The “tax gap” is the difference between the tax HMRC should collect and the tax it actually collects. Over the last nineteen years, most of the tax gap has fallen by two-thirds – a remarkable achievement. But a deep dive into HMRC’s latest tax gap statistics shows that HMRC has lost control of small business tax: 40% of corporation tax due from small businesses is not being paid. The small business tax gap rose sharply during the pandemic – and hasn’t fallen since.

If HMRC had closed the small business tax gap as effectively as it closed other tax gaps, it would collect £15 billion more each year.

The FT’s report on the new data is here. Our analysis is below.

The tax gap

The difference between the tax that should be paid and the tax HMRC actually collect is the “tax gap”. HMRC say it’s £46.8bn.1 There are a large number of uncertainties, but HMRC’s tax gap estimate work is generally regarded as world-leading.2

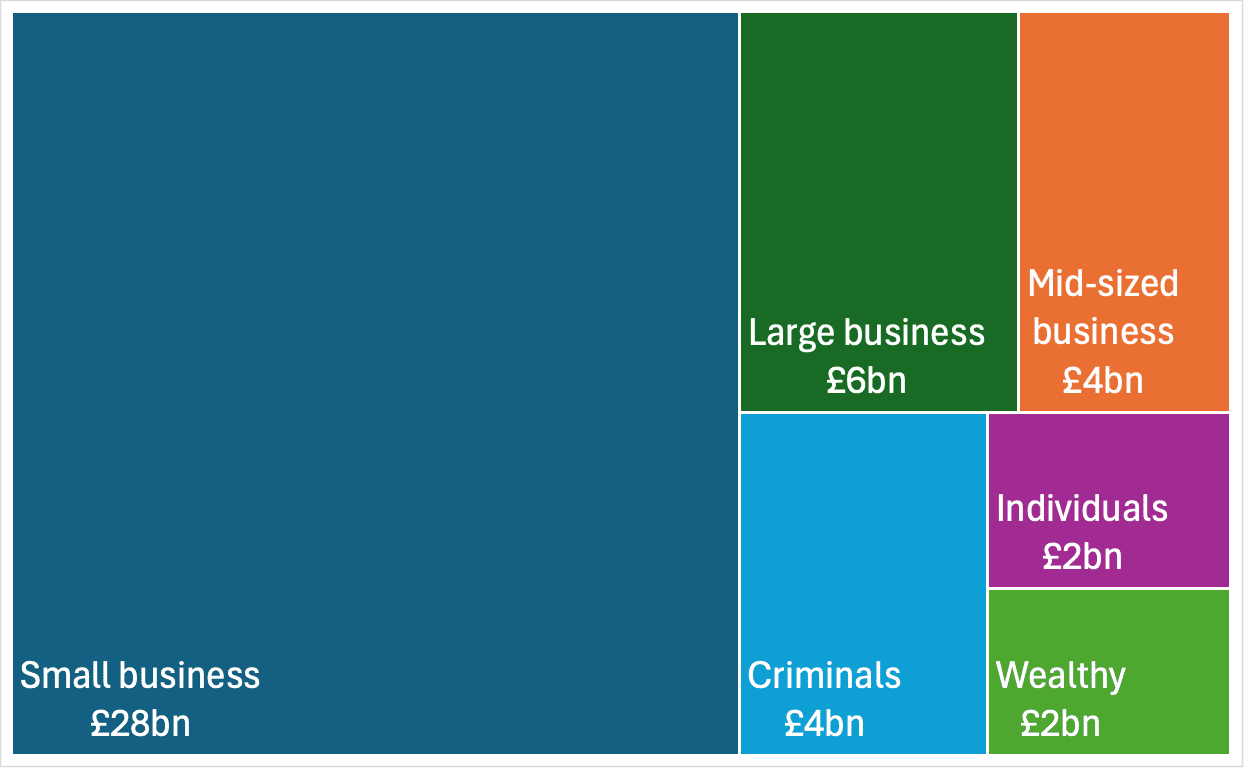

Where is most of the tax gap?

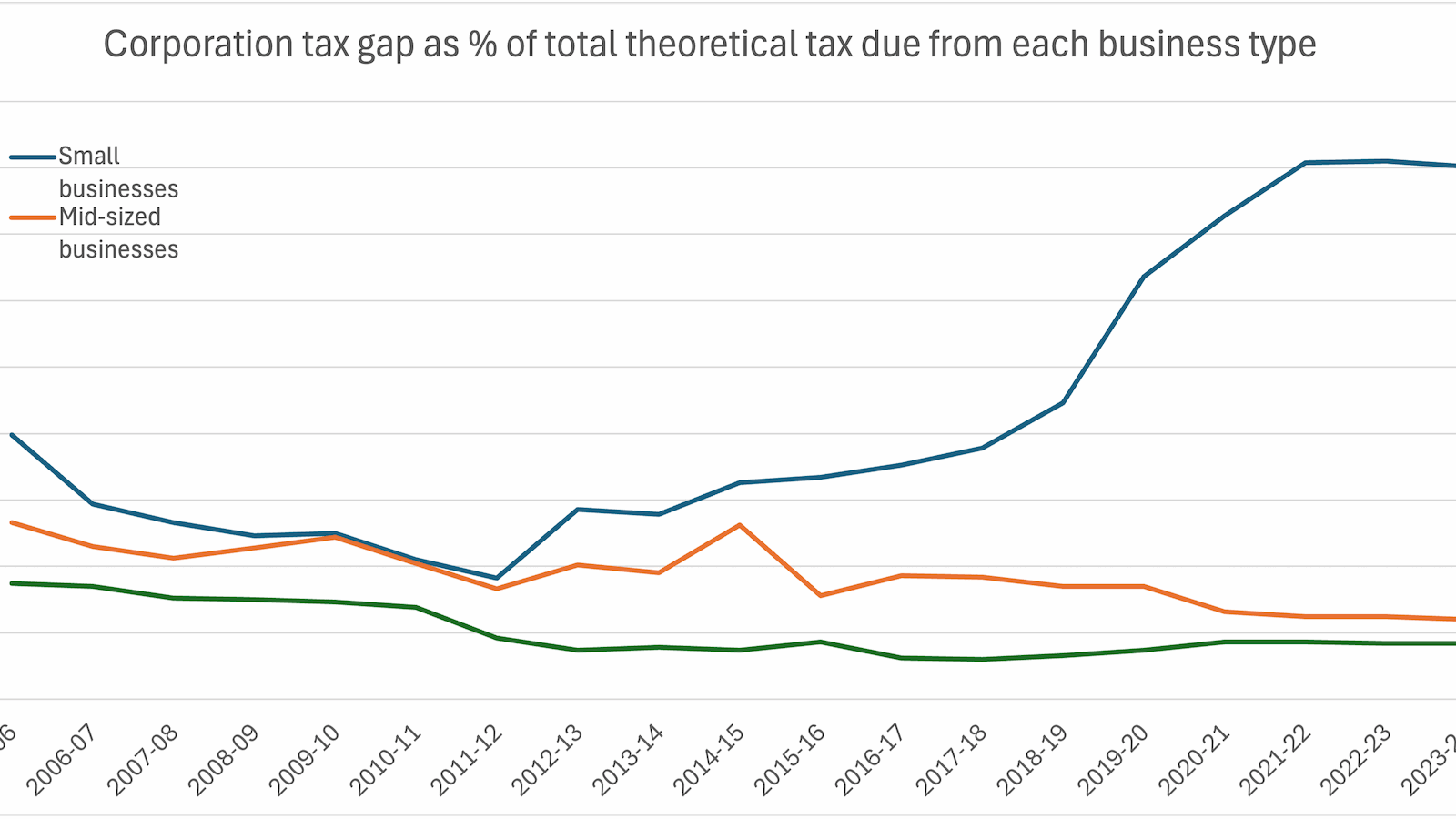

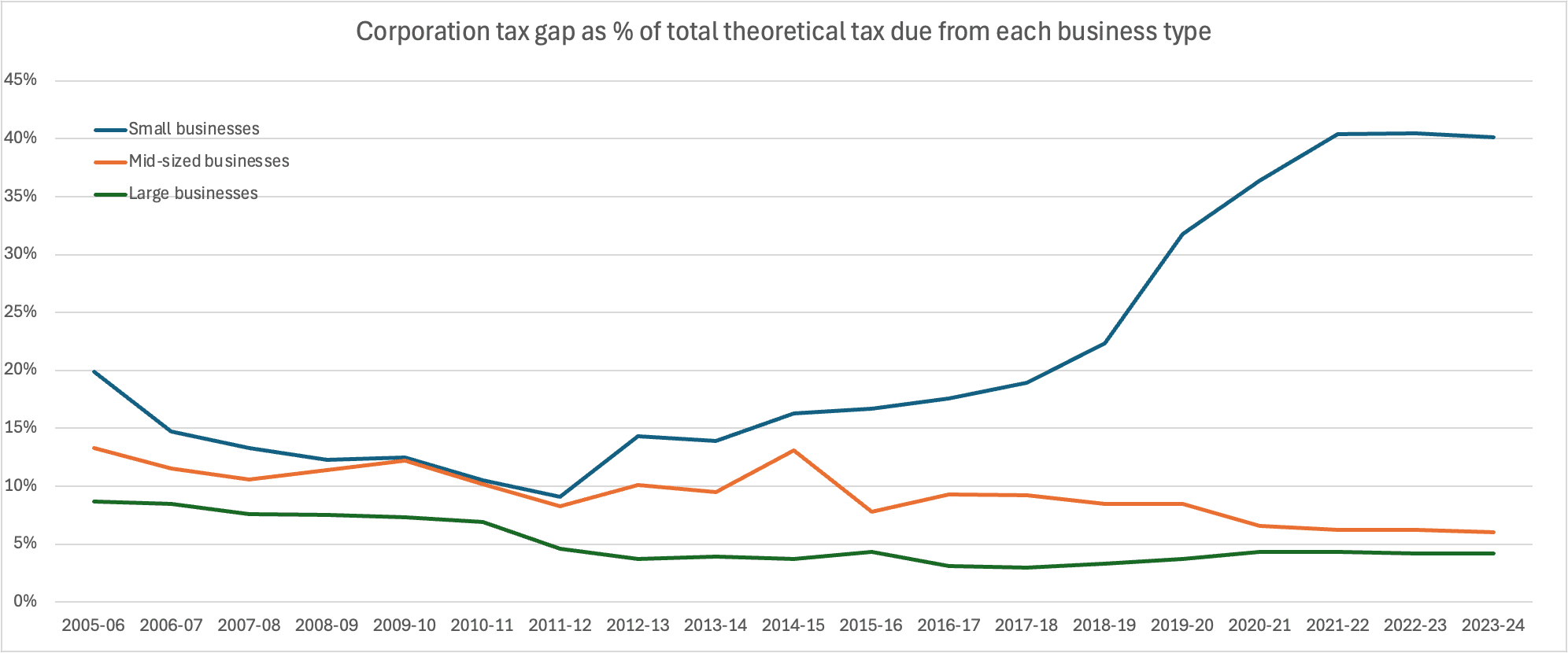

Most of the tax gap is from small businesses, meaning businesses with a turnover of less than £10m and less than twenty employees:34

What’s happened to the small business tax gap?

Small businesses have always been the most likely sector to pay the wrong tax (whether by accident or design). However in the last few years, something has changed:5

That sharp uptick in 2019/20 may have initially been caused by the pandemic, but we don’t see that effect for other types of taxpayer, and its now clear that the trend didn’t slow down after the pandemic.6 There have been a series of upward statistical revisions to data for recent years. These took the 2022/23 small business corporation tax gap from 32% to 40% (with the 2021/22, 2022/23 and 2023/24 figures being essentially identical). However HMRC sources have confirmed to us that these revisions don’t call earlier figures into question, and so the apparent trend in the data is real, and not just a statistical artifact.

It is astonishing that 40% of all corporation tax due from small businesses is now not being paid.

There’s a sharp contrast with the large and mid-sized business corporation tax gap, which HMRC has been remarkably successful at closing.

The wider picture

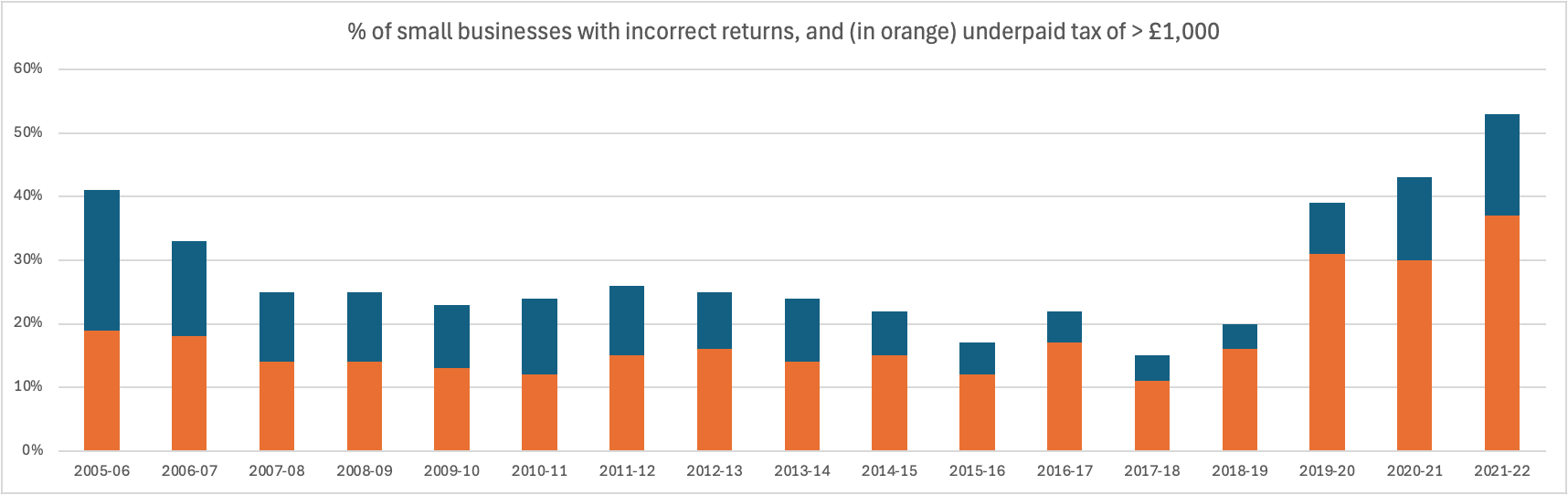

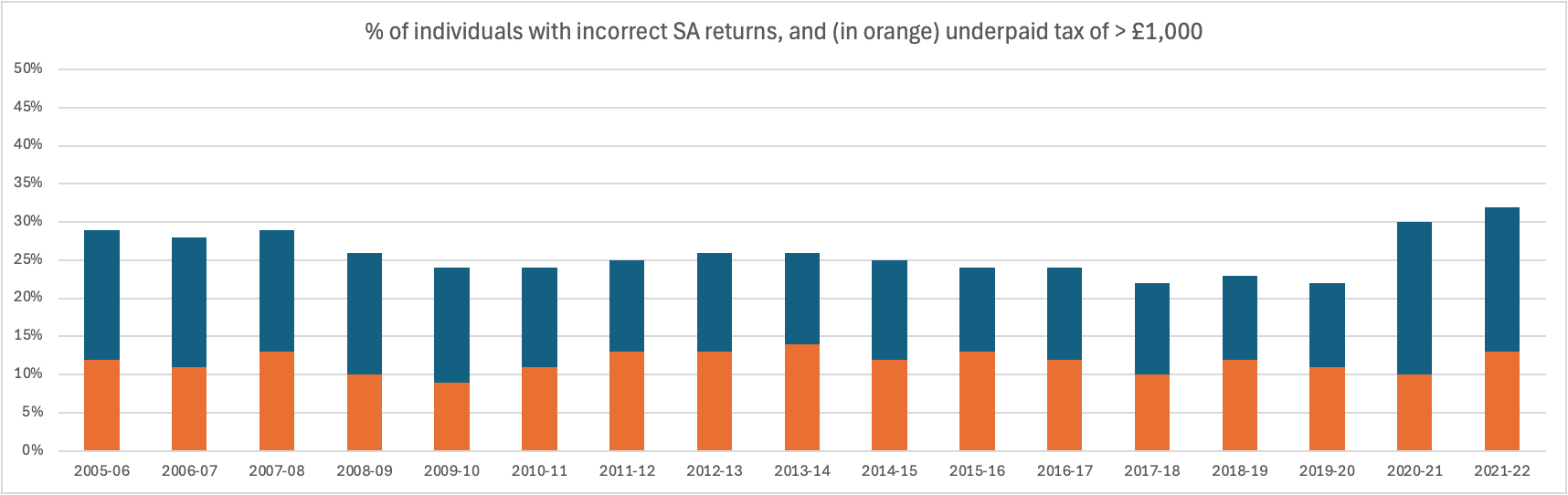

The problems appear to be widespread. HMRC data shows that well over a third of small businesses now underpay their tax by more than £1,000 – a doubling since 2018/19.

An obvious explanation is that this is a post-Covid effect. However there’s no such trend seen if we look at the figures for tax returns from individuals:7

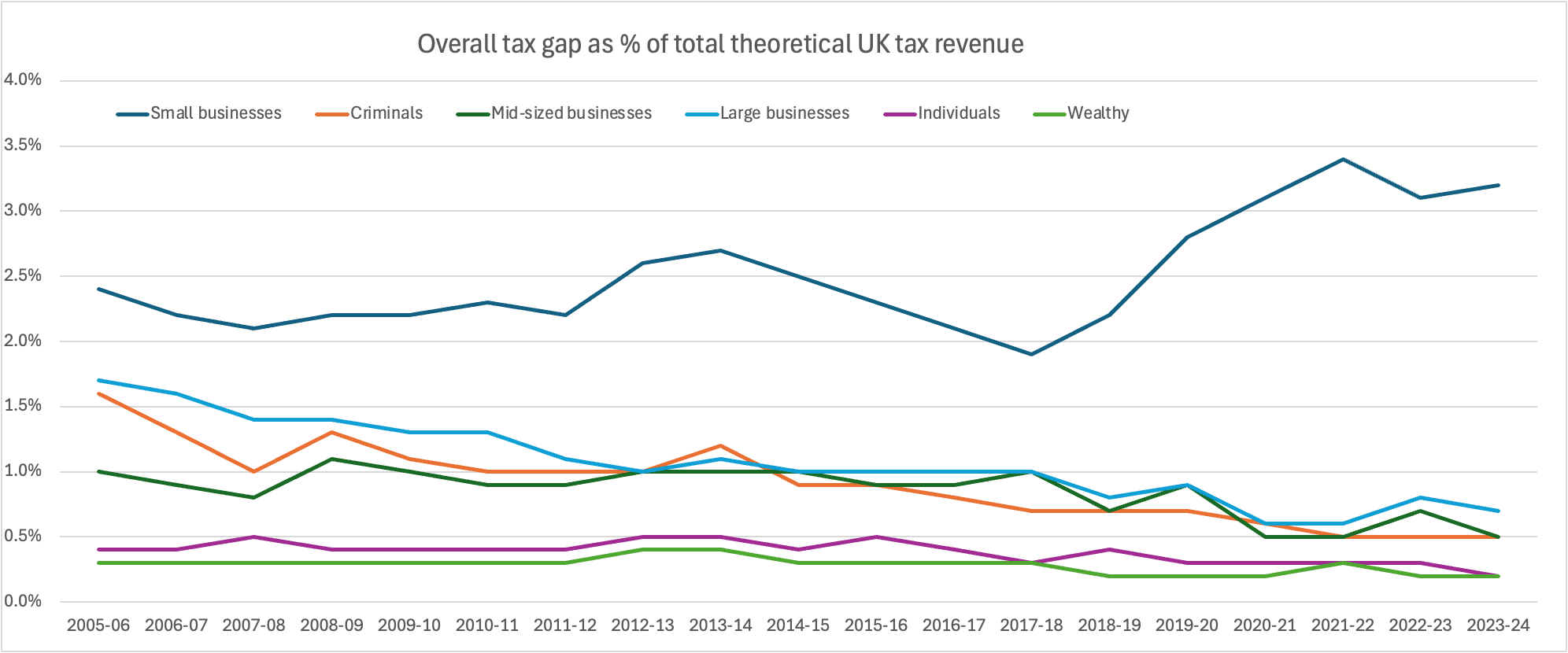

And it’s worse than this. The small business tax gap isn’t limited to corporation tax. If we step back and look at the HMRC figures across all taxes we see another dramatic divergence:8

HMRC have generally done an excellent job shrinking the tax gap, with declines across the board. But after 2017/18 something changed.

The small business tax gap increased from 2.4% of all UK tax revenues in 2005/6 to 3.2% in 2023/24. The rest of the tax gap fell precipitously over that period – large businesses from 1.7% to 0.7%; mid-sized businesses from 1.% to 0.5%.

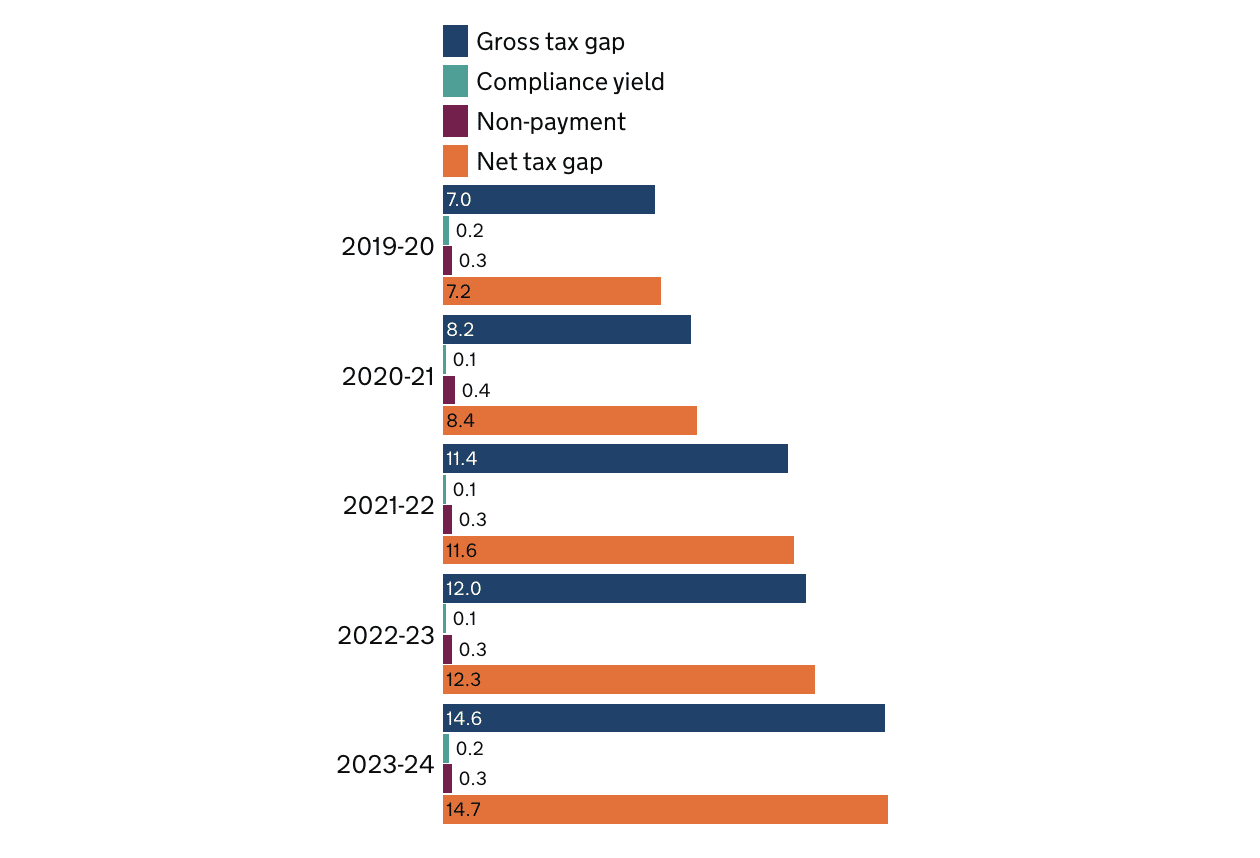

But whilst the small business tax gap has increased, the efforts to close it have not. This chart from HMRC’s report shows that the tax gap doubled over the last five years, but “compliance yield” (the return from HMRC’s investigation/compliance work) didn’t change at all:9

How much are we losing?

If the small business tax gap had declined at the same rate as the mid-sized business tax gap, HMRC would collect an additional £15 billionevery year.101112).

What is going on?

Small businesses have always been responsible for the majority of tax evasion and non-compliance. The cliché of men in white vans receiving payment in cash isn’t that far from the truth. This explains why the small business tax gap is hard to close. It doesn’t explain why it’s increased.

We believe there are two key factors: a decline in HMRC customer service to small companies, and an upsurge in avoidance and evasion which doesn’t really relate to small companies at all, but is technically allocated to them.

A decline in HMRC customer services

There have been many anecdotal reports of a decline in HMRC customer service (see page 31 of this CBI report and this from the Chartered Institute of Taxation). It’s not merely that HMRC funding has failed to keep pace with inflation; its most experienced personnel were moved onto other projects, particularly Brexit and the pandemic, and didn’t move back (see paragraph 1.8 onwards in this National Audit Office report). We are also hearing about long-term problems with the quality and length of staff training deteriorating.

It isn’t surprising that it’s small business that suffers the most from these problems.

We’ve talked before about realistic ways that the tax gap could be reduced.

Additional funding is a pre-requisite, but on its own isn’t enough.

We are increasingly hearing about problems with the length and quality of training new HMRC employees receive. Customer service needs to be prioritised. HMRC needs to get back in touch with taxpayers, so it can assist the vast majority that are trying to be compliant, and proactively identify those that are not. HMRC’s approach to investigations and disputes needs to change: right now it often pursues weak and irrelevant cases, cases that are oppressive to taxpayers (and sometimes inexplicable and disturbing) but at the same time misses what’s happening on the ground.

Avoidance and evasion

We are inundated with reports of tax avoidance and evasion – more than we can ever investigate. Most of these are relate to small businesses. Some are “traditional” tax avoidance schemes marketed to small businesses. But a great many involve companies established to act as employers of contract workers, evading or avoiding tax on the workers’ remuneration (usually without the workers’ knowledge). These structures are little more than scams, but there are vast numbers of them, and they make up most of the schemes listed on the avoidance pages on the HMRC website. Our sources at both HMRC and in the tax avoidance “industry” have told us they believe these schemes cost HMRC £5bn each year. And the critical point: these schemes are technically classified as small businesses.

So it’s our view, albeit based on anecdote and sources rather than hard evidence, that much of the growing small business tax gap is driven by remuneration tax avoidance schemes.

Another possibility is that a media focus on tax avoidance by billionaires and multinationals has taken too many headlines, and distracted too many people, from what the majority of tax avoidance and evasion actually looks like. We should follow the data.13

What needs to change

One answer is funding. However, HM Treasury mustn’t just shower HMRC with additional funding; new funds need to be carefully directed and managed. Failures to deliver important cases, or drop bad cases, should be investigated; not to blame individuals, but to find out what, systemically, is going wrong, and how to fix it.

Another answer is having the right tools to attack aggressive avoidance. The recent Government consultation is very promising – but HMRC will need both focus and funding to make any new legislation work.

HMRC’s success in reducing the tax gap over the last 20 years suggest that its failure to close the small business tax gap can and should be remedied. £15bn is an extraordinary sum to lose behind the administrative sofa.

Footnotes

Other figures are sometimes quoted, but they are statistically naive. Richard Murphy produced a figure of £90bn back in 2019, but he did this by adopting a “top-down” methodology which, as HMRC and the IMF (page 46 here) have explained, requires a series of significant adjustments which Murphy does not make. Murphy’s estimate also fails the “smell test”. It requires us to believe HMRC are missing more than 95% of all tax evasion – that does not seem plausible given that HMRC conduct random audits of businesses (absent HMRC being corrupt, which is Murphy’s view). We’re unaware of any tax expert who believes Murphy’s approach is credible, and no country has adopted it. ↩︎

Estimating the tax gap is a very difficult exercise, with numerous sources of error and uncertainty. HMRC does an impressive job to rigorous standards, generally believed to be the best in the world (most tax authorities only produce tax gap figures for VAT, which is a far simpler job given that it can be estimated with reasonable accuracy “top-down” from national accounts data). About ten years ago, HMRC’s homework was favourably reviewed by the IMF, who made various recommendations, most of which have been followed. More recently it was also reviewed by the Office for National Statistics. ↩︎

It’s sometimes said that the estimates ignore offshore avoidance. This is not quite right, and there are two separate points here.

First, our work identified that HMRC does not systematically match up offshore account reporting with self assessment data. But that is different from saying that offshore is not included in HMRC’s tax evasion estimates. At most, HMRC’s estimate may be missing some evasion that would be identified by cross-checking HMRC’s sources of data. If so, the amounts are likely modest.

Second, HMRC’s tax gap does not include areas where something we might describe of as “avoidance” is actually permitted under the rules – for example the “double Irish” structure Google used prior to 2015. So in 2015 it was a very valid criticism to say that the tax gap estimates ignore multinational tax avoidance. However, things have changed since 2015. The many anti–avoidance rules implemented post-2015 make it much harder to see what “avoidance” remains permissible. Even the Tax Justice Network estimates (of which we’ve been very critical) show multinational avoidance costing the UK less than £2bn. This second criticism therefore feels of limited relevance today. ↩︎

Also note that the definition of “avoidance” doesn’t encompass planning that’s clearly permitted by the rules (even if many people wish it wasn’t). So, for example, the big tax advantages for non-doms aren’t a result of tax avoidance – they’re how the rules work. Ditto carried interest, avoiding SDLT on commercial property using enveloping, etc. More on the definition of “tax avoidance” here. ↩︎

Our source for this, and all the data in this article, are the HMRC tax gap tables – see tables 5.2, 5.4 and 5.5. ↩︎

The only other taxes where the tax gap has gone up over this period are inheritance tax (which likely results from so many more estates becoming subject to the tax) and landfill tax (we don’t know why that is; it’s an area where our team has no knowledge or expertise) ↩︎

Overall errors crept up slightly but errors of over £1,000 have been broadly static. ↩︎

This is from table 1.4 of the HMRC tax gap tables. ↩︎

Many thanks to Heather Self for identifying this point. ↩︎

As the figure is based on the HMRC tax gap statistics, it is subject to considerable uncertainty; we cannot quantity the uncertainty (given the lack of quantitative error analysis in the HMRC statistics). ↩︎

About £9.5bn corporation tax and £5.5bn other tax (mostly VAT). We can’t show this directly, as there are no detailed statistics for VAT non-compliance in the tax gap tables, and no figures for VAT revenues from small business in the VAT statistics. But HMRC figures show small business PAYE compliance has dramatically improved, with the tax gap reducing by 2/3 – we expect this is due to the widespread move towards outsourced automated PAYE services. Other taxes are not significant to most small businesses, and so by a process of elimination we can be reasonably confident that most of the non-CT tax gap here is VAT ↩︎

It can seem counter-intuitive that the corporation tax gap is bigger than the VAT gap, not just in this case but generally. Since VAT is 20% of turnover, and corporation tax (in this period) 19% of profit, if someone evades tax won’t the VAT loss be greater? Why is the corporation tax gap bigger than the VAT gap? Primarily because VAT compliance is (broad generalisation) easier than corporation tax compliance. It’s your turnover (if you’re a business that only supplies standard rated products) less your inputs. Corporation tax is much more nebulous – what ends up as your “profit” is often less than obvious. What’s more, VAT is hard to avoid or evade these days – sales to customers are visible; sales to business customers leave a paper trail. There’s an additional factor for small companies that every company pays corporation tax, but only companies with over £85,000 of revenue (in 2023/24) are subject to VAT. ↩︎

Obviously that doesn’t mean HMRC should reduce its efforts to prevent avoidance/evasion by the wealthy and large business, or that we shouldn’t be talking about it. ↩︎

27 responses to “The small business tax crisis: 40% of tax due isn’t paid”

Could some of the employment taxes evasion be occurring in sectors where people work illegally. I’m thinking of illegal immigrants, and people in the UK legally but on visas which state ‘work not permitted’.

We’d need a rough idea of the numbers of illegal workers over time to see if it correlates.

I also wonder if the increase in the minimum wage has made a difference. An employer has to sell an awful lot of stuff every hour, profitably, to pay a new staffer even what the minimum wage plus employment taxes was 4 years ago.

The employment rights bill, if enacted, will further disincentivise legal employment of entry level candidates.

While Making Tax Digital has happened after my retirement, I think the proposals to start quarterly updates for gross annual income of £50,000 (from self-employment and/or property income) from April 2026 may have quite impact as HMRC intend to use quarterly update data to “pre populate” self assessment tax returns. The threshold falls to £30,000 from April 2027 and to £20,000 “within the life of this Parliament”. While the VAT threshhold sits way above at £90,000. But partnerships aren’t yet within MTD. Your thoughts?

Has HMRC proposed any specific strategies or timelines to address the growing small business tax gap?

Do you not think that the wholesale avoidance of employment taxes/NIC by small companies deliberately set up to do so would be better included in criminal activity rather that small business?

very much so!

Dan, having seen both sides of this, I am not convinced a one sentence answer is sufficient explanation.

If you mean those who promote such schemes i would say a definite YES.

Those who have used the schemes, I would say no, yes there is some who knew what they were doing is wrong, but there has been a lot of decent people who were went it to this after been given proper advice, (and this is why penalties against many have never been sought or have failed to have been given).

As a Inspector of taxes once told me some tax avoidance has been legalised (the example he gave me was cash ISA’S – the only ones available at the time).

Human nature within HMRC comes into this. It must be more satisfying for the investigators to prize avoided taxes out of multinationals and the rich than chasing plumbers for the odd few thousand of evaded tax. The latter will add up to a material sum, but will require a vast expansion of investigative expertise (see above for comment on that) and an acceptance that the yield/cost ratio will deteriorate

Is this the tax gap that Making Tax Digital Income Tax is supposed to reduce or is HMRC focusing on the wrong tax gap with is dogged continuation of MTDI?

Interesting analysis. In the context where after waiting for a response for around 6 months I had to get my MP to contact HMRC in order for me to be able to pay a tax bill, it’s not really surprising.

I’m not a statistician and that’s why I’m probably confused. There are 5.5m SMEs in the country, how can HMRC extrapolate anything meaningful from enquiring into a sample of these? I’ve seen figures of circa 300,000 HMRC inspections into SMEs a year, which is presumably across a significant number of taxes, which would fragment any tax specific findings (eg corp tax, PAYE etc).

I’d imagine a large number of these are aspect enquiries rather than full blown tax enquiries too.

statistically a random sample of 400 companies will give you an accurate figure, with a 5% margin of error. It’s how opinion polls work. HMRC has a much larger sample than 400, but they have to make sure it’s representative of companies as a whole, which takes some thought (but isn’t terribly difficult).

See for example https://en.wikipedia.org/wiki/Sampling_(statistics)

one further point i wish to make.

The NAO report states at 1.19 ‘However, new staff typically need up to four years

to become fully effective.’

This I would say from experience is right, however even in my time there these was never told to perspective compliance people (the time considered was 2 years). Now you are finding people getting promoted within 2 years as the norm. Partly because wages have not kept up with the private sector and this is how people get a real pay rise (and yes i did hear this personally said).

This leads to the next point, staff retention, I really would like to know what the % of ‘trained staff’ HMRC are keeping.

In the late teens, HMRC were already having problems retaining staff in the inner city offices, one ‘story’ amongst others I heard at the time was one of the big Accountants was telling perspective employees go and do 2 years at HMRC then come back and have a conversation with us. OK some could say this is a myth, but I can well believe it!

At the end of day I want a tax department that works for everyone.

As a small business owner, I understand the sentiment of the tax gap, based as it is on being taxed from “pound one”, but I don’t understand how white van man shows up in the stats, if he’s operating a cash only system?

One of the other areas of non comp,iance is the “closing the business down just before accounts are due”, which I think is a well known tactic.

In hospitality, (my sector) it already feels as if we’re being milked dry yet we as a sector supply billions to the Treasury.

ah, because HMRC does random audits of tradespeople. So this makes it statistically trivial to estimate evasion across the entire population.

It’s different for people who completely invisible to HMRC (i.e. because they’re *only ever* paid in cash) or people who moonlight in a cash-only job. HMRC calls them “ghosts” and “moonlighters”, and here the uncertainties are much greater.

There is no doubt that HMRC needs more and better resources, not just to deal with the tax gap, but to generally provide the level of service all taxpayers should be entitled to.

However, I would also advocate for a system along the lines of the one used by the French whereby companies have to obtain a Certificate of Tax Regularity, no detail just confirmation that they are up-to-date with their taxes, which has to be presented when bidding for contracts. To address the issue of the small companies not involved in corporate RFP’s, perhaps have such certificates made available via Companies House website for all to see. I suspect that public opinion will be a great motivator for many.

Two thoughts on the uptick. Firstly, there appears to be a void left in the accountancy market as large firms strive to get larger, leaving a gap where businesses can go to for good tax compliance advice. The accountancy profession often acts as the first line of defence for HMRC (Rarely recognized) and smaller practices may not be as strong on this aspect. Then secondly, there is the move to do it all yourself, with the abundance of new accounting and tax packages, increasing the number of unrespresented taxpayers.I wonder if there is any data on this point?

The resaon for the sharp increase isn’t that less tax has been paid, it’s due to the underlying statistical method changing from being projections to using REP data. HMRC: “The Corporation Tax gap for 2019 to 2020 through to 2022 to 2023 has been revised upwards, mainly due to increases in the small businesses Corporation Tax gap derived from REP data. Small business for 2021 to 2022 are now based on REP data rather than being projected from 2020 to 2021.”

If you look at the underlying tables, you will see (Table 5.2) that the non-payment component has gone from 0.1 to 0.3 bn from y/e 2006 to 2024, and that compliance yield has gone from 0.1 to 0.2 in the same period. Those are objectively measurable. But, you will see the Gross estimates dramatically increasing after 2019, inline with the change in methodology.

So, no-one has taken their eye off the ball, the amount of tax loss has not signifiantly increased, the chart merely shows that the method of estimates has changed.

So, the next question would be: “Is the REP method more reliable than the previous method?”

I thought that was a possible answer, but HMRC sources are clear that there absolutely has been a real change.

They used a new way of estimating and then went back and recalculated old numbers using new methods. The estimates have quadrupled in 4-5 years, without any explanation about why other than they are doing things differently when estimating. If there has been real change then it’s not reflected in the objective measurables, which one would expect to change too. HMRC assertions need to be backed up by detail. They have a history of making really poor estimates.

The Post Office also thought their system was infalliable. Look how that turned out.

When I was working in private medical practice, all the big earners were incorporating themselves into personal service companies.

HMRC need to work closely with Companies House (which needs a major overhaul) and look at different professional sectors.

Having left HMRC SME compliance in 2019 under voluntary redundancy I am not surprised one bit about this.

In fact I have been expecting this and this goes back to 2015/16 and the office closure plan and the wrong decision to locate the offices in the major cities, to say senior management weren’t warned would be an understatement.

HMRC refer to 19/20 and 20/21 compliance programme certainly 19/20 there were still local offices open however Brexit was causing real problems for HMRC, 20/21 was pandemic issues and I am surprised much random enquiry work was done.

The point about Revenue training programmes and pushing irrelevant cases is well made and is true.

Only a few weeks ago a former senior colleague (and friend) who still works there stated training now was nowhere near like it was.

Now working in the private sector I can vouch for this as well, some of the replies I see are frankly awful, and people are getting promoted who are not either trained sufficiently lack experience or are capable to so the job.

This on the top of calls not getting answered (yes it has happened to me, wrong advice) and it taking 4 months for CIS refunds to be made.

There is plenty more I could add, as why this has happened, but don’t have the time just now.

I was once proud to have belonged to the HMRC now I feel embarrassed about it, as I said this has been 10 years in the making.

HMRC used to use some of the big boys in the external Tax Training market and some of their people used to study of the ADIT exams. All stopped and in house now which seems very short-sighted.

I’m being dense here. By “tax gap” HMRC are estimating what they think is missing – but based on what data? If I file accounts with Cos House my liability is pretty obvious I would have thought – so I guess they don’t mean this. Perhaps HMRC mean cash in hand, double book keeping and so on…

Any houghts pls?

HMRC conducts random audits, and that lets them estimate overall levels of most types of avoidance, evasion and non-compliance with great accuracy.

The exception is stuff that isn’t picked up in random audits….

This 2017/18 explosion coincides with the office closure programme. Many experienced staff were lost to redundancy at vast expense to the department and replaced with youngsters without a tax background. The loss of experienced coaches, mentors, trainers and tutors also meant that there was nobody to bring the newcomers up to standard.

Thank you for the information, the graphs are very clear. Perhaps the scam tax firms should be classed as criminal, they are.