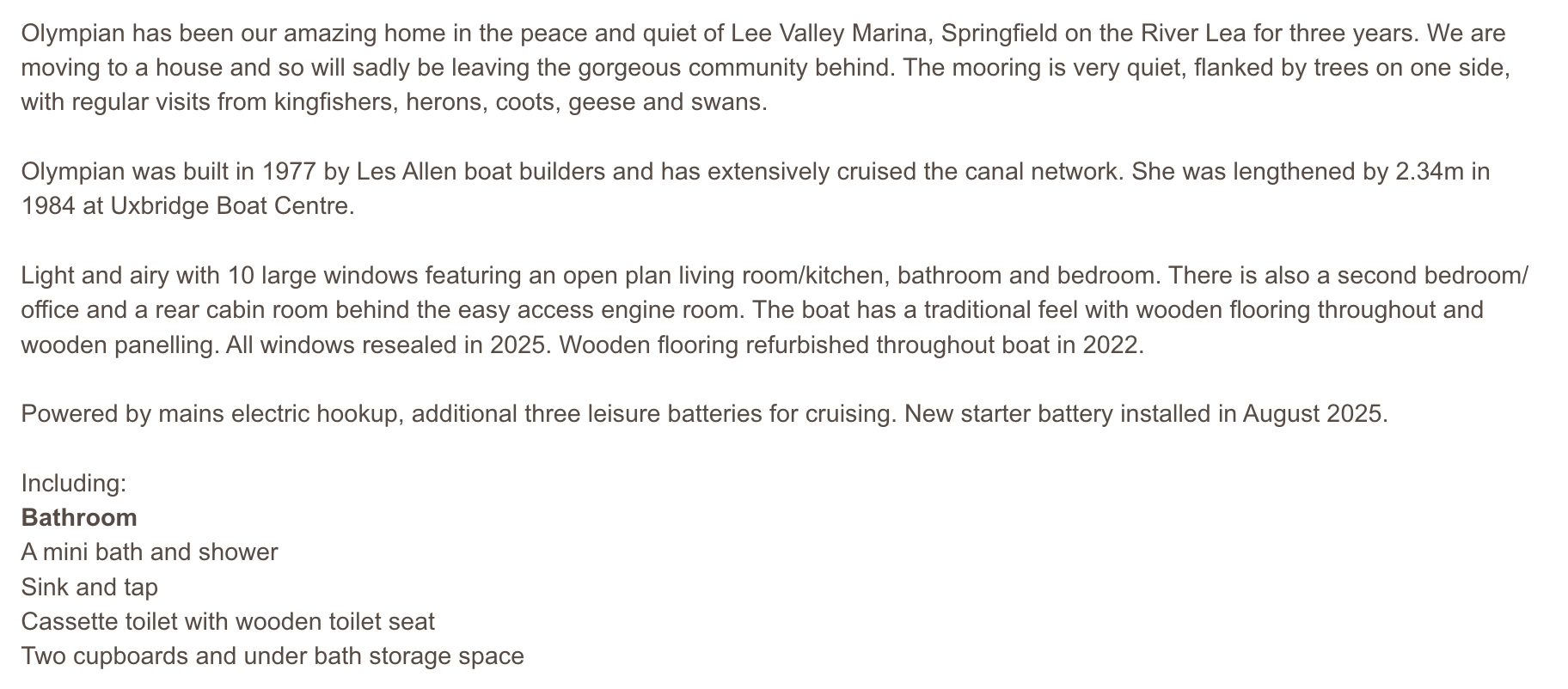

Zack Polanski and his partner lived on a boat for three years, and described it as their “amazing home”. Mr Polanski was registered to vote at a nearby bungalow. If, as seems likely, that was his main residence, then Mr Polanski and his partner should have paid council tax there – but they didn’t. Mr Polanski’s team says he only stayed at the boat “occasionally” – but if that’s true, then registering to vote at the bungalow may have been a criminal offence.

The background

The Times has reported that the Green Party leader and his partner “appear in recent years to have stayed on a narrowboat at a marina”.1

If the boat was in fact Mr Polanski’s “sole or main residence” then he and/or his partner should have registered for, and paid, council tax for those three years.

They recently advertised the narrowboat, which was berthed at the Lee Valley Marina. The advertisement said it had been their “amazing home” for three years:

The other key facts, as established by The Times, other newspapers, and our own investigation:

- Mr Polanski was registered to vote at a bungalow next to the Marina. Nine people were registered at that address – most of them didn’t live there, but lived on boats moored at the marina, and used the bungalow as a postal address (presumably given the practical difficulty of getting post delivered to a boat).2

- Mr Polanski is currently registered to vote in Hackney, but doesn’t appear to have been registered there during the three years he owned the boat – at that time he was solely registered to vote at the marina (which is in Waltham Forest3).

- He told The Times that he rented a room as a lodger at an unstated other property (believed to be in Hackney).4

- A local launderette collected Mr Polanski’s laundry every two-to-three weeks (and local sources have told us that it was an amount of laundry suggesting regular occupation, not just occasional visits).

- We understand from local sources that Mr Polanski was frequently seen in the area around the marina.

- Another narrowboat at the marina was at one point registered for council tax. Mr Polanski’s boat never was.5

Polanski’s team originally gave two responses.

First, they said that he “stays there only occasionally”. That contradicts the other known facts. It also suggests Mr Polanski breached electoral law, by registering to vote somewhere where he was not in fact resident. That’s potentially a criminal offence. We don’t think that’s what happened – we think his team misled The Times.6

Second, they said that Mr Polanski’s council tax is “included in the rent he pays his landlord” of a house (believed to be in Hackney) where Mr Polanski was a lodger. That’s irrelevant – whether Mr Polanski agrees to contribute to someone else’s council tax because he’s renting a room is irrelevant to whether he personally owes council tax on the narrowboat. If you have your main residence at one dwelling, and an arrangement to live in another, then council tax may be due on both.7

The evidence therefore suggests to us that the boat was Mr Polanski’s main residence, and he and/or his partner should have registered for, and paid, council tax.

Mr Polanski’s spokesperson refused to tell us whether it was still his position that he stayed at the boat “occasionally”, even after we said that suggested a criminal offence could have been committed. All they would tell us was:

“Zack denies any wrongdoing. Houseboat living comes with its own unique circumstances and practical considerations. Zack is consulting with his legal advisers.“

What if Mr Polanski really did stay there only occasionally?

We should say at the outset we think Mr Polanski’s team misled The Times and he didn’t really stay at the boat “occasionally”.

But if he did, then he has a different problem. To get on to the electoral roll you have to sign a declaration that you are resident at the address you give.8 To be “resident” requires “a considerable degree of permanence” – sleeping there, keeping possessions there, and treating it as a home.9 Staying somewhere “occasionally” is the opposite of that.10

So if Mr Polanski’s team is right that he was only there “occasionally”, then the declaration he signed to get on to the electoral roll at the marina was false – and knowingly or recklessly giving false information on an electoral registration application is a criminal offence, punishable by a fine and up to two years in prison.11 That is a much more serious problem than a council tax bill. It is also why we don’t believe the “occasionally” line: the obvious reading of the evidence is that the boat was Mr Polanski’s home, his electoral registration said as much, and the only thing he got wrong was the council tax.

How council tax applies to boats

The short answer is that if the boat was Mr Polanski’s sole or main residence then it should have been registered for council tax, and he and/or his partner should have paid council tax for three years. We think most people would expect council tax to be payable if you live on a permanently moored boat. That intuition is correct – but the way that the tax applies in such a case is surprisingly complex.

Council tax is a tax on dwellings, not a tax on people for being in a local authority area. Whether a boat is a “dwelling” depends on a chain of provisions in the Local Government Finance Act 1988 (LGFA 1988) and the Local Government Finance Act 1992 (LGFA 1992).

The basic charge is in section 1 LGFA 1992.

A “dwelling” for council tax purposes is broadly anything that would have been a “rateable hereditament” under the General Rate Act 1967, but is now domestic property and not on the non-domestic rating list: section 3 LGFA 1992.12

The key provision is section 66(4) LGFA 1988. It reads:

“Subsection (1) above [which defines domestic property] does not apply in the case of a mooring occupied by a boat, but if in such a case the boat is the sole or main residence of an individual, the mooring and the boat, together with any garden, yard, outhouse or other appurtenance belonging to or enjoyed with them, are domestic property.”

So both the mooring and the boat become domestic property – but only if the boat is somebody’s “sole or main residence”.13

If the boat is not anyone’s sole or main residence, none of this applies. The marina’s berths sit in the marina operator’s non-domestic rates assessment, the boat owner pays their mooring fee, and there is no separate council tax bill on the boat.14

There are therefore two key questions:

First: is the mooring sufficiently fixed and exclusive to be a “hereditament” – i.e. a unit of property capable of being separately rated?

Second: is the boat the occupant’s “sole or main residence”?

If the answer to either is “no”, there is no council tax dwelling. If both are “yes”, the mooring and boat together are a council tax dwelling, and somebody is liable to pay the bill.15

The first question is straightforward in this case. We understand that the boat was moored at the marina for three years. It is therefore clear from the caselaw that it is an “hereditament”.161718

Was the boat Mr Polanski’s “sole or main residence”?

The concept of “sole or main residence” is not defined in legislation. The leading case, Williams v Horsham District Council, established the rule that a person’s main residence will be the dwelling that a reasonable onlooker, with knowledge of the material facts, would regard as the person’s home.

A series of cases have looked at various factors:19

- Where the person actually sleeps, and how often.

- Where the person’s partner or family lives.

- Where the person’s possessions are kept.

- Where post is delivered.

- Where the person is registered to vote.2021

- Where the person is registered with a GP and dentist.

- The address used for banks, HMRC, DVLA, employer, and other official purposes.

- Security of tenure at the various properties.

- Length of time at each property.

- Whether the person describes the property as their home in correspondence, marketing material, social media, etc.

No one factor wins by itself. The combination is what a “reasonable onlooker” considers.22

Note that the legality of the occupation is not a factor. This was a “leisure mooring”, and so the fact Mr Polanski resided there may have been a breach of his contract with the marina, and/or a breach of planning control. But if there is residential use then council tax applies, regardless of whether that use was lawful.23

Then looking at the factors: we know Mr Polanski and his partner spent a considerable amount of time on the boat, and described it as their “home”. We know that he was registered to vote at the marina, and nowhere else. We know he had post delivered there, and had possessions there.

We can’t exclude the possibility that he actually spent more time at his lodgings, but on the basis of the available evidence, and the fact that Mr Polanski is refusing to comment, it seems to us that, on the Williams test, the reasonable onlooker would conclude the narrowboat was their home. If that is correct, then Mr Polanski and/or his partner should have registered for and paid council tax.24

What happens next?

If the boat were the sole or main residence of Polanski (or his partner) for three years, then on the analysis above the boat and mooring should have been entered in the council tax valuation list, and council tax should have been billed. The local billing authority is the London Borough of Waltham Forest.25

In practice, councils have a standard process when they discover that someone has been living in an un-banded dwelling for several years and not paying council tax. First the boat and mooring are added to the valuation list by the Valuation Office Agency (VOA)26; then Waltham Forest issues backdated demands. 27

We expect the boat and mooring would be in Band A28, meaning a total council tax for three years of around £4,000.29

Most UK taxes have tax-geared penalties if a taxpayer was “careless”. We think Mr Polanski probably was “careless” – he lived somewhere without, it seems, ever considering if he should be paying council tax. However that is not relevant – council tax penalties do not turn on whether someone was “careless”. There is simply a fixed £70 penalty if someone fails, without reasonable excuse, to notify the council of a matter affecting their council tax liability. No interest is charged on overdue council tax.

Discussions of politicians’ tax mistakes are often accompanied by calls for police investigations and prosecutions. In this case, and most others, such calls would be misplaced. There is no reason to believe that Mr Polanski’s failure to pay council tax was intentional or dishonest. Questions of criminal tax evasion therefore don’t arise. However we would note for completeness that there appears to be no criminal offence attaching to failure to register a property for council tax (unless accompanied by a failure to respond to a council information request, or a false statement of some kind).30

There is a specific criminal offence under section 106 of the Local Government Finance Act which applies if a member of a local authority votes on council tax matters at a time their council tax payments are overdue by two months or more. Mr Polanski is a member of the London Assembly, which is a local authority for this purpose. However, whilst the point is not beyond doubt, we believe the better view is section 106 doesn’t apply where a dwelling has failed to be registered for council tax.

Disclosure

Dan Neidle, the founder of Tax Policy Associates, is a member of the Labour Party. Tax Policy Associates has no political affiliation. Our previous reports suggesting politicians failed to pay tax have investigated Angela Rayner (twice), Keir Starmer, Ian Lavery, Nadhim Zahawi and Richard Tice. We have also published reports dismissing allegations that Rishi Sunak and Jeremy Hunt avoided tax.

Thanks most of all to James Beal at The Times for unearthing this story. Many thanks to T, I and P for their council tax expertise, K for their electoral law analysis, and A for valuation advice.

Photograph of Springfield Marina by Nigel Cox, CC BY-SA 2.0, via Wikimedia Commons

The mansion tax map: where the money comes from

Has council tax really gone up? The evidence.

Council tax on ‘expensive homes’ – but most of the money comes from the not-so-rich

Council tax on expensive homes: could the Budget raise £1bn+?

How to reform property tax

Richard Tice signed accounts wrongly claiming £98,000 of tax exemptions

Footnotes

We provided a small amount of assistance with the story but full credit goes to James Beal and The Times. ↩︎

We expect this is why he never received a council tax demand – the council’s systems saw people registered at the bungalow and (presumably) somebody was paying council tax for the property. So the council saw nothing amiss. Its systems had no way of knowing that many of those registered at the bungalow were actually living on boats moored nearby. ↩︎

The Times said the marina is in Hackney – it’s in an area many would refer to as “Hackney” but is technically within the London Borough of Waltham Forest. ↩︎

It’s unclear why he did this. The marina describes its berths as leisure moorings let under non-residential agreements, and requires owners to provide proof of a home address – we would speculate that he had to maintain another address in order to use the marina. ↩︎

The Valuation Office Agency maintains a register of council tax-registered dwellings. The register is continuous – i.e. if a dwelling is removed (because a house is demolished, or a boat leaves, then the dwelling remains on the register but is marked “deleted”. See for example the extensive council tax entries for boats moored at South Dock Marina. ↩︎

Note that technically Mr Polanski breached election law in any event, because he signed a declaration saying that he resided at the bungalow when he clearly did not. The technical nature of the breach means that we doubt any investigation or prosecution would be in the public interest. ↩︎

In a typical lodger arrangement the resident with the senior interest (the freehold owner or tenant) is the person liable for council tax under section 6 LGFA 1992. The lodger normally is not the liable party even at the flat – they are paying their share via rent, which is not the same thing. So “I pay council tax through my rent as a lodger” can be true in everyday speech without telling us anything useful about whether council tax was paid on the right dwelling. ↩︎

An application to register must contain the address in respect of which the applicant applies to be registered and at which they are resident on the date of the application: regulation 26 of the Representation of the People (England and Wales) Regulations 2001. The applicant must also confirm that the information given is true; the gov.uk online form requires the same declaration. The statutory entitlement to be registered is in section 4 of the Representation of the People Act 1983, which requires the elector to be “resident” at the address on the relevant date. ↩︎

Section 5 RPA 1983 tells the registration officer to have regard to the purpose and other circumstances of the person’s presence or absence. The leading common-law authority is Fox v Stirk; Ricketts v Registration Officer for the City of Cambridge [1970] 2 QB 463, in which Lord Widgery said residence “imports a considerable degree of permanence”. Lord Denning MR’s three propositions in the same case are still the starting point: a person can have two residences; temporary presence does not amount to residence; and temporary absence does not destroy residence. Boaters without a fixed address are expected to use a declaration of local connection under section 7B RPA 1983, not to register at someone else’s house as a postal convenience. ↩︎

The Electoral Commission have said that it is unlikely that owning a second property which is visited only for recreational purposes would meet the residency qualification – see paragraph 4.15 of this guidance, also here. That is consistent with Scott v Phillips 1974 SLT 32, where an occasionally-used holiday home was incidental to an elector’s main home, and was not a second residence. There is an excellent, albeit slightly outdated, guide to the caselaw from the Law Commission. ↩︎

Section 13D RPA 1983, inserted by the Electoral Administration Act 2006, makes it an offence to provide false information to a registration officer in connection with registration. The offence requires the false information to be given knowingly or recklessly, and is punishable with a fine and up to two years’ imprisonment. If Mr Polanski then voted in reliance on that registration, there is a further question under section 61 RPA 1983 about voting while subject to a legal incapacity. Prosecutions are uncommon and we are not suggesting one would be brought here – the point is simply that the “occasionally” line, if true, creates a legal problem of its own. We think the much more likely explanation is that the boat was Mr Polanski’s main residence, his electoral registration accurately reflected that, and Mr Polanski’s team misled The Times without realising the electoral law consequences. ↩︎

The cross-reference to the General Rate Act 1967 means a great deal of pre-1990 rating caselaw is still directly relevant to council tax. That’s why the cases on rateable occupation discussed below – most of which long pre-date the 1992 Act – still bite. ↩︎

Note the structure of section 66: subsection (1) defines domestic property generally; subsection (4) carves boats and moorings out of that and brings them back in only if the boat is someone’s sole or main residence. This means that, contrary to some shorthand summaries, a moored boat is not domestic property simply because someone is sleeping on it. There must be sole or main residence. The current text dates from the Rating (Caravans and Boats) Act 1996. ↩︎

The Valuation Office Agency’s treatment of moorings for non-domestic rating is set out in its Rating Manual section 670: moorings. Its council tax treatment of pitches and moorings is set out in its Council Tax Manual, Practice Note 7, which says expressly that a boat brought to a mooring should not be regarded as a dwelling unless its use will be as a sole or main residence. ↩︎

The VOA’s guidance puts the same point in practical terms. A pitch or mooring must be both a hereditament and domestic property before it becomes a council tax dwelling. A formal mooring will usually be a hereditament. An informal mooring may become one if the occupation has enough permanence. But a boat brought to a mooring should not be treated as a council tax dwelling unless it is being used, or will be used, as someone’s sole or main residence. See the VOA’s Council Tax Manual, Practice Note 7, particularly paragraphs 2.3, 3.2, 4.2, 4.6, 4.9 and 7.1. Local authority guidance says the same thing in plainer terms, although it is not law: Torbay Council says charges apply when a caravan or boat moves onto a pitch or mooring and the person living there must pay council tax if it is their sole or main residence; Surrey Heath Borough Council says that when a residential boat is on a mooring, council tax is payable, and that Class R may apply if it is moved off the mooring; Waltham Forest’s exemptions guidance lists Class R as an unoccupied caravan pitch or boat mooring. Shelter Legal gives the same summary: a boat permanently fixed to a mooring and used as someone’s sole or main residence is a dwelling. ↩︎

For council tax (as for rates), occupation must satisfy four longstanding common-law ingredients: it must be actual, exclusive, beneficial, and not too transient. The classic statement is in John Laing & Son Ltd v Kingswood Assessment Area Assessment Committee [1949] 1 KB 344. The four ingredients are reaffirmed by the Court of Appeal in Reeves v Northrop [2013] EWCA Civ 362 at [18] and [22], drawing on a long line of authority including Westminster Council v Southern Railway Co [1936] AC 511, London County Council v Wilkins [1957] AC 362 and the closely analogous boat case of Cinderella Rockerfellas Ltd v Rudd (Valuation Officer) [2003] EWCA Civ 529, [2003] 1 WLR 2423, in which the Court of Appeal held that the Tuxedo Royale, a converted ferry permanently moored as a floating nightclub on the River Tyne, was a rateable hereditament: although the vessel itself was a chattel, the occupation by it of the riverbed had sufficient quality of permanence to satisfy the four-part test.

The difficult question for boats is often transience. A boat passing through a stretch of canal or estuary, or a continuous cruiser moving every fortnight under a Canal & River Trust licence, is unlikely to create a hereditament anywhere. The boater is what Sir Alan Ward in Reeves v Northrop called a “wayfarer”, not a “settler”. The Court of Appeal upheld the High Court’s decision that a converted tug moored in the same general position in the Taw estuary had crossed the line into rateability, even though the mooring had no formal infrastructure – no pontoon, no shore power, no sewerage, just lines, stakes and a dug-out mud berth. The dominant fact was the length of occupation – this was not the only factor, but was crucial on those facts. By the time of the tribunal appeal, the family had made their home there for some two years. On a marina mooring with reserved berthing for three years, this part of the test would likely be very straightforward. A marina is a long way from a tug rotting on a mud flat. The first hurdle would be much easier for a billing authority to clear than it was in Reeves. ↩︎

There is one genuine complication. If the marina operator can move boats around between berths, and individual boaters do not have exclusive possession of any particular berth, the rating analysis can shift: the marina may be a single composite hereditament, with the marina operator in “paramount occupation” and individual berth holders being mere licensees with no separately rateable interest. This is the “paramount occupation” doctrine from Westminster Council v Southern Railway Co [1936] AC 511. It is reflected in the VOA’s Rating Manual section on moorings and Council Tax Practice Note 7. We understand that Mr Polanski’s boat had a permanent berth, and so these complications do not arise – even if the marina had a theoretical right to move the boat from one berth to another (see para 4.8 of Practice Note 7). There seems to be widespread abuse of this rule by residential marinas, with arrangements in place for berths to be swapped a couple of times a year for the sole purpose of avoiding council tax. We suspect in the modern world a court would find that artificial arrangements of this kind don’t prevent a mooring from being a hereditament – but it would make sense to change the law to put the point beyond doubt. ↩︎

If a boat does leave, then empty moorings are exempt under Class R of the Council Tax (Exempt Dwellings) Order 1992, which exempts “a dwelling consisting of a pitch or a mooring which is not occupied by a caravan or, as the case may be, a boat”. When the boat returns, liability returns with it. This is a routine point but worth making, because it explains why a billing authority would not lose interest just because the boat occasionally moves. The corollary is that having moved the boat once or twice during a multi-year period, as in Reeves, does not break permanence. ↩︎

There is a good summary of the caselaw in Marshall v Bath and North East Somerset Council [2024] EWHC 2551 (Admin). There are earlier cases which remain useful factual examples, particularly where a person has a family home elsewhere and lives away for work, but they have to be applied through the Williams reasonable-onlooker test. In Marshall, the High Court dismissed an appeal by a law student who claimed his Bath flat was his sole or main residence while in fact he stayed there only at weekends for part of the period and spent the working week with his parents in London. The Tribunal’s finding that the Bath flat was not his main residence was upheld as a fact-and-degree assessment for the Tribunal applying Williams. ↩︎

The condition for getting on to the electoral roll is “residence” at the address: section 4 of the Representation of the People Act 1983, and as discussed above this requires “a considerable degree of permanence” in the elector’s life (Fox v Stirk; Ricketts v Registration Officer for the City of Cambridge [1970] 2 QB 463). The two tests are not, however, the same. Council tax asks where a person’s sole or main residence is – singular, picking one winner. The electoral test asks whether an address is a residence – and a person can lawfully be registered at two addresses if each independently satisfies the Fox v Stirk test (see the Electoral Commission’s guidance on second homes and students). So electoral registration is not determinative of where someone’s main residence is for council tax purposes: a second-home owner can be correctly registered at both, while only one is the council tax main residence; and conversely Williams itself involved a couple registered at both properties where the supposedly secondary one won. But the inverse is highly suggestive. Being registered at only one address – and signing a declaration of truth to that effect, with criminal liability under section 13D RPA 1983 if it is knowingly/recklessly false – is the elector’s own contemporaneous statement, made to a public official, that this address has the requisite permanence in their life. A reasonable onlooker applying Williams will give that real weight, particularly as against third-party material such as estate-agent prose or marina paperwork. Williams itself, and most billing-authority guidance (e.g. West Northamptonshire, Fareham), expressly list the electoral roll as a relevant factor. ↩︎

Continuous cruisers can register to vote by way of a declaration of local connection, which does not itself create a council tax dwelling – there is no fixed mooring to tax. But Polanski is not described as a continuous cruiser; the Times’ account is of a fixed marina berth. ↩︎

Most billing authorities publish guidance setting out the indicia they apply in deciding whether a property is a sole or main residence. West Northamptonshire Council says there is no statutory definition, that residence implies some permanence, that temporary presence does not make residence and temporary absence does not break it, and lists intention, time spent, family ties, legal interest, possessions, doctors, schools and electoral roll as relevant factors. Fareham Borough Council says main residence is not necessarily where a person spends most time or most nights, and quotes the Williams reasonable-onlooker test. Bradford and Stratford-on-Avon publish very similar lists. None of this guidance is itself binding law – it is just how councils operationalise the Williams test – but it shows the kind of evidence a billing authority would in practice look at. ↩︎

The VOA’s Council Tax Practice Note 1 addresses unlawful use directly. Reeves v Northrop itself involved an unauthorised mooring with no planning permission for residential use. ↩︎

For ordinary houses and flats, council tax liability follows the hierarchy in section 6 LGFA 1992: the first resident with a sufficient interest, in descending order – freeholder, leaseholder, statutory/secure/introductory tenant, contractual licensee, any other resident, and only then the owner. Boats are slightly different, and section 7 LGFA 1992 therefore modifies the normal section 6 hierarchy, so that (broadly speaking) the owner of the boat is treated the same way as a freeholder. The result, very broadly, is that the owner of the boat is liable if they’re resident; failing that, any resident is liable; failing that, the owner ,whether resident or not. Joint owners and joint residents are jointly and severally liable.. So which of Mr Polanski and his partner are liable will depend on who owned the boat. ↩︎

The marina sits within the London Borough of Waltham Forest, not Hackney. The Times’s reference to “Hackney” appears to be a geographic shorthand; the relevant billing authority for council tax purposes is determined by the location of the dwelling, which here is the mooring. Council tax is administered by the billing authority for the area in which the dwelling is situated: section 1(2) LGFA 1992. ↩︎

Council tax can only be charged on a dwelling that is in the council tax valuation list. The VOA – not the council – compiles and maintains the list under section 22 LGFA 1992, and decides what is and is not a dwelling. The listing officer’s duties are in section 22 and section 23 LGFA 1992. The mechanics of altering the list, including the effective date for new entries, are in the Council Tax (Alteration of Lists and Appeals) (England) Regulations 2009. The council’s role is to tell the VOA. Regulation 3 of the Council Tax (Administration and Enforcement) Regulations 1992 requires the billing authority to supply the listing officer with information it has about properties that may be dwellings. Section 27 LGFA 1992 obliges the council to notify the listing officer of facts it considers relevant to the listing. ↩︎

Critically, when the VOA enters a new dwelling in the list following a “material day” some years ago, it backdates the entry to that material day. There is no statutory time-bar on how far back the list can be altered for an omission of this kind (in this respect council tax is very different from e.g. income tax and corporation tax, where there are strict statutory limitation periods). There is no general statutory cut-off on how far back the council can go to issue the original demand. The six-year limitation in regulation 34(3) of the Council Tax (Administration and Enforcement) Regulations 1992 bites only on the application for a liability order. As the High Court explained in Regentford Ltd v Thanet District Council, the sum becomes “due” – and the six-year clock starts – only when the demand is served, not when the underlying liability arose. The effective dates for alterations to the list are governed by the Council Tax (Alteration of Lists and Appeals) (England) Regulations 2009, particularly regulations 11–14. Where a dwelling has come into existence (or come to be used as a dwelling) and was wrongly omitted from the list, the listing officer must alter the list to show the dwelling with effect from the day on which the circumstances giving rise to the alteration arose: see regulation 11. The VOA’s Council Tax Manual and Practice Note 7 set out how this is operated for moorings. If Waltham Forest concluded that the boat had been someone’s sole or main residence since (say) 2023, it would expect the VOA to insert an entry in the list with an effective date in 2023. ↩︎

The practical answer is that virtually all houseboats are placed in Band A unless they are exceptionally large or luxurious floating structures – see for example the extensive council tax entries for South Dock Marina. The technical answer is as follows. For council tax, every dwelling must be assigned to a band reflecting its open‑market freehold value with vacant possession on 1 April 1991 – see section 21 LGFA 1992 and regulation 6 of The Council Tax (Situation and Valuation of Dwellings) Regulations 1992.For boats permanently moored, section 66(4) LGFA treats the mooring and the boat together as a single domestic property. VOA guidance confirms that, where the boat is on a mooring with sufficient permanence, the valuation reflects the capital value of the boat and mooring as a single hereditament, valued as a hypothetical freehold with vacant possession, on 1 April 1991. We spoke to a valuation specialist who conducted a very approximate “back-of-the-envelope” valuation by (1) applying the house price index changes since 1991 to the estimated £100k value of the boat today, suggesting a £15k value in 1991, and (2) adding his estimate from historic records that an inner east London freehold mooring in 1991 would have been worth £20k on the open market. So a total of £35k, below the £40k limit of Band A. Given the very approximate nature of this exercise, he couldn’t exclude the possibility the boat would actually be in Band B, meaning a total council tax due of around £5,000 rather than around £4,000. The difference is sufficiently small that we did not engage in a more detailed valuation exercise. ↩︎

We don’t know the exact dates, but Waltham Forest’s Band A rates were £1,370.37 for 2023/24, £1,449.15 for 2024/25, and £1,518.43 for 2025/26. ↩︎

There are specific council tax offences, but none cover failure to register, presumably because such failures are rare and hard to engineer. Section 3 of the Fraud Act won’t apply because there is no legal duty as such to register a property. ↩︎

Leave a Reply