This is a version of the article published by the Sunday Times on 1 January 2023 – it summarises some of the themes I wrote about in 2022, and some more that I’ll be writing about in 2023.

Kwasi Kwarteng’s “fiscal event” last September was widely perceived as a disaster, but at its heart was a kernel of undoubted truth: there are features of our tax system that discourage growth — and we should fix them.

Here are five.

Income tax marginal rates over 60%

The boldest, and most criticised, element of the Kwarteng mini-Budget was to scrap the 45p top rate to “simplify taxes” and “incentivise growth”. The problem with this is that, even if you accept the premises of Kwarteng’s position, 45p is not even close to the highest marginal tax rate in the UK.

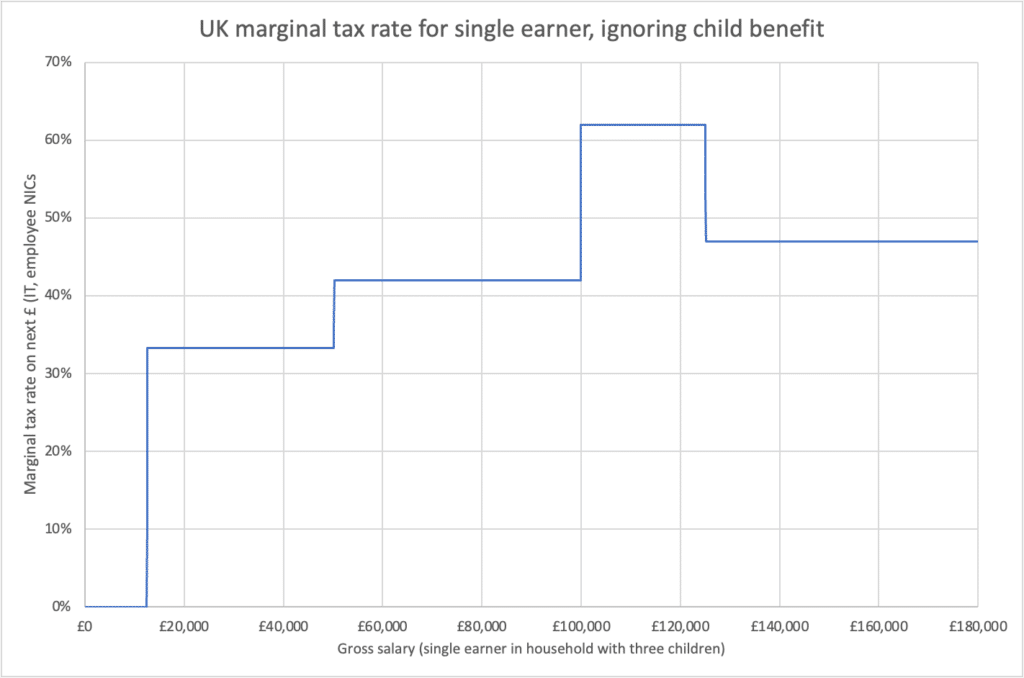

The marginal tax rate at any given income is the tax rate you pay on the next pound you earn. That’s crucially important, because it affects your incentive to earn that extra pound.

I’ve charted the marginal rate of income tax and employee national insurance for different incomes, and it looks like this:

This should immediately start ringing alarm bells. Why do the comfortably-off (£100-120k) pay a higher marginal rate of tax – 62%! – than those on really high incomes? Because at point the personal allowance starts to taper away – with every £1 of income earned about £100k, the personal allowance reduces by 50p.

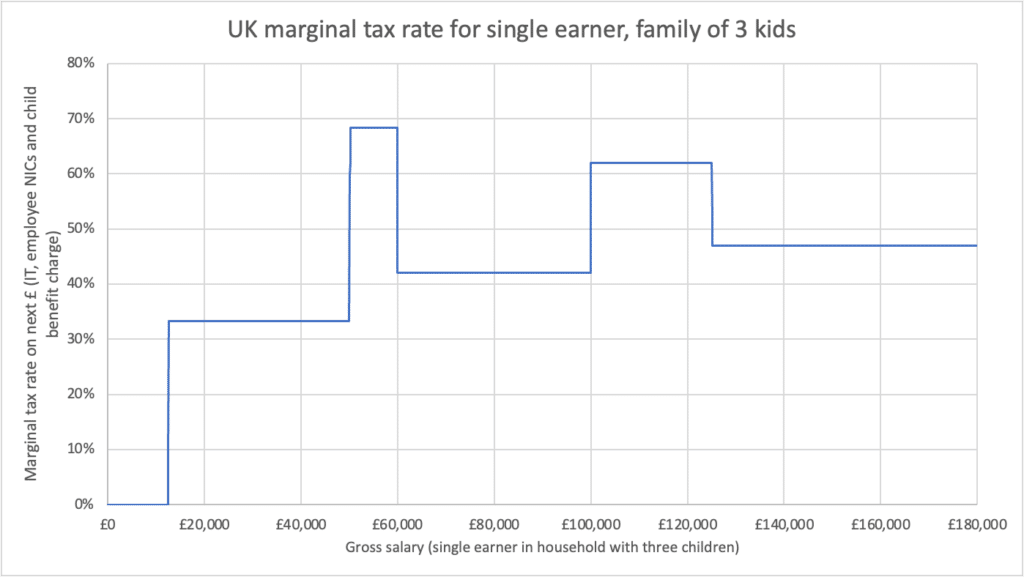

But we’re only getting started. What if you have three children all qualifying for child benefit? Well…

Child benefits starts to be withdrawn at £50,000 – resulting in a marginal rate of 68% between £50k and £60k.

Sad to say, we can make even that result look good if we throw in the effect of the Government’s much-heralded “tax free childcare” scheme. This entitles you to up to £2,000 per child. The catch is that it completely disappears if your earnings hit £100k. A couple can each earn £99,000 and they keep the benefit; but if one earns £100k they lose it (even if the other earns nothing).

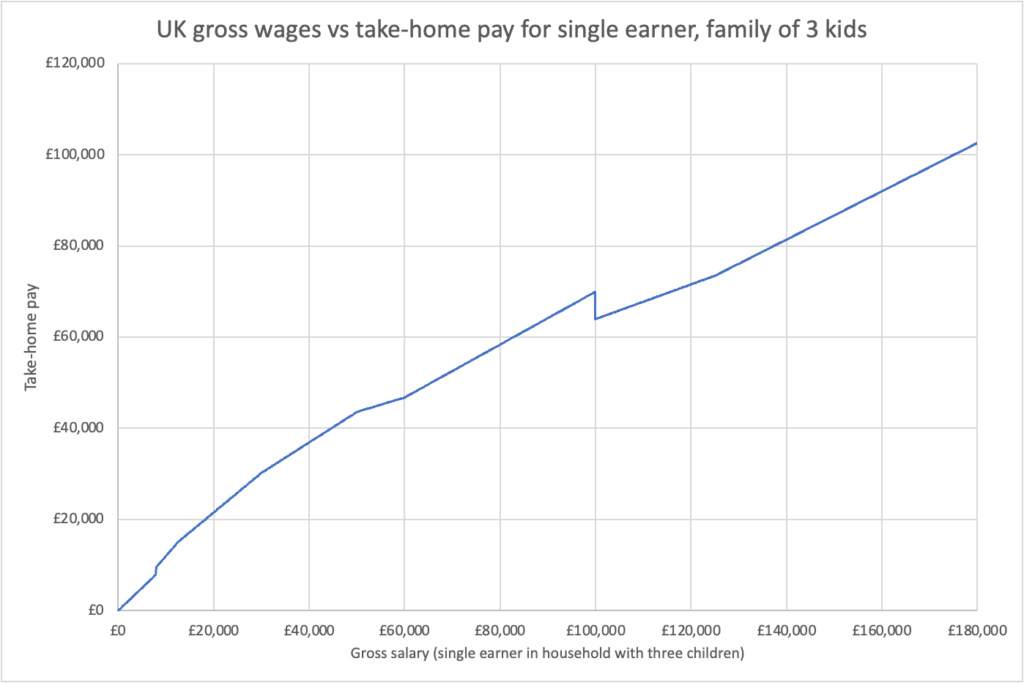

What marginal tax rate is that? Well, if you’re claiming tax-free childcare for three children, and currently earn £99,999, your take-home pay is £69,884. Earn £1 more, and your take-home pay is less – £63,942. That’s an infinite marginal tax rate, so slightly tricky to show in a chart. Instead, here’s a chart of gross vs net wages:

The ”dip” at £100k shows the drop in post-tax income, which isn’t recovered until you earn £20,000.

Put all of this together, and what does it mean?

It means that people who can control their hours usually think very carefully before putting themselves in the £50-£60,000 bracket, or the £100-£125k bracket.If they’re employed, they often make additional pension contributions, use salary sacrifice schemes, or find other ways to earn the money, but not pay tax on it. If they’re self-employed they often just stop working for the year. These are not good things for the UK economy.

And, worse still, all these tapering effects are triggered by one person’s income hitting the £50k/£100k trigger points. That means that the Smiths (who each earn £60k) are much better off than the Joneses (where she earns £120k, and he stays at home). The Smiths take home £93k after tax; the Joneses £75k. There are many reasons why the Joneses may have chosen that one of them should work and one not – it’s mystifying why the Government should slap an £18k penalty on their choice. The irony is that these accidental tax effects are so much larger than the deliberate tax policies Governments announce with much fanfare – the “marriage allowance” is worth a fairly pathetic £252/year.

Why isn’t there outrage about this? I think in part because people earning £50k or £100k feel it’s ungrateful or, worse, unBritish to complain about paying tax. And people earning less don’t want to hear the complaints. But it’s not about whether people on high incomes should pay more tax – it’s about whether they should pay more tax in a fair rational way, or in an unfair irrational way.

So a truly reforming Chancellor would declare war on marginal tax rates above 50%. We can do this without giving a handout to people on high incomes – the cost can be recovered by slightly increasing the top rate of tax. And the cost may be less than the Treasury historically thought, given that people are currently going out of their way to avoid paying these rates. And those on benefits also face ridiculously high marginal tax rates of up to 96% as benefits are withdrawn, creating a perverse incentive not to work (there’s outstanding work on this from the Resolution Foundation here).

Here’s the political challenge: politicians on the Right have to accept slightly higher taxes for some high-earners, and politicians on the Left have to accept slightly lower taxes for some others. Will they?

VAT punishing small businesses for growing

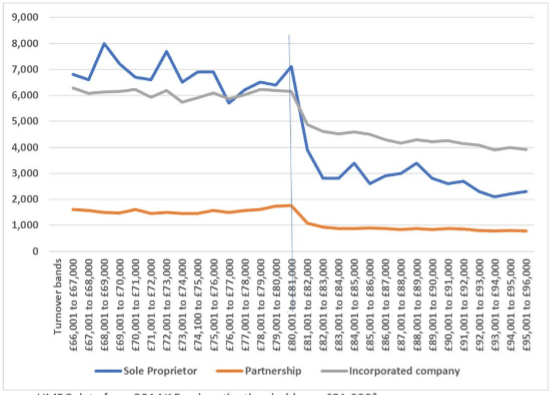

This chart should keep the Chancellor up at night:

It shows, for a given £ of turnover/revenue, how many businesses there are in the UK at that level of turnover/revenue.

You’d expect a reasonably smooth curve, falling from a large number of small businesses on the left side, down to a smaller number of larger businesses on the right. But we don’t see that at all – we see a dramatic cliff edge right on the VAT registration threshold (now £85,000). Businesses whose revenue hits the threshold suddenly have to charge VAT, meaning that – overnight – they must either raise prices or lose profits by up to 20%.

The chart tells us that many businesses respond to this by suppressing their turnover so it never hits £85,000. A cynic would say that they do this by taking cash under the table, and not telling HMRC. But there’s recent academic evidence that the cynic is wrong – this isn’t dodgy bookkeeping… businesses are genuinely holding back their growth as they approach the £85k threshold. The data is compelling, but I hear plenty of first hand stories too – plumbers going on holiday for the rest of the tax year; electricians not hiring an apprentice; coffee shops deciding not to open up another branch.

So here’s powerful evidence that the UK tax system has created a powerful brake on the growth of small companies…. some of which might, in time, grow into large companies.

There are two bad answers to this problem, and one good but difficult one.

The first bad answer is that we should raise the threshold from £85k. This is crushingly expensive, and doesn’t solve the problem… it just moves it.

The second bad answer is that the UK has one of the highest VAT thresholds in the world, and we should reduce it to the average (around £30k). Given the sudden impact that would have on tens of thousands of businesses, this would require a Chancellor to be brave-bordering-on-suicidal.

The good – but difficult – answer is that we shouldn’t have this kind of cliff edge threshold at all. And apps and digitalisation mean that now we don’t need to. Instead of VAT suddenly applying at 20% at £85k, what if it applied at 1% at £30k, and then slowly crept upwards, hitting 20% at £140k? We’d collect the same amount of tax, but without creating an incentive to stop growth.

Until recently, expecting anyone to operate a system like that would’ve been delusional, but the modern digital systems HMRC has put in place make it achievable. It would take years of planning, with HMRC having to provide free apps and compliance solutions to small businesses. The challenge is less technical and more political – politicians have to sell, and voters to accept, the idea that raising tax is necessary for growth.

Three dysfunctional land taxes

We have three taxes on land in the UK – council tax, business rates, and stamp duty. Three parts of a very broken puzzle.

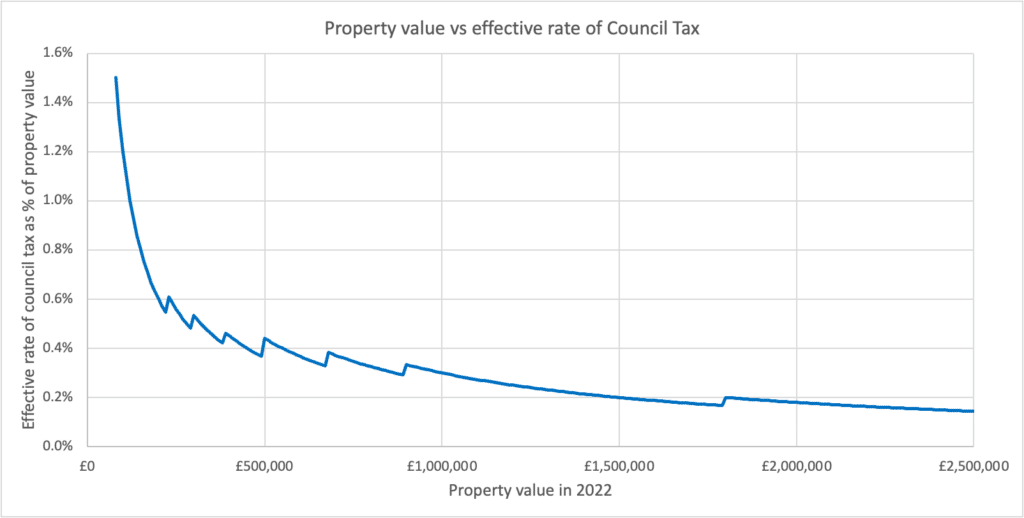

Here’s a chart showing how much council tax is paid as a % of the value of a property:

The more expensive the property, the less significant council tax becomes. That’s not how any tax should work. And in England, council tax is based on 1991 valuations that bear little relation to the housing market today.

Almost as bad is the equivalent tax for businesses – business rates.

The most common criticism of business rates – that it’s an unfair tax on retail businesses – is wrong. All the evidence shows that, in the long run, most of the economic burden of business rates falls on landlords (because rents are lower than they would be if business rates didn’t exist).

But there are other big problems with the tax. It’s based on the “rentable value”, but the rentable value is so frequently updated that you can end up with a situation, where rents have fallen, and the business rates haven’t caught up (which is in many cases where we are now). Another problem: business rates are taxed on the rental value of a property, taking into account whether it’s been improved. That’s a disincentive to invest in improving property. The answer?

And the final broken puzzle piece: stamp duty. It’s a good rule of taxation that we shouldn’t be discouraging transactions. Yet, as everyone who buys a house knows, that’s exactly what stamp duty does. It distorts the housing market and, by punishing people for moving in search of work, distorts the labour market too.

How can we solve the land tax puzzle? By scrapping all three broken taxes and replacing them with land value tax – an annual tax based on the unimproved value of land. Instead of acting as a brake on investment, it would encourage it. Moving house would become a tax-free event. The economic burden would fall on landlords, not tenants.

Land value tax has political support from economists across the political spectrum – all we need are politicians with courage to sell the idea that if we want to repeal bad unpopular taxes, then we have to create new, better, ones.

Corporation tax

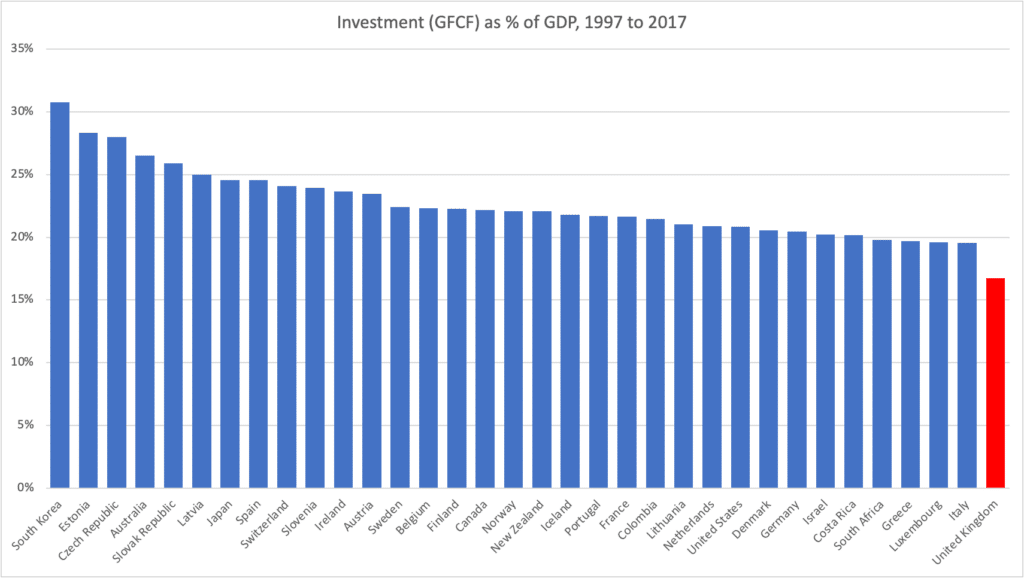

According to the Office for National Statistics, from 1997 to 2017, the UK had the lowest level of investment (as a proportion of GDP) in the OECD:

Is tax one of the reasons behind this?

It’s trite economics that businesses do things they’re incentivised to do. The problem is that UK tax relief for investment exhibits the two deadly sins of tax policy: it’s really complicated, and it changes all the time. This means that you’d have to be brave or foolish to make long term investment plans on the strength of today’s tax relief rules – you can’t be sure you’ll qualify, and you certainly can’t be sure the rules will be the same when your investment actually comes to fruition. Which is another way of saying that the tax relief rules fail to achieve their purpose of incentivising investment.

We need a radical solution. What if we didn’t have complicated rules governing what kinds of investments get tax relief, but just gave tax relief to all investment? Paid for by increasing the rate of corporate tax, so the reform was tax-neutral overall. And guaranteed to remain unchanged for the length of a Parliament – ideally with cross-party agreement that gives reasonable assurance for the longer term. Suddenly we’d create a powerful incentive to invest, made all the greater by the increased tax rate.

This isn’t my invention – it’s called “full expensing” and it’s supported by the CBI and economists across the political spectrum. But we’d need politicians – and voters! – to accept the counterintuitive truth that sometimes tax rates have to go up to encourage growth.

None of these issues are new. The Office of Tax Simplification has proposed reforming most of them. The problem has been that politicians prefer to duck difficult questions. Instead of adopting the OTS’ proposals, the Truss Government abolished the OTS. Let’s hope that, in an outbreak of Christmas cheer, Mr Hunt reverses that mystifying decision.

Photo by CHUTTERSNAP on Unsplash

Is VAT stopping 26,000 businesses from growing? More on the VAT growth brake.

Why VAT may be a brake on UK growth, and how to fix it

A modest proposal for a new tax

New data suggests Scotland’s 48p tax rate may be losing money

John Healey should cut National Insurance, not raise the personal allowance

Leave a Reply