The internet is full of people promising effortless tax refunds. For many, the business model is simple: invent expenses, file claims at volume, and take a cut. These “refund factories” exploit HMRC’s “process now, check later” systems, operating largely out of sight – but at a scale that may represent a material slice of the UK’s £47bn tax gap.

It is rare to see exactly how these schemes operate. Usually they remain hidden from view until a tax tribunal decision exposes what was done and how the claims were fabricated.

Until recently, the most notorious example was Apostle Accounting Ltd, the failed firm run by high-profile adviser Zoe Goodchild. A Tribunal last year found that Apostle had deliberately submitted a false tax return – and that Goodchild had reported her client to the police when he complained. This was no isolated incident – it’s been reported that Apostle made more than 800 false returns, shielded by vexatious criminal complaints.1

A reported case2 last week reveals another firm submitting fake tax refund claims – Oxford-based Welcome Accountancy.3

The current regulatory framework is visibly failing to stop firms like Welcome and Apostle. While new rules coming into force this year are intended to curb the abuse, there is a real risk they will miss the mark – imposing administrative burdens on normal advisers, while the fraudsters simply find a new workaround. We believe a better answer is aggressive enforcement, and the use of the criminal law. Bad actors will only stop when the personal risks outweigh the rewards.

The false claim

Yasir Badoume was an employee, paying tax on his employment income under PAYE. Employees can only claim a tax deduction for expenses in very limited cases. That, however, didn’t stop Welcome Accountancy Services.

In January 2020, Mr Badoume authorised Welcome Accountancy Services to act as his agent. Welcome then submitted tax returns for six tax years, claiming tax refunds for employment expenses. The refund claims were very large – in 2021-22 they claimed expenses of over £21,000 against income of £88,247, for supposed travel expenses, professional fees, other expenses and capital allowances.

This was implausible on its face. Employees don’t claim capital allowances.4

It was, however, initially successful: the returns generated tax repayments, made to Welcome Accountancy Services. We don’t know what proportion, if any, were paid to the actual taxpayer, Mr Badoume.5

This is often the problem with tax refunds – HMRC often grants the refunds automatically (sometimes instantly) and only checks them later. That is convenient for normal taxpayers making a genuine correction and refund claim; but it opens the door to bad actors.

In this case, HMRC opened an enquiry within the statutory deadline (a year from submission of the return) and assessed additional tax. Welcome Accountancy appealed, with the matter reaching a Tribunal last month.

More than negligence or incompetence

It is not a criminal offence to make a mistake preparing a tax return, even if the adviser is negligent or incompetent. This case, however, appeared rather more than a mistake.

When HMRC opened an enquiry into Mr Badoume’s tax return, they received this explanation from Mr Omar Ali, a partner at Welcome:

“By UK tax laws 20 percent of expenses6 paid by taxpayer are allowed to be claimed but if and where expenses are excessive, please amend the figures.”

As the Tribunal said, this is an “utterly false premise”. Indeed the Tribunal thought the suggestion was “so implausible” – particularly coming from a firm describing itself as certified chartered accountants – that it did not believe anyone at Welcome genuinely thought it was permissible.7

The Tribunal also noted the invitation to HMRC to “amend the figures” if they seemed excessive. As the Tribunal observed, “To a reasonable reader, this suggests that the representative himself had little confidence in the accuracy of the figures previously provided”.8

When asked for supporting evidence, Welcome said it had shredded the taxpayer’s records after six months due to storage constraints. The Tribunal did not believe this:

“We do not accept that records were shredded after six months because we do not believe that there were ever any records to shred; the expense claims were, in our view, a figment of the imagination of whoever at Welcome Accountancy Services completed the Appellant’s tax returns.”

Despite initially claiming the records had been destroyed, Welcome subsequently produced 30 receipts and a travel schedule for part of the 2021-22 year. But HMRC checked the vehicle’s MOT records, and the numbers did not add up:

- Welcome’s schedule claimed 13,718 miles of business travel in just eight months of the 2021-22 tax year.

- The vehicle’s actual total mileage for the entire year, per MOT records, was only 10,700 miles – and that would include non-business travel.

The Tribunal concluded that the travel schedule “was prepared in order to fit in with the receipts previously provided and the travel expense claim previously made rather than to accord with any reality”.9

A subsequent email from Welcome asserted that HMRC officers had said 20% of income could be claimed as expenses, and accused HMRC of racial targeting. A “senior accountant” at Welcome continued this theme, writing that “This is a racial issue as my practice has been targeted on prejudice basis and I have clear proof of that and I am awaiting full reply from The Chief Executive.”

Welcome then failed to defend their position. There was “almost zero engagement” with the Tribunal. No skeleton argument or witness statement was filed. Neither the appellant nor Welcome attended the hearing.

The Tribunal concluded that Welcome submitted tax returns on behalf of a client knowing that the expense claims were inaccurate, rejected Welcome’s supposed “20% of income” expenses approach as implausible, and said the claimed expenses were “a figment of the imagination”.

An unregulated firm

Anyone can describe themselves as an “accountant”, but only members of a UK or overseas accounting body can say they’re a “chartered accountant”. 10

This doesn’t appear to have stopped Welcome Accountancy. The Tribunal said that the firm described itself as “Welcome Accountancy Certified Accountants”, but found nothing in the correspondence to suggest it was actually recognised by the Association of Chartered Certified Accountants. It referred the decision to the ACCA for investigation.11

Evidence of fraud

The Tribunal held that the loss of tax was intentional. It follows that, if Welcome Accountancy acted dishonestly, then a criminal offence may12 have been committed, either a specific statutory tax offence or the common law offence of “cheating the revenue“.

Mr Badoume may also have been defrauded, given Welcome had represented that they were providing a genuine tax advisory service but (on the Tribunal’s findings) actually knew they were fabricating claims, and that their actions would cause Mr Badoume a financial loss.13 Again this will turn on whether Welcome acted dishonestly.

Was this a one-off?

It seems not.

The Tribunal says that Welcome filed a complaint covering what looked like eighteen similar cases. If we assume all eighteen had similar claims to Mr Badoume, that implies over £500,000 of lost tax.

A normal firm would not have eighteen cases like this – or even one. And if this were some freak one-off, perhaps the work of a rogue employee, Welcome’s response makes little sense: rather than treating the claim as an error, it defended it, advanced an invented “20%” rule, and persisted when challenged (including making an entirely spurious accusation of racism). The natural inference is that these were not isolated fabrications but part of a broader practice. If so, the 18 cases may simply be the number HMRC’s normal processes happened to uncover, rather than the full extent of the false claims Welcome submitted.

The consequence for Welcome Accountancy

In the few cases where firms like Welcome Accountancy have been caught, the people behind the firms seem to just walk away – leaving the clients with no recourse. Even when HMRC commences a fraud investigation, the usual response is to file for insolvency and start up again with another company.

Our view is that the best answer isn’t regulation – which puts a burden on compliant businesses and is ignored by bad actors – but effective enforcement.

That’s what’s required in this case – and we expect HMRC’s Fraud Investigation Service is already investigating Welcome Accountancy.

As the Tribunal noted, it is unclear quite whether Mr Badoume is a victim or a participant. The Tribunal concluded that the fact Welcome Accountancy had Mr Badoume’s national insurance number means he probably knew the claims were being made; that may be, but it is also possible he is completely unaware of the tax refunds made in his name.

The new regulation

Today, anyone can call themselves a tax adviser, and start filing tax returns and refund claims on behalf of clients. That will change in May 2026 following the enactment of Finance Act 2026. Tax advisory firms will have to start registering with HMRC, or they won’t be able to file tax returns on behalf of clients. Ellen Milner, director of public policy at the CIOT, has written an excellent article on the new “almost regulation” of tax advice.

We share Ellen’s scepticism. And there’s an obvious response: we expect some bad actors will start using their client’s own log-in details to file tax returns as if they were the client – therefore making the rogue firm invisible to HMRC. In the US, firms that do this are referred to as “ghost” tax preparers. 14

If HMRC discovers the behaviour – and they may not – they can send a “compliance notice“, with fines of up to £10,00015 for firms and the individuals controlling them.

And HMRC get a separate line of attack if they can show that a firm is acting intentionally to bring about a loss of tax for HMRC. Under the new “sanctionable conduct” rules HMRC has powers to request client files and, ultimately, assess penalties of up to 100% of the tax that was lost.

In principle these rules should enable HMRC to aggressively police rogue firms like Welcome Accountancy, without the time, cost and risk of a criminal prosecution. The practical question is whether HMRC will have the resources and willingness to do this.

We would suggest one simple step to deter ghost preparers: large civil penalties for any adviser that uses a taxpayer’s own log-in credentials to file a tax return, with the penalties applying to the individual filing the return and others responsible. There should be no need to prove dishonesty, or anything beyond the simple fact that the adviser accessed the taxpayer’s own account.16 Right now this behaviour isn’t even forbidden: it should be.

But the more important step is aggressive and effective enforcement. When there’s reason to believe that fraud is being committed, the HMRC response shouldn’t be exchanges of correspondence and tax tribunal hearings – it should be dawn raids, and arrests.

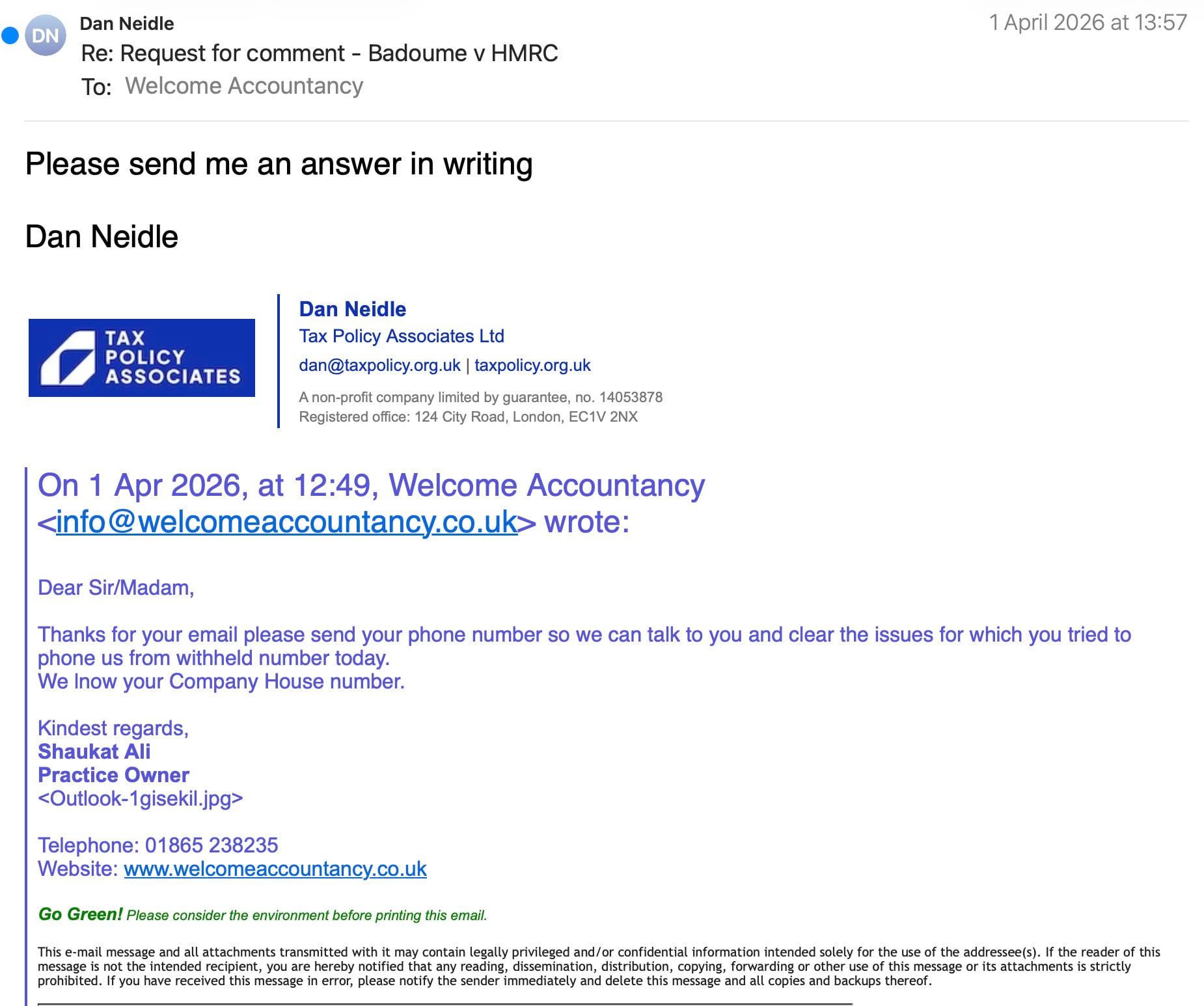

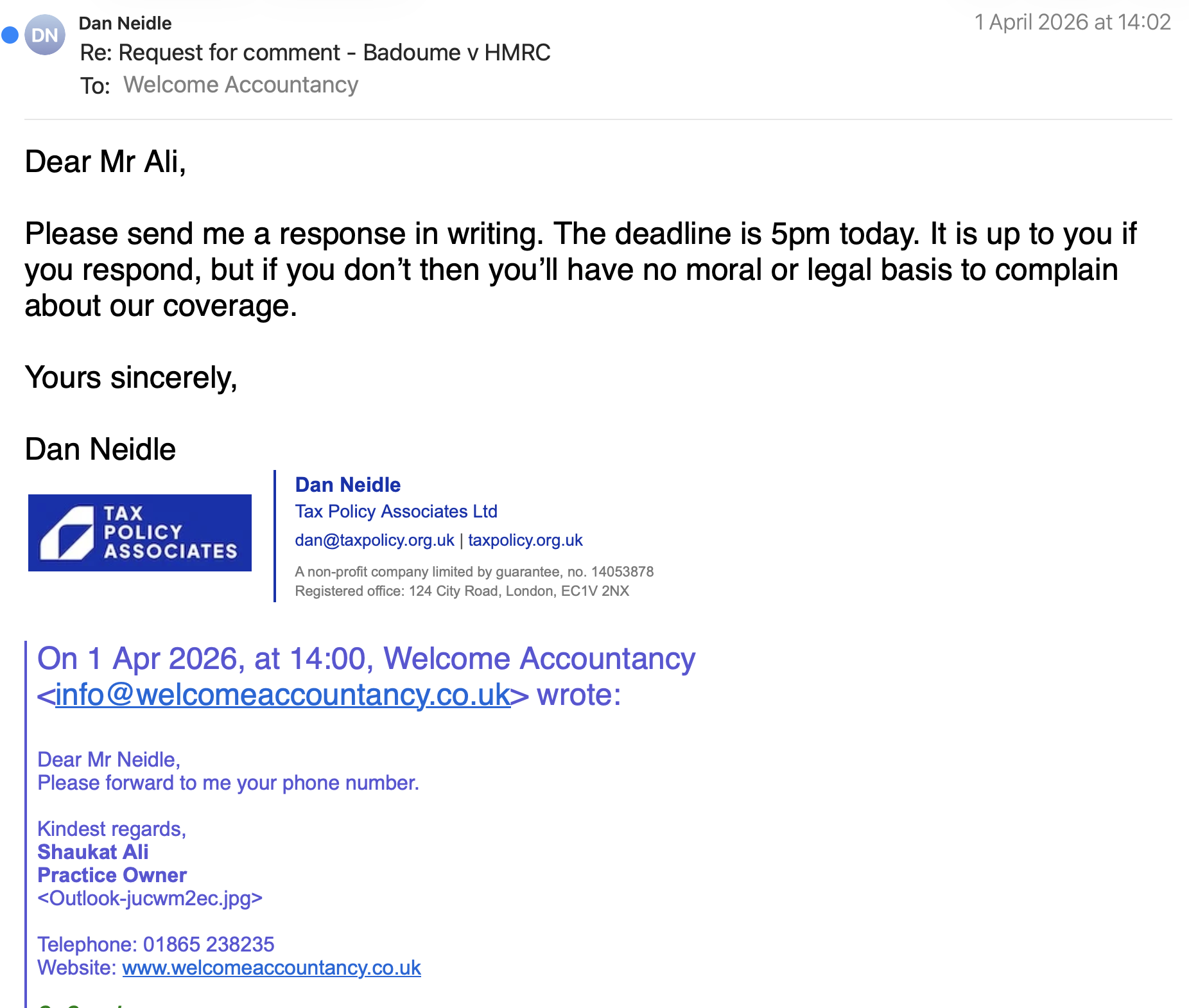

Welcome Accountancy’s response

We called the telephone number on Welcome Accountancy’s website to establish that this was the correct firm, and then sent an email asking for comment. They seemed keen to speak in person; but (as is our normal practice) we asked for a response in writing. We never received one.

Here’s the correspondence:

![Dan Neidle

Request for comment - Badoume v HMRC

To: infocaxvelcomeaccountancy co uk

Dear Mr. Omar Ali and Mr. Shaukat Ali,

| am the founder of Tax Policy Associates, a think tank established to improve UK

tax policy.

We are writing in relation to the First-tier Tribunal decision in Badoume v HMRC

[2026] UKFTT 484 (TC), which refers to “Welcome Accountancy Services”

The Tribunal found that your firm submitted tax returns “knowing that the expense

claims made were inaccurate”, described the claims as “a figment of the

imagination”, and rejected your asserted “20%” expenses approach as implausible.

The Tribunal also noted that you admitted destroying client records after six months,

recorded “almost zero engagement” from you and that neither you nor your client

attended the hearing.

We intend to report on this decision and will be calling for HMRC and other

authorities to consider whether a criminal investigation is appropriate.

Do you accept or dispute these findings, and can you explain your failure to engage

with the Tribunal process?

Also: you describe yourselves as “certified accountants”, but we can find no

evidence you are recognised by the ACCA. Can you please clarify your status?

Please reply by 5pm today.

Yours sincerely,

Dan Neidle

Dan Neidle

TAX Tax Policy Associates Ltd

G oot ey ATES dan@taxpolicy.org.uk | taxpolicy.org.uk

Acongcolnco ean, Teer by quecamer. ne “4.535%

Reqeeet Mee “24 Oly Boat Locenn ECTS ZNX](https://taxpolicy.org.uk/wp-content/uploads/2026/04/Screenshot-2026-04-05-at-17.57.40.png)

Many thanks to M for drawing our attention to this case, and for additional research on this article.

Footnotes

At one point there was a fraud investigation into Ms Goodchild; we don’t know its current status. Apostle was was fined £40,000 by its professional body, the Institute of Certified Bookkeepers (ICB), for anti-money laundering failings. Goodchild’s successor firm, Innovate Accounting, successfully applied for membership of another professional body, the Institute of Accountants and Bookkeepers (IAB). The AIB excluded her in March 2026 following accusations of misconduct and dishonesty. ↩︎

Badoume v HMRC [2026] UKFTT 484 (TC). The hearing was on 23 March 2026 at Taylor House, London, before Tribunal Judge Keith Gordon and Member John Woodman. Judgment was released on 27 March 2026 – a notable achievement by the judges. ↩︎

The firm appears to be a partnership; there is no live company with that name. There was a Welcome Accountancy Ltd incorporated in 2016, owned by one of the individuals behind the current Welcome Accountancy, but it was dissolved in 2018. ↩︎

That’s a slight over-simplification. In principle there are rare cases where an employee can claim, for example if the employer insists the employee purchases plant/machinery to carry out their job – but none of our team is aware of a case where this has happened. ↩︎

Paragraph 23: “The tax overpayments claimed on the returns were duly repaid. In accordance with the instructions on the tax returns, those repayments were made to Welcome Accountancy Services.” ↩︎

This appears to be a typo by Welcome Accountancy; they surely meant “income”. ↩︎

And, as the Tribunal noted, if Welcome Accountancy really believed there was a 20% rule, they would have simply claimed 20%, and not divided the claim between three categories, with fictional stated expenditures. ↩︎

The rules governing deductions for employee expenses are, as the Tribunal noted, “notoriously rigid, narrow and restricted in their operation”. It would be surprising for an employee’s deductible expenses to amount to 2% of their income; 20% is not credible. ↩︎

Paragraph 96(5)(b). The Tribunal also noted that many of the claimed journeys were one-way only, with no return leg — inconsistent with any plausible travel pattern. ↩︎

Enforcement takes the rather expensive route of the ICAEW applying for an injunction. It’s an offence to hold yourself out as a solicitor or barrister, but the term “accountant” is not protected by statute, only by private tort actions. There have been calls in the past for this to change. ↩︎

Paragraph 45 of the judgment: the Tribunal found the firm’s conduct to be “sufficiently concerning to merit our sending a copy of this decision to the Association for their investigation”. ↩︎

We say “may” because the Tribunal was applying the civil standard; any prosecution would of course have to establish guilt beyond reasonable doubt. ↩︎

Not the loss of the expenses claim, as he was never entitled to an expenses claim, but the loss of fees, and potentially penalties. ↩︎

Ghost filings have already been seen in the context of R&D tax relief. HMRC started blocking/investigating R&D tax relief claims by suspect firms, and those firms started avoiding this by filing directly, using their clients’ log-in details. ↩︎

It’s not explicit in the legislation, but in our view it’s reasonably clear that the £5k/£10k fine is for each incident of non-compliance, and not a flat £5k/£10k per firm. ↩︎

It would be sensible and fair to add a prominent warning at the point of logging-in. ↩︎

Finance Monthly fabricated an interview with me

Herran Finance – another fake bank at Companies House

Who’s behind the fake banks on Companies House?

UK companies with no UK director are 17× more likely to show signs of fraud

How do promoters get rich from selling hopeless tax avoidance schemes?

Leave a Reply