There are plenty of reasons to be suspicious of PPE Medpro. The way it obtained a contract to supply PPE to the Government during the pandemic. The oddity of there being both a UK company and Isle of Man company with the same name (something most businesses would try to avoid). The alleged uselessness of the PPE it supplied. The steps taken to hide that it was owned by Douglas Barrowman. That Baroness Mone (his wife) both introduced PPE Medpro to the Government and shares in its profits. The documentary it funded to defend the couple.

So the news that PPE Medpro is involved in a peculiar loan arrangement is not surprising.

Companies that borrow money often grant security to the lender. Sometimes a mortgage – in much the same way that an individual would borrow from a bank; other times, the security isn’t over land, but is over assets. The benefit for the lender is that, if the borrower becomes insolvent, a secured lender is paid out in priority to ordinary unsecured creditors. The charge can be “fixed” or “floating” (“fixed” is practically more difficult in many cases, but has a higher priority in insolvency).

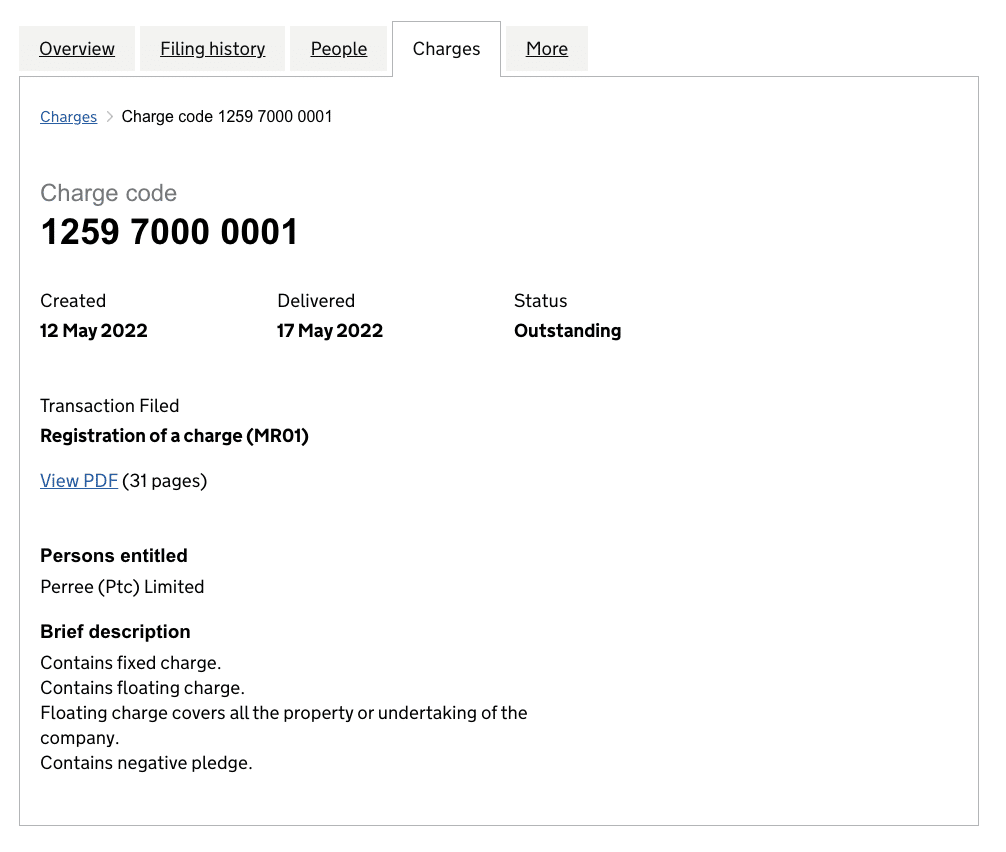

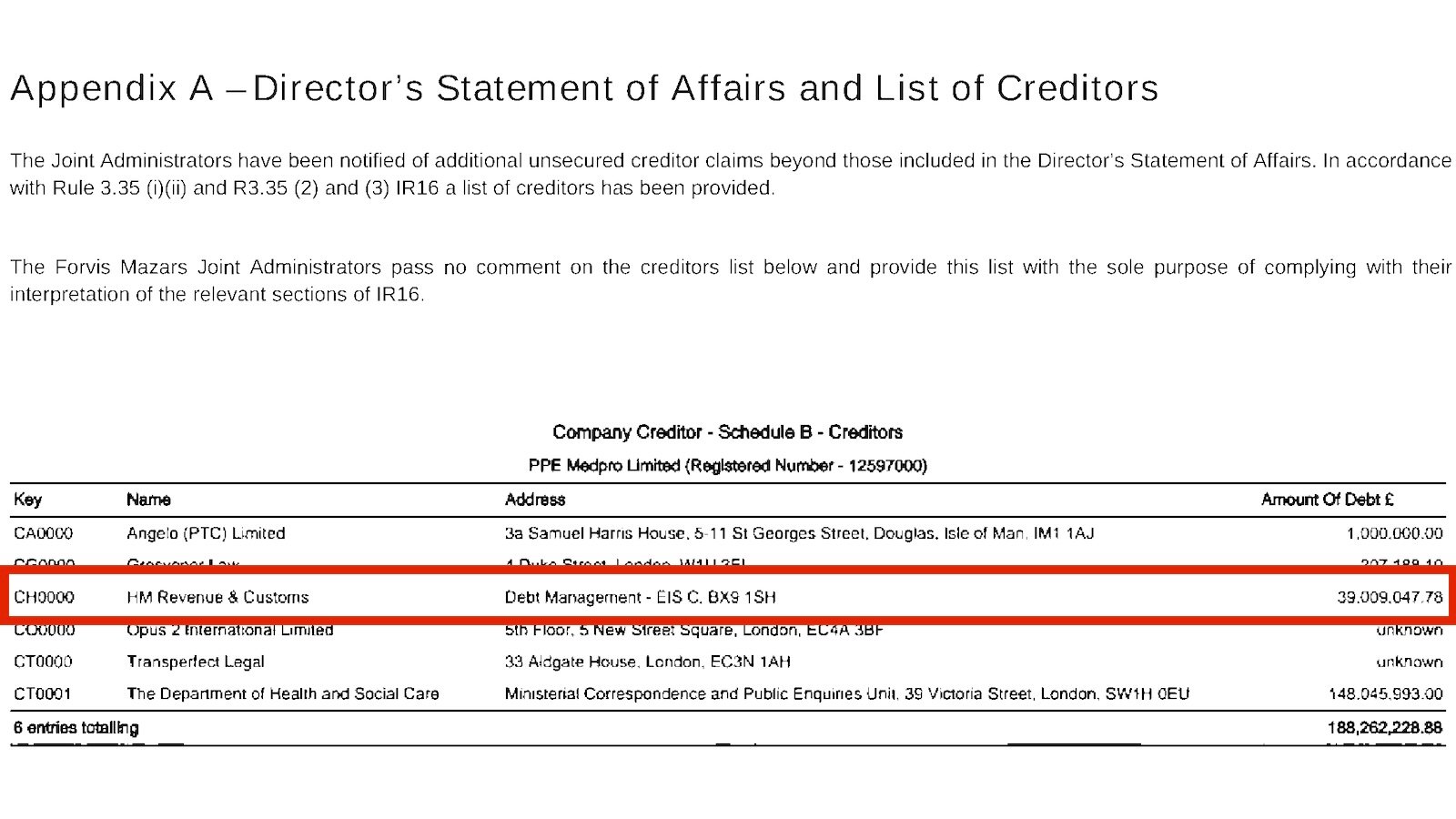

You can see the security granted by a company on its Companies House charge register. Here’s the charge register for PPE Medpro Limited:

You can click through that to the debenture (the document creating the charge). In case this is withdrawn/amended, I’ve saved a copy here. The debenture secures obligations under a loan facility from a BVI company called Perree (PTC) Limited – the company involved in the shadowy ownership arrangements of his Belgravia house.

There are several interesting things about this:

1. The BVI loan

Obvious questions arise:

- Why did PPE Medpro take a loan in 2022? There have been no reports of it undertaking additional business (except for funding the documentary).

- How much was the loan?

- Why was the loan secured? It’s an unusual step for an intra-group loan.

We currently have no way to answer these questions (the balance sheet date for the most recent accounts pre-dates the facility).

It’s not normally a great idea for UK companies to borrow from tax haven companies, because interest they pay on the loan is subject to a 20% withholding tax. Probably one of three things happened:

- This is an interest free loan

- Some structure was put in place to avoid the withholding tax – e.g. discounted notes. This isn’t something many tax advisers would recommend these days.

- They forgot or ignored the legal requirement to withhold tax.

2. The struck-off solicitor

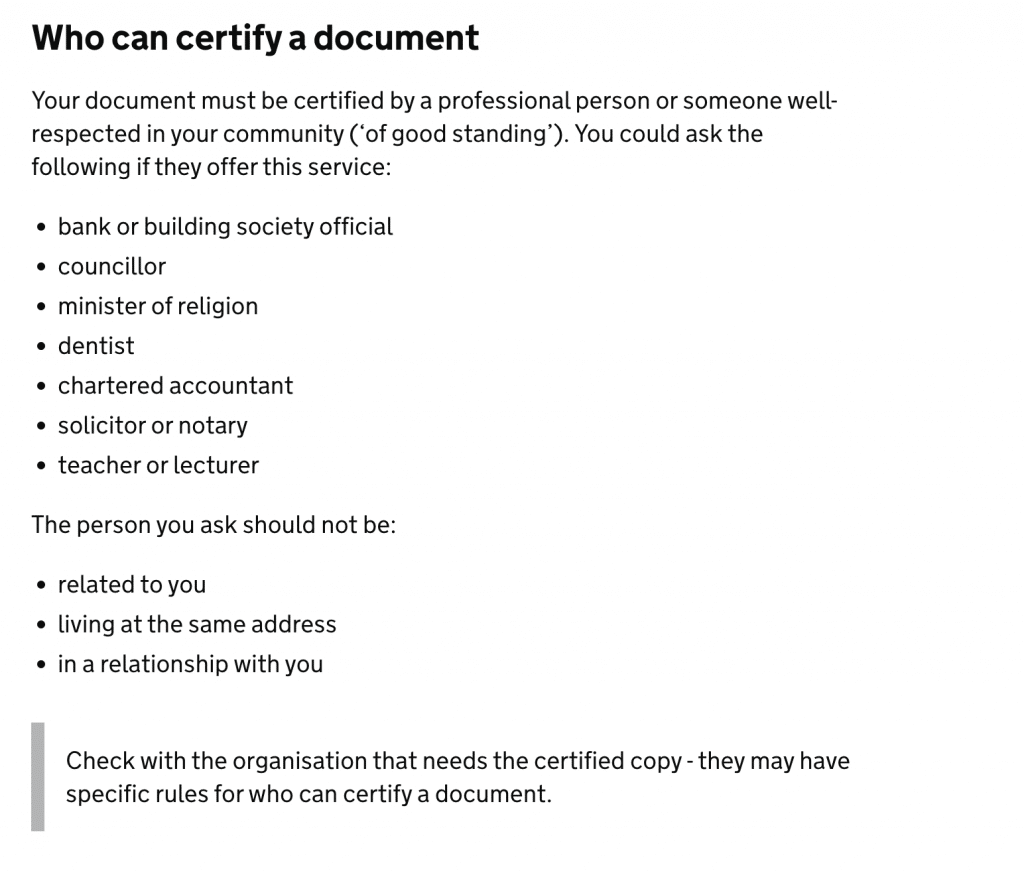

When a charge is filed with Companies House, it has to be accompanied by a copy of the charging document (here, the debenture). To provide some assurance this is a copy of the actual document, it has to be “certified”.

Here’s what the UK government website says about certified copies:1

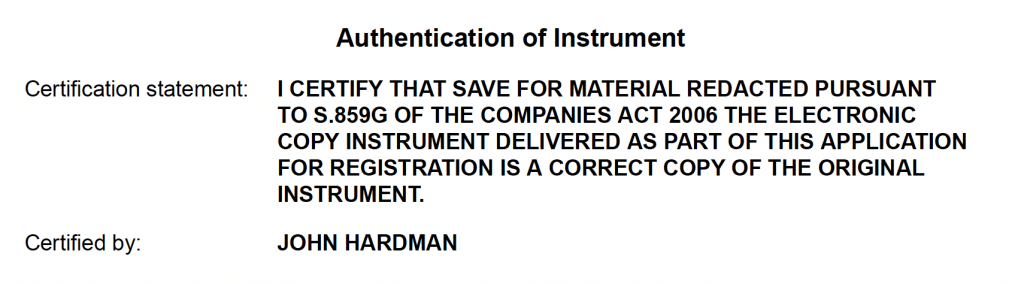

Here’s who certified the PPE Medpro charge:

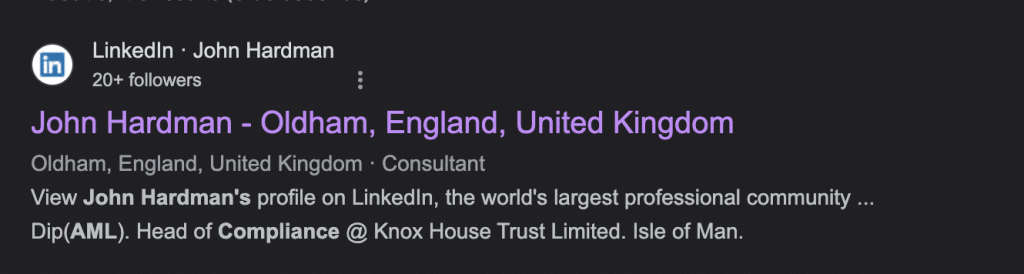

John Hardman is effectively Barrowman’s in-house lawyer.2. However, you can see only traces of this on the public internet, including Companies House connections with Barrowman and an old LinkedIn profile:3

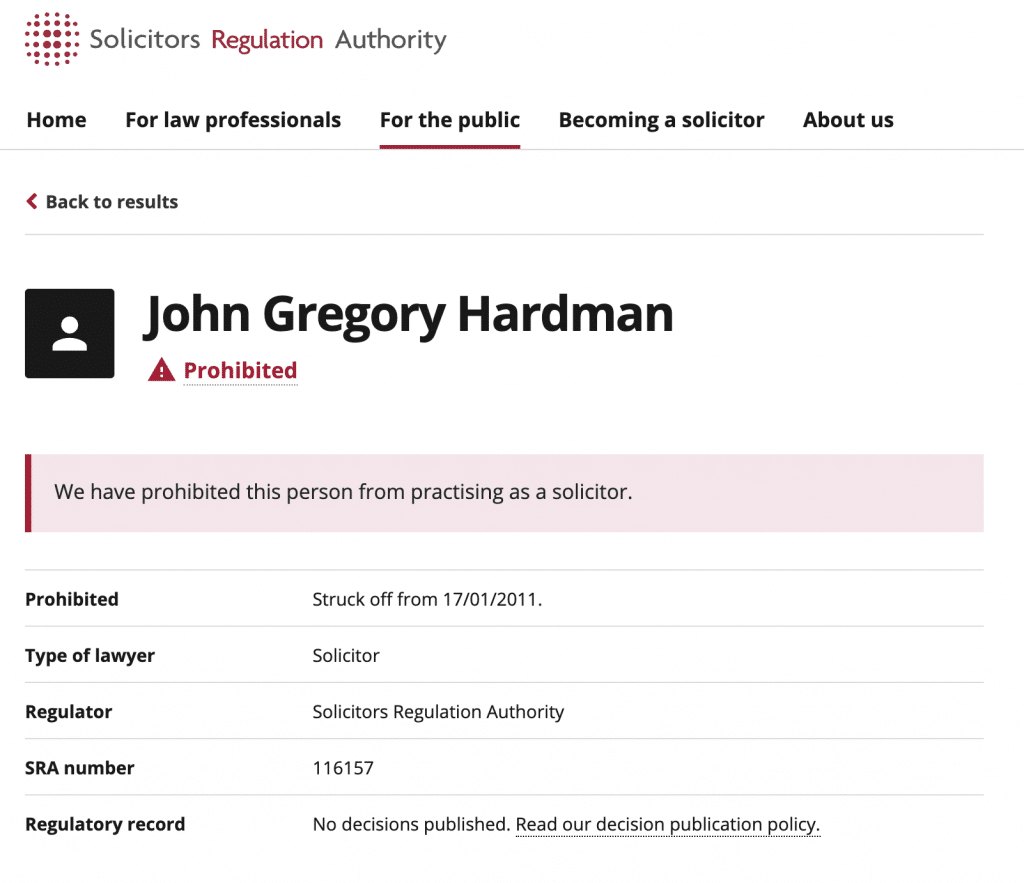

Hardman is an interesting choice for a legal adviser, because he is a former solicitor who was struck off for dishonesty:

You can’t see the details online, but I’ve obtained them – he was struck off for stealing client money to support his failing business (he then went bankrupt).

Three more obvious questions:

- Why does Douglas Barrowman employ as his in-house lawyer someone who was struck off for dishonesty?

- Why do the Isle of Man authorities think such a person is acceptable to work in a regulated business?

- Is Hardman’s certification of the debenture is valid, given he has no professional status? If not, does this invalidate the charge, or just remove the normal presumption the certified copy is a true copy? If the charge were invalid then it would not have priority over other creditors of PPE Medpro such as (to pick random examples) the Government or HMRC.

Many thanks to Y for background research on this.

Footnotes

This accords with my understanding, but I’m embarrassed to say I don’t know the legal authority for this. Very possibly there isn’t one – but I’d be most grateful for any thoughts. ↩︎

Not to be confused with the tax adviser John Hardman, formerly at Pinsent Masons, who has no connection to these matters. Of course there are likely many other unrelated John Hardmans. ↩︎

Hardman recently removed all content from his LinkedIn profile ↩︎

Douglas Barrowman and Michelle Mone may have avoided tax on their £65m PPE profits

PPE Medpro made £200m but never filed full accounts. The law should change.

Barrowman – more evidence of fraud: his seven mysterious “shadow companies”

Douglas Barrowman made more than £100m selling disastrous tax avoidance schemes. New evidence shows the schemes defrauded both HMRC and his own clients.

![32 [F1 General false statement offence] [F1 False statements: basic offence]

[F' (1) It is an offence for a person, without reasonable excuse, to—

(a) deliver or cause to be delivered to the registrar for the purposes of this Part any document that is misleading,

false or deceptive in a material particular, or

(b) make to the registrar, for the purposes of this Part, any statement that is misleading, false or deceptive in a

material particular.](https://taxpolicy.org.uk/wp-content/uploads/2023/12/Screenshot-2023-12-28-at-11.41.07-640x118.png)

Douglas Barrowman: 25 more companies with unlawfully hidden ownership

Leave a Reply to John Burt Cancel reply