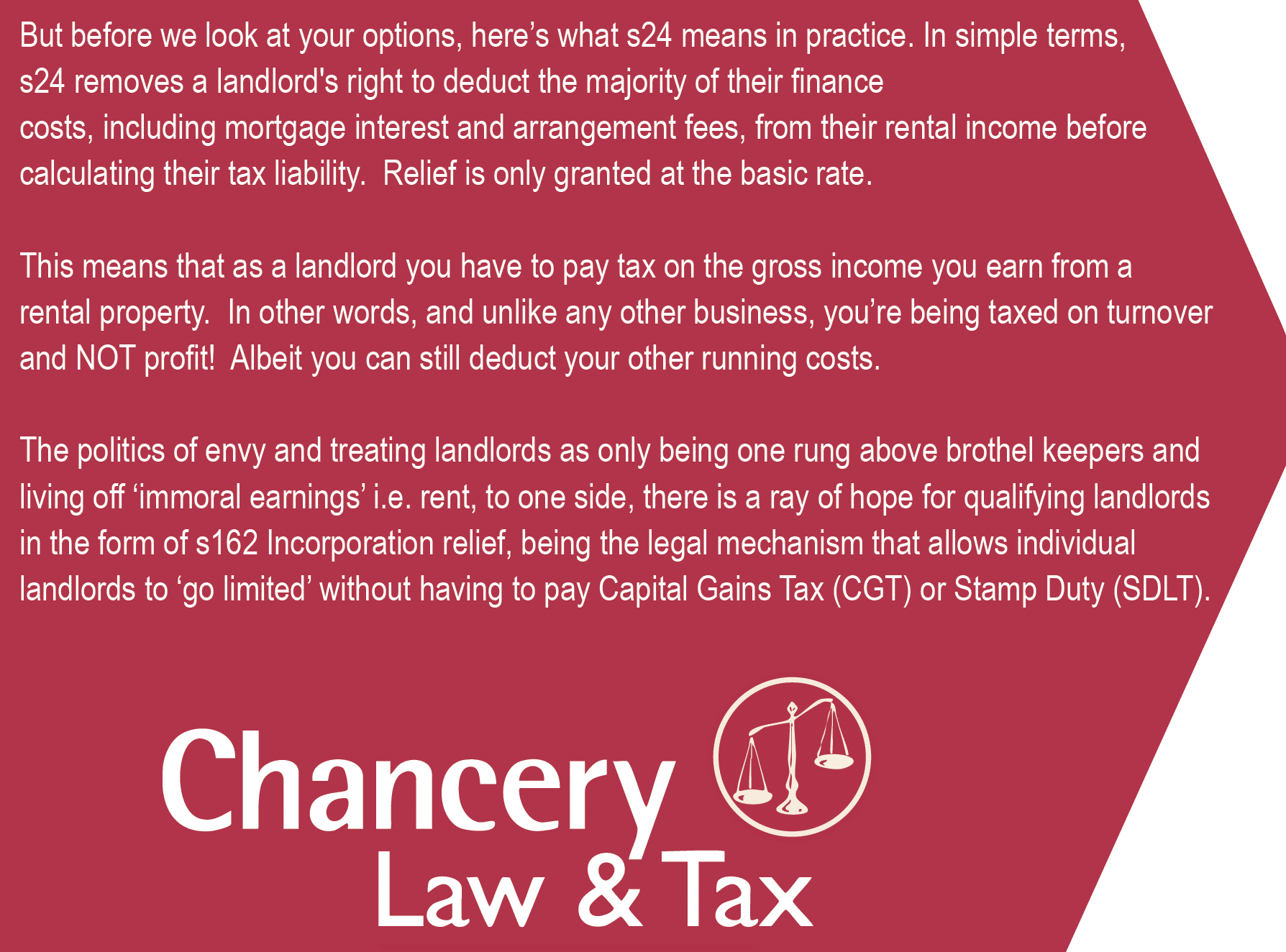

It’s attractive for some landlords to move their property rental business into a company. The company will then pay corporation tax at 25% rather than income tax at up to 45% (although dividends paid by the company to the landlord will be subject to income tax). However the bigger advantage is that the “section 24” limitation on interest tax relief only applies to individuals; not companies.

Incorporating therefore creates a potentially significant ongoing tax benefit for landlords.

But there is a big risk. Incorporation of a landlord’s business can easily trigger capital gains tax and stamp duty land tax. These will often be very large liabilities, much larger than the ongoing tax saving. Great care needs to be taken.

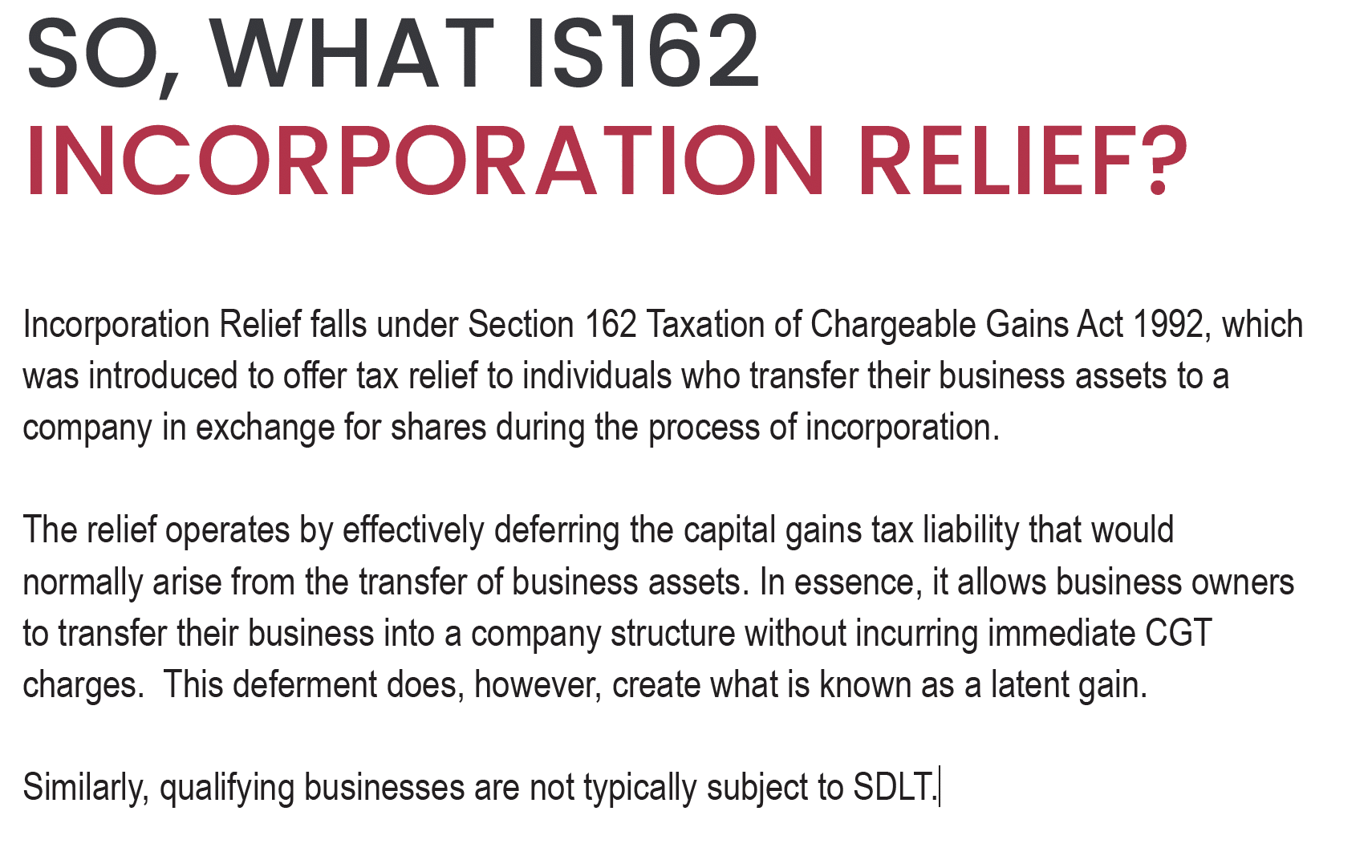

Mr Gimple’s guide mainly discusses the section 162 TCGA “incorporation relief” from capital gains tax. However it claims that section 162 also applies to stamp duty land tax:

This claim is simply wrong. Section 162 does not apply to SDLT in any manner.

This isn’t a one-off mistake. The guide goes on to say that “qualifying businesses are not typically subject to SDLT”:

It’s another serious error. In all cases where an individual is incorporating a property rental business, there will be an up-front SDLT charge – potentially a very high one given current rates.

If the individual is carrying on a property rental business in partnership then the complex rules in Schedule 15 Finance Act 2003 may apply to prevent an SDLT charge – but specialist advice is required. There is zero connection between s162 and Schedule 15 (or indeed any aspect of SDLT).

These errors suggest that Mr Gimple and Chancery Law & Tax lack a basic understanding of SDLT.

The Less Tax for Landlords connection

Mr Gimple is promoting incorporation to the very landlords who were sold the failed Less Tax for Landlords scheme. There are some highly complex SDLT consequences of the LT4L scheme2In particular the complex “sum of the lower proportion” rules which apply where the beneficial interest in a property has been partnership property of this kind of property investment partnership. The matter is further complicated by changes in the LLP members’ entitlement to income, and potentially also by the paragraph 12A elections rules., and on the evidence of this guide, Mr Gimple’s firm lacks the expertise to deal with them. Given his track record, we would strongly advise affected landlords to instead seek independent advice from an adviser with tax qualifications.

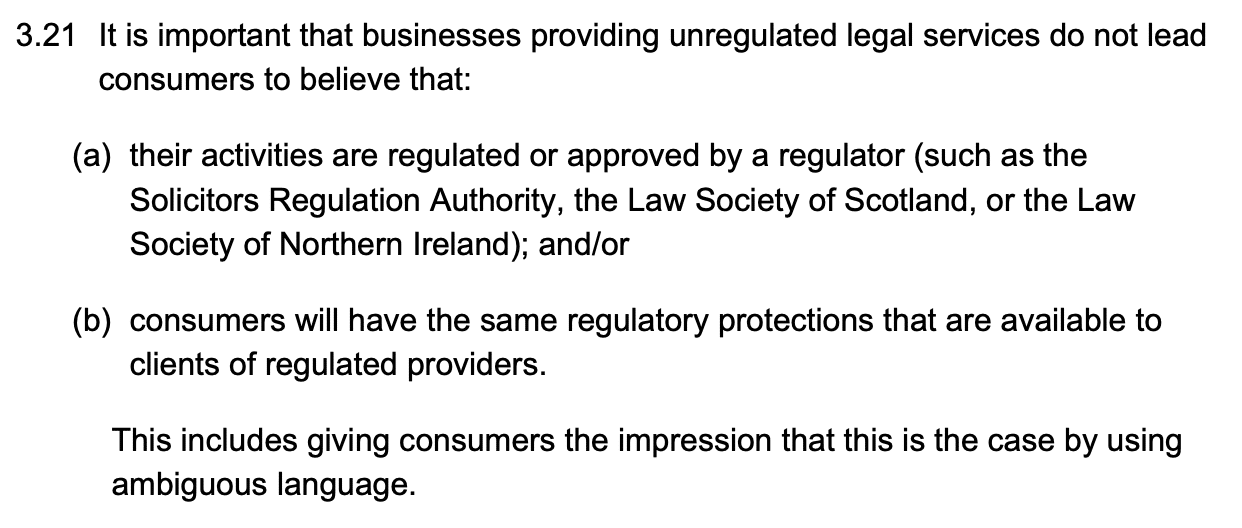

Is it legal to call the firm “Chancery Law & Tax”?

Chancery Law & Tax obviously have the word “Law” in the title, and say they’re “one of the UK’s leading providers of Legal Services”. They claim to provide a Will writing service.

It’s an open question whether this amounts to holding out that the firm is regulated. If it is, that’s a criminal offence, for the company and its directors, under section 10 of the Administration of Justice Act 1985.

The SRA may wish to consider whether Mr Gimple has gone too far.

Chancery Law & Tax may also have breached the Competition and Markets Authority’s guidance for unregulated providers of legal services, in particular:

Finally, the Advertising Standards Authority may have a view on how reasonable it is for a small unregulated firm with a dismal history to say it is “one of the UK’s leading providers of Legal Services”.

Who should landlords turn to for advice?

Landlords, and anyone else needing tax advice, should use a regulated firm, and only deal with regulated professionals. If you’re speaking to a salesman like Mr Gimple, with no legal or tax qualifications, then our view is that you’re making a mistake, and potentially a very expensive one.

- 1

- 2In particular the complex “sum of the lower proportion” rules which apply where the beneficial interest in a property has been partnership property of this kind of property investment partnership. The matter is further complicated by changes in the LLP members’ entitlement to income, and potentially also by the paragraph 12A elections rules.

8 responses to “Tony Gimple and Chancery Law & Tax: a one-man argument for the regulation of tax advice”

Fyi in case anyone missed this other LT4L critique:

https://elysium-law.com/news/cgt-rebasing-why-less-tax-for-landlords-planning-doesnt-work/

If there is a criminal offence, then could the Proceeds of Crime Act be used to recover fees conned out of customers?

It would only need one prosecution which left the promoter net underwater to drastically shrink the activity.

At the moment, why would they not do phoenix after phoenix?

Another great article, Dan.

On the question of CL&T holding itself out as a regulated firm, you might note one of Mr Gimple’s LinkedIn posts from 2 weeks ago in which he states: “Based in London and Durham, Chancery Law & Tax is a specialist law firm that primarily works with portfolio landlords and property developers along with SME owner managers.”

That seems pretty explicit (and mis-leading) to me.

Thank you for continuing to expose these people, who continue to exploit hard-working landlords who just want to get on and run a decent business. It’s unbelievable that Mr Gimple is still pushing this stuff, and even more incredible, he can’t be stopped.

Why are there no systems in place to prevent people just starting up another business?

When I was in business people could just declare bankruptcy and it seemed to me start up again under another name.

Super article, keep it up!

There have always been and always will be chancers and crooks in society. But unless there are actual ways to disincentise and punish wrongdoing, these types brains work on the basis that no penalty/disincentive must = an incentive. The downside is not one – like banning people from being directors after they have ripped off society. Must be quaking!

People need to be legally pilloried, jailed and exposed but HMRC as good as encourages them with their lax attitude, promotion of ‘pay now, ask questions later’ schemes etc.

Isn’t it the definition of insanity to do the same bad things over and over and expect different results?

Another example of the result of having a wildly complex tax system which allows people like this to promote snake oil like this