There’s a problem with a lot of Left-wing tax advocacy: it identifies a political challenge, and proposes a policy aimed at solving it. But the authors believe so strongly in the policy’s righteousness that all of their time and focus is spent on advocacy, and none on analysis. They don’t speak to outside experts, don’t think about incentives and consequences, and only look at data to find support for the proposal. It’s “policy-based evidence-making”… and ultimately it doesn’t help anybody.

It would be invidious to pick on one example – but I’m going to do that anyway.

Here’s a proposal out today from the European Greens.1.

It’s a perfect illustration of my point, because of the way it jumps from identifying a political problem to a solution, without any attempt at considering how that solution would play out. And in reality, the proposal would be a disaster – in the very year the Greens pick as their exemplar, it would have cost governments billions of Euro in tax revenue.

The policy challenge

Here’s how the Greens start:

We can agree or disagree with this, but it’s undoubtedly a valid position to hold.

The conventional policy answer would be: tax capital gains at a broadly equivalent rate to labour income. That’s justified on grounds of vertical equity (the rich should pay tax at the same rate as the poor), horizontal equity (rich people making capital gains should pay tax at the same rate as rich people receiving large bonuses), and anti-avoidance (because otherwise people convert income into capital gains to achieve a lower rate).

But the Greens take a different approach.

The proposal

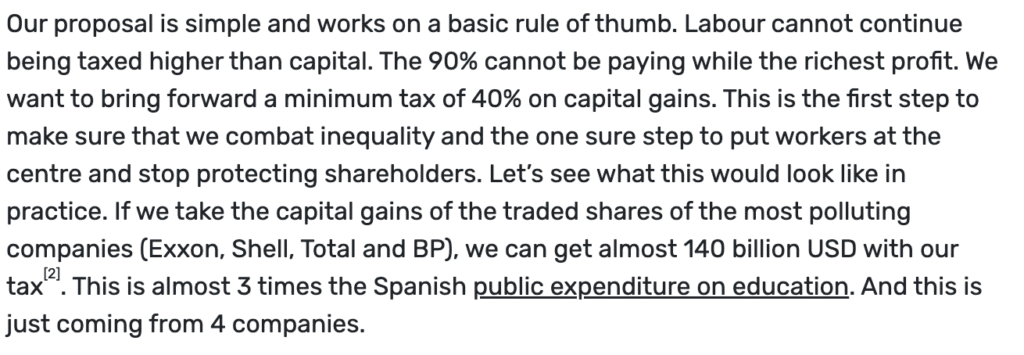

In other words: a 40% minimum tax on capital gains, and for listed shares it would be on gains whether realised or unrealised.

To be clear, if I buy €1,000 of shares today, and sell them next year for €2,000, then that’s obviously a €1,000 capital gain on which I’d pay tax (at a minimum of 40%). But even if I don’t sell them next year, if they’re worth €2,000 then I’d pay capital gains tax on my unrealised €1,000 gain.

There are very few countries that tax unrealised capital gains. Many people find the idea counterintuitive or unfair, but it’s supported by many economists on the basis that an unrealised gain is just as “real” as income or a realised gain. Tax specialists tend to be more cautious, worrying about the difficulty of valuing property, and the practical problems that will arise from paying out refunds when people have unrealised capital losses2.

Reasonable people can certainly differ, and the Greens are absolutely not being unreasonable in seeking to tax unrealised capital gains.

Reasonable people can also disagree with a blanket 40% rate. Better to track the rate of tax on income (or, more sensibly, dividends). If capital gains is taxed at a higher rate than dividends then people will take dividends instead; if it’s lower (as is generally the case now), they’ll manufacture gains instead of taking dividends. The solution is surely to unify the rate, not to pick 40%.

These are not my point. There are two much bigger issues.

Fudging the data

You’d expect any credible tax policy proposal to be accompanied by some figures – ideally an estimate of the revenue consequences.

Here’s what the Greens give us:

There are two massive problems with this.

First, the detail is all wrong, because only a small percentage of the shareholders of these four companies will be taxed by the proposal:

- any EU proposal is obviously only going to tax the capital gains of EU citizens. What percentage of these four companies’ shareholdings is held by EU citizens? I expect not much. Most of the shareholders will be outside the EU (certainly BP and Exxon, and probably also Shell).

- The majority of the EU shareholders will be institutions rather than individuals. The OECD has estimated that only 18% of shareholdings in publicly listed companies are held by private companies and individuals.3. I’m assuming the Greens are not proposing taxing pension funds and other institutional investors – pension funds are generally exempt from tax, and institutional investors will either be exempt from tax (e.g. OEICs) or taxed on a mark-to-market basis already (e.g. investment banks).

So the true figure will probably be closer to $14bn.

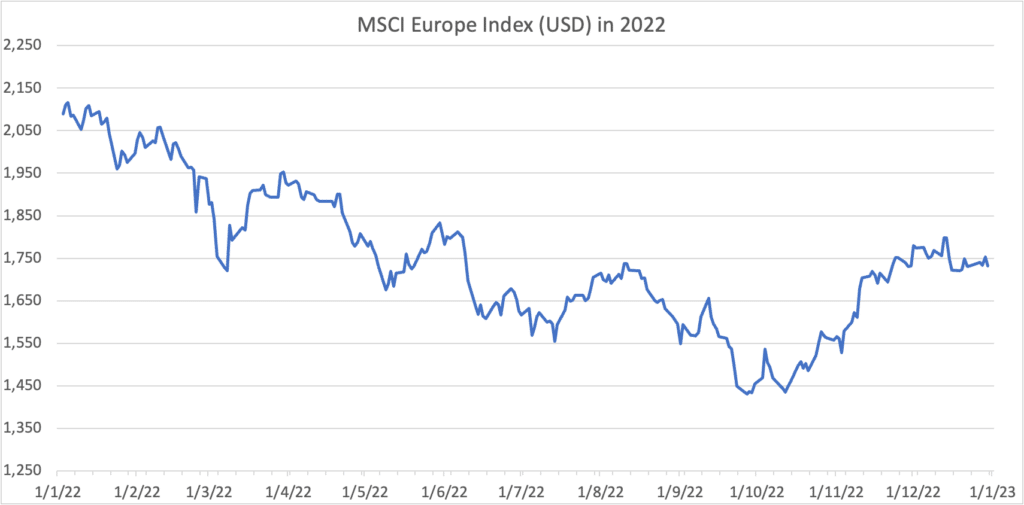

Second, the big picture: it’s extraordinarily selective to pick four companies who’ve had a good energy crisis. The proposal applies to all listed companies… so what was the total gain in market capitalisation of all listed European equities in 2022?

It was negative.4

If this proposal had been adopted in 2022, it would have cost European governments money.

The $140bn figure is embarrassing on every level.

It’s the epitome of policy-based evidence-making. They’ve started with the idea they want to tax capital gains more heavily, and then gone hunting for some numbers that support the idea. Any neutral enquiry – “hmm, I wonder what the effect of the policy would have been in 2022” – would led to the conclusion that the policy would have cost governments €billions in 2022.

Ignoring the incentives

This isn’t a proposal to tax unrealised capital gains – it’s a proposal to tax unrealised capital gains of listed shares.

That’s a huge problem – because it creates a powerful incentive for taxpayers (and particularly the very wealthy) to not hold listed shares.

Some might create avoidance structures – e.g. establishing their own private SPV/fund in a non-EU country, and have that SPV/fund acquire listed equities. Others would simply reallocate investments to listed debt (e.g. high yield bonds), unlisted equities, real estate, private funds, and other asset classes. And you’d certainly see a decline in entrepreneurs listing their private companies.

All of which means the tax yield would be much less than expected, with the potential for undesirable non-tax consequences too (I personally think we benefit from having successful companies listed rather than private).

A good rule of thumb for tax policy is: don’t tax something in a way that depends upon a feature which has no economic reality, and can easily be changed. No baker in the UK puts chocolate on their gingerbread men covered in chocolate, other than two spots for eyes – because having more chocolate than that triggers 20% VAT. Whether a company is listed is, in many cases, about as economically relevant as chocolate eyes. It’s a terrible basis for taxing shareholders in the company.

I’m unconvinced it’s a good idea to tax unrealised capital gains. But if you disagree, it’s imperative you tax all unrealised capital gains.

How to do better

Three simple suggestions:

- All tax policy proposals should be “red teamed“. People who weren’t involved in the design of the proposal should sit down and think about how they, as a taxpayer, would react to it. What are their incentives? What are the loopholes?

- Europe is blessed with thousands of tax academics and tax practitioners (in government and the private sector). It’s madness to propose a tax policy without speaking to some of them. I’m certain any tax academic or practitioner would immediately have identified the two problems above.

- Finally, don’t confuse means with ends. The end result here should be fair taxation of capital gains, and the question should have been: how do we best achieve that? But I suspect that this project started with a desire to tax unrealised capital gains, and that led to everything else.

Image by Stable Diffusion⚠️ – “a calculator violently exploding in a massive fireball, dramatic, award winning, pop art, roy lichtenstein”

Footnotes

If your response is “well, we won’t refund tax for capital losses”, then the policy is no longer a tax on capital gains, and instead a crude and rather random expropriation of property ↩︎

See this document, the sixth bullet point on page 6 and Figure 2 on page 12 ↩︎

I used the MSCI Europe index captures about 85% of European equities and is therefore a reasonable way to answer the question; there will be other approaches, but the answer will likely be the same… 2022 was a bad year for equities. Historical data from investing.com. ↩︎

Tax will go up but public services will get worse. This is why.

Inside a fake tax refund factory

![THE HON. MRS JUSTICE COLLINS RICE DBE CB

Approved Judgment

Kamal v Tax Policy Associates

31. In the circumstances, the pleading that it was ‘false and misleading’ to suggest that a

judicial finding of breach of duty had been made against him is incapable of forming a

part of the just disposal of Mr Kamal’s libel claim. The attempt to do so is an abuse of

the court’s processes. I grant the Defendant’s application to strike out [5(b)] of Mr

Kamal’s particulars of claim.](https://taxpolicy.org.uk/wp-content/uploads/2026/03/padded_judgment-640x360.jpg)

We defeated an £8m libel claim – and it shows libel law and the Tax Bar need reform.

Finance Monthly fabricated an interview with me

Mandelson and the Epstein emails: could he be prosecuted?

Leave a Reply to John Cancel reply