Which MP is the highest earner? Who receives the highest donations? Who takes the most foreign trips? We’ve just launched an interactive map that lets you explore all this and more.

Apologies – this is currently down… the map needs to be updated. We hope to get to this soon.

There’s an important political debate about what gifts an MP should accept, and what outside roles are appropriate. We’ll leave that to others.12 However, we do think it’s important for MPs’ gifts, donations, earnings and other financial affairs to be publicly visible.

So we’ve launched an interactive map. You can use it directly below, or click here for a full screen version.

How to use it

Hopefully the map is reasonably intuitive, but this is a quick guide:

- Change the “shading” box on the left to shade the map to show donations (i.e. gifts made for political campaigning), gifts (i.e. personal gifts), earnings, foreign trips, shareholdings, etc

- Then you can zoom in and click on individual constituencies to see all the data for individual MPs, all cross-linked from every source we could pull data off.

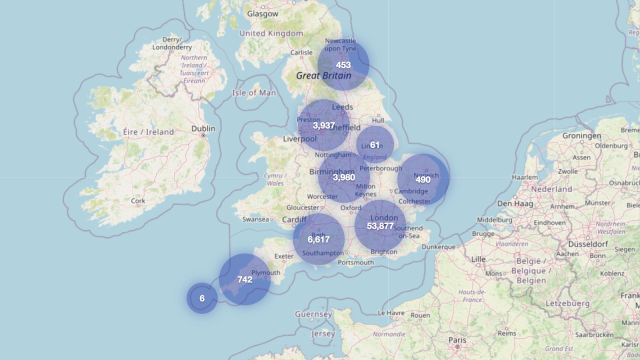

- When looking at foreign trips, you can click the “world map” button to see the countries MPs have visited.

- Or enter text in the “category” box to e.g. see all trade union funding.

- Or enter text in the “donor” box to see all donations/gifts from particular individuals/companies. Note that you may need to zoom in to see the shading for smaller constituencies (particularly London).

Limitations

All donations, employment, paid trips, and other benefits are reported by MPs, and Parliament publishes a register of them. We used Parliament’s fantastic API (together with the Companies House API) to create this interactive map.

The data is often not very good – there are many errors, particularly around company and individuals’ names. We tried to fix and match them as well as we could. But the errors suggest that there is no checking of data by Parliamentary authorities – we’ll be writing more about this soon.

Please do leave comments below, either with suggestions for improving the map, or if you find anything interesting. Or drop us a line (using the About/Contact menu option at the top of this page).

Other sources

There are other similar projects:

- Open Innovations have an impressive hex map, with lots of textual data as well. More sophisticated than ours in many ways, but lacks the Companies House linking. And a different presentation – some people prefer hex maps; we prefer geographical ones.

- This from Sky and Tortoise Media is brilliant for looking at individual MPs.

- They Work For You has a text-based index⚠️, which (invaluably) shows changes over time.

- There is an indexed text search here⚠️, from a husband and wife team.

Please let us know if we’ve missed any.

Many thanks to the brilliant M, who wrote the code that powers the map. He’s done something amazing, for no pay or reward of any kind, and doesn’t even want to be credited.

The map is © M and Tax Policy Associates Ltd (as his agent), and licensed under the Creative Commons BY-SA 4.0 licence. That means you can freely refer to it, copy it, and use it however you wish, provided you credit M and Tax Policy Associates Ltd.

Footnotes

To answer a question that’s often raised – there are usually no tax implications from gifts, which is why we haven’t commented on the recent controversies. Gifts from an employer are taxable. Gifts made by someone who dies within seven years can be subject to inheritance tax. Gifts to trusts and companies can sometimes have an immediate inheritance tax charge. But gifts (meaning gratuitous payments which are not in exchange for something valuable) made to individuals by someone who isn’t an employer aren’t subject to income tax. The exception, as someone pointed out in the comments, is where the gift is related to the employment and coming from someone who has received services, like a tip (the authority for that is Calvert v Wainwright) – there will be evidentiary challenges proving that any gift to an MP is for services rendered (and indeed likely more serious adverse consequences for the parties than tax). The foregoing reflects the conventional view, but some very knowledgeable people have suggested in the comments below that there may be in some cases a question as to whether it is correct. This may be something we look into further, but (having made extensive enquiries) the practical answer seems to be that nobody – HMRC or advisers – can recall a politician being taxed on a gift they receive. ↩︎

It is sometimes suggested we should change the law so MPs are taxed on gifts – we don’t see the case for that. There is a rational case that gifts should be banned, and a rational case that gifts should be permitted. Permitting them, but subjecting them to a uniquely punitive tax regime, doesn’t seem justified. ↩︎

What would a land value tax actually do?

What if Andy Burnham lowered the mansion tax threshold to £1.5m?

Has Britain run out of “other people” to tax?

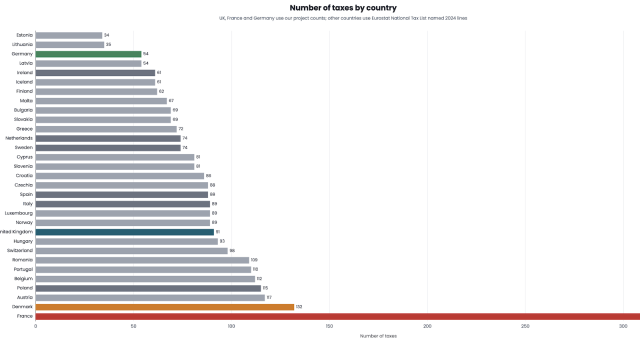

The UK has 90 different taxes. France has 348. Germany has 60. Why?

Why does Britain have more taxes than at any time since 1834?

Leave a Reply