Last year we revealed an inept and dangerous landlord tax avoidance scheme promoted by Property118 and Cotswold Barristers. They responded with a weird campaign of denial, threats and abuse. HMRC then started to investigate, but Property118 didn’t tell their clients. HMRC’s conclusion? Property118 had unlawfully failed to notify HMRC they were promoting a tax avoidance scheme. Property118 and Cotswold Barristers’ response? Telling their clients this is a normal procedure for “innovative tax arrangements” and nothing to worry about.

UPDATE 16 February 2024: Property118 have published a defence of their position. Per their usual practice, the article doesn’t contain a single reference to legislation, just a series of irrelevant quotes from HMRC manuals. Competent tax advisers always start with the legislation. HMRC guidance can sometimes be of assistance, but it’s not the law, and legally and practically cannot be relied upon. What you certainly can’t do is try to reach your desired result by citing HMRC guidance as if it’s legislation.

UPDATE 11 July 2024: Property118 are appealing against HMRC’s two DOTAS notifications, expect to have to appeal against discovery assessments, and are asking their clients to make donations to fund their appeals. Property118 aren’t telling their clients what their KC has said about their prospects of prevailing – we expect those prospects are very poor. And on 18 July 2024, HMRC issued a stop notice.

Property118 run a popular landlord website and sell a series of incompetent tax avoidance schemes. Nobody at Property118 has any tax expertise, and they rely heavily on a peculiar barristers chambers (“Cotswold Barristers”) who also appear to have no tax expertise.

We published a report on Property118 back in September saying that their scheme didn’t work and, worse, could default landlords’ mortgages. UK Finance, the mortgage lenders’ industry body, agreed.

We subsequently discovered an even worse element to Property118’s scheme that involved throwing lots of money around in a circle and claiming it created a big tax saving – generating a total of £500k+ in “fees” to a YouTuber who then extensively promoted Property118 without revealing his financial interest.1 And then we went through Property118 client files and found a series of serious errors, as well as evidence that Cotswold Barristers was just “rubber-stamping” standard form advice without giving it any independent thought.

Property118’s initial response

Most of the tax avoidance scheme promoters we’ve reported on simply refuse to comment, and hope that if they stay silent then everything will work out.2

Property118’s response was very different.

- They responded aggressively to our requests for comment, and seemed angry that we wouldn’t accept a recorded Zoom call instead of correspondence.

- They then invited me for a drink.

- Next, they hired a tax KC to provide an opinion that their scheme worked. More conventional types would have hired a KC who says any old avoidance scheme works. Property118 instead hired a reputable KC, but asked her to advise on largely irrelevant questions instead of the ones that mattered. In particular: was the mortgage defaulted? Was this a tax avoidance scheme that should have been disclosed to HMRC under the “DOTAS” disclosure rules? Did anti-avoidance rules apply? What did Property118’s ineptly drafted documents actually do? None of this was covered.

- They instructed a law firm to send us a summary of the KC’s opinion, demand we retract our report, say we weren’t permitted to publish the summary, and threaten to sue us for libel. We published the opinion and our analysis of it. We weren’t sued.

- The law firm involved didn’t realise what they’d gotten themselves into; soon after we responded, either Property118 sacked the law firm for being sensible, or the law firm sacked Property118 for being bonkers (we don’t know which it was) .

- They then made a series of weird, conspiratorial personal attacks on me, complete with spooky AI generated pictures. They accused me of being unqualified, and said that the many other advisers critical of Property118 were acting out of jealousy for not having thought of these brilliant ideas themselves.

- Property118 then referred me to the Solicitors Regulation Authority for being mean to them. I’ve heard nothing further about this – I’d hope the SRA see the referral as an obviously vexatious abuse of the regulatory process to retaliate against a critic.

- And finally there were a succession of supposed technical responses to our reports, none of which actually engaged with the substance of what we had said. The peak of this was an article by Mark Smith of Cotswold Barristers claiming that DOTAS didn’t apply🔒 (since deleted; this is an archived version), which would be disappointing if handed in by a work experience student.

- Then, at some point in November 2023, Property118 went silent, and deleted their main technical response.

Why did they go silent? Because HMRC had started to act.

HMRC investigates historic incorporation relief claims

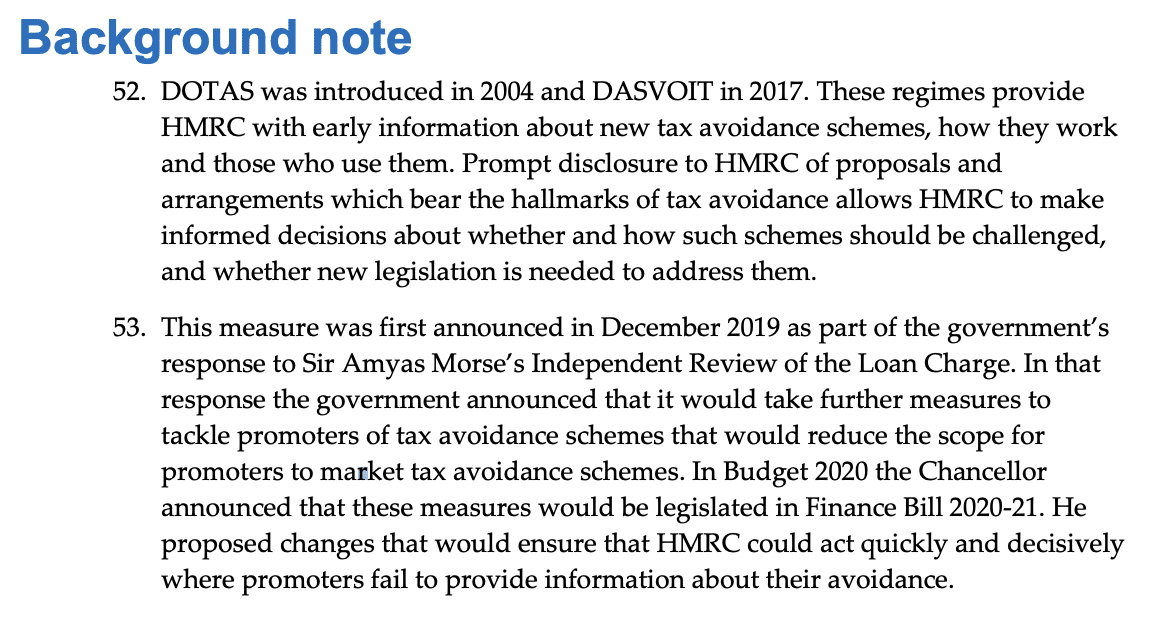

On 16 November 2023, HMRC announced that they’d started to investigate incorporation relief claims from as far back as 2017/18.3. “Incorporation relief” is a tax relief that Property118 relied upon to move landlords’ properties into the structure without capital gains tax. However they got the details badly wrong.

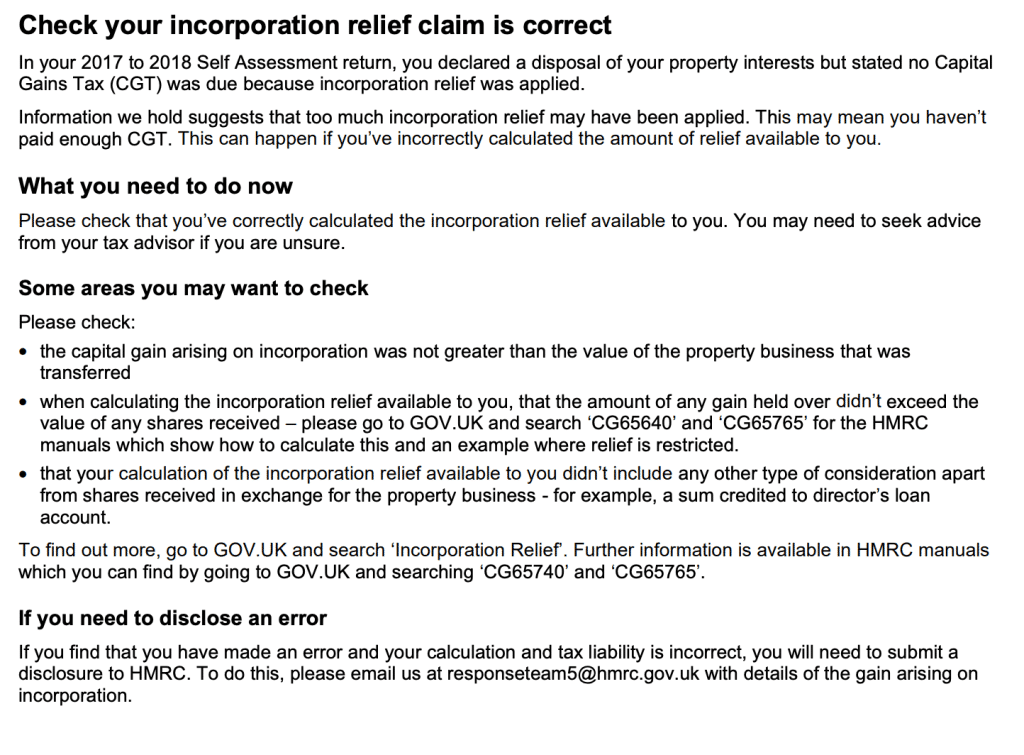

Here’s the key part of a letter which HMRC sent to taxpayers:

It’s the third bullet here which kills the Property118 scheme. Property118 create a director loan through a very peculiar circular arrangement. This means that some capital gains tax will always be due, as CGT will be charged on the proportion of the sale consideration that isn’t shares.4 From the client files we’ve reviewed, it seems Property118 did not appreciate this, and told their clients there would be no capital gains tax at all.5

HMRC concludes it’s a notifiable avoidance scheme

It was always reasonably clear that Property118’s schemes should have been disclosed to HMRC under DOTAS – the rules requiring disclosure of tax avoidance schemes. Property118’s denials of this revealed only that they and Cotswold Barristers had a very poor understanding of the rules. Ray McCann, who when at HMRC led the launch of DOTAS, described their responses as “hopelessly wrong“.

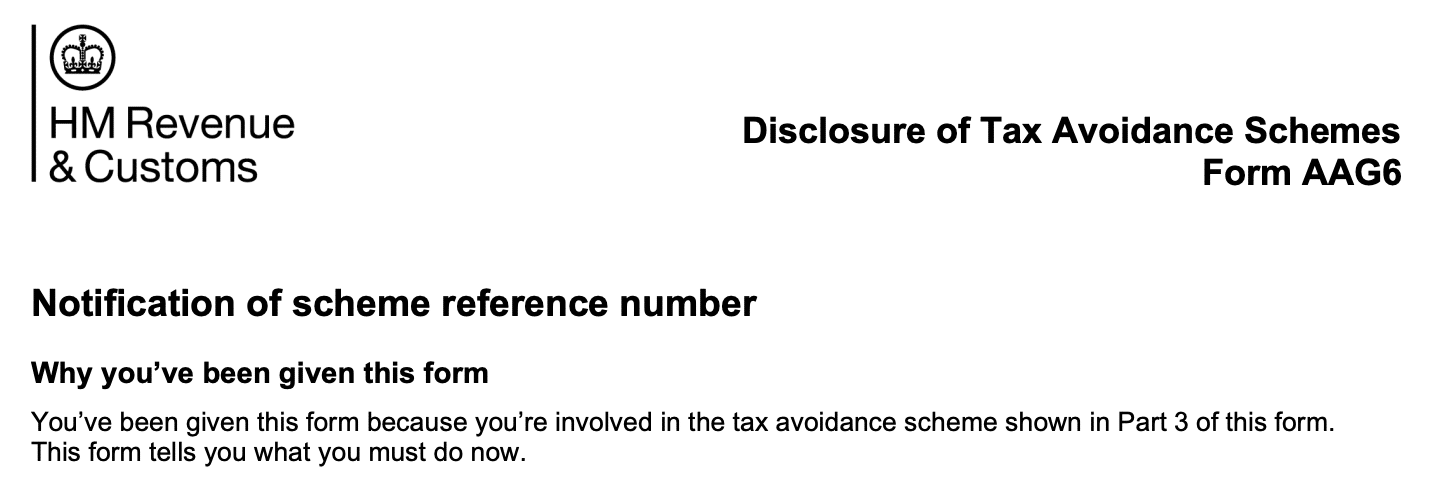

HMRC clearly agreed. They sent a formal notice to Property118, saying HMRC had reasonable grounds to suspect that Property118’s incorporation structures, and its circular funding structure, were notifiable under DOTAS. Property118 then had 30 days to try to satisfy HMRC that the arrangements were not in fact notifiable. Property118 failed to do that and, as a consequence, HMRC issued Property118 with two tax avoidance “scheme reference numbers“. 6

The rules then require Property118 to notify their client of the scheme names and reference numbers and provide this form7

How did Property118 explain this to their clients?

This all created a bit of a problem for Property118. Having been adamant that they weren’t selling a tax avoidance scheme, and that they got on splendidly with HMRC, they now have to send to clients a somewhat scary form that starts like this:

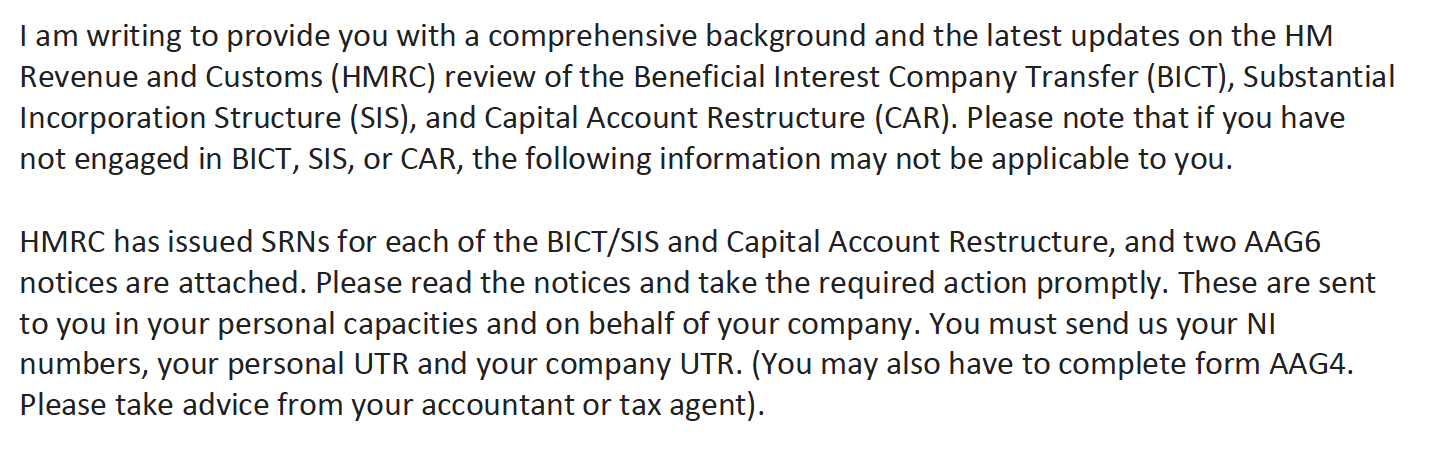

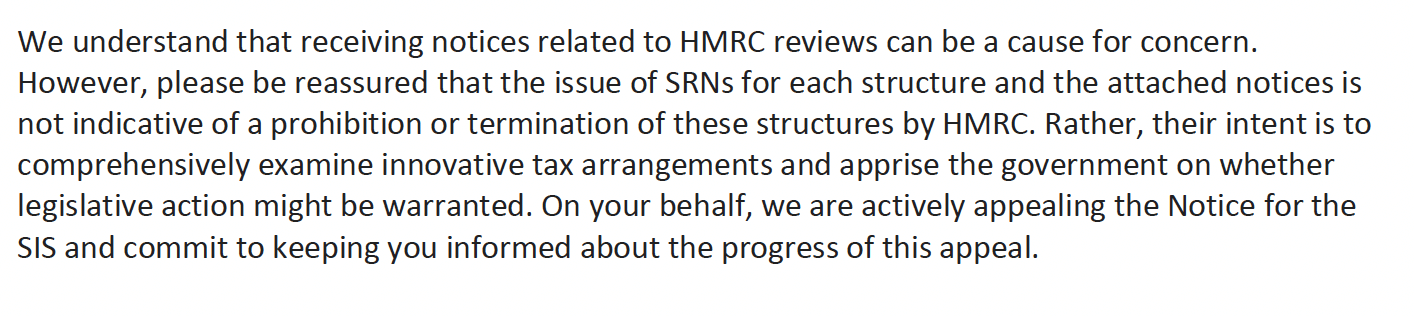

Property118 and Cotswold Barristers should have clearly explained what had happened, and what it means for their client. Instead they decided to mislead their clients with an email which manages not to mention the terms “avoidance” or “DOTAS”:

What is an SRN? What is the required action? Why did this happen? Cotswold Barristers don’t say. We’ve uploaded a full copy of the email here.

“You may have to complete form AAG4” is exceptionally unhelpful. Cotswold Barristers should be saying to their clients who used the schemes for past years that they will have to submit this form.

Instead, Cotswold Barristers provide reassurance which is comforting, sympathetic, and completely wrong:

No, the intention of DOTAS is not to enable HMRC to “comprehensively examine innovative tax arrangements”. It’s to enable HMRC to discover tax avoidance schemes as soon as they’re used, so it can decide whether to challenge them and/or ask the Government to enact legislation closing any loopholes. 8 This is well known to all practitioners, and was restated when DOTAS was amended in 2021 to enable SRNs to be issued to rogue promoters:

Anyone reading this will realise the truth: that it’s now likely that Property118’s clients will be the subject of HMRC enquiries, and face large tax liabilities, plus interest and potentially penalties.

It’s sweet that Property118 are appealing HMRC’s decision that the “substantial incorporation structure” is disclosable (good luck with that), but that suggests even they can’t defend the circular “capital account restructure”.9

So why did Cotswold Barristers and Property118 provide that those empty, sympathetic and wrong words of reassurance?

In other circumstances we’d say it’s deliberate deception, but we believe Cotswold Barristers and Property118 are simply unqualified and unable to advise properly on tax.

But whether it’s fraud or haplessness, the question is whether a barrister is permitted to act in this way. That is something we’ll be returning to soon.

Thanks to everyone who contributed to the original Property118 article, particularly those who were happy to be credited by name (when they knew Property118’s reputation for bullying and abuse).

“This is fine” cartoon © KC Green, and used with his kind permission.

Footnotes

We are shocked to find unethical behaviour by YouTubers, particularly in the landlord real estate world. ↩︎

It generally doesn’t. ↩︎

Because, at the time, that was the furthest HMRC could go back. It’s a kind of triage, first attacking the oldest periods, and then (when they’re done and have time) moving onto the newer ones. The approach is absolutely rational for HMRC, but has the considerable disadvantage for taxpayers that it can be years before your avoidance scheme is challenged. The answer is: don’t do avoidance schemes. ↩︎

It’s very clear in this HMRC example. ↩︎

Our analysis goes further, and says that there are several good reasons to believe the Property118 scheme is completely disqualified from incorporation relief. We expect HMRC will take these points, in the fullness of time, but for now is applying the much easier calculation point, given that it’s just arithmetic. ↩︎

As an aside, there is a rather odd paragraph in the Finance Act 2021 legislation that created the new notice procedure. Subsection 311(9) says: “The allocation of a reference number to arrangements or proposed arrangements is not to be regarded as constituting an indication by HMRC that the arrangements could as a matter of law result in the obtaining by any person of a tax advantage”. Of course the intention is to stop promoters using SRNs as badges of approval from HMRC, but quite what the legal effect is of the subsection, we have no idea. Possibly it has none; possibly it would assist in fraud proceedings against dishonest promoters who did try to use SRNs as promotional material? ↩︎

The version of the Regulations on legislation.gov.uk is unfortunately out of date; however the subsequent amendments aren’t material to the scenario discussed here. ↩︎

DOTAS also means HMRC can, after issuing the SRNs, use its new powers to require Property118 to provide further information about their scheme, including documents and names of clients. We expect this will happen soon, if it hasn’t already ↩︎

It looks like at some point they changed their mind, and decided to appeal that too; quite hard to see what the basis for this will be. ↩︎

TikTok tax avoidance from Arka Wealth: why the Government and the Bar should act

Witness tampering from tax avoidance firm Property118?

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Tax barristers and fraud: how the Bar responded to our allegations

Leave a Reply